Resources

About Us

Industrial Brakes and Clutches Market Size, Share & Trends Analysis, by Product Type, Actuation (Hydraulic, Pneumatic, Electromagnetic, Spring-Applied), End-use Industry, and Geography — Global Opportunity Analysis & Forecast (2026–2036)

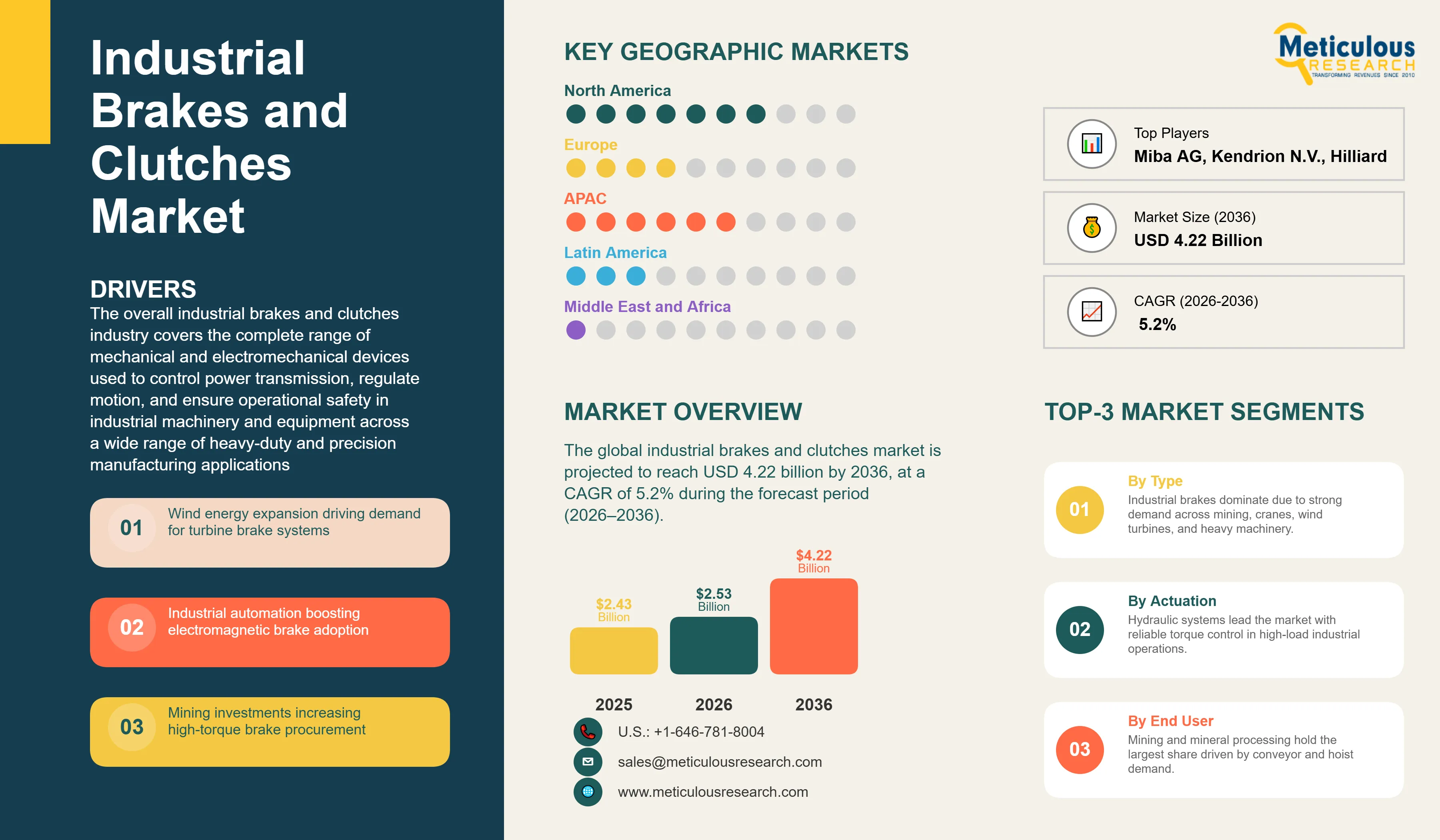

Report ID: MREP - 1041963 Pages: 292 May-2026 Formats*: PDF Category: Energy and Power Delivery: 24 to 72 Hours Download Free Sample ReportThe global industrial brakes and clutches market was valued at USD 2.43 billion in 2025. The market is projected to reach USD 4.22 billion by 2036, growing from USD 2.53 billion in 2026 at a CAGR of 5.2% during the forecast period (2026–2036).

Click here to: Get Free Sample Pages of this Report

The overall industrial brakes and clutches industry covers the complete range of mechanical and electromechanical devices used to control power transmission, regulate motion, and ensure operational safety in industrial machinery and equipment across a wide range of heavy-duty and precision manufacturing applications. The market includes disc brakes, drum brakes, caliper disc brakes, spring-applied brakes, electromagnetic brakes and clutches, hydraulic and pneumatic clutches and brakes, friction clutches, and overrunning and backstop clutches deployed across end-use industries including mining and mineral processing, oil and gas, wind energy, marine and offshore, metals and steel processing, crane and hoist and material handling, paper and pulp, power generation, construction and heavy equipment, and general industrial manufacturing.

These systems are integral to the safe and efficient operation of industrial machinery where uncontrolled motion, overload conditions, and the need for precise torque transmission present significant risks to equipment integrity, personnel safety, and production continuity. Industrial brakes are required to decelerate, stop, or hold machinery under high-torque and high-load conditions, while industrial clutches enable controlled engagement and disengagement of power transmission between drive components. Together, brake and clutch systems address the full spectrum of motion control requirements in both heavy-duty industrial applications, where hydraulic or pneumatic actuation provides the torque capacity and thermal dissipation required by mining conveyors, offshore cranes, and rolling mills, and in precision automation applications, where electromagnetic spring-applied brakes deliver the fast response times and compact form factors required by servo motor drives, robotic joints, and automated guided vehicles.

The growth of the industrial brakes and clutches market is primarily driven by continued global expansion in key end-use industries that impose demanding torque handling and operational safety requirements on powertrain components. In mining and mineral processing, sustained extraction activity driven by growing demand for critical minerals including copper, lithium, nickel, and cobalt for the energy transition has supported capital expenditure on heavy conveyor systems, hoists, and grinding mills, all of which require high-capacity brake and clutch systems. According to the U.S. Geological Survey's Mineral Commodity Summaries 2025, the value of nonfuel mineral commodity production in the United States reached approximately USD 106 billion in 2024, reflecting continued investment activity across ferrous and nonferrous metal production. In wind energy, according to the Global Wind Energy Council's Global Wind Report 2025, global wind power capacity reached 1,136 GW by the end of 2024, following 117 GW of new installations in that year alone. The Council forecasts an average of 164 GW of annual new capacity additions through 2030, creating a sustained long-term demand pipeline for rotor, yaw, and pitch brake systems that are critical to turbine control and emergency stopping functions.

The acceleration of industrial automation is further reinforcing demand for electromagnetic and spring-applied brakes and clutches. According to the International Federation of Robotics' World Robotics 2025 report, global industrial robot installations reached 542,000 units in 2024, more than double the volume installed a decade earlier, with a global operational stock of 4.66 million units across manufacturing industries. The expansion of robotic assembly lines, collaborative robot platforms, and automated guided vehicles, each of which requires compact, energy-efficient braking systems capable of precise torque control and fail-safe holding functions, is generating consistent incremental demand for electromagnetic brakes and spring-applied clutch/brake combinations across the industrial automation segment.

Despite strong structural growth drivers, the market faces challenges related to the high engineering specificity required for brake and clutch system selection in extreme-duty applications, where variations in duty cycle, ambient temperature, hazardous environment classification, and torque profile can significantly affect system performance and service life. The increasing prevalence of electrically driven machinery in sectors traditionally served by hydraulic or pneumatic actuation, including cranes, offshore drilling equipment, and mining conveyors, is requiring system manufacturers to develop hybrid electromechanical braking configurations that can deliver the torque capacity of conventional hydraulic systems within the control architecture of electric drive platforms. Additionally, the ongoing pressure on industrial operators to reduce total cost of ownership through extended maintenance intervals and remote condition monitoring is driving demand for brake and clutch systems with integrated sensor packages and digital monitoring capabilities.

Growing global investment in wind energy infrastructure, expanding adoption of industrial automation, and increasing demand for critical minerals are together creating significant opportunities for brake and clutch system manufacturers that can offer purpose-built solutions for the performance requirements of these high-growth end markets. The integration of condition monitoring and predictive maintenance capability into brake and clutch platforms is creating new service revenue opportunities for manufacturers that can offer connected powertrain component management alongside hardware supply. In emerging markets across Southeast Asia, the Middle East, and Africa, expanding investment in mining, port infrastructure, and industrial manufacturing is opening new demand centers for both standard and custom-engineered brake and clutch solutions that have historically been underserved by established global suppliers.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 4.22 Billion |

|

Market Size in 2026 |

USD 2.53 Billion |

|

Market Size in 2025 |

USD 2.43 Billion |

|

Revenue Growth Rate (2026–2036) |

CAGR of 5.2% |

|

Dominating Product Type |

Industrial Brakes |

|

Fastest Growing Product Type |

Electromagnetic Brakes and Clutches |

|

Dominating Actuation |

Hydraulic |

|

Fastest Growing Actuation |

Electromagnetic |

|

Dominating End-use Industry |

Mining and Mineral Processing |

|

Fastest Growing End-use Industry |

Wind Energy |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Wind Energy Capacity Expansion Creating Sustained Long-Term Demand for Specialized Rotor, Yaw, and Pitch Brake Systems

The global wind energy sector's accelerating deployment trajectory represents one of the most structurally durable growth drivers for purpose-built industrial brake systems in the current market. Wind turbines require multiple distinct brake system types to manage rotor deceleration during emergency stops, yaw system positioning to align the nacelle with wind direction, and pitch control to adjust blade angle for load management. All of these functions depend on hydraulic, spring-applied, or electromechanical brake and clutch systems that must perform reliably across multi-decade operational lifetimes in remote or offshore environments where maintenance access is constrained and system failure can result in significant production loss or structural damage.

According to the Global Wind Energy Council's Global Wind Report 2025, global wind power capacity reached 1,136 GW by the end of 2024 following 117 GW of new additions in that year, comprising 109 GW from onshore installations and 8 GW from offshore wind. The Council projects annual new capacity additions to reach an average of 164 GW through 2030, representing a continuous pipeline of new turbine installations each requiring application-specific brake components across rotor, yaw, pitch, and generator shaft positions. The projected CAGR for the global wind sector is 8.8% through 2030, establishing wind energy as the fastest-growing primary demand segment for industrial brake systems globally.

The technical requirements of wind turbine brake systems differ substantially from those in conventional industrial applications, demanding high cyclic fatigue resistance, corrosion protection for offshore and coastal environments, and compatibility with turbine control electronics for automated engagement. Leading brake system manufacturers including Regal Rexnord Corporation, through its Svendborg Brakes and Twiflex brands, and Dellner Bubenzer Group have developed dedicated wind turbine brake product lines combining disc brake calipers, hydraulic power units, and electronic control systems designed specifically for onshore and offshore turbine platforms. The ongoing transition toward larger wind turbine platforms with higher rotor torque and heavier nacelle assemblies is increasing the performance requirements for yaw and rotor brakes, creating upgrade and replacement demand even across older turbine installations as operators seek to extend asset operational life.

Industrial Automation and Industry 4.0 Adoption Driving Demand for Precision Electromagnetic and Spring-Applied Brake and Clutch Systems

The sustained expansion of industrial automation across global manufacturing sectors is generating increasing demand for compact, electronically controlled electromagnetic brakes and spring-applied clutch/brake combinations that can integrate directly into servo motor drives, robotic joints, and automated guided vehicle platforms. According to the International Federation of Robotics' World Robotics 2025 report, global industrial robot installations reached 542,000 units in 2024, more than double the annual volume recorded a decade earlier, with the global operational stock of industrial robots growing to 4.66 million units. China alone accounted for 295,000 robot installations in 2024, representing 54% of global deployments, while India recorded a new high of 9,100 units installed, up 7% year on year.

Each servo-driven robotic axis and automated guided vehicle drive system requires an integrated fail-safe electromagnetic or permanent magnet brake capable of reliably holding the load in a power-off condition and engaging rapidly in response to emergency stop commands. The proliferation of collaborative robots, automated guided vehicles, and autonomous mobile robots across logistics, automotive, and electronics manufacturing environments is creating strong incremental demand for compact, low-inertia electromagnetic brake and clutch combinations that can fit within the constrained form factors of these automation platforms while delivering the consistent engagement torque and response time required for safe operation alongside human workers.

The evolution of Industry 4.0 platforms is also accelerating the transition from conventional fixed-interval replacement of brake and clutch components toward condition-based maintenance approaches that leverage onboard sensors and connectivity to assess component wear in real time. Manufacturers including Kendrion N.V. and Mayr Antriebstechnik GmbH & Co. KG are integrating wear monitoring sensors and condition diagnostics directly into brake and clutch assemblies, enabling plant operators to assess brake lining wear, engagement response time, and holding torque performance without manual inspection. This shift toward sensor-equipped brakes and clutches is reinforcing procurement from manufacturers that offer connected system capabilities alongside hardware, creating a competitive distinction for suppliers that can deliver complete digital powertrain component management solutions rather than standalone mechanical components.

Mining and Mineral Processing Capacity Expansion Sustaining Procurement of High-Torque Hydraulic and Pneumatic Brake and Clutch Systems

Mining and mineral processing operations represent the most demanding torque and thermal performance environment for industrial brake and clutch systems, where shaft-mounted caliper disc brakes and fluid power clutches must manage the inertial loads of large conveyors, hoists, crushers, and grinding mills operating continuously under high ambient temperatures and dust loading. These applications require brake and clutch systems engineered to specific shaft dimensions, duty cycles, and stopping torque profiles, and represent a stable long-cycle procurement category driven by both new capacity additions and the ongoing replacement of wear components across existing installed equipment.

Global demand for critical minerals required for clean energy technologies including electric vehicle batteries, power grid storage, and wind turbine components is sustaining capital investment in mining capacity across multiple commodities. According to the U.S. Geological Survey's Mineral Commodity Summaries 2025, the value of nonfuel mineral commodity production in the United States reached approximately USD 106 billion in 2024, with copper, gold, and iron ore among the commodities valued at more than USD 1 billion individually. Internationally, sustained capital allocation toward copper, lithium, cobalt, and nickel extraction in Latin America, Africa, and Australia is driving ongoing procurement of high-capacity conveyor drive systems, grinding mill drives, and shaft hoisting equipment that each rely on application-engineered hydraulic and pneumatic clutch and brake systems for load control and emergency stopping.

Leading manufacturers including Regal Rexnord Corporation through its Wichita Clutch and Industrial Clutch brands, Eaton Corporation plc through its Airflex product line, and Dellner Bubenzer Group offer purpose-built fluid power clutches and disc brake systems for mining conveyor, hoist, and mill drive applications, addressing the high torque capacities and thermal management requirements of these installations. The expansion of deep-level and remote mining operations is also increasing demand for brake and clutch systems certified for hazardous area operation, as well as for custom-engineered configurations capable of managing the higher inertial loads associated with larger-capacity mining equipment designed to meet the productivity requirements of modern high-volume extraction operations.

By Product Type: In 2026, the Industrial Brakes Segment to Dominate the Global Industrial Brakes and Clutches Market

Based on product type, the industrial brakes and clutches industry is segmented into industrial brakes and industrial clutches. In 2026, the industrial brakes segment is expected to account for the largest share of this market. The leading position of this segment is attributed to the broad deployment of disc brakes, drum brakes, caliper brakes, and spring-applied brakes across the full range of safety-critical industrial applications where controlled deceleration, emergency stopping, and load-holding performance are mandatory functional requirements. In mining conveyor systems, hoisting equipment, offshore cranes, and wind turbine rotor systems, the braking system represents the primary mechanical safety device and is subject to the most stringent engineering specification, certification, and maintenance requirements of any powertrain component. The need for certified fail-safe operation in hazardous environments classified under ATEX, IECEx, and MSHA standards, combined with the requirement for engineered solutions that address specific shaft dimensions, mounting configurations, and torque capacities, reinforces the higher average selling price and revenue concentration in the industrial brakes segment.

Within industrial brakes, the caliper disc brake subsegment, including hydraulic and spring-applied caliper configurations, is expected to account for the largest share, driven by the proven performance of this technology in high-torque, high-thermal applications including mining hoists, offshore drilling draw-works, and crane systems where precise engagement control and reliable heat dissipation are required across continuous-duty operating cycles.

However, the electromagnetic brakes and clutches segment is projected to register the highest growth during the forecast period. The high growth of this segment is driven by the accelerating adoption of servo motor-driven automation platforms, collaborative robotics, and automated guided vehicles across global manufacturing and logistics operations, each of which requires compact electromagnetic or permanent magnet brake and clutch systems capable of delivering fast response times, precise engagement control, and fail-safe holding performance within the space and weight constraints of modern automation hardware.

By Actuation: In 2026, the Hydraulic Actuation Segment to Account for the Largest Share

Based on actuation, the industrial brakes and clutches industry is segmented into hydraulic, pneumatic, electromagnetic, spring-applied, and others. In 2026, the hydraulic actuation segment is expected to account for the largest share of this market. This dominance is driven by the widespread adoption of hydraulically actuated disc brakes and fluid power clutch systems across the most demanding heavy-industry applications, including mining conveyors, offshore cranes and winches, oil and gas drilling draw-works, and rolling mill drives, where hydraulic actuation provides the torque capacity, thermal management, and precise engagement control required to safely manage high-inertia rotating machinery. The ability of hydraulically actuated systems to deliver controlled braking torque over extended engagement cycles, combined with the inherent fail-safe characteristic of spring-offset hydraulic caliper designs, makes hydraulic actuation the dominant technology choice for high-consequence industrial braking applications globally.

However, the electromagnetic actuation segment is projected to register the highest growth during the forecast period. The high growth of this segment is driven by the rapid expansion of industrial automation, robotics, and servo drive applications that require electronically controlled, compact brake and clutch systems capable of integration with digital control architectures. The proliferation of electromagnetic spring-applied brakes and permanent magnet brakes in servo motors, collaborative robots, automated guided vehicles, and packaging and material handling equipment is generating consistent incremental demand across a broad installed base of automation hardware that continues to expand at an accelerating pace in Asia Pacific and other high-growth manufacturing regions.

By End-use Industry: In 2026, the Mining and Mineral Processing Segment to Hold the Largest Share

Based on end-use industry, the industrial brakes and clutches industry is segmented into mining and mineral processing, oil and gas, wind energy, marine and offshore, metals and steel processing, crane, hoist and material handling, paper and pulp, power generation, construction and heavy equipment, and other end-use industries. In 2026, the mining and mineral processing segment is expected to account for the largest share of this market. This reflects the dominant position of this sector as the single largest end-use category for high-torque hydraulic and pneumatic brake and clutch systems, where conveyor belt drives, hoist systems, grinding mill drives, and crusher drives each require engineered brake and clutch systems capable of managing the highest inertial loads encountered in industrial machinery operation. The sustained global capital investment in metal and mineral extraction driven by demand from the clean energy transition, particularly for copper, lithium, cobalt, nickel, and iron ore, maintains active procurement of both OEM powertrain components for new capacity installations and replacement wear parts for the existing mining equipment fleet.

However, the wind energy segment is projected to register the highest CAGR during the forecast period. The high growth of this segment is driven by the record pace of new wind turbine installations globally and the specific, recurring brake system requirements of each turbine installation across rotor, yaw, pitch, and generator shaft positions. With global wind power capacity projected to grow at a CAGR of 8.8% through 2030 according to Global Wind Energy Council data, the cumulative number of wind turbines in operation globally will continue to expand, creating both new installation demand for turbine brake systems and a growing base of operating turbines requiring periodic brake lining replacement and caliper overhaul across multi-decade operational lives.

Based on geography, the overall industrial brakes and clutches market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. In 2026, North America is expected to account for the largest share of this market. This growth is driven by the highest concentration of safety-regulation-driven procurement in industrial brake and clutch systems globally, encompassing MSHA enforcement of braking system performance standards for mining equipment, OSHA general industry regulations governing machinery guarding and motion control, and API standards for oil and gas drilling equipment that collectively mandate documented engineering controls for rotating machinery in hazardous operating environments. The substantial installed base of oil and gas drilling and production equipment across the Gulf of Mexico and onshore basins in the United States and Canada represents a significant recurring demand source for pneumatic and hydraulic clutch systems used in draw-work, pump drive, and mud pump applications. The presence of leading system manufacturers including Regal Rexnord Corporation and Eaton Corporation plc, together with established distribution and aftermarket service networks, reinforces the procurement confidence of North American industrial buyers seeking certified and fully supported brake and clutch solutions.

However, the Asia Pacific industrial brakes and clutches market is expected to grow at the fastest rate from 2026 to 2036. The rapid growth of this market is driven by the massive expansion of mining, steel processing, and cement manufacturing capacity across China, India, Australia, and Southeast Asia, all of which generate sustained demand for high-torque brake and clutch systems across conveyor, hoist, and mill drive applications. China's continuing investment in manufacturing automation, which drove the country to account for 295,000 of the 542,000 industrial robots installed globally in 2024 according to the International Federation of Robotics, is generating incremental demand for electromagnetic and spring-applied brakes across servo-driven manufacturing platforms. India's growing wind energy deployment, with 3,420 MW of new wind capacity added in 2024 according to the Global Wind Energy Council's Global Wind Report 2025, and its expanding mining activity driven by government investment in critical mineral extraction are creating additional demand centers for purpose-built brake and clutch systems across these sectors.

Europe is a large and well-established market for industrial brakes and clutches, supported by a mature industrial base across sectors including steel, automotive, marine, and paper and pulp manufacturing. The region's strong regulatory framework, including the ATEX Directive for equipment used in potentially explosive atmospheres, the Machinery Directive, and ISO performance standards governing crane and hoist braking systems, sustains compliance-driven procurement of certified brake and clutch systems across European manufacturing industries. European manufacturers including Dellner Bubenzer Group, Mayr Antriebstechnik GmbH & Co. KG, KEB Automation KG, SIBRE Siegerland-Bremsen GmbH, and R+W Antriebselemente GmbH maintain strong competitive positions in their home region supported by close application engineering relationships and deep expertise across European industrial end markets.

The global industrial brakes and clutches market is moderately consolidated, with competition primarily driven by torque handling capacity, environmental certification coverage, application engineering expertise, and the strength of aftermarket friction lining and spare parts supply networks. Key differentiators include certification coverage for hazardous area classifications under ATEX, IECEx, MSHA, and API standards; the availability of custom-engineered configurations for specific shaft dimensions, duty cycles, and mounting arrangements; the integration of condition monitoring sensors and digital service platforms into brake and clutch assemblies; and the geographic reach of field service and repair capabilities across end-user operating sites.

Large diversified industrial powertrain manufacturers such as Regal Rexnord Corporation and Eaton Corporation plc compete through comprehensive brake and clutch product portfolios addressing the full range of actuation technologies, broad global distribution networks, and strong aftermarket supply positions in friction linings, hydraulic power units, and spare components that generate recurring revenue alongside capital equipment sales. Specialty industrial brake manufacturers including Dellner Bubenzer Group and SIBRE Siegerland-Bremsen GmbH compete through deep application expertise in heavy-industry installations for mining, marine, offshore, and crane markets, while precision electromagnetic brake and clutch specialists including Kendrion N.V. and Mayr Antriebstechnik GmbH & Co. KG compete through superior electromagnetic design and close integration with servo motor drive manufacturers and automation system integrators. Regionally focused manufacturers including KEB Automation KG and R+W Antriebselemente GmbH maintain strong competitive positions in European automation markets, while Ogura Industrial Corp. competes effectively across Asian automation and light-industrial markets through its established electromagnetic clutch and brake product range.

The report provides a comprehensive competitive analysis based on an assessment of key players' product portfolios, geographic presence, and strategic initiatives undertaken over the past few years.

Some of the key players operating in the global industrial brakes and clutches market include Regal Rexnord Corporation (U.S.), Eaton Corporation plc (Ireland), Kendrion N.V. (Netherlands), Dellner Bubenzer Group (Sweden), Mayr Antriebstechnik GmbH & Co. KG (Germany), Ogura Industrial Corp. (Japan), SIBRE Siegerland-Bremsen GmbH (Germany), KEB Automation KG (Germany), WPT Power Corporation (U.S.), Hilliard Corporation (U.S.), Force Control Industries, Inc. (U.S.), Carlisle Brake & Friction (U.S.), Miba AG (Austria), R+W Antriebselemente GmbH (Germany), and Cross+Morse (UK), among others.

The global industrial brakes and clutches market is expected to reach USD 4.22 billion by 2036 from an estimated USD 2.53 billion in 2026, at a CAGR of 5.2% during the forecast period 2026–2036.

In 2026, the industrial brakes segment is expected to hold the largest share of this market, driven by the broad deployment of disc, drum, caliper, and spring-applied brake systems across safety-critical applications in mining, crane and hoist, marine, and wind energy sectors.

The electromagnetic brakes and clutches segment is expected to register the highest CAGR during the forecast period 2026–2036, driven by the accelerating adoption of servo motor-driven automation platforms, collaborative robotics, and automated guided vehicles that require compact, electronically controlled fail-safe braking solutions.

In 2026, the hydraulic actuation segment is expected to hold the largest share of this market, reflecting the dominant position of hydraulically actuated disc brakes and fluid power clutch systems across heavy-industry applications including mining, offshore, and rolling mill operations.

The growth of this market is primarily driven by the global expansion of wind energy infrastructure, the accelerating adoption of industrial automation and robotics, sustained investment in mining and mineral processing driven by the clean energy transition, growing industrial capital expenditure in Asia Pacific, and the integration of condition monitoring and digital service capabilities into brake and clutch system platforms.

Key players in the global industrial brakes and clutches market include Regal Rexnord Corporation (U.S.), Eaton Corporation plc (Ireland), Kendrion N.V. (Netherlands), Dellner Bubenzer Group (Sweden), Mayr Antriebstechnik GmbH & Co. KG (Germany), Ogura Industrial Corp. (Japan), SIBRE Siegerland-Bremsen GmbH (Germany), KEB Automation KG (Germany), WPT Power Corporation (U.S.), Hilliard Corporation (U.S.), Force Control Industries, Inc. (U.S.), Carlisle Brake & Friction (U.S.), Miba AG (Austria), R+W Antriebselemente GmbH (Germany), and Cross+Morse (UK).

Asia Pacific is expected to register the highest growth rate in the global industrial brakes and clutches market during the forecast period 2026–2036, driven by the largest concentration of new industrial robot deployments globally, accelerating wind energy capacity additions, and the sustained expansion of mining and steel processing infrastructure across China, India, and Southeast Asia.

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates