Resources

About Us

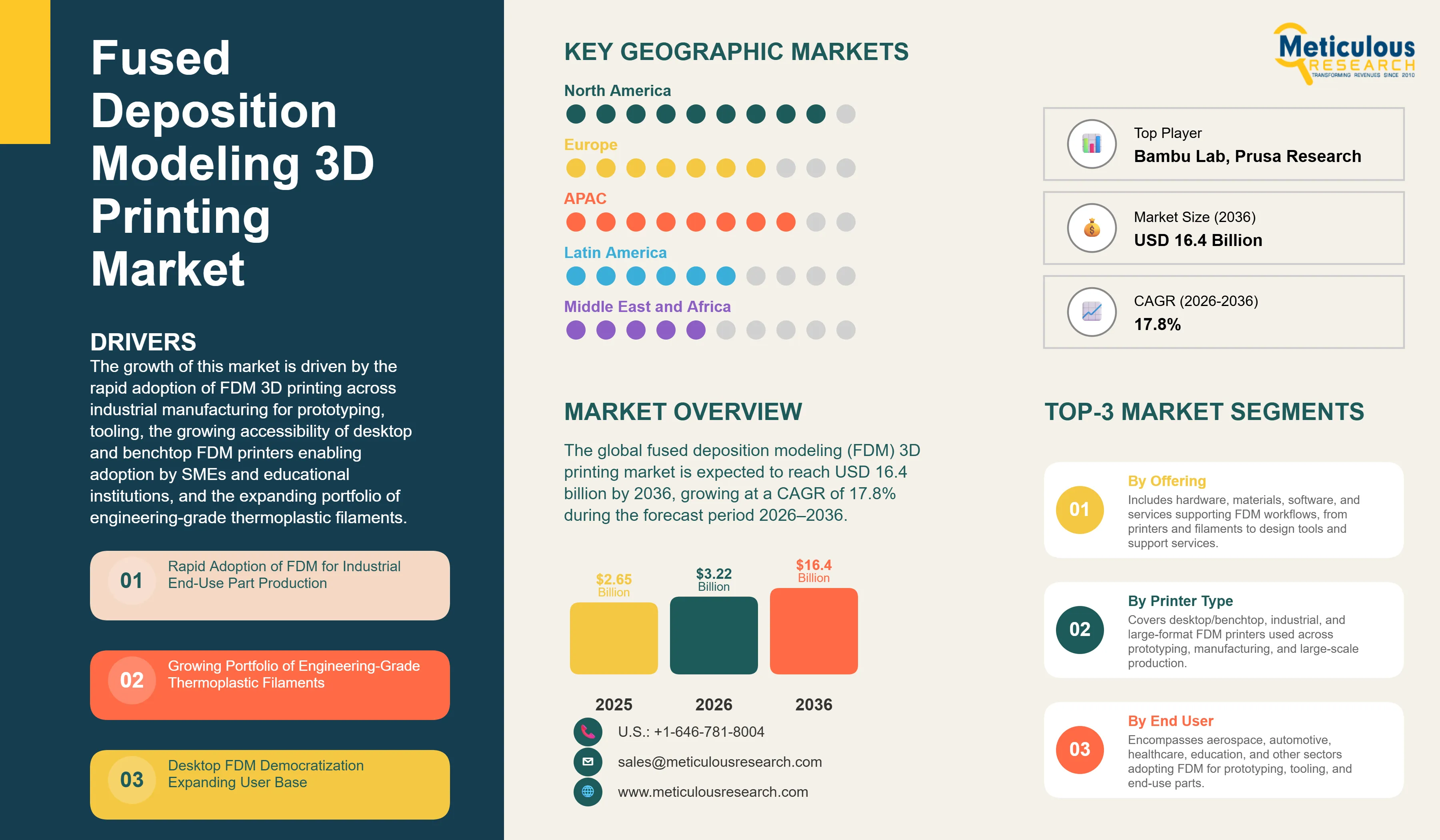

The global fused deposition modeling (FDM) 3D printing market was valued at USD 2.65 billion in 2025. This market is expected to reach USD 16.4 billion by 2036 from an estimated USD 3.22 billion in 2026, growing at a CAGR of 17.8% during the forecast period 2026–2036.

The growth of this market is primarily driven by the rapid adoption of FDM 3D printing across industrial manufacturing for prototyping, tooling, and end-use part production, the growing accessibility of desktop and benchtop FDM printers enabling adoption by SMEs and educational institutions, and the expanding portfolio of engineering-grade thermoplastic filaments including high-performance polymers such as PEEK, ULTEM, and polycarbonate that are enabling FDM to address functional manufacturing requirements.

However, the inherent anisotropic mechanical properties of FDM-produced parts, the relatively slow print speeds of FDM processes compared to powder bed fusion alternatives, and the post-processing requirements associated with support material removal restrain the growth of this market.

The growing adoption of large-format FDM systems in construction, tooling, and composite layup tool manufacturing; the emergence of continuous carbon fiber-reinforced FDM printing enabling lightweight structural component production; and the integration of FDM printing with generative design and AI-driven topology optimization software represent significant market growth opportunities.

Furthermore, the rising deployment of FDM printing in distributed on-demand manufacturing models and defense part reproduction programs is a major trend shaping this market.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global FDM 3D printing market includes all revenue generated from FDM printer hardware, filament and support material consumables, design and slicing software, and professional services, including maintenance, training, and managed printing, deployed across industrial and non-industrial end user segments globally.

FDM, the most widely deployed additive manufacturing technology worldwide, builds parts layer-by-layer by extruding molten thermoplastic filament through a heated nozzle onto a build platform, producing functional parts directly from digital design files without tooling requirements.

FDM’s combination of material versatility, equipment cost accessibility across the full range from sub-USD 200 desktop units to USD 500,000+ industrial systems, and compatibility with a growing portfolio of engineering-grade polymers has established it as the dominant additive manufacturing technology by installed base across virtually all end-user segments.

The most significant driver of the global FDM 3D printing market is the transition from prototyping-only use cases to series production of functional end-use parts, mainly in aerospace and defense, automotive, and medical device end markets.

Stratasys reported in 2025 that aerospace and defense represent its largest and fastest‑growing FDM‑based revenue segment, with flight‑capable thermoplastic parts produced on Fortus and F900 systems deployed across Boeing, Airbus, and Lockheed Martin supply chains.

The U.S. Air Force and Navy programs have qualified and deployed FDM‑produced ULTEM 9085 components for aircraft‑interior and non‑structural applications, while the U.S. Navy’s shipboard additive‑manufacturing program includes FDM‑class systems on multiple vessel classes for on‑demand replacement‑part production.

In healthcare, FDM is increasingly deployed for anatomical models, surgical planning guides, custom orthoses, and medical‑device prototyping, with FDA 510(k) clearance pathways for polymer‑extrusion–produced medical devices now well established.

Key 2025–2026 developments reshaping the FDM market include Stratasys’ launch of the H350 SAF system (a Powder‑Bed–based platform) and its ongoing Fortus‑platform refresh, Bambu Lab’s continued disruption of the desktop FDM segment with multi‑material, high‑speed printing, Markforged’s use of continuous‑fiber‑reinforced FFF/CFR in defense‑sector fixtures and tooling, and the growing adoption of Fused Granulate Fabrication (FGF), a large‑format pellet‑fed variant of FFF/FDM in automotive tooling, construction, and composite‑layup tool manufacturing.

Continuous Fiber Reinforcement Enabling Structural FDM Parts

The integration of continuous carbon fiber, fiberglass, and Kevlar reinforcement within FDM printing, pioneered by Markforged and now expanded to multiple vendors, is enabling the production of structural parts with tensile strengths approaching aluminum at substantially lower weight and without tooling investment.

Markforged’s Metal X and X7 composite systems are deployed across defense supply chains for flight-critical bracket and fixture production, and the U.S. Army and Navy both maintain Markforged systems for on-demand part reproduction at forward operating locations.

This trend is expanding the addressable application scope of FDM beyond non-structural components and accelerating adoption in aerospace, automotive, and industrial end markets that previously required metal fabrication.

Desktop FDM Democratization and Multi-Material Printing Accessibility

The rapid democratization of high-capability desktop FDM printing is being driven by Bambu Lab’s Core XY multi-material high-speed platforms, achieving print speeds of 500+ mm/s, along with the emergence of large-format desktop systems such as the PRUSA XL developed by Prusa Research. This shift is expanding the FDM user base into consumer, education, and SME markets at price points previously unavailable at comparable capability levels.

Bambu Lab achieved unicorn valuation in 2024 and displaced legacy desktop FDM brands across multiple markets based on product benchmarks, while Prusa Research continues to maintain strong positioning in community-driven and education-focused segments. This democratization trend is driving the highest unit volume growth in the desktop/benchtop segment and expanding the installed base, which in turn drives recurring revenue from filaments and software.

|

Parameters |

Details |

|---|---|

|

Market Size by 2036 |

USD 16.4 Billion |

|

Market Size in 2026 |

USD 3.22 Billion |

|

Market Size in 2025 |

USD 2.65 Billion |

|

Revenue Growth Rate (2026–2036) |

CAGR of 17.8% |

|

Dominating Offering |

Hardware |

|

Fastest Growing Offering |

Materials |

|

Dominating Printer Type |

Desktop/Benchtop FDM Printers |

|

Fastest Growing Printer Type |

Industrial FDM Printers |

|

Dominating End User |

Aerospace & Defense |

|

Fastest Growing End User |

Healthcare & Medical Devices |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Based on offering, the global FDM 3D printing market is segmented into hardware, materials, software, and services. In 2026, the hardware segment is expected to account for the largest share of around 45–50% of the global FDM 3D printing market.

The large market share of this segment is attributed to the dominant revenue contribution of FDM printer system sales across both desktop and industrial segments, the ongoing equipment upgrade cycles at aerospace and automotive OEMs and their supply chain partners, and the premium pricing of industrial FDM systems from Stratasys, 3D Systems, and competing vendors that concentrate hardware revenue at high average selling prices.

Stratasys’ Fortus 450mc and F900 industrial FDM systems are typically priced in the low‑ to mid‑six‑figure range per unit (roughly USD 100,000–300,000+ depending on configuration and region), and procurement cycles at defense and aerospace OEMs are generating steady, albeit episodic, hardware‑revenue streams.

However, the materials segment is projected to register the highest CAGR during the forecast period. The high growth of this segment is driven by the expanding portfolio of engineering-grade and high-performance thermoplastic filaments, including PEEK, ULTEM 9085, ULTEM 1010, polycarbonate, and composite filaments reinforced with carbon fiber, glass fiber, and metal particles, that command significantly higher per-kilogram prices than commodity PLA and ABS filaments.

The growing adoption of FDM for end-use part production (rather than prototyping) increases per-machine filament consumption substantially, and the proprietary filament ecosystems maintained by industrial FDM vendors ensure recurring, high-margin materials revenue per installed system.

Based on printer type, the global FDM 3D printing market is segmented into desktop/benchtop FDM printers, industrial FDM printers, and large-format FDM printers.

In 2026, the desktop/benchtop FDM printers segment is expected to account for the largest share by unit volume of the global FDM 3D printing market. The large market share of this segment is attributed to the multi-million unit installed base of desktop FDM systems globally across education, hobbyist, prosumer, and SME markets; the extremely high unit shipment volumes driven by sub‑USD 1,000 (and often sub‑USD 500) desktop systems from Bambu Lab, Prusa Research, Creality, and Elegoo; and the broad geographic distribution of desktop FDM adoption across developed and developing economies alike.

However, the industrial FDM printers segment is projected to register the highest CAGR during the forecast period by revenue. The high growth of this segment is driven by expanding procurement of Stratasys Fortus-series, F900, and Neo systems for aerospace tooling and end-use part production, the growing adoption of industrial FDM in automotive manufacturing for custom assembly fixtures and low-volume production parts, and the entry of new industrial FDM vendors, including Markforged, UltiMaker (following the merger with MakerBot), and Rize, which are broadening the competitive set and increasing total available spending in the industrial segment.

Based on end user, the global FDM 3D printing market is segmented into aerospace and defense, automotive, healthcare and medical devices, consumer electronics, education and research, architecture and construction, consumer products and retail, and others.

In 2026, the aerospace and defense segment is expected to account for the largest share of the global FDM 3D printing market by revenue. The large market share of this segment is attributed to the longest history of industrial FDM adoption, the highest per-unit equipment and materials spending driven by the use of premium ULTEM and polycarbonate materials in flight-qualified applications, and the defense sector’s sustained investment in FDM for on-demand maintenance parts production and distributed manufacturing.

Stratasys’ aerospace and defense customer base includes Boeing, Airbus, NASA, the U.S. Air Force, and dozens of tier-1 aerospace suppliers.

However, the healthcare and medical devices segment is projected to register the highest CAGR during the forecast period. The high growth of this segment is driven by the expanding use of FDM in anatomical model production for surgical planning, the growing adoption of FDM for custom orthoses and prosthetics manufacturing, and the increasing investment by medical device OEMs in FDM for design validation and limited-series device production.

FDA’s guidance on additive manufacturing for medical devices is increasingly clarifying the regulatory pathway for FDM-produced medical products, reducing the barriers to clinical deployment and accelerating growth of the healthcare segment.

Based on geography, the global FDM 3D printing market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. In 2026, North America is expected to account for the largest share of around 35–40% of the global FDM 3D printing market.

North America’s leading position is attributed to the headquarters location of Stratasys (Minnetonka, Minnesota) and the highest concentration of industrial FDM end users in aerospace and defense, an advanced manufacturing ecosystem that supports the highest per‑unit industrial FDM spending globally, and strong government support for additive manufacturing, including the America Makes national additive manufacturing institute and U.S. Department of Defense distributed manufacturing programs.

However, Asia Pacific is expected to register the highest growth rate during the forecast period. This growth is driven by the rapid expansion of China’s domestic FDM printer manufacturing ecosystem, led by companies such as Bambu Lab, Creality, Elegoo, and Flashforge, which collectively ship millions of desktop and prosumer units annually.

Additionally, increasing adoption of FDM technology in automotive and electronics manufacturing across Japan and South Korea, along with the growing deployment of FDM systems in educational and research institutions across China, India, and Southeast Asia, supported by government-led STEM and advanced manufacturing initiatives, is further accelerating regional market growth.

The global FDM 3D printing market exhibits a dual-tier competitive structure, characterized by a moderately concentrated industrial segment anchored by Stratasys Ltd., which maintains the largest installed base of industrial FDM systems globally, and a highly fragmented desktop/consumer segment comprising numerous vendors, predominantly headquartered in China. Competition within the industrial tier is primarily driven by material compatibility breadth, part accuracy and repeatability, build volume capabilities, and the strength of application engineering and customer support.

The report provides a comprehensive competitive assessment based on key strategic developments undertaken by leading players over the past few years. Prominent players operating in the global FDM 3D printing market include Stratasys Ltd., Bambu Lab, Prusa Research, Creality 3D Technology Co., Ltd., Markforged, Inc., UltiMaker B.V., 3D Systems Corporation, Formlabs, Inc., Zortrax S.A., Raise3D Technologies, Inc., ROBOZE S.r.l., Rize, Inc., Essentium, Inc., Cincinnati Incorporated, and BigRep GmbH, among others.

The global FDM 3D printing market is expected to reach USD 16.4 billion by 2036 from an estimated USD 3.22 billion in 2026, at a CAGR of 17.8% during the forecast period 2026–2036.

In 2026, the hardware segment is expected to hold the largest share of the global FDM 3D printing market.

The materials segment is expected to register the highest CAGR during the forecast period 2026–2036.

In 2026, the desktop/benchtop FDM printers segment is expected to hold the largest share of the global FDM 3D printing market by unit volume.

The growth of this market is driven by rapid adoption of FDM across industrial manufacturing, the growing accessibility of desktop FDM systems, the expanding portfolio of engineering-grade thermoplastic filaments, and the transition from prototyping to end-use part production. Key opportunities include continuous fiber reinforcement enabling structural FDM parts, large-format FDM in construction and automotive tooling, and distributed on-demand manufacturing programs in defense.

Key players are Stratasys Ltd., Bambu Lab, Prusa Research, Creality 3D Technology Co., Ltd., Markforged, Inc., UltiMaker B.V., 3D Systems Corporation, Formlabs, Inc., Zortrax S.A., Raise3D Technologies, Inc., ROBOZE S.r.l., Rize, Inc., Essentium, Inc., Cincinnati Incorporated, and BigRep GmbH.

Asia Pacific is expected to register the highest growth rate in the global FDM 3D printing market during the forecast period 2026–2036.

1. Introduction

1.1. Market Definition and Scope

1.2. Currency & Limitations

1.3. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Data Collection Methods

2.3. Market Estimation and Forecast Methodology

2.4. Assumptions and Limitations

3. Executive Summary

3.1. Market Overview

3.2. Market Analysis by Offering

3.3. Market Analysis by Printer Type

3.4. Market Analysis by End User

3.5. Market Analysis by Geography

4. Market Dynamics

4.1. Overview

4.2. Drivers

4.2.1. Rapid Adoption of FDM for Industrial End-Use Part Production

4.2.2. Growing Portfolio of Engineering-Grade Thermoplastic Filaments

4.2.3. Desktop FDM Democratization Expanding User Base

4.2.4. Defense and Aerospace Programs Driving Industrial FDM Procurement

4.3. Restraints

4.3.1. Anisotropic Mechanical Properties Limiting Structural Applications

4.3.2. Post-Processing Requirements for Support Material Removal

4.4. Opportunities

4.4.1. Continuous Fiber Reinforcement Enabling Structural FDM Components

4.4.2. Large-Format FDM in Construction, Automotive Tooling, and Composite Manufacturing

4.4.3. Distributed On-Demand Manufacturing in Defense Supply Chains

4.5. Challenges

4.5.1. Competition from Powder Bed Fusion and Resin-Based Additive Manufacturing

4.5.2. IP Fragmentation and Filament Ecosystem Lock-In

4.6. Porter’s Five Forces Analysis

5. FDM 3D Printing Market, by Offering

5.1. Overview

5.2. Hardware

5.2.1. FDM Printers

5.2.2. Print Heads

5.2.3. Build Platforms

5.3. Materials

5.3.1. Thermoplastic Filaments

5.3.1.1. PLA

5.3.1.2. ABS

5.3.1.3. PETG

5.3.1.4. Nylon

5.3.1.5. TPU

5.3.1.6. High-Performance Polymers (PEEK, ULTEM, PC)

5.3.2. Composite Filaments

5.3.3. Support Materials

5.4. Software

5.4.1. Design & Slicing Software

5.4.2. Simulation & Optimization Software

5.5. Services

5.5.1. Maintenance & Support

5.5.2. Training & Education

5.5.3. Managed 3D Printing Services

6. FDM 3D Printing Market, by Printer Type

6.1. Overview

6.2. Desktop/Benchtop FDM Printers

6.3. Industrial FDM Printers

6.4. Large-Format FDM Printers

7. FDM 3D Printing Market, by End User

7.1. Overview

7.2. Aerospace & Defense

7.3. Automotive

7.4. Healthcare & Medical Devices

7.5. Consumer Electronics

7.6. Education & Research

7.7. Architecture & Construction

7.8. Consumer Products & Retail

7.9. Other End Users

8. FDM 3D Printing Market, by Geography

8.1. Overview

8.2. North America

8.2.1. U.S.

8.2.2. Canada

8.3. Europe

8.3.1. Germany

8.3.2. U.K.

8.3.3. France

8.3.4. Italy

8.3.5. Spain

8.3.6. Netherlands

8.3.7. Czech Republic

8.3.8. Poland

8.3.9. Rest of Europe

8.4. Asia Pacific

8.4.1. China

8.4.2. Japan

8.4.3. South Korea

8.4.4. India

8.4.5. Australia

8.4.6. Singapore

8.4.7. Rest of Asia Pacific

8.5. Latin America

8.5.1. Brazil

8.5.2. Mexico

8.5.3. Rest of LATAM

8.6. Middle East and Africa

8.6.1. UAE

8.6.2. Saudi Arabia

8.6.3. South Africa

8.6.4. Rest of MEA

9. Competitive Landscape

9.1 Overview

9.2 Key Growth Strategies

9.3 Competitive Benchmarking

9.4 Competitive Dashboard

9.4.1 Industry Leaders

9.4.2 Market Differentiators

9.4.3 Vanguards

9.4.4 Emerging Companies

9.5 Market Share Analysis (2025)

10. Company Profiles

10.1. Stratasys Ltd.

10.2. Bambu Lab

10.3. Prusa Research a.s.

10.4. Creality 3D Technology Co., Ltd.

10.5. Markforged, Inc.

10.6. UltiMaker B.V.

10.7. 3D Systems Corporation

10.8. Formlabs, Inc.

10.9. Zortrax S.A.

10.10. Raise3D Technologies, Inc.

10.11. ROBOZE S.r.l.

10.12. Rize, Inc.

10.13. Essentium, Inc.

10.14. Cincinnati Incorporated

10.15. BigRep GmbH

10.16. Others

11. Appendix

11.1. Questionnaire

11.2. Available Customization Options

11.3. Related Reports

Published Date: May-2023

Published Date: Jul-2022

Published Date: Oct-2024

Subscribe to get the latest industry updates