Resources

About Us

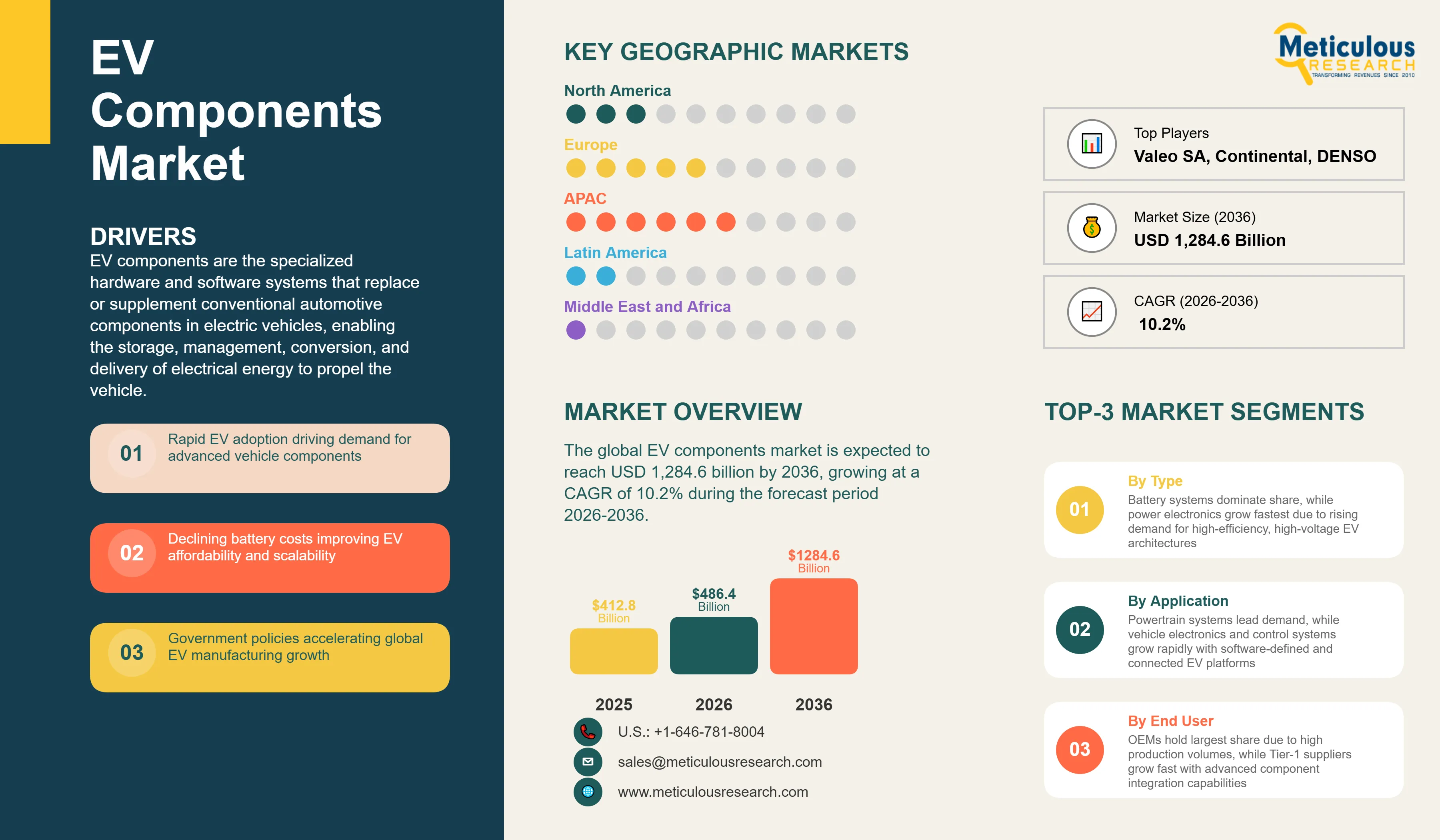

The global EV components market was valued at USD 412.8 billion in 2025. This market is expected to reach USD 1,284.6 billion by 2036 from an estimated USD 486.4 billion in 2026, growing at a CAGR of 10.2% during the forecast period 2026-2036. According to the IEA's Global EV Outlook 2025, global electric car sales reached approximately 17 million units in 2024, representing approximately 20% of all new cars sold globally, and the IEA projects electric vehicles will account for well over half of new car sales globally before the end of this decade under its Stated Policies Scenario, establishing the long-term trajectory that is driving EV component market growth.

Click here to: Get Free Sample Pages of this Report

EV components are the specialized hardware and software systems that replace or supplement conventional automotive components in electric vehicles, enabling the storage, management, conversion, and delivery of electrical energy to propel the vehicle. The battery system, which stores energy electrochemically in thousands of lithium-ion cells assembled into modules and packs with integrated battery management electronics, is the largest single component cost in an EV and the central enabling technology of the entire powertrain. The electric drive system converts the stored electrical energy into mechanical torque through a permanent magnet or induction electric motor and a reduction gearbox. Power electronics including the traction inverter, DC-DC converter, and on-board charger convert voltages and manage energy flow between the battery, motor, and electrical systems. Thermal management systems maintain the battery and drive components within their optimal temperature ranges. Vehicle control units and software tie everything together, managing energy use, driver interfaces, safety systems, and increasingly over-the-air feature updates.

The market is growing because global EV sales are growing at a pace that consistently exceeds even optimistic forecasts from a few years prior. According to the IEA's Global EV Outlook 2025, global electric car sales reached approximately 17 million units in 2024, representing approximately 20% of global new car sales. China's dominance is notable: the China Passenger Car Association reported over 12 million new energy vehicle sales in China in 2024, representing over 40% of China's total new passenger vehicle sales that year, making China's domestic EV market alone approximately equal to the entire global EV market of just three years earlier. According to BNEF and the IEA’s latest EV outlooks, global electric car sales were about 17 million in 2024 and are expected to keep rising strongly through 2030, with EVs reaching roughly 40% or more of new car sales globally under current policy settings.

Two specific technology trends are shaping the component landscape. The transition from 400-volt to 800-volt electrical architecture across premium and mass-market EV platforms is changing the specifications of every electrical component in the vehicle, requiring inverters, converters, motors, and charging systems designed for higher voltage operation that can support ultra-fast charging and improve drivetrain efficiency. According to Infineon Technologies' 2025 Automotive Market Outlook, wide-bandgap semiconductors particularly silicon carbide power devices are becoming the standard choice for 800-volt EV inverters and chargers, with the silicon carbide content per vehicle growing rapidly as 800-volt architecture adoption scales up. Separately, the progressive integration of vehicle software platforms and over-the-air update capabilities across all EV brands is expanding the vehicle control unit and software component category from a relatively minor item to a significant value driver within the overall EV component mix.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 1,284.6 Billion |

|

Market Size in 2026 |

USD 486.4 Billion |

|

Market Size in 2025 |

USD 412.8 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 10.2% |

|

Dominating Component Type |

Battery Systems |

|

Fastest Growing Component Type |

Power Electronics |

|

Dominating Vehicle Type |

Passenger Vehicles |

|

Fastest Growing Vehicle Type |

Commercial Vehicles |

|

Dominating Propulsion Type |

Battery Electric Vehicles (BEVs) |

|

Fastest Growing Propulsion Type |

Plug-in Hybrid Electric Vehicles (PHEVs) |

|

Dominating Application |

Powertrain Systems |

|

Fastest Growing Application |

Vehicle Electronics and Control Systems |

|

Dominating End User |

OEMs |

|

Fastest Growing End User |

Tier-1 Suppliers |

|

Dominating Material Type |

Metals (Aluminum, Copper) |

|

Fastest Growing Material Type |

Semiconductor Materials |

|

Dominating Geography |

Asia-Pacific |

|

Fastest Growing Geography |

Europe |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Battery Costs Continuing to Fall, Accelerating Mass Market Adoption

The steady decline in lithium-ion battery pack costs per kilowatt-hour has been the single most important trend enabling EV mass-market adoption, and it continued in 2024 and into 2025. According to BloombergNEF’s 2025 Battery Price Survey, average lithium-ion battery pack prices fell to a record low of about $108/kWh in 2025, reflecting continued cost declines driven by overcapacity, competition, and the shift to lower-cost chemistries. BloombergNEF projects that battery pack prices will reach approximately USD 105 per kWh by 2026, a level that is widely considered to make BEVs directly cost-competitive with comparable ICE vehicles at the point of purchase without subsidies in most major markets. CATL's announcement of its Shenxing Plus battery in 2025, claiming 4C ultra-fast charging capability and energy density above 370 Wh/kg at the cell level, illustrates the continued technology advancement alongside cost reduction that is sustaining the battery improvement trajectory.

The falling cost trajectory is also changing the relative importance of battery system cost within the total EV component bill of materials. As battery cost per kWh falls, automakers can afford to include larger battery packs for a given total vehicle price, improving range, while the share of total vehicle cost represented by the battery gradually decreases, improving vehicle economics for both manufacturers and consumers. According to Volkswagen Group's 2025 Annual Report, the company's internal battery cost reduction roadmap targets ongoing improvement in cell chemistry and manufacturing efficiency, and Volkswagen's unified cell strategy, which will standardize one cell format across its multiple EV brands to achieve manufacturing scale efficiency, reflects the industry-wide push to reduce battery component costs through standardization and scale.

Silicon Carbide Semiconductors Transforming Power Electronics Architecture

The adoption of silicon carbide power semiconductors in EV traction inverters and on-board chargers is one of the most commercially significant technology transitions in the EV components market, as SiC devices enable more efficient, more compact, and more thermally capable power conversion than conventional silicon IGBTs while being essential for the 800-volt vehicle architectures that support ultra-fast charging. According to Infineon Technologies' 2025 Automotive Market Outlook, the silicon carbide power device market in automotive applications is growing at above-average rates as 800-volt EV platforms proliferate across OEM product lines. Infineon, which acquired Cypress Semiconductor and expanded its power semiconductor capabilities specifically to serve the EV market, reported its Automotive segment revenues growing above average in its 2025 first half results, driven by SiC inverter content growth.

The supply chain for silicon carbide is increasingly competitive, with major semiconductor companies including STMicroelectronics, Wolfspeed, onsemi, and Bosch investing heavily in SiC wafer and device manufacturing capacity. According to STMicroelectronics' 2025 investor communications, the company is investing around USD 1.8 billion in SiC manufacturing capacity expansion to serve automotive customer demand, reflecting the scale of procurement commitments it has received from EV OEMs and Tier-1 suppliers for SiC inverter content in upcoming EV platforms. Tesla's in-house development of SiC-based inverter technology for its own vehicles and CATL's integration of power electronics into its CTP battery pack architecture are examples of how leading EV innovators are approaching the power electronics transition.

OEM Vertical Integration Reshaping the EV Component Supply Chain

A defining structural trend in the EV components market is the progressive vertical integration of major EV OEMs into the production of key components that were previously sourced entirely from Tier-1 suppliers and specialist component manufacturers. Tesla has been the pioneer of this approach, producing its own battery cells through the Gigafactory in partnership with Panasonic and developing its own traction inverter, BMS software, and vehicle control systems in-house. BYD has taken vertical integration further than any other EV manufacturer, producing its own batteries through its FinDreams Battery subsidiary, its own power semiconductors through BYD Semiconductor, electric motors, and a large proportion of other key EV components, allowing it to maintain very competitive manufacturing costs. According to BYD’s 2024 Annual Report, the company sold about 1.765 million battery electric vehicles globally in 2024 and roughly 4.27 million new energy vehicles overall, reinforcing its position as one of the world’s leading EV manufacturers and supporting its vertically integrated component strategy.

The traditional automotive Tier-1 suppliers are responding to this vertical integration pressure by accelerating their own transformation toward EV-optimized component offerings and in some cases developing direct relationships with battery manufacturers and semiconductor companies that bypass the OEM layer for component development. Bosch has invested heavily in SiC power semiconductor development, Valeo has developed its own electric motor and power electronics systems, and ZF Friedrichshafen has expanded into electric drive system integration. According to Bosch's 2025 financial results presentation, its e-Mobility division was growing at significantly above-average rates, with EV powertrain components representing a growing share of its overall automotive technology revenue.

Rapid Adoption of Electric Vehicles Globally

According to the IEA's Global EV Outlook 2025, global electric car sales reached approximately 17-18 million units in 2024, representing approximately 20% of all new cars sold globally and marking the first time that electric vehicles exceeded one in five new car sales worldwide. The China Passenger Car Association's 2025 data shows over 12 million NEV sales in China in 2024, representing more than 40% of domestic new passenger vehicle sales. According to BloombergNEF's Electric Vehicle Outlook 2025, EV penetration is expected to reach 46% of global new car sales by 2030 under its main scenario, implying continued rapid demand growth for every EV component category throughout the forecast period. Global commercial vehicle electrification is also accelerating, with electric bus deployments growing across China, Europe, and increasingly other markets, and electric trucks entering commercial service with Daimler Truck, Volvo Trucks, and Tesla Semi generating growing commercial vehicle EV component demand alongside the dominant passenger vehicle market.

Declining Battery Costs

According to BloombergNEF's Battery Price Survey 2025, average lithium-ion battery pack prices fell to approximately USD 108 per kWh in 2025. BloombergNEF projects further falls toward approximately USD 105 per kWh by 2026, approaching the price parity threshold with ICE vehicles. CATL's announcement in 2025 of its Shenxing Plus battery at above 370 Wh/kg energy density and 4C charging capability demonstrates that cost reduction and performance improvement are advancing simultaneously. The IEA's Critical Minerals Market Review 2025 noted that lithium prices in 2024 fell significantly from their 2022 peak, easing one of the primary raw material cost pressures on battery manufacturers and contributing to the continued pack cost reduction trajectory.

Growth in Next-Generation Batteries (Solid-State)

Solid-state batteries, which replace the liquid electrolyte in conventional lithium-ion cells with a solid ionic conductor, promise higher energy density, faster charging, and improved safety compared with liquid-electrolyte cells, and their commercial development is approaching key milestones. According to Toyota's disclosed roadmap, the company aims to begin solid-state battery production for EVs between 2027 and 2028, a timeline that has been updated and reaffirmed in the company's 2025 investor communications. QuantumScape reported in its 2025 first quarter results that it had begun shipping Alpha-2 generation solid-state battery cells to automotive partners for validation testing. Solid Power also reported automotive partner testing progress in its 2025 communications. If these programs achieve the reliability and cost targets required for automotive qualification, solid-state batteries could represent a step-change improvement in EV range, charging speed, and safety that drives a new component specification cycle with very large procurement implications for battery manufacturers and their material suppliers.

Integration of Power Electronics and Software

The progressive integration of power electronics, vehicle control software, and connectivity systems is creating a new category of intelligent EV component systems that deliver value through software as much as through hardware. OTA software updates that can add new features, improve efficiency, or correct safety issues without requiring a workshop visit are becoming standard practice across major EV brands. Infineon, NXP Semiconductors, and STMicroelectronics are all investing in automotive microcontroller and domain controller architectures specifically designed for software-defined vehicle platforms, and this software and semiconductor content growth is driving above-average revenue growth in the vehicle electronics and control systems component category.

By Component Type: In 2026, Battery Systems to Dominate

Based on component type, the global market for EV components is segmented into battery systems (cells, modules, packs, and BMS), electric drive systems (motors and gearboxes), power electronics (inverters, converters, and on-board chargers), thermal management systems, charging components, vehicle control units and software, and other components. In 2026, the battery systems segment is expected to account for the largest share of the global EV components market. The battery pack typically represents 30 to 40% of total EV vehicle cost according to BloombergNEF's 2025 analysis, making it the single largest component cost in any EV. With approximately 17-18 million EV sales in 2024 and growing rapidly, the scale of battery system procurement is the dominant revenue category in the EV component market by a very large margin. CATL's 2025 annual revenue exceeding RMB 423 billion, a substantial portion from EV battery sales, illustrates the commercial scale of the battery systems segment.

However, the power electronics segment is projected to register the highest CAGR during the forecast period. The transition to 800-volt vehicle architectures, the adoption of silicon carbide inverters, the growing complexity of multi-motor EV drivetrains, and the increasing sophistication of on-board charging systems are all driving above-average growth in power electronics content per vehicle.

By Vehicle Type: In 2026, Passenger Vehicles to Hold the Largest Share

Based on vehicle type, the global EV components market is segmented into passenger vehicles, commercial vehicles, and two-wheelers and three-wheelers. In 2026, the passenger vehicles segment is expected to account for the largest share of the global EV components market. Passenger EVs represent the overwhelming majority of global EV sales by unit count and by total component procurement value.

However, the commercial vehicles segment is projected to register the highest CAGR during the forecast period. Electric buses and trucks are at an earlier stage of electrification than passenger cars but are transitioning rapidly, particularly in China where electric bus fleets are already very large, and in Europe and North America where zero-emission truck regulations in California and the EU's CO2 standards for heavy-duty vehicles are compelling commercial vehicle manufacturers to accelerate electrification. Each commercial EV contains significantly more battery and drivetrain component value than a passenger EV due to its larger battery pack, higher-powered motor, and more robust charging system, making commercial vehicle electrification a high-value growth segment for EV component suppliers.

EV Components Market by Region: Asia-Pacific Leading by Share, Europe by Growth

Based on geography, the global EV components market is segmented into Asia-Pacific, North America, Europe, Latin America, and the Middle East and Africa.

In 2026, Asia-Pacific is expected to account by far the largest share of the global EV components market. China's dominance of the global EV industry is reflected in its dominance of the EV components market: the China Passenger Car Association reported over 12 million NEV sales in China in 2024, representing over 40% of domestic new vehicle sales and well over half of global EV sales. China hosts the world's largest battery manufacturers including CATL and BYD, the world's most active EV manufacturing base producing vehicles for domestic consumption and export, and a large domestic supply chain for EV components from battery cells to power electronics and motors. CATL's 2025 revenues exceeding RMB 423 billion confirm the commercial scale of the Chinese battery manufacturing industry. South Korea's LG Energy Solution, Samsung SDI, and SK On are the world's third, fourth, and fifth-largest EV battery manufacturers per SNE Research's 2025 data, with manufacturing facilities in South Korea and internationally, and Korea's significant automotive electronics and semiconductor industries add to Asia-Pacific's component procurement weight. Japan hosts Toyota, Honda, and major component suppliers including Denso, Aisin, and Panasonic that are all scaling up EV component development and production. India is beginning to transition its automotive production toward EVs, with domestic EV two-wheeler sales already very large and passenger EV sales growing rapidly.

However, the European market for EV components is expected to grow at the fastest CAGR during the forecast period. Europe's component market growth is driven by two powerful forces: the very large and accelerating EV production ramp-up by European automakers, and the EU's regulatory framework that creates binding demand through its 2035 effective ban on new ICE vehicle sales. According to the European Automobile Manufacturers Association's 2025 data, BEV market share in Europe reached approximately 14% of new car registrations in 2024 and is expected to continue growing as the 2035 deadline approaches. The European automotive supply chain including Bosch, Continental, ZF, Valeo, and their extensive Tier-1 and Tier-2 supplier networks is investing heavily in EV component manufacturing capacity, with Bosch's 2025 results showing its e-Mobility division growing significantly above the company's overall average. Northvolt's battery manufacturing in Sweden, and the CATL, BYD, and Samsung SDI European cell manufacturing facilities under various stages of development, are building out the European battery component supply chain. The EU Battery Regulation's domestic manufacturing incentives and battery passport requirements are creating additional policy-driven investment in European EV component production capacity.

North America is a rapidly growing EV components market, driven by the U.S. Inflation Reduction Act's domestic content requirements that effectively mandate U.S.-based EV component manufacturing to qualify for the consumer EV tax credit. According to the Alliance for Automotive Innovation's 2025 data, U.S. EV sales reached approximately 1.3 million units in 2024, representing approximately 8% of new car sales and growing. The IRA's Section 45X manufacturing tax credits are supporting the construction of U.S. battery cell and component manufacturing facilities by Panasonic in Kansas, LG Energy Solution in Michigan and Arizona, Samsung SDI in Indiana, and SK On in Georgia, each representing multi-billion dollar investments that will generate significant U.S. domestic EV component procurement as they reach full production through the forecast period.

The EV components market is served by a diverse ecosystem including dedicated EV battery manufacturers that dominate the highest-value component category, traditional automotive Tier-1 suppliers transitioning their product portfolios toward EV-specific components, semiconductor companies developing power devices and microcontrollers for EV applications, and the OEMs themselves through vertical integration of key component manufacturing. Competition is based on component performance specifications, manufacturing scale efficiency, supply security, EV-specific technology capabilities particularly in battery chemistry and power electronics, and the depth of OEM co-development relationships.

CATL is the world's dominant EV battery manufacturer, reporting revenues exceeding CNY 360 billion in 2025 and holding approximately 37% global market share per SNE Research's 2025 data, with products ranging from standardized LFP cells for mass-market EVs to high-performance NMC cells and its proprietary cell-to-pack and cell-to-chassis battery architectures for premium applications. BYD is both the world's largest EV manufacturer and a major battery and component supplier through its FinDreams Battery and BYD Semiconductor subsidiaries, with over 1.76 million BEV sales in 2024 per the company's 2025 Annual Report. Bosch's e-Mobility division is growing rapidly, covering electric motors, power electronics, and integrated drive systems, with the company investing over EUR 3 billion in electromobility in recent years according to its 2025 results communications. Valeo reported its electrification-related revenues growing significantly above its overall top line in its 2025 half-year results, driven by 48V mild hybrid and full electric drive system deliveries. Infineon Technologies is the world's leading automotive semiconductor company and a critical supplier of SiC inverter devices and microcontrollers for EV applications, with its 2025 automotive segment growing above average driven by EV power semiconductor demand.

The report provides a comprehensive competitive analysis based on a thorough review of leading players' product portfolios, manufacturing scale, OEM relationships, and recent strategic developments. Some of the key players operating in the global EV components market include Robert Bosch GmbH (Germany), DENSO Corporation (Japan), Continental AG (Germany), BYD Company Ltd. (China), Contemporary Amperex Technology Co. Limited/CATL (China), LG Energy Solution Ltd. (South Korea), Panasonic Holdings Corporation (Japan), Samsung SDI Co. Ltd. (South Korea), Valeo SA (France), ZF Friedrichshafen AG (Germany), Magna International Inc. (Canada), Hyundai Mobis Co. Ltd. (South Korea), Aisin Corporation (Japan), Infineon Technologies AG (Germany), and NXP Semiconductors N.V. (Netherlands), among others.

The global EV components market is expected to reach USD 1,284.6 billion by 2036 from an estimated USD 486.4 billion in 2026, at a CAGR of 10.2% during the forecast period 2026-2036.

The power electronics segment is projected to register the highest CAGR

Asia-Pacific dominates, with China alone accounting for over 12 million NEV sales in 2024 per the China Passenger Car Association's 2025 data, representing over 40% of domestic new vehicle sales.

Key players are Robert Bosch GmbH (Germany), DENSO Corporation (Japan), Continental AG (Germany), BYD Company Ltd. (China), CATL (China), LG Energy Solution Ltd. (South Korea), Panasonic Holdings Corporation (Japan), Samsung SDI Co. Ltd. (South Korea), Valeo SA (France), ZF Friedrichshafen AG (Germany), Magna International Inc. (Canada), Hyundai Mobis Co. Ltd. (South Korea), Aisin Corporation (Japan), Infineon Technologies AG (Germany), and NXP Semiconductors N.V. (Netherlands), among others.

Europe is expected to register the highest growth rate during the forecast period 2026-2036. According to the European Automobile Manufacturers Association's 2025 data, BEV market share reached approximately 14% in 2024 and is growing toward the EU's 2035 effective ICE sales ban, the IRA-equivalent policy driver in the form of the EU Battery Regulation and Net Zero Industry Act is driving very large EV component manufacturing capacity investments, and Bosch's 2025 results confirming above-average e-Mobility growth illustrates the commercial momentum building in the European EV component supply chain.

1. Introduction

1.1. Market Definition

1.2. Market Ecosystem

1.3. Currency and Limitations

1.3.1. Currency

1.3.2. Limitations

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Data Collection & Validation Process

2.2.1. Secondary Research

2.2.2. Primary Research & Validation

2.2.2.1. Primary Interviews with Experts

2.2.2.2. Approaches for Country-/Region-Level Analysis

2.3. Market Estimation

2.3.1. Bottom-Up Approach

2.3.2. Top-Down Approach

2.3.3. Growth Forecast

2.4. Data Triangulation

2.5. Assumptions for the Study

3. Executive Summary

4. Market Overview

4.1. Introduction

4.2. Market Dynamics

4.2.1. Drivers

4.2.1.1. Rapid Adoption of Electric Vehicles Globally

4.2.1.2. Government Incentives and Emission Regulations

4.2.1.3. Declining Battery Costs

4.2.1.4. Advancements in EV Technology

4.2.2. Restraints

4.2.2.1. High Initial Cost of EV Components

4.2.2.2. Supply Chain Constraints (Lithium, Rare Earths)

4.2.2.3. Charging Infrastructure Limitations

4.2.3. Opportunities

4.2.3.1. Growth in Next-Generation Batteries (Solid-State)

4.2.3.2. Expansion of EV Production Capacity

4.2.3.3. Integration of Power Electronics and Software

4.2.3.4. Second-Life Battery Applications

4.2.4. Challenges

4.2.4.1. Standardization of Components

4.2.4.2. Thermal Management and Safety Issues

4.3. Technology Landscape

4.3.1. Battery Technologies (Li-ion, Solid-State)

4.3.2. Electric Drive Systems

4.3.3. Power Electronics (Inverters, Converters)

4.3.4. Thermal Management Systems

4.3.5. Vehicle Control and Software Platforms

4.4. EV Component Ecosystem

4.4.1. Raw Material Suppliers

4.4.2. Component Manufacturers

4.4.3. Tier-1 Suppliers

4.4.4. OEMs

4.4.5. Aftermarket and Service Providers

4.5. Value Chain Analysis

4.5.1. Raw Material Extraction (Lithium, Cobalt, Nickel)

4.5.2. Component Manufacturing

4.5.3. Vehicle Assembly

4.5.4. Distribution and Sales

4.5.5. Aftermarket Services

4.6. Regulatory and Standards Landscape

4.6.1. Emission and EV Regulations

4.6.2. Battery Safety Standards

4.6.3. Charging and Interoperability Standards

4.7. Porter's Five Forces Analysis

4.8. Investment and Industry Trends

4.8.1. Expansion of EV Manufacturing Facilities

4.8.2. Strategic Partnerships and Joint Ventures

4.8.3. Vertical Integration by OEMs

4.9. Cost and Pricing Analysis

4.9.1. Cost Breakdown of EV Components

4.9.2. Battery Cost Trends ($/kWh)

4.9.3. Cost Reduction Strategies

5. EV Components Market, by Component Type

5.1. Introduction

5.2. Battery Systems

5.2.1. Battery Cells

5.2.2. Battery Modules

5.2.3. Battery Packs

5.2.4. Battery Management Systems (BMS)

5.3. Electric Drive Systems

5.3.1. Electric Motors

5.3.2. Gearboxes/Transmission Systems

5.4. Power Electronics

5.4.1. Inverters

5.4.2. Converters

5.4.3. On-Board Chargers (OBC)

5.5. Thermal Management Systems

5.6. Charging Components

5.6.1. Charging Ports

5.6.2. Charging Controllers

5.7. Vehicle Control Units and Software

5.8. Other Components

6. EV Components Market, by Vehicle Type

6.1. Introduction

6.2. Passenger Vehicles

6.3. Commercial Vehicles

6.4. Two-Wheelers and Three-Wheelers

7. EV Components Market, by Propulsion Type

7.1. Introduction

7.2. Battery Electric Vehicles (BEVs)

7.3. Plug-in Hybrid Electric Vehicles (PHEVs)

7.4. Hybrid Electric Vehicles (HEVs)

8. EV Components Market, by Application

8.1. Introduction

8.2. Powertrain Systems

8.2.1. Traction Systems

8.2.2. Energy Storage Systems

8.3. Charging Infrastructure Integration

8.4. Thermal and Energy Management

8.5. Vehicle Electronics and Control Systems

8.6. Other Applications

9. EV Components Market, by End User

9.1. Introduction

9.2. OEMs

9.3. Tier-1 Suppliers

9.4. Aftermarket

10. EV Components Market, by Material Type

10.1. Introduction

10.2. Metals (Aluminum, Copper)

10.3. Plastics and Composites

10.4. Semiconductor Materials

11. EV Components Market, by Geography

11.1. Introduction

11.2. North America

11.2.1. U.S.

11.2.2. Canada

11.3. Europe

11.3.1. Germany

11.3.2. U.K.

11.3.3. France

11.3.4. Italy

11.3.5. Spain

11.3.6. Netherlands

11.3.7. Sweden

11.3.8. Norway

11.3.9. Rest of Europe

11.4. Asia-Pacific

11.4.1. China

11.4.2. India

11.4.3. Japan

11.4.4. South Korea

11.4.5. Australia

11.4.6. Indonesia

11.4.7. Thailand

11.4.8. Vietnam

11.4.9. Rest of Asia-Pacific

11.5. Latin America

11.5.1. Brazil

11.5.2. Mexico

11.5.3. Argentina

11.5.4. Chile

11.5.5. Colombia

11.5.6. Rest of Latin America

11.6. Middle East & Africa

11.6.1. UAE

11.6.2. Saudi Arabia

11.6.3. South Africa

11.6.4. Turkey

11.6.5. Egypt

11.6.6. Rest of Middle East & Africa

12. Competitive Landscape

12.1. Overview

12.2. Key Growth Strategies

12.3. Competitive Benchmarking

12.4. Competitive Dashboard

12.4.1. Industry Leaders

12.4.2. Market Differentiators

12.4.3. Vanguards

12.4.4. Emerging Companies

12.5. Market Ranking/Positioning Analysis of Key Players, 2025

13. Company Profiles

13.1. Robert Bosch GmbH

13.2. DENSO Corporation

13.3. Continental AG

13.4. BYD Company Ltd.

13.5. Contemporary Amperex Technology Co. Limited (CATL)

13.6. LG Energy Solution Ltd.

13.7. Panasonic Holdings Corporation

13.8. Samsung SDI Co., Ltd.

13.9. Valeo SA

13.10. ZF Friedrichshafen AG

13.11. Magna International Inc.

13.12. Hyundai Mobis Co., Ltd.

13.13. Aisin Corporation

13.14. Infineon Technologies AG

13.15. NXP Semiconductors N.V.

14. Appendix

14.1. Additional Customization

14.2. Related Reports

Published Date: Feb-2026

Published Date: Feb-2026

Published Date: Sep-2024

Published Date: Apr-2022

Subscribe to get the latest industry updates