Resources

About Us

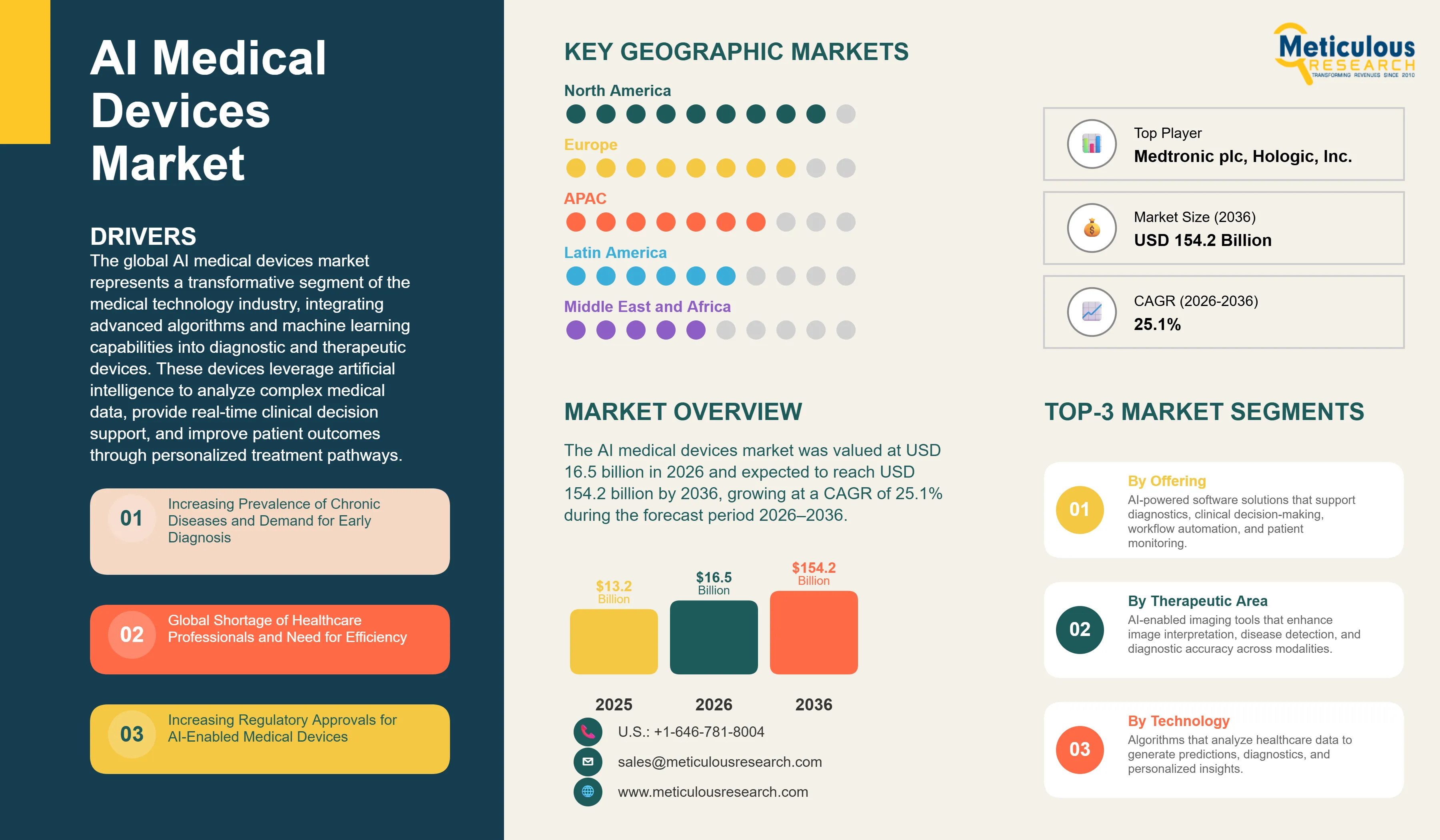

The global AI medical devices market was valued at USD 16.5 billion in 2026. This market is expected to reach USD 154.2 billion by 2036, growing at a CAGR of 25.1% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global AI medical devices market represents a transformative segment of the medical technology industry, integrating advanced algorithms and machine learning capabilities into diagnostic and therapeutic devices. These devices leverage artificial intelligence to analyze complex medical data, provide real-time clinical decision support, and improve patient outcomes through personalized treatment pathways. The market includes a wide range of applications, from AI-enabled imaging systems in radiology to wearable devices that monitor cardiac health. As healthcare systems globally face increasing pressure from rising chronic disease prevalence and professional shortages, AI medical devices have emerged as critical tools for enhancing diagnostic accuracy and operational efficiency.

The rapid growth of the market is primarily driven by the increasing volume of FDA-authorized AI-enabled devices. As of March 2026, the FDA database includes 1,451 AI-enabled medical devices, a significant increase from 1,250 in the previous year. This surge in regulatory approvals reflects the maturing of AI technologies and their successful integration into clinical workflows. Radiology remains the most dominant therapeutic area, accounting for approximately 76% of all AI-enabled clearances in 2025. The ability of AI to assist radiologists in identifying subtle anomalies in medical images, such as early-stage tumors or vascular issues, has made it an indispensable component of modern diagnostic imaging.

However, the market faces significant restraints, particularly regarding data privacy and the high cost of implementation. The integration of AI into medical devices requires the processing of vast amounts of sensitive patient data, raising concerns about security and ethical use. Furthermore, the high initial investment required for AI-integrated systems and the necessary training for healthcare professionals can be a barrier for smaller hospitals and diagnostic centers. Despite these challenges, the shift toward remote patient monitoring and the growth of digital health infrastructure in emerging markets provide substantial opportunities for market expansion. The integration of AI into cardiology and neurology is also expected to drive future growth, as new devices for real-time heart monitoring and brain activity analysis gain regulatory clearance.

The competitive landscape is characterized by intense innovation and strategic partnerships between medical device manufacturers and technology companies. Leading players like GE HealthCare, Siemens Healthineers, and Philips are increasingly collaborating with AI specialists and cloud providers to enhance their digital health offerings. The development of 'software as a medical device' (SaMD) is a key trend, allowing for more flexible and scalable AI applications that can be deployed across various hardware platforms. As the industry moves toward 2036, the focus is expected to shift toward generative AI and its potential to further personalize patient care and streamline clinical documentation.

The primary driver for the AI medical devices market is the increasing prevalence of chronic diseases and the growing need for early and accurate diagnosis. According to the World Health Organization, noncommunicable diseases (NCDs) account for approximately 43 million deaths annually, representing nearly 75% of all global deaths, with cardiovascular diseases, cancer, chronic respiratory diseases, and diabetes being the leading contributors. AI-enabled medical devices support earlier detection, risk stratification, and continuous monitoring of these conditions, enabling timely interventions and improved patient outcomes. Furthermore, the global burden of cardiovascular disease alone is responsible for approximately 17.9 million deaths each year, underscoring the need for advanced diagnostic technologies.

Another key driver is the global shortage of healthcare professionals. AI medical devices can assist in managing high patient volumes by prioritizing urgent cases and automating routine diagnostic tasks. This is particularly relevant in radiology and pathology, where the volume of medical images and samples is growing faster than the number of specialists. AI-driven triage systems can flag critical findings in real-time, ensuring that patients with life-threatening conditions receive immediate attention. This efficiency gain is essential for maintaining the quality of care in overburdened healthcare systems.

A major restraint is the concern regarding data privacy and cybersecurity. AI medical devices rely on large datasets of patient information to train and refine their algorithms. Protecting this data from unauthorized access and ensuring compliance with regulations such as GDPR and HIPAA is a significant challenge for manufacturers and healthcare providers. Any data breach could lead to severe legal and reputational consequences, as well as undermining patient trust in AI technologies. Additionally, the 'black box' nature of some AI algorithms, where the reasoning behind a decision is not transparent, remains a concern for clinicians and regulators.

The growth of remote patient monitoring and the integration of AI into wearable devices present significant opportunities. AI-enabled wearables can continuously track vital signs and provide early warnings for potential health issues, allowing for proactive care in a home setting. This is especially beneficial for managing chronic conditions and supporting aging populations. Furthermore, the expansion of healthcare infrastructure in emerging economies, particularly in Asia-Pacific and Latin America, provides a large untapped market for AI medical devices. Government initiatives to digitalize healthcare and improve access to advanced medical technology are expected to drive adoption in these regions.

Evolving regulatory guidelines for AI/ML-based software as a medical device (SaMD) remain a key challenge. Regulators like the FDA and EMA are continuously updating their frameworks to keep pace with rapid technological advancements. Manufacturers must navigate complex approval processes and demonstrate the safety, efficacy, and generalizability of their AI algorithms across diverse patient populations. Interoperability issues also pose a challenge, as AI tools must be seamlessly integrated with existing Electronic Health Records (EHR) and hospital information systems to be clinically effective.

Radiology continues to lead the AI medical device market, with a vast majority of clearances concentrated in diagnostic imaging. However, there is a growing trend toward multi-modal AI, which integrates data from various sources such as imaging, genomics, and clinical records to provide a more holistic view of patient health. This approach allows for more accurate diagnosis and personalized treatment planning, particularly in oncology and complex neurological disorders.

The adoption of cloud-based AI platforms is a significant trend, enabling healthcare providers to access advanced AI tools without the need for extensive on-site computing infrastructure. These platforms allow for the rapid deployment of AI applications and facilitate collaboration between healthcare institutions. Cloud integration also enables continuous updates to AI algorithms, ensuring that clinicians always have access to the latest diagnostic capabilities.

Based on therapeutic area, the market is segmented into Radiology, Cardiology, Neurology, Oncology, and others. In 2026, the radiology segment is expected to hold the largest share of the market. This dominance is due to the high volume of AI-enabled diagnostic imaging tools cleared by regulatory bodies and the widespread adoption of AI for image interpretation. AI algorithms are particularly effective at identifying patterns in X-rays, CT scans, and MRIs, improving the speed and accuracy of diagnosis.

Cardiology is projected to register the highest CAGR during the forecast period. This growth is driven by the increasing deployment of AI for real-time ECG analysis, heart failure prediction, and the monitoring of cardiac arrhythmias. The rise of AI-enabled wearable heart monitors and the growing burden of cardiovascular diseases globally are key factors supporting this segment's rapid expansion.

North America is expected to dominate the global AI medical devices market in 2026, primarily due to its advanced healthcare infrastructure and the high rate of FDA authorizations for AI-enabled devices. The U.S. is the leading hub for medical device innovation, with a high concentration of technology companies and research institutions. The Healthcare Foresights report valued the U.S. AI-enabled medical devices market at $5.58 billion in 2026, reflecting strong clinical adoption. The key companies operating in the North American market are GE HealthCare, Siemens Healthineers, Philips, Medtronic, and Abbott.

Asia-Pacific is projected to witness the fastest growth during the forecast period. This is driven by rapid digital transformation in healthcare, increasing investments in medical technology in China and India, and government initiatives to improve healthcare access. China's rapid adoption of AI in medical imaging and its growing manufacturing capabilities are major drivers for the region. The key companies operating in the Asia-Pacific market are Canon Medical Systems, Fujifilm Holdings, Terumo Corporation, and various emerging AI specialists in the region.

The market is projected to reach USD 154.2 billion by 2036, growing at a CAGR of 25.1% from 2026 to 2036.

The radiology segment is expected to hold the largest share in 2026, due to the high volume of AI-enabled diagnostic imaging tools.

The increasing prevalence of chronic diseases and the global shortage of healthcare professionals are the primary drivers.

Asia-Pacific is projected to witness the highest CAGR due to rapid digitalization and expanding healthcare infrastructure.

AI algorithms can identify subtle anomalies in medical images that may be missed by the human eye, improving screening and diagnosis.

Concerns regarding patient data privacy, cybersecurity, and the high initial cost of implementation are major restraints.

They allow for continuous remote monitoring of vital signs, providing early warnings and supporting proactive chronic disease management.

It allows for flexible and scalable AI applications that can be deployed across various hardware platforms and clinical settings.

Collaborations between medical device manufacturers and AI specialists are accelerating innovation and the development of digital health solutions.

Leading companies include GE HealthCare, Siemens Healthineers, Philips, Medtronic, and Abbott.

1. Introduction

1.1. Market Definition

1.2. Market Scope

1.3. Currency and Pricing

2. Research Methodology

2.1. Research Process

2.2. Data Collection & Sources

2.2.1. Primary Research

2.2.2. Secondary Research

2.3. Market Sizing & Forecasting

2.3.1. Bottom-up Approach

2.3.2. Top-down Approach

2.4. Data Triangulation & Validation

2.5. Assumptions & Limitations

3. Executive Summary

3.1. Market Overview

3.2. Segmental Analysis

3.3. Geographic Outlook

3.4. Competitive Insights

4. Market Insights

4.1. Introduction

4.2. Market Dynamics

4.2.1. Drivers

4.2.1.1. Increasing Prevalence of Chronic Diseases and Demand for Early Diagnosis

4.2.1.2. Global Shortage of Healthcare Professionals and Need for Efficiency

4.2.2. Restraints

4.2.2.1. Data Privacy Concerns and Cybersecurity Risks

4.2.2.2. High Initial Implementation and Training Costs

4.2.3. Opportunities

4.2.3.1. Growth of Remote Patient Monitoring and AI-Enabled Wearables

4.2.3.2. Expansion of Healthcare Infrastructure in Emerging Markets

4.2.4. Challenges

4.2.4.1. Evolving Regulatory Frameworks for AI/ML-Based SaMD

4.2.4.2. Interoperability and Integration with Existing Clinical Workflows

4.3. Porter’s Five Forces Analysis

4.4. Regulatory Landscape

4.5. Value Chain Analysis

5. Global AI Medical Devices Market Assessment, by Offering

5.1. Introduction

5.2. Software (SaMD)

5.3. Hardware (AI-Integrated Devices)

5.4. Services

6. Global AI Medical Devices Market Assessment, by Therapeutic Area

6.1. Introduction

6.2. Radiology

6.3. Cardiology

6.4. Neurology

6.5. Oncology

6.6. Others

7. Global AI Medical Devices Market Assessment, by Technology

7.1. Introduction

7.2. Machine Learning

7.3. Natural Language Processing

7.4. Computer Vision

8. Global AI Medical Devices Market Assessment, by End User

8.1. Introduction

8.2. Hospitals & Clinics

8.3. Diagnostic Centers

8.4. Pharmaceutical & Biotechnology Companies

8.5. Academic & Research Institutions

9. Global AI Medical Devices Market Assessment, by Geography

9.1. Introduction

9.2. North America

9.2.1. U.S.

9.2.2. Canada

9.3. Europe

9.3.1. Germany

9.3.2. UK

9.3.3. France

9.3.4. Italy

9.3.5. Spain

9.3.6. Rest of Europe

9.4. Asia-Pacific

9.4.1. China

9.4.2. India

9.4.3. Japan

9.4.4. Singapore

9.4.5. Australia

9.4.6. South Korea

9.4.7. Rest of Asia-Pacific

9.5. Latin America

9.5.1. Brazil

9.5.2. Mexico

9.5.3. Rest of Latin America

9.6. Middle East & Africa

9.6.1. UAE

9.6.2. Saudi Arabia

9.6.3. South Africa

9.6.4. Rest of MEA

10. Competitive Landscape

10.1. Introduction

10.2. Market Share Analysis

10.3. Competitive Benchmarking

10.4. Strategic Developments

10.4.1. Product Launches & Enhancements

10.4.2. Partnerships & Collaborations

10.4.3. Mergers & Acquisitions

11. Company Profiles (Active Manufacturers Only)

11.1. GE HealthCare Technologies Inc.

11.2. Siemens Healthineers AG

11.3. Koninklijke Philips N.V.

11.4. Medtronic plc

11.5. Abbott Laboratories

11.6. Johnson & Johnson

11.7. Stryker Corporation

11.8. Boston Scientific Corporation

11.9. Canon Medical Systems Corporation

11.10. Fujifilm Holdings Corporation

11.11. Hologic, Inc.

11.12. Terumo Corporation

11.13. Smith & Nephew plc

11.14. Roche Holding AG

11.15. NVIDIA Corporation

11.16. Aidoc Medical Ltd.

11.17. Viz.ai, Inc.

11.18. Arterys Inc. (Tempus)

11.19. Zebra Medical Vision (Nanox)

11.20. Butterfly Network, Inc.

12. Appendix

Published Date: Jul-2026

Published Date: Jun-2026

Published Date: Jun-2026

Published Date: Apr-2026

Published Date: Feb-2026

Subscribe to get the latest industry updates