Resources

About Us

Connected Medical Devices Market Size, Share & Trends Analysis by Type, Deployment Mode, Component, End User, and Geography - Global Opportunity Analysis and Industry Forecast (2026-2036)

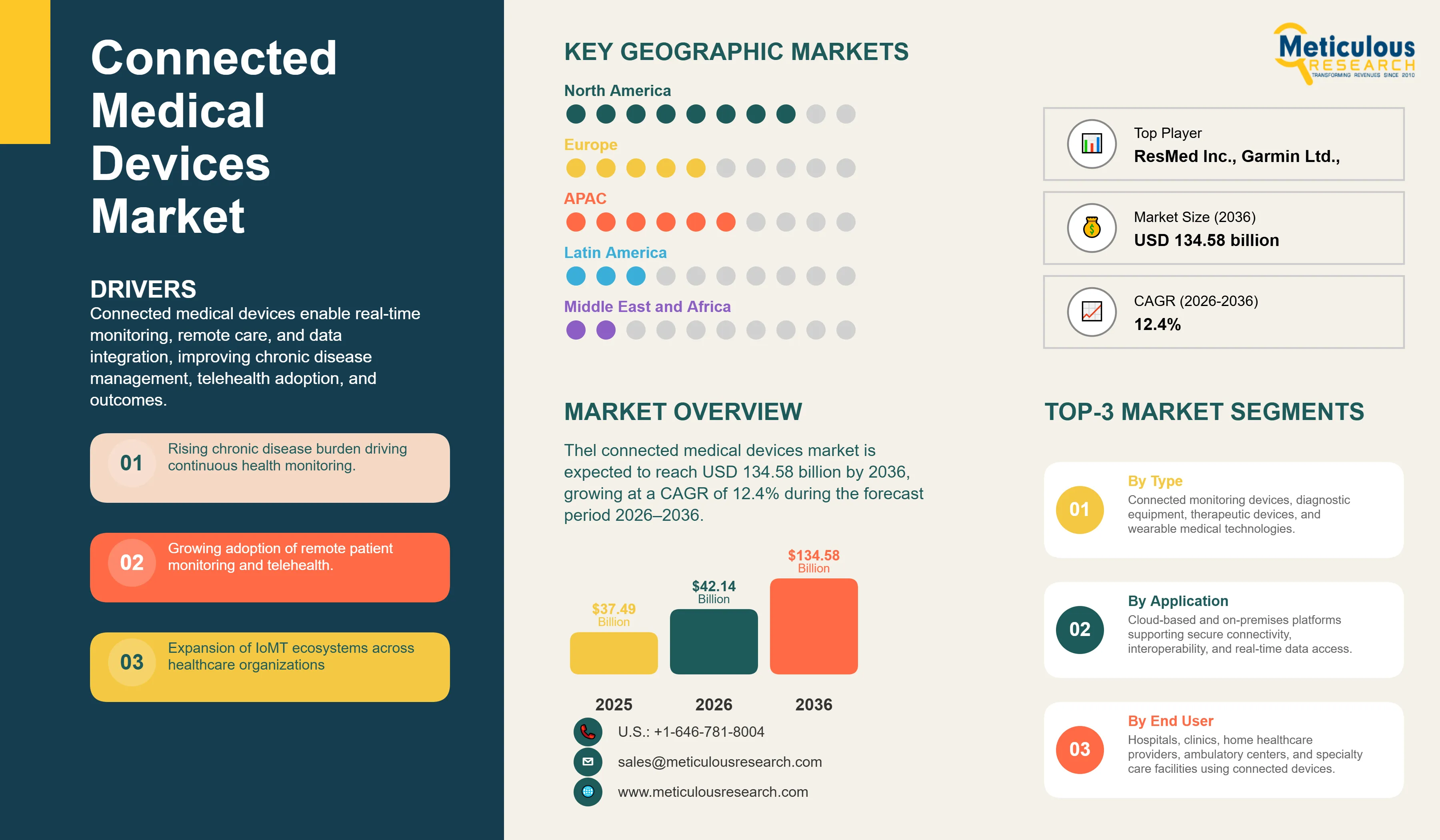

Report ID: MRHC - 1042044 Pages: 275 Jun-2026 Formats*: PDF Category: Healthcare Delivery: 24 to 72 Hours Download Free Sample ReportThe global connected medical devices market was valued at USD 42.14 billion in 2026. This market is expected to reach USD 134.58 billion by 2036, growing at a CAGR of 12.4% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global connected medical devices market is a cornerstone of the Internet of Medical Things (IoMT) revolution, providing the essential infrastructure for continuous, data-driven patient monitoring and clinical intervention. Connected medical devices, including wearable sensors, smart infusion pumps, and connected diagnostic equipment, enable healthcare providers to aggregate real-time data from various clinical and home settings into a unified patient record. As of 2026, the market is undergoing a significant transformation, driven by the global imperative to address the rising prevalence of chronic diseases and the increasing demand for remote patient monitoring (RPM) and telehealth services.

The transition toward integrated and cloud-native connected device ecosystems is essential for improving clinical productivity and patient outcomes in modern healthcare. Modern connected medical devices leverage advanced sensors and AI-driven tools to provide clinicians with actionable insights, facilitating more accurate diagnoses and personalized treatment planning. Furthermore, the integration of connected devices with Electronic Health Records (EHRs) and hospital information systems ensures that stakeholders have immediate access to a comprehensive view of the patient's health status. As healthcare systems transition toward value-based care models, the demand for connected device solutions that can demonstrate improved clinical outcomes and reduced hospital readmissions is expected to surge.

Drivers: Expanding the Care Continuum with Integrated Connected Medical Devices and IoT

The primary driver for the connected medical devices market is the increasing global burden of chronic diseases, which requires continuous monitoring and more efficient patient management. According to the World Health Organization (WHO), noncommunicable diseases account for approximately 74% of all deaths globally. The rising prevalence of diabetes, cardiovascular diseases, respiratory disorders, and hypertension is accelerating the adoption of connected medical devices that enable real-time monitoring and timely clinical intervention. In addition, the ongoing shift toward digital health and the growing demand for remote patient monitoring (RPM) are supporting market growth. Government initiatives promoting digital healthcare and interoperability are further encouraging healthcare providers to invest in connected medical devices that can seamlessly integrate with broader healthcare information systems.

Restraints: Data Privacy Concerns and Technical Integration Challenges

Market growth is restrained by the high cost of implementing comprehensive connected device solutions and the technical challenges of achieving seamless data interoperability across disparate device platforms and legacy IT systems. For many healthcare organizations, the initial capital investment and ongoing maintenance costs of a connected device fleet can be a significant barrier. Additionally, the lack of standardized data protocols between different device manufacturers often leads to data silos, making it difficult to achieve a truly unified patient record. Concerns regarding data privacy and cybersecurity in centralized information hubs also act as deterrents to market expansion. Furthermore, the significant organizational change management and specialized training required for successful connected device implementation can lead to slower adoption rates.

Opportunities: Advancing AI-Driven Device Analytics and Cloud-Native Platforms

The integration of artificial intelligence (AI) and machine learning (ML) into connected medical device platforms offers substantial growth opportunities. AI-powered tools can analyze complex physiological data and clinical evidence to identify subtle anomalies, facilitating more precise diagnosis and treatment planning. By 2026, AI-driven predictive analytics are being used to forecast the risk of acute medical events, enabling proactive intervention and improving patient safety. Furthermore, the shift toward cloud-native (SaaS) connected device platforms provides healthcare organizations with superior scalability, flexibility, and lower upfront costs. Cloud-based solutions also facilitate real-time data sharing among diverse clinical specialists, supporting multi-disciplinary collaboration, which is particularly beneficial for regional healthcare networks.

Evolution toward Holistic and AI-Powered Patient Care Orchestration

Connected medical devices are increasingly evolving from standalone monitoring tools into AI-enabled patient care ecosystems that integrate data from wearables, diagnostic equipment, and electronic health records. According to the World Health Organization (WHO), noncommunicable diseases account for approximately 74% of global deaths, creating a growing need for continuous and proactive patient management. In addition, the U.S. FDA has authorized more than 1,000 AI-enabled medical devices as of 2025, highlighting the increasing adoption of AI-driven clinical decision support and automation. This trend is accelerating the shift toward enterprise-wide patient management aimed at improving clinical outcomes and operational efficiency.

Integration of Advanced Sensors and Edge Computing in Medical Devices

The integration of advanced sensors and edge computing is enabling connected medical devices to process data in real time and support faster clinical interventions. According to the Consumer Technology Association (CTA), global shipments of wearable technologies continue to expand as demand for continuous health monitoring increases. Furthermore, the proliferation of 5G networks and advancements in low-power semiconductor technologies are supporting the deployment of edge-enabled medical devices capable of performing on-device analytics, reducing latency, and enhancing patient safety in critical care and remote monitoring applications.

Analysis by Type

Based on type, the consumer medical devices segment is expected to hold the largest share in 2026. This dominance is driven by the increasing consumer focus on wellness management and home-based monitoring. The clinical remote patient monitoring (RPM) devices segment is projected to register the highest CAGR, reflecting the increasing demand for structured interpretation and AI-driven documentation to improve clinical productivity and regulatory compliance. Hospital-grade connected devices remain a critical segment, providing the high-precision data necessary for clinical decision-making.

Analysis by Deployment Mode

Based on deployment mode, the cloud-based segment is expected to account for the largest share in 2026. The advantages of cloud deployment, such as scalability, reduced IT burden, and ease of real-time data sharing among global clinical teams, make it highly attractive to healthcare organizations. Approximately 78% of new connected device installations in 2026 are opting for SaaS models. The on-premises segment continues to serve large organizations with specific data sovereignty requirements and those with significant existing IT infrastructure.

North America is expected to dominate the global connected medical devices market in 2026, accounting for an estimated 43.5% of total revenue. The region's leadership is driven by the widespread adoption of remote patient monitoring technologies, a well-established healthcare infrastructure, and strong investments in digital health. According to the U.S. Centers for Disease Control and Prevention (CDC), six in ten adults in the U.S. have at least one chronic disease, increasing the demand for continuous monitoring solutions. Favorable reimbursement policies, growing utilization of home healthcare, and the presence of leading manufacturers such as Medtronic, Abbott, GE HealthCare, and Philips further support market growth across the U.S. and Canada.

Asia Pacific is projected to register the fastest growth during the forecast period. Rising incidences of diabetes and cardiovascular diseases, expanding healthcare expenditures, and government-led digital health initiatives are accelerating the adoption of connected medical devices across China, India, and Japan. According to the International Diabetes Federation (IDF), the Western Pacific region accounts for more than 215 million adults living with diabetes, creating substantial demand for continuous glucose monitoring and remote patient monitoring solutions. Increasing penetration of wearable technologies, improving internet connectivity, and the expansion of home-based care are expected to create significant opportunities for both global and regional market participants.

The competitive landscape of the global connected medical devices market is characterized by intense innovation and strategic consolidations as vendors seek to provide end-to-end patient care orchestration platforms. Leading players are differentiating themselves through the sophistication of their AI engines and their ability to provide seamless integration with EHRs and other clinical management platforms. Strategic acquisitions of niche sensor and analytics companies are a common trend as vendors seek to enhance their diagnostic capabilities. The market is also seeing increased collaboration between connected device vendors and healthcare providers to ensure seamless patient monitoring across the care continuum.

Key players operating in the global connected medical devices market include Medtronic plc (Ireland), GE HealthCare Technologies Inc. (U.S.), Koninklijke Philips N.V. (Netherlands), Abbott Laboratories (U.S.), Johnson & Johnson Services, Inc. (U.S.), Boston Scientific Corporation (U.S.), Baxter International Inc. (U.S.), F. Hoffmann-La Roche Ltd (Switzerland), Garmin Ltd. (Switzerland), and various emerging technology providers specializing in wearable sensors and AI-driven diagnostic tools.

The market is projected to reach USD 134.58 billion by 2036, growing at a CAGR of 12.4% from 2026 to 2036.

What are the primary operational outcomes for hospitals using integrated connected device solutions?

Hospitals report a significant reduction in hospital readmissions and an improvement in the accuracy of patient monitoring.

The connected wearable devices segment is expected to register the fastest growth through 2036, driven by increasing consumer adoption of smartwatches and wearable biosensors, rising demand for continuous health monitoring, and the growing prevalence of chronic diseases. Advances in sensor technologies, AI-enabled analytics, and the expansion of remote patient monitoring programs are further supporting the rapid adoption of connected wearable devices.

Around 70% of new deployments are cloud-native, enabling real-time data sharing and scalability.

North America holds the largest share, estimated at 43.5% in 2026, driven by high IoT adoption and mature IT infrastructure.

AI enables the prediction of acute medical events and automates routine data curation, improving diagnostic consistency and patient safety.

The surge in patient volume is driving the demand for integrated connected device platforms to manage the high volume of physiological data.

Hospitals and clinics are the primary adopters, managing the highest volumes of patient data and connected device fleets.

These systems provide the continuous, data-driven patient management necessary to improve clinical outcomes and reduce the total cost of care.

The top 5 players are Medtronic plc, GE HealthCare Technologies Inc., Koninklijke Philips N.V., Abbott Laboratories, and Johnson & Johnson.

Published Date: Jul-2026

Published Date: Jun-2026

Published Date: Apr-2026

Published Date: Feb-2026

Published Date: Feb-2026

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates