Resources

About Us

Medical Device Reprocessing Market Size, Share, Trends & Forecast Analysis by Device Type (Cardiovascular, Gastroenterology & Endoscopy), Type of Reprocessing (Single-use, Reusable), Reprocessor Type, Processing Stage, Application, End User, and Geography - Global Forecast to 2036

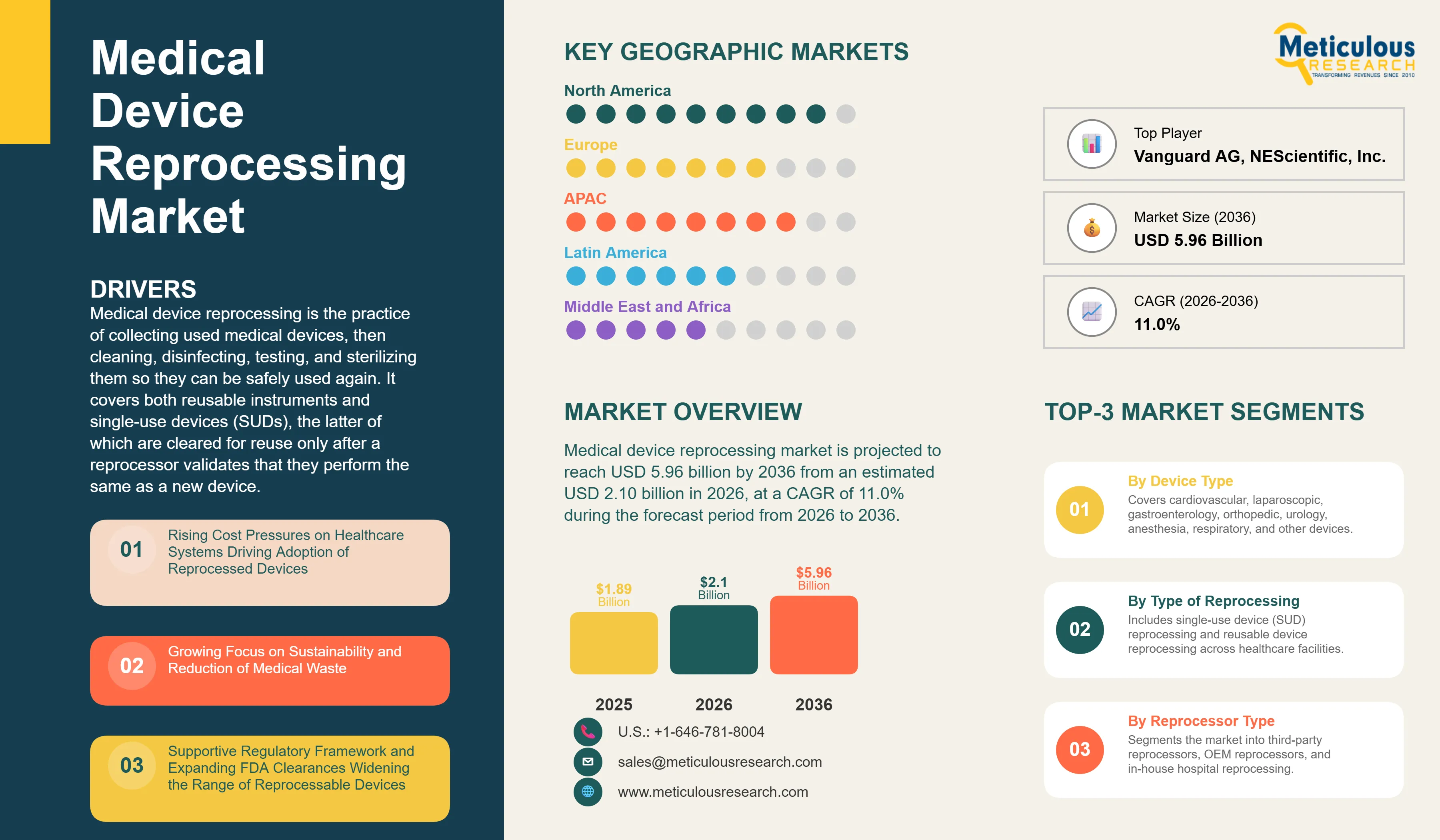

Report ID: MRHC - 1042102 Pages: 251 Jul-2026 Formats*: PDF Category: Healthcare Delivery: 24 to 72 Hours Download Free Sample ReportThe global medical device reprocessing market is projected to reach USD 5.96 billion by 2036 from an estimated USD 2.10 billion in 2026, at a CAGR of 11.0% during the forecast period from 2026 to 2036.

Click here to: Get Free Sample Pages

Click here to: Get Free Sample Pages

Medical device reprocessing is the practice of collecting used medical devices, then cleaning, disinfecting, testing, and sterilizing them so they can be safely used again. It covers both reusable instruments and single-use devices (SUDs), the latter of which are cleared for reuse only after a reprocessor validates that they perform the same as a new device. Reprocessing is carried out by specialist third-party companies, by original manufacturers, and, in some cases, within the hospital itself. The result is a cheaper, lower-waste alternative to buying new devices for every procedure.

Reprocessed single-use devices typically cost around half the price of new equivalents, and for expensive items such as cardiac catheters, electrophysiology tools, and ultrasound probes, the savings per case are substantial. Stryker, one of the largest reprocessors, reported that its programs saved customers close to USD 239 million in 2025 while serving roughly 3,773 healthcare facilities. With hospital margins under strain, this kind of saving is hard to ignore, and it explains why adoption keeps climbing.

Sustainability has become the second big reason. Healthcare is a large source of waste and greenhouse gas emissions, and reprocessing directly cuts both. In 2025, Stryker's programs kept about 5 million pounds of used devices out of landfills. Many hospitals have pledged to reduce emissions in line with wider climate targets, and reprocessing gives them a practical way to make progress without changing clinical care. Groups such as the Association of Medical Device Reprocessors and the National Academy of Medicine have pointed to reprocessing as a proven way to lower cost, waste, and emissions at the same time.

Regulation ties the two together. In the United States, the FDA holds reprocessors to the same standards as original manufacturers, requiring clearance before a reprocessed single-use device can be sold. That oversight has built trust among clinicians and steadily grown the list of devices approved for reuse. As new clearances arrive, cost pressure persists, and sustainability goals firm up, the medical device reprocessing market is set for strong growth over the coming decade.

Medical Device Reprocessing Market: Insights from Industry Leaders

"A few years ago, hospitals mainly asked us how much they could save. Today, the conversation starts with compliance, traceability, and sustainability. Cost savings are still important, but customers want complete confidence that every reprocessed device meets the same performance and safety standards as a new one."

– Vice President, Medical Device Reprocessing Company

"The biggest opportunity isn't just expanding the number of devices we can reprocess. It's helping hospitals integrate reprocessing into their procurement strategy so it becomes a routine part of supply chain planning rather than a standalone sustainability initiative."

– Commercial Director, Medical Device Reprocessing Provider

"Our goal isn't simply to reduce supply costs. We need solutions that help us manage budgets without asking clinicians to compromise on performance or patient safety. That's why we only adopt reprocessed devices when the clinical evidence and regulatory oversight are well established."

– Director of Supply Chain, Multi-Hospital Health System

Rising Cost Pressures on Healthcare Systems

The strongest force behind the market is the need for hospitals to spend less. Supply costs are one of the largest line items in a hospital budget, and reprocessed single-use devices offer an immediate way to trim them. Because a reprocessed device usually costs about half of a new one, facilities can lower procedure costs without asking clinicians to change how they work.

The numbers add up quickly in high-volume, high-cost areas. Catheters, guidewires, and electrophysiology devices are used in large quantities and carry steep price tags when bought new, so reusing them frees up meaningful budget. Stryker has noted that over a recent five-year span, it helped nearly 50 integrated delivery networks save more than USD 1 million each per year in supply chain costs. For finance and procurement teams under pressure, results like these make reprocessing an easy business case to approve.

This financial logic holds across almost every care setting, from large academic hospitals to smaller community facilities and surgery centers. As long as healthcare budgets stay tight and device prices keep rising, demand for reprocessed devices will keep expanding, which places cost savings at the center of the growth of this market.

Growing Focus on Sustainability and Reduction of Medical Waste

A second, fast-strengthening driver is the push to make healthcare greener. Hospitals generate a great deal of waste, and disposable devices are a large part of it. Reprocessing offers a direct way to shrink that footprint by giving devices a second life instead of sending them to a landfill after a single use.

The impact is measurable. Reprocessing programs run by companies such as Stryker and Cardinal Health keep millions of pounds of used devices out of landfills each year and cut the greenhouse gas emissions tied to making new products. Many health systems have committed to cutting emissions sharply by 2030 and reaching net zero by mid-century, and reprocessing helps them move toward those pledges while keeping patient care unchanged. Cardinal Health, for example, announced plans in 2026 to open a new reprocessing facility in Australia to expand its remanufacturing capacity.

Because sustainability targets are now written into procurement decisions at many hospitals, reprocessing has shifted from a nice-to-have to a standard part of supply strategy. This alignment between cost savings and environmental goals gives the driver real staying power over the forecast period.

Supportive Regulatory Framework and Expanding FDA Clearances

Clear regulation has been essential to building confidence in reprocessed devices, and it continues to widen the market. In the United States, the FDA treats reprocessors of single-use devices as manufacturers and requires them to prove, through data, that a reprocessed device is as safe and effective as a new one before it can be sold. This oversight reassures clinicians and hospitals that reused devices meet a high bar.

The pace of new clearances keeps opening up fresh device categories. Innovative Health, a reprocessor focused on cardiology and electrophysiology, received its 50th FDA clearance in January 2026, adding another widely used cardiac device to the list of items hospitals can reuse. Each new clearance turns a device that once had to be discarded into a source of savings, and it expands the addressable pool for reprocessors.

As the FDA framework matures and clearances accumulate, the range of reprocessable devices grows well beyond the catheters and compression sleeves of earlier years to include complex electrophysiology, surgical, and diagnostic tools. This steady expansion of what can be reprocessed is a dependable source of long-term market growth.

Expansion into Ambulatory Surgical Centers and International Markets

One of the clearest opportunities lies in taking reprocessing beyond large hospitals into ambulatory surgical centers and markets outside North America. As more surgery moves to outpatient settings, these centers face the same cost pressure as hospitals but often lack the scale to absorb high device prices, which makes reprocessed devices an attractive option.

Ambulatory surgical centers are already the fastest-growing customer group for reprocessing. Their focus on efficiency and tight per-case economics fits well with a service that lowers device cost without disrupting clinical routines. Reprocessors are tailoring their programs to suit smaller sites, offering simpler logistics and predictable savings that work for lower procedure volumes.

International markets add a second layer of growth. Adoption has historically been strongest in the United States, where the FDA framework is well established, but interest is rising across Europe, Asia-Pacific, Latin America, and the Middle East. Cardinal Health's planned facility in Australia is one sign of this shift. As other countries build clearer rules for reprocessing and cost and sustainability pressures spread, large new markets are opening up, giving reprocessors room to grow well beyond their home base.

By Device Type: Cardiovascular Devices Lead the Market in 2026

By device type, the market spans cardiovascular, general and laparoscopic surgery, gastroenterology and endoscopy, orthopedic, urology, anesthesia and respiratory, and other devices. Cardiovascular devices hold the largest share of revenue in 2026, at close to 38%. Hospitals reprocess large numbers of catheters, guidewires, and electrophysiology tools, and because these carry high prices when bought new, the savings from reusing them are significant. The concentration of expensive single-use devices in cardiac and EP labs keeps this segment in front.

Gastroenterology and endoscopy devices are set to grow the quickest through 2036. Rising numbers of endoscopic procedures, together with the high cost of scopes and their accessories, are pushing facilities to reprocess more of these tools, both to save money and to reduce the waste that comes with disposables.

By Type of Reprocessing: Single-use Device Reprocessing Leads the Market in 2026

Split by type of reprocessing, the market covers single-use device (SUD) reprocessing and reusable device reprocessing. SUD reprocessing takes the larger share in 2026, at roughly 72%. This is where the money is: reusing costly disposables that were designed to be thrown away after one use delivers the clearest savings, and it is the area where FDA clearances and reprocessor investment have been concentrated.

Reusable device reprocessing is expected to expand at a faster pace over the forecast period. Closer scrutiny of how flexible endoscopes and surgical instruments are cleaned, along with a move by some hospitals to bring sterile processing back in-house, is lifting demand for validated reprocessing of reusable devices.

By Reprocessor Type: Third-party Reprocessors Lead the Market in 2026

By reprocessor type, the market includes third-party reprocessors, original equipment manufacturer (OEM) reprocessors, and in-house or hospital reprocessing. Third-party reprocessors hold the largest share in 2026, at about 64%. Established, FDA-cleared specialists such as Stryker Sustainability Solutions, Cardinal Health, and Innovative Health run the collection, cleaning, testing, and sterilization at scale, and hospitals rely on them for consistent quality and documented savings.

OEM reprocessors are projected to grow the fastest. As original manufacturers acquire reprocessing firms and build their own programs, they are able to offer customers a full lifecycle service for the devices they make, which is helping this group gain ground.

By Processing Stage: Sterilization Leads the Market in 2026

Looked at by processing stage, the market runs from collection and sorting through cleaning and disinfection, sterilization, functional testing and verification, and packaging and distribution. Sterilization holds the largest share in 2026, at roughly 33%. It is the step that makes a used device safe to reuse, it demands validated equipment and tight controls, and it carries much of the value in the reprocessing chain.

Functional testing and verification is expected to grow the fastest. As reprocessors handle more complex devices and as buyers ask for firmer proof of quality, the effort spent confirming that each device works exactly as it should is rising, which lifts this stage.

By Application: Cardiology Leads the Market in 2026

By application, the market covers cardiology, general surgery, gastroenterology, orthopedics, urology, and other areas. Cardiology holds the largest share in 2026, at about 36%. Cath labs and electrophysiology labs use a high volume of expensive single-use devices, so reprocessing them produces some of the biggest per-case savings in the hospital, which keeps cardiology in the lead.

Gastroenterology is projected to grow the fastest through 2036. Growing procedure volumes and the steep cost of endoscopic tools are prompting more GI departments to fold reprocessed devices into everyday practice.

By End User: Hospitals Lead the Market in 2026

By end user, the market is split among hospitals, ambulatory surgical centers, specialty clinics, and others. Hospitals hold the largest share in 2026, at close to 68%. They carry out the bulk of complex procedures, buy the most single-use devices, and have the scale and purchasing teams to run structured reprocessing programs, so they account for most of the demand.

Ambulatory surgical centers are expected to grow the fastest. As more procedures shift to outpatient sites and those centers look for ways to control per-case costs, they are adopting reprocessed devices at a quick pace, making them the highest-growth setting.

North America Leads the Market in 2026

By region, the market is split across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. North America holds the largest share in 2026, at roughly 52%.

North America's lead rests on a well-established FDA framework, high procedure volumes, and steady pressure on providers to reduce supply costs. The United States is the dominant national market, home to the leading reprocessors, including Stryker Sustainability Solutions, Johnson & Johnson (SterilMed), Cardinal Health, and Innovative Health, and supported by wide clinician acceptance of FDA-cleared reprocessed devices.

Asia-Pacific is expected to record the fastest growth over the forecast period. Rising healthcare spending, growing procedure volumes, and a stronger focus on cost control across China, India, and Japan are lifting interest in reprocessing, and new facilities in the region point to expanding capacity. Europe remains an important market, led by Germany, where government backing and hospital sustainability efforts support steady adoption.

Leading companies in the market have grown through new facility openings, acquisitions, fresh FDA clearances, and moves into new regions. Adding reprocessable device categories and expanding capacity have been the most common ways players strengthen their position, alongside acquisitions that bring reprocessing expertise in-house.

Prominent companies active in the global medical device reprocessing market include Stryker Corporation (through Stryker Sustainability Solutions) (U.S.), Johnson & Johnson (through SterilMed, Inc.) (U.S.), Medline Industries, LP (Medline ReNewal) (U.S.), Cardinal Health, Inc. (Sustainable Technologies) (U.S.), Arjo AB (Sweden), Innovative Health, LLC (U.S.), Vanguard AG (Germany), NEScientific, Inc. (U.S.), SureTek Medical (U.S.), ReNu Medical, Inc. (U.S.), Hogy Medical Co., Ltd. (Japan), STERIS plc (U.S.), Getinge AB (Sweden), SteriPro Canada Inc. (Canada), and Centurion Medical Products Corporation (U.S.).

|

Particulars |

Details |

|

Forecast Period |

2026 to 2036 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

CAGR (Value) |

11.0% |

|

Market Size (Value) in 2026 |

USD 2.10 Billion |

|

Market Size (Value) in 2036 |

USD 5.96 Billion |

|

Segments Covered |

By Device Type - Cardiovascular Devices - General & Laparoscopic Surgery Devices - Gastroenterology & Endoscopy Devices - Orthopedic, Urology, Anesthesia & Respiratory, Others By Type of Reprocessing - Single-use Device (SUD) Reprocessing - Reusable Device Reprocessing By Reprocessor Type - Third-party Reprocessors - OEM Reprocessors - In-house/Hospital Reprocessing By Processing Stage - Collection & Sorting, Cleaning & Disinfection, Sterilization, Testing & Verification, Packaging & Distribution By Application - Cardiology, General Surgery, Gastroenterology, Orthopedics, Urology, Others By End User - Hospitals - Ambulatory Surgical Centers - Specialty Clinics - Others |

|

Countries Covered |

North America (U.S., Canada), Europe (Germany, U.K., France, Italy, Spain, and Rest of Europe), Asia-Pacific (Japan, China, India, South Korea, Australia, and Rest of Asia-Pacific), Latin America (Brazil, Mexico, and Rest of Latin America), and the Middle East & Africa (Saudi Arabia, UAE, South Africa, and Rest of Middle East & Africa) |

|

Key Companies |

Stryker Corporation (Stryker Sustainability Solutions) (U.S.), Johnson & Johnson (SterilMed, Inc.) (U.S.), Medline Industries, LP (Medline ReNewal) (U.S.), Cardinal Health, Inc. (Sustainable Technologies) (U.S.), Arjo AB (Sweden), Innovative Health, LLC (U.S.), Vanguard AG (Germany), SureTek Medical (U.S.), ReNu Medical, Inc. (U.S.), Hogy Medical Co., Ltd. (Japan), STERIS plc (U.S.), Getinge AB (Sweden), SteriPro Canada Inc. (Canada), MATACHANA Group (Spain), and REMA System GmbH (Germany). |

The global medical device reprocessing market size is estimated at USD 2.10 billion in 2026.

The market is projected to grow from USD 2.10 billion in 2026 to USD 5.96 billion by 2036, at a CAGR of 11.0%.

The medical device reprocessing market is projected to reach USD 5.96 billion by 2036, at a compound annual growth rate (CAGR) of 11.0% from 2026 to 2036.

Key companies in this market include Stryker Corporation (Stryker Sustainability Solutions) (U.S.), Johnson & Johnson (SterilMed, Inc.) (U.S.), Medline Industries, LP (Medline ReNewal) (U.S.), Cardinal Health, Inc. (Sustainable Technologies) (U.S.), Arjo AB (Sweden), Innovative Health, LLC (U.S.), Vanguard AG (Germany), SureTek Medical (U.S.), ReNu Medical, Inc. (U.S.), Hogy Medical Co., Ltd. (Japan), STERIS plc (U.S.), Getinge AB (Sweden), SteriPro Canada Inc. (Canada), MATACHANA Group (Spain), and REMA System GmbH (Germany) among others.

The entry of original manufacturers into reprocessing through acquisitions, and the growing use of device tracking and program management tools to improve savings, are prominent trends in the market.

In 2026, cardiovascular devices lead by device type, single-use device reprocessing leads by type, third-party reprocessors lead by reprocessor type, sterilization leads by processing stage, cardiology leads by application, hospitals lead by end user, and North America leads by region. Gastroenterology and endoscopy devices, along with ambulatory surgical centers, are expected to grow the fastest.

North America holds the largest share of the market in 2026, supported by a mature FDA framework and strong cost pressure on providers. Asia-Pacific is expected to record the highest growth rate over the forecast period as awareness and regulation develop.

Key drivers include rising cost pressures on healthcare systems, a growing focus on sustainability and medical waste reduction, and a supportive regulatory framework with expanding FDA clearances. Together, these are lifting adoption of reprocessed devices across care settings.

Published Date: Jun-2026

Published Date: Jun-2026

Published Date: Apr-2026

Published Date: Feb-2026

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates