Resources

About Us

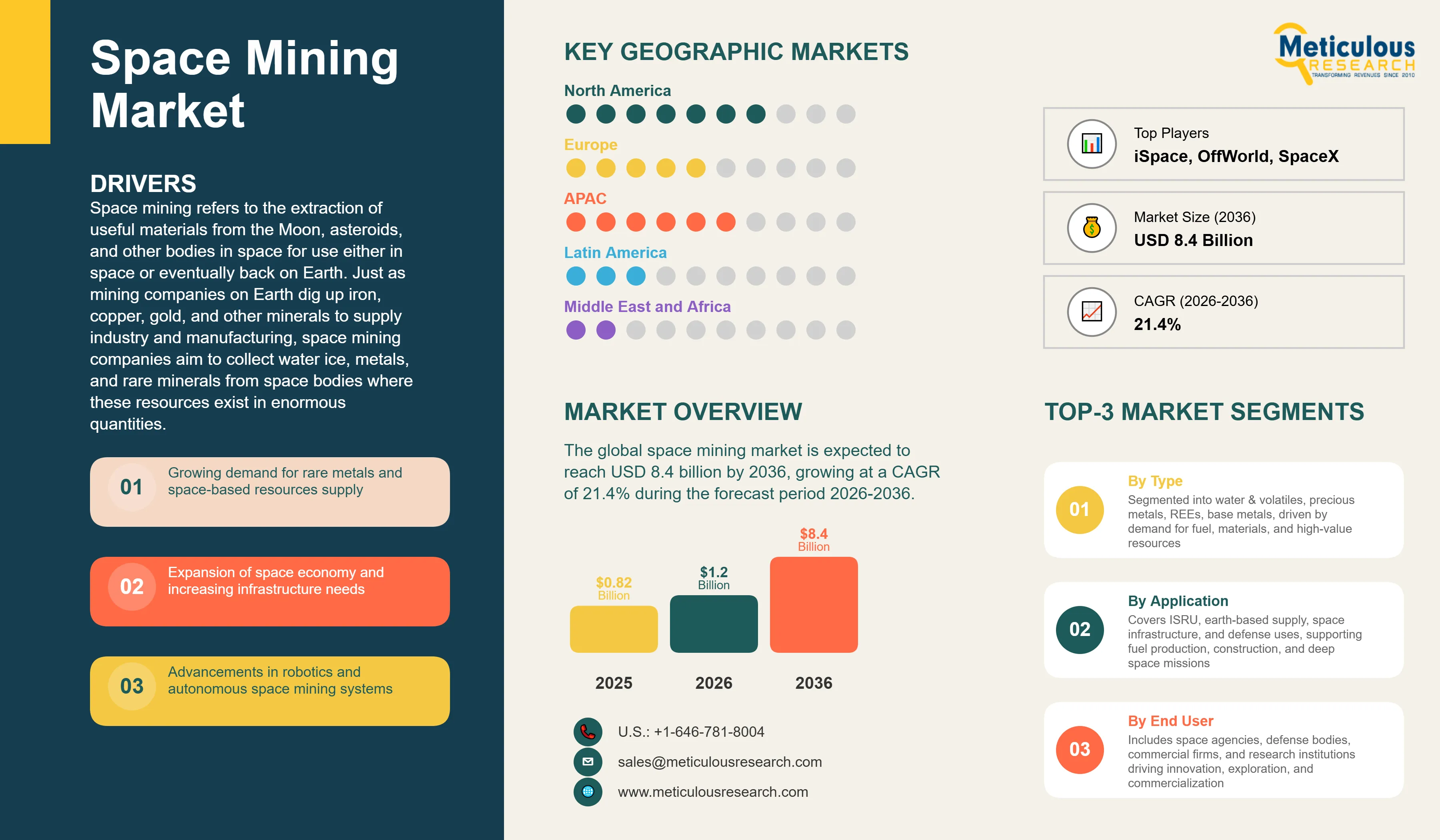

The global space mining market was valued at USD 0.82 billion in 2025. This market is expected to reach USD 8.4 billion by 2036 from an estimated USD 1.2 billion in 2026, growing at a CAGR of 21.4% during the forecast period 2026-2036.

Click here to: Get Free Sample Pages of this Report

Space mining refers to the extraction of useful materials from the Moon, asteroids, and other bodies in space for use either in space or eventually back on Earth. Just as mining companies on Earth dig up iron, copper, gold, and other minerals to supply industry and manufacturing, space mining companies aim to collect water ice, metals, and rare minerals from space bodies where these resources exist in enormous quantities. The most immediately valuable target is water ice that has been confirmed in permanently shadowed craters at the Moon's poles. When split into its component hydrogen and oxygen using solar electricity, water ice becomes rocket fuel. A Moon-based fuel depot that can refuel spacecraft headed for Mars or deeper into the solar system would eliminate the need to carry all that propellant from Earth, dramatically reducing the cost and weight of deep space missions.

The market is still in its very early stages, with current activity concentrated on exploration, technology development, and small-scale demonstration missions rather than commercial resource extraction. However, the investment flowing into space mining is growing steadily as NASA's Artemis program returns humans to the Moon and creates concrete near-term demand for in-space resource utilization technology, as the cost of space access falls due to reusable rockets, and as multiple countries including the United States, Luxembourg, the UAE, and Japan have passed national laws explicitly granting their citizens and companies the right to own and sell resources they extract from space bodies. These legal frameworks are essential for creating a commercially viable space mining industry, as they give potential investors and operators confidence that the resources they extract will be legally theirs to use and sell.

Two significant near-term opportunities are driving the current phase of investment. The use of water ice mined from the Moon's polar craters as rocket propellant for deep space missions is the most commercially immediate application, and NASA's Artemis program is actively developing in-situ resource utilization technology precisely because being able to refuel on the Moon would make the entire Artemis program and future Mars missions dramatically cheaper. Second, the development of permanent lunar infrastructure including habitats, power systems, and laboratories will need construction materials, radiation shielding, and structural components that are far too expensive to transport from Earth, making lunar regolith processing and construction a high-priority application for space mining technology.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 8.4 Billion |

|

Market Size in 2026 |

USD 1.2 Billion |

|

Market Size in 2025 |

USD 0.82 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 21.4% |

|

Dominating Resource Type |

Water and Volatiles |

|

Fastest Growing Resource Type |

Precious Metals (PGMs) |

|

Dominating Mining Location |

Lunar Surface |

|

Fastest Growing Mining Location |

Near-Earth Asteroids (NEAs) |

|

Dominating Mission Stage |

Exploration and Prospecting |

|

Fastest Growing Mission Stage |

Extraction and Excavation |

|

Dominating Application |

In-Space Resource Utilization (ISRU) |

|

Fastest Growing Application |

Space Infrastructure Development |

|

Dominating End User |

Space Agencies |

|

Fastest Growing End User |

Commercial Space Companies |

|

Dominating Equipment Type |

Mining Robots and Rovers |

|

Fastest Growing Equipment Type |

Processing and Refining Systems |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

NASA Artemis Program Creating the First Real Commercial Market for Space Mining Technology

The most important commercial development driving the space mining market forward is NASA's Artemis program returning humans to the Moon and its explicit commitment to developing and using in-situ resource utilization technology as part of that program. NASA has contracted multiple companies including Intuitive Machines, Astrobotic, and Masten Space Systems under its Commercial Lunar Payload Services program to deliver scientific payloads to the Moon, including instruments designed to prospect for water ice deposits and test resource extraction techniques. The Lunar Compact Spectrometer and MOXIE experiment, which successfully produced oxygen from the Martian atmosphere as a precursor demonstration, represent the kind of technology that NASA is investing in as preparation for full-scale lunar resource utilization.

For commercial space mining companies, the Artemis program represents both a funded customer for their early technology development and a proof of concept that will validate the commercial opportunity. When NASA demonstrates that lunar ice can be successfully extracted and converted to rocket fuel, it will establish the technical foundations that private space fuel depot companies need to build their commercial business models on. The Artemis program's timeline targeting a permanent lunar outpost and eventually a sustained human presence on the Moon provides a credible pathway to large-scale space mining commercial demand, and companies that establish technology leadership now are positioning themselves for the contracts and commercial opportunities that will flow from that program.

Water Ice on the Moon is the Immediate Commercial Prize

While the popular imagination of space mining often focuses on the possibility of returning platinum or gold from asteroids to Earth, the real near-term commercial opportunity that is driving most of the investment in the space mining industry today is the extraction of water ice from permanently shadowed craters at the Moon's poles. NASA's LCROSS mission confirmed the presence of water ice in the Moon's southern polar region in 2009, and subsequent data from the Lunar Reconnaissance Orbiter and India's Chandrayaan-1 mission have confirmed that significant water ice deposits exist at both poles. The commercial value of this water ice is not primarily as drinking water but as the source material for rocket propellant: splitting water into hydrogen and oxygen through electrolysis using solar power produces the same propellant combination used by the Space Shuttle's main engines and a wide variety of rocket systems.

A commercial lunar fuel depot that could produce and sell rocket propellant from lunar ice would fundamentally change the economics of deep space exploration and eventually of space commerce more broadly. Every kilogram of propellant that a Mars mission or deep space spacecraft can refuel with at the Moon rather than carrying from Earth reduces the amount of propellant that needs to be launched from Earth's surface, which is by far the most expensive part of any space mission. TransAstra Corporation, Maxar Technologies, and several NASA-contracted companies are specifically targeting water ice extraction and processing as their primary near-term space mining objective, and the business case for this application is commercially credible in a way that asteroid metal mining to Earth is not yet.

Regulatory Clarity in Key Markets Enabling Private Investment

A significant and commercially important trend in the space mining market is the progressive development of national legal frameworks that give space mining companies in key countries the legal right to own and sell resources they extract from space bodies. The United States passed the Commercial Space Launch Competitiveness Act in 2015, which explicitly grants American citizens and companies the right to possess, own, transport, use, and sell resources they extract from asteroids and other space bodies. Luxembourg, the UAE, Japan, the United Arab Emirates, and several other countries have subsequently passed equivalent national legislation. These laws are very important for the commercial viability of space mining because they answer the fundamental investor question of whether the resources extracted will legally belong to the company that extracted them, which is a prerequisite for building a business plan around resource extraction.

The legal situation is not without complexity. The 1967 Outer Space Treaty, which the United States and most space-faring nations have signed, prohibits national appropriation of the Moon and other celestial bodies. The national laws passed in the U.S. and Luxembourg are carefully drafted to comply with this by granting ownership of extracted resources rather than ownership of the celestial body itself, essentially the same principle that allows fishermen to own the fish they catch from the open ocean without claiming ownership of the ocean. The growing number of countries passing space resource ownership laws is creating a more stable legal environment for private investment and is encouraging more companies and investors to take space mining seriously as a commercial opportunity rather than a theoretical future concept.

Growth of Space Economy and Infrastructure

The rapid expansion of the broader space economy, including satellite constellations, space tourism, commercial space stations, and deep space exploration missions, is creating growing demand for in-space resources that cannot be sustainably or economically supplied from Earth. Every kilogram of material launched from Earth's surface currently costs between USD 1,000 and USD 10,000 depending on the rocket and destination, which makes even relatively simple construction materials prohibitively expensive to deliver to the Moon or beyond in the quantities that permanent space infrastructure would require. A permanent lunar base would need thousands of tonnes of structural material, radiation shielding, and life support consumables that are simply too expensive to launch from Earth at any realistic program scale. The development of the broader space economy is therefore creating a structural demand for in-space resource extraction that grows stronger as space activity becomes more ambitious and more sustained, making space mining not a distant speculative concept but an increasingly near-term necessity for the continued expansion of human activity in space.

Advancements in Robotics and Autonomous Systems

The rapid improvement in robotics, autonomous systems, and artificial intelligence that has transformed industries on Earth is also making space mining more technically and commercially feasible by enabling robotic systems that can operate independently in the harsh and remote environments of the Moon and asteroids without requiring continuous human supervision. A mining robot on the Moon must deal with the two-week lunar night when solar power is unavailable, extreme temperature swings of over 300 degrees Celsius between sunlit and shadowed areas, abrasive and electrostatically charged lunar dust that can damage mechanical components, and communication delays that make real-time human control from Earth impractical. Modern autonomous robotics can handle these challenges through sophisticated onboard decision-making that allows robots to respond to changing environmental conditions, navigate complex terrain, and continue working through situations that would stall a remotely controlled system waiting for human instruction. NASA's Perseverance rover on Mars, which has operated largely autonomously for years, demonstrates that autonomous robotic systems can function reliably in extreme extraterrestrial environments, providing important technical validation for the concept of autonomous space mining operations.

In-Situ Resource Utilization (ISRU)

In-situ resource utilization, the practice of using materials available at a space destination to support operations there rather than bringing everything from Earth, is the most immediately commercially and operationally important application of space mining and the area attracting the greatest near-term investment and development effort. The fundamental insight behind ISRU is simple: if you need water, oxygen, rocket fuel, or construction materials in space, it is far better and cheaper to produce or collect them where you are than to launch them from Earth. NASA has identified ISRU as a critical enabler of its long-term Moon and Mars exploration architecture and has invested in ISRU technology development through its Game Changing Development program and its collaboration with industry through the Commercial Lunar Payload Services contracts. The Oxygen and Volatiles Extraction demonstration payload planned for a CLPS lunar delivery mission will attempt to extract oxygen from lunar soil, directly demonstrating the commercial and operational potential of ISRU technology that underpins the near-term space mining market.

Development of Lunar Bases and Space Stations

The development of permanent human infrastructure on and around the Moon through NASA's Artemis program, its international Lunar Gateway station, and the growing ecosystem of commercial lunar programs represents a large and growing demand source for in-situ resource extraction capabilities. A lunar outpost that operates continuously with a rotating crew will require water for drinking, cooking, and hygiene, oxygen for breathing, rocket propellant for return trips and supply missions, and construction materials for expanding and protecting habitat structures. Meeting these needs entirely from Earth launches would be extraordinarily expensive and would severely limit the scale and ambition of any lunar program. The ability to extract water from lunar polar ice deposits, process lunar regolith into construction materials and oxygen, and eventually manufacture structural components from lunar metals would transform the economics of sustained lunar presence and make the entire Artemis program significantly more affordable and achievable. This connection between lunar infrastructure development and space mining demand is one of the clearest and most commercially credible demand signals in the market.

By Resource Type: In 2026, Water and Volatiles to Dominate

Based on resource type, the global space mining market is segmented into water and volatiles, precious metals, rare earth elements, base metals, and other resources. In 2026, the water and volatiles segment is expected to account for the largest share of the global space mining market. Water ice confirmed in the permanently shadowed polar craters of the Moon represents the most commercially immediately relevant space mining target because its value as rocket propellant feedstock and as a source of drinking water, oxygen, and hydrogen for life support systems is directly applicable to the Artemis program's near-term operational needs. The substantial investment by NASA in ISRU technology development and the multiple commercial lunar delivery missions carrying water ice prospecting instruments confirm water and volatiles as the highest-priority resource type in the current market.

However, the precious metals segment, particularly platinum group metals, is projected to register the highest CAGR during the forecast period. Certain types of asteroids contain extraordinary concentrations of platinum group metals including platinum, palladium, rhodium, and iridium that could be worth trillions of dollars at current Earth market prices if extracted and brought to market. The long-term value of asteroid precious metal mining is enormous, and as the costs of deep space missions fall and the technology for asteroid capture and processing matures, the commercial case for precious metal asteroid mining is expected to become progressively more credible, driving growing investment and development activity through the forecast period.

By Mining Location: In 2026, Lunar Surface to Hold the Largest Share

Based on mining location, the global space mining market is segmented into lunar surface, near-earth asteroids, and Mars and other celestial bodies. In 2026, the lunar surface segment is expected to account for the largest share of the global space mining market. The Moon is the closest and most practically accessible destination for space mining operations, located only three days travel from Earth and the target of the most well-funded and advanced space mining technology development programs through NASA's Artemis initiative, the European Space Agency's lunar programs, and the commercial lunar lander missions of iSpace, Astrobotic, and other CLPS providers. The confirmed presence of water ice at the lunar poles, the growing understanding of the Moon's mineral resources from decades of remote sensing data, and the proximity to Earth that makes the Moon the most practical first target for any space mining mission collectively make the lunar surface the dominant location for near-term space mining investment and operations.

However, the near-earth asteroids segment is projected to register the highest CAGR during the forecast period. Certain classes of near-earth asteroids contain extraordinary concentrations of metallic resources including iron, nickel, cobalt, and platinum group metals in concentrations far higher than any ore deposits on Earth. As the cost of deep space missions falls with reusable launch vehicles and as asteroid mining technology develops through demonstration missions, the enormous resource value of near-earth asteroids is expected to attract growing investment and eventually commercial extraction activity. The very large estimated resource value of the most metal-rich near-earth asteroids, with some individual objects estimated to contain more platinum than has been mined in all of human history, provides a compelling long-term commercial motivation for continued investment.

By Mission Stage: In 2026, Exploration and Prospecting to Hold the Largest Share

Based on mission stage, the global space mining market is segmented into exploration and prospecting, extraction and excavation, processing and refining, and transportation and delivery. In 2026, the exploration and prospecting segment is expected to account for the largest share of the global space mining market. The current market is overwhelmingly focused on the earliest stage of the mining value chain, where orbiting spacecraft, surface rovers, and lander-deployed instruments survey, map, and characterize resource deposits to identify exactly where the most accessible and richest concentrations of valuable materials are located. All of the commercial lunar lander missions currently contracted under NASA's CLPS program include prospecting payloads, and the remote sensing data these missions will generate is essential for planning future extraction operations. This exploration-focused investment represents the foundational stage of building a space mining industry, comparable to the geological survey activities that precede any Earth-based mining project.

However, the extraction and excavation segment is projected to register the highest CAGR during the forecast period. As exploration missions confirm resource locations and quality, the investment emphasis will shift progressively toward developing and deploying the actual extraction equipment, including robotic excavators, drilling systems, and material handling equipment that can operate on the lunar surface or on an asteroid and produce usable quantities of the target resource. NASA's ISRU demonstration programs and several commercial companies are actively developing prototype extraction equipment, and the first small-scale extraction demonstrations are expected to occur during the forecast period, driving rapid growth in this segment from its current very small base.

By Application: In 2026, ISRU to Hold the Largest Share

Based on application, the global space mining market is segmented into in-space resource utilization (ISRU), earth-based resource supply, space infrastructure development, defense and strategic applications, and emerging applications. In 2026, the ISRU segment is expected to account for the largest share of the global space mining market. The production of rocket propellant, breathable oxygen, and water from lunar resources for use by astronauts and spacecraft operating on and around the Moon is the most immediately commercially and operationally relevant application of space mining, and it has attracted the most focused investment from NASA and its commercial partners. ISRU is prioritized over earth-based resource supply in the near term because extracting even small quantities of useful materials in space and using them there provides an immediate and enormous cost saving by reducing the amount of consumables that need to be launched from Earth, without requiring the technically much more challenging task of transporting asteroid metals back to Earth's surface.

However, the space infrastructure development segment is projected to register the highest CAGR during the forecast period. Using mined lunar materials to construct habitats, radiation shields, landing pads, roads, and other physical infrastructure on the Moon represents the natural next step after ISRU demonstrates that useful quantities of resources can be extracted and processed in space. As the Artemis program progresses toward a permanent lunar outpost, the demand for in-situ construction using lunar materials will grow substantially, creating the fastest-growing application category for space mining technology and investment through the forecast period.

By End User: In 2026, Space Agencies to Hold the Largest Share

Based on end user, the global space mining market is segmented into space agencies, defense organizations, commercial space companies, and research institutions. In 2026, the space agencies segment is expected to account for the largest share of the global space mining market. NASA's investment in ISRU technology through its Commercial Lunar Payload Services program, Artemis infrastructure development, and its Game Changing Development programs represents the largest single source of space mining-related investment in the world today. ESA's lunar resource utilization programs, JAXA's lunar exploration activities, and the space agency programs of China, India, and other nations collectively make space agencies the dominant current buyers of space mining technology development and demonstration services. This government agency-led demand is the commercial foundation of the current market, providing the funded contracts that give technology developers the revenue to advance their capabilities.

However, the commercial space companies segment is projected to register the highest CAGR during the forecast period. As technology matures and the regulatory framework solidifies, private companies pursuing space mining as a commercial business are expected to drive increasingly rapid investment growth. Companies including TransAstra, OffWorld, and iSpace are building their business models around commercial space mining services, and the commercial demand from private space stations, commercial lunar programs, and eventually space manufacturing facilities is expected to diversify the customer base well beyond government space agencies as the decade progresses.

By Equipment Type: In 2026, Mining Robots and Rovers to Hold the Largest Share

Based on equipment type, the global space mining market is segmented into mining robots and rovers, drilling and excavation equipment, processing and refining systems, and transportation systems. In 2026, the mining robots and rovers segment is expected to account for the largest share of the global space mining market. Robotic vehicles capable of traversing the lunar surface or an asteroid surface, collecting and transporting regolith or rock samples, and carrying instrument packages for resource detection and characterization represent the highest-development and highest-investment equipment category in the current market. NASA's lunar rover programs, commercial lander missions carrying rover payloads, and the robotics development programs of companies including OffWorld and iSpace are driving investment in this category.

However, the processing and refining systems segment is projected to register the highest CAGR during the forecast period. As exploration and extraction activities progress, the equipment needed to actually convert raw extracted materials into usable products, including electrolysis systems to split water into hydrogen and oxygen, furnaces to process lunar regolith into oxygen and metal, and refining systems to produce propellant-grade hydrogen and oxygen, will represent the highest-value equipment category in a maturing space mining industry. The development of practical and reliable in-space processing systems is the critical technology bottleneck that separates current exploratory space mining activity from genuine commercial resource production.

Space Mining Market by Region: North America Leading by Share, Asia-Pacific by Growth

Based on geography, the global space mining market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

In 2026, North America is expected to account for the largest share of the global space mining market. The United States dominates the space mining market through the combination of NASA's very large ISRU technology investment programs under the Artemis initiative, the most commercially advanced space mining technology companies including Astrobotic, TransAstra, OffWorld, Moon Express, and iSpace's U.S. operations, and the legal framework established by the 2015 Commercial Space Launch Competitiveness Act that gives American companies the clearest and most established legal right to own resources extracted from space bodies. NASA's Commercial Lunar Payload Services program, which has contracted multiple American companies for lunar delivery missions carrying resource prospecting payloads, is the largest single government investment program in space mining technology in the world and makes North America the commercial center of the current market. Canada's growing space industry and its contributions to lunar rover and robotics programs add further North American depth to the market.

However, the Asia-Pacific space mining market is expected to grow at the fastest CAGR during the forecast period. China has placed lunar resource utilization at the center of its national space program and its Chang'e lunar exploration series has delivered increasingly capable lunar rovers and landers, with Chang'e-5 successfully returning the first lunar samples since the Apollo era in 2020. China's plans for a permanent International Lunar Research Station at the Moon's south pole, scheduled for development through the 2030s, will create substantial demand for in-situ resource utilization technology that China is actively developing through its national space program and supporting commercial companies. Japan's iSpace has flown its first commercial lunar landing mission and is developing a series of increasingly capable lunar landers and resource prospecting rovers. India's Chandrayaan lunar program confirmed water ice at the Moon's poles and its continued lunar exploration investments position India as a significant Asia-Pacific space mining market participant. South Korea and Australia are growing their national space programs and space industry sectors, contributing to the region's growth trajectory.

Europe plays an important role in the global space mining market through the European Space Agency's lunar resource utilization programs and the unique contribution of Luxembourg, which has established itself as a global center for space resource law and commercial space activity through its SpaceResources initiative that provides legal certainty for space resource extraction by Luxembourg-incorporated companies. ESA's partnership programs with commercial lunar lander companies, its investment in ISRU technology development, and the growing national space programs of Germany, France, and the UK contribute to Europe's market position. The UAE's national space program, which has grown rapidly to include the Hope Mars orbiter and ambitious lunar exploration plans, represents an important emerging market contributor from the Middle East and Africa region.

The space mining market includes a range of participants from established defense and aerospace prime contractors providing spacecraft and integration services, through specialized commercial space companies building lunar landers and mining robots, to the national space agencies that are the primary current customers for space mining technology development. Most commercial space mining companies are still at early development stages and have not yet demonstrated commercial resource extraction, making this a market where technology development contracts and government grants are currently more important than commercial product sales.

iSpace, a Japanese company with offices in the U.S. and Europe, has flown its first commercial lunar landing mission and is developing a series of lunar landers and rovers specifically designed to support resource prospecting and eventually extraction operations. Astrobotic Technology has delivered its first payload to the lunar surface under a NASA CLPS contract and is developing the Griffin lander for heavier payloads and the CubeRover platform for surface exploration. TransAstra is developing the Honey Bee asteroid mining spacecraft and lunar mining robots, targeting water ice extraction as its primary near-term commercial application. OffWorld is building robots specifically designed for off-world mining operations across the Moon, asteroids, and Mars. Lockheed Martin, Northrop Grumman, Airbus, and Thales Alenia Space provide the spacecraft manufacturing, systems integration, and technology development services that underpin the space mining value chain.

The report provides a comprehensive competitive analysis based on a thorough review of leading players' mission histories, technology capabilities, government contract status, investment funding, and recent strategic developments. Some of the key players operating in the global space mining market include iSpace Inc. (Japan/U.S.), Astrobotic Technology Inc. (U.S.), Moon Express Inc. (U.S.), Planetary Resources/ConsenSys Space (U.S.), Deep Space Industries/Bradford Space (U.S.), TransAstra Corporation (U.S.), OffWorld Inc. (U.S.), Maxar Technologies Inc. (U.S.), Lockheed Martin Corporation (U.S.), Northrop Grumman Corporation (U.S.), Blue Origin LLC (U.S.), SpaceX (U.S.), Sierra Space Corporation (U.S.), Thales Alenia Space (France/Italy), and Airbus SE (Netherlands), among others.

The global space mining market is expected to reach USD 8.4 billion by 2036 from an estimated USD 1.2 billion in 2026, at a CAGR of 21.4% during the forecast period 2026-2036.

In 2026, the water and volatiles segment is expected to hold the largest share of the global space mining market, driven by lunar water ice representing the most commercially immediate space mining target as the source of rocket propellant for NASA's Artemis program and future deep space missions.

The precious metals segment is expected to register the highest CAGR during the forecast period 2026-2036, driven by the enormous long-term value of platinum group metals in certain asteroid types and the growing investment in demonstration missions and technology development targeting metallic asteroid mining.

In 2026, the lunar surface segment is expected to hold the largest share of the global space mining market, reflecting the Moon being the closest, most accessible, and most heavily invested-in space mining destination driven by NASA's Artemis program and multiple commercial lunar lander programs.

In 2026, the in-space resource utilization segment is expected to hold the largest share of the global space mining market, reflecting ISRU as the most immediately commercially and operationally valuable application of space mining for producing rocket fuel, oxygen, and water from lunar resources.

The market is primarily driven by NASA's Artemis program creating concrete funded demand for in-situ resource utilization technology as an essential component of its sustainable lunar exploration architecture, and by the growth of the broader space economy creating structural demand for in-space resources that cannot be economically supplied from Earth as space activity becomes more ambitious and sustained.

Key players are iSpace Inc. (Japan/U.S.), Astrobotic Technology Inc. (U.S.), Moon Express Inc. (U.S.), Planetary Resources/ConsenSys Space (U.S.), Deep Space Industries/Bradford Space (U.S.), TransAstra Corporation (U.S.), OffWorld Inc. (U.S.), Maxar Technologies Inc. (U.S.), Lockheed Martin Corporation (U.S.), Northrop Grumman Corporation (U.S.), Blue Origin LLC (U.S.), SpaceX (U.S.), Sierra Space Corporation (U.S.), Thales Alenia Space (France/Italy), and Airbus SE (Netherlands), among others.

Asia-Pacific is expected to register the highest growth rate in the global space mining market during the forecast period 2026-2036, driven by China's national commitment to permanent lunar infrastructure development requiring in-situ resource utilization, Japan's growing commercial lunar lander and rover programs through iSpace, and India's confirmed water ice detection capability and continued lunar exploration investment.

1. Introduction

1.1. Market Definition

1.2. Market Ecosystem

1.3. Currency and Limitations

1.3.1. Currency

1.3.2. Limitations

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Data Collection & Validation Process

2.2.1. Secondary Research

2.2.2. Primary Research & Validation

2.2.2.1. Primary Interviews with Experts

2.2.2.2. Approaches for Country-/Region-Level Analysis

2.3. Market Estimation

2.3.1. Bottom-Up Approach

2.3.2. Top-Down Approach

2.3.3. Growth Forecast

2.4. Data Triangulation

2.5. Assumptions for the Study

3. Executive Summary

4. Market Overview

4.1. Introduction

4.2. Market Dynamics

4.2.1. Drivers

4.2.1.1. Increasing Demand for Rare Metals and Resources

4.2.1.2. Growth of Space Economy and Infrastructure

4.2.1.3. Advancements in Robotics and Autonomous Systems

4.2.1.4. Rising Investments in Lunar and Asteroid Missions

4.2.2. Restraints

4.2.2.1. High Mission Costs and Technological Barriers

4.2.2.2. Uncertain Regulatory and Legal Framework

4.2.2.3. Limited Commercial Viability in Early Stages

4.2.3. Opportunities

4.2.3.1. Resource Utilization for In-Space Manufacturing

4.2.3.2. Development of Lunar Bases and Space Stations

4.2.3.3. In-Situ Resource Utilization (ISRU)

4.2.3.4. Strategic Defense and Space Sovereignty Initiatives

4.2.4. Challenges

4.2.4.1. Extreme Environmental Conditions

4.2.4.2. Logistics and Transportation Complexity

4.3. Technology Landscape

4.3.1. Autonomous Mining Robotics

4.3.2. Remote Sensing and Resource Detection

4.3.3. Space Drilling and Excavation Technologies

4.3.4. In-Situ Resource Processing (ISRU)

4.3.5. Space Transportation and Logistics Systems

4.4. Space Mining Value Chain

4.4.1. Exploration and Resource Identification

4.4.2. Extraction and Mining Operations

4.4.3. Processing and Refining

4.4.4. Transportation and Logistics

4.4.5. End-Use Applications

4.5. Value Chain Analysis

4.5.1. Spacecraft and Robotics Manufacturers

4.5.2. Technology and Component Providers

4.5.3. Space Agencies and Defense Organizations

4.5.4. Commercial Space Companies

4.5.5. End Users

4.6. Regulatory and Legal Landscape

4.6.1. Outer Space Treaty and International Frameworks

4.6.2. National Space Resource Policies (U.S., Luxembourg, UAE, etc.)

4.6.3. Licensing and Ownership Rights

4.7. Porter's Five Forces Analysis

4.8. Investment and Industry Trends

4.8.1. Government Space Exploration Programs

4.8.2. Private Sector Investments and Startups

4.8.3. Strategic Collaborations and Partnerships

5. Space Mining Market, by Resource Type

5.1. Introduction

5.2. Water and Volatiles

5.2.1. Ice Deposits (Lunar/Polar Regions)

5.2.2. Hydrogen and Oxygen Extraction

5.3. Precious Metals

5.3.1. Platinum Group Metals (PGMs)

5.3.2. Gold and Silver

5.4. Rare Earth Elements (REEs)

5.5. Base Metals

5.5.1. Iron

5.5.2. Nickel

5.5.3. Cobalt

5.6. Other Resources

6. Space Mining Market, by Mining Location

6.1. Introduction

6.2. Lunar Surface

6.3. Near-Earth Asteroids (NEAs)

6.4. Mars and Other Celestial Bodies

7. Space Mining Market, by Mission Stage

7.1. Introduction

7.2. Exploration and Prospecting

7.3. Extraction and Excavation

7.4. Processing and Refining

7.5. Transportation and Delivery

8. Space Mining Market, by Application

8.1. Introduction

8.2. In-Space Resource Utilization (ISRU)

8.2.1. Fuel Production (Hydrogen, Oxygen)

8.2.2. Life Support Systems

8.2.3. Construction Materials for Space Infrastructure

8.3. Earth-Based Resource Supply

8.3.1. Precious Metal Supply

8.3.2. Industrial Raw Materials

8.4. Space Infrastructure Development

8.4.1. Lunar Bases and Habitats

8.4.2. Space Stations

8.4.3. Deep Space Missions

8.5. Defense and Strategic Applications

8.5.1. Space Resource Security

8.5.2. Military Space Operations

8.6. Emerging Applications

8.6.1. Space Manufacturing

8.6.2. Space Tourism Support

8.6.3. Interplanetary Missions

9. Space Mining Market, by End User

9.1. Introduction

9.2. Space Agencies

9.3. Defense Organizations

9.4. Commercial Space Companies

9.5. Research Institutions

10. Space Mining Market, by Equipment Type

10.1. Introduction

10.2. Mining Robots and Rovers

10.3. Drilling and Excavation Equipment

10.4. Processing and Refining Systems

10.5. Transportation Systems

11. Space Mining Market, by Operation Mode

11.1. Introduction

11.2. Autonomous Operations

11.3. Remote Teleoperation

11.4. Hybrid Operations

12. Space Mining Market, by Geography

12.1. Introduction

12.2. North America

12.2.1. U.S.

12.2.2. Canada

12.2.3. Mexico

12.3. Europe

12.3.1. Luxembourg

12.3.2. Germany

12.3.3. France

12.3.4. U.K.

12.3.5. Italy

12.3.6. Spain

12.3.7. Netherlands

12.3.8. Rest of Europe

12.4. Asia-Pacific

12.4.1. China

12.4.2. India

12.4.3. Japan

12.4.4. South Korea

12.4.5. Australia

12.4.6. Singapore

12.4.7. Rest of Asia-Pacific

12.5. Latin America

12.5.1. Brazil

12.5.2. Mexico

12.5.3. Argentina

12.5.4. Chile

12.5.5. Colombia

12.5.6. Rest of Latin America

12.6. Middle East & Africa

12.6.1. UAE

12.6.2. Saudi Arabia

12.6.3. Israel

12.6.4. South Africa

12.6.5. Turkey

12.6.6. Rest of Middle East & Africa

13. Competitive Landscape

13.1. Overview

13.2. Key Growth Strategies

13.3. Competitive Benchmarking

13.4. Competitive Dashboard

13.4.1. Industry Leaders

13.4.2. Market Differentiators

13.4.3. Vanguards

13.4.4. Emerging Companies

13.5. Market Ranking/Positioning Analysis of Key Players, 2025

14. Company Profiles

14.1. iSpace Inc.

14.2. Astrobotic Technology, Inc.

14.3. Moon Express, Inc.

14.4. Planetary Resources (acquired by ConsenSys)

14.5. Deep Space Industries (acquired by Bradford Space)

14.6. TransAstra Corporation

14.7. OffWorld Inc.

14.8. Maxar Technologies Inc.

14.9. Lockheed Martin Corporation

14.10. Northrop Grumman Corporation

14.11. Blue Origin LLC

14.12. SpaceX

14.13. Sierra Space Corporation

14.14. Thales Alenia Space

14.15. Airbus SE

15. Appendix

15.1. Additional Customization

15.2. Related Reports

Published Date: Apr-2026

Subscribe to get the latest industry updates