Resources

About Us

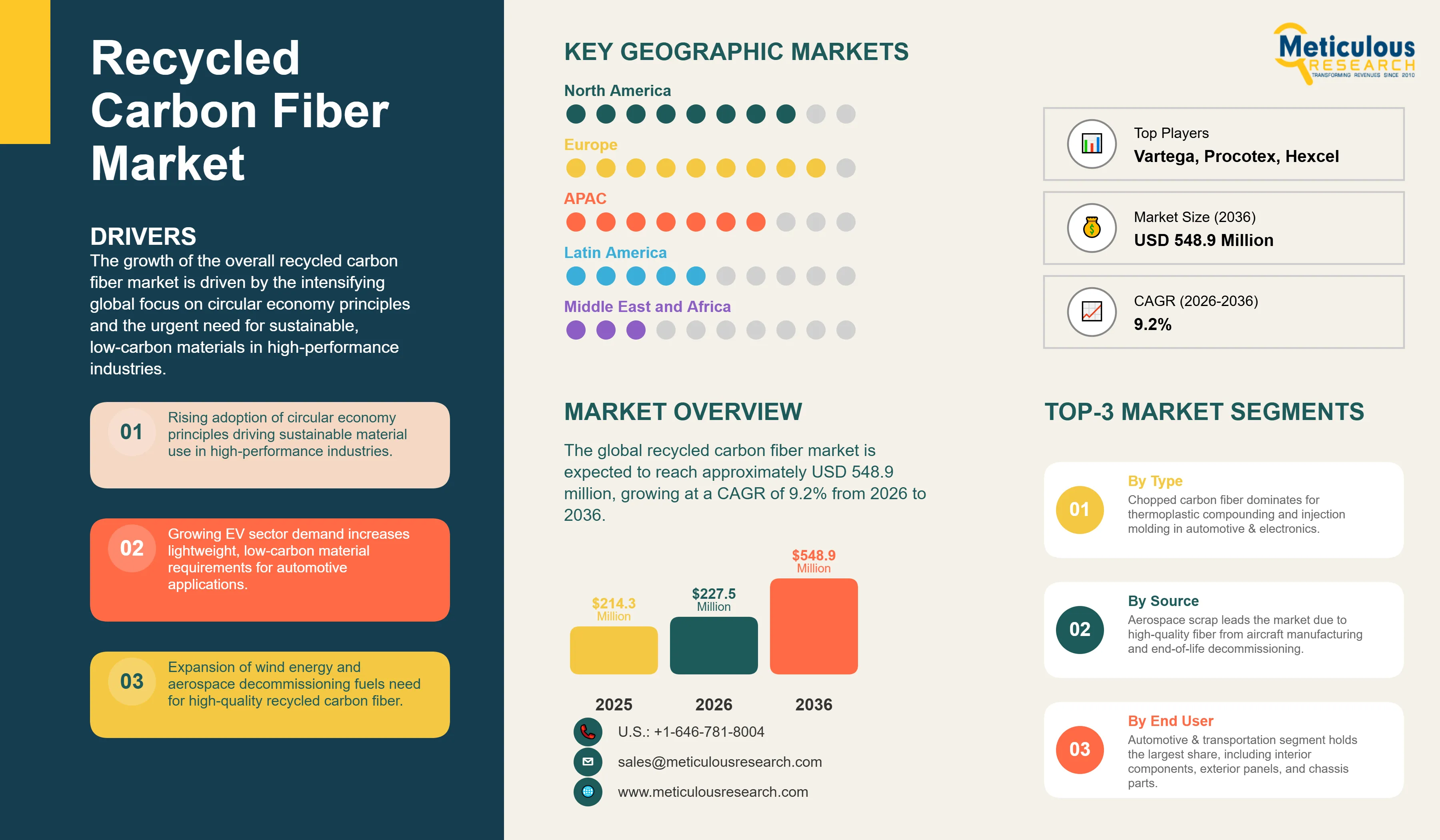

The global recycled carbon fiber market was valued at USD 214.3 million in 2025. The market is expected to reach approximately USD 548.9 million by 2036 from USD 227.5 million in 2026, growing at a CAGR of 9.2% from 2026 to 2036. The growth of the overall recycled carbon fiber market is driven by the intensifying global focus on circular economy principles and the urgent need for sustainable, low-carbon materials in high-performance industries. As manufacturers seek to reduce the environmental impact of composite waste and lower the total cost of ownership (TCO) for carbon fiber applications, recycled fibers have become a viable alternative to virgin carbon fiber. The rapid expansion of the electric vehicle (EV) sector, coupled with the increasing decommissioning of commercial aircraft and wind turbine blades, continues to fuel significant growth of this market across all major geographic regions.

Click here to: Get Free Sample Pages of this Report

Recycled carbon fiber (rCF) is a high-value material recovered from carbon fiber reinforced polymer (CFRP) waste through advanced thermal, chemical, or mechanical processes. These fibers retain a significant portion of the mechanical properties of virgin carbon fiber while offering a substantially lower carbon footprint—often up to 95-99% lower—and a more competitive price point. The market is defined by high-efficiency recovery technologies such as pyrolysis and solvolysis, which allow for the reclamation of clean, high-quality fibers that can be re-integrated into new composite applications. These materials are indispensable for industries seeking to achieve “closed-loop” manufacturing and meet ambitious net-zero emission targets.

The market includes a diverse range of product formats, ranging from chopped and milled fibers for thermoplastic compounding to non-woven mats and fabrics for structural reinforcements. These products are increasingly integrated with advanced sizing chemistries and digital traceability platforms to provide services such as material certification and life cycle assessment (LCA) data. The ability to provide stable, high-performance material recovery while minimizing landfill waste has made advanced recycled carbon fiber the technology of choice for industries where resource efficiency and environmental compliance are paramount.

The global industrial sector is pushing hard to modernize its material supply chains, aiming to meet circularity and sustainability targets. This drive has increased the adoption of rCF in non-structural and semi-structural components, with advanced recovery processes helping to stabilize the supply of high-performance fibers. At the same time, the rapid growth in the wind energy and aerospace decommissioning markets is increasing the need for scalable and efficient recycling solutions.

Proliferation of Closed-Loop Take-Back Systems and OEM Partnerships

Manufacturers across the aerospace and automotive industries are rapidly shifting to closed-loop recycling models, moving well beyond traditional waste disposal toward smarter, integrated take-back systems. Gen 2 Carbon’s latest recovery platforms deliver high-quality reclaimed fibers that are being re-integrated into aerospace interiors, while Vartega’s partnerships with automotive OEMs have enabled the use of recycled fibers in high-volume thermoplastic components. The real game-changer comes with “smart” take-back programs featuring digital material passports like those being developed by Mitsubishi Chemical Group, which maintain material traceability and quality assurance even as fibers move through multiple life cycles. These advancements make high-efficiency carbon fiber recycling practical and cost-effective for everyone from Tier 1 suppliers to global aircraft manufacturers chasing circularity and lower carbon footprints.

Innovation in Fiber Length Retention and Thermoplastic Compounding

Innovation in fiber recovery and downstream processing is rapidly driving the recycled carbon fiber market, as the thermoplastic compounding and 3D printing sectors scale up. Equipment suppliers are now designing recycling trains specifically for high-purity aerospace and automotive scrap, with tight control over fiber length distribution, surface sizing, and impurity levels to meet stringent performance specifications. This often involves advanced pyrolysis and chemical recycling processes capable of handling complex resin systems without degrading the underlying carbon fibers.

At the same time, growing focus on circular economy principles is pushing manufacturers to develop recycled carbon fiber solutions tailored to high-performance thermoplastic resins such as PEEK, PA, and PP. These systems help recover value from manufacturing offcuts and end-of-life parts, concentrating and processing them into drop-in replacements for virgin chopped fibers. By combining high-efficiency recovery with precisely controlled compounding stages, these new designs support both primary composite production and closed-loop recycling, strengthening the sustainability and resource security of the broader advanced materials value chain.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 548.9 Million |

|

Market Size in 2026 |

USD 227.5 Million |

|

Market Size in 2025 |

USD 214.3 Million |

|

Market Growth Rate (2026-2036) |

CAGR of 9.2% |

|

Dominating Region |

Europe |

|

Fastest Growing Region |

North America |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Type, Source, End-use, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Drivers: Circular Economy Mandates and Sustainability Targets

A key driver of the recycled carbon fiber market is the rapid movement of the global industry toward circularity and environmental stewardship. Global regulations requiring the reduction of industrial waste and the adoption of sustainable materials have created significant incentives for the adoption of carbon fiber recycling technologies. The EU Circular Economy Action Plan, the U.S. National Strategy to Advance the Circular Economy, and China’s “Circular Economy Promotion Law” drive manufacturers toward scalable solutions that recycled carbon fiber systems can uniquely provide. It is estimated that as landfill taxes rise and carbon emissions become more strictly regulated through 2036, the need for high-performance recycled materials increases significantly; therefore, recycled carbon fiber, with its ability to recover up to 90% of virgin fiber properties at a fraction of the environmental cost, is considered a crucial enabler of modern industrial strategies.

Opportunity: Expansion of EV and Wind Energy Markets

The rapid growth of the electric vehicle (EV) and wind energy sectors provides great opportunities for the recycled carbon fiber market. Indeed, the global surge in lightweighting initiatives has created a compelling demand for materials that can reduce vehicle weight and improve energy efficiency. These applications require high strength-to-weight ratios and the ability to handle complex geometries, all attributes that are met with advanced recycled carbon fiber compounds. The EV battery tray and wind turbine blade recycling markets are set to expand significantly through 2036, with recycled fibers poised for an expanding share as operators seek to monetize waste streams. Furthermore, the increasing demand for sustainable materials in the sporting goods and electronics sectors is stimulating demand for modular, high-quality recycled fiber systems that provide material independence and resilience.

Why Does Chopped Carbon Fiber Dominate the Market?

The chopped carbon fiber segment accounts for around 65-70% of the overall recycled carbon fiber market in 2026. This is mainly attributed to the primary use of this format in thermoplastic compounding and injection molding across a wide range of industries. These fibers offer the most efficient way to enhance the mechanical properties of plastic resins while maintaining high-volume processing capabilities. The automotive and electronics sectors alone consume the vast majority of chopped recycled fiber production, with major projects in Europe and North America demonstrating the material’s capability to handle demanding structural and semi-structural applications.

However, the non-woven mats and fabrics segment is expected to grow at a significant CAGR during the forecast period, driven by the growing utility-scale projects in aerospace interiors, sporting goods, and large-scale composite panels. The ability to produce high-value textile products from reclaimed fibers makes non-woven formats highly attractive for modern industrial users.

How Does Aerospace Scrap Lead the Market?

Based on source, the aerospace scrap segment holds the largest share of the overall market in 2026, accounting for around 55-60% of the overall market. From large-scale aircraft manufacturing offcuts to end-of-life airframe decommissioning, the use of aerospace-grade scrap is central to the supply of high-quality recycled carbon fiber. Current large-scale recycling projects are increasingly specifying aerospace scrap for its superior fiber quality and consistent material properties compared to automotive or industrial waste.

The automotive scrap and wind turbine scrap segments continue to find critical applications in industries where high-volume material availability is prioritized. However, the shift toward closed-loop recycling and digital traceability is pushing the requirement for standardized recovery systems that allow businesses to scale their recycling capacity while minimizing their carbon footprint.

How is Europe Maintaining Dominance in the Global Recycled Carbon Fiber Market?

Europe holds the largest share of the global recycled carbon fiber market in 2026. The largest share of this region is primarily attributed to the advanced industrial base and the presence of the world’s leading aerospace and automotive manufacturing hubs, particularly in Germany, France, and the UK. Europe alone accounts for a significant portion of global recycled fiber consumption, with its position as a leading hub for sustainability-driven innovation driving sustained growth. The presence of leading manufacturers like Gen 2 Carbon and a well-developed composite recycling supply chain provides a robust market for both standard and high-performance recycled fiber solutions.

Which Factors Support North America and Asia-Pacific Market Growth?

North America and Asia-Pacific together account for a growing share of the global recycled carbon fiber market. The growth of these markets is mainly driven by the need for material sustainability and the implementation of stringent environmental mandates. The demand for closed-loop systems in North America is mainly due to its large-scale aerospace projects and the presence of innovators like Vartega and Carbon Conversions.

In Asia-Pacific, the leadership in electronics manufacturing and the push for EV adoption are driving the adoption of high-efficiency recycled carbon fiber. Countries like Japan, China, and South Korea are at the forefront, with significant focus on integrating recycled fibers into digital factory environments and high-volume consumer products.

The companies such as Gen 2 Carbon, Vartega, Carbon Conversions, and SGL Carbon lead the global recycled carbon fiber market with a comprehensive range of recovery and compounding solutions, particularly for large-scale aerospace and automotive applications. Meanwhile, players including Toray Industries, Inc., Mitsubishi Chemical Group, Teijin Limited, and Hexcel Corporation focus on specialized closed-loop systems and high-performance reclaimed fibers targeting the aerospace and wind energy sectors. Emerging manufacturers and integrated players such as Shocker Composites, Carbon Fiber Recycling, Inc., and Procotex are strengthening the market through innovations in chemical recycling technology and smart material monitoring systems.

The recycled carbon fiber market is expected to grow from USD 227.5 million in 2026 to USD 548.9 million by 2036.

The recycled carbon fiber market is expected to grow at a CAGR of 9.2% from 2026 to 2036.

The major players include Gen 2 Carbon, Vartega, Carbon Conversions, SGL Carbon, and Toray Industries, Inc., among others.

The main factors include circular economy mandates, sustainability targets, and the rapid expansion of the EV and wind energy sectors.

Europe will lead the global recycled carbon fiber market in terms of market share, while North America is expected to witness significant growth during the forecast period 2026 to 2036.

1. Introduction

1.1 Market Definition

1.2 Market Ecosystem

1.3 Currency and Limitations

1.3.1 Currency

1.3.2 Limitations

1.4 Key Stakeholders

2. Research Methodology

2.1 Research Approach

2.2 Data Collection & Validation

2.2.1 Secondary Research

2.2.2 Primary Research

2.3 Market Assessment

2.3.1 Market Size Estimation

2.3.2 Bottom-Up Approach

2.3.3 Top-Down Approach

2.3.4 Growth Forecast

2.4 Assumptions for the Study

3. Executive Summary

3.1 Overview

3.2 Market Analysis, by Type

3.3 Market Analysis, by Source

3.4 Market Analysis, by End-use

3.5 Market Analysis, by Geography

3.6 Competitive Analysis

4. Market Insights

4.1 Introduction

4.2 Global Recycled Carbon Fiber Market: Impact Analysis of Market Drivers (2026–2036)

4.2.1 Intensifying Global Focus on Circular Economy and Sustainability

4.2.2 Cost Advantages of Recycled Carbon Fiber over Virgin Fiber

4.2.3 Stringent Environmental Regulations and Landfill Restrictions

4.3 Global Recycled Carbon Fiber Market: Impact Analysis of Market Restraints (2026–2036)

4.3.1 Technical Challenges in Maintaining Fiber Length and Mechanical Properties

4.3.2 Lack of Standardized Certification for Recycled Composite Materials

4.4 Global Recycled Carbon Fiber Market: Impact Analysis of Market Opportunities (2026–2036)

4.4.1 Rising Demand for Lightweight Materials in Electric Vehicles (EVs)

4.4.2 Adoption of Digital Traceability and Material Passports

4.5 Global Recycled Carbon Fiber Market: Impact Analysis of Market Challenges (2026–2036)

4.5.1 Complexity of Recycling Multi-Material and Thermoset Composites

4.5.2 Variability in Quality and Supply of End-of-Life Scrap

5. Global Recycled Carbon Fiber Market, by Type

5.1 Introduction

5.2 Chopped Carbon Fiber

5.3 Milled Carbon Fiber

5.4 Non-woven Mats & Fabrics

5.5 Others

6. Global Recycled Carbon Fiber Market, by Source

6.1 Introduction

6.2 Aerospace Scrap

6.3 Automotive Scrap

6.4 Wind Turbine Scrap

6.5 Others (Sporting Goods, Industrial Scrap)

7. Global Recycled Carbon Fiber Market, by End-use

7.1 Introduction

7.2 Automotive & Transportation

7.2.1 Interior Components

7.2.2 Exterior Panels

7.2.3 Chassis & Structural Parts

7.3 Aerospace & Defense

7.3.1 Commercial Aircraft

7.3.2 Military & Defense

7.3.3 Space & Satellites

7.4 Wind Energy

7.5 Sporting Goods

7.6 Electronics

7.7 Others

8. Global Recycled Carbon Fiber Market, by Geography

8.1 Introduction

8.2 North America

8.2.1 U.S.

8.2.2 Canada

8.3 Europe

8.3.1 Germany

8.3.2 France

8.3.3 U.K.

8.3.4 Italy

8.3.5 Rest of Europe

8.4 Asia-Pacific

8.4.1 China

8.4.2 Japan

8.4.3 India

8.4.4 South Korea

8.4.5 Rest of Asia-Pacific

8.5 Latin America

8.5.1 Brazil

8.5.2 Mexico

8.5.3 Rest of Latin America

8.6 Middle East & Africa

9. Competitive Landscape

9.1 Overview

9.2 Key Growth Strategies

9.3 Competitive Benchmarking

9.4 Market Share Analysis (2025)

9.5 Competitive Dashboard

9.5.1 Industry Leaders

9.5.2 Market Differentiators

9.5.3 Vanguards

9.5.4 Emerging Companies

9.6 Market Ranking / Positioning Analysis of Key Players, 2025

10. Company Profiles (Business Overview, Financial Overview, Product Portfolio, Strategic Developments)

10.1 Gen 2 Carbon

10.2 Vartega

10.3 Carbon Conversions

10.4 SGL Carbon

10.5 Toray Industries, Inc.

10.6 Mitsubishi Chemical Group

10.7 Teijin Limited

10.8 Hexcel Corporation

10.9 Shocker Composites

10.10 Carbon Fiber Recycling, Inc.

10.11 Procotex

10.12 Karborek Recycling Carbon Fibers

11. Appendix

11.1 Questionnaire

11.2 Related Reports

Published Date: Sep-2024

Published Date: Sep-2024

Published Date: May-2024

Published Date: Oct-2024

Published Date: Mar-2025

Subscribe to get the latest industry updates