Resources

About Us

Paperization Market Size, Share & Trends Analysis by Product Type, Application, Technology, End User, and Geography - Global Opportunity Analysis and Industry Forecast (2026-2036)

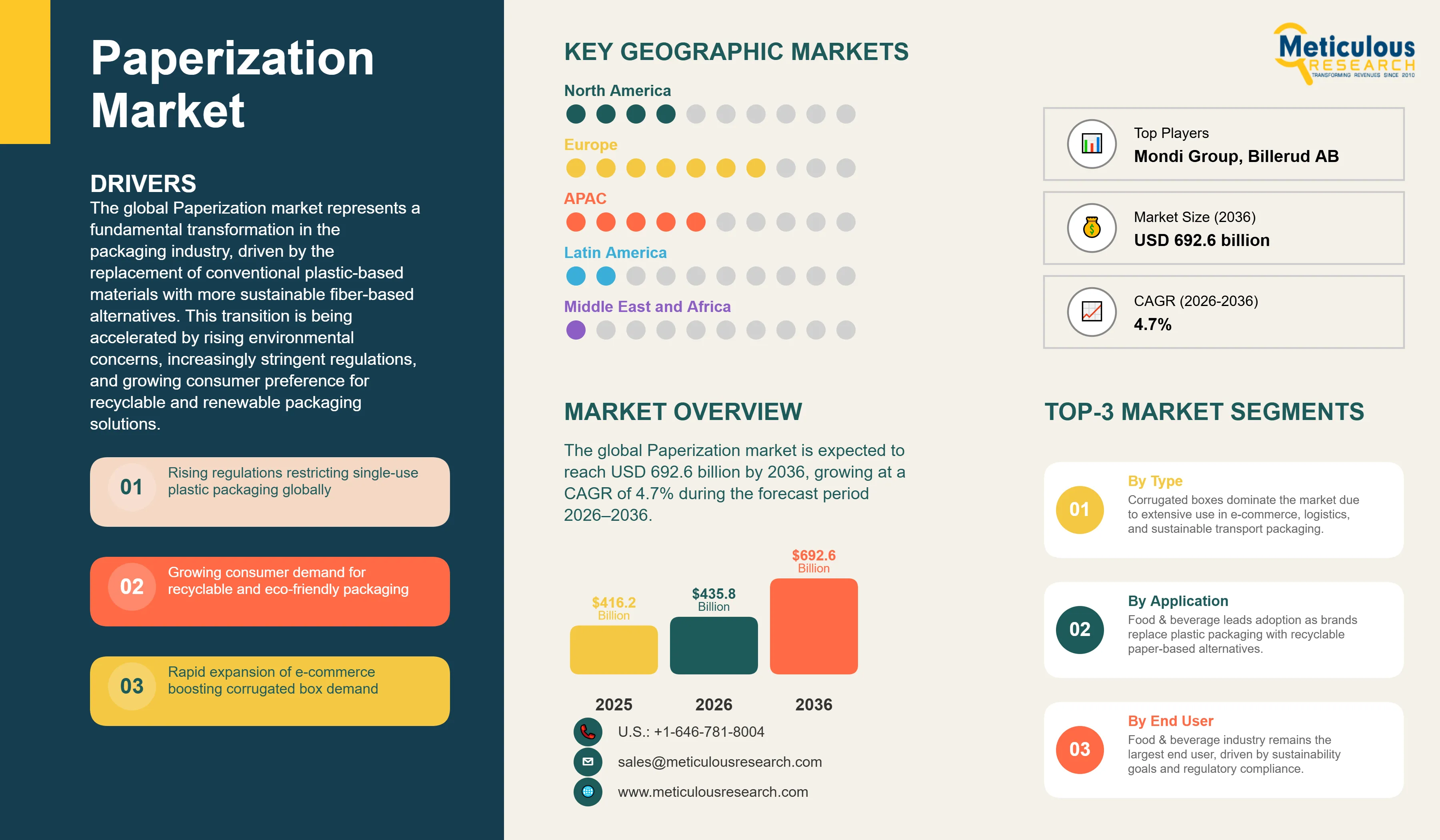

Report ID: MRCHM - 1042063 Pages: 277 Jun-2026 Formats*: PDF Category: Chemicals and Materials Delivery: 24 to 72 Hours Download Free Sample ReportThe global Paperization market is estimated to be USD 435.8 billion in 2026. This market is expected to reach USD 692.6 billion by 2036, growing at a CAGR of 4.7% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

The global Paperization market represents a fundamental transformation in the packaging industry, driven by the replacement of conventional plastic-based materials with more sustainable fiber-based alternatives. This transition is being accelerated by rising environmental concerns, increasingly stringent regulations, and growing consumer preference for recyclable and renewable packaging solutions. According to the OECD, global plastic waste more than doubled from 156 million tonnes in 2000 to 353 million tonnes in 2019, while only 9% of plastic waste was ultimately recycled, highlighting the need for alternative packaging materials.

Governments and regulatory bodies are further supporting the shift toward paper-based packaging. In the European Union, packaging accounts for approximately 40% of plastics consumption and around half of marine litter, prompting the implementation of the Packaging and Packaging Waste Regulation (PPWR), which aims to make all packaging placed on the EU market recyclable in an economically viable manner by 2030. In addition, EU legislation targets recycling rates of 85% for paper and cardboard packaging by 2030, reflecting strong policy support for fiber-based materials.

Paperization encompasses a broad range of technologies and products, including advanced barrier coatings, molded fiber packaging, folding cartons, liquid packaging cartons, and innovative paperboard structures that deliver functionality comparable to plastics while reducing environmental impact. Paper and cardboard already represent the largest packaging waste stream in Europe, accounting for approximately 40% of total packaging waste generated in 2021, underscoring their central role in circular economy initiatives. Consequently, the paperization market has emerged as a critical enabler of sustainable packaging strategies across food and beverage, e-commerce, healthcare, personal care, and consumer goods industries, supporting global efforts to minimize plastic waste and promote a circular economy.

Drivers: Accelerating the Transition to Circular Economies through Sustainable Paper-Based Packaging Solutions

A primary driver for the Paperization market is the increasing global emphasis on sustainability and the urgent need to reduce plastic waste. Governments and regulatory bodies worldwide are implementing stricter measures to curb single-use plastics. For example, the European Union's Single-Use Plastics Directive (SUPD) imposes restrictions on several disposable plastic products and has accelerated the adoption of fiber-based alternatives across food service, retail, and consumer goods applications. In addition, paper-based packaging benefits from strong end-of-life recovery systems. According to the European Paper Packaging Alliance, the recycling rate for paper and cardboard packaging in Europe reached approximately 83.2% in 2022, remaining among the highest recycling rates of all packaging materials and exceeding the EU's 2030 recycling target of 85% by only a narrow margin. The renewable nature and high recyclability of paper have made it an increasingly attractive option for environmentally conscious consumers and businesses. Furthermore, growing corporate sustainability commitments and packaging circularity goals among global brands are fostering innovation and accelerating the adoption of paperization solutions.

Restraints: Performance Limitations, Cost Implications, and Supply Chain Volatility

Despite the strong drivers, the Paperization market faces several restraints. A significant challenge lies in the inherent performance limitations of paper compared to certain plastics, particularly concerning moisture, grease, and oxygen barrier properties. While advancements in barrier coatings are addressing these issues, achieving comparable performance often comes with increased complexity and cost. The initial investment required for transitioning from plastic to paper-based packaging, including new machinery and specialized materials, can be substantial for manufacturers. Moreover, the increasing demand for pulp and fiber resources, driven by the paperization trend, could lead to supply chain volatility and price fluctuations, impacting the overall cost-effectiveness of paper-based solutions. The availability of high-quality recycled fiber also remains a concern in some regions.

Opportunities: Innovation in Barrier Coatings, Molded Fiber, and E-commerce Packaging

Significant opportunities in the Paperization market are arising from continuous advances in barrier coating technologies and fiber-based packaging formats. Innovations in bio-based and water-based barrier coatings are enabling paper materials to replace plastics in demanding applications such as food packaging by improving moisture, oxygen, and grease resistance while maintaining compatibility with established paper recycling streams. These developments are expanding the use of paper in applications that historically relied on multilayer plastic packaging.

The molded fiber packaging segment also presents substantial growth opportunities as manufacturers increasingly adopt sustainable alternatives to plastic trays, clamshells, and protective packaging used in food service and . In addition, the rapid expansion of e-commerce is generating strong demand for sustainable secondary packaging solutions, particularly corrugated boxes. According to the United Nations Conference on Trade and Development (UNCTAD), global e-commerce sales exceeded USD 27 trillion in 2022, highlighting the growing importance of packaging solutions for online retail. Furthermore, corrugated packaging benefits from highly developed recovery systems; the European Federation of Corrugated Board Manufacturers (FEFCO) estimates that corrugated packaging in Europe achieves recycling rates exceeding 80%. As brands seek to comply with evolving packaging regulations and meet consumer expectations for environmentally responsible deliveries, the adoption of paper-based packaging solutions is expected to accelerate.

Advancements in Sustainable Barrier Coatings

A pivotal trend in the Paperization market is the rapid advancement of sustainable barrier coatings that enable paper-based packaging to replace plastics in applications requiring moisture, oxygen, and grease resistance. The shift is being supported by circular economy regulations and strong recycling infrastructure. According to the European Commission, paper and cardboard packaging are subject to an 85% recycling target by 2030, encouraging the development of recyclable barrier technologies. In Europe, paper and cardboard packaging already achieved a recycling rate of approximately 83% in 2022, among the highest of all packaging materials, according to the European Paper Packaging Alliance (EPPA). Consequently, manufacturers are increasingly investing in water-based, bio-based, and dispersion coatings that maintain packaging performance while improving compatibility with existing paper recycling streams.

Growing Adoption of Molded Fiber Packaging

The market is witnessing increasing adoption of molded fiber packaging as brands seek sustainable alternatives to plastic trays, clamshells, and protective packaging. Molded fiber products are manufactured primarily from recycled paper and renewable fibers, supporting circular economy objectives. According to the American Forest & Paper Association (AF&PA), the paper recycling rate in the United States averaged nearly 65–69% in recent years, providing a stable feedstock base for recycled fiber packaging production. Furthermore, the Food and Agriculture Organization (FAO) estimates that global paper and paperboard production exceeded 410 million metric tons in 2023, highlighting the scale and availability of fiber resources supporting the expansion of molded fiber applications in food service, consumer electronics, and protective packaging.

Digitalization and Smart Packaging Integration

The integration of digitalization and smart packaging capabilities into paper-based solutions is an emerging trend across the packaging industry. Technologies such as QR codes, RFID, and NFC tags are improving traceability, authentication, and consumer engagement while supporting recycling initiatives. According to GS1, more than 2 billion GS1 barcodes are scanned globally every day, and the organization is driving the transition toward next-generation 2D codes capable of carrying richer product and sustainability information. In parallel, regulatory initiatives such as the European Union's Digital Product Passport framework are accelerating demand for intelligent packaging solutions that can enhance transparency, combat counterfeiting, and facilitate more efficient post-consumer recycling processes.

Analysis by Product Type

Based on product type, the corrugated boxes segment is expected to hold the largest share in 2026. Corrugated boxes are indispensable for shipping, logistics, and e-commerce, offering robust protection and high recyclability. The molded fiber segment is projected to grow at the fastest CAGR, driven by its versatility as a sustainable alternative to plastic in various applications, including food service, electronics, and medical packaging. Other significant product types include folding cartons, liquid packaging cartons, and paper bags, all contributing to the broader paperization trend.

Analysis by Application

By application, the food & beverage segment is expected to account for the largest share in 2026. This dominance is primarily due to stringent regulations targeting single-use plastics in food service and the increasing consumer demand for sustainable food packaging. The e-commerce segment is projected to witness rapid growth, driven by the need for lightweight, protective, and eco-friendly packaging solutions for online deliveries. Other key applications include personal care & cosmetics, healthcare, and industrial packaging, where paper-based solutions are gaining traction.

Analysis by Technology

By technology, the molding segment, particularly for molded fiber products, is expected to grow at the fastest CAGR. This technology offers cost-effective and sustainable alternatives to plastic for various trays, inserts, and containers. The coating & lamination segment, encompassing barrier coatings and other functional layers, holds a significant share due to its critical role in enhancing the performance of paper-based packaging for demanding applications. Printing and converting technologies also play a vital role in customizing and finishing paper packaging solutions.

Analysis by End User

By end user, the food & beverage industry is expected to hold the largest share in 2026, driven by the massive volume of packaging required for consumables and the strong push for sustainability in this sector. The retail & e-commerce sector is also a significant end-user, with a growing demand for paper-based packaging for product presentation and shipping. Other end-user segments include consumer goods, industrial manufacturing, and healthcare, all increasingly adopting paperization solutions to meet environmental goals and regulatory compliance.

Europe

Europe is expected to dominate the global Paperization market in 2026, supported by its stringent regulatory framework and well-established circular economy initiatives. Policies such as the EU Single-Use Plastics Directive (SUPD) and the Packaging and Packaging Waste Regulation (PPWR) have accelerated the adoption of paper-based alternatives across food service, retail, and consumer goods applications. According to the European Commission, packaging accounts for approximately 40% of plastics consumption in the EU, making it a key focus area for sustainability initiatives. In addition, the European Paper Packaging Alliance (EPPA) reported that paper and cardboard packaging achieved a recycling rate of approximately 83% in Europe in 2022, among the highest recycling rates of any packaging material. Coupled with strong consumer preference for environmentally friendly products and the presence of leading packaging manufacturers such as Smurfit Westrock, Mondi, and Stora Enso, these factors position Europe as the leading region in the global paperization market.

North America

North America is projected to witness significant growth in the Paperization market, driven by rising consumer awareness, expanding sustainability commitments, and increasing restrictions on single-use plastics at the state and municipal levels. Several U.S. states, including California, New York, and Colorado, have implemented legislation aimed at reducing plastic waste, encouraging the adoption of recyclable paper-based packaging solutions. According to the American Forest & Paper Association (AF&PA), the United States maintained a paper recycling rate of approximately 65–69% in recent years, providing a strong foundation for circular fiber-based packaging systems. Furthermore, the U.S. Census Bureau reported that e-commerce sales exceeded USD 1.19 trillion in 2024, supporting robust demand for corrugated boxes and other paper-based packaging formats. Major consumer goods and retail brands are also increasing investments in sustainable packaging to meet corporate environmental targets and evolving consumer expectations, further accelerating regional market growth.

Asia Pacific

Asia Pacific is expected to be the fastest-growing region in the Paperization market, fueled by rapid industrialization, increasing disposable incomes, and growing environmental concerns in countries like China, India, and Japan. While the region still faces challenges in waste management infrastructure, governments are increasingly implementing policies to reduce plastic pollution, driving demand for paper-based alternatives. The vast consumer base and the rise of e-commerce platforms are also contributing to the demand for sustainable packaging solutions, making it a key growth hub for paperization.

Latin America

The Latin American Paperization market is expected to experience steady growth, driven by increasing environmental awareness, evolving regulatory landscapes, and the expansion of the food & beverage sector. Countries in the region are gradually adopting policies to curb plastic waste, leading to a growing demand for paper-based packaging solutions. Investments in sustainable packaging technologies and the entry of international players are further contributing to market expansion.

Middle East & Africa

The Middle East & Africa Paperization market is anticipated to grow, albeit at a slower pace, influenced by increasing government initiatives to promote sustainability and diversify economies away from fossil fuels. While the adoption of paper-based packaging is still in its nascent stages in some parts of the region, growing environmental consciousness and the expansion of the retail sector are expected to drive demand for sustainable packaging solutions in the coming years.

The global Paperization market is characterized by a mix of established packaging giants and innovative startups, all vying for market share through product innovation, strategic partnerships, and sustainability initiatives. Key players are investing heavily in research and development to enhance the barrier properties of paper-based materials, develop advanced molded fiber solutions, and integrate digital technologies for improved traceability and consumer engagement. Strategic collaborations between material suppliers, packaging converters, and brand owners are crucial for accelerating the adoption of paperization solutions across various end-use industries. The competitive landscape is dynamic, with a strong emphasis on developing cost-effective and high-performance alternatives to traditional plastic packaging.

Mondi Group, Smurfit Westrock plc, Stora Enso, International Paper, Metsä Board, Georgia-Pacific, Huhtamäki, Graphic Packaging International, Billerud AB, Sonoco Products, Pratt Industries, Cascades, Mayr-Melnhof Karton, Nippon Paper Industries, Oji Holdings, UPM-Kymmene, Packaging Corporation of America, Rengo Co., Ltd., SIG Group AG, Tetra Pak International

The global Paperization market is estimated to be USD 435.8 billion in 2026.

Key drivers include stringent environmental regulations (e.g., EU SUPD), increasing consumer demand for sustainable packaging, and corporate sustainability commitments.

Restraints include performance limitations of paper compared to plastics, higher initial costs of transition, and potential supply chain volatility for pulp and fiber resources.

Opportunities lie in continuous innovation in sustainable barrier coatings, the growing adoption of molded fiber packaging, and the increasing demand from the e-commerce sector for eco-friendly solutions.

The corrugated boxes segment is expected to hold the largest share due to its widespread use in shipping and logistics.

The food & beverage segment is projected to account for the largest share, driven by regulations against single-use plastics and consumer preferences.

Europe is expected to dominate the market due to its stringent regulatory environment and advanced recycling infrastructure.

Asia Pacific is projected to witness the fastest growth, fueled by rapid industrialization and increasing environmental awareness.

The top 3 manufacturers are Mondi Group, Smurfit Kappa Group, and Stora Enso.

Key trends include advancements in sustainable barrier coatings, growing adoption of molded fiber packaging, and the integration of digitalization and smart packaging features.

Published Date: May-2026

Published Date: May-2026

Published Date: May-2026

Published Date: Apr-2026

Published Date: Apr-2026

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates