Resources

About Us

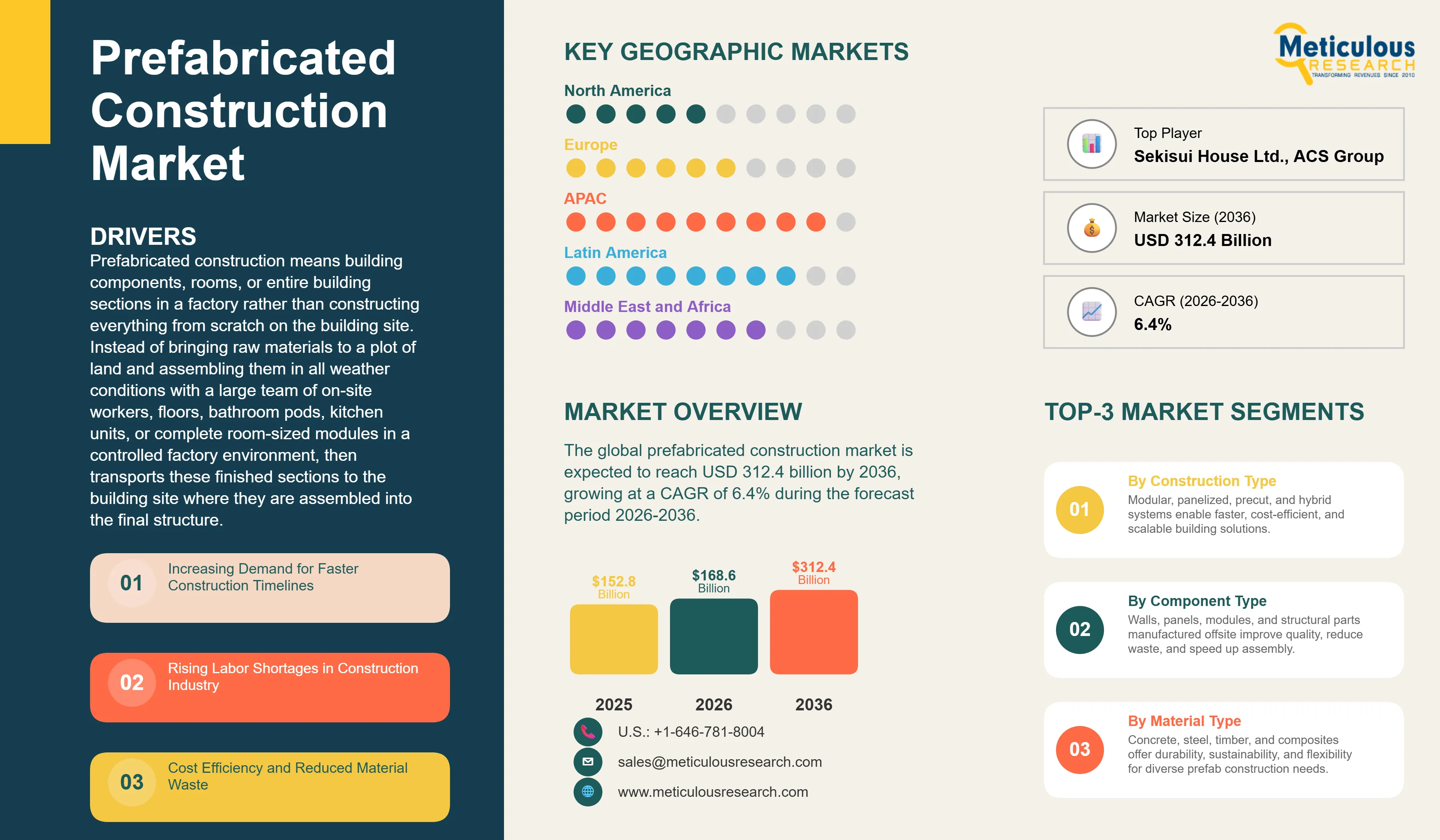

The global prefabricated construction market was valued at USD 152.8 billion in 2025. This market is expected to reach USD 312.4 billion by 2036 from an estimated USD 168.6 billion in 2026, growing at a CAGR of 6.4% during the forecast period 2026-2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Prefabricated construction means building components, rooms, or entire building sections in a factory rather than constructing everything from scratch on the building site. Instead of bringing raw materials to a plot of land and assembling them in all weather conditions with a large team of on-site workers, a prefabricated construction company builds walls, floors, bathroom pods, kitchen units, or complete room-sized modules in a controlled factory environment, then transports these finished sections to the building site where they are assembled into the final structure. Think of it like manufacturing a car on an assembly line rather than building it in the customer's driveway. The factory setting allows for better quality control, less material waste, faster production through parallel working, and much reduced dependence on on-site labor. A building that would take 18 months to construct using traditional methods can often be assembled on site in a fraction of that time when the components arrive pre-finished from a factory.

The market is growing because the construction industry globally is facing a serious and worsening combination of challenges that traditional building methods are increasingly unable to address effectively. Construction labor shortages are severe in most developed markets as skilled tradespeople retire and younger workers choose other industries, driving up labor costs and causing project delays. The demand for new housing in cities around the world far outstrips current supply, creating housing affordability crises in major metropolitan areas that governments are under pressure to address quickly. Material costs are volatile and project cost overruns are common in traditional construction. Clients in healthcare, education, and data center construction need buildings delivered on tight schedules that conventional construction regularly misses. Prefabrication addresses all of these challenges simultaneously by moving most of the work off site into a controlled manufacturing environment where productivity is higher, quality is more consistent, schedules are more predictable, and labor requirements on site are dramatically reduced.

Two particularly significant opportunities are shaping the market's development. The integration of digital building information modeling technology with prefabricated construction is transforming how buildings are designed and coordinated, allowing architects and engineers to design in three-dimensional digital models that directly drive the manufacturing specifications for prefabricated components, reducing design errors, eliminating clashes between different building systems, and dramatically reducing the rework and waste that plague traditional construction projects. In addition, the rapid growth of cross-laminated timber and mass timber construction as a sustainable prefabricated building material is opening significant new market opportunities, particularly for mid-rise residential and commercial buildings where timber's sustainability credentials, its prefabrication compatibility, and its impressive structural performance relative to its weight are attracting developers seeking green building certifications and sustainable construction credentials.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 312.4 Billion |

|

Market Size in 2026 |

USD 168.6 Billion |

|

Market Size in 2025 |

USD 152.8 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 6.4% |

|

Dominating Construction Type |

Modular Construction |

|

Fastest Growing Construction Type |

Hybrid Prefabrication Systems |

|

Dominating Component Type |

Walls and Panels |

|

Fastest Growing Component Type |

Complete Modules/Units |

|

Dominating Material Type |

Concrete |

|

Fastest Growing Material Type |

Wood (Timber/CLT) |

|

Dominating Application |

Residential Construction |

|

Fastest Growing Application |

Industrial Construction |

|

Dominating End User |

Real Estate Developers |

|

Fastest Growing End User |

Government and Public Sector |

|

Dominating Project Type |

New Construction |

|

Fastest Growing Project Type |

Renovation and Retrofit |

|

Dominating Geography |

Asia-Pacific |

|

Fastest Growing Geography |

Middle East & Africa |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Housing Shortage Crisis Driving Government-Backed Prefab Adoption

The severe housing affordability and supply crisis affecting major cities across the United Kingdom, Australia, the United States, Canada, and Singapore is creating strong government policy support for prefabricated and modular construction as one of the most practical and rapidly deployable solutions available. Traditional construction simply cannot build housing fast enough, at low enough cost, or with the limited available skilled labor to address the scale of undersupply in these markets. The UK government has set targets for dramatically increased housing output that conventional housebuilders cannot meet without adopting offsite construction methods, and government bodies including Homes England have specifically endorsed modular construction as a priority delivery vehicle for affordable housing programs. Singapore's Housing Development Board has been one of the world's most advanced and long-standing adopters of prefabricated construction for public housing, with PPVC (Prefabricated Prefinished Volumetric Construction) now mandated for new public housing developments to address the labor shortage and speed requirements of its urban housing programs.

The combination of government mandate, housing supply urgency, and growing developer confidence in prefabricated construction quality is creating a demand environment in the housing sector that is driving rapid growth in modular and panelized residential construction capacity. Companies including Sekisui House and Daiwa House in Japan, which deliver a very large proportion of Japan's new housing output through factory-built systems, demonstrate that prefabricated residential construction can become the industry standard rather than a niche alternative when the right market conditions exist. The trajectory of government housing policy in multiple developed countries increasingly points toward the mandatory or strongly incentivized adoption of offsite construction methods for publicly funded housing, creating a large and policy-secured demand base for prefabricated construction capacity through the forecast period.

Mass Timber and CLT Creating a New Premium Prefabricated Construction Category

Cross-laminated timber and mass timber construction have emerged over the past decade from a Nordic specialty into a globally recognized and commercially significant prefabricated construction material that is transforming the design possibilities for mid-rise and tall timber buildings. CLT panels are manufactured in factories by bonding layers of structural timber at alternating grain directions to create large, dimensionally stable panels that can be used for floors, walls, and roofs in buildings of six to twenty or more storeys. The CLT panels are precision-cut to exact dimensions by computer-controlled machines in the factory, delivered to site, and assembled rapidly by crane with minimal on-site labor, delivering the speed and labor efficiency benefits of prefabrication in an inherently sustainable material whose carbon is sequestered in the structure for the building's lifetime.

The mass timber construction market is growing at a significantly faster rate than the broader prefabricated construction market, driven by the strong sustainability credentials of timber buildings that support green building certification requirements and corporate environmental targets, the aesthetic appeal of exposed timber interiors that is creating premium market positioning for CLT residential and office buildings, and the growing regulatory acceptance of tall timber buildings in building codes that had previously restricted timber to low-rise construction. Skanska, Lendlease, and Laing O'Rourke are among the large construction groups investing in mass timber construction capabilities, and specialist CLT panel manufacturers including Binderholz, Stora Enso, and Mayr-Melnhof are scaling production capacity in response to rapidly growing demand from both Europe and North American markets.

Logistics Hubs and E-Commerce Driving Industrial Prefab Growth

The extraordinary growth of e-commerce fulfillment and logistics infrastructure globally, with Amazon, DHL, FedEx, and hundreds of other logistics and retail companies building large networks of distribution centers, warehouses, and last-mile fulfillment facilities, has become one of the most commercially important demand drivers for prefabricated industrial construction. The scale and speed at which these logistics facilities need to be built to support growing e-commerce delivery expectations makes prefabricated steel structure and panelized building systems the natural construction method of choice: standardized warehouse and distribution center designs can be largely prefabricated in factories with minimal variation, and the industry's preference for rapid building delivery to operational status makes the 30 to 50% schedule reduction that prefabricated industrial construction delivers over traditional construction extremely commercially valuable.

The data center construction market is another very rapidly growing driver of industrial prefabricated construction, with hyperscale data center operators including Amazon Web Services, Microsoft Azure, Google Cloud, and Meta building enormous data center campuses globally on accelerated schedules that traditional construction methods cannot meet. Prefabricated data center modules, where cooling, power distribution, server rack infrastructure, and building structure are integrated in factory-built modules that can be deployed as self-contained units and rapidly connected to form larger facilities, have become the dominant construction methodology for hyperscale data center development, creating a large and fast-growing specialized segment within the broader industrial prefabricated construction market.

Increasing Demand for Faster Construction Timelines

The primary driver of the prefabricated construction market is the construction industry's growing inability to meet client schedule requirements and market delivery timelines using traditional on-site construction methods, creating structural demand for the 30 to 50% schedule reductions that prefabricated construction can deliver across most project types. Hospital construction projects that are needed urgently to address healthcare capacity shortages cannot wait the three to five years that traditional construction requires. Hotel developers need to open new properties during peak travel seasons and cannot afford schedule overruns that miss opening targets by months. Government infrastructure programs are held to delivery commitments by electoral timelines. Data center operators are competing to deliver capacity for cloud services customers who have signed capacity reservation agreements with specific operational dates. In all of these cases, the faster and more predictable construction schedule that prefabrication delivers through parallel factory manufacturing and simplified on-site assembly translates directly into measurable commercial or operational value that clients are willing to pay a premium for, creating durable demand for prefabricated construction solutions across multiple application sectors.

Rising Labor Shortages in Construction Industry

The construction industry is experiencing a severe and structural labor shortage in most developed markets, driven by the retirement of an aging skilled workforce without sufficient replacement from younger generations, the physical demands and outdoor working conditions of construction that reduce its attractiveness relative to other career options, and the cyclical nature of construction employment that discourages long-term workforce commitment. In the United States, the Associated Builders and Contractors estimated a shortage of over 500,000 construction workers in 2023. The UK construction industry faces critical skills shortages in trades including bricklaying, plastering, and roofing. Japan, Germany, and Australia all face similar skilled construction labor deficits. Prefabricated construction directly addresses this challenge by moving the majority of construction activity from site to factory, where work can be performed in a controlled environment by a more stable manufacturing workforce with less dependence on the specific skilled trades that are in shortest supply. A modular building factory can produce housing units with a much smaller and differently skilled workforce than would be required to build the same housing conventionally on site, allowing output to be maintained or expanded despite the tight labor market.

Integration with BIM and Digital Construction Technologies

The integration of building information modeling with prefabricated construction manufacturing represents the most commercially transformative technology opportunity in the market, creating end-to-end digital workflows where a building is designed in a three-dimensional digital model that directly generates the manufacturing instructions for each prefabricated component, eliminating the manual translation steps that previously created errors and inefficiencies between design and fabrication. When an architect designs a building in BIM software and every prefabricated wall panel, floor cassette, and structural module is generated directly from that model with accurate dimensions, connection details, and coordination checks against all other building systems, the potential for expensive on-site clashes between structural, mechanical, and electrical components is dramatically reduced. Projects that implement full BIM-to-fabrication digital workflows consistently report significant reductions in design changes during construction, faster approval of shop drawings, and fewer unexpected coordination problems during assembly. Laing O'Rourke's advanced engineering enterprise approach and Skanska's digital construction programs demonstrate how leading contractors are using BIM integration with prefabrication to achieve consistent project delivery improvements that generate competitive advantage and client confidence.

Growth in Sustainable and Green Building Solutions

Prefabricated construction offers measurable sustainability advantages over traditional construction that are becoming increasingly commercially valuable as corporate sustainability commitments, green building certification requirements, and environmental regulations tighten across most major markets. Factory-based construction generates significantly less material waste than site construction, where offcuts, damaged materials, and weather-exposed unused materials contribute to typical on-site waste rates of 10 to 15% of material purchased. Prefabricated construction reduces on-site construction period, which reduces noise, dust, vehicle movements, and community disruption in urban areas. The precision manufacturing of prefabricated components allows better insulation installation quality control, tighter building envelopes, and more consistent energy performance than site-built construction where quality varies with worker skill and weather conditions. Mass timber prefabricated construction specifically offers very strong carbon credentials because the biogenic carbon stored in the timber structure offsets much or all of the building's embodied carbon. Developers seeking LEED, BREEAM, or Green Star certification, and corporations building to net-zero carbon commitments, are finding that prefabricated construction is a very effective way to improve the sustainability performance of their building projects compared with conventional construction.

By Construction Type: In 2026, Modular Construction to Dominate

Based on construction type, the global prefabricated construction market is segmented into modular construction, panelized construction, precut construction, and hybrid prefabrication systems. In 2026, the modular construction segment is expected to account for the largest share of the global prefabricated construction market. Modular construction, which creates three-dimensional room-sized units in a factory and stacks or connects them on site to form the complete building, delivers the most complete level of prefabrication and therefore the largest schedule and labor savings of any construction type. The growing commercial application of modular construction to hotels, student accommodation, healthcare facilities, and multi-family residential buildings, where highly repetitive floor plans justify the upfront investment in module design and factory setup, has established modular construction as the dominant high-value segment within the prefabricated construction market.

However, the hybrid prefabrication systems segment is projected to register the highest CAGR during the forecast period. Hybrid approaches that combine prefabricated elements such as structural panels, bathroom and kitchen pods, and pre-fitted service modules with traditional construction for other building elements are proving to be the most practically accessible entry point for contractors and developers who want to gain the schedule and labor benefits of prefabrication without committing to fully modular construction. As more construction companies develop experience with hybrid prefabrication and as the supply of prefabricated components expands, the market for partial prefabrication solutions is growing faster than fully modular approaches.

By Material Type: In 2026, Concrete to Hold the Largest Share

Based on material type, the global prefabricated construction market is segmented into concrete, steel, wood (timber/CLT), glass and composite materials, and other materials. In 2026, the concrete segment is expected to account for the largest share of the overall market. Precast concrete elements including wall panels, floor planks, columns, beams, and stairs represent the largest and most globally widespread form of prefabricated construction component, used extensively in residential apartment construction, commercial buildings, infrastructure, and industrial facilities across all major markets. The combination of concrete's structural performance, fire resistance, acoustic properties, and cost-effectiveness with the productivity and quality benefits of factory precasting makes precast concrete the dominant prefabricated construction material by volume and value.

However, the wood (timber/CLT) segment is projected to register the highest CAGR during the forecast period. The rapidly growing mass timber and CLT construction market, driven by sustainability credentials, design innovation, and regulatory changes enabling taller timber buildings, is making timber prefabricated construction one of the fastest-growing segments in the broader prefabricated market. Significant investment in CLT manufacturing capacity across Europe, North America, and Australia is expanding the supply of prefabricated timber components to meet rapidly growing demand.

By Application: In 2026, Residential Construction to Hold the Largest Share

Based on application, the global prefabricated construction market is segmented into residential construction, commercial construction, industrial construction, institutional construction, and infrastructure and public projects. In 2026, the residential construction segment is expected to account for the largest share of the overall market. Housing represents by far the largest single application for prefabricated construction globally by both unit volume and total value. Japan leads the world in prefabricated residential construction adoption with over 15% of new homes built using factory-based methods through companies including Sekisui House and Daiwa House. Scandinavia, Germany, and Australia have significant and growing prefabricated residential construction sectors. The acute housing supply crisis in the UK, Canada, and Australia is driving strong government policy support for factory-built homes that is expected to accelerate residential prefab adoption substantially through the forecast period.

However, the industrial construction segment is projected to register the highest CAGR during the forecast period. The explosive growth of e-commerce distribution infrastructure, hyperscale data centers, and manufacturing facility construction globally is creating very large and fast-growing demand for prefabricated steel structural and panelized building systems in the industrial sector. The standardized, repetitive nature of most warehouse and data center building designs makes industrial construction particularly well-suited to prefabrication, and the industry's intense schedule sensitivity creates strong willingness to use prefabricated methods that can deliver on tighter timelines.

By End User: In 2026, Real Estate Developers to Hold the Largest Share

Based on end user, the global market is segmented into real estate developers, government and public sector, construction companies, and industrial enterprises. In 2026, the real estate developers segment is expected to account for the largest share of the global prefabricated construction market. Real estate developers are the primary procurers of new construction across residential, commercial, and mixed-use sectors, and their adoption of prefabricated construction methods for new developments is the dominant revenue driver in the market. Developers motivated by the competitive advantages of faster project delivery, more predictable construction costs, and lower on-site labor requirements are progressively shifting their project specifications toward prefabricated solutions.

However, the government and public sector segment is projected to register the highest CAGR during the forecast period. Governments facing housing supply crises, healthcare infrastructure backlogs, and school building programs are increasingly mandating or strongly incentivizing prefabricated construction methods to accelerate delivery and improve cost predictability. Singapore's HDB public housing program, the UK's government-backed affordable housing programs, and Australia's defense and public infrastructure construction programs represent large government-led procurement pipelines that are growing rapidly.

Prefabricated Construction Market by Region: Asia-Pacific Leading by Share, Middle East and Africa by Growth

Based on geography, the global prefabricated construction market is segmented into Asia-Pacific, North America, Europe, Latin America, and the Middle East and Africa.

In 2026, Asia-Pacific is expected to account for the largest share of the global overall market. The region's dominance reflects both the extraordinary scale of construction activity in China and the highly advanced prefabricated construction industry of Japan. China is by far the world's largest construction market by volume and is undergoing a significant shift toward prefabricated construction driven by government policy mandates requiring prefab methods in public housing and large infrastructure projects in major cities, combined with severe urban construction site labor management challenges and a national policy push for construction industrialization. China's State Council has set explicit targets for the proportion of new construction using prefabricated methods, creating a policy-driven demand signal across the country's enormous construction industry. Japan's Sekisui House and Daiwa House are among the world's most technologically advanced and commercially successful prefabricated house builders, having delivered millions of factory-built homes over several decades. South Korea, Singapore, and Australia all have significant and growing prefabricated construction markets driven by housing supply pressures, government mandates, and advanced local manufacturing capabilities.

However, the Middle East and Africa region is expected to grow at the fastest CAGR during the forecast period. The Middle East, particularly Saudi Arabia and the UAE, is experiencing an unprecedented wave of mega-project construction as part of Vision 2030 and similar national transformation programs that are building entirely new cities, tourism destinations, industrial zones, and infrastructure networks on an accelerated timeline that conventional construction methods cannot support alone. Saudi Arabia's NEOM project, The Line, Qiddiya, and numerous other giga-projects collectively represent hundreds of billions of dollars of construction that must be delivered on politically important timelines, making prefabricated construction methods for housing, hospitality, and support infrastructure practically necessary rather than optional. The UAE's continued commercial real estate and hospitality construction pipeline, including the rapid build-out of hotel and residential capacity associated with Dubai's continuing tourism growth, is creating large-scale demand for prefabricated construction systems. Red Sea Global, the Saudi developer of the Red Sea Project and Amaala tourism developments, has committed to using modular and prefabricated construction methods to meet its ambitious delivery schedules.

Europe is a technically sophisticated and environmentally progressive prefabricated construction market, with particularly strong positions in Scandinavia, Germany, the Netherlands, and the UK. Sweden and Norway have among the highest prefabricated housing adoption rates in Europe, with a long tradition of timber-frame factory-built homes. Germany has a well-developed precast concrete and modular construction industry serving both residential and commercial sectors. The UK's government-backed affordable housing modernization agenda and the strong corporate sustainability targets of UK commercial real estate developers are driving growing adoption of offsite construction methods. North America is a large and growing market with the U.S. modular construction industry serving healthcare, hospitality, and multifamily residential sectors, and Canada's growing adoption of prefabricated construction methods for housing programs in response to its severe housing affordability crisis.

The prefabricated construction market includes large integrated construction and property companies that have built prefabrication capabilities into their construction delivery, specialist prefabricated building manufacturers focused on specific market segments, and national construction champions with advanced factory building capabilities serving their domestic markets. Competition is based on the quality and speed of construction delivery, the breadth and customizability of prefabricated building product offerings, geographic reach and logistics capability, financial strength for large project execution, and the digital design and manufacturing integration capabilities that differentiate leading players from commodity competitors.

Laing O'Rourke has built what it describes as a disruptive offsite manufacturing capability through its Explore Industrial Park facility in the UK, which produces complete building components for its major construction projects, and has established a strong reputation for technology-led prefabricated construction delivery on complex healthcare, education, and commercial projects. Bouygues Construction and Skanska are among the largest European construction groups with significant and growing prefabricated construction divisions. Sekisui House and Daiwa House dominate Japan's prefabricated residential construction market with decades of operational excellence and continuous technology development in factory-built housing. Lendlease has made significant investments in modular construction for high-rise residential and commercial buildings across Australia, the US, and the UK. Kiewit and VINCI Construction serve large infrastructure and commercial construction markets with advanced prefabrication capabilities.

The report provides a comprehensive competitive analysis based on a thorough review of leading players' construction capabilities, project portfolios, geographic presence, and recent strategic developments. Some of the key players operating in the global prefabricated construction market include Laing O'Rourke (UK), Bouygues Construction (France), Skanska AB (Sweden), Daiwa House Industry Co. Ltd. (Japan), Sekisui House Ltd. (Japan), Red Sea Global (Saudi Arabia), Lendlease Corporation (Australia), Kiewit Corporation (U.S.), VINCI Construction (France), Balfour Beatty plc (UK), ACS Group (Spain), Larsen & Toubro Limited (India), Tata Projects Limited (India), Hickory Group (Australia), and Modscape Pty Ltd. (Australia), among others.

The global prefabricated construction market is expected to reach USD 312.4 billion by 2036 from an estimated USD 168.6 billion in 2026, at a CAGR of 6.4% during the forecast period 2026-2036.

In 2026, the modular construction segment is expected to hold the largest share of the global prefabricated construction market, driven by the hotel, student accommodation, healthcare, and multi-family residential sectors' adoption of three-dimensional room-sized modular units that deliver the largest schedule and labor savings of any prefabrication approach.

The hybrid prefabrication systems segment is expected to register the highest CAGR during the forecast period 2026-2036, driven by hybrid approaches combining prefabricated elements with traditional construction being the most accessible entry point for contractors and developers, allowing partial adoption of prefabrication benefits without the full commitment of entirely modular construction.

In 2026, the residential construction segment is expected to hold the largest share of the global prefabricated construction market, reflecting housing being by far the largest single application for prefabricated construction globally by both unit volume and total value, with Japan, China, and Scandinavia leading adoption rates.

Asia-Pacific is expected to dominate the global prefabricated construction market in 2026, driven by China's enormous construction volumes and government mandates for construction industrialization, Japan's world-leading prefabricated residential construction industry through Sekisui House and Daiwa House, and the large construction programs of South Korea, Singapore, and Australia.

The market is primarily driven by the construction industry's growing inability to meet delivery timelines and output requirements using traditional methods as labor shortages worsen and client schedule requirements tighten, and by the acute housing supply crisis in major cities across the UK, Australia, Canada, and other developed markets that is driving government policy mandates for faster housing delivery through prefabricated and offsite construction methods.

Key players are Laing O'Rourke (UK), Bouygues Construction (France), Skanska AB (Sweden), Daiwa House Industry Co. Ltd. (Japan), Sekisui House Ltd. (Japan), Red Sea Global (Saudi Arabia), Lendlease Corporation (Australia), Kiewit Corporation (U.S.), VINCI Construction (France), Balfour Beatty plc (UK), ACS Group (Spain), Larsen & Toubro Limited (India), Tata Projects Limited (India), Hickory Group (Australia), and Modscape Pty Ltd. (Australia), among others.

The Middle East and Africa region is expected to register the highest growth rate in the global prefabricated construction market during the forecast period 2026-2036, driven by Saudi Arabia's Vision 2030 giga-projects including NEOM that require prefabricated construction methods to meet their ambitious delivery timelines, and the UAE's continued large-scale hotel, residential, and commercial construction activity.

1. Introduction

1.1 Market Definition

1.2 Market Ecosystem

1.3 Currency and Limitations

1.3.1 Currency

1.3.2 Limitations

1.4 Key Stakeholders

2. Research Methodology

2.1 Research Approach

2.2 Data Collection & Validation Process

2.2.1 Secondary Research

2.2.2 Primary Research & Validation

2.2.2.1 Primary Interviews with Experts

2.2.2.2 Approaches for Country-/Region-Level Analysis

2.3 Market Estimation

2.3.1 Bottom-Up Approach

2.3.2 Top-Down Approach

2.3.3 Growth Forecast

2.4 Data Triangulation

2.5 Assumptions for the Study

3. Executive Summary

4. Market Overview

4.1 Introduction

4.2 Market Dynamics

4.2.1 Drivers

4.2.1.1 Increasing Demand for Faster Construction Timelines

4.2.1.2 Rising Labor Shortages in Construction Industry

4.2.1.3 Cost Efficiency and Reduced Material Waste

4.2.1.4 Growth in Urbanization and Infrastructure Development

4.2.2 Restraints

4.2.2.1 High Initial Design and Setup Costs

4.2.2.2 Transportation and Logistics Constraints

4.2.2.3 Limited Customization Perception

4.2.3 Opportunities

4.2.3.1 Adoption of Modular and Offsite Construction Techniques

4.2.3.2 Integration with BIM and Digital Construction Technologies

4.2.3.3 Growth in Sustainable and Green Building Solutions

4.2.3.4 Expansion in Emerging Markets

4.2.4 Challenges

4.2.4.1 Regulatory and Building Code Variability

4.2.4.2 Supply Chain and Project Coordination Complexity

4.3 Technology Landscape

4.3.1 Modular Construction Technologies

4.3.2 Panelized Construction Systems

4.3.3 3D Volumetric Construction

4.3.4 Digital Design and BIM Integration

4.3.5 Robotics and Automation in Offsite Construction

4.4 Prefabricated Construction Ecosystem

4.4.1 Design and Engineering (BIM, Digital Twin)

4.4.2 Manufacturing and Fabrication

4.4.3 Transportation and Logistics

4.4.4 On-Site Assembly and Installation

4.4.5 Project Management and Integration

4.5 Value Chain Analysis

4.5.1 Raw Material Suppliers

4.5.2 Prefabrication Manufacturers

4.5.3 Contractors and Builders

4.5.4 Developers and Real Estate Companies

4.5.5 End Users

4.6 Regulatory and Standards Landscape

4.6.1 Building Codes and Compliance Standards

4.6.2 Sustainability and Green Building Regulations

4.6.3 Modular Construction Standards

4.7 Porter’s Five Forces Analysis

4.8 Investment and Industry Trends

4.8.1 Growth in Offsite Construction Investments

4.8.2 Public Infrastructure Projects

4.8.3 Adoption of Smart and Sustainable Construction

4.9 Cost and Pricing Analysis

4.9.1 Cost Comparison: Prefabricated vs Traditional Construction

4.9.2 Cost by Construction Type

4.9.3 Lifecycle Cost Benefits

5. Prefabricated Construction Market, by Construction Type

5.1 Introduction

5.2 Modular Construction

5.2.1 Permanent Modular Construction

5.2.2 Relocatable Modular Buildings

5.3 Panelized Construction

5.3.1 Structural Panels

5.3.2 Insulated Panels

5.4 Precut Construction

5.5 Hybrid Prefabrication Systems

6. Prefabricated Construction Market, by Component Type

6.1 Introduction

6.2 Walls and Panels

6.3 Floors and Roofs

6.4 Columns and Beams

6.5 Staircases and Structural Components

6.6 Complete Modules/Units

7. Prefabricated Construction Market, by Material Type

7.1 Introduction

7.2 Concrete

7.3 Steel

7.4 Wood (Timber/CLT)

7.5 Glass and Composite Materials

7.6 Other Materials

8. Prefabricated Construction Market, by Application

8.1 Introduction

8.2 Residential Construction

8.2.1 Single-Family Housing

8.2.2 Multi-Family Housing

8.2.3 Affordable Housing Projects

8.3 Commercial Construction

8.3.1 Office Buildings

8.3.2 Retail Spaces

8.3.3 Hospitality (Hotels)

8.4 Industrial Construction

8.4.1 Warehouses and Logistics Centers

8.4.2 Manufacturing Facilities

8.5 Institutional Construction

8.5.1 Healthcare Facilities

8.5.2 Educational Buildings

8.6 Infrastructure and Public Projects

8.6.1 Transportation Infrastructure

8.6.2 Public Utilities and Government Buildings

9. Prefabricated Construction Market, by End User

9.1 Introduction

9.2 Real Estate Developers

9.3 Government and Public Sector

9.4 Construction Companies

9.5 Industrial Enterprises

10. Prefabricated Construction Market, by Project Type

10.1 Introduction

10.2 New Construction

10.3 Renovation and Retrofit

11. Prefabricated Construction Market, by Geography

11.1 Introduction

11.2 North America

11.2.1 U.S.

11.2.2 Canada

11.3 Europe

11.3.1 Germany

11.3.2 U.K.

11.3.3 France

11.3.4 Netherlands

11.3.5 Sweden

11.3.6 Norway

11.3.7 Italy

11.3.8 Spain

11.3.9 Rest of Europe

11.4 Asia-Pacific

11.4.1 China

11.4.2 Japan

11.4.3 India

11.4.4 South Korea

11.4.5 Australia

11.4.6 Singapore

11.4.7 Indonesia

11.4.8 Vietnam

11.4.9 Rest of Asia-Pacific

11.5 Latin America

11.5.1 Brazil

11.5.2 Mexico

11.5.3 Argentina

11.5.4 Chile

11.5.5 Colombia

11.5.6 Rest of Latin America

11.6 Middle East & Africa

11.6.1 UAE

11.6.2 Saudi Arabia

11.6.3 South Africa

11.6.4 Turkey

11.6.5 Egypt

11.6.6 Rest of Middle East & Africa

12. Competitive Landscape

12.1 Overview

12.2 Key Growth Strategies

12.3 Competitive Benchmarking

12.4 Competitive Dashboard

12.4.1 Industry Leaders

12.4.2 Market Differentiators

12.4.3 Vanguards

12.4.4 Emerging Companies

12.5 Market Ranking/Positioning Analysis of Key Players, 2025

13. Company Profiles

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

13.1 Laing O'Rourke

13.2 Bouygues Construction

13.3 Skanska AB

13.4 Daiwa House Industry Co., Ltd.

13.5 Sekisui House Ltd.

13.6 Red Sea Global

13.7 Lendlease Corporation

13.8 Kiewit Corporation

13.9 VINCI Construction

13.10 Balfour Beatty plc

13.11 ACS Group

13.12 Larsen & Toubro Limited

13.13 Tata Projects Limited

13.14 Hickory Group

13.15 Modscape Pty Ltd.

14. Appendix

14.1 Additional Customization

14.2 Related Reports

Published Date: Feb-2026

Published Date: Feb-2026

Subscribe to get the latest industry updates