Resources

About Us

Autonomous Construction Robots Market by Type (Demolition Robots, Material Handling Robots, Building Construction Robots, Finishing Robots), Application (Residential, Commercial, Industrial), and End-use Vertical - Global Forecast to 2036

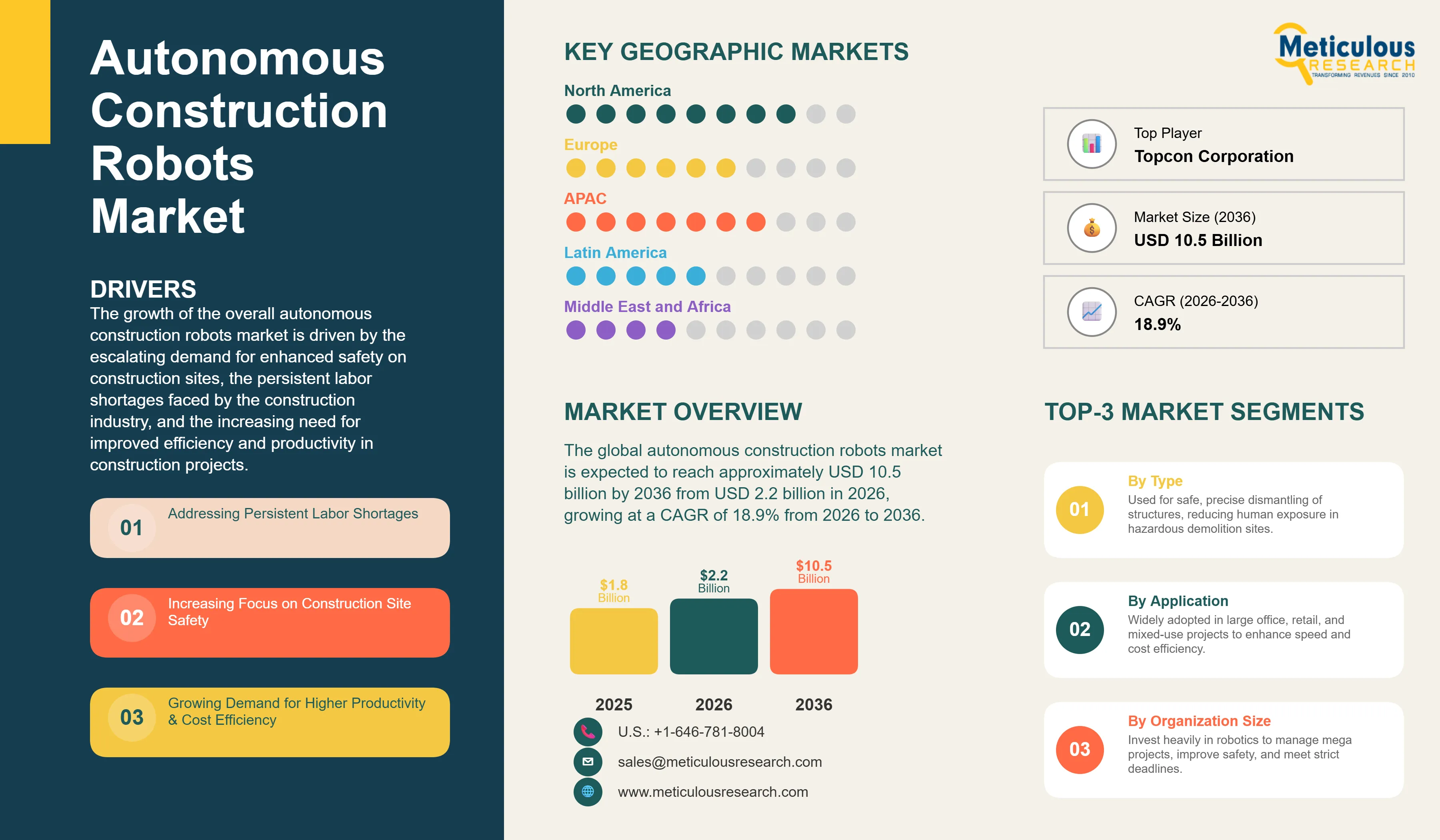

Report ID: MRSE - 1041812 Pages: 281 Feb-2026 Formats*: PDF Category: Semiconductor and Electronics Delivery: 24 to 72 Hours Download Free Sample ReportThe global autonomous construction robots market was valued at USD 1.8 billion in 2025. The market is expected to reach approximately USD 10.5 billion by 2036 from USD 2.2 billion in 2026, growing at a CAGR of 18.9% from 2026 to 2036. The growth of the overall autonomous construction robots market is driven by the escalating demand for enhanced safety on construction sites, the persistent labor shortages faced by the construction industry, and the increasing need for improved efficiency and productivity in construction projects. As construction companies seek to mitigate risks, reduce operational costs, and accelerate project timelines, the adoption of autonomous robots for tasks such as demolition, material handling, and finishing is becoming increasingly critical. Furthermore, advancements in artificial intelligence, machine learning, and sensor technologies are enabling these robots to perform complex tasks with greater precision and autonomy, further propelling market expansion. The integration of Building Information Modeling (BIM) and digital twins with robotic systems is also creating new opportunities for seamless automation and optimized construction workflows.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Autonomous construction robots represent a transformative shift in the construction industry, integrating advanced robotics, artificial intelligence, and automation to perform tasks with minimal human intervention. These robots are designed to enhance safety, improve efficiency, and address labor shortages across various construction phases, from site preparation and material handling to building and finishing. The market is characterized by a diverse range of robotic solutions, including demolition robots, material handling robots, bricklaying robots, painting robots, and inspection drones, each tailored to specific construction applications.

The market encompasses a spectrum of technologies, from semi-autonomous systems that assist human workers to fully autonomous robots capable of executing complex tasks independently. These systems leverage sophisticated sensors, navigation systems, and AI-powered algorithms to perceive their environment, make decisions, and execute actions with high precision. The integration of these robots with Building Information Modeling (BIM) and digital twin technologies allows for seamless data exchange and optimized project management, leading to significant improvements in productivity, quality, and cost-effectiveness. The ability of these robots to operate in hazardous environments also contributes to a safer working environment for human laborers.

The global construction industry is undergoing a significant transformation, driven by the need for sustainable practices, increased productivity, and improved safety standards. This transformation has accelerated the adoption of autonomous construction robots, as traditional construction methods often face challenges such as labor scarcity, high operational costs, and safety risks. Organizations are increasingly prioritizing robotic solutions to overcome these hurdles, leading to a surge in demand for advanced automation in construction. The rapid pace of technological innovation, coupled with supportive government policies and growing investments in smart infrastructure, is further solidifying autonomous construction robots as a foundational technology for the future of the construction sector.

The autonomous construction robots market is witnessing a significant trend towards deeper integration of artificial intelligence (AI) and machine learning (ML) capabilities, moving beyond pre-programmed tasks to more adaptive and intelligent operations. Leading manufacturers are embedding advanced AI algorithms into their robotic systems, enabling them to perceive complex construction environments, interpret real-time data from sensors, and make autonomous decisions on the fly. For instance, AI-powered robots can now dynamically adjust their demolition paths based on structural integrity assessments, optimize material placement to minimize waste, or identify potential safety hazards before they escalate. This shift towards intelligent autonomy allows robots to handle unforeseen challenges, collaborate more effectively with human workers, and continuously learn from their operational experiences, leading to higher efficiency and reduced human intervention. The development of self-learning algorithms that can adapt to varying site conditions and project requirements is a key differentiator, driving the market towards more sophisticated and versatile robotic solutions.

Another prominent trend in the autonomous construction robots market is the increasing adoption of collaborative robots, or cobots, designed to work alongside human construction workers in a shared workspace. Unlike traditional industrial robots that operate in segregated areas, cobots are equipped with advanced safety features, such as force and proximity sensors, allowing them to detect human presence and adjust their movements to prevent collisions. This trend is driven by the recognition that full automation is not always feasible or desirable in complex construction tasks, and that a collaborative approach can leverage the strengths of both humans and robots. Cobots are being deployed for tasks requiring precision and repetitive actions, such as drilling, welding, and assembly, while human workers focus on supervision, complex problem-solving, and tasks requiring fine motor skills or creative judgment. This human-robot collaboration enhances overall productivity, improves ergonomic conditions for workers, and facilitates the transfer of knowledge between human experts and robotic systems, paving the way for more integrated and efficient construction workflows.

|

Parameter |

Details |

|

Market Size by 2036 |

USD 10.5 Billion |

|

Market Size in 2026 |

USD 2.2 Billion |

|

Market Size in 2025 |

USD 1.8 Billion |

|

Market Growth Rate (2026–2036) |

CAGR of 18.9% |

|

Dominating Region |

North America |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Type, Application, End-use Vertical, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

A primary driver for the autonomous construction robots market is the critical need to address persistent labor shortages and improve safety standards within the global construction industry. Many regions face an aging workforce and a declining interest in manual labor, leading to significant project delays and increased costs. Autonomous robots can fill these gaps by performing repetitive, dangerous, or physically demanding tasks, such as heavy lifting, demolition, and working at heights. This not only mitigates the impact of labor scarcity but also drastically reduces the risk of accidents and injuries on construction sites, which are among the most hazardous work environments. The increasing focus on worker well-being and stringent safety regulations are compelling construction firms to invest in robotic solutions that can operate autonomously in high-risk areas, thereby protecting human workers and ensuring project continuity.

The growing integration of autonomous construction robots with Building Information Modeling (BIM) and digital twin technologies presents a significant opportunity for market expansion. BIM provides a comprehensive digital representation of a construction project, while digital twins offer real-time virtual models that mirror physical assets. When combined with autonomous robots, these technologies enable highly precise and efficient construction workflows. Robots can directly access BIM data for task execution, such as precise material placement or automated inspection, and feed real-time progress data back into the digital twin for continuous monitoring and optimization. This synergy allows for predictive maintenance, early detection of deviations from design, and improved resource management, leading to enhanced project quality, reduced rework, and accelerated completion times. The ability to create a fully integrated digital construction ecosystem is a powerful incentive for adoption, driving innovation and investment in autonomous robotic solutions.

The Demolition Robots segment accounts for the largest share of the overall autonomous construction robots market in 2026. This dominance is primarily driven by the increasing global demand for safe and efficient demolition of old structures, particularly in urban areas undergoing redevelopment or requiring infrastructure upgrades. Demolition robots can operate in hazardous environments, reducing human exposure to risks such as falling debris, dust, and structural collapse. Their ability to perform precise and controlled demolition, often remotely, makes them indispensable for projects in densely populated areas or those involving complex structures. Furthermore, advancements in robotic arm technology and specialized attachments have expanded their capabilities, allowing them to handle a wider range of demolition tasks with greater speed and accuracy.

The Material Handling Robots segment is expected to witness the fastest growth during the forecast period. This growth is fueled by the critical need to automate the movement of heavy and bulky materials on construction sites, which is a labor-intensive and injury-prone activity. Material handling robots, including robotic cranes, forklifts, and autonomous guided vehicles (AGVs), improve efficiency, reduce manual labor, and enhance safety by precisely transporting materials across the site. The increasing scale and complexity of construction projects, coupled with labor shortages, are driving the rapid adoption of these robots to streamline logistics and optimize material flow.

The Commercial segment holds the largest market share in 2026, driven by the extensive use of autonomous construction robots in large-scale commercial building projects such as office complexes, shopping malls, and high-rise structures. These projects often involve repetitive tasks, large volumes of materials, and tight deadlines, making them ideal candidates for automation. Autonomous robots can significantly accelerate construction timelines, reduce labor costs, and improve the quality of work in commercial applications. Tasks like bricklaying, concrete pouring, painting, and facade installation can be performed with high precision and consistency by robots, leading to more efficient project execution and higher returns on investment for developers. The growing trend of modular construction and prefabrication in the commercial sector further boosts the demand for robotic solutions that can handle standardized components with speed and accuracy.

The Residential segment is expected to witness significant growth, particularly with the rise of automated home construction and prefabrication techniques. While currently smaller than the commercial segment, the increasing demand for affordable housing and faster construction methods is driving innovation and adoption of autonomous robots in residential projects. The Industrial segment also shows strong potential, especially in the construction of factories, warehouses, and energy infrastructure, where large-scale, repetitive tasks benefit greatly from robotic automation.

The Large Enterprises segment commands the largest share of the global autonomous construction robots market in 2026. This dominance is primarily driven by the significant capital investment required for acquiring and integrating advanced robotic systems, coupled with the extensive project scales and complex operational needs inherent to these organizations. Large construction firms, often involved in mega-projects and infrastructure development, have the financial capacity to invest in high-cost autonomous robots and the technical expertise to manage their deployment and maintenance. Their focus on maximizing efficiency, ensuring safety across vast sites, and adhering to strict project timelines makes autonomous robots an indispensable asset. Furthermore, large enterprises often have established R&D departments or partnerships with technology providers, enabling them to customize and integrate robotic solutions tailored to their specific requirements.

The Small and Medium Enterprises (SMEs) segment is expected to witness substantial growth during the forecast period. While SMEs may face challenges in initial investment and technical expertise, the increasing availability of more affordable, user-friendly, and modular robotic solutions is lowering the barrier to entry. As autonomous construction robots become more accessible through leasing options, robotics-as-a-service (RaaS) models, and simplified integration processes, SMEs are anticipated to adopt these solutions for specialized tasks, improving their competitiveness and efficiency in niche construction markets. The growing ecosystem of startups offering innovative and cost-effective robotic solutions is further accelerating SME adoption.

The Infrastructure vertical commands the largest share of the global autonomous construction robots market in 2026. This leadership stems from the extensive use of autonomous robots in large-scale public works, road construction, bridge building, tunnel excavation, and utility projects. These projects often involve hazardous environments, repetitive tasks over vast areas, and stringent safety requirements, making them ideal candidates for robotic automation. Autonomous robots can perform tasks such as excavation, paving, surveying, and inspection with high precision, speed, and consistency, significantly improving project efficiency and safety. The global push for modernizing aging infrastructure and developing new smart cities further fuels the demand for robotic solutions that can accelerate project completion and reduce human exposure to dangerous conditions.

The Building Construction vertical is poised for significant growth, driven by the increasing adoption of robots for tasks like bricklaying, concrete pouring, welding, and painting in both residential and commercial buildings. The Demolition vertical also represents a critical application, with autonomous robots offering safer and more efficient methods for dismantling structures, particularly in urban renewal projects. The Mining vertical is another key area, where robots are used for excavation, drilling, and material transport in hazardous mining environments.

North America holds the largest share of the global autonomous construction robots market in 2026. This dominance is primarily attributable to the region’s robust construction industry, significant government investments in infrastructure development, and a strong emphasis on workplace safety regulations. The United States, in particular, is a key market, driven by initiatives like the Infrastructure Investment and Jobs Act, which allocates substantial funding for modernizing roads, bridges, and public utilities. The presence of leading construction technology companies, coupled with a high adoption rate of advanced automation solutions and a proactive approach to addressing labor shortages, further solidifies North America’s leading position. Canada and Mexico are also witnessing growing adoption, supported by increasing construction activities and a focus on technological integration.

Asia-Pacific is the fastest-growing regional market for autonomous construction robots during the forecast period, driven by rapid urbanization, massive infrastructure development projects, and supportive government policies promoting automation in the construction sector. Countries like China, India, and Japan are at the forefront of this growth, with significant investments in smart city initiatives and the adoption of advanced construction techniques. The region’s large population and growing demand for residential and commercial spaces are creating immense opportunities for robotic solutions to enhance productivity and efficiency. Furthermore, the increasing focus on sustainable construction practices and the need to overcome labor challenges are accelerating the deployment of autonomous robots across various construction applications.

Europe represents a substantial and steadily growing share of the global autonomous construction robots market, shaped by stringent environmental regulations, a strong focus on worker safety, and a mature construction industry embracing digital transformation. Countries such as Germany, the United Kingdom, France, and the Nordic countries are leading the adoption of robotic solutions, driven by the need to improve efficiency, reduce waste, and address skilled labor shortages. The European Union’s initiatives to promote sustainable construction and smart infrastructure development further stimulate market growth. The region benefits from a well-established ecosystem of robotics manufacturers, research institutions, and construction firms collaborating to develop and deploy innovative autonomous solutions.

Latin America is an emerging market for autonomous construction robots, with countries like Brazil, Argentina, and Mexico showing increasing interest in adopting advanced construction technologies. The region’s growing infrastructure development projects and the need to improve construction efficiency are driving initial investments in robotic solutions. While adoption is currently lower compared to developed regions, the potential for growth is significant as economic conditions improve and awareness of robotic benefits increases.

The Middle East & Africa region is also experiencing nascent growth in the autonomous construction robots market, primarily driven by large-scale construction projects in the GCC countries (e.g., Saudi Arabia, UAE) and South Africa. These projects, often characterized by ambitious timelines and a demand for cutting-edge technologies, are creating opportunities for the deployment of autonomous robots. The region’s focus on diversifying economies and investing in smart infrastructure is expected to fuel further adoption of robotic solutions in the construction sector.

Companies such as Caterpillar Inc., Komatsu Ltd., Built Robotics, Inc., FBR Ltd., and Boston Dynamics lead the global autonomous construction robots market with comprehensive, integrated platforms that combine hardware, software, and advanced automation capabilities. Meanwhile, players including Trimble Inc., Topcon Corporation, Husqvarna Group, and Construction Robotics focus on specific architectural niches—such as surveying and mapping, demolition, and bricklaying—targeting enterprises with particular performance preferences or existing project requirements. Emerging and expanding providers such as Advanced Construction Robotics, Inc., Cybe Construction, and Fastbrick Robotics are strengthening their market positions through innovations in automated material handling, 3D printing construction, and purpose-built offerings for residential and commercial applications.

The global autonomous construction robots market is expected to grow from USD 2.2 billion in 2026 to USD 10.5 billion by 2036.

The global autonomous construction robots market is projected to grow at a CAGR of 18.9% from 2026 to 2036.

The demolition robots segment is expected to dominate the market in 2026 due to the increasing need for safe and efficient dismantling of old structures. The material handling robots segment is projected to accelerate its growth as enterprises demand more robust solutions for automating the movement of heavy and bulky materials on construction sites.

AI and machine learning are transforming the autonomous construction robots market by enabling robots to move beyond pre-programmed tasks toward more adaptive and intelligent operations. Leading vendors are embedding advanced AI algorithms into their robotic systems, allowing them to perceive complex construction environments, interpret real-time data from sensors, and make autonomous decisions on the fly, leading to higher efficiency and reduced human intervention.

North America holds the largest share of the global autonomous construction robots market in 2026. The region’s dominance is primarily driven by its robust construction industry, significant government investments in infrastructure development, and a strong emphasis on workplace safety regulations.

The leading companies include Caterpillar Inc., Komatsu Ltd., Built Robotics, Inc., FBR Ltd., Boston Dynamics, Trimble Inc., and Topcon Corporation.

Published Date: Jan-2026

Published Date: May-2024

Published Date: Jan-2025

Published Date: May-2025

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates