Resources

About Us

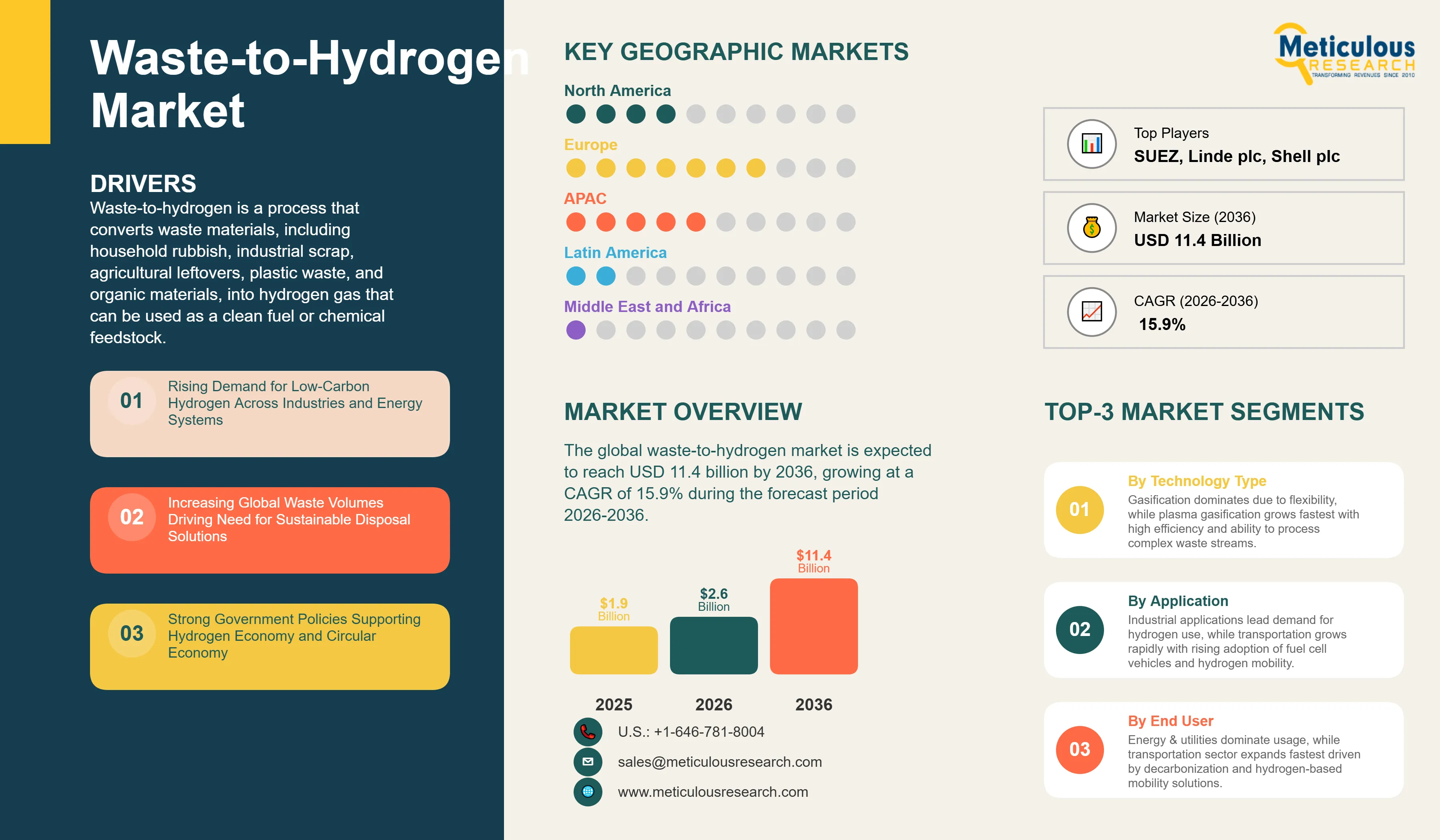

Waste-to-Hydrogen Market Size, Share & Trends Analysis by Technology Type, Feedstock Type, Application, and End-Use Industry- Global Opportunity Analysis & Industry Forecast (2026-2036)

Report ID: MRSE - 1041936 Pages: 290 Apr-2026 Formats*: PDF Category: Semiconductor and Electronics Delivery: 24 to 72 Hours Download Free Sample ReportThe global waste-to-hydrogen market was valued at USD 1.9 billion in 2025. This market is expected to reach USD 11.4 billion by 2036 from an estimated USD 2.6 billion in 2026, growing at a CAGR of 15.9% during the forecast period 2026-2036.

Click here to: Get Free Sample Pages of this Report

Waste-to-hydrogen is a process that converts waste materials, including household rubbish, industrial scrap, agricultural leftovers, plastic waste, and organic materials, into hydrogen gas that can be used as a clean fuel or chemical feedstock. Instead of sending waste to a landfill or an incinerator, waste-to-hydrogen facilities use heat, chemical reactions, or biological processes to break down the carbon and hydrogen content of waste into a mixture of gases, from which hydrogen is then extracted, purified, and compressed for use. The basic process is similar to how coal has been converted to gas for over a century, but applied to a much broader range of waste materials as feedstocks. The result is hydrogen that has a much lower carbon footprint than hydrogen made from natural gas and that also solves a waste management problem at the same time, addressing two significant environmental challenges with a single facility.

The market is growing because it sits at the intersection of two powerful trends: the rapidly growing global hydrogen economy and the equally urgent global waste management crisis. Governments and industries around the world have committed to scaling up hydrogen use as a clean fuel for transportation, industrial processes, and power generation, but the primary challenge facing the hydrogen economy is producing enough hydrogen cheaply enough and with low enough carbon emissions to justify the investment in hydrogen infrastructure. Waste-to-hydrogen offers a pathway to hydrogen production that uses a feedstock that is both free or even negatively priced because operators are paid to take waste, and that has a lower net carbon footprint than conventional steam methane reforming of natural gas. For waste management operators and municipalities facing growing landfill costs, stricter environmental regulations, and the need to reduce waste going to landfill, the ability to convert waste into a valuable hydrogen product rather than simply disposing of it is commercially and politically very attractive.

Two significant near-term opportunities are shaping market development. The integration of waste-to-hydrogen facilities with existing waste management infrastructure, including municipal waste processing centers, industrial waste treatment facilities, and agricultural biogas plants, allows new hydrogen production capacity to be built alongside established waste collection and sorting infrastructure rather than requiring entirely new waste supply chains to be developed. Enerkem's commercial waste-to-methanol plant in Edmonton, Canada, and several European waste gasification projects that are adding hydrogen production steps demonstrate that this integration model is commercially feasible. The growing deployment of hydrogen refueling infrastructure for buses, trucks, and other vehicles in Europe, Japan, South Korea, and California is creating near-term local demand for hydrogen that waste-to-hydrogen facilities can supply at competitive prices compared with green hydrogen from electrolysis, whose costs remain higher at current electricity prices.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 11.4 Billion |

|

Market Size in 2026 |

USD 2.6 Billion |

|

Market Size in 2025 |

USD 1.9 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 15.9% |

|

Dominating Technology Type |

Gasification |

|

Fastest Growing Technology Type |

Plasma Gasification |

|

Dominating Feedstock Type |

Municipal Solid Waste (MSW) |

|

Fastest Growing Feedstock Type |

Plastic Waste |

|

Dominating Application |

Industrial Applications |

|

Fastest Growing Application |

Transportation |

|

Dominating End-Use Industry |

Energy & Utilities |

|

Fastest Growing End-Use Industry |

Transportation |

|

Dominating Hydrogen Type |

Low-Carbon Hydrogen |

|

Fastest Growing Hydrogen Type |

Green Hydrogen |

|

Dominating Deployment Model |

Centralized Production Facilities |

|

Fastest Growing Deployment Model |

Decentralized/On-Site Production |

|

Dominating Geography |

Europe |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Cities and Municipalities Seeing Waste-to-Hydrogen as a Two-Problem Solution

One of the clearest commercial trends driving the waste-to-hydrogen market is the growing recognition by city governments and waste management authorities that waste-to-hydrogen facilities solve two pressing problems simultaneously: the growing challenge of managing municipal solid waste sustainably as landfill capacity shrinks and environmental regulations tighten, and the need to develop local clean hydrogen supply for public transport fleets, municipal vehicles, and local industrial users that are transitioning to hydrogen. A city that builds a waste-to-hydrogen plant can reduce the amount of waste going to landfill or incineration, generate revenue from selling hydrogen to its own bus and refuse truck fleet, and reduce the carbon footprint of both its waste management and its transport operations in a single investment. Several European and Japanese cities have pursued exactly this logic in developing waste-to-hydrogen projects.

The waste management revenue stream is particularly important for the economics of waste-to-hydrogen. Waste-to-hydrogen plants typically receive gate fees for accepting waste, similar to what landfills and waste-to-energy incinerators charge, and these gate fees effectively subsidize the cost of hydrogen production by providing revenue from the feedstock rather than requiring the operator to buy it. When a waste-to-hydrogen plant can collect USD 50 to USD 100 per tonne in gate fees for municipal or industrial waste while simultaneously producing hydrogen worth USD 3 to USD 5 per kilogram, the combined revenue from both waste processing and hydrogen sales can make the project financially viable at a hydrogen production cost that would otherwise be uncompetitive with natural gas-based hydrogen. This dual revenue model is one of the strongest arguments for waste-to-hydrogen relative to other hydrogen production routes and is driving growing interest from both waste management companies looking for higher-value waste processing options and from hydrogen developers looking for lower-cost production pathways.

Plastic Waste Gasification Attracting Major Investment

The conversion of plastic waste specifically into hydrogen through gasification and pyrolysis is emerging as a particularly attractive waste-to-hydrogen application because plastic waste is an abundant, high-calorific-value feedstock with a growing supply availability as plastic recycling targets expose the large fraction of plastic waste that mechanical recycling cannot process. Plastic waste typically contains 80 to 90% carbon and hydrogen by mass, making it an excellent feedstock for thermochemical conversion to hydrogen-rich syngas. The hydrogen content per tonne of plastic waste feedstock is higher than for mixed municipal solid waste, which contains significant water and inert material, making plastic waste one of the most technically attractive feedstocks for waste-to-hydrogen operations.

Several major companies are investing in plastic waste gasification for hydrogen production. Thyssenkrupp's waste gasification technology, Shell's Quest refinery which incorporates waste-derived feedstocks, and several specialist companies in Europe and North America are developing commercial-scale plastic waste to hydrogen plants. The combination of gate fees for accepting plastic waste that mechanical recyclers cannot handle, carbon credits for diverting plastic from landfill or incineration, and hydrogen sales revenue creates a three-stream revenue model for plastic waste to hydrogen operations that improves project economics substantially compared with single-feedstock hydrogen production approaches.

EU Hydrogen Strategy and IRA Creating Enabling Policy Environments

The rapid development of supportive policy frameworks for hydrogen production and waste management in Europe and the United States is creating the enabling conditions for waste-to-hydrogen commercial development by providing financial incentives, regulatory clarity, and demand creation programs that significantly improve project economics. The European Union's Hydrogen Strategy targets 10 million tonnes of domestic renewable hydrogen production by 2030, and while the primary pathway is green hydrogen from electrolysis, waste-derived hydrogen is explicitly recognized in the EU taxonomy as a sustainable activity that can qualify for green finance and investment incentives under certain conditions. Several EU member states have developed national hydrogen strategies that include provisions for waste-derived hydrogen alongside electrolysis-based green hydrogen.

The U.S. Inflation Reduction Act's clean hydrogen production tax credit under Section 45V provides up to USD 3 per kilogram of clean hydrogen based on the lifecycle carbon intensity of the production process. Waste-to-hydrogen production can qualify for significant 45V credits if the lifecycle carbon emissions meet the required thresholds, which for some waste feedstocks and technology combinations they do. The combination of 45V production credits and the separate investment tax credits for waste processing and energy infrastructure under the IRA is making waste-to-hydrogen project development economics substantially more favorable in the U.S. market and is expected to catalyze a significant wave of project development activity through the forecast period similar to what the IRA has done for direct air capture and other clean energy technologies.

Growing Demand for Low-Carbon Hydrogen

The most powerful demand driver for the waste-to-hydrogen market is the rapidly expanding global hydrogen economy's need for hydrogen production pathways that can deliver hydrogen at lower carbon intensity and competitive cost compared with conventional steam methane reforming of natural gas. The global hydrogen market currently produces approximately 95% of its hydrogen from fossil fuels, primarily natural gas and coal, emitting roughly 900 million tonnes of carbon dioxide annually in the process. Transitioning this production to low-carbon or zero-carbon hydrogen is a central objective of climate policy in the EU, U.S., Japan, South Korea, and Australia, each of which has adopted national hydrogen strategies with ambitious low-carbon hydrogen production targets. Waste-to-hydrogen can deliver hydrogen at lower net carbon intensity than fossil-based hydrogen because the organic carbon in waste feedstocks is either biogenic in origin or represents carbon that would otherwise be released through decomposition or incineration of the waste, giving waste-derived hydrogen a favorable lifecycle carbon accounting in most jurisdictions' regulatory frameworks.

Rising Waste Management Challenges Globally

The accelerating global waste management crisis, with landfills in many countries approaching capacity, stricter environmental regulations limiting landfill and incineration disposal options, and growing public and political pressure to reduce waste going to disposal, is creating strong structural demand for waste processing alternatives that convert waste into valuable products rather than simply disposing of it. The global production of municipal solid waste exceeds 2 billion tonnes annually and is growing as populations and living standards rise in developing countries. In Europe, the EU Landfill Directive has progressively restricted the fraction of waste that can be landfilled, and the EU Circular Economy Action Plan sets targets for waste reduction and material recovery that create regulatory pressure on waste management operators to find higher-value applications for the waste streams they process. For waste management companies facing these pressures, the ability to convert previously landfilled or incinerated waste into hydrogen that can be sold as a fuel product transforms a cost center into a revenue-generating operation, creating strong business model motivation for investment in waste-to-hydrogen technology.

Integration with Waste Management and Energy Systems

The most commercially practical near-term opportunity for waste-to-hydrogen is the integration of hydrogen production steps with existing waste-to-energy and waste processing infrastructure, leveraging the established waste collection networks, preprocessing facilities, and operating experience of the waste management industry rather than building entirely new waste supply chains from scratch. Several waste-to-energy companies that already operate gasification and pyrolysis plants for electricity or heat generation are adding hydrogen extraction and purification steps to their existing facilities to produce hydrogen alongside or instead of power, capturing additional value from the same waste feedstock at relatively modest incremental capital cost. Veolia, SUEZ, and Hitachi Zosen, which all have extensive waste-to-energy operations, are developing waste-to-hydrogen capabilities that build on their existing waste processing infrastructure and customer relationships. This integrated approach allows faster commercial development of waste-to-hydrogen capacity than building dedicated hydrogen-only waste conversion facilities and leverages the financial strength and established market positions of existing waste management players to accelerate technology deployment.

Hydrogen Use in Mobility and Industrial Decarbonization

The growing deployment of hydrogen fuel cell buses, refuse collection vehicles, forklifts, and heavy trucks in proximity to urban waste management facilities creates natural local demand for hydrogen that waste-to-hydrogen facilities are well-positioned to supply. A waste management operator that converts its own waste into hydrogen to fuel its own collection fleet achieves a circular economy model that reduces both waste disposal costs and vehicle fuel costs while demonstrating a compelling sustainability story. Several cities in Europe and Japan have developed exactly this model, with waste processing facilities supplying hydrogen to refueling stations for municipal vehicle fleets. The heavy-duty transport sector's increasing adoption of hydrogen fuel cells for long-haul trucks, where battery electric technology faces range and refueling time limitations, is creating growing demand for hydrogen in logistics hubs and along major freight corridors where waste-to-hydrogen facilities can be sited to serve this demand. The industrial sector's use of hydrogen for chemical production, steel manufacturing, and refinery operations represents a large and established hydrogen demand base that waste-to-hydrogen can supply at competitive prices for production facilities with access to suitable waste feedstock streams.

By Technology Type: In 2026, Gasification to Dominate

Based on technology type, the global market is segmented into gasification, pyrolysis, anaerobic digestion with reforming, plasma gasification, and steam reforming of waste-derived feedstocks. In 2026, the gasification segment is expected to account for the largest share of the global waste-to-hydrogen market. Gasification, which partially combusts waste in a controlled oxygen-limited environment to produce a mixture of carbon monoxide and hydrogen called syngas, is the most commercially deployed and technically mature waste-to-hydrogen technology. The syngas produced by gasification is then further processed through a water-gas shift reaction to increase hydrogen concentration, followed by pressure swing adsorption purification to produce high-purity hydrogen. Gasification can accept a wide range of waste feedstocks including municipal solid waste, industrial waste, and biomass, making it the most flexible and broadly applicable waste-to-hydrogen technology.

However, the plasma gasification segment is projected to register the highest CAGR during the forecast period. Plasma gasification uses extremely high-temperature plasma torches to convert waste into syngas at temperatures of 3,000 to 10,000 degrees Celsius, producing a much cleaner syngas than conventional gasification with virtually no tar, char, or toxic emissions, and capable of processing the most contaminated and mixed waste streams that other technologies struggle with. While plasma gasification has higher energy requirements and capital costs than conventional gasification, the superior syngas quality and ability to process otherwise unprocessable waste feedstocks is attracting growing interest and investment as the technology matures toward commercial scale.

By Feedstock Type: In 2026, Municipal Solid Waste to Hold the Largest Share

Based on feedstock type, the global market is segmented into municipal solid waste, industrial waste, agricultural waste, plastic waste, and biomass and organic waste. In 2026, the municipal solid waste segment is expected to account for the largest share of the global waste-to-hydrogen market. MSW is the largest and most consistently available waste feedstock globally, with every city and town producing continuous volumes of household and commercial waste that needs to be processed. The gate fees that waste-to-hydrogen facilities can charge for accepting MSW provide an important revenue contribution that supports project economics, and the political and commercial alignment between waste management authorities seeking sustainable waste disposal solutions and hydrogen developers seeking low-cost feedstock makes MSW the most commercially active feedstock category in the current market.

However, the plastic waste segment is projected to register the highest CAGR during the forecast period. As discussed in the trends section, plastic waste's high hydrogen and carbon content, growing availability from unrecyclable plastic streams, and the gate fee plus hydrogen sales dual revenue model make it an increasingly attractive feedstock for waste-to-hydrogen development. The rapidly growing regulatory pressure on plastic waste diversion from landfill in Europe, North America, and Asia-Pacific is expected to increase the supply of plastic waste feedstock available for waste-to-hydrogen processing significantly through the forecast period.

By Application: In 2026, Industrial Applications to Hold the Largest Share

Based on application, the global market is segmented into transportation, industrial applications, power generation, energy storage and grid applications, and residential and commercial energy use. In 2026, the industrial applications segment is expected to account for the largest share of the global waste-to-hydrogen market. Industrial hydrogen use for refining, chemical production, and increasingly steel manufacturing represents the largest existing hydrogen demand that waste-to-hydrogen can directly serve, and many early waste-to-hydrogen commercial projects are located near industrial facilities that are existing hydrogen users seeking lower-carbon supply alternatives. The large per-facility hydrogen volumes consumed by refineries and chemical plants provide strong commercial demand for the output of large centralized waste-to-hydrogen production facilities.

However, the transportation segment is projected to register the highest CAGR during the forecast period. The growing deployment of hydrogen fuel cell buses, trucks, and eventually passenger vehicles in major metropolitan areas is creating a new and fast-growing local hydrogen demand that is geographically well-matched to urban waste-to-hydrogen facilities that can produce hydrogen near where it is consumed. The European Commission's Alternative Fuels Infrastructure Regulation mandating hydrogen refueling stations along major EU transport corridors, Japan's and South Korea's hydrogen mobility programs, and California's zero-emission truck regulation are collectively creating the growing hydrogen demand in transportation that waste-to-hydrogen facilities can serve.

By Hydrogen Type: In 2026, Low-Carbon Hydrogen to Hold the Largest Share

Based on hydrogen type, the global market is segmented into green hydrogen from renewable waste processes, low-carbon hydrogen, and grey/blue hybrid hydrogen. In 2026, the low-carbon hydrogen segment is expected to account for the largest share of the global waste-to-hydrogen market. The majority of waste-to-hydrogen production currently and through the near term will fall into the low-carbon category, which encompasses hydrogen produced from waste with a carbon intensity significantly lower than conventional fossil fuel-based hydrogen but not necessarily zero. The specific carbon intensity classification of waste-to-hydrogen depends on the feedstock type, the conversion technology, and whether any supplementary energy inputs come from fossil or renewable sources, and most current projects using mixed waste feedstocks and grid electricity for auxiliary power produce hydrogen in the low-carbon rather than strictly green category.

However, the green hydrogen segment is projected to register the highest CAGR during the forecast period. As renewable electricity becomes more widely available and affordable and as waste-to-hydrogen developers optimize their facility designs to minimize fossil energy inputs, an increasing proportion of waste-to-hydrogen production will meet the criteria for green hydrogen designation under evolving regulatory frameworks. The premium pricing and preferential treatment that green hydrogen receives under the EU Delegated Acts and the U.S. 45V production credit hierarchy create strong incentives for waste-to-hydrogen operators to design and operate their facilities to qualify for green hydrogen certification, driving progressive improvement in the carbon intensity of waste-to-hydrogen production.

Waste-to-Hydrogen Market by Region: Europe Leading by Share, Asia-Pacific by Growth

Based on geography, the global market is segmented into Europe, North America, Asia-Pacific, Latin America, and the Middle East and Africa.

In 2026, Europe is expected to account for the largest share of the global waste-to-hydrogen market. Europe leads the market because it combines the world's most developed hydrogen policy framework with highly developed waste management infrastructure, the strictest waste disposal regulations that create strong feedstock availability, and the most active investment activity in waste-to-hydrogen commercial projects. The UK's Project Cavendish, which aims to produce hydrogen from municipal solid waste gasification for the Humber industrial cluster, and several Netherlands-based waste-to-hydrogen projects associated with the Rotterdam industrial cluster represent some of the most commercially advanced waste-to-hydrogen developments globally. Germany's REMondis waste management group, France's Total and Veolia, and UK-based Enerjem are among the European companies most actively developing waste-to-hydrogen commercial programs. The European Hydrogen Bank's auctions and the EU Innovation Fund are providing direct grant funding for pioneering waste-to-hydrogen projects that are establishing the commercial benchmarks and regulatory precedents needed for broader market development. Norway's interest in hydrogen as a transport and industrial fuel, Sweden's circular economy leadership, and the Netherlands' active hydrogen hub development make these smaller European markets disproportionately important in the global waste-to-hydrogen commercial development landscape.

However, the Asia-Pacific waste-to-hydrogen market is expected to grow at the fastest CAGR during the forecast period. Japan has the most technically advanced and commercially active waste-to-hydrogen program in Asia-Pacific, driven by its acute waste management challenges in a densely populated island nation with limited landfill space, its advanced waste-to-energy industry that provides the technology platform for adding hydrogen production, and its strong government commitment to developing a hydrogen-based economy for transportation, industry, and power generation. Hitachi Zosen, Kawasaki Heavy Industries, and Mitsubishi Heavy Industries are all developing waste gasification and hydrogen production technologies, and several Japanese municipalities have launched waste-to-hydrogen pilot projects. South Korea's hydrogen economy roadmap includes waste-to-hydrogen as a pathway to domestic hydrogen production, and Korean waste management companies are developing conversion projects. China's enormous waste management challenges, growing hydrogen policy support, and large manufacturing base for gasification and processing equipment make it a potentially very large future market. India's growing urban waste volumes and expanding hydrogen policy framework represent additional emerging market opportunities in Asia-Pacific.

North America is a growing waste-to-hydrogen market primarily driven by the United States, where the IRA's 45V hydrogen production tax credits and investment incentives for waste processing are creating significantly improved project economics for waste-to-hydrogen developments. Enerkem's commercial waste-to-chemicals facility in Edmonton, Canada, which produces methanol and ethanol from municipal solid waste through gasification and is being adapted to include hydrogen production, is one of the most commercially advanced waste conversion facilities in North America and represents an important proof point for the technology. California's zero-emission transport mandates and its very large urban waste streams make it a particularly active state for waste-to-hydrogen project development, and several gasification and pyrolysis companies are targeting the California market with projects designed to supply the state's growing network of hydrogen refueling stations for buses and trucks.

The waste-to-hydrogen market includes industrial gas majors with hydrogen expertise and distribution networks, integrated energy and waste management companies developing proprietary conversion technologies, specialist technology providers targeting specific waste types or conversion processes, and emerging companies developing novel approaches to waste hydrogen production. Competition is based on conversion technology efficiency, feedstock flexibility, hydrogen purity and quality, project development and financing capability, and the ability to secure both waste supply agreements and hydrogen offtake contracts simultaneously.

Air Liquide and Linde, as the world's two largest industrial gas companies, bring extensive hydrogen production, purification, storage, and distribution expertise alongside their own growing interest in low-carbon hydrogen supply, making them natural leaders in commercializing waste-to-hydrogen at industrial scale. Veolia and SUEZ bring large established waste management operations and the feedstock relationships and sorting infrastructure that are essential for reliable waste-to-hydrogen feedstock supply. Enerkem has the most commercially advanced waste gasification to chemical products facility globally and is developing hydrogen production capabilities on that platform. EQTEC is a specialist gasification technology developer focused on waste-to-syngas and hydrogen production. Hitachi Zosen brings Japanese waste gasification engineering heritage and active development of waste-to-hydrogen pilot programs. Haldor Topsoe, now Topsoe, is a leading catalyst and process technology company whose syngas upgrading and hydrogen purification technologies are essential components of waste-to-hydrogen production systems.

The report provides a comprehensive competitive analysis based on a thorough review of leading players' technology portfolios, project development track records, commercial partnerships, and recent strategic developments. Some of the key players operating in the global waste-to-hydrogen market include Air Liquide (France), Linde plc (UK/Ireland), Veolia Environnement S.A. (France), Enerkem Inc. (Canada), Shell plc (UK/Netherlands), TotalEnergies SE (France), Mitsubishi Heavy Industries Ltd. (Japan), SUEZ (France), Hitachi Zosen Corporation (Japan), Waste Management Inc. (U.S.), Siemens Energy AG (Germany), Thyssenkrupp AG (Germany), Plug Power Inc. (U.S.), Haldor Topsoe A/S (Denmark), and EQTEC plc (UK/Ireland), among others.

The global waste-to-hydrogen market size is expected to reach USD 11.4 billion by 2036 from an estimated USD 2.6 billion in 2026, at a CAGR of 15.9% during the forecast period 2026-2036.

In 2026, the gasification segment is expected to hold the largest share of the global waste-to-hydrogen market, reflecting gasification being the most commercially deployed and technically mature waste-to-hydrogen conversion technology with the broadest feedstock acceptance capability and the largest number of operating commercial facilities globally.

The plasma gasification segment is expected to register the highest CAGR during the forecast period 2026-2036, driven by the technology's ability to process the most contaminated and mixed waste streams that conventional gasification cannot handle and its superior syngas quality, with growing investment from companies developing commercial-scale plasma gasification systems for urban waste processing.

In 2026, the industrial applications segment is expected to hold the largest share of the global waste-to-hydrogen market, reflecting large industrial hydrogen users in refining and chemical production representing the most commercially established demand base for waste-to-hydrogen output at scale.

The transportation segment is projected to register the highest CAGR during the forecast period, driven by the growing deployment of hydrogen fuel cell buses, refuse trucks, and heavy-duty vehicles in metropolitan areas that creates local hydrogen demand well-matched to urban waste-to-hydrogen production facilities.

The market is primarily driven by the global hydrogen economy's need for low-carbon hydrogen production pathways that can compete on cost with conventional natural gas-based hydrogen while delivering lower carbon emissions, and by the growing waste management crisis creating strong commercial and regulatory motivation for waste management operators to convert unrecyclable waste into valuable hydrogen products rather than sending it to landfill or incineration.

Key players are Air Liquide (France), Linde plc (UK/Ireland), Veolia Environnement S.A. (France), Enerkem Inc. (Canada), Shell plc (UK/Netherlands), TotalEnergies SE (France), Mitsubishi Heavy Industries Ltd. (Japan), SUEZ (France), Hitachi Zosen Corporation (Japan), Waste Management Inc. (U.S.), Siemens Energy AG (Germany), Thyssenkrupp AG (Germany), Plug Power Inc. (U.S.), Haldor Topsoe A/S (Denmark), and EQTEC plc (UK/Ireland), among others.

Asia-Pacific is expected to register the highest growth rate in the global waste-to-hydrogen market during the forecast period 2026-2036, driven by Japan's advanced waste-to-hydrogen technology development programs and strong hydrogen economy policy, South Korea's hydrogen economy roadmap including waste-derived hydrogen, and China's enormous waste management needs combined with growing hydrogen policy support.

Published Date: Apr-2024

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates