Resources

About Us

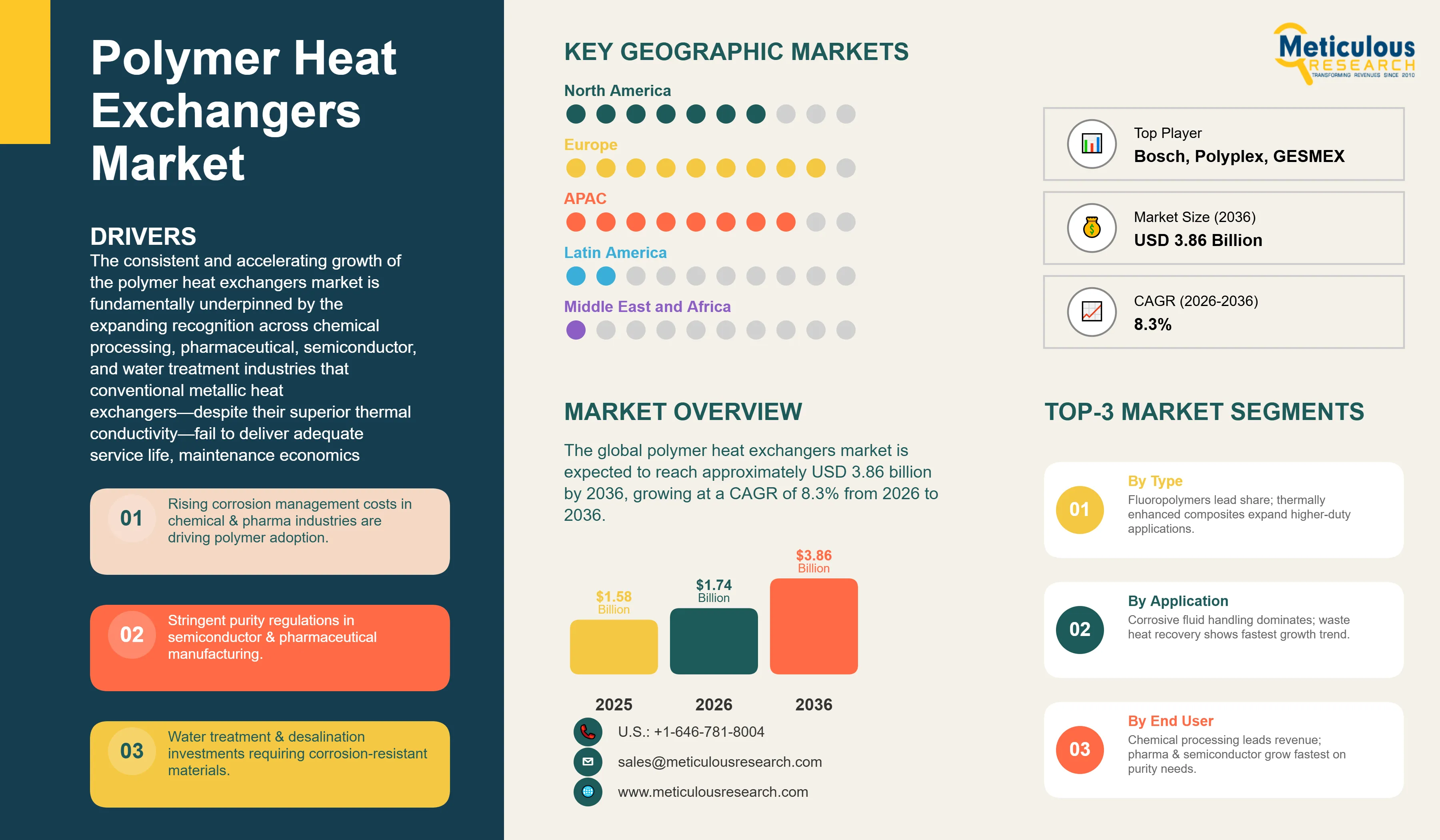

The global polymer heat exchangers market was valued at USD 1.58 billion in 2025. The market is expected to reach approximately USD 3.86 billion by 2036 from USD 1.74 billion in 2026, growing at a CAGR of 8.3% from 2026 to 2036. The consistent and accelerating growth of the polymer heat exchangers market is fundamentally underpinned by the expanding recognition across chemical processing, pharmaceutical, semiconductor, and water treatment industries that conventional metallic heat exchangers — despite their superior thermal conductivity — fail to deliver adequate service life, maintenance economics, or product purity requirements in applications involving highly corrosive process fluids, ultra-pure water systems, and aggressive cleaning regimes. Polymer heat exchangers, engineered from fluoropolymers including polytetrafluoroethylene and polyvinylidene fluoride, polypropylene, polyether ether ketone, and advanced high-performance thermoplastics, deliver exceptional chemical resistance spanning virtually the entire pH spectrum from concentrated acids to strong caustics, inherent non-fouling surfaces minimizing cleaning frequency and downtime, and elimination of metallic ion contamination that compromises product quality in pharmaceutical and semiconductor applications. The convergence of advancing polymer processing technologies enabling fabrication of increasingly complex heat exchanger geometries, growing regulatory scrutiny of metallic contamination in food, pharmaceutical, and electronics manufacturing, and escalating operational cost pressures driving demand for longer-life, lower-maintenance thermal management solutions is creating powerful and sustained market growth momentum across multiple high-value industrial segments globally.

Click here to: Get Free Sample Pages of this Report

Polymer heat exchangers are thermal management devices constructed from engineering plastics and high-performance polymers rather than conventional metals, designed to transfer heat between fluid streams in process applications where metallic materials are unsuitable due to corrosion, contamination, fouling, weight, or cost constraints. The fundamental thermal engineering challenge of polymer heat exchangers — that most polymers exhibit thermal conductivities one to two orders of magnitude lower than metals (0.1-0.5 W/m.K for polymers versus 10-400 W/m.K for metals) — is addressed through design strategies including extremely thin wall thicknesses in hollow fiber and film configurations maximizing heat transfer area per unit volume, use of thermally enhanced polymer compounds incorporating graphite, boron nitride, or carbon fiber fillers increasing effective thermal conductivity to 1-5 W/m.K, and geometric innovations including corrugated plate designs and turbulence-promoting surface features maximizing convective heat transfer coefficients to compensate for lower material thermal conductivity. Contemporary polymer heat exchanger designs achieve heat transfer performance approaching or matching metallic alternatives in many application contexts while delivering the chemical resistance, non-fouling, weight reduction, and contamination prevention benefits that justify their application in demanding industrial environments.

The polymer heat exchanger market is segmented across distinct material platforms addressing different performance envelopes. Fluoropolymers — particularly PTFE, PVDF, PFA, and ETFE — represent the premium performance segment offering resistance to virtually all industrial chemicals including concentrated hydrofluoric acid, hot sulfuric acid, chlorine, and powerful oxidizing agents at service temperatures up to 200-260 degrees Celsius depending on specific material and pressure requirements. Polypropylene heat exchangers serve the largest volume segment of moderately corrosive applications including dilute acids, caustic solutions, and many organic solvents at temperatures below 90 degrees Celsius, offering substantially lower material costs than fluoropolymers while providing adequate chemical resistance for the majority of industrial corrosive heat transfer applications. PEEK heat exchangers address demanding applications requiring both chemical resistance and elevated temperature capability approaching 250 degrees Celsius combined with superior mechanical strength enabling higher operating pressures than other polymer alternatives. High-performance polysulfone, polyphenylene sulfide, and glass-filled specialty thermoplastic composites occupy intermediate performance positions combining moderate chemical resistance with enhanced mechanical and thermal properties enabling applications where standard polypropylene is inadequate but full fluoropolymer specifications are unnecessary.

The competitive landscape of the polymer heat exchanger market encompasses dedicated polymer heat exchanger specialists competing with thermal engineering companies that have developed polymer product lines to complement metallic exchanger portfolios. Ametek Fluoropolymer Products, GESMEX (Germany), Etched Plate Heat Exchangers, Bram-Cor (Italy), and Georg Fischer Piping Systems represent specialist manufacturers with deep application expertise in specific polymer materials and exchanger configurations. Larger thermal management companies including Alfa Laval, API Heat Transfer, and Kelvion have developed polymer heat exchanger offerings targeting crossover applications where customers specify polymer alternatives within broader thermal management procurement programs. The market is experiencing accelerating innovation in polymer composite heat exchangers — combining polymer matrices with thermally conductive fillers — that promise to substantially improve the heat transfer performance limitation that has historically constrained polymer heat exchangers to lower-duty applications, potentially opening substantially larger market segments currently served exclusively by metallic alternatives.

Advanced Polymer Composites Closing the Thermal Conductivity Gap with Metals

The most consequential technical trend reshaping polymer heat exchanger market potential is the rapid advancement of thermally conductive polymer composites that substantially reduce the inherent thermal conductivity disadvantage of conventional engineering plastics relative to metallic heat exchanger materials. Research and commercial development programs incorporating boron nitride nanoplatelets, expanded graphite flakes, carbon fiber networks, and aluminum nitride particles as thermally conductive fillers within fluoropolymer and engineering thermoplastic matrices have demonstrated composite thermal conductivities of 2-10 W/m.K — representing order-of-magnitude improvements over unfilled polymer bases while preserving the chemical resistance and non-contaminating properties that define polymer heat exchangers' market value proposition. These thermally enhanced polymer composites enable polymer heat exchanger designs that compete directly with metallic alternatives in moderate-duty heat transfer applications — substantially expanding the addressable market beyond the corrosion-limited niche where polymer heat exchangers have historically been specified. Companies including Celanese, Victrex, Solvay, and specialty compounders are commercializing thermally conductive polymer compounds specifically targeted at heat exchanger applications, with automotive thermal management, electronics cooling, and industrial process heat recovery representing the primary growth opportunities for thermally enhanced polymer heat exchanger systems.

Hollow Fiber Polymer Heat Exchanger Innovation for Ultra-High Purity Applications

Hollow fiber polymer heat exchanger technology — adapted from membrane separation module manufacturing techniques to create dense bundles of small-diameter polymer tubes providing exceptional heat transfer area per unit volume — is experiencing significant growth driven by expanding semiconductor and pharmaceutical industry applications where ultra-high purity process requirements and rigorous contamination prevention standards mandate polymer construction throughout fluid handling and thermal management systems. Hollow fiber PTFE and PFA heat exchangers achieve specific surface areas of 500-2,000 m2/m3 — substantially exceeding conventional shell-and-tube configurations at 50-200 m2/m3 — enabling compact, high-performance heat exchangers suitable for installation in space-constrained cleanroom environments serving semiconductor wet processing systems. The semiconductor industry's transition to advanced node fabrication — 3nm, 2nm, and sub-2nm process nodes requiring increasingly precise temperature control of ultra-pure chemical baths and deionized water systems — creates demanding specifications for hollow fiber polymer heat exchangers where metallic ion leaching from conventional materials would contaminate process chemicals causing defects in critical circuit features. Medical device sterilization systems, bioreactor temperature control, and high-purity pharmaceutical water systems represent additional high-value application segments driving hollow fiber polymer heat exchanger demand beyond the semiconductor sector.

|

Parameter |

Details |

|

Market Size by 2036 |

USD 3.86 Billion |

|

Market Size in 2026 |

USD 1.74 Billion |

|

Market Size in 2025 |

USD 1.58 Billion |

|

Market Growth Rate (2026-2036) |

CAGR of 8.3% |

|

Dominating Region |

Europe |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Material Type, Product Type, Application, End-User Industry, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Drivers: Chemical Industry Expansion and Corrosion Management Imperatives

The primary market driver for polymer heat exchangers is the persistent and growing challenge of corrosion management in chemical processing, pharmaceutical manufacturing, and water treatment operations that consume enormous financial resources through equipment replacement, maintenance labor, production downtime, and contamination incidents attributable to metallic material degradation. The National Association of Corrosion Engineers estimates global corrosion costs at approximately USD 2.5 trillion annually — representing approximately 3.4% of global GDP — with process industry heat exchangers representing a significant proportion of corrosion-related maintenance and replacement expenditure. Polymer heat exchangers address this challenge by eliminating corrosion as a failure mode entirely in chemical resistance-limited applications, with properly specified fluoropolymer heat exchangers routinely achieving 15-20 year service lives in concentrated acid applications where metallic alternatives require replacement every 2-5 years — delivering total cost of ownership advantages that justify polymer heat exchangers' higher initial capital cost across multi-decade plant operating lifetimes. The global chemical industry's sustained capital investment in capacity expansion — particularly in Asia where large-scale chemical complexes are being constructed across China, India, and Southeast Asia — creates growing demand for polymer heat exchangers in applications including hydrochloric acid production and handling, chlor-alkali processing, fluorochemicals manufacturing, and specialty chemical synthesis where process fluid corrosivity mandates non-metallic heat transfer solutions.

Opportunity: Water Treatment and Desalination Infrastructure Investment

The global water scarcity crisis and expanding investment in desalination, industrial wastewater treatment, and water recycling infrastructure creates a substantial and rapidly growing opportunity for polymer heat exchangers in applications where conventional metallic heat exchangers fail due to the highly corrosive nature of concentrated brine, chlorinated water treatment streams, and chemically aggressive effluent treatment reagents. Multi-stage flash and multi-effect distillation desalination processes expose heat exchangers to high-salinity brine at elevated temperatures creating severe marine corrosion conditions that defeat conventional carbon steel and even stainless steel heat exchanger materials at economically viable maintenance intervals — creating compelling economics for polymer heat exchangers capable of long-term reliable operation in these aggressive environments. The Middle East's continued massive investment in seawater desalination capacity — Saudi Arabia's NEOM project includes one of the world's largest planned desalination facilities — combined with growing municipal and industrial water recycling investment in water-stressed regions including Western United States, Australia, and Mediterranean Europe creates a large and growing market for polymer heat exchangers in thermal desalination pre-heaters, brine heaters, and distillate condensers. Industrial wastewater treatment applications including acid mine drainage neutralization, electroplating rinse water recovery, semiconductor fab ultrapure water systems, and pharmaceutical process water purification similarly require polymer heat exchanger materials capable of reliable operation in chemically challenging treatment streams.

Why Do Fluoropolymers Lead the Polymer Heat Exchanger Market?

Fluoropolymers command approximately 45-50% of total polymer heat exchanger market revenue in 2026, reflecting their unrivaled chemical resistance profile spanning the complete spectrum of industrial acids, bases, oxidizing agents, and organic solvents, combined with broad temperature capability and the critical non-stick, non-contaminating surface properties required in pharmaceutical, semiconductor, and food processing applications. PTFE — the flagship fluoropolymer with service temperatures to 260 degrees Celsius and resistance to virtually all chemicals except molten alkali metals and elemental fluorine — serves the most demanding chemical processing heat transfer applications as both primary construction material for heat exchanger tubes and as lining material for metallic shell components providing composite constructions combining fluoropolymer chemical resistance with metallic structural integrity. PVDF offers a cost-effective alternative to PTFE for applications not requiring full fluoropolymer resistance, with superior weldability enabling more complex fabrication geometries and better mechanical properties at moderate temperatures, while PFA and ETFE address specific application requirements where PTFE's processing limitations restrict geometric complexity. The polypropylene segment represents the largest volume material category by number of installed units, serving the broad middle ground of moderately corrosive applications where fluoropolymer performance is not required but metallic corrosion remains a significant concern — including dilute acid pickling systems, caustic scrubber systems, and swimming pool and aquaculture water treatment applications where polypropylene's cost-performance ratio is highly competitive.

How Does Shell & Tube Maintain Market Leadership?

The shell and tube product type accounts for approximately 38-42% of polymer heat exchanger market revenue in 2026, benefiting from engineers' familiarity with shell-and-tube thermal and hydraulic design methodologies that enable straightforward specification of polymer alternatives as direct replacements for metallic shell-and-tube exchangers in corrosive service upgrades. Polymer shell-and-tube heat exchangers retain the fundamental configuration of tube bundles contained within cylindrical shells, with PTFE or polypropylene tubes replacing metallic tubes while shell components may be constructed from polymer, fiber-reinforced plastic, or rubber-lined carbon steel depending on application requirements and economic optimization. The plate heat exchanger segment demonstrates strong growth momentum at approximately 10-12% CAGR, driven by advances in polymer plate forming technologies enabling fabrication of corrugated heat transfer plates with geometric complexity approaching metallic plate designs, combined with the inherent compactness and high heat transfer efficiency of plate configurations that are particularly valuable in space-constrained process environments. Hollow fiber heat exchangers represent the fastest-growing product type at approximately 13-15% CAGR, driven by semiconductor and pharmaceutical industry demand for ultra-high purity, high-surface-area compact heat exchangers where hollow fiber PTFE and PFA constructions provide unmatched performance across critical specifications including chemical purity, particle generation, and heat transfer density required for advanced manufacturing processes.

How Does Corrosive Fluid Handling Dominate Application Segments?

The corrosive fluid handling application segment represents approximately 42-46% of total polymer heat exchanger market in 2026, encompassing the vast range of chemical processing, metal surface treatment, and industrial manufacturing applications where process fluids including mineral acids, caustic solutions, oxidizing agents, and aggressive organic solvents demand non-metallic heat transfer surfaces for reliable long-term operation. Hydrochloric acid heating and cooling represents one of the largest single application categories, with polymer heat exchangers serving steel pickling operations, chlor-alkali production facilities, and HCl synthesis and purification systems where acid concentrations and temperatures create service conditions that defeat even highly alloyed metallic materials at economic maintenance intervals. Sulfuric acid heat exchangers in fertilizer production, petroleum refining alkylation units, and battery acid manufacturing represent another major application category where polymer heat exchangers provide compelling lifecycle economics compared to tantalum and exotic alloy alternatives historically specified for concentrated acid service. The waste heat recovery application is experiencing significant growth momentum at approximately 11-13% CAGR, driven by industrial energy efficiency imperatives creating demand for polymer heat exchangers capable of recovering low-grade heat from corrosive flue gases, acidic condensates, and contaminated process streams previously vented or cooled without energy recovery due to the unavailability of cost-effective corrosion-resistant heat transfer technology.

Why Does Chemical Processing Command Market Leadership?

The chemical processing end-user segment commands approximately 35-40% of polymer heat exchanger market revenue in 2026, reflecting the chemical industry's position as both the earliest adopter of polymer heat exchanger technology and the end-user sector with the broadest range of corrosive heat transfer applications driving sustained and growing polymer heat exchanger demand. Chemical plants managing inorganic acids including hydrochloric, sulfuric, nitric, hydrofluoric, and phosphoric acid across production, purification, storage, and distribution operations require polymer heat exchangers throughout thermal management systems where metallic materials would corrode rapidly creating contamination, safety, and operational reliability concerns. The pharmaceutical and biotechnology end-user segment represents the fastest-growing market at approximately 11-13% CAGR, driven by the pharmaceutical industry's strict requirements for materials of construction that prevent metallic ion contamination of drug substance and drug product streams, combined with the aggressive cleaning and sterilization regimes — including CIP/SIP with strong caustic and acidic cleaning agents — that create cyclic corrosive stress exceeding the capability of even high-grade stainless steel in some critical applications. The semiconductor and electronics end-user segment commands premium pricing through the stringent purity and particle generation specifications mandated for heat exchangers contacting ultra-pure water, high-purity chemicals, and process gases in advanced semiconductor fabrication, with hollow fiber PTFE and PFA heat exchangers serving as standard equipment in 300mm wafer fab chemical distribution and temperature control systems at leading manufacturers including TSMC, Samsung, and Intel.

How is Europe Maintaining Market Leadership?

Europe holds approximately 32-36% of the global polymer heat exchanger market in 2026, supported by the continent's dense concentration of chemical, pharmaceutical, and specialty materials manufacturing industries that collectively represent the most established and technically sophisticated end-user base for advanced polymer heat exchanger applications globally. Germany, the Netherlands, Belgium, and France host some of the world's largest chemical complexes — BASF's Ludwigshafen Verbund, Shell's Pernis refinery, INEOS's Antwerp operations, and Solvay's multiple European sites — that operate extensive networks of corrosive fluid heat exchangers where polymer alternatives have achieved substantial market penetration over decades of application development. European pharmaceutical manufacturing centers in Switzerland, Germany, Ireland, and Italy apply stringent materials of construction standards mandating polymer heat exchangers in critical contact applications involving drug substances, with GMP compliance requirements creating clear specification frameworks that favor polymer materials over metallic alternatives in contamination-sensitive heat transfer services. The European chemical industry's ongoing transition toward renewable feedstocks, bio-based chemical production, and green chemistry processes frequently introduces new corrosive process streams and cleaning regimes where conventional metallic heat exchanger materials are inadequate, creating continuous demand pull for polymer heat exchanger solutions capable of handling novel chemical environments associated with green chemistry manufacturing.

Which Factors Drive Asia-Pacific's Rapid Growth?

Asia-Pacific demonstrates the highest regional growth rate at approximately 10-12% CAGR, propelled by the simultaneous expansion of multiple high-value end-user industries that represent core polymer heat exchanger markets across China, South Korea, Taiwan, and India. Taiwan and South Korea's semiconductor industries — home to TSMC, Samsung Foundry, SK Hynix, and Micron's expanding Asian operations — represent the most technically demanding and economically valuable polymer heat exchanger application cluster in the Asia-Pacific region, with next-generation fab construction programs creating consistent demand for hollow fiber PTFE and PFA heat exchangers meeting the most stringent purity specifications in commercial heat exchanger manufacturing. China's massive chemical industry expansion — the largest in the world by output value and continuing to grow rapidly through both capacity expansion and import substitution programs — creates broad-based demand for polymer heat exchangers in acid handling, chlor-alkali processing, and specialty chemical manufacturing applications, with domestic Chinese polymer heat exchanger manufacturers including Zhejiang Jiansheng and related companies developing competitive offerings for the cost-sensitive middle market while international specialists capture premium corrosion-resistant and high-purity segments. India's pharmaceutical industry — the world's largest supplier of generic medicines by volume and increasingly serving regulated markets in North America and Europe with quality requirements demanding GMP-compliant polymer materials — is driving growing polymer heat exchanger adoption in API manufacturing and formulation facilities upgrading to international quality standards.

The global polymer heat exchangers market features a mix of dedicated specialty manufacturers and diversified thermal equipment companies. Ametek Fluoropolymer Products (AMETEK Inc.), GESMEX GmbH, and Polyplex Solutions represent leading dedicated polymer heat exchanger specialists with deep application expertise spanning fluoropolymer and engineering thermoplastic constructions across chemical, pharmaceutical, and semiconductor end-users. Bram-Cor SpA (Italy), Georg Fischer Piping Systems, and Bosch Thermotechnology have established strong positions in pharmaceutical and food processing polymer heat exchanger applications through cleanroom-compatible product designs and comprehensive GMP documentation support. Alfa Laval AB, API Heat Transfer, and Kelvion Holding GmbH serve polymer heat exchanger market segments through dedicated product lines complementing their broader metallic heat exchanger portfolios, leveraging established thermal engineering sales channels and application engineering capabilities. Advanced thermal management companies including Celrad Plastic Heat Exchangers, Exergy LLC (hollow fiber specialist), and Mersen (carbon and fluoropolymer thermal equipment) address specialized application requirements in corrosion-critical and ultra-high purity segments. Emerging competitors from Asia including Chinese manufacturers Zhejiang Jiansheng and Indian suppliers developing polypropylene and PVDF heat exchanger lines for domestic chemical and pharmaceutical markets are expanding competitive dynamics in cost-sensitive applications, while material innovators including Solvay, Victrex, and Celanese advance thermally conductive polymer compounds enabling next-generation high-performance polymer heat exchanger products.

The global polymer heat exchangers market is expected to grow from USD 1.74 billion in 2026 to USD 3.86 billion by 2036.

The global polymer heat exchangers market is projected to grow at a CAGR of 8.3% from 2026 to 2036.

Fluoropolymers dominate the market representing 45-50% of revenue through PTFE and PVDF's unmatched chemical resistance in demanding corrosive applications. PEEK and advanced high-performance thermoplastic composites demonstrate the fastest growth driven by expanding semiconductor and pharmaceutical applications requiring elevated temperature capability combined with ultra-high purity and superior mechanical properties.

Advanced polymer composites incorporating boron nitride, expanded graphite, and carbon fiber thermally conductive fillers are achieving thermal conductivities of 2-10 W/m.K -- representing order-of-magnitude improvements over unfilled polymer bases -- enabling polymer heat exchangers to compete in moderate-duty applications previously served exclusively by metallic alternatives, substantially expanding the total addressable market beyond traditional corrosion-limited niches.

Europe leads with approximately 32-36% of global market driven by its concentrated chemical and pharmaceutical manufacturing base and stringent materials of construction regulations. Asia-Pacific demonstrates the fastest growth at 10-12% CAGR propelled by semiconductor fabrication expansion in Taiwan and South Korea, chemical industry growth in China, and pharmaceutical manufacturing upgrading in India.

The leading companies include Ametek Fluoropolymer Products, GESMEX GmbH, Bram-Cor SpA, Georg Fischer Piping Systems, Bosch Thermotechnology, Alfa Laval AB, API Heat Transfer, Kelvion Holding GmbH, Mersen, and Exergy LLC, with material suppliers Solvay, Victrex, and Celanese advancing thermally conductive polymer compound platforms enabling next-generation product performance.

1. Introduction

1.1 Market Definition

1.2 Market Scope

1.3 Research Methodology

1.4 Assumptions & Limitations

2. Executive Summary

3. Market Overview

3.1 Introduction

3.2 Market Dynamics

3.2.1 Drivers

3.2.2 Restraints

3.2.3 Opportunities

3.2.4 Challenges

3.3 Thermally Conductive Polymer Composites: Technology Evolution & Market Impact

3.4 Regulatory Landscape: GMP, FDA, and Materials of Construction Standards

3.5 Porter's Five Forces Analysis

4. Global Polymer Heat Exchangers Market, by Material Type

4.1 Introduction

4.2 Fluoropolymers

4.2.1 PTFE (Polytetrafluoroethylene)

4.2.2 PVDF (Polyvinylidene Fluoride)

4.2.3 PFA (Perfluoroalkoxy Alkane)

4.2.4 ETFE (Ethylene Tetrafluoroethylene)

4.3 Polypropylene (PP)

4.3.1 Homopolymer PP

4.3.2 Copolymer & Glass-Filled PP

4.4 PEEK (Polyether Ether Ketone)

4.5 Polyethylene (HDPE & UHMWPE)

4.6 Polysulfone & PPS (Polyphenylene Sulfide)

4.7 Thermally Conductive Polymer Composites

5. Global Polymer Heat Exchangers Market, by Product Type

5.1 Introduction

5.2 Shell & Tube Heat Exchangers

5.2.1 Fixed Tube Sheet Design

5.2.2 U-Tube & Floating Head Design

5.3 Plate Heat Exchangers

5.3.1 Gasketed Plate Heat Exchangers

5.3.2 Welded & Semi-Welded Plate Exchangers

5.4 Hollow Fiber Heat Exchangers

5.4.1 PTFE Hollow Fiber Modules

5.4.2 PFA & Specialty Fluoropolymer Fiber Modules

5.5 Double Pipe Heat Exchangers

5.6 Air-Cooled & Finned Polymer Heat Exchangers

6. Global Polymer Heat Exchangers Market, by Application

6.1 Introduction

6.2 Corrosive Fluid Handling

6.2.1 Acid Heating & Cooling (HCl, H2SO4, HF, HNO3)

6.2.2 Caustic & Alkali Stream Heat Transfer

6.2.3 Oxidizing Agent & Chlorine Handling

6.3 Waste Heat Recovery

6.3.1 Corrosive Flue Gas Heat Recovery

6.3.2 Acidic Condensate Recovery

6.4 Desalination & Water Treatment

6.4.1 Seawater Desalination (MSF, MED)

6.4.2 Industrial Wastewater Treatment

6.5 Condensation & Evaporation

6.6 Gas Cooling & Quenching

6.7 Ultra-High Purity Process Heating & Cooling

7. Global Polymer Heat Exchangers Market, by End-User Industry

7.1 Introduction

7.2 Chemical Processing

7.2.1 Inorganic Chemicals (Chlor-Alkali, Acids)

7.2.2 Specialty & Fine Chemicals

7.2.3 Petrochemicals & Refining

7.3 Pharmaceutical & Biotechnology

7.3.1 API Manufacturing

7.3.2 Bioprocessing & Fermentation

7.3.3 Sterile Water & CIP/SIP Systems

7.4 Food & Beverage

7.4.1 Dairy & Beverage Processing

7.4.2 Edible Oil & Sugar Processing

7.5 Power Generation

7.5.1 Flue Gas Desulfurization Systems

7.5.2 Nuclear Power Cooling Systems

7.6 Semiconductor & Electronics

7.6.1 Wet Process Chemical Distribution

7.6.2 Ultrapure Water (UPW) Temperature Control

7.7 HVAC & Refrigeration

8. Global Polymer Heat Exchangers Market, by Region

8.1 Introduction

8.2 North America

8.2.1 U.S.

8.2.2 Canada

8.3 Europe

8.3.1 Germany

8.3.2 U.K.

8.3.3 France

8.3.4 Netherlands

8.3.5 Belgium

8.3.6 Switzerland

8.3.7 Rest of Europe

8.4 Asia-Pacific

8.4.1 China

8.4.2 Japan

8.4.3 South Korea

8.4.4 Taiwan

8.4.5 India

8.4.6 Rest of Asia-Pacific

8.5 Latin America

8.5.1 Brazil

8.5.2 Mexico

8.5.3 Rest of Latin America

8.6 Middle East & Africa

8.6.1 Saudi Arabia

8.6.2 UAE

8.6.3 South Africa

8.6.4 Rest of Middle East & Africa

9. Competitive Landscape

9.1 Overview

9.2 Key Growth Strategies

9.3 Competitive Benchmarking

9.4 Competitive Dashboard

9.4.1 Industry Leaders

9.4.2 Market Differentiators

9.4.3 Vanguards

9.4.4 Emerging Companies

9.5 Market Ranking/Positioning Analysis of Key Players, 2025

10. Company Profiles

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

10.1 Ametek Fluoropolymer Products (AMETEK Inc.)

10.2 GESMEX GmbH

10.3 Bram-Cor SpA

10.4 Georg Fischer Piping Systems Ltd.

10.5 Alfa Laval AB

10.6 API Heat Transfer Inc.

10.7 Kelvion Holding GmbH

10.8 Mersen SA

10.9 Exergy LLC

10.10 Bosch Thermotechnology (Robert Bosch GmbH)

10.11 Polyplex Solutions (WMT & Associates)

10.12 Corrosion Resistant Products Ltd. (CRP)

10.13 ETEC GmbH

10.14 Celrad Plastic Heat Exchangers BV

10.15 Zhejiang Jiansheng Plastic Industry Co., Ltd.

11. Appendix

11.1 Questionnaire

11.2 Related Reports

Published Date: Oct-2024

Subscribe to get the latest industry updates