Resources

About Us

CNC Machine Tools Market Size, Share & Trends Analysis by Machine Type (CNC Turning, Milling, Grinding, Automation Level (Standalone, Semi-Automated), Application, End User, and Sales Channel - Global Opportunity Analysis & Industry Forecast (2026-2036)

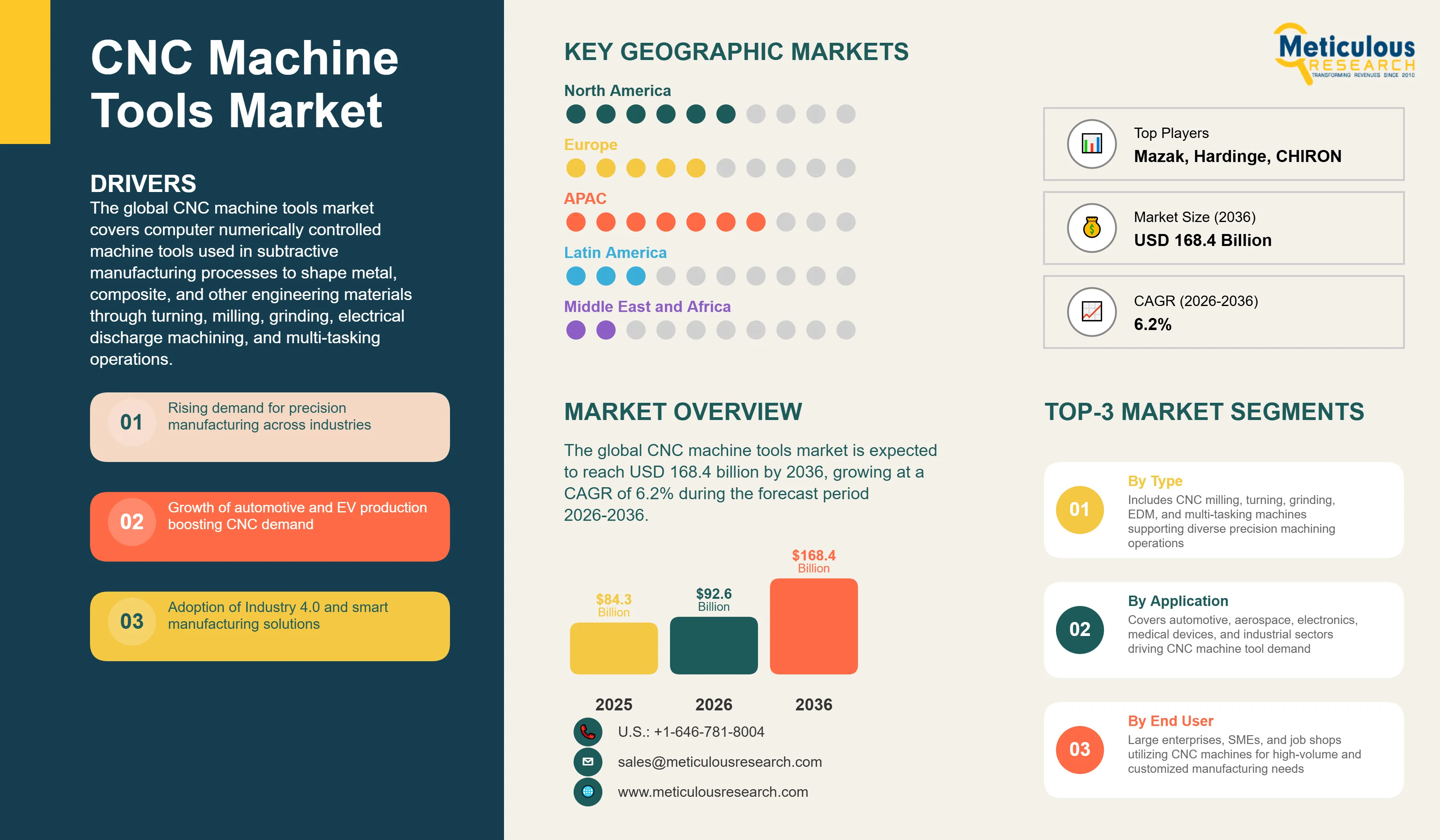

Report ID: MRSE - 1041896 Pages: 280 Apr-2026 Formats*: PDF Category: Semiconductor and Electronics Delivery: 24 to 72 Hours Download Free Sample ReportThe global CNC machine tools market was valued at USD 84.3 billion in 2025. This market is expected to reach USD 168.4 billion by 2036 from an estimated USD 92.6 billion in 2026, growing at a CAGR of 6.2% during the forecast period 2026-2036.

Click here to: Get Free Sample Pages of this Report

The global CNC machine tools market covers computer numerically controlled machine tools used in subtractive manufacturing processes to shape metal, composite, and other engineering materials through turning, milling, grinding, electrical discharge machining, and multi-tasking operations. The market encompasses the full range of CNC machine types from standard 2-axis and 3-axis turning lathes and machining centers through high-end 5-axis simultaneous machining centers, multi-tasking mill-turn machines, and advanced hybrid additive-subtractive platforms, together with the CNC control systems, drive systems, tooling, and automation and material handling systems that constitute complete CNC machining cell installations.

The growth of the global CNC machine tools market is primarily driven by the continuous global expansion of precision manufacturing output across the automotive, aerospace, electronics, and medical device industries that collectively represent the primary CNC machine tool end-user base and whose production volume growth directly drives machine tool investment cycles. The accelerating adoption of Industry 4.0 and smart manufacturing principles across global manufacturing operations is creating demand for the more capable, connected, and intelligent CNC machine platforms that integrate digital twin, predictive maintenance, adaptive process control, and MES connectivity features that enable manufacturers to achieve the productivity, quality, and operational efficiency improvements that smart manufacturing programs target.

Two significant opportunities are shaping the market's long-term trajectory. The integration of artificial intelligence and IoT connectivity into CNC machine platforms represents the most technically transformative near-term opportunity, enabling real-time adaptive process control, predictive tool wear monitoring, automated quality inspection, and connected factory data integration that fundamentally improve the productivity and quality output of CNC machining operations. The expanding adoption of additive-subtractive hybrid machine tools that combine metal additive manufacturing with precision CNC machining in a single platform represents a compelling opportunity for manufacturers requiring complex internal features, near-net-shape processing of expensive alloys, and part repair and remanufacturing capabilities that conventional subtractive-only CNC machining cannot address.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 168.4 Billion |

|

Market Size in 2026 |

USD 92.6 Billion |

|

Market Size in 2025 |

USD 84.3 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 6.2% |

|

Dominating Machine Type |

CNC Milling Machines |

|

Fastest Growing Machine Type |

Multi-Tasking Machines |

|

Dominating Axis Configuration |

3-Axis Machines |

|

Fastest Growing Axis Configuration |

5-Axis Machines |

|

Dominating Automation Level |

Standalone CNC Machines |

|

Fastest Growing Automation Level |

CNC Machines Integrated with Robotics |

|

Dominating Application |

Automotive |

|

Fastest Growing Application |

Medical Devices |

|

Dominating End User |

Large Enterprises |

|

Fastest Growing End User |

Small & Medium Enterprises (SMEs) |

|

Dominating Sales Channel |

Direct Sales (OEM) |

|

Fastest Growing Sales Channel |

Online/Platform-Based Sales |

|

Dominating Geography |

Asia-Pacific |

|

Fastest Growing Geography |

North America |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Integration of AI, IoT, and Digital Twin Technologies

The progressive integration of artificial intelligence, Internet of Things connectivity, and digital twin simulation into CNC machine tool platforms represents the most transformative technology trend reshaping the market. Modern CNC machine builders including DMG MORI, Mazak, Okuma, and FANUC are incorporating machine learning-based adaptive process control systems that monitor spindle load, cutting force, vibration signatures, and thermal compensation parameters in real time to automatically optimize cutting conditions, extend tool life, and prevent machining defects without requiring operator intervention. Predictive maintenance systems that analyze machine component vibration, temperature, and performance data against trained failure models can predict bearing, spindle, and drive system failures with sufficient advance warning to schedule maintenance during planned downtime rather than experiencing unplanned production stoppages that generate far higher economic impact than the maintenance activity itself.

Digital twin platforms that create synchronized virtual models of physical CNC machines enable manufacturers to simulate machining processes in software before executing them on the physical machine, verifying NC program correctness, optimizing cutting parameters for minimum cycle time and tool wear, and detecting potential collisions between the workpiece, tooling, and machine structure without risking actual machine damage or workpiece scrap. FANUC's MT-LINKi and FIELD system, DMG MORI's CELOS digital platform, and Mazak's Smooth Technology suite represent the leading commercial implementations of smart CNC machine platforms incorporating these connected intelligence capabilities, and the competitive pressure to match these digital capabilities is driving IoT and AI feature adoption across the broader machine tool industry globally.

Accelerating Adoption of 5-Axis and Multi-Tasking Machining

The manufacturing industry's accelerating transition from conventional 3-axis machining with multiple workpiece setups toward 5-axis simultaneous machining and multi-tasking mill-turn operations represents a productivity transformation trend that is driving both upgrading of existing machine inventories and new machine investment with substantially higher per-unit value. Five-axis simultaneous machining allows complex contoured surfaces, undercuts, and multi-face features to be machined in a single workpiece setup that eliminates the repositioning errors, setup time, and work-in-progress handling costs associated with multi-operation 3-axis machining sequences. For aerospace structural components, turbine blades, medical implants, and precision die and mold production, the dimensional accuracy improvement achieved by eliminating repositioning is commercially critical and is driving strong conversion from 3-axis to 5-axis machining across these precision manufacturing applications.

Multi-tasking mill-turn machines that perform both turning and milling operations, and in advanced configurations also grinding, gear cutting, and laser processing, represent the highest value-added segment of the CNC machine tool market and are growing rapidly in adoption across precision component manufacturing for aerospace, medical, and automotive applications. The ability to complete a complex part in a single machine setup reduces total machining cycle time, eliminates inter-operation handling and fixturing, and improves dimensional accuracy by maintaining a single datum reference throughout the complete machining sequence. Leading multi-tasking machine builders including Mazak's Integrex series, DMG MORI's NTX series, and Okuma's MULTUS series are competing on the breadth of operations integratable in a single platform and the sophistication of CAM software support for complex multi-tasking programming.

Manufacturing Reshoring and Industrial Policy-Driven Demand

The global trend of strategic manufacturing reshoring to domestic or allied-country production locations, accelerated by supply chain vulnerability experiences during COVID-19, semiconductor supply disruptions, and geopolitical trade tensions, is creating an important structural demand driver for CNC machine tool investment in North America, Europe, and allied manufacturing economies. The U.S. CHIPS and Science Act's USD 52 billion commitment to domestic semiconductor manufacturing, the Inflation Reduction Act's incentives for domestic electric vehicle and battery manufacturing, and defense industrial base expansion programs collectively represent hundreds of billions of dollars of new U.S. manufacturing facility investment that will require extensive CNC machine tool procurement to equip production operations. European strategic autonomy initiatives in semiconductor manufacturing, defense industrial production, and critical component supply are generating equivalent reshoring-driven manufacturing investment in Germany, France, Italy, and other EU member states.

The reshoring trend is particularly beneficial for premium CNC machine tool builders including DMG MORI, Mazak, Haas, Okuma, and European manufacturers, as new high-value manufacturing facilities for semiconductors, aerospace, defense, and medical devices typically specify the highest-capability 5-axis and multi-tasking machine platforms with full digital connectivity and automation integration that represent the highest per-machine revenue and margin positions in the market. Government procurement programs for reshored defense and strategic manufacturing also tend to specify domestically produced or allied-nation manufactured machine tools, creating preferential market access for machine builders with domestic production operations in the reshoring destination countries.

Increasing Demand for High-Precision Manufacturing

The fundamental and growing requirement for dimensional precision, surface finish quality, and geometric accuracy in manufactured components across the aerospace, medical device, semiconductor equipment, and precision mechanical engineering industries is the primary demand driver of the CNC machine tools market, as CNC machining is the dominant production technology capable of achieving the micrometer-level tolerances and sub-micron surface roughness specifications that define product quality in these high-value manufacturing sectors. Aerospace structural components machined from titanium and aluminum alloys require dimensional tolerances of plus or minus 5 to 25 micrometers across complex three-dimensional surfaces that only high-performance multi-axis CNC machining centers can reliably achieve in production environments. Medical implant components including orthopedic hip and knee joint replacements require surface finish values below 0.1 micrometers Ra and dimensional tolerances of 2 to 10 micrometers that demand the most precise CNC grinding and finishing machine platforms available. The progressive tightening of precision requirements across manufacturing sectors as product performance demands increase and component miniaturization advances is creating sustained demand for higher-capability and more precise CNC machine tools that continuously renews the machine tool investment cycle.

Rising Adoption of Industry 4.0 and Smart Manufacturing

The accelerating global adoption of Industry 4.0 principles across manufacturing operations is creating demand for CNC machine tool platforms with the digital connectivity, data generation, and intelligent processing capabilities required to participate in smart factory architectures where machines communicate production data, quality metrics, and operational status continuously to manufacturing execution systems, quality management platforms, and enterprise resource planning systems. Smart manufacturing programs that target real-time production visibility, automated quality control, predictive maintenance, and adaptive process optimization require CNC machines equipped with standardized communication protocols including OPC-UA and MTConnect, embedded IoT sensors and data acquisition systems, edge computing capability for local data processing, and open software interfaces that allow integration with third-party analytics and automation platforms. Machine builders that have invested in developing compelling smart manufacturing platform capabilities are gaining competitive advantage in the market segments where manufacturers have active Industry 4.0 transformation programs, and the growing proportion of CNC machine procurement decisions where digital connectivity and smart features are primary evaluation criteria is expanding the revenue premium that advanced digital machine platforms can command relative to conventional machines.

Integration of AI and IoT in CNC Machines

The commercial integration of artificial intelligence and IoT connectivity into CNC machine tool platforms represents the highest-value technology upgrade opportunity in the current market cycle, enabling the development of adaptive process control, predictive maintenance, and connected factory integration capabilities that justify premium pricing and create strong customer switching costs through deep integration with manufacturing data infrastructure. AI-enabled adaptive cutting parameter optimization systems that continuously adjust feed rate, spindle speed, and depth of cut based on real-time cutting force and vibration feedback can improve machining productivity by 15 to 30% relative to fixed-parameter programs while simultaneously extending tool life and reducing scrap rates. Predictive maintenance AI systems trained on large fleets of installed machines can detect impending failures with 90% or higher accuracy weeks before failure occurrence, enabling maintenance scheduling that virtually eliminates unplanned downtime in production-critical machining operations. CNC machine builders that develop compelling AI and IoT capability packages, validated by demonstrated productivity and cost improvement results in customer applications, are positioned to command premium pricing that improves market revenue and margin performance while creating compelling upgrade and service revenue streams from the large installed base of legacy machines.

Growth of Additive-Subtractive Hybrid Machines

The development of hybrid machine tool platforms that combine directed energy deposition or powder bed fusion additive manufacturing with precision CNC subtractive machining in a single integrated platform represents a commercially compelling technology opportunity that addresses manufacturing requirements that neither pure additive nor pure subtractive processes can satisfy individually. Hybrid machining enables the near-net-shape deposition of complex internal geometries including cooling channels, lattice structures, and internal cavities using additive processes, followed by precision CNC finish machining of exterior surfaces and precision features to final dimensional and surface finish specifications, in a single integrated workflow that eliminates the handling, fixturing, and datum transfer operations required when additive and subtractive processes are performed on separate machines. Key aerospace applications including turbine blade repair and modification, large structural titanium component fabrication from wire-arc additive deposition, and tooling manufacture with conformal cooling channels are driving the commercial adoption of hybrid machines from DMG MORI's LASERTEC series, Mazak's Integrex i-AM series, and specialist hybrid machine builders. The growing availability of hybrid machine platforms at competitive price points relative to standalone additive systems plus dedicated CNC finishing machines is expanding the market beyond early-adopter aerospace and die and mold applications into broader precision engineering and contract manufacturing markets.

By Machine Type: In 2026, CNC Milling Machines to Dominate

Based on machine type, the global CNC machine tools market is segmented into CNC turning machines, CNC milling machines, CNC grinding machines, CNC electrical discharge machines, multi-tasking machines, and other CNC machine tools. In 2026, the CNC milling machines segment is expected to account for the largest share of the global CNC machine tools market. The large share of this segment is attributed to vertical machining centers and horizontal machining centers representing the most versatile and universally adopted CNC machine platform across all manufacturing industries, from small job shops operating single VMCs for prototype and short-run production to large automotive and aerospace facilities deploying hundreds of HMCs in flexible manufacturing systems for high-volume precision component production. The breadth of applications addressed by CNC milling platforms, spanning prismatic part machining, mold and die production, structural component manufacture, and precision feature generation, generates the highest aggregate demand volume of any CNC machine type.

However, the multi-tasking machines segment is poised to register the highest CAGR during the forecast period. The high growth of this segment is attributed to the compelling productivity and accuracy advantages of mill-turn and hybrid multi-tasking platforms over conventional multi-operation machining sequences, the strong adoption by aerospace, medical, and precision engineering manufacturers seeking to reduce work-in-progress inventory and improve dimensional accuracy through single-setup machining, and the expanding portfolio of commercially available multi-tasking platforms at progressively more accessible price points from major machine builders including Mazak, DMG MORI, and Okuma.

By Axis Configuration: In 2026, 3-Axis Machines to Hold the Largest Share

Based on axis configuration, the global CNC machine tools market is segmented into 2-axis, 3-axis, 4-axis, 5-axis, and multi-axis machines. In 2026, the 3-axis machines segment is expected to account for the largest share of the global CNC machine tools market. The dominance of 3-axis machines reflects their position as the standard configuration for the majority of prismatic part machining operations in automotive, general engineering, mold production, and electronics manufacturing applications where three-axis interpolation provides adequate machining capability for the feature geometry required and represents the lowest acquisition cost and programming complexity entry point for the large global population of small and medium manufacturing enterprises procuring CNC machining capability.

However, the 5-axis machines segment is projected to register the highest CAGR during the forecast period. This growth is driven by the aerospace industry's mandatory requirement for 5-axis simultaneous machining of structural components, turbine blades, and engine casings, the medical device industry's adoption of 5-axis machining for orthopedic implants and complex surgical instruments, and the progressive reduction in 5-axis machine acquisition cost relative to 3-axis machines as competition among machine builders intensifies and manufacturing volumes increase, making 5-axis machining economically accessible to a broader range of manufacturers.

By Automation Level: In 2026, Standalone CNC Machines to Hold the Largest Share

Based on automation level, the global CNC machine tools market is segmented into standalone CNC machines, semi-automated machines, fully automated CNC systems, and CNC machines integrated with robotics. In 2026, the standalone CNC machines segment is expected to account for the largest share of the global CNC machine tools market. The dominance of standalone machines reflects the large global installed base and ongoing procurement of individual CNC machining centers, lathes, and grinding machines by the broad population of contract manufacturers, job shops, small and medium enterprises, and educational and research institutions that represent the numerically largest segment of the global CNC machine tool customer base and that predominantly operate individual machines rather than integrated automated cells.

However, the CNC machines integrated with robotics segment is projected to register the highest CAGR during the forecast period. This growth is driven by the manufacturing industry's accelerating adoption of robot-tended machine tool cells that automate workpiece loading and unloading operations to enable unattended extended-shift machining, the compelling productivity and labor cost economics of robotic automation in markets with high manufacturing labor costs, and the improving ease of robot-machine integration enabled by collaborative robot platforms from FANUC, KUKA, Universal Robots, and ABB that reduce integration complexity and programming effort compared with conventional industrial robot automation.

By Application: In 2026, Automotive to Hold the Largest Share

Based on application, the global CNC machine tools market is segmented into automotive, aerospace and defense, electronics and semiconductor, medical devices, industrial machinery, energy and power, and others. In 2026, the automotive segment is expected to account for the largest share of the global CNC machine tools market. The automotive industry's position as the dominant CNC machine tool end user reflects its enormous global production scale, with approximately 80 to 90 million vehicles produced annually requiring CNC-machined powertrain components, structural parts, brake system components, and transmission housings in very high volumes, and its accelerating transition to electric vehicle production that is generating substantial new CNC machine investment for EV motor housings, battery enclosures, and gearbox components that differ in design from combustion engine equivalents and require new machining capacity.

However, the medical devices segment is projected to register the highest CAGR during the forecast period. This growth is driven by the rapidly growing global demand for orthopedic implants, dental prosthetics, surgical instruments, and precision medical device components in aging developed-market populations and expanding middle-class healthcare access in emerging markets, the stringent dimensional and surface finish specifications of medical components that can only be achieved through CNC machining, and the short product development cycles of medical device companies that require flexible high-mix low-volume CNC machining capability with rapid changeover and full process documentation capabilities.

By End User: In 2026, Large Enterprises to Hold the Largest Share

Based on end user, the global CNC machine tools market is segmented into large enterprises, small and medium enterprises, and contract manufacturing and job shops. In 2026, the large enterprises segment is expected to account for the largest share of the global CNC machine tools market. Large manufacturing enterprises including automotive OEMs and Tier 1 suppliers, aerospace prime contractors and major tier suppliers, large electronics and semiconductor manufacturers, and major industrial equipment producers represent the highest per-account CNC machine procurement volumes, purchasing machines in quantities from dozens to hundreds per capital expenditure cycle and specifying the most capable and highest-value machine configurations with full automation, connectivity, and tooling packages.

However, the SMEs segment is projected to register the highest CAGR during the forecast period. This growth is driven by the progressive expansion of CNC machine tool adoption into small and medium manufacturing companies in developing manufacturing economies including India, Vietnam, Indonesia, and Mexico where industrialization and manufacturing capability development are creating large new CNC machine tool demand centers, the availability of increasingly capable and affordable CNC machine platforms from Asian manufacturers that are making CNC machining accessible to smaller enterprises at lower capital thresholds, and the growth of SME manufacturing in developed markets supported by reshoring trends and defense subcontract opportunities.

By Sales Channel: In 2026, Direct Sales (OEM) to Hold the Largest Share

Based on sales channel, the global CNC machine tools market is segmented into direct sales, distributor and dealer networks, and online and platform-based sales. In 2026, the direct sales segment is expected to account for the largest share of the global CNC machine tools market. Direct OEM sales relationships characterize the procurement model of large enterprise customers who purchase high volumes of machines, require customized application engineering support, negotiate enterprise-level service agreements, and benefit from the factory direct pricing, financing arrangements, and technical collaboration that machine builder direct sales teams facilitate. The high per-unit value and technical complexity of CNC machine tool transactions, particularly for multi-axis and automated systems, make direct sales relationships the preferred procurement model for the highest-value customer accounts.

However, the online and platform-based sales segment is projected to register the highest CAGR during the forecast period. This growth is driven by the emergence of industrial machine tool e-commerce platforms and digital procurement channels that are improving market access for SME buyers, the increasing availability of standard CNC machine models through online channels at transparent pricing that appeals to technically confident buyers seeking efficient procurement without traditional dealer interactions, and the growing adoption of digital product configurators and virtual application demonstrations by machine builders targeting broader market reach beyond their direct sales force coverage areas.

CNC Machine Tools Market by Region: Asia-Pacific Leading by Share, North America by Growth

Based on geography, the global CNC machine tools market is segmented into Asia-Pacific, Europe, North America, Latin America, and the Middle East and Africa.

In 2026, Asia-Pacific is expected to account for the largest share of the global CNC machine tools market. The largest share of this region is mainly due to China's position as both the world's largest CNC machine tool producer and the world's largest consumer, with domestic machine tool consumption driven by the country's enormous manufacturing sector spanning automotive, electronics, aerospace, and general engineering industries that collectively generate annual CNC machine procurement volumes exceeding those of any other country by a substantial margin. Japanese machine tool makers including Mazak, Makino, Okuma, FANUC, and Mori Seiki represent the global technology leaders in precision CNC machine design and are major export contributors to the region's market value. South Korea's advanced manufacturing sector anchored by automotive and electronics industries, Taiwan's precision machine tool manufacturing industry including leading makers like Hiwin and Victor Taichung, and the rapidly expanding manufacturing sectors of India, Vietnam, Thailand, and Indonesia are all contributing to Asia-Pacific's dominant regional market position. China's domestic machine tool builders including Shenyang Machine Tool, Dalian Machine Tool, and Haitian Precision are also significant market participants competing on cost-competitive platforms for the mid-tier and value manufacturing segments.

However, the North American CNC machine tools market is expected to grow at the fastest CAGR during the forecast period. North America's rapid growth is driven by the manufacturing reshoring wave catalyzed by the CHIPS and Science Act, Inflation Reduction Act, and defense industrial base expansion programs that are bringing semiconductor, EV, battery, and defense component manufacturing capacity back to the United States and Mexico at a scale and speed unprecedented in recent manufacturing history. Each new fab, EV assembly plant, battery gigafactory, and defense production facility represents a major CNC machine tool procurement program for equipping production lines, and the concentration of multiple simultaneous large-scale manufacturing facility investments in the 2025 to 2030 period is creating a sustained period of above-trend CNC machine demand in the North American market. The U.S. and Mexican manufacturing sectors are also benefiting from nearshoring supply chain diversification by Asian and European manufacturers seeking production presence in the Americas, adding further manufacturing investment and CNC machine procurement activity to the regional market.

Europe represents the second-largest and most technically sophisticated regional CNC machine tools market, led by Germany's world-class precision engineering manufacturing sector and its concentration of both machine tool builders and machine tool users among the highest-value and most technically demanding industrial customer groups globally. Germany's mechanical engineering, automotive, aerospace, and energy equipment industries represent the most intensive CNC machine tool users in Europe, and German machine builders including DMG MORI, CHIRON, EMAG, and Trumpf supply both the domestic market and global export markets with premium machine platforms. Italy's strong precision manufacturing tradition in general engineering, packaging machinery, and automotive components, Switzerland's watchmaking, medical device, and high-precision engineering industries, and the growing manufacturing sectors of Poland and Czech Republic as part of Central Europe's expanding industrial base collectively contribute to Europe's significant and stable CNC machine tool market position.

The global CNC machine tools market is moderately fragmented, with a tier of global premium machine builders competing on technology performance, digital capability, and application expertise, alongside a large number of regional and cost-competitive manufacturers serving mid-range and volume market segments. Competition is focused on machining accuracy and repeatability, spindle performance, control system capability, digital connectivity and smart manufacturing features, axis configuration range, automation integration options, and the depth of application engineering and service support that premium end-user customers require.

DMG MORI leads the global premium CNC machine market through the broadest portfolio of turning, milling, 5-axis, multi-tasking, and laser processing platforms combined with the CELOS digital platform providing comprehensive machine connectivity and smart manufacturing capabilities. Mazak competes globally across turning, milling, multi-tasking, and laser machine categories with its Smooth Technology CNC control suite and iSMART Factory connectivity platform. FANUC occupies a unique dual role as both a CNC control system supplier to the majority of machine builders globally and a direct CNC machine manufacturer through its Robodrill and Robocut product lines. Haas Automation has established the largest market position in the mid-range machining center segment in the United States through its direct sales model and competitive value pricing. Okuma's OSP CNC control system with its Thermo-Friendly Concept thermal compensation and machining simulation capabilities differentiates its product offering across the turning and milling machine range.

The report provides a comprehensive competitive analysis based on an extensive assessment of leading players' product portfolios, geographic presence, technology capabilities, and key strategic developments. Some of the key players operating in the global CNC machine tools market include DMG MORI Co. Ltd. (Japan/Germany), Mazak Corporation (Japan), Haas Automation Inc. (U.S.), Okuma Corporation (Japan), FANUC Corporation (Japan), Makino Milling Machine Co. Ltd. (Japan), Doosan Machine Tools (South Korea), Hyundai WIA Corporation (South Korea), GF Machining Solutions (Switzerland), Hurco Companies Inc. (U.S.), Hardinge Inc. (U.S.), EMAG GmbH & Co. KG (Germany), Yamazaki Mazak Corporation (Japan), CHIRON Group SE (Germany), and Fives Group (France), among others.

The global CNC machine tools market is expected to reach USD 168.4 billion by 2036 from an estimated USD 92.6 billion in 2026, at a CAGR of 6.2% during the forecast period 2026-2036.

In 2026, the CNC milling machines segment is expected to hold the largest share of the global CNC machine tools market, driven by vertical and horizontal machining centers representing the most versatile and universally adopted CNC machine platform across all manufacturing industries.

The multi-tasking machines segment is expected to register the highest CAGR during the forecast period 2026-2036, driven by the strong manufacturing demand for mill-turn and hybrid platforms that reduce part handling, improve dimensional accuracy through single-setup machining, and deliver productivity advantages for complex precision components in aerospace, medical, and precision engineering applications.

In 2026, the 3-axis machines segment is expected to hold the largest share of the global CNC machine tools market, reflecting the 3-axis machining center's dominant position as the standard configuration for the majority of prismatic part machining applications across manufacturing industries globally.

In 2026, the automotive segment is expected to hold the largest share of the global CNC machine tools market, driven by automotive's enormous global production scale and the significant new CNC machine investment being generated by the transition to electric vehicle production.

The growth of this market is primarily driven by the continuous global expansion of precision manufacturing output across automotive, aerospace, electronics, and medical device industries generating sustained CNC machine investment demand, the accelerating adoption of Industry 4.0 and smart manufacturing creating preference for digitally connected and AI-capable CNC platforms, and the large-scale manufacturing reshoring programs in North America and Europe generating above-trend CNC machine procurement for new high-value production facilities.

Key players are DMG MORI Co. Ltd. (Japan/Germany), Mazak Corporation (Japan), Haas Automation Inc. (U.S.), Okuma Corporation (Japan), FANUC Corporation (Japan), Makino Milling Machine Co. Ltd. (Japan), Doosan Machine Tools (South Korea), Hyundai WIA Corporation (South Korea), GF Machining Solutions (Switzerland), Hurco Companies Inc. (U.S.), Hardinge Inc. (U.S.), EMAG GmbH & Co. KG (Germany), Yamazaki Mazak Corporation (Japan), CHIRON Group SE (Germany), and Fives Group (France), among others.

North America is expected to register the highest growth rate in the global CNC machine tools market during the forecast period 2026-2036, driven by the manufacturing reshoring wave catalyzed by the CHIPS Act, Inflation Reduction Act, and defense industrial base expansion programs creating large-scale new CNC machine procurement demand for semiconductor, EV, battery, and defense manufacturing facilities.

Published Date: Feb-2026

Published Date: Sep-2023

Published Date: Oct-2022

Published Date: Oct-2024

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates