Resources

About Us

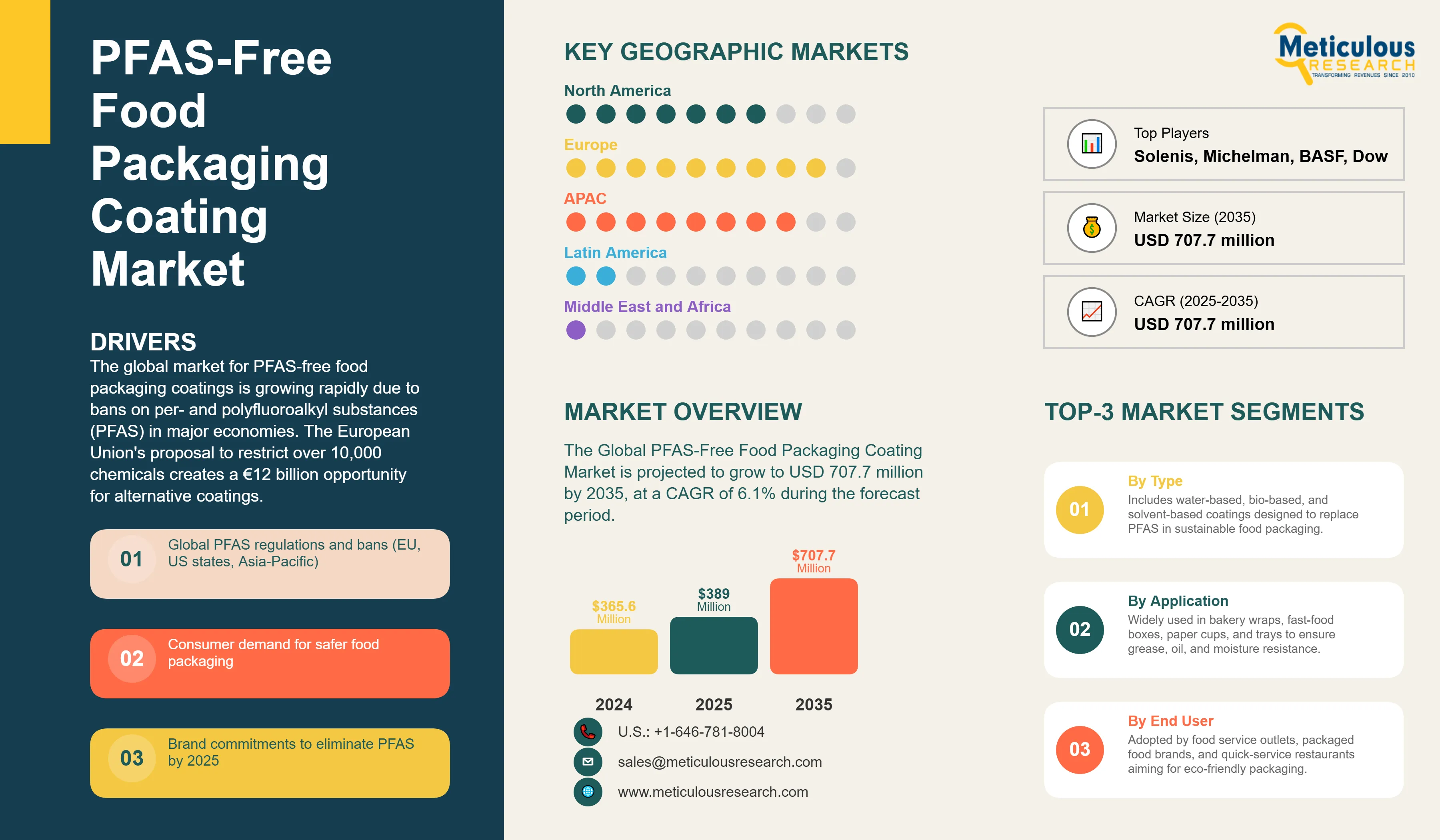

The Global PFAS-Free Food Packaging Coating Market was valued at USD 365.6 million in 2024. The PFAS-free coating market for food packaging is estimated to reach USD 389.0 million in 2025 and is projected to grow to USD 707.7 million by 2035, at a CAGR of 6.1% during the forecast period.

Global PFAS-Free Food Packaging Coating Market 2025 - Key Statistics

|

Metric |

Value |

|

Market Value (2025) |

USD 389 million |

|

Market Value (2035) |

USD 707.7 million |

|

CAGR (2025-2035) |

6.1% |

|

Largest Coating Type |

Water-Based Dispersions (30-40% share) |

|

Fastest Growing Segment |

Bio-Based Coatings (8.7% CAGR) |

|

Leading Application |

Quick Service Restaurants (40-50% share) |

|

Dominant Substrate |

Paper and Paperboard (60-65% share) |

|

Top Region by Market Size |

Europe (35-40% share) |

|

Fastest Growth Region |

Asia-Pacific (7.8% CAGR) |

Global PFAS-Free Food Packaging Coating Market Overview

Click here to: Get Free Sample Pages of this Report

Why is the Global PFAS-Free Food Packaging Coating Market Growing Rapidly?

Global PFAS-Free Food Packaging Coating Market Size, Growth Projections and Forecast Analysis

|

Metric |

Value |

|

Global PFAS-Free Coating Market Value (2025) |

USD 389 million |

|

PFAS Alternative Coating Market Forecast (2035) |

USD 707.7 million |

|

Forever Chemical-Free Packaging CAGR (2025-2035) |

6.1% |

Market Segmentation - Global PFAS-Free Food Packaging Coating Market

The global PFAS-free food packaging coating market is divided into several categories. These include coating type, substrate material, application technology, end-use application, industry vertical, and geographic region. The types of coatings are water-based dispersions, bio-based polymers, wax coatings, clay-based barriers, and silicone alternatives. The substrates include paper/paperboard, molded fiber, flexible films, metal, and glass. The technologies used are extrusion coating, dispersion application, solution coating, and vacuum deposition. The applications involve QSR packaging, retail food, E-commerce delivery, and institutional service.

Water-Based Dispersions Lead PFAS-Free Coating Market with 30-40% Share in 2025

Quick Service Restaurant Applications Drive 40-50% of PFAS-Free Coating Demand

Quick service restaurants (QSR) will account for 40-50% of global PFAS-free coating demand in 2025. This demand is driven by the need for high-volume packaging and direct food contact standards. The QSR industry uses over 250 billion food packaging units each year. It faces strict performance requirements for hot, greasy foods, which creates technical challenges for PFAS alternatives.

McDonald's has publicly committed to removing PFAS chemicals from all guest packaging worldwide by 2025. This decision comes after pressure from public health advocates and campaigns that highlighted the presence of PFAS in common packaging, like Big Mac boxes and fries bags. The company has also been phasing out other harmful chemicals such as BPA, BPS, and phthalates from its packaging as part of a wider push for sustainability and product responsibility. With over 38,000 restaurants globally, this commitment will significantly impact the reduction of PFAS in food packaging worldwide.

European Market Leads Global PFAS-Free Food Packaging Coating Market with 35-40% Market Share

Key Market Drivers, Restraints, and Emerging Trends in PFAS-Free Food Packaging Coating Market

The global PFAS-free food packaging coating market is mainly driven by the new regulations, consumer preferences, technological advancements, and company pledges to be more sustainable. Challenges involve improving performance, managing costs, and changing supply chains. New trends highlight the use of bio-based materials, applications of nanotechnology, and circular design principles.

Impact of Key Growth Drivers and Restraints on PFAS-Free Coating Market

Base CAGR: 6.1%

PFAS-Free Coating Market Drivers

|

Driver |

CAGR Impact |

Key Factors |

|

Regulatory Bans & Restrictions |

+2.1% |

|

|

Brand & Retailer Commitments |

+1.5% |

|

|

Consumer Health Awareness |

+1.2% |

|

|

Technology Innovation |

+1.1% |

|

PFAS-Free Packaging Market Restraints

|

Restraint |

CAGR Impact |

Mitigation Strategies |

|

Performance Limitations |

-1.6% |

|

|

Cost Premiums |

-1.3% |

|

|

Technical Adoption Barriers |

-0.9% |

|

Competitive Landscape - Leading PFAS-Free Coating Manufacturers and Innovators

The global PFAS-free food packaging coating market is highly competitive. It includes specialty chemical companies, coating manufacturers, bio-material innovators, and packaging converters that are creating sustainable solutions.

Solenis is a leading company in specialty chemicals. They offer a range of eco-friendly, PFAS-free barrier coatings for food and beverage packaging. Their TopScreen™ technology features multi-layer barrier coatings designed for molded pulp and paper packaging applications. These coatings provide resistance to water, oil, and grease while ensuring recyclability and compostability. Solenis also helps converters and brands meet changing sustainability and regulatory needs with their expertise and resources.

Michelman is a known supplier of water-based barrier coatings that are PFAS-free and safe for food contact. Their Michem Coatings include options that resist oil and grease while maintaining recyclability and printability for fiber-based flexible and rigid packaging. Michelman works closely with packaging converters and industry partners to create solutions that replace polyethylene (PE) and other non-recyclable materials. They aim for circular packaging designs.

Large chemical companies like BASF, Dow, and Arkema are making significant investments in bio-based, sustainable barrier technologies. BASF's ecovio® portfolio combines biodegradable polymers with mineral fillers to provide effective barrier performance for frozen food packaging. Dow’s RHOBARR® series emphasizes recyclability while effectively blocking oil and moisture.

Bio-material companies such as Novamont offer agricultural-based coatings like Mater-Bi®, which is made from corn starch. This product provides industrial compostability and grease resistance for food packaging. Cargill develops plant-based barrier coatings, leveraging extensive agricultural supply chains to ensure sourcing of sustainable raw materials.

Packaging converters and paper producers like Stora Enso and Sappi incorporate PFAS-free coatings directly into their fiber products. They provide complete solutions that reduce costs and improve quality control. Their integrated approach speeds up adoption by offering technical support and performance optimization services.

New startups like Notpla, which focuses on seaweed-based edible coatings, and Xampla, known for developing plant protein-based films, have gained significant investments and formed partnerships with major brands. They are pushing forward the commercialization of innovative, biodegradable, and PFAS-free packaging materials.

Recent Developments in Global PFAS-Free Food Packaging Coating Market 2024-2025

March 2025: Solenis LLC expanded its partnership with Zume to scale production of sustainable, PFAS-free molded fiber packaging for food service applications. The collaboration leverages Solenis’ expertise in functional additives and barrier coatings combined with Zume’s patented molded-fiber manufacturing.

September 2024: Heidelberg and Solenis announced a collaboration to develop a cost-effective process to integrate PFAS-free barrier coatings directly into flexible fibre-based paper packaging via roll-fed flexo printing using Heidelberg’s Boardmaster press.

|

Report Coverage |

Details |

|

Market Size (2025) |

USD 389 Million |

|

Coating Types |

Water-Based, Bio-Based, Wax, Clay, Silicone Alternatives |

|

Substrate Materials |

Paper/Paperboard, Molded Fiber, Flexible Films, Metal, Glass |

|

Technologies |

Extrusion, Dispersion, Solution Coating, Vacuum Deposition |

|

Applications |

QSR, Retail Food, E-commerce, Institutional Service |

|

End-Use Industries |

Food Service, Manufacturing, Retail, Delivery Services |

|

Geographic Coverage |

North America, Europe, Asia-Pacific, LATAM, MEA |

|

Key Companies |

Solenis, Michelman, BASF, Dow, Arkema, DSM, Cargill, Novamont |

|

Analysis Includes |

Regulatory impact, technology trends, sustainability metrics, competitive strategies, company profiles, market share/ranking analysis, Porter’s Five Forces analysis, key market trends and drivers |

The global PFAS-free food packaging coating market is valued at USD 389 million in 2025, replacing traditional fluorochemical coatings across food contact applications.

The PFAS-free coating market is projected to reach USD 707.7 million by 2035, driven by regulatory bans and brand commitments to eliminate forever chemicals.

The global PFAS-free food packaging coating market is expected to grow at 6.1% CAGR between 2025 and 2035.

Water-based dispersions command 30-40% market share, offering optimal performance-cost balance with existing application infrastructure.

Quick service restaurants represent 40-50% of demand, requiring high-performance alternatives for greasy food packaging across billions of units annually.

1. Market Definition & Scope

1.1. Market Definition

1.2. Market Ecosystem

1.3. Currency (USD)

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Process of Data Collection and Validation

2.2.1. Secondary Research

2.2.2. Primary Research/Interviews with Key Opinion Leaders from the Industry

2.3. Market Sizing and Forecast

2.3.1. Market Size Estimation Approach

2.3.1.1. Bottom-up Approach

2.3.1.2. Top-down Approach

2.3.2. Growth Forecast Approach

2.3.3. Assumptions for the Study

3. Executive Summary

3.1. Overview

3.2. Segmental Analysis

3.2.1. Global PFAS-Free Food Packaging Coating Market, by Coating Type

3.2.2. Global PFAS-Free Food Packaging Coating Market, by Substrate

3.2.3. Global PFAS-Free Food Packaging Coating Market, by Technology

3.2.4. Global PFAS-Free Food Packaging Coating Market, by Application

3.2.5. Global PFAS-Free Food Packaging Coating Market, by End-Use Industry

3.2.6. Global PFAS-Free Food Packaging Coating Market, by Region

3.3. Competitive Landscape

3.4. Strategic Recommendations

4. Market Insights

4.1. Overview

4.2. Factors Affecting Market Growth

4.2.1. Drivers

4.2.1.1. Global PFAS regulations and bans (EU, US states, Asia-Pacific)

4.2.1.2. Consumer demand for safer food packaging

4.2.1.3. Brand commitments to eliminate PFAS by 2025

4.2.1.4. Litigation risks and liability concerns

4.2.1.5. ESG requirements and sustainability goals

4.2.2. Restraints

4.2.2.1. Higher costs compared to traditional PFAS coatings

4.2.2.2. Performance gaps in oil and grease resistance

4.2.2.3. Limited production capacity for alternatives

4.2.2.4. Recycling and composability challenges

4.2.3. Opportunities

4.2.3.1. Bio-based coating innovation

4.2.3.2. Nanotechnology applications

4.2.3.3. Circular economy packaging solutions

4.2.3.4. Government incentives for sustainable packaging

4.2.4. Trends

4.2.4.1. Plant-based barrier coatings

4.2.4.2. Aqueous dispersion technologies

4.2.4.3. Multi-layer barrier systems

4.2.4.4. Smart packaging integration

4.2.5. Challenges

4.2.5.1. Achieving food safety certifications

4.2.5.2. Scaling production for global demand

4.2.5.3. Maintaining shelf life and product integrity

4.3. Porter's Five Forces Analysis

4.3.1. Bargaining Power of Suppliers

4.3.2. Bargaining Power of Buyers

4.3.3. Threat of Substitutes

4.3.4. Threat of New Entrants

4.3.5. Degree of Competition

4.4. Regulatory Landscape Impact on Global PFAS-Free Coating Market

4.4.1. Regional Regulations

4.4.1.1. EU REACH and Single-Use Plastics Directive

4.4.1.2. US EPA PFAS Strategic Roadmap

4.4.1.3. State-level PFAS bans (Maine, California, etc.)

4.4.1.4. Asia-Pacific regulations

4.4.2. Industry Standards and Certifications

4.4.2.1. FDA food contact regulations

4.4.2.2. BfR recommendations

4.4.2.3. Compostability standards (BPI, TÜV)

4.4.3. Future Regulatory Evolution

4.4.3.1. Global PFAS treaty considerations

4.4.3.2. Extended producer responsibility

4.4.3.3. Chemical transparency requirements

5. Impact of Sustainability on Global PFAS-Free Food Packaging Coating Market

5.1. Elimination of forever chemicals from food chain

5.2. Biodegradability and compostability enhancement

5.3. Carbon footprint reduction through bio-based materials

5.4. Water protection and environmental remediation

5.5. Circular economy integration

5.6. Life cycle assessment improvements

5.7. Contribution to UN SDGs and corporate sustainability targets

6. Competitive Landscape

6.1. Overview

6.2. Key Growth Strategies

6.3. Competitive Benchmarking

6.4. Competitive Dashboard

6.4.1. Market Leaders

6.4.2. Innovation Champions

6.4.3. Regional Specialists

6.4.4. Emerging Players

6.5. Market Share/Ranking Analysis, by Key Players, 2024

6.6. Mergers, Acquisitions, Partnerships & Licensing Activity

6.7. Technology Roadmap: PFAS-Free Coating Solutions to 2030

7. Global PFAS-Free Food Packaging Coating Market Assessment—By Coating Type

7.1. Overview

7.2. Water-Based Coatings

7.2.1. Acrylic Dispersions

7.2.2. Polyurethane Dispersions

7.2.3. Styrene-Acrylic Copolymers

7.3. Bio-Based Coatings

7.3.1. Polylactic Acid (PLA) Coatings

7.3.2. Polyhydroxyalkanoates (PHA)

7.3.3. Chitosan-Based Coatings

7.3.4. Alginate Coatings

7.4. Wax-Based Coatings

7.4.1. Natural Waxes

7.4.2. Synthetic Waxes

7.5. Clay-Based Coatings

7.6. Silicone-Based Coatings

7.7. Others

7.7.1. Protein-Based Coatings

7.7.2. Nanocellulose Coatings

8. Global PFAS-Free Food Packaging Coating Market Assessment—By Substrate

8.1. Overview

8.2. Paper and Paperboard

8.2.1. Corrugated Board

8.2.2. Folding Cartons

8.2.3. Food Service Paper

8.3. Molded Fiber

8.3.1. Bagasse

8.3.2. Bamboo

8.3.3. Wheat Straw

8.4. Flexible Packaging

8.5. Metal

8.6. Glass

8.7. Others

9. Global PFAS-Free Food Packaging Coating Market Assessment—By Technology

9.1. Overview

9.2. Extrusion Coating

9.3. Dispersion Coating

9.4. Solution Coating

9.5. Vacuum Deposition

9.6. Lamination

9.7. Others

10. Global PFAS-Free Food Packaging Coating Market Assessment—By Application

10.1. Overview

10.2. Quick Service Restaurants (QSR)

10.3. Retail Food Packaging

10.4. E-commerce Food Delivery

10.5. Institutional Food Service

10.6. Others

11. Global PFAS-Free Food Packaging Coating Market Assessment—By End-Use Industry

11.1. Overview

11.2. Food Service Industry

11.3. Food Manufacturing

11.4. Retail and Grocery

11.5. E-commerce and Delivery Services

11.6. Institutional and Catering

11.7. Others

12. Global PFAS-Free Food Packaging Coating Market Assessment—By Region

12.1. Overview

12.2. North America

12.2.1. United States

12.2.2. Canada

12.2.3. Mexico

12.3. Europe

12.3.1. Germany

12.3.2. France

12.3.3. United Kingdom

12.3.4. Netherlands

12.3.5. Denmark

12.3.6. Sweden

12.3.7. Italy

12.3.8. Spain

12.3.9. Rest of Europe

12.4. Asia-Pacific

12.4.1. China

12.4.2. Japan

12.4.3. South Korea

12.4.4. India

12.4.5. Australia

12.4.6. New Zealand

12.4.7. Southeast Asia

12.4.8. Rest of Asia-Pacific

12.5. Latin America

12.5.1. Brazil

12.5.2. Argentina

12.5.3. Rest of Latin America

12.6. Middle East & Africa

12.6.1. GCC Countries

12.6.2. South Africa

12.6.3. Rest of MEA

13. Company Profiles (Business Overview, Financial Overview, Product Portfolio, Strategic Developments, and SWOT Analysis)

13.1. Solenis LLC

13.2. Michelman Inc.

13.3. BASF SE

13.4. Dow Inc.

13.5. Arkema S.A.

13.6. Evonik Industries AG

13.7. Clariant AG

13.8. Celanese Corporation

13.9. AkzoNobel N.V.

13.10. H.B. Fuller Company

13.11. Mitsubishi Chemical Group

13.12. Stora Enso Oyj

13.13. WestRock Company

13.14. Sappi Limited

13.15. ITC Limited (Paperboards and Specialty Papers Division)

13.16. Nippon Paper Industries Co., Ltd.

13.17. Cargill Incorporated

13.18. Novamont S.p.A.

13.19. Paramelt B.V.

13.20. Omya AG

13.21. Imerys S.A.

13.22. Cork Industries

13.23. Others

14. Appendix

14.1. Available Customization

14.2. Related Reports

Published Date: Apr-2026

Published Date: Feb-2026

Published Date: Nov-2024

Published Date: Nov-2024

Published Date: Oct-2024

Subscribe to get the latest industry updates