Resources

About Us

Mental-Care & Nootropic Ingredients Market by Ingredient Type (Botanical Extracts/Adaptogens, Amino Acids, Vitamins & Minerals, Synthetic Nootropics), Function (Stress/Anxiety Relief, Mood Enhancement, Cognitive Performance, Application, and Distribution Channel - Global Forecast to 2035

Report ID: MRFB - 1041624 Pages: 369 Jan-2026 Formats*: PDF Category: Food and Beverages Delivery: 2 to 4 Hours Download Free Sample ReportMental-Care & Nootropic Ingredients Market Size & Forecast

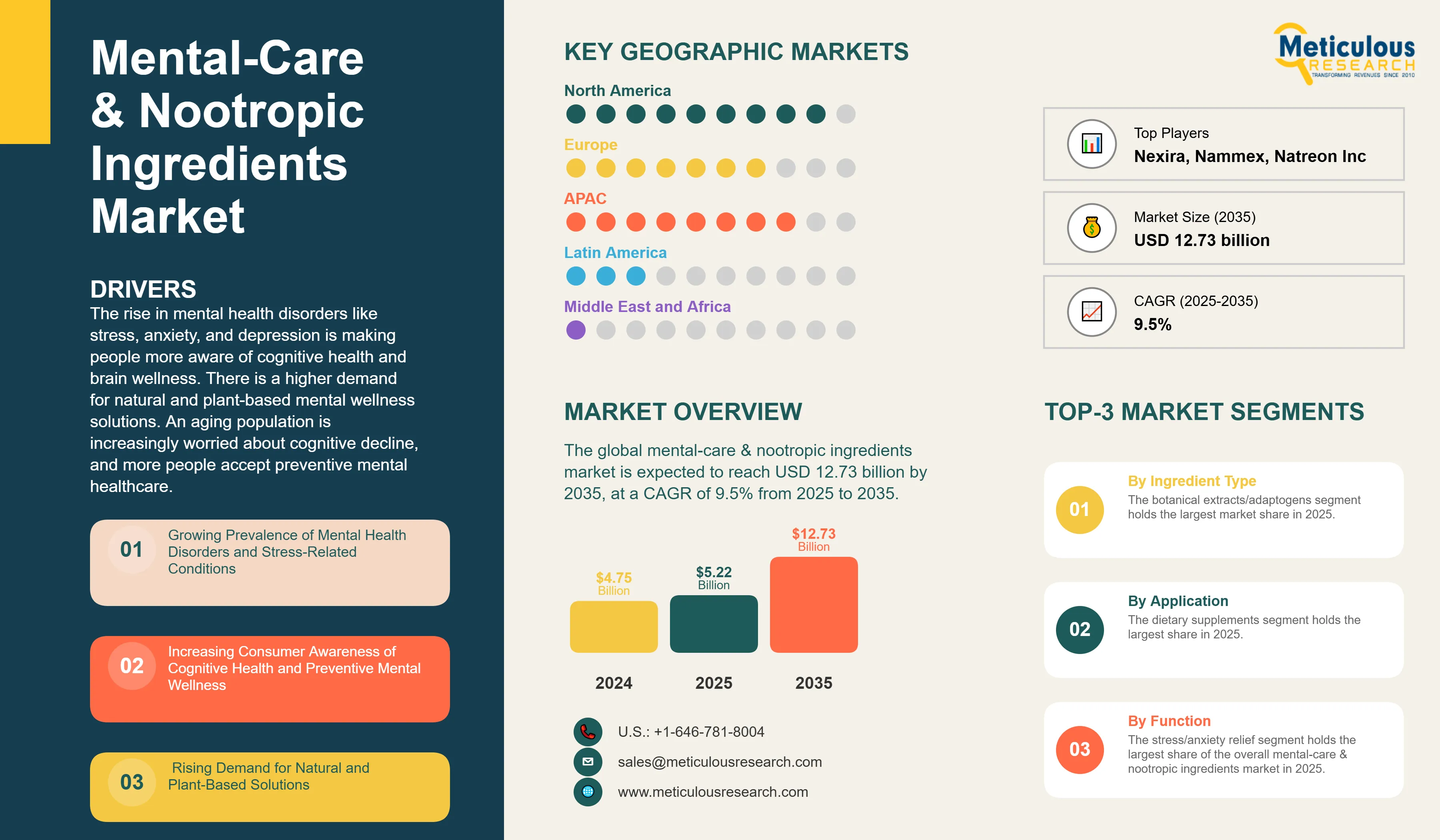

The global mental-care & nootropic ingredients market is projected to reach USD 12.72 billion by 2035 from an estimated USD 5.07 billion in 2025, at a CAGR of 9.6% during the forecast period from 2025 to 2035.

Mental-care and nootropic ingredients are specialized compounds that support cognitive function, emotional well-being, and mental performance through different neurobiological processes. These ingredients include plant extracts, adaptogens, amino acids, vitamins, minerals, omega-3 fatty acids, probiotics that target the gut-brain connection, and synthetic nootropics aimed at improving memory, focus, stress resilience, and overall brain health. The increasing awareness of mental wellness as a key part of overall health, along with the rise of stress-related disorders and concerns about cognitive health, has made these ingredients essential in dietary supplements, functional foods and beverages, and pharmaceutical products.

Key factors driving this market include the rise in mental health disorders and stress-related issues, growing consumer awareness of cognitive health and preventive mental wellness, increased demand for natural and plant-based options, expanding clinical validation and acceptance of mental wellness claims, and the rising use of nootropic ingredients in functional foods and drinks. According to the World Health Organization, over 1 billion people globally are living with mental health conditions, with anxiety and depression being the most common. The economic impact is significant; depression and anxiety cost the global economy an estimated USD 1 trillion each year in lost productivity.

The COVID-19 pandemic worsened mental health issues worldwide. Estimates show a 26% rise in depression and a 28% increase in anxiety disorders during this time, leading to ongoing demand for cognitive support products. From 2018 to 2022, the number of published papers referencing the gut-brain axis more than doubled. This shows growing scientific interest in psychobiotics and the microbiome's role in mental wellness. Research shows that 66% of global consumers actively look for cognitive health products. This marks a shift from treating problems reactively to managing cognitive wellness proactively.

With the growing research on the gut-brain axis and psychobiotic innovation, more people are adopting personalized nutrition for cognitive health. There is also a rise in functional beverages and increasing clinical support for mental wellness ingredients. As a result, the mental-care and nootropic ingredients market is expected to grow significantly. This growth is fueled by wellness trends, scientific progress, and a shift toward preventive mental health management in a world that is becoming more stressful.

Click here to: Get Free Sample Copy of this report

Growing Prevalence of Mental Health Disorders and Stress-Related Conditions

The rising global challenge of mental health disorders is a key factor driving the market for mental-care and nootropic ingredients. According to the World Health Organization's 2024 data, nearly 1 in every 7 people (about 1.1 billion) worldwide live with a mental disorder. Anxiety disorders affect 359 million people, while depressive disorders impact 280 million globally. Mental health issues are common in all countries and communities, affecting people of all ages and income levels.

The COVID-19 pandemic worsened mental health problems globally. It caused a 25% increase in cases of anxiety and depression, leading to more interest in natural remedies for mental wellness. The lasting effects of the pandemic continue to shape consumer behavior. More people are aware of the importance of mental health, which has increased the demand for cognitive support products. Suicide remains a tragic outcome of mental health issues, claiming an estimated 727,000 lives in 2021 and ranking as a leading cause of death among young people.

Modern lifestyle factors like workplace stress, academic pressure, digital overload, and multitasking are contributing to rising concerns about cognitive health. The occurrence of neurological disorders, such as dementia and Alzheimer's disease, is increasing as the global population ages. In Brazil alone, 1.8 million people currently have dementia, a number that is expected to reach 5.6 million by 2050. These demographic and lifestyle changes are creating strong and growing demand for mental-care ingredients in dietary supplements, functional foods, and pharmaceutical applications. This positions mental wellness solutions as essential parts of preventive healthcare strategies.

Increasing Consumer Awareness of Cognitive Health and Preventive Mental Wellness

There is a growing consumer awareness regarding cognitive health and preventive mental wellness. This change is fundamentally shifting demand in the mental-care and nootropic ingredients market. Research shows that 66% of global consumers actively look for cognitive health products. Many prioritize mental health and seek natural solutions. This represents a shift from reactive treatment to proactive cognitive wellness management.

The destigmatization of mental health discussions has helped normalize the use of supplements for cognitive support, aided by public health campaigns and celebrity advocacy. The WHO identifies mental disorders as a leading cause of global disability and highlights the close link between mental and physical health in its public health frameworks. More consumers understand that caring for mental health from an early age is key to long-term well-being. This awareness is especially strong among younger demographics. Gen Z and Millennials show significant interest in cognitive enhancement and mental performance improvement.

The spread of educational content through digital platforms, social media influencers, and health-focused media has increased consumers' knowledge about specific cognitive-enhancing ingredients. Consumers are becoming more familiar with adaptogens like ashwagandha and rhodiola, nootropic compounds such as bacopa and lion's mane mushroom, and traditional cognitive-support ingredients like ginkgo biloba and phosphatidylserine. This knowledge helps them make more informed purchasing decisions and increases demand for clinically validated, high-quality formulations.

The self-care movement and biohacking culture have boosted interest in cognitive enhancement, especially among professionals, students, and entrepreneurs seeking an edge in competitive environments. This growing awareness is contributing to continuous market growth, as cognitive wellness becomes a part of mainstream health practices.

Rising Demand for Natural and Plant-Based Solutions

Consumer preference for natural, plant-based, and clean-label products is a key driver in the mental-care and nootropic ingredients market. In 2024, over 62% of global consumers favored herbal or plant-based supplements. This trend is especially strong in cognitive health, where worries about synthetic compounds and pharmaceutical side effects affect buying choices. Natural products captured a significant market share in 2024, fueled by consumer demand for health and wellness options viewed as gentle and safe.

Traditional medicine systems like Ayurveda, Traditional Chinese Medicine, and indigenous healing practices have offered validated botanical ingredients that appeal to today's consumers looking for natural solutions. Ayurvedic nootropics such as Bacopa monnieri (Brahmi), Ashwagandha, and Shankhpushpi have scientific backing for their cognitive benefits while also maintaining cultural significance. India produces about 85% of the global ashwagandha supply, grown on more than 14,000 hectares, highlighting the strong demand for traditional cognitive-support plants.

The clean-label movement has reached cognitive health products, with consumers wanting clear ingredient sourcing, organic certifications, and minimal processing. European consumers, in particular, show a strong preference for vegan, gluten-free, and sustainably sourced nootropic ingredients, with around 49% prioritizing herbal origins in their cognitive supplement choices. Market research shows that consumers of functional products place a high priority on ingredient quality over taste, favoring natural ingredients like ginkgo biloba and essential vitamins instead of synthetic options. Adaptogenic ingredients such as ashwagandha, reishi mushrooms, and lion's mane are becoming common in cognitive health formulas, reflecting growing consumer interest in holistic wellness.

Expanding Clinical Validation and Regulatory Acceptance of Mental Wellness Claims

Growing investment in clinical research and expanding regulatory pathways for mental wellness claims create significant opportunities for the nootropic ingredients market. Major ingredient suppliers and pharmaceutical companies are increasing their funding in clinical trials to prove cognitive health benefits, allowing for differentiation among scientifically validated ingredients. Companies focused on research, clinical validation, and quality control can establish themselves as credible leaders in the nootropics category.

Regulatory changes in key markets are opening new avenues for approved mental wellness claims. Health Canada has allowed certain probiotic strains to make claims related to stress reduction and cognitive function, setting a precedent for psychobiotic claims. Japan's Foods for Specified Health Uses (FOSHU) labeling system permits cognitive health claims for approved functional ingredients, creating a regulatory route that aids product differentiation and premium positioning.

The emerging field of psychobiotics, which targets the gut-brain axis through probiotic supplementation, is showing strong clinical evidence supporting mental health applications. Leading probiotic strains like Lactobacillus rhamnosus and Bifidobacterium longum 1714 have proven effective in clinical trials for stress, anxiety, and cognitive function. Health Canada approved gut-brain axis claims for Lallemand's Cerebiome®, stating that it "helps moderate general feelings of anxiety" and "promotes healthy mood balance." This shows regulatory acceptance of psychobiotic mental wellness claims.

Academic and government research efforts are improving our understanding of cognitive health ingredients. The U.S. government's Healthy Brain Initiative provides a plan for addressing brain health and incorporating cognitive wellness into public health practices. The World Health Organization has adopted Global Action Plans on mental health and neurological disorders, requiring member states to develop national brain strategies by 2030-31. These initiatives create a positive environment for ingredient development and market growth.

By Ingredient Type: The Botanical Extracts/Adaptogens Segment Dominated the Mental-Care & Nootropic Ingredients Market in 2025

Based on ingredient type, the mental-care and nootropic ingredients market is divided into botanical extracts, amino acids, vitamins and minerals, omega-3s and lipids, probiotics and microbiome-based ingredients, synthetic nootropics, and others. In 2025, the botanical extracts segment held the largest share at 32.4% of the mental-care and nootropic ingredients market. This large market share comes from the rising consumer preference for natural and plant-based solutions for managing stress, enhancing cognitive function, and improving emotional well-being. More scientific support for traditional adaptogenic herbs like ashwagandha, rhodiola, ginseng, and lion's mane mushroom, along with the increasing popularity of Ayurvedic and traditional medicine globally, also helps this segment’s growth.

The clean-label trend and consumer preference for botanical ingredients over synthetic options continue to boost demand. For example, ashwagandha makes up a significant part of the adaptogenic ingredients market, with India producing about 85% of the global supply from over 14,000 hectares.

On the other hand, the probiotics and microbiome-based segment is expected to show the highest CAGR of 13.5% during the forecast period. This growth mainly comes from expanding research and clinical evidence supporting the connection between the gut and brain, rising consumer awareness of psychobiotics for mental wellness, and the emergence of new probiotic strains designed to influence neurotransmitter production and stress response.

By Function: The Stress/Anxiety Relief Segment Dominated the Mental-Care & Nootropic Ingredients Market in 2025

Based on function, the mental care and nootropic ingredients market is divided into several categories: stress and anxiety relief, mood enhancement and emotional well-being, cognitive performance, neuroprotection and brain health, sleep and recovery, and energy and mental fatigue. In 2025, the stress and anxiety relief segment made up the largest share at 26.1% of the market. This segment's size shows the widespread effects of chronic stress on today's population and the increasing preference for natural, non-drug options for managing stress.

The World Health Organization reports that the COVID-19 pandemic led to a 25% rise in anxiety and depression cases worldwide. This surge has greatly increased consumer interest in natural ways to improve mental wellness. Ingredients such as ashwagandha, rhodiola rosea, L-theanine, GABA, and magnesium are common in this segment. Clinical studies show these ingredients can help balance cortisol levels and support healthy stress responses.

Meanwhile, the sleep and recovery segment is experiencing the fastest growth, with a compound annual growth rate (CAGR) of 10.8%. Quality sleep is now recognized as a key part of mental health and cognitive performance. More people are becoming aware of the connection between poor sleep, anxiety, depression, burnout, and lower productivity. This awareness drives consumers to look for targeted solutions to support sleep.

By Application: The Dietary Supplements Segment Dominated the Mental-Care & Nootropic Ingredients Market in 2025

Based on application, the mental-care and nootropic ingredients market is divided into dietary supplements, functional foods and beverages, personal care or nutraceutical cosmetics, pharmaceuticals for clinical mental health use, sports nutrition, and others. In 2025, the dietary supplements segment held the largest share, accounting for 44.5% of the mental-care and nootropic ingredients market. This growth is due to a strong supplement industry, high consumer awareness of cognitive health benefits, and a rising preference for convenient, encapsulated delivery formats that provide precise dosing and standardized ingredient concentrations.

The global dietary supplements market reached USD 133.77 billion in 2024. It is expected to grow at a rate of 4.9% each year through 2032, with brain health supplements becoming one of the fastest-growing categories in this area. The rising number of cognitive health concerns worldwide, especially among older populations looking to maintain mental sharpness and prevent age-related cognitive decline, continues to drive this demand.

On the other hand, the functional foods and beverages segment is anticipated to see the highest growth rate at 11.7% during the forecast period. This increase is mainly due to more consumers seeking health benefits in their daily consumption, the rising need for convenient on-the-go options, and the continued innovation in adaptogenic and nootropic-infused beverage formulas.

By Distribution Channel: The Direct Sales to Manufacturers Segment Dominated the Mental-Care & Nootropic Ingredients Market in 2025

Based on distribution channel, the mental-care and nootropic ingredients market is divided into direct sales to manufacturers, distributors, ingredient brokers, online B2B platforms, and others. In 2025, the direct sales to manufacturers segment held the largest share at 41.1% of the mental-care and nootropic ingredients market. This is due to the removal of intermediary costs, the ability to provide customized ingredient solutions for specific manufacturer needs, and the established relationships between major ingredient suppliers and large nutraceutical and pharmaceutical manufacturers.

The direct sales model provides significant benefits in terms of customization and technical support. Ingredient suppliers work directly with manufacturers to deliver tailored solutions. These include custom particle sizes, specialized extraction methods, proprietary blends, and application-specific standardization levels.

However, the online B2B platforms segment is expected to have the highest compound annual growth rate (CAGR) of 13.7% during the forecast period. This growth is mainly fueled by the digital shift in ingredient sourcing processes. Additionally, online platforms offer convenience and accessibility for small and medium-sized manufacturers, along with increasing access to detailed product information, certifications, and documentation through digital channels.

North America Dominated the Mental-Care & Nootropic Ingredients Market in 2025

Based on geography, the mental-care and nootropic ingredients market is divided into North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa. In 2025, North America held the largest share of 33.5% of the global mental-care and nootropic ingredients market. North America's leading position comes from high consumer awareness about cognitive health, a strong wellness culture, the presence of major market players, supportive regulations that assist product development and market access, and high consumer spending power.

The U.S. leads the global nootropics market, thanks to its strong health and wellness industry. About 60% of the adult population takes dietary supplements. The well-developed retail infrastructure, which includes both physical stores with dedicated nootropic sections and advanced e-commerce platforms, ensures wide product availability for various demographic groups. Additionally, the region's vibrant biohacking culture and growing interest in cognitive improvement among students, professionals, and entrepreneurs have broadened the customer base beyond typical supplement users.

However, Asia-Pacific is projected to have the highest compound annual growth rate of 11.4% during the forecast period. This rapid growth is fueled by increasing urbanization, a rise in health awareness among the growing middle class, a higher prevalence of mental health issues, the blending of traditional herbal knowledge with modern nootropic products, and significant growth of e-commerce platforms that improve access to cognitive health products. Countries like China, India, Japan, and South Korea are emerging as key growth centers in the Asia-Pacific market.

Key Companies

Major companies in the global mental-care & nootropic ingredients market have implemented various strategies to expand their product offerings and augment their market shares. The key strategies followed by most companies include clinical validation and research investment, product launch and enhancement, collaboration, partnership and agreement, and others (acquisition, vertical integration, and sustainable sourcing initiatives).

Some of the prominent players operating in the global mental-care & nootropic ingredients market include Sabinsa Corporation (U.S.), Arjuna Natural Pvt. Ltd. (India), Ixoreal Biomed Inc. (India), Natreon Inc. (U.S.), Kyowa Hakko Bio Co. Ltd. (Japan), DSM-Firmenich (Switzerland), Chr. Hansen Holding A/S - Novonesis (Denmark), Glanbia Nutritionals (Ireland), Verdure Sciences (U.S.), Nexira (France), and Nammex (Canada).

|

Particulars |

Details |

|

Number of Pages |

369 |

|

Format |

|

|

Forecast Period |

2025–2035 |

|

Base Year |

2024 |

|

CAGR (Value) |

9.6% |

|

Market Size (Value) in 2025 |

USD 5.07 Billion |

|

Market Size (Value) in 2035 |

USD 12.72 Billion |

|

Segments Covered |

By Ingredient Type

By Function

By Application

By Distribution Channel

|

|

Countries Covered |

North America (U.S., Canada), Europe (Germany, France, U.K., Italy, Spain, and Rest of Europe), Asia-Pacific (China, India, Japan, South Korea, Australia, and Rest of Asia-Pacific), Latin America (Brazil, Mexico, Argentina, and Rest of Latin America), and the Middle East & Africa (Saudi Arabia, UAE, and Rest of Middle East & Africa) |

|

Key Companies |

Sabinsa Corporation (U.S.), Arjuna Natural Pvt. Ltd. (India), Ixoreal Biomed Inc. (India), Natreon Inc. (U.S.), Kyowa Hakko Bio Co. Ltd. (Japan), DSM-Firmenich (Switzerland), Chr. Hansen Holding A/S - Novonesis (Denmark), Glanbia Nutritionals (Ireland), Verdure Sciences (U.S.), Nexira (France), and Nammex (Canada) |

The global mental-care & nootropic ingredients market size is projected to reach USD 5.07 billion in 2025.

The market is projected to grow from USD 5.07 billion in 2025 to USD 12,724.9 million by 2035, at a CAGR of 9.6%.

The mental-care & nootropic ingredients market analysis indicates substantial growth, with projections indicating the market will reach USD 12.72 billion by 2035, at a compound annual growth rate (CAGR) of 9.6% from 2025 to 2035.

The key companies operating in this market include Sabinsa Corporation (U.S.), Arjuna Natural Pvt. Ltd. (India), Ixoreal Biomed Inc. (India), Natreon Inc. (U.S.), Kyowa Hakko Bio Co. Ltd. (Japan), DSM-Firmenich (Switzerland), Chr. Hansen Holding A/S - Novonesis (Denmark), Glanbia Nutritionals (Ireland), Verdure Sciences (U.S.), Nexira (France), and Nammex (Canada).

Gut-brain axis and psychobiotic innovation, functional beverage expansion and nootropic coffee alternatives, and personalized nutrition approaches for cognitive health are prominent trends in the mental-care & nootropic ingredients market.

By ingredient type, the botanical extracts/adaptogens segment is forecasted to hold the largest market share during 2025-2035; by function, the stress/anxiety relief segment is expected to dominate; by application, the dietary supplements segment is expected to hold the largest share; by distribution channel, the direct sales to manufacturers segment is expected to dominate; and by geography, North America is expected to hold the largest share of the market during 2025-2035.

By region, North America held the largest share of the mental-care & nootropic ingredients market in 2025. The large share is attributed to high consumer awareness regarding cognitive health, a well-established wellness culture, and strong consumer spending power. However, Asia-Pacific is expected to register the highest growth rate during the forecast period, driven by increasing urbanization and integration of traditional herbal knowledge with modern nootropic formulations.

Key drivers include the growing prevalence of mental health disorders and stress-related conditions, increasing consumer awareness of cognitive health and preventive mental wellness, rising demand for natural and plant-based solutions, expanding clinical validation and regulatory acceptance of mental wellness claims, and the growing integration of nootropic ingredients into functional beverages and foods. These factors are collectively driving the adoption of mental-care ingredients across applications.

Published Date: Feb-2025

Published Date: Jan-2025

Published Date: Jan-2025

Published Date: Oct-2024

Published Date: Aug-2024

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates