Resources

About Us

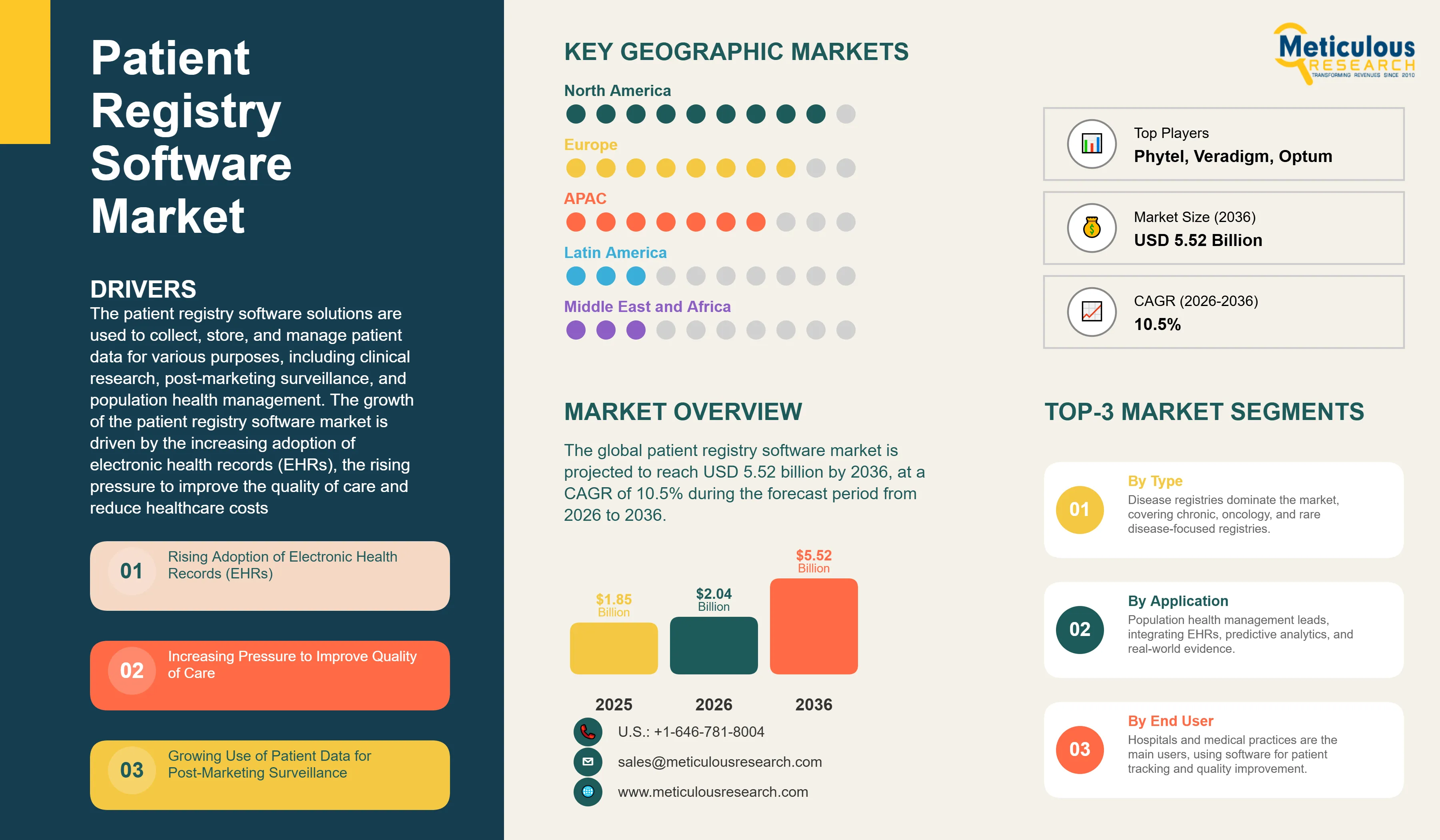

The global patient registry software market was valued at USD 1.85 billion in 2025 and is projected to reach USD 5.52 billion by 2036 from USD 2.04 billion in 2026, at a CAGR of 10.5% during the forecast period from 2026 to 2036. The patient registry software solutions are used to collect, store, and manage patient data for various purposes, including clinical research, post-marketing surveillance, and population health management. The growth of the patient registry software market is driven by the increasing adoption of electronic health records (EHRs), the rising pressure to improve the quality of care and reduce healthcare costs, and the growing use of patient registry data for post-marketing surveillance. Additionally, the growing emphasis on population health management initiatives and the expansion of cloud-based solutions are expected to support the growth of this market throughout the forecast period.

Click here to: Get Free Sample Pages of this Report

The global patient registry software market is mainly driven by technological advancements, regulatory requirements, and the growing emphasis on data-driven healthcare decision-making. Patient registry software is a fundamental component in modern healthcare, enabling applications ranging from clinical trial management to public health surveillance and post-marketing surveillance. The market includes key manufacturers such as Phytel, Inc. (an IBM Corporation Company), Quintiles IMS Holdings, Inc., and McKesson Corporation, alongside emerging specialized manufacturers focusing on specific disease areas and functionalities.

The transition from paper-based records to electronic health records (EHRs) has been one of the most significant market drivers. This shift has created substantial demand for patient registry software that can integrate with EHRs and other healthcare IT systems to provide a comprehensive view of the patient journey. Furthermore, the integration of advanced analytics and artificial intelligence (AI) is expanding the addressable market for patient registry software, enabling new applications in predictive modeling, risk stratification, and personalized medicine. The development of cloud-based patient registry solutions has revolutionized the accessibility and scalability of registry platforms, enabling healthcare organizations to manage patient data more efficiently.

Shift Towards Cloud-Based Solutions and Patient-Powered Research Networks (PPRNs)

The patient registry software market is witnessing a rapid shift towards cloud-based solutions, which offer greater flexibility, scalability, and accessibility compared to on-premise solutions. Cloud-based platforms enable healthcare organizations to reduce infrastructure costs while improving data accessibility across multiple locations. The emergence of patient-powered research networks (PPRNs) is also driving significant innovation in the market. PPRNs are patient-led initiatives that collect and share health data for research purposes, empowering patients to participate actively in clinical research. The development of user-friendly and patient-centric registry software is enabling the growth of PPRNs and supporting the shift towards patient-centered care models. Companies such as Veradigm LLC and Health Catalyst, Inc. are investing heavily in cloud-based solutions to maintain competitive advantage.

Integration of Real-World Evidence and Artificial Intelligence

The integration of real-world evidence (RWE) and artificial intelligence (AI) is driving significant innovation in the patient registry software market. RWE is data collected from real-world sources, such as EHRs, claims data, and patient-reported outcomes, providing insights into disease progression and treatment effectiveness in actual clinical practice. The use of AI and machine learning to analyze RWE is enabling new insights into disease progression, treatment effectiveness, and patient outcomes. Advanced analytics capabilities are enabling healthcare organizations to identify patient cohorts, predict treatment responses, and optimize clinical workflows. The development of AI-powered patient registry software is creating new opportunities for the development of personalized and predictive healthcare solutions. Manufacturers such as Inovalon Holdings, Inc. and Optum, Inc. are leveraging AI and advanced analytics to differentiate their offerings in the market.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 5.52 Billion |

|

Market Size in 2026 |

USD 2.04 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 10.5% |

|

Dominating Registry Type |

Disease Registries |

|

Fastest Growing Deployment Type |

Cloud-Based Solutions |

|

Largest Functionality Segment |

Population Health Management |

|

Dominant End-User Segment |

Hospitals and Medical Practices |

|

Leading Geographic Region |

North America |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Drivers: Rising Adoption of EHRs and Pressure to Improve Quality of Care

The primary drivers of the patient registry software market include the rising adoption of electronic health records (EHRs) and the increasing pressure to improve the quality of care while reducing healthcare costs. Government regulations promoting the adoption of EHRs, combined with declining software costs, are accelerating market penetration. The increasing demand for advanced data management and analytics capabilities in healthcare organizations is fueling growth in the registry software segment. The proliferation of chronic diseases and the growing need for disease-specific registries is creating sustained demand for specialized registry solutions. Additionally, the expansion of population health management programs is driving demand for registry software used in health monitoring and preventive care initiatives.

Opportunity: Emerging Applications and Technological Innovation

The patient registry software market offers substantial opportunities through emerging applications and continuous technological innovation. The development of advanced cloud-based registry platforms is creating new market segments with significant growth potential. The expansion of patient-powered research networks (PPRNs) is opening new revenue streams for registry software providers. The integration of AI and machine learning capabilities in registry software is driving demand for sophisticated analytics solutions. The growing adoption of personalized medicine approaches is creating opportunities for registry software that supports genomic data management and precision health applications. Manufacturers investing in research and development to address these emerging applications are well-positioned to capture market share.

Why Do Disease Registries Dominate the Market?

Disease registries represent the largest registry type segment in the patient registry software market, driven by the increasing prevalence of chronic diseases and the growing need for data to support clinical research and public health initiatives. The development of new and advanced disease registries for a wide range of conditions, including cardiovascular diseases, diabetes, cancer, and rare diseases, has accelerated market adoption. Disease registries enable healthcare organizations to track patient outcomes, monitor treatment effectiveness, and identify best practices for disease management. The integration of disease-specific registries with EHRs and clinical decision support systems is expanding the addressable market. Major manufacturers including Phytel, Inc., Quintiles IMS Holdings, Inc., and Veradigm LLC have established strong market positions through continuous innovation and product development focused on disease-specific solutions.

How Are Drug and Device Registries Driving Growth?

Drug and device registries represent the fastest-growing registry type segments within the patient registry software market. The proliferation of new pharmaceutical products and medical devices has created substantial demand for post-marketing surveillance registries. Regulatory requirements for post-market surveillance of drugs and devices are driving adoption of specialized registry software among pharmaceutical and medical device manufacturers. The expansion of real-world evidence initiatives for regulatory submissions is creating new opportunities for registry software providers. Manufacturers such as McKesson Corporation and Inovalon Holdings, Inc. are investing heavily in drug and device registry solutions to address emerging market demands and regulatory requirements.

How Do Hospitals and Medical Practices Lead the Market?

Hospitals and medical practices represent the largest end-user segment for patient registry software, driven by the increasing adoption of EHRs and the growing emphasis on quality improvement initiatives. Healthcare organizations are utilizing patient registry software to track patient outcomes, monitor treatment effectiveness, and support clinical decision-making. The integration of registry software with EHRs and other clinical systems is enabling healthcare providers to access comprehensive patient data and improve care coordination. The development of user-friendly registry platforms that integrate seamlessly with existing healthcare IT infrastructure is accelerating adoption among hospitals and medical practices. Major healthcare systems are investing in advanced registry solutions to support population health management and value-based care models.

How Are Pharmaceutical and Device Companies Expanding Their Use of Registries?

Pharmaceutical and medical device manufacturers are expanding their use of patient registry software for post-marketing surveillance, real-world evidence collection, and regulatory compliance. The increasing regulatory requirements for post-market surveillance are driving adoption of specialized registry solutions among pharmaceutical and device companies. The use of patient registries to collect real-world evidence for regulatory submissions and health economic studies is creating new opportunities for registry software providers. Companies such as Quintiles IMS Holdings, Inc. and Medidata Solutions are developing specialized registry solutions tailored to the needs of pharmaceutical and device manufacturers. The expansion of real-world evidence initiatives is expected to drive continued growth in this end-user segment.

How Does North America Maintain Its Leadership in the Global Patient Registry Software Market?

North America is expected to hold the largest share of the global patient registry software market in 2026, driven by the advanced healthcare infrastructure, high adoption of EHRs, and strong regulatory framework for data management. The U.S. has emerged as a major market for patient registry software, with numerous healthcare organizations implementing advanced registry solutions. Canada is also experiencing significant growth in patient registry adoption, driven by government initiatives to improve healthcare quality and efficiency. The region has established manufacturers such as Phytel, Inc. (IBM), Optum, Inc., and Health Catalyst, Inc. driving innovation in registry solutions. The key companies operating in the North America patient registry software market are Phytel, Inc., Optum, Inc., Health Catalyst, Inc., Inovalon Holdings, Inc., and Cerner Corporation.

Which Regions Are Experiencing Steady Growth?

Europe and Asia-Pacific are projected to experience steady growth in the patient registry software market, driven by the adoption of advanced healthcare technologies and increasing focus on population health management. Europe is characterized by a strong demand for data privacy-compliant registry solutions and advanced analytics capabilities. The expansion of healthcare IT initiatives across European countries is creating demand for patient registry software. Asia-Pacific is experiencing rapid growth driven by the expansion of healthcare infrastructure, increasing adoption of EHRs, and growing demand for population health management solutions. The region offers significant opportunities for registry software providers, with countries such as China, Japan, and India investing heavily in healthcare IT infrastructure. Latin America and the Middle East & Africa are emerging markets with growing demand for patient registry software, driven by healthcare infrastructure development and increasing adoption of digital health solutions.

The key players profiled in the global patient registry software market report include Phytel, Inc. (IBM Corporation), Quintiles IMS Holdings, Inc., McKesson Corporation, Medidata Solutions, Veradigm LLC, Inovalon Holdings, Inc., Health Catalyst, Inc., Optum, Inc., Allscripts Healthcare Solutions, and Cerner Corporation, among others.

The global patient registry software market is valued at USD 2.04 billion in 2026 and is expected to reach USD 5.52 billion by 2036.

The market is expected to grow at a CAGR of 10.5% from 2026 to 2036.

The key players include Phytel, Inc. (IBM Corporation), Quintiles IMS Holdings, Inc., McKesson Corporation, Medidata Solutions, Veradigm LLC, and Inovalon Holdings, Inc.

The main factors include the rising adoption of EHRs, increasing pressure to improve quality of care, growing use of patient data for post-marketing surveillance, expansion of population health management programs, and the shift towards cloud-based solutions.

North America is expected to maintain leadership, while Europe and Asia-Pacific are projected to experience steady growth during the forecast period.

1. Introduction

1.1 Market Definition

1.2 Market Ecosystem

1.3 Currency & Limitations

1.3.1 Currency

1.3.2 Limitations

1.4 Key Stakeholders

2. Research Methodology

2.1 Research Process

2.2 Data Collection & Validation

2.2.1 Secondary Research

2.2.2 Primary Research

2.3 Market Assessment

2.3.1 Market Size Estimation

2.3.2 Bottom-Up Approach

2.3.3 Top-Down Approach

2.3.4 Growth Forecast

2.4 Assumptions for the Study

2.5 Limitations for the Study

3. Executive Summary

4. Market Insights

4.1 Introduction

4.2 Market Dynamics

4.2.1 Drivers

4.2.1.1 Rising Adoption of Electronic Health Records (EHRs)

4.2.1.2 Increasing Pressure to Improve Quality of Care

4.2.1.3 Growing Use of Patient Data for Post-Marketing Surveillance

4.2.1.4 Expansion of Population Health Management Programs

4.2.2 Restraints

4.2.2.1 Data Privacy and Security Concerns

4.2.2.2 High Implementation Costs

4.2.3 Opportunities

4.2.3.1 Cloud-Based Solutions and Patient-Powered Research Networks

4.2.3.2 Integration of Real-World Evidence (RWE) and AI

4.2.3.3 Emerging Personalized Medicine Applications

4.2.3.4 Expansion of Rare Disease Registries

4.3 Value Chain Analysis

5. Global Patient Registry Software Market, by Registry Type

5.1 Introduction

5.2 Disease Registries

5.2.1 Chronic Disease Registries

5.2.2 Rare Disease Registries

5.2.3 Oncology Registries

5.3 Drug Registries

5.3.1 Post-Marketing Surveillance Registries

5.3.2 Pharmacovigilance Registries

5.4 Device Registries

5.4.1 Implant Registries

5.4.2 Diagnostic Device Registries

5.5 Other Registry Types

6. Global Patient Registry Software Market, by Software Type

6.1 Introduction

6.2 On-Premise Solutions

6.3 Cloud-Based Solutions

6.4 Hybrid Solutions

7. Global Patient Registry Software Market, by Pricing Model

7.1 Introduction

7.2 Subscription-Based Pricing

7.3 Perpetual License

7.4 Usage-Based Pricing

7.5 Hybrid Pricing Model

8. Global Patient Registry Software Market, by Database Type

8.1 Introduction

8.2 Public Registries

8.3 Commercial Registries

8.4 Academic & Institutional Registries

9. Global Patient Registry Software Market, by Functionality

9.1 Introduction

9.2 Population Health Management (PHM)

9.3 Health Information Exchange (HIE) Integration

9.4 Point-of-Care (POC) Clinical Decision Support

9.5 Research & Real-World Evidence Analytics

9.6 Reporting & Regulatory Compliance

10. Global Patient Registry Software Market, by End User

10.1 Introduction

10.2 Hospitals and Medical Practices

10.3 Pharmaceutical Companies

10.4 Medical Device Manufacturers

10.5 Research Institutions

10.6 Government Agencies

10.7 Other End Users

11. Global Patient Registry Software Market, by Geography

11.1 Introduction

11.2 North America

11.2.1 U.S.

11.2.2 Canada

11.3 Europe

11.3.1 Germany

11.3.2 U.K.

11.3.3 France

11.3.4 Italy

11.3.5 Spain

11.3.6 Russia

11.3.7 Rest of Europe

11.4 Asia-Pacific

11.4.1 China

11.4.2 Japan

11.4.3 India

11.4.4 South Korea

11.4.5 Australia

11.4.6 Rest of Asia-Pacific

11.5 Latin America

11.5.1 Brazil

11.5.2 Mexico

11.5.3 Argentina

11.5.4 Rest of Latin America

11.6 Middle East & Africa

11.6.1 Saudi Arabia

11.6.2 South Africa

11.6.3 Rest of Middle East & Africa

12. Competitive Landscape

12.1 Introduction

12.2 Key Growth Strategies

12.3 Competitive Benchmarking

12.4 Market Share Analysis

13. Company Profiles

13.1 Phytel, Inc. (IBM Corporation)

13.2 IQVIA Holdings Inc.

13.3 McKesson Corporation

13.4 Medidata Solutions

13.5 Veradigm LLC

13.6 Inovalon Holdings, Inc.

13.7 Health Catalyst, Inc.

13.8 Optum, Inc.

13.9 Allscripts Healthcare Solutions

13.10 Oracle Cerner

13.11 Others

14. Appendix

14.1 Questionnaire

14.2 Available Customization

Published Date: Jul-2026

Published Date: Jun-2026

Published Date: Jan-2025

Published Date: Mar-2024

Subscribe to get the latest industry updates