Resources

About Us

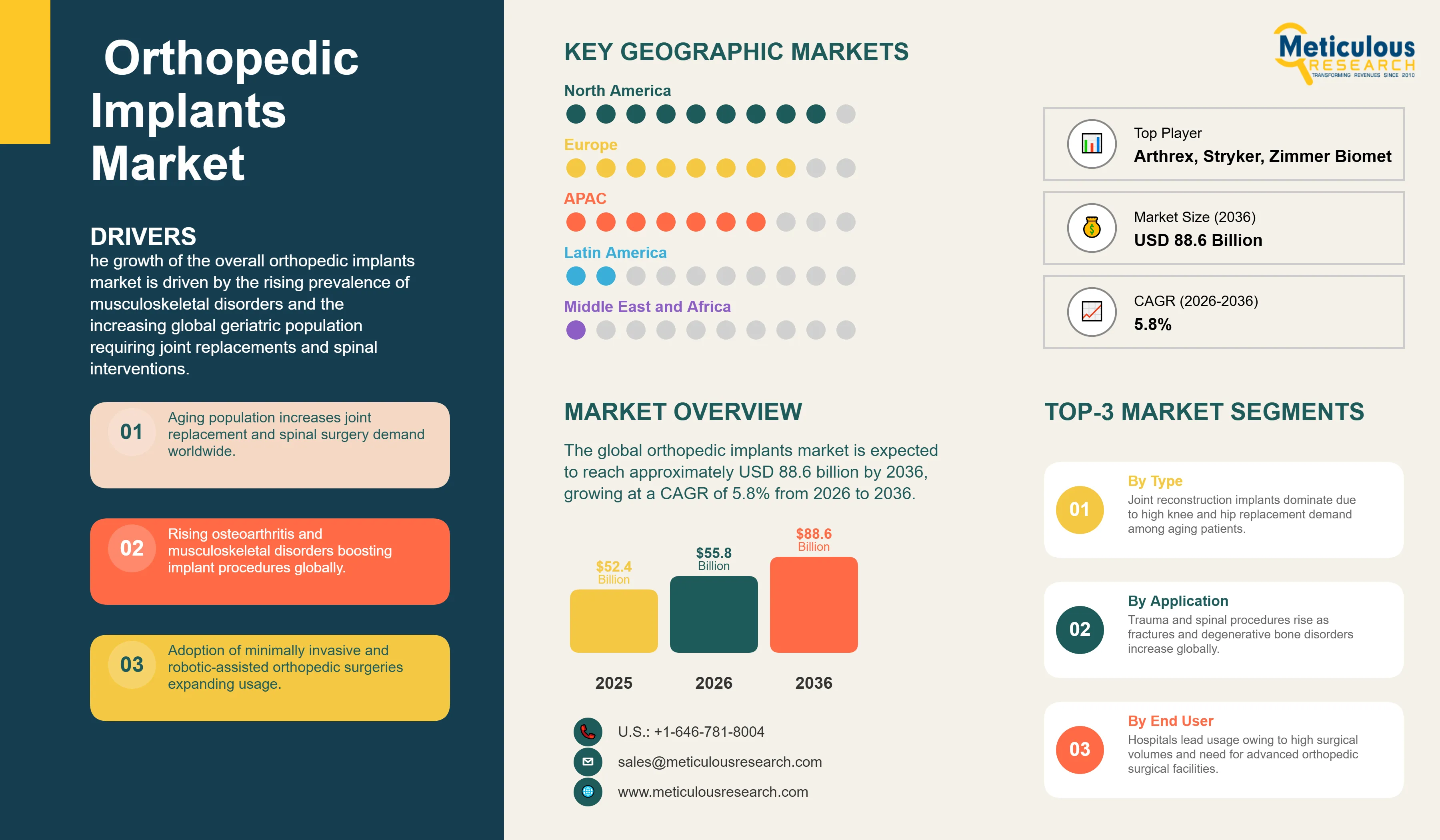

The global orthopedic implants market was valued at USD 52.4 billion in 2025. The market is expected to reach approximately USD 88.6 billion by 2036 from USD 55.8 billion in 2026, growing at a CAGR of 5.8% from 2026 to 2036. The growth of the overall orthopedic implants market is driven by the rising prevalence of musculoskeletal disorders and the increasing global geriatric population requiring joint replacements and spinal interventions. As manufacturers seek to integrate more biocompatible materials and address the demand for personalized surgical solutions, advanced orthopedic implant systems have become essential for restoring mobility and improving the quality of life for patients worldwide. The rapid expansion of minimally invasive surgical (MIS) techniques and the increasing adoption of robotic-assisted orthopedic procedures continue to fuel significant growth of this market across all major geographic regions.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Orthopedic implants are specialized medical devices used to replace or support damaged bone and joint structures, facilitating functional restoration and pain relief. These systems include joint prostheses, spinal fusion devices, trauma plates, and dental implants, which are designed to withstand significant mechanical stress and integrate seamlessly with biological tissues. The market is defined by high-performance materials such as titanium alloys, advanced ceramics, and PEEK polymers, which significantly enhance the longevity and stability of implants in diverse clinical applications. These systems are indispensable for surgeons seeking to optimize patient outcomes and meet the rising demand for active lifestyle preservation.

The market includes a diverse range of solutions, ranging from standard off-the-shelf implants for routine procedures to complex patient-specific designs for revision surgeries and oncology cases. These systems are increasingly integrated with advanced technologies such as 3D printing (additive manufacturing) and bioactive coatings to provide services such as improved osseointegration and reduced risk of implant failure. The ability to provide stable, high-precision results while minimizing surgical trauma has made advanced orthopedic implants the technology of choice for healthcare providers where clinical efficiency and patient safety are paramount.

The global healthcare sector is pushing hard to modernize surgical capabilities, aiming to reduce hospital stays and personalized recovery goals. This drive has increased the adoption of smart implants featuring integrated sensors, with advanced data analytics helping to monitor implant health and patient activity levels in real-time. At the same time, the rapid growth in the ambulatory surgical center (ASC) market is increasing the need for high-reliability, clinically-proven implant systems tailored for outpatient settings.

Proliferation of 3D-Printed and Patient-Specific Implants

Manufacturers across the orthopedic industry are rapidly shifting to personalized surgical solutions, moving well beyond traditional standardized sizing toward high-precision, patient-specific setups. Stryker’s latest Triathlon Tritanium platforms deliver significantly higher biological fixation for knee replacements, while DePuy Synthes’ recent custom-made craniomaxillofacial solutions have slashed surgical time and improved aesthetic outcomes. The real game-changer comes with 3D-printed porous structures that maintain peak mechanical performance while mimicking the architectural properties of natural bone. These advancements make high-precision orthopedics practical and cost-effective for everything from community hospitals to specialized trauma centers chasing clinical excellence and faster recovery.

Innovation in Robotic-Assisted and Smart Implant Systems

Innovation in robotic-assisted and smart implant systems is rapidly driving the orthopedic market, as surgical procedures become more precise and data-driven. Equipment suppliers are now designing units that combine the structural integrity of traditional implants with the versatility of digital planning software in a single workflow, saving valuable operating room time and simplifying surgical logistics. These systems often involve advanced navigation and real-time feedback technology capable of handling ultra-fine alignment metrics without compromising surgical speed or clinical reliability.

At the same time, growing focus on value-based care is pushing manufacturers to develop orthopedic solutions tailored to outpatient settings. These systems help reduce healthcare costs through optimized inventory management and the use of sterile-packed, single-use instrument kits. By combining high-density surgical precision with robust logistical performance, these new designs support both technological advancement and hospital sustainability, strengthening the resilience of the broader healthcare value chain.

|

Parameter |

Details |

|

Market Size by 2036 |

USD 88.6 Billion |

|

Market Size in 2026 |

USD 55.8 Million |

|

Market Size in 2025 |

USD 52.4 Million |

|

Market Growth Rate (2026-2036) |

CAGR of 5.8% |

|

Dominating Region |

North America |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Product Type, Material, Procedure, End-user, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Drivers: Aging Population and Rise of Chronic Bone Disorders

A key driver of the orthopedic implants market is the rapid movement of the global healthcare industry toward active-aging, highly functional recovery. Global patient demand for active lifestyles, effective joint preservation, and minimally invasive treatments has created significant incentives for the adoption of advanced orthopedic implants. The trend toward “outpatient” surgery and the integration of implants into daily mobility routines drive manufacturers toward scalable solutions that modern orthopedics can uniquely provide. It is estimated that as global life expectancy rises and diagnostic tools for osteoarthritis become more accessible through 2036, the need for robust, effective implants increases significantly; therefore, joint reconstruction and spinal systems, with their ability to ensure high-density mechanical support, are considered a crucial enabler of modern geriatric care strategies.

Opportunity: Expansion in Emerging Markets and Digital Integration

The rapid growth of the healthcare infrastructure in emerging economies and digital surgical technologies provides great opportunities for the orthopedic implants market. Indeed, the global surge in hospital construction has created a compelling demand for systems that can replace traditional conservative treatments and integrate seamlessly into digital hospital models. These applications require high reliability, material transparency, and the ability to handle high-volume surgical environments, all attributes that are met with advanced implant solutions. The orthopedic market in Asia-Pacific and Latin America is set to expand significantly through 2036, with patient-specific implants poised for an expanding share as manufacturers seek to maximize patient satisfaction and minimize surgical complications. Furthermore, the increasing demand for AI-driven surgical planning and virtual reality training tools for surgeons is stimulating demand for modular implant solutions that provide high-speed results and design flexibility.

Why Do Joint Reconstruction Implants Lead the Market?

The joint reconstruction segment accounts for a significant portion of the overall orthopedic implants market in 2026. This is mainly attributed to the versatile use of this technology in supporting daily mobility and pain relief within extremely diverse patient populations, such as the elderly and sports professionals. These systems offer the most comprehensive way to ensure skeletal integrity across diverse high-frequency movements. The knee and hip replacement sectors alone consume a large share of orthopedic implant production, with major projects in North America and Europe demonstrating the technology’s capability to handle high-density mechanical requirements. However, the orthobiologics and smart implant segments are expected to grow at a rapid CAGR during the forecast period, driven by the growing need for biological healing, clinical procedures, and regenerative medicine systems.

How Does the Hospital Segment Dominate?

Based on end-user, the hospitals segment holds the largest share of the overall market in 2026. This is primarily due to the massive volume of orthopedic surgeries performed in inpatient settings and the rigorous safety standards required for complex surgical interventions. Current large-scale healthcare facilities are increasingly specifying high-density implant integrations to ensure compliance with global clinical standards and patient expectations for faster, visible recovery results.

The ambulatory surgical centers (ASCs) segment is expected to witness the fastest growth during the forecast period. The shift toward outpatient orthopedics and the complexity of minimally invasive surgical suites are pushing the requirement for advanced implant systems that can handle varied procedural types and mechanical stresses while ensuring absolute reliability for cost-effective healthcare systems.

Why Does the Metallic Segment Lead the Market?

The metallic segment commands the largest share of the global orthopedic implants market in 2026. This dominance stems from its superior mechanical stability, structural consistency in records, and excellent biocompatibility for load-bearing joints, making it the material of choice for high-performance orthopedic products. Large-scale operations in joint replacement, trauma fixation, and spinal fusion drive demand, with advanced alloys from suppliers like Zimmer Biomet and Stryker enabling reliable performance in extreme physiological environments.

However, the ceramic and polymeric segments are poised for steady growth through 2036, fueled by expanding applications in wear-resistant surfaces and radiolucent spinal formulations. Manufacturers face mounting pressure to optimize outcomes for younger, more active patients, where advanced ceramics provide a low-friction alternative for long-term implant survival.

How is North America Maintaining Dominance in the Global Orthopedic Implants Market?

North America holds the largest share of the global orthopedic implants market in 2026. The largest share of this region is primarily attributed to the massive healthcare expenditure and the presence of the world’s most advanced orthopedic manufacturing hubs, particularly in the United States. The U.S. alone accounts for a significant portion of global orthopedic implant production, with its position as a leading innovator of surgical technology driving sustained growth. The presence of leading manufacturers like Zimmer Biomet and Stryker and a well-developed clinical research network provides a robust market for both standard and high-density orthopedic solutions.

Which Factors Support Europe and Asia-Pacific Market Growth?

Europe and Asia-Pacific together account for a substantial share of the global orthopedic implants market. The growth of these markets is mainly driven by the need for technological modernization in the geriatric care, sports medicine, and trauma sectors. The demand for advanced implant systems in Europe is mainly due to its stringent regulatory standards and the presence of innovators like Smith & Nephew and Medtronic.

In Asia-Pacific, the leadership in medical tourism and the push for surgical safety innovation are driving the adoption of high-reliability orthopedic implants. Countries like China, India, and Japan are at the forefront, with significant focus on integrating robotic-assisted solutions into daily surgical routines and advanced implant treatments to ensure the highest levels of performance and reliability.

How are Latin America and Middle East & Africa Expanding?

Latin America is witnessing significant expansion in the orthopedic implants market, driven by the region’s emergence as a critical hub for private healthcare services and medical device manufacturing. Countries like Brazil, Mexico, and Colombia are increasingly adopting digital surgical planning to meet international clinical standards and ensure the “quality” credentials of their healthcare providers. The presence of global orthopedic giants and a growing focus on the medical device value chain provide a fertile ground for advanced implant solutions.

In the Middle East & Africa, the market is fueled by the rapid development of specialized orthopedic hospitals and the establishment of new medical cities, particularly in Saudi Arabia and the UAE. These nations are integrating advanced orthopedic passports into their smart healthcare and sustainable wellness initiatives to ensure long-term patient performance. Additionally, the focus on trauma care in regions like South Africa and Egypt is driving the adoption of high-reliability implant systems to ensure effective healing and compliance with global healthcare regulations.

The companies such as Zimmer Biomet, Stryker Corporation, Johnson & Johnson (DePuy Synthes), and Smith & Nephew plc lead the global orthopedic implants market with a comprehensive range of joint reconstruction and trauma solutions, particularly for large-scale hospital and high-speed surgical applications. Meanwhile, players including Medtronic plc, Globus Medical, and Enovis focus on specialized spinal-grade and high-density formulations targeting the professional and regulatory sectors. Emerging manufacturers and integrated players such as Arthrex, Inc., NuVasive, and Integra LifeSciences are strengthening the market through innovations in minimally invasive technology and modular implant platforms.

The global orthopedic implants market is expected to grow from USD 55.8 billion in 2026 to USD 88.6 billion by 2036.

The global orthopedic implants market is projected to grow at a CAGR of 5.8% from 2026 to 2036.

Joint reconstruction implants are expected to dominate the market in 2026 due to their superior ability to support mobility and joint replacement. However, orthobiologics and smart implants are projected to be the fastest-growing segments owing to their increasing adoption in next-generation healing systems where biological data delivery is required.

Robotics and 3D printing are transforming the orthopedic implants landscape by demanding higher surgical precision, lower procedural friction, and improved patient-specific repair. These technologies drive the adoption of advanced materials like porous titanium and additive-manufactured structures, enabling orthopedic manufacturers to support the complex formulations and high-frequency requirements of next-generation surgical products.

North America holds the largest share of the global orthopedic implants market in 2026. The largest share of this region is primarily attributed to the massive healthcare expenditure and the presence of the world’s most advanced orthopedic manufacturing hubs in the United States. Europe and Asia-Pacific together account for a substantial share, driven by high-end applications in joint replacement and trauma care.

The leading companies include Zimmer Biomet, Stryker Corporation, Johnson & Johnson (DePuy Synthes), Smith & Nephew plc, and Medtronic plc.

1. Introduction

1.1. Market Definition

1.2. Market Scope

1.3. Research Methodology

1.4. Assumptions & Limitations

2. Executive Summary

3. Market Overview

3.1. Introduction

3.2. Market Dynamics

3.2.1. Drivers

3.2.2. Restraints

3.2.3. Opportunities

3.2.4. Challenges

3.3. Impact of Robotics and 3D Printing on Orthopedic Implants

3.4. Porter's Five Forces Analysis

3.5. Value Chain Analysis

4. Global Orthopedic Implants Market, by Product Type

4.1. Introduction

4.2. Joint Reconstruction Implants

4.2.1. Knee Implants

4.2.2. Hip Implants

4.2.3. Shoulder & Elbow Implants

4.3. Spinal Implants

4.3.1. Fusion Implants

4.3.2. Non-fusion Implants

4.4. Trauma Implants

4.5. Dental Implants

4.6. Craniomaxillofacial Implants

4.7. Orthobiologics

4.8. Others

5. Global Orthopedic Implants Market, by Material

5.1. Introduction

5.2. Metallic Implants

5.3. Ceramic Implants

5.4. Polymeric Implants

6. Global Orthopedic Implants Market, by Procedure

6.1. Introduction

6.2. Open Surgery

6.3. Minimally Invasive Surgery (MIS)

7. Global Orthopedic Implants Market, by End-user

7.1. Introduction

7.2. Hospitals

7.3. Orthopedic Clinics

7.4. Ambulatory Surgical Centers (ASCs)

8. Global Orthopedic Implants Market, by Region

8.1. Introduction

8.2. North America

8.2.1. U.S.

8.2.2. Canada

8.3. Europe

8.3.1. Germany

8.3.2. France

8.3.3. U.K.

8.3.4. Italy

8.3.5. Spain

8.3.6. Netherlands

8.3.7. Rest of Europe

8.4. Asia-Pacific

8.4.1. China

8.4.2. Japan

8.4.3. South Korea

8.4.4. India

8.4.5. Australia

8.4.6. Rest of Asia-Pacific

8.5. Latin America

8.5.1. Brazil

8.5.2. Mexico

8.5.3. Argentina

8.5.4. Chile

8.5.5. Colombia

8.5.6. Rest of Latin America

8.6. Middle East & Africa

8.6.1. Saudi Arabia

8.6.2. UAE

8.6.3. Qatar

8.6.4. South Africa

8.6.5. Egypt

8.6.6. Nigeria

8.6.7. Rest of Middle East & Africa

9. Competitive Landscape

9.1. Overview

9.2. Key Growth Strategies

9.3. Competitive Benchmarking

9.4. Competitive Dashboard

9.4.1. Industry Leaders

9.4.2. Market Differentiators

9.4.3. Vanguards

9.4.4. Emerging Companies

9.5. Market Ranking/Positioning Analysis of Key Players, 2025

10. Company Profiles (Manufacturers & Providers)

10.1. Zimmer Biomet

10.2. Stryker Corporation

10.3. Johnson & Johnson (DePuy Synthes)

10.4. Smith & Nephew plc

10.5. Medtronic plc

10.6. Globus Medical, Inc.

10.7. Enovis (DJO Global)

10.8. Arthrex, Inc.

10.9. NuVasive, Inc.

10.10. Integra LifeSciences

10.11. Colfax Corporation

10.12. Wright Medical Group N.V.

11. Appendix

11.1. Questionnaire

11.2. Related Reports

Published Date: Mar-2026

Published Date: Sep-2024

Published Date: May-2024

Published Date: Apr-2023

Subscribe to get the latest industry updates