Resources

About Us

Orthopedic Robotics Market by Product Type (Robotic Systems, Instruments & Accessories, Software & Services), Application (Joint Replacement Surgery, Spine Surgery, Trauma Surgery, Sports Medicine), End-User (Hospitals, Ambulatory Surgical Centers, Specialty Orthopedic Clinics), Technology (Active Robotic Systems, Semi-active Robotic Systems, Passive Robotic Systems) -- Global Forecast to 2036

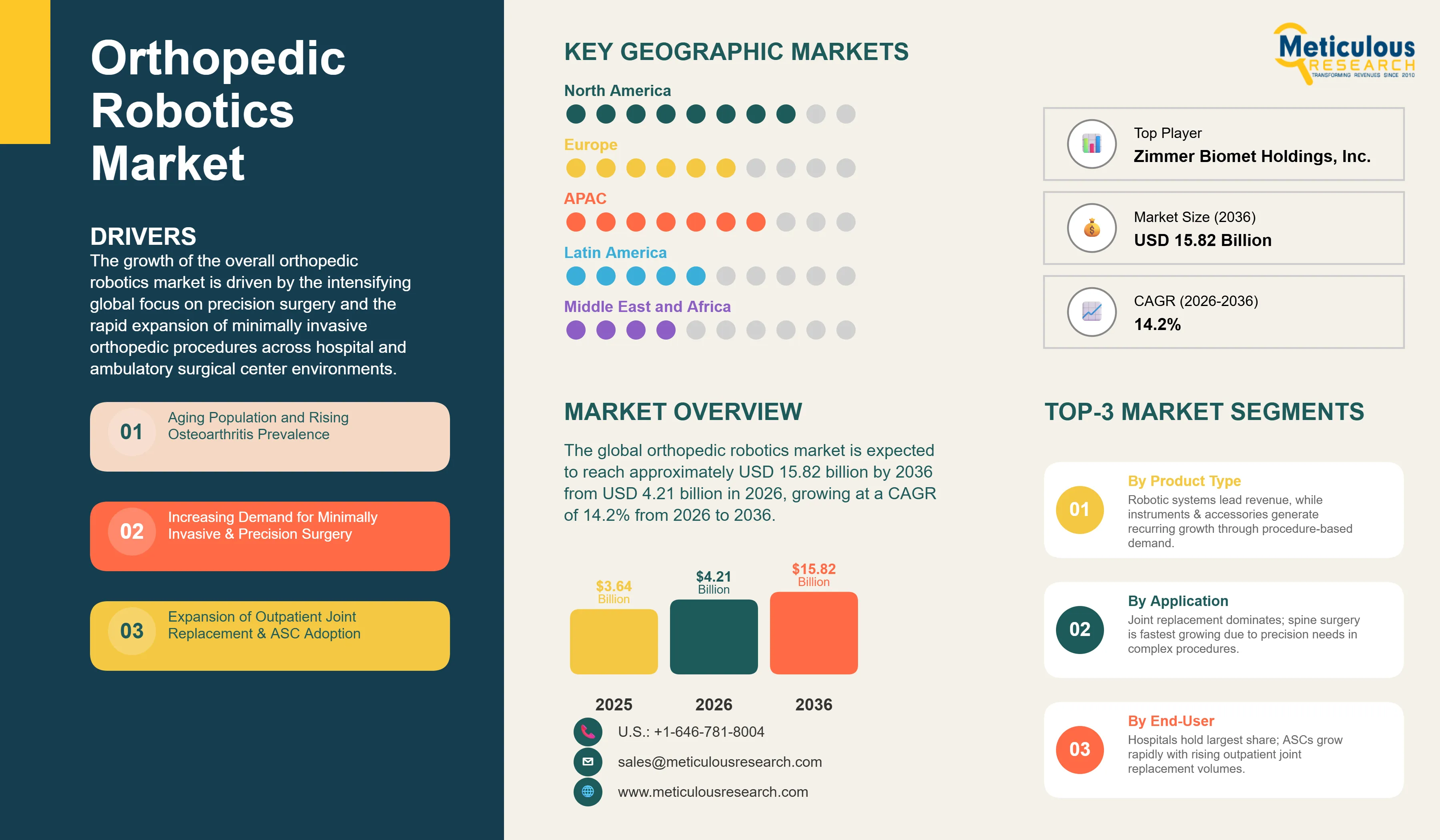

Report ID: MRHC - 1041818 Pages: 293 Mar-2026 Formats*: PDF Category: Healthcare Delivery: 24 to 72 Hours Download Free Sample ReportThe global orthopedic robotics market was valued at USD 3.64 billion in 2025. The market is expected to reach approximately USD 15.82 billion by 2036 from USD 4.21 billion in 2026, growing at a CAGR of 14.2% from 2026 to 2036. The growth of the overall orthopedic robotics market is driven by the intensifying global focus on precision surgery and the rapid expansion of minimally invasive orthopedic procedures across hospital and ambulatory surgical center environments. As healthcare institutions seek to integrate more accuracy into their surgical workflows and address the increasing demand for improved patient outcomes with reduced complications and recovery times, advanced robotic surgical platforms have become essential for maintaining competitive positioning and clinical excellence. The rapid expansion of aging populations requiring joint replacement procedures and the increasing need for complex spine surgeries with sub-millimeter precision continue to fuel significant growth of this market across all major geographic regions.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Orthopedic robotics systems represent critical surgical platforms designed to provide enhanced precision, consistency, and safety in bone and joint procedures through computer-assisted navigation and robotic arm manipulation. These systems integrate advanced imaging technologies including CT and fluoroscopy for preoperative planning, real-time intraoperative tracking enabling sub-millimeter accuracy in implant positioning, haptic feedback mechanisms preventing inadvertent soft tissue damage, and comprehensive data analytics supporting continuous surgical technique optimization. The market is defined by sophisticated technologies such as artificial intelligence-powered surgical planning, augmented reality visualization overlays, and force-sensing instruments, which significantly enhance surgical outcomes and operational efficiency in complex orthopedic interventions. These platforms are indispensable for orthopedic surgeons seeking to optimize implant longevity, reduce revision surgery rates, and achieve reproducible outcomes across varying patient anatomies and pathologies.

The market encompasses diverse robotic platforms ranging from semi-active systems providing surgical guidance while allowing surgeon control of cutting instruments, to fully active systems autonomously executing bone preparation steps under surgeon supervision, and passive systems offering mechanical stabilization for manual instrument manipulation. Contemporary platforms increasingly feature modular architectures enabling single system deployment across multiple procedure types—total knee arthroplasty, total hip arthroplasty, unicompartmental knee replacement, and revision procedures—maximizing capital equipment utilization and return on investment for hospital systems. The evolution toward open platform ecosystems accepting multiple implant manufacturer components represents significant market shift, breaking traditional proprietary system lock-in models and enabling surgeons to select preferred implant designs while leveraging robotic precision benefits.

The global orthopedic surgery landscape faces mounting pressure to improve outcomes while controlling costs, as bundled payment models and value-based care frameworks shift financial risk to providers for complications and readmissions. Robotic systems address these imperatives through demonstrable improvements in implant alignment accuracy, reduced surgical trauma from smaller incisions and tissue-sparing approaches, shorter hospital stays through accelerated recovery protocols, and lower revision rates extending implant longevity—collectively supporting economic value propositions despite substantial upfront capital investment. Simultaneously, surgeon training standardization through robotic platforms creates reproducibility advantages, as digital surgery enables objective skill assessment, structured learning curricula, and remote mentoring capabilities addressing geographic access barriers to surgical expertise particularly relevant in developing markets.

Proliferation of Ambulatory Surgical Center Adoption and Outpatient Joint Replacement

Healthcare delivery transformation toward outpatient orthopedic surgery creates substantial opportunities for compact, efficient robotic systems tailored to ambulatory surgical center operational models. Total knee and hip arthroplasty procedures historically requiring multi-day inpatient stays increasingly transition to same-day discharge protocols, driven by enhanced recovery after surgery (ERAS) pathways, improved pain management techniques, and patient selection criteria identifying appropriate candidates for outpatient procedures. This shift favors robotic platforms offering streamlined workflows—rapid system setup/breakdown minimizing operating room turnover time, intuitive user interfaces reducing learning curves for ASC staff less experienced with robotic technology, and competitive pricing structures aligned with ASC reimbursement economics where per-procedure costs matter more than capital amortization across high volumes characteristic of hospital systems.

Innovation in AI-Powered Surgical Planning and Predictive Analytics

Artificial intelligence integration represents transformative advancement in orthopedic robotics, extending beyond intraoperative navigation toward comprehensive surgical decision support. Machine learning algorithms analyze vast datasets from previous procedures, identifying optimal implant positioning parameters for specific patient anatomies, predicting soft tissue balancing requirements based on preoperative imaging and demographic factors, and recommending procedural modifications reducing complication risks. These AI capabilities enable personalized surgical planning superseding standardized approaches, accounting for patient-specific factors including bone quality, ligament laxity, anatomical variations, and functional requirements—optimizing outcomes for individual patients rather than population averages.

The value extends to practice-level analytics, where aggregated surgical data supports quality improvement initiatives, identifies training opportunities through objective performance metrics, and provides evidence for value-based contracting negotiations with payers. Remote monitoring capabilities enable manufacturer support teams to proactively address system performance issues, optimize software algorithms based on real-world usage patterns, and deliver over-the-air updates enhancing functionality without service visits—creating competitive advantages for manufacturers establishing comprehensive data ecosystems. The regulatory landscape increasingly accommodates AI-driven medical devices through FDA's predetermined change control plans enabling continuous software improvement while maintaining safety oversight, accelerating innovation cycles previously constrained by traditional device approval pathways requiring discrete submissions for functionality changes.

|

Parameter |

Details |

|

Market Size by 2036 |

USD 15.82 Billion |

|

Market Size in 2026 |

USD 4.21 Billion |

|

Market Size in 2025 |

USD 3.64 Billion |

|

Market Growth Rate (2026-2036) |

CAGR of 14.2% |

|

Dominating Region |

North America |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Product Type, Application, End-User, Technology, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Drivers: Aging Population and Rising Osteoarthritis Prevalence

A key driver of the orthopedic robotics market is the demographic shift toward aging populations globally, with individuals over 65 years—the primary demographic for joint replacement surgery—projected to reach 1.5 billion by 2050 according to UN population projections. Osteoarthritis prevalence increases dramatically with age, affecting approximately 30% of individuals over 65 and creating sustained demand for total knee and hip arthroplasty procedures as conservative treatments prove inadequate for severe joint degeneration. This demographic imperative combines with rising obesity rates exacerbating joint wear, increasing life expectancy creating younger patient populations seeking durable implants lasting decades, and growing patient awareness and acceptance of surgical interventions as quality of life becomes prioritized over pain tolerance. The procedural volume growth—total knee replacements in United States alone projected to exceed 3.5 million annually by 2030 compared to 700,000 in 2010—creates hospital system imperative to improve surgical efficiency and outcomes, positioning robotic systems as strategic investments enabling higher throughput while maintaining quality standards increasingly scrutinized under value-based reimbursement models penalizing complications and readmissions.

Opportunity: Value-Based Healthcare and Outcomes-Focused Reimbursement

The healthcare payment model transformation from fee-for-service toward bundled payments and value-based arrangements creates compelling economic rationale for robotic surgery adoption despite substantial capital requirements. Medicare's Comprehensive Care for Joint Replacement (CJR) model holds hospitals financially accountable for 90-day episode costs including complications, readmissions, and revision procedures—creating strong incentive to optimize initial surgery quality preventing downstream expenses. Robotic systems demonstrably improve implant positioning accuracy, with studies showing reduced outlier rates from 20-30% in manual procedures to <5% with robotic assistance, directly correlating with improved functional outcomes and lower revision rates. These clinical benefits translate to financial performance under bundled payment models, as avoided complications generate savings far exceeding per-procedure robotic system costs when analyzed across patient populations. Additionally, commercial payers increasingly implement similar bundled payment arrangements and outcomes-based contracting, expanding value proposition beyond Medicare to broader payer mix, while international markets including Germany, UK, and Japan implement payment reforms creating analogous incentive structures favoring quality over volume and positioning robotic surgery as strategic differentiator for healthcare systems competing on outcomes metrics.

Why Do Robotic Systems Lead the Market?

The robotic systems segment accounts for approximately 65-70% of total market revenue in 2026, representing the core capital equipment investment hospitals make when establishing robotic orthopedic surgery capabilities. These systems—ranging from $500,000 to $1+ million per unit depending on configuration and capabilities—constitute significant capital expenditure requiring multi-year financial planning and executive approval. Leading platforms including Stryker's Mako, Zimmer Biomet's ROSA, Smith+Nephew's CORI, and Johnson & Johnson's VELYS demonstrate diverse technological approaches, from imageless systems using intraoperative data acquisition to image-based platforms requiring preoperative CT scans. The capital equipment nature creates high switching costs once deployed, as surgeon training investment, staff familiarity, and implant inventory alignment with specific platforms discourage system changes, generating installed base advantages for early market entrants. However, instruments & accessories segment demonstrates highest growth rate at 16-18% CAGR, driven by recurring revenue nature of disposable cutting guides, single-use instruments, and procedure-specific instrument packs generating ongoing revenue streams throughout system lifetime, creating attractive business models for manufacturers as recurring revenue provides predictable cash flows compared to episodic capital equipment sales.

How Does Joint Replacement Surgery Dominate?

Based on application, the joint replacement surgery segment holds approximately 70-75% of the overall market in 2026, dominated by total knee and hip arthroplasty procedures where robotic assistance delivers most demonstrable clinical and economic value. Knee replacement particularly benefits from robotic precision, as millimeter-level variations in implant alignment and rotation significantly impact functional outcomes, implant longevity, and patient satisfaction—factors directly addressed by robotic systems' sub-millimeter accuracy and reproducibility across varying patient anatomies. Hip replacement similarly leverages robotic advantages in achieving optimal cup positioning, leg length restoration, and offset reconstruction, though arguably requires less precision than knee procedures given ball-and-socket joint tolerance for minor positioning variations. The spine surgery segment demonstrates highest growth rate at 18-20% CAGR, driven by expanding indications as manufacturers develop specialized platforms for minimally invasive spine procedures, pedicle screw placement, deformity correction, and complex revision surgeries where navigation and robotics provide substantial safety and accuracy advantages over traditional fluoroscopy-based techniques.

Why Do Hospitals Command Market Leadership?

The hospitals segment commands approximately 75-80% of orthopedic robotics market in 2026, reflecting capital-intensive nature of robotic systems aligning with hospital financial resources and procedural volumes justifying investment. Large hospital systems and academic medical centers lead adoption, leveraging economies of scale across multiple operating rooms, high surgical volumes amortizing capital costs, and institutional brand differentiation through technology leadership attracting surgeons and patients. Teaching hospitals particularly value robotic platforms for standardized surgical training, objective skill assessment, and research opportunities generating publications and grants enhancing institutional reputation. However, ambulatory surgical centers represent fastest-growing segment at 17-19% CAGR, driven by outpatient joint replacement growth, development of compact robotic systems designed for ASC workflows, and ASC operators seeking competitive differentiation in increasingly crowded market where technology capabilities influence surgeon practice patterns and patient referrals, creating willingness to invest in robotics despite smaller procedural volumes and tighter operating margins compared to hospital settings.

How Do Active and Semi-active Systems Compete?

Semi-active robotic systems dominate the market with approximately 55-60% share in 2026, representing platforms where the robot provides surgical guidance and haptic boundaries while the surgeon manually operates cutting instruments—balancing automation benefits with surgeon control preferences. This approach addresses surgeon concerns about fully autonomous systems, maintains tactile feedback valued by experienced surgeons, and typically requires less extensive training compared to active systems. Leading semi-active platforms including Stryker's Mako use this approach for knee and hip procedures. Active robotic systems, where the robot autonomously executes bone cuts and preparation steps under surgeon supervision, hold approximately 30-35% market share, concentrated in spine applications where precision screw placement and trajectory control particularly benefit from automation. Passive robotic systems, providing mechanical guides without powered assistance, represent declining legacy technology as active and semi-active systems demonstrate superior accuracy and workflow efficiency justifying additional cost and complexity.

How is North America Maintaining Market Leadership?

North America holds approximately 45-50% of global orthopedic robotics market in 2026, anchored by United States' large joint replacement procedure volumes (1+ million annually), favorable reimbursement environment supporting technology adoption, and presence of major robotic system manufacturers. Medicare coverage for robotic joint replacement without additional patient cost-sharing removes financial barrier to adoption, while private insurers generally provide comparable coverage recognizing clinical evidence supporting robotic-assisted procedures. The region benefits from mature ambulatory surgical center market embracing outpatient joint replacement, high surgeon awareness and training availability through manufacturer-sponsored programs and professional society education, and competitive healthcare market where hospitals invest in technology differentiation attracting high-value orthopedic service lines. Canada contributes modestly to regional market given government healthcare system constraints on capital expenditure, though select centers of excellence deploy robotic systems particularly in major urban markets serving both Canadian patients and medical tourism from United States seeking lower-cost procedures.

Which Factors Drive Asia-Pacific's Rapid Growth?

Asia-Pacific demonstrates highest growth rate at 16-18% CAGR, propelled by multiple factors: rapidly aging populations in Japan, South Korea, and China creating dramatic increases in joint replacement demand; rising middle-class prosperity enabling healthcare expenditure on premium services including robotic surgery; medical tourism growth particularly in Thailand, Singapore, and India where international patients seek high-quality orthopedic procedures at costs substantially below Western markets; and government healthcare modernization initiatives supporting technology adoption as countries develop advanced medical capabilities. Japan leads regional adoption with established orthopedic robotics utilization comparable to Western markets, leveraging domestic robotic technology expertise and national health insurance coverage supporting advanced procedures. China represents enormous potential given population scale and government emphasis on healthcare infrastructure development, though adoption currently concentrated in top-tier urban hospitals given capital costs and training requirements. India's medical tourism segment drives robotic adoption in select private hospitals serving international patients, while domestic market remains price-sensitive favoring conventional surgical approaches for majority of procedures.

The companies such as Stryker Corporation (Mako Surgical), Zimmer Biomet Holdings, Inc. (ROSA Knee System), Smith+Nephew plc (CORI Surgical System), and Medtronic plc (Mazor X Stealth Edition) lead the global orthopedic robotics market through established robotic platforms, comprehensive implant portfolios, and extensive surgeon training networks. Johnson & Johnson (DePuy Synthes - VELYS Digital Surgery), Globus Medical, Inc. (ExcelsiusGPS), NuVasive, Inc. (Pulse platform), and Think Surgical, Inc. (TMINI Robotic System) strengthen market presence through specialized spine robotics capabilities and innovative platform architectures. Meanwhile, emerging players including TINAVI Medical Technologies Co., Ltd., Corin Group (OMNIBotics), Medacta International SA (ROSA Knee System partnership), Exactech, Inc. (Active Robotics), and Brainlab AG (Curve Image Guided Surgery) are expanding competitive dynamics through cost-optimized systems targeting price-sensitive markets, open-platform architectures enabling multi-vendor implant compatibility, and specialized capabilities in trauma surgery and sports medicine applications underserved by established manufacturers.

The global orthopedic robotics market is expected to grow from USD 4.21 billion in 2026 to USD 15.82 billion by 2036.

The global orthopedic robotics market is projected to grow at a CAGR of 14.2% from 2026 to 2036.

Robotic systems dominate the market representing 65-70% of revenue as core capital equipment. However, instruments & accessories demonstrate fastest growth at 16-18% CAGR driven by recurring revenue nature of disposable components and procedure-specific instrument packs.

AI and machine learning enable personalized surgical planning analyzing patient-specific anatomy, predict optimal implant positioning based on historical outcomes data, provide real-time intraoperative decision support, support predictive maintenance of robotic systems, and enable continuous algorithm improvement through analysis of surgical performance metrics across large procedure datasets.

North America holds 45-50% of global market driven by high procedure volumes, favorable reimbursement, and established technology adoption. Asia-Pacific demonstrates fastest growth at 16-18% CAGR propelled by aging populations, rising prosperity, and medical tourism expansion.

The leading companies include Stryker Corporation (Mako Surgical), Zimmer Biomet Holdings, Inc., Smith+Nephew plc, Medtronic plc, Johnson & Johnson (DePuy Synthes), Globus Medical, Inc., and NuVasive, Inc.

Published Date: Jul-2026

Published Date: Feb-2026

Published Date: Jan-2025

Published Date: Nov-2024

Published Date: Jun-2026

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates