Resources

About Us

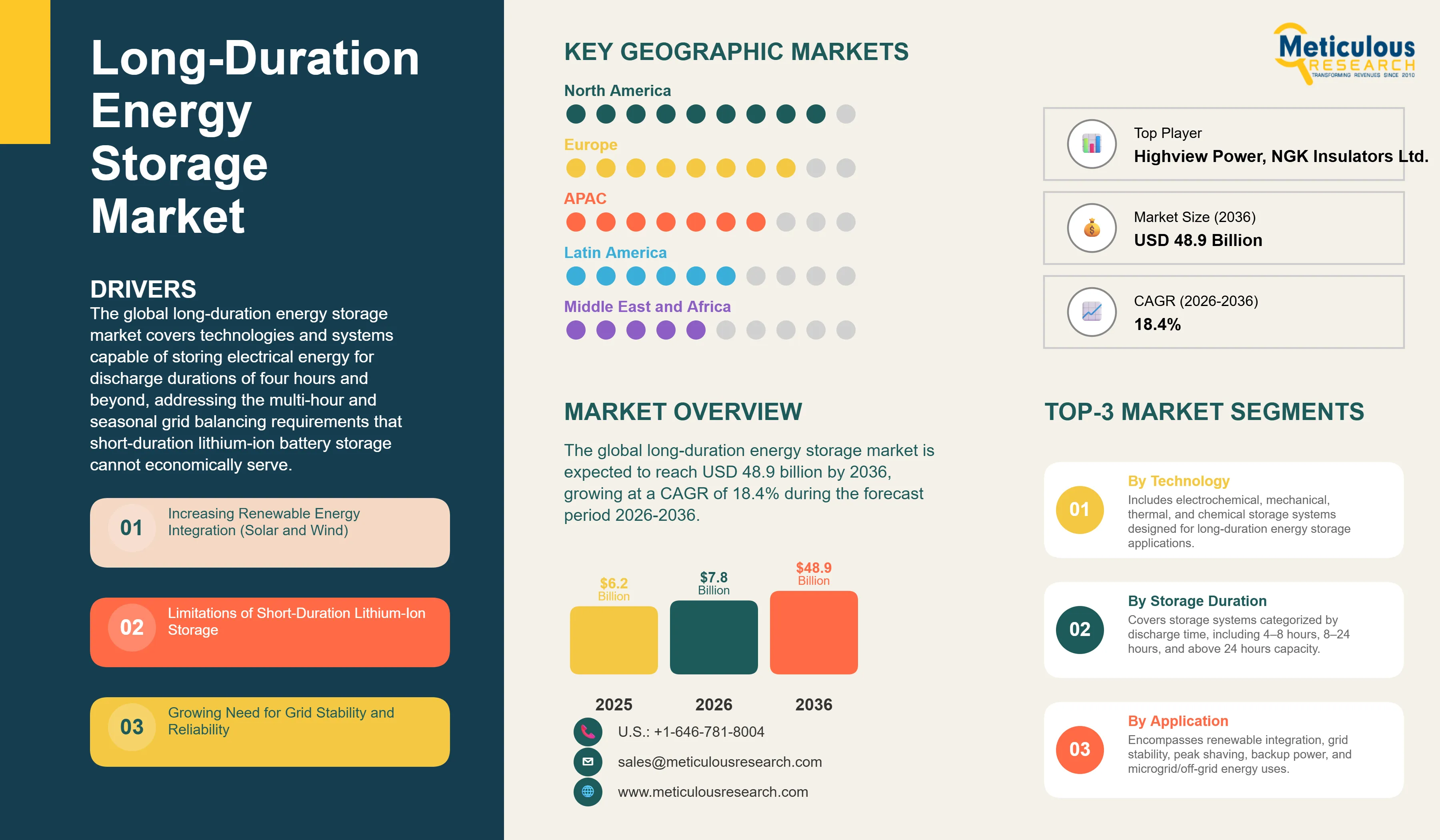

The global long-duration energy storage market was valued at USD 6.2 billion in 2025. This market is expected to reach USD 48.9 billion by 2036 from an estimated USD 7.8 billion in 2026, growing at a CAGR of 18.4% during the forecast period 2026-2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global long-duration energy storage market covers technologies and systems capable of storing electrical energy for discharge durations of four hours and beyond, addressing the multi-hour and seasonal grid balancing requirements that short-duration lithium-ion battery storage cannot economically serve. The market encompasses electrochemical technologies including vanadium redox flow batteries, iron-air batteries, and sodium-sulfur batteries; mechanical technologies including pumped hydro storage, compressed air energy storage, liquid air energy storage, and gravity-based systems; thermal storage including molten salt, solid-state, and cryogenic platforms; and chemical storage encompassing hydrogen-based storage and power-to-gas systems. These technologies collectively serve the grid stability, renewable integration, and energy resilience requirements of utilities, independent power producers, commercial and industrial customers, and off-grid communities.

The market's growth is driven by the accelerating global buildout of variable renewable energy capacity, which is creating multi-hour and multi-day supply-demand imbalances that short-duration storage cannot address. The structural limitation of four-hour lithium-ion systems in managing overnight solar gaps, multi-day wind lulls, and seasonal demand variations is motivating grid operators and policymakers to actively support the commercialization of long-duration alternatives. The U.S. Department of Energy's Long-Duration Storage Shot targeting an 90% reduction in storage costs for systems delivering more than 10 hours of duration, the European Union's battery regulation and grid flexibility frameworks, and national LDES procurement programs in the U.K., Australia, and California are creating the policy and funding environment required to scale nascent LDES technologies toward commercial deployment.

The market faces meaningful structural constraints. The capital cost of most LDES technologies remains substantially higher than short-duration lithium-ion alternatives on a per-kWh basis, and the absence of established revenue frameworks for the multi-hour grid services that LDES uniquely provides creates project financing uncertainty that slows investment decisions. Most electrochemical and novel mechanical LDES technologies are at early commercial stage with limited operational track records, increasing perceived technology risk for utilities and financiers accustomed to the established performance history of pumped hydro and lithium-ion systems.

These constraints are being progressively addressed as early commercial LDES deployments accumulate operational data, as power purchase agreement and capacity market structures evolve to compensate multi-hour storage services, and as technology costs decline through manufacturing scale and materials innovation. Form Energy's iron-air battery deployments with Georgia Power, Highview Power's liquid air energy storage commercial projects in the U.K., and Hydrostor's advanced compressed air energy storage pipeline in North America are building the commercial reference base that will enable broader project finance and utility procurement in the second half of the forecast period.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 48.9 Billion |

|

Market Size in 2026 |

USD 7.8 Billion |

|

Market Size in 2025 |

USD 6.2 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 18.4% |

|

Dominating Technology |

Mechanical Storage |

|

Fastest Growing Technology |

Electrochemical Storage |

|

Dominating Storage Duration |

4 to 8 Hours |

|

Fastest Growing Storage Duration |

Above 24 Hours |

|

Dominating Application |

Renewable Energy Integration |

|

Fastest Growing Application |

Microgrids and Off-Grid Systems |

|

Dominating End User |

Utilities |

|

Fastest Growing End User |

Independent Power Producers (IPPs) |

|

Dominating Installation Type |

Grid-Scale Storage |

|

Fastest Growing Installation Type |

Off-Grid Systems |

|

Dominating Energy Capacity |

100 to 500 MWh |

|

Fastest Growing Energy Capacity |

Above 500 MWh |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Increasing Renewable Energy Integration (Solar and Wind)

The rapid global expansion of solar and wind generation capacity is creating multi-hour energy surplus and deficit periods that fundamentally require long-duration storage to manage. Solar generation produces surplus power during midday hours that exceeds real-time demand and must be stored for evening and overnight consumption, while wind generation variability creates multi-day periods of low output that cannot be bridged by four-hour battery systems. The International Energy Agency projects that achieving net-zero electricity systems will require 10 times the current installed storage capacity globally by 2050, with long-duration systems providing the majority of the incremental capacity needed to firm variable renewable output across daily and seasonal timescales. California's grid operator CAISO, the U.K.'s National Grid ESO, and Germany's Bundesnetzagentur have each identified multi-hour storage procurement as a critical near-term grid investment priority as renewable penetration approaches and exceeds 50% of annual generation in their respective markets.

Limitations of Short-Duration Lithium-Ion Storage

The structural inability of four-hour lithium-ion battery systems to serve multi-hour grid balancing, overnight renewable energy shifting, and seasonal storage applications is creating an addressable market gap for long-duration technologies that complements rather than competes with short-duration storage deployment. Lithium-ion system economics deteriorate sharply for storage durations beyond four to six hours due to the linear scaling of battery cell costs with energy capacity, making eight-hour and longer lithium-ion systems uneconomical relative to LDES technologies whose capital cost structures are partially or fully decoupled from discharge duration. The recognition by grid planners, utilities, and regulators that a storage-only clean electricity grid requires both short-duration and long-duration technologies serving distinct grid service functions is creating parallel procurement frameworks for LDES that are no longer competing against short-duration storage for the same project mandates.

Growth in Renewable Energy Curtailment Mitigation

The escalating volume of renewable energy curtailed globally due to transmission constraints, negative pricing periods, and the absence of sufficient storage capacity represents a quantified revenue opportunity for LDES projects. The U.S. Energy Information Administration estimated approximately 4% of utility-scale solar and wind generation was curtailed in 2024, representing billions of dollars of generation value that LDES could capture by absorbing surplus power during curtailment periods and discharging during high-demand hours. In California, Texas, and the U.K., curtailment volumes are concentrated in predictable seasonal and diurnal patterns that align well with the operating profiles of long-duration storage systems, enabling project developers to structure offtake contracts around the curtailment capture value proposition alongside additional grid service revenue streams.

Development of Novel Storage Technologies (Iron-Air, Flow Batteries)

The commercial emergence of iron-air, vanadium redox flow, and zinc-bromine flow battery technologies specifically designed for long-duration applications is expanding the addressable LDES technology portfolio beyond pumped hydro and compressed air to include scalable, sitable electrochemical platforms that can be deployed at grid-connected sites without specific geological or topographic requirements. Form Energy's iron-air battery technology, which uses the reversible rusting of iron to store and release energy at a projected cost below USD 20 per kWh for long-duration applications, represents a potential step-change in electrochemical LDES economics that could enable broad grid-scale deployment across locations where pumped hydro and compressed air storage are not feasible. Vanadium redox flow batteries from companies including Invinity Energy Systems, ESS Tech, and Sumitomo Electric offer demonstrated multi-thousand-cycle lifetimes exceeding 20 years with no degradation in storage capacity, providing a total cost of ownership advantage over lithium-ion for applications requiring frequent deep cycling over extended project lives.

Commercialization of Iron-Air and Flow Battery Technologies

The transition of iron-air and flow battery LDES platforms from development-stage to early commercial deployment marks the most significant competitive development in the LDES market during the current period. Form Energy's multi-megawatt iron-air battery systems entering commercial operation with utility partners in the United States and ESS Tech's all-iron flow battery deployments at commercial and industrial sites are establishing operational performance track records that are enabling project finance conversations and scaling manufacturing investment. The demonstrated ability of flow batteries to deliver thousands of full depth-of-discharge cycles without capacity degradation is making them increasingly competitive against lithium-ion for applications requiring daily multi-hour cycling across project lives of 20 years or more.

Expansion of Government-Funded LDES Demonstration Programs

National governments are deploying substantial public funding to accelerate LDES technology demonstrations that bridge the gap between laboratory performance and grid-scale commercial operation. The U.S. DOE's Office of Clean Energy Demonstrations has committed over USD 350 million to LDES projects under the Grid Resilience and Innovation Partnerships program. The U.K.'s Longer Duration Energy Storage Demonstration program and the European Innovation Fund's LDES project grants are funding commercial-scale demonstrations of compressed air, liquid air, flow battery, and gravity storage systems. These funded demonstrations are generating publicly available operational data that is progressively reducing technology risk perceptions among utilities and infrastructure investors, accelerating the pathway from demonstration to commercial procurement.

Growing Role of Pumped Hydro Modernization and Expansion

Pumped hydro storage, which accounts for over 90% of global installed long-duration storage capacity, is undergoing significant capacity expansion and operational modernization through both new greenfield project development and the upgrading of existing facilities with variable-speed pump-turbine technology that improves grid balancing responsiveness. The global pumped hydro project pipeline tracked by the International Hydropower Association exceeds 150 GW of projects in advanced development or construction, representing a multi-decade wave of new capacity that will maintain pumped hydro's dominant position in the long-duration storage market while providing the grid-scale firming capacity required for deep renewable integration in major electricity markets.

By Technology: In 2026, Mechanical Storage to Dominate

Based on technology, the global long-duration energy storage market is segmented into electrochemical storage, mechanical storage, thermal energy storage, chemical energy storage, and other LDES technologies. In 2026, the mechanical storage segment is expected to account for the largest share of the market, reflecting the overwhelming dominance of pumped hydro storage in the global installed long-duration storage capacity base. Pumped hydro represents approximately 90% of total installed LDES capacity globally, with over 170 GW of operational capacity across Asia, Europe, and North America providing multi-hour to multi-day energy shifting services. The mature technology status, multi-decade operational lifetimes, and low levelized cost of storage for well-sited pumped hydro projects make it the reference benchmark against which all emerging LDES technologies are assessed. Compressed air energy storage projects in development in Canada, the United States, and Australia are adding to the mechanical storage pipeline alongside pumped hydro expansion.

Electrochemical storage is projected to register the highest CAGR during the forecast period, driven by the commercial scale-up of iron-air, vanadium redox flow, and all-iron flow battery technologies that offer deployment flexibility not available to pumped hydro and compressed air systems, enabling LDES at grid-connected substations and industrial sites without specific geological or hydrological prerequisites.

By Storage Duration: In 2026, 4 to 8 Hours to Hold the Largest Share

Based on storage duration, the global long-duration energy storage market is segmented into 4 to 8 hours, 8 to 24 hours, and above 24 hours. In 2026, the 4 to 8 hours segment is expected to account for the largest share of the market. This segment represents the initial commercial frontier of long-duration storage, covering the discharge duration range immediately beyond the commercial sweet spot of four-hour lithium-ion systems and addressing the overnight solar energy shifting and evening peak demand applications that represent the largest near-term grid service revenue opportunity for LDES. The majority of current commercial LDES project procurements in the United States, U.K., and Australia target storage durations in the 6 to 12 hour range where economic value is clearest and technology options are most established.

The above 24 hours segment is projected to register the highest CAGR during the forecast period, representing the frontier of seasonal and multi-day storage applications that become essential for electricity grids with renewable penetration exceeding 80% of annual generation. Hydrogen-based storage, liquid air energy storage, and large-scale pumped hydro with very high reservoir capacity are the primary technology candidates for this duration tier, which will see accelerating deployment in the second half of the forecast period as renewable penetration in leading markets approaches levels requiring multi-day storage support.

By Application: In 2026, Renewable Energy Integration to Hold the Largest Share

Based on application, the global long-duration energy storage market is segmented into renewable energy integration, grid stability and frequency regulation, peak shaving and load shifting, backup power and resilience, and microgrids and off-grid systems. In 2026, the renewable energy integration segment is expected to account for the largest share, reflecting the primary value proposition of LDES as the essential complement to variable renewable generation that enables clean electricity systems to deliver reliable power independent of short-term solar and wind output variations. The deployment of LDES for renewable integration is being actively incentivized through capacity auction frameworks, storage mandates, and renewable firming contracts across the United States, United Kingdom, Australia, and Germany.

Microgrids and off-grid systems is projected to register the highest CAGR during the forecast period. Island grids, remote mining operations, military installations, and data centers requiring 24-hour clean power supply without utility grid backup are driving demand for LDES systems capable of providing multiple days of energy autonomy, supporting the deployment of both flow battery and liquid air storage technologies in off-grid applications at premium pricing relative to utility grid-connected installations.

By End User: In 2026, Utilities to Hold the Largest Share

Based on end user, the global long-duration energy storage market is segmented into utilities, independent power producers, commercial and industrial, and government and public sector. In 2026, the utilities segment is expected to account for the largest share of the market, reflecting utilities' role as the primary procurers of grid-scale long-duration storage capacity through regulated capital investment programs, competitive storage tenders, and bilateral capacity contracts. Utilities in California, Arizona, New York, the U.K., and Germany are advancing LDES procurement frameworks that mandate multi-hour storage procurement alongside renewable energy portfolio targets.

Independent power producers are projected to register the highest CAGR during the forecast period, driven by the growing developer activity in merchant LDES projects capturing renewable energy arbitrage and capacity market revenues without utility offtake backing, enabled by the increasing depth of LDES-relevant grid services markets and the improving project economics of leading LDES technologies.

By Installation Type: In 2026, Grid-Scale Storage to Hold the Largest Share

Based on installation type, the global long-duration energy storage market is segmented into grid-scale storage, behind-the-meter storage, and off-grid systems. In 2026, the grid-scale segment is expected to account for the largest share, reflecting the concentration of long-duration storage value creation in large transmission-connected systems that provide multi-hour balancing services to bulk electricity markets. Grid-scale LDES projects ranging from 50 MW to several hundred MW in capacity connected at the transmission or distribution substation level represent the primary commercial opportunity for the current generation of pumped hydro, compressed air, flow battery, and large-scale thermal storage technologies.

Off-grid systems is projected to register the highest CAGR during the forecast period, supported by the strong economics of LDES in displacing diesel generation at remote and island locations where the fuel cost of conventional backup generation and the grid extension cost create favorable economics for renewable-plus-LDES systems even at current technology costs.

By Energy Capacity: In 2026, 100 to 500 MWh to Hold the Largest Share

Based on energy capacity, the global long-duration energy storage market is segmented into below 100 MWh, 100 to 500 MWh, and above 500 MWh. In 2026, the 100 to 500 MWh segment is expected to account for the largest share, representing the project size range that aligns with current utility procurement tender requirements and the commercial scale of leading LDES technology deployments. Projects in this capacity range balance site availability, grid interconnection requirements, and capital commitment levels that are within the investment threshold of utility capital programs and infrastructure fund mandates.

The above 500 MWh segment is projected to register the highest CAGR during the forecast period, driven by the progression of LDES from initial commercial deployments toward large flagship projects targeting gigawatt-hour scale capacity. Multi-gigawatt-hour pumped hydro projects in Australia, compressed air storage projects in Canada, and hydrogen-coupled seasonal storage installations in Northern Europe represent the pipeline of above-500 MWh projects that will define the market's scale trajectory through the late forecast period.

Long-Duration Energy Storage Market by Region: North America Leading by Share, Asia-Pacific by Growth

Based on geography, the global long-duration energy storage market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

In 2026, North America is expected to account for the largest share of the global long-duration energy storage market. The region's leadership is anchored by the United States, where the combination of the Inflation Reduction Act's investment tax credit for standalone storage, the DOE's Long-Duration Storage Shot, and California and New York state-level storage procurement mandates has created the most financially supportive policy environment for LDES commercialization globally. California's CPUC storage mandate, requiring utilities to procure substantial LDES capacity by 2030, is directly driving procurement activity from Pacific Gas and Electric, Southern California Edison, and San Diego Gas and Electric that represents among the largest utility LDES tender pipelines worldwide. The active developer ecosystem including Form Energy, Hydrostor, Highview Power, and Energy Vault with projects in advanced development across the United States and Canada, supported by DOE loan guarantee and grant programs, is building the early commercial reference base for the full range of LDES technology categories.

Europe represents the second largest regional market, driven by the European Union's ambition to deploy 600 GW of renewable energy by 2030 under the REPowerEU program that creates structural multi-hour storage demand at a scale requiring long-duration solutions beyond the capacity of short-duration lithium-ion systems alone. The U.K.'s Longer Duration Energy Storage Demonstration competition, Germany's hydrogen storage investment programs, Norway's pumped hydro pipeline leveraging exceptional topographical and hydrological resources, and the Nordic region's seasonal storage requirements collectively create a diverse and deep pipeline of LDES projects across technology categories. The EU Innovation Fund's support for large-scale CAES, liquid air, and advanced flow battery projects is advancing commercial demonstrations of multiple LDES technology platforms toward investment-grade operational track records.

However, Asia-Pacific is expected to grow at the fastest CAGR during the forecast period. China's massive renewable energy deployment, exceeding 1.2 TW of installed wind and solar capacity in 2025, is creating an urgent and structurally large demand for long-duration balancing capability at a scale that no other region approaches. China's National Development and Reform Commission has designated new energy storage as a strategic industry priority with specific LDES procurement targets embedded in provincial energy transition plans. Australia's ambitious 82% renewable electricity target by 2030 under the Capacity Investment Scheme is driving an exceptional pipeline of pumped hydro, battery, and emerging LDES technology projects across the National Electricity Market. India's renewable energy expansion under its 500 GW non-fossil capacity target and Japan's strategic battery and hydrogen storage programs are further reinforcing the region's position as the fastest-growing LDES market through the forecast period.

The global long-duration energy storage market features a competitive ecosystem spanning established industrial conglomerates with mature mechanical and electrochemical storage technology portfolios, purpose-built LDES technology developers advancing novel electrochemical and mechanical platforms, and integrated energy companies combining project development expertise with proprietary storage technology. The competitive structure is relatively fragmented compared with the lithium-ion storage market, reflecting the diversity of technology approaches and the early commercial stage of most non-pumped-hydro LDES technologies, where no single platform has yet achieved the market dominance that lithium-ion has established in short-duration storage.

Key players operating in the global long-duration energy storage market include Form Energy Inc. (U.S.), ESS Tech Inc. (U.S.), Fluence Energy Inc. (U.S.), Highview Power (U.K.), Hydrostor Inc. (Canada), Siemens Energy AG (Germany), General Electric Company (U.S.), Mitsubishi Power (Japan), Sumitomo Electric Industries Ltd. (Japan), NGK Insulators Ltd. (Japan), Invinity Energy Systems (U.K.), Energy Vault Holdings Inc. (U.S.), Malta Inc. (U.S.), Primus Power Corporation (U.S.), and Redflow Limited (Australia), among others.

The global long-duration energy storage market is expected to reach USD 48.9 billion by 2036 from an estimated USD 7.8 billion in 2026, at a CAGR of 18.4% during the forecast period 2026-2036.

In 2026, the mechanical storage segment is expected to hold the largest share, driven by the overwhelming dominance of pumped hydro in the global installed long-duration storage capacity base, which accounts for approximately 90% of total installed LDES capacity worldwide.

Electrochemical storage is expected to register the highest CAGR during the forecast period 2026-2036, driven by the commercial scale-up of iron-air, vanadium redox flow, and all-iron flow battery technologies that offer siting flexibility advantages over pumped hydro and compressed air and whose costs are declining with manufacturing scale and materials innovation.

The above 24 hours segment is projected to register the highest CAGR during the forecast period, representing the frontier of seasonal and multi-day storage requirements that become essential for electricity grids with renewable penetration exceeding 80% of annual generation, addressable by hydrogen-based storage, liquid air, and large pumped hydro systems.

Microgrids and off-grid systems is projected to register the highest CAGR, driven by strong economics for LDES in displacing diesel at remote mining operations, island grids, and industrial facilities requiring 24-hour clean power autonomy, where fuel cost avoidance and grid independence value justify current LDES cost levels.

Growth is primarily driven by the accelerating global renewable energy buildout creating multi-hour supply-demand imbalances that short-duration storage cannot address, the structural cost limitations of lithium-ion systems at discharge durations beyond four to six hours that create an addressable market for LDES technologies, supportive government funding and procurement frameworks in the United States, Europe, and Australia, and the commercial emergence of iron-air and flow battery platforms offering new siting flexibility and long project life economics.

Asia-Pacific is expected to register the highest growth rate during the forecast period 2026-2036, driven by China's massive renewable energy deployment scale requiring gigawatt-scale long-duration balancing capacity, Australia's 82% renewable target driving an exceptional LDES project pipeline, and India's and Japan's strategic storage investment programs supporting the region's rapid clean energy transition.

Key players are Form Energy Inc. (U.S.), ESS Tech Inc. (U.S.), Fluence Energy Inc. (U.S.), Highview Power (U.K.), Hydrostor Inc. (Canada), Siemens Energy AG (Germany), General Electric Company (U.S.), Mitsubishi Power (Japan), Sumitomo Electric Industries Ltd. (Japan), NGK Insulators Ltd. (Japan), Invinity Energy Systems (U.K.), Energy Vault Holdings Inc. (U.S.), Malta Inc. (U.S.), Primus Power Corporation (U.S.), and Redflow Limited (Australia), among others.

1. Introduction

1.1 Market Definition

1.2 Market Ecosystem

1.3 Currency and Limitations

1.3.1 Currency

1.3.2 Limitations

1.4 Key Stakeholders

2. Research Methodology

2.1 Research Approach

2.2 Data Collection and Validation Process

2.2.1 Secondary Research

2.2.2 Primary Research and Validation

2.2.2.1 Primary Interviews with Experts

2.2.2.2 Approaches for Country/Region-Level Analysis

2.3 Market Estimation

2.3.1 Bottom-Up Approach

2.3.2 Top-Down Approach

2.3.3 Growth Forecast

2.4 Data Triangulation

2.5 Assumptions for the Study

3. Executive Summary

4. Market Overview

4.1 Introduction

4.2 Market Dynamics

4.2.1 Drivers

4.2.2 Restraints

4.2.3 Opportunities

4.2.4 Challenges

4.3 Technology Landscape

4.3.1 Electrochemical Storage (Flow Batteries, Advanced Li-ion)

4.3.2 Mechanical Storage (Pumped Hydro, Compressed Air)

4.3.3 Thermal Energy Storage

4.3.4 Chemical Storage (Hydrogen-Based Storage)

4.4 Value Chain Analysis

4.4.1 Raw Material and Component Suppliers

4.4.2 Technology Providers

4.4.3 EPC and System Integrators

4.4.4 Utilities and Grid Operators

4.4.5 End Users

4.5 Regulatory and Policy Landscape

4.5.1 Renewable Energy and Storage Policies

4.5.2 Grid Integration Regulations

4.5.3 Incentive Programs and Subsidies

5. Long-Duration Energy Storage Market, by Technology

5.1 Introduction

5.2 Electrochemical Storage

5.2.1 Flow Batteries

5.2.1.1 Vanadium Redox Flow Batteries

5.2.1.2 Zinc-Bromine Flow Batteries

5.2.2 Advanced Lithium-ion Batteries

5.2.3 Sodium-Sulfur Batteries

5.2.4 Iron-Air Batteries

5.3 Mechanical Storage

5.3.1 Pumped Hydro Storage

5.3.2 Compressed Air Energy Storage (CAES)

5.3.3 Liquid Air Energy Storage (LAES)

5.3.4 Flywheel Energy Storage

5.4 Thermal Energy Storage

5.4.1 Molten Salt Storage

5.4.2 Solid-State Thermal Storage

5.4.3 Cryogenic Energy Storage

5.5 Chemical Energy Storage

5.5.1 Hydrogen Storage

5.5.2 Power-to-Gas Systems

5.5.3 Synthetic Fuels

5.6 Other LDES Technologies

6. Long-Duration Energy Storage Market, by Storage Duration

6.1 Introduction

6.2 4 to 8 Hours

6.3 8 to 24 Hours

6.4 Above 24 Hours

7. Long-Duration Energy Storage Market, by Application

7.1 Introduction

7.2 Renewable Energy Integration

7.3 Grid Stability and Frequency Regulation

7.4 Peak Shaving and Load Shifting

7.5 Backup Power and Resilience

7.6 Microgrids and Off-Grid Systems

8. Long-Duration Energy Storage Market, by End User

8.1 Introduction

8.2 Utilities

8.3 Independent Power Producers (IPPs)

8.4 Commercial and Industrial

8.5 Government and Public Sector

9. Long-Duration Energy Storage Market, by Installation Type

9.1 Introduction

9.2 Grid-Scale Storage

9.3 Behind-the-Meter Storage

9.4 Off-Grid Systems

10. Long-Duration Energy Storage Market, by Energy Capacity

10.1 Introduction

10.2 Below 100 MWh

10.3 100 to 500 MWh

10.4 Above 500 MWh

11. Long-Duration Energy Storage Market, by Geography

11.1 Introduction

11.2 North America

11.2.1 U.S.

11.2.2 Canada

11.3 Europe

11.3.1 Germany

11.3.2 U.K.

11.3.3 France

11.3.4 Italy

11.3.5 Spain

11.3.6 Netherlands

11.3.7 Norway

11.3.8 Sweden

11.3.9 Denmark

11.3.10 Rest of Europe

11.4 Asia-Pacific

11.4.1 China

11.4.2 Japan

11.4.3 India

11.4.4 South Korea

11.4.5 Australia

11.4.6 Singapore

11.4.7 Malaysia

11.4.8 Thailand

11.4.9 Indonesia

11.4.10 Vietnam

11.4.11 Rest of Asia-Pacific

11.5 Latin America

11.5.1 Brazil

11.5.2 Mexico

11.5.3 Chile

11.5.4 Argentina

11.5.5 Colombia

11.5.6 Rest of Latin America

11.6 Middle East and Africa

11.6.1 UAE

11.6.2 Saudi Arabia

11.6.3 South Africa

11.6.4 Israel

11.6.5 Turkey

11.6.6 Rest of Middle East and Africa

12. Competitive Landscape

12.1 Overview

12.2 Key Growth Strategies

12.3 Competitive Benchmarking

12.4 Competitive Dashboard

12.4.1 Industry Leaders

12.4.2 Market Differentiators

12.4.3 Vanguards

12.4.4 Emerging Companies

12.5 Market Ranking/Positioning Analysis of Key Players, 2025

13. Company Profiles

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

13.1 Form Energy, Inc.

13.2 ESS Tech, Inc.

13.3 Fluence Energy, Inc.

13.4 Highview Power

13.5 Hydrostor Inc.

13.6 Siemens Energy AG

13.7 General Electric Company

13.8 Mitsubishi Power

13.9 Sumitomo Electric Industries, Ltd.

13.10 NGK Insulators, Ltd.

13.11 Invinity Energy Systems

13.12 Energy Vault Holdings, Inc.

13.13 Malta Inc.

13.14 Primus Power Corporation

13.15 Redflow Limited

14. Appendix

14.1 Additional Customization

14.2 Related Reports

Published Date: May-2026

Published Date: Jul-2024

Published Date: Jun-2023

Subscribe to get the latest industry updates