Resources

About Us

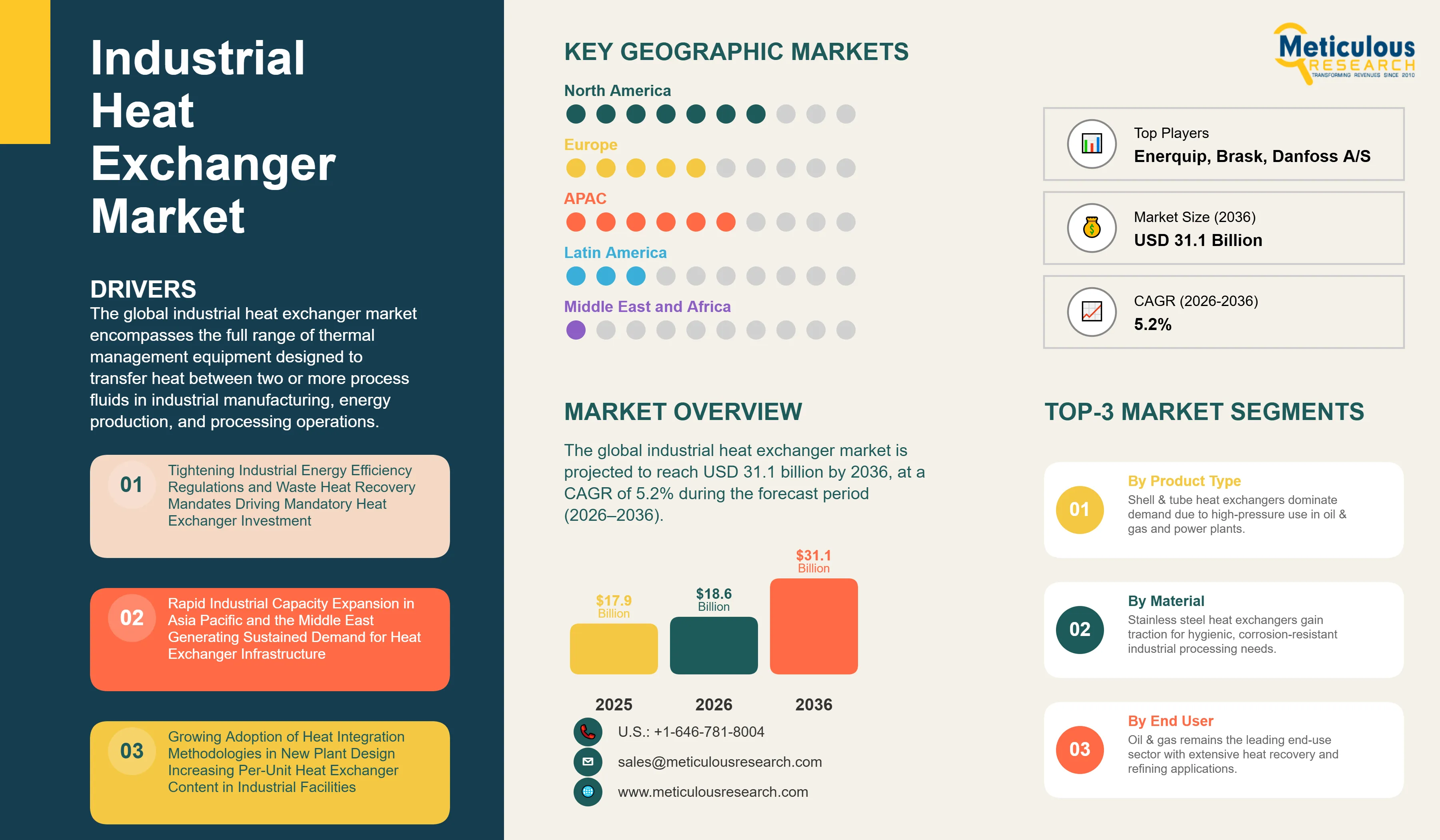

Industrial Heat Exchanger Market Size, Share & Trends Analysis, by Product Type, Material, and End-use Industry — Global Opportunity Analysis & Forecast (2026–2036)

Report ID: MREP - 1041991 Pages: 276 May-2026 Formats*: PDF Category: Energy and Power Delivery: 24 to 72 Hours Download Free Sample ReportThe global industrial heat exchanger market was valued at USD 17.9 billion in 2025. The market is projected to reach USD 31.1 billion by 2036, growing from USD 18.6 billion in 2026 at a CAGR of 5.2% during the forecast period (2026–2036).

Click here to: Get Free Sample Pages of this Report

The global industrial heat exchanger market encompasses the full range of thermal management equipment designed to transfer heat between two or more process fluids in industrial manufacturing, energy production, and processing operations. The market includes shell and tube heat exchangers, plate heat exchangers covering gasketed, brazed, semi-welded, and fully welded configurations air cooled heat exchangers, spiral heat exchangers, and double pipe heat exchangers deployed across end-use industries including oil and gas, chemical and petrochemical, power generation, food and beverage processing, pharmaceutical and biotechnology, HVAC and district energy, pulp and paper, and metals and mining.

These systems are integral to industrial plant operations where precise thermal control is required to manage process fluid temperatures, recover waste heat, condense vapors, vaporize liquids, and optimize overall energy utilization. Heat exchangers operate across a wide range of temperature, pressure, and corrosivity conditions, and are designed in a broad range of materials including carbon steel, stainless steel, titanium, and nickel and high-performance alloys to match specific process fluid compatibility requirements.

The growth of the industrial heat exchanger market is primarily driven by the progressive tightening of industrial energy efficiency regulations across major manufacturing economies, which is shifting heat recovery investment from discretionary capital expenditure toward a compliance-driven procurement priority. According to the International Energy Agency, the industrial sector accounts for approximately 37 percent of global final energy demand, with thermal processes — including heating, cooling, condensing, and heat recovery — representing the dominant share of industrial energy consumption. This structural dependence on thermal energy management across the global manufacturing base creates sustained demand for heat exchanger systems capable of maximizing thermal efficiency and minimizing energy input across production processes.

In the United States, the Department of Energy's Industrial Efficiency and Decarbonization Office has identified waste heat recovery through advanced heat exchanger deployment as one of the highest-impact levers for reducing industrial energy consumption. The DOE's Better Plants program, which works with over 300 U.S. manufacturing partners, actively promotes heat integration and heat recovery best practices, reinforcing procurement momentum for high-efficiency heat exchanger systems across energy-intensive sectors including chemicals, food processing, and metals manufacturing.

In Europe, the revised Energy Efficiency Directive (Directive 2023/1791), formally adopted in September 2023 and requiring transposition by Member States by October 11, 2025, mandates a binding EU-level energy consumption reduction target of at least 11.7 percent by 2030 relative to 2020 projections. This directive places significant compliance obligations on large industrial enterprises to audit their thermal energy use and implement heat recovery measures, creating a structured investment cycle for heat exchanger upgrades and new installations across European manufacturing facilities.

In addition to regulatory compliance, growing awareness among industrial operators of the operational and financial impact of suboptimal thermal management including elevated fuel costs, increased cooling water consumption, greater process variability, and higher carbon emissions is reinforcing demand for advanced heat exchanger technologies. The integration of industrial IoT capabilities and digital performance monitoring into heat exchanger systems is further accelerating adoption by enabling predictive fouling detection, real-time thermal performance tracking, and condition-based maintenance scheduling that reduce operational costs and extend equipment service life.

Despite strong growth fundamentals, the market faces challenges related to the high capital expenditure associated with heat exchanger installation and system integration in retrofit applications, where existing plant layouts and process piping configurations complicate the introduction of new thermal equipment. Fouling remains the dominant operational challenge across a broad range of industrial applications, where deposits of scale, biological growth, corrosion products, and process debris on heat transfer surfaces progressively reduce thermal efficiency and increase pressure drop, leading to unplanned maintenance and production losses. The complexity of material selection for process fluids with high corrosivity, elevated temperature, or mixed-phase compositions continues to influence procurement decisions and total cost of ownership calculations across industrial buyers.

The tightening of global industrial energy efficiency and decarbonization regulations is creating significant opportunities for heat exchanger manufacturers offering integrated thermal management solutions that combine high-efficiency equipment with waste heat recovery engineering services, digital monitoring, and lifecycle performance guarantees. The growing adoption of compact plate and welded heat exchanger designs is opening new addressable markets in small and mid-size manufacturing enterprises that were previously served exclusively by conventional shell and tube configurations. In addition, the rapid expansion of chemical and petrochemical manufacturing capacity in Asia Pacific and the Middle East, alongside the accelerating buildout of pharmaceutical and food processing facilities in emerging markets, is creating structurally new demand segments for high-efficiency and hygienic-grade heat exchanger technologies.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 31.1 Billion |

|

Market Size in 2026 |

USD 18.6 Billion |

|

Market Size in 2025 |

USD 17.9 Billion |

|

Revenue Growth Rate (2026–2036) |

CAGR of 5.2% |

|

Dominating Product Type |

Shell and Tube Heat Exchangers |

|

Fastest Growing Product Type |

Plate Heat Exchangers |

|

Dominating Material |

Carbon Steel |

|

Fastest Growing Material |

Stainless Steel |

|

Dominating End-use Industry |

Oil and Gas |

|

Fastest Growing End-use Industry |

Chemical and Petrochemical |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

EU Energy Efficiency Directive and Global Industrial Decarbonization Mandates Driving Mandatory Heat Recovery Investment

The progressive tightening of industrial energy efficiency regulations across major manufacturing economies represents one of the most structurally significant demand drivers in the global industrial heat exchanger market, shifting heat recovery investment from largely optional capital spending toward a compliance-driven expenditure category with clearly defined performance obligations and regulatory deadlines.

The European Union's revised Energy Efficiency Directive (Directive 2023/1791), requiring transposition across Member States by October 2025, has introduced binding energy savings obligations that directly incentivize industrial operators to maximize waste heat recovery and minimize thermal energy losses through heat exchanger upgrades and new installations. Large enterprises in energy-intensive sectors are now required to conduct formal energy audits every four years and implement all cost-effective energy efficiency measures identified, including heat recovery systems and high-performance heat exchanger installations. This regulatory framework creates a structured procurement cycle for heat exchanger systems across European chemical, food processing, paper, and manufacturing industries, reinforcing sustained capital investment in advanced thermal management infrastructure.

In the United States, the Department of Energy's Industrial Efficiency and Decarbonization Office has established industrial waste heat recovery as a priority investment area, supported by funding mechanisms under the Inflation Reduction Act of 2022 that extended tax credits to industrial energy efficiency improvements, including heat integration and heat recovery system installations. The IRA's Section 48C Advanced Energy Project Credit, which allocated USD 10 billion to qualifying advanced energy manufacturing and industrial efficiency projects, has stimulated procurement activity for advanced heat exchanger systems in sectors including chemicals, metals, and food processing that are undertaking heat integration and decarbonization capital projects.

Globally, the enforcement of China's updated Energy Conservation Law, which was revised in 2024 to strengthen mandatory energy efficiency standards for industrial facilities above specified energy consumption thresholds, is compelling large-scale adoption of heat recovery and waste heat utilization systems across the country's extensive manufacturing base. India's Perform, Achieve and Trade scheme under the Bureau of Energy Efficiency, which covers energy-intensive industrial sectors representing a significant share of the country's total industrial energy consumption, similarly reinforces compliance-led demand for heat exchanger upgrades among covered facilities. Taken together, these regulatory developments are creating a globally coordinated and sustained investment cycle for industrial heat exchanger systems that transcends individual sector or regional growth dynamics.

Plate Heat Exchanger Technology Advancing Into Applications Historically Dominated by Shell and Tube Designs

The ongoing displacement of conventional shell and tube heat exchanger configurations by compact plate-based heat exchanger technologies in new industrial installations represents the most significant product-level competitive shift currently reshaping the global industrial heat exchanger market. Plate heat exchangers including gasketed, brazed, semi-welded, and fully welded designs deliver heat transfer coefficients three to five times higher than comparable shell and tube configurations, enabling significantly more compact and lighter thermal management solutions that require less floor space, less material input, and less installation time in new construction and retrofit projects.

Advances in fully welded plate heat exchanger designs such as Alfa Laval AB's Compabloc and AlfaRex product lines and Kelvion Holdings GmbH's NT series welded plate heat exchangers have progressively extended plate-based technology into high-pressure and high-temperature applications in oil and gas refining, chemical processing, and power generation that were previously considered outside the viable operating envelope of plate heat exchangers. The elimination of gaskets in fully welded designs addresses the traditional limitation of gasketed plate exchangers in aggressive chemical media and high-temperature service conditions, enabling adoption across a significantly broader range of industrial process applications.

Brazed plate heat exchangers, widely deployed in HVAC, district energy, and refrigeration applications by manufacturers including SWEP International AB and Danfoss A/S, are also gaining adoption in food and beverage processing and pharmaceutical manufacturing where compact footprint and high thermal efficiency in a permanently sealed construction provide operational advantages over conventional designs. In parallel, spiral heat exchangers — offered by Alfa Laval and Tranter, Inc. — are gaining adoption in highly fouling applications involving slurries, viscous fluids, and fibrous media in pulp and paper, chemical, and wastewater treatment processes, where their single-channel geometry and high shear velocity fundamentally reduce fouling propensity compared to both shell and tube and flat-plate designs.

In response to this structural technology shift, established shell and tube manufacturers including Koch Heat Transfer Company, LP, API Heat Transfer Inc., and BORSIG GmbH are expanding their heat exchanger portfolios with enhanced tube geometries, high-performance tubesheet configurations, and application-specific alloy selections that maintain the competitive relevance of shell and tube designs in large-scale oil and gas, power generation, and chemical applications where no plate-based technology can cost-effectively match their throughput, pressure rating, or thermal cycling resilience.

Industrial IoT Integration and Predictive Fouling Detection Transforming Heat Exchanger Lifecycle Management

The incorporation of industrial IoT sensors, real-time data analytics, and connectivity platforms into heat exchanger systems is reshaping both the economics and the operational model of heat exchanger ownership across energy-intensive industries, fundamentally improving the commercial case for advanced heat exchanger investment by reducing unplanned downtime and extending equipment service intervals.

Fouling — the accumulation of scale, corrosion products, biological growth, and process debris on heat transfer surfaces — is the dominant operational challenge in industrial heat exchanger management, with industry studies estimating that fouling-related energy penalties, maintenance costs, and production losses represent a substantial share of total heat exchanger lifecycle costs across oil and gas, chemical, and food processing industries. Conventional maintenance practices, based on fixed cleaning intervals determined by historical experience rather than real-time equipment condition, lead to either premature maintenance interventions that interrupt production unnecessarily or continued operation with degraded thermal performance that consumes excess energy and accelerates mechanical deterioration.

Connected heat exchanger management platforms, such as Alfa Laval's 360° Service digital performance monitoring solution, deploy wireless pressure drop sensors and temperature transmitters to provide operators with continuous, real-time insight into thermal effectiveness, fouling progression rates, and estimated remaining service intervals based on actual operating conditions rather than scheduled maintenance cycles. Similarly, Kelvion Holdings GmbH's digital service solutions integrate remote performance monitoring capabilities that allow maintenance teams to track heat exchanger condition across multiple plant sites, prioritize interventions based on actual thermal degradation data, and schedule cleaning during planned production shutdowns rather than responding to unexpected equipment failures.

GEA Group AG has similarly developed digital heat exchanger monitoring tools for the food and dairy processing sector, where predictive fouling detection directly supports compliance with sanitation interval requirements and helps operators minimize unnecessary cleaning-in-place cycles that consume water, cleaning chemicals, and production time. The business case for connected heat exchanger management platforms is particularly compelling for large industrial operators managing fleets of heat exchangers across refinery, chemical plant, or food processing facility environments, where the cumulative impact of fouling-driven energy losses, unplanned downtime, and accelerated equipment wear represents a significant and quantifiable operational cost reduction opportunity. This trend is accelerating the transition from transactional heat exchanger procurement toward longer-term asset management and performance-based service relationships that generate predictable aftermarket revenue for system manufacturers.

By Product Type: In 2026, the Shell and Tube Heat Exchangers Segment to Dominate the Global Industrial Heat Exchanger Market

Based on product type, the industrial heat exchanger market is segmented into shell and tube heat exchangers, plate heat exchangers, air cooled heat exchangers, spiral heat exchangers, double pipe heat exchangers, and other heat exchangers. In 2026, the shell and tube heat exchangers segment is expected to account for the largest share of this market. The leading position of this segment is attributed to the proven suitability of shell and tube technology for the most demanding industrial thermal management requirements, including high-pressure crude oil and hydrocarbon stream processing in petroleum refining, high-temperature process fluid heating and cooling in chemical and petrochemical manufacturing, and steam generation and condensation in power generation and industrial utility systems. Pulse-jet pulse-cleaned and fixed-tubesheet shell and tube configurations are capable of handling a wider range of pressures, temperatures, and corrosive process media than any other heat exchanger product type, making them the default technology selection for large-scale industrial plant applications where reliability and operational resilience under extreme process conditions take precedence over thermal compactness. Koch Heat Transfer Company's TWISTED TUBE technology and API Heat Transfer's product portfolio exemplify the continued product development investment sustaining this segment's competitive relevance in oil and gas and chemical processing applications.

However, the plate heat exchangers segment is projected to register the highest growth during the forecast period. The high growth of this segment is driven by the accelerating displacement of shell and tube configurations in new small and mid-size industrial installation projects, the growing adoption of fully welded and brazed plate designs that have extended plate heat exchanger operating envelopes into higher-pressure and higher-temperature applications previously reserved for shell and tube technology, and the favourable total cost of ownership profile of plate designs in applications where their significantly smaller footprint, lower material requirement, and easier mechanical cleaning translate into meaningful capital and operational cost advantages.

By Material: In 2026, the Carbon Steel Segment to Hold the Largest Share

Based on material, the industrial heat exchanger market is segmented into carbon steel, stainless steel, titanium, nickel and high-performance alloys, copper and copper alloys, and other materials. In 2026, the carbon steel segment is expected to account for the largest share of this market. The growth of this segment is driven by the broad applicability of carbon steel construction in large-scale shell and tube heat exchanger installations across oil and gas refining, power generation, and chemical processing applications where process fluid corrosivity is managed through chemical treatment, protective coatings, or sacrificial corrosion allowances rather than inherent material resistance. Carbon steel heat exchangers deliver a structurally robust and cost-effective solution across the majority of moderate-temperature and moderate-pressure industrial applications, and their lower material cost relative to stainless steel, titanium, and high-performance alloy alternatives makes them the default construction choice for the capital cost-sensitive procurement environments characteristic of large-scale refinery and power plant projects.

However, the stainless steel segment is projected to register the highest growth during the forecast period. The high growth of this segment is driven by mandatory hygienic construction requirements embedded in food safety regulations including the U.S. Food Safety Modernization Act, the European Hygienic Engineering and Design Group standards, and 3-A Sanitary Standards that specify stainless steel as the required material of construction for heat transfer surfaces in direct product contact across food, beverage, and dairy processing applications. The parallel growth of pharmaceutical manufacturing under FDA current good manufacturing practice and European Medicines Agency guidelines, which mandate corrosion-resistant and cleanable material surfaces in all product-contact equipment, is similarly reinforcing stainless steel adoption. The increasing presence of chloride-bearing and wet sour service conditions in oil and gas applications involving produced water and acid gas streams is additionally driving incremental adoption of duplex and super duplex stainless steel heat exchanger tube bundles and plates across upstream and midstream processing environments.

By End-use Industry: In 2026, the Oil and Gas Segment to Hold the Largest Share

Based on end-use industry, the industrial heat exchanger market is segmented into oil and gas, chemical and petrochemical, power generation, food and beverage processing, pharmaceutical and biotechnology, HVAC and district energy, pulp and paper, metals and mining, and other end-use industries. In 2026, the oil and gas segment is expected to account for the largest share of this market, reflecting the status of this sector as the most thermally intensive and heat exchanger-dense industrial category globally. Petroleum refining operations require large networks of heat exchangers across crude preheat trains, fractionating column overhead condensers and reboilers, product coolers, and amine treating and sour water processing units, with a typical large refinery incorporating several hundred individual heat exchanger units across its process units. The upstream and midstream sectors similarly require heat exchangers for produced water handling, gas compression cooling, glycol regeneration, and liquefied natural gas processing operations. The ongoing expansion of liquefied natural gas export capacity in the United States, Qatar, and Australia, alongside the continued growth of refining and natural gas processing capacity in the Middle East and Asia Pacific, is sustaining strong capital investment in oil and gas heat exchanger systems globally.

However, the chemical and petrochemical segment is projected to register the highest growth during the forecast period. The high growth of this segment is driven by the accelerating buildout of chemical manufacturing capacity in Asia Pacific and the Middle East, where large-scale petrochemical complexes integrating steam crackers, aromatics units, and derivative chemical production facilities are creating substantial heat exchanger demand across a broad range of process fluid temperatures, pressures, and corrosivity profiles. The growing production of specialty chemicals, polymer intermediates, and electronic chemicals in South Korea, China, Taiwan, and Singapore is additionally generating demand for high-performance plate and welded heat exchanger systems capable of meeting the precise temperature control and high-purity fluid handling requirements characteristic of specialty chemical manufacturing processes. The increasing adoption of heat integration methodologies in new chemical plant design, driven by both energy cost considerations and carbon emission reduction obligations, is expanding per-unit heat exchanger content in newly commissioned chemical facilities relative to older plant designs.

Based on geography, the overall industrial heat exchanger market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. In 2026, North America is expected to account for the largest share of this market. This growth is driven by the presence of the world's largest integrated refining and petrochemical manufacturing complex along the U.S. Gulf Coast, which encompasses over 130 petroleum refineries and a dense concentration of chemical and polymer production facilities that collectively represent one of the largest installed bases of industrial heat exchanger equipment globally. The large volume of aging heat exchanger infrastructure across North American refinery, chemical plant, and power generation assets — a significant portion of which was installed prior to 2000 and is approaching or exceeding design service life — is creating a substantial capital reinvestment cycle driven by equipment replacement, process efficiency improvement, and emissions compliance requirements. The presence of leading heat exchanger manufacturers and engineering firms including Koch Heat Transfer Company, LP, API Heat Transfer Inc., and Holtec International, Inc., combined with a mature industrial maintenance and repair services infrastructure, reinforces the depth of the North American market.

However, the Asia Pacific industrial heat exchanger market is expected to grow at the fastest rate from 2026 to 2036. The rapid growth of this market is driven by the massive expansion of refining, chemical, power generation, and food processing capacity across China, India, South Korea, Japan, and Southeast Asia. China's continued buildout of large-scale petrochemical and coal-to-chemicals facilities, alongside its ongoing investments in power generation and district heating infrastructure, is generating sustained capital investment in heat exchanger systems across an increasingly diverse range of industrial process applications. India's rapidly expanding refining capacity — with the Petroleum Planning and Analysis Cell reporting refinery capacity additions across multiple projects — alongside the growth of pharmaceutical and specialty chemical manufacturing, is creating a structurally expanding demand base for both standardized and application-specific heat exchanger systems. The rapid development of industrial manufacturing capacity across Vietnam, Indonesia, Thailand, and Malaysia, driven by supply chain diversification investment flows from global manufacturers, is additionally broadening the Asia Pacific heat exchanger market beyond its historical concentration in China, Japan, and South Korea.

Europe represents a large and well-established market for industrial heat exchangers, supported by a comprehensive regulatory framework that includes the Industrial Emissions Directive, the revised Energy Efficiency Directive, and a range of sector-specific process safety and pressure equipment standards including the Pressure Equipment Directive (PED 2014/68/EU) that collectively drive both compliance-led equipment investment and technology quality standards. European manufacturers including Alfa Laval AB, Kelvion Holdings GmbH, GEA Group AG, Funke Wärmeaustauscher Apparatebau GmbH, and HRS Heat Exchangers Ltd. maintain strong market positions in their home region, supported by deep application engineering expertise across European refining, chemical, food, and pharmaceutical industrial sectors and close integration with the region's engineering, procurement, and construction contractor community.

The Middle East and Africa region represents a growing market for industrial heat exchangers, driven primarily by the continued expansion of oil and gas production, refining, and petrochemical manufacturing capacity across Saudi Arabia, the United Arab Emirates, Qatar, Kuwait, and Iraq, where national energy companies and their international partners are investing in large-scale hydrocarbon processing projects that incorporate significant heat exchanger requirements. The Latin America market is supported primarily by the oil and gas and mining sectors in Brazil, Mexico, and Colombia, alongside growing food and beverage processing manufacturing capacity across the region.

The global industrial heat exchanger market is moderately consolidated, with competition primarily driven by thermal efficiency, material and fabrication quality, application engineering expertise, geographic service capabilities, and the strength of aftermarket maintenance and parts offerings. Key differentiators among leading manufacturers include the breadth of product portfolios covering multiple heat exchanger technologies and construction materials, the availability of pressure equipment certified designs compliant with ASME, EN, and PED standards across global markets, the level of application-specific engineering support provided to customers in oil and gas, chemical, and food processing industries, and the scale and reach of global service and spare parts networks.

Large diversified heat exchanger manufacturers such as Alfa Laval AB and GEA Group AG compete through comprehensive product portfolios covering plate, shell and tube, and air cooled technologies, extensive global sales and service networks, and strong aftermarket parts and cleaning services businesses that generate recurring revenue alongside capital equipment sales. Specialty manufacturers including Kelvion Holdings GmbH and Tranter, Inc. compete through superior plate heat exchanger technology and deep application expertise in chemical, HVAC, and oil and gas markets. Brazed plate heat exchanger specialists including SWEP International AB, operating as a subsidiary of Dover Corporation, and Danfoss A/S maintain strong positions in HVAC, district energy, and refrigeration applications through focused product development and a broad global distribution network. Regionally focused manufacturers including Funke Wärmeaustauscher Apparatebau GmbH and HRS Heat Exchangers Ltd. maintain competitive positions in European markets through customized engineering capabilities and deep sector expertise, while BORSIG GmbH and Holtec International, Inc. compete effectively in large-scale chemical and nuclear power generation heat exchanger applications respectively.

The report provides a comprehensive competitive analysis based on an assessment of key players' product portfolios, geographic presence, and strategic initiatives undertaken over the past few years.

Some of the key players operating in the global industrial heat exchanger market include Alfa Laval AB (Sweden), Kelvion Holdings GmbH (Germany), GEA Group AG (Germany), Chart Industries, Inc. (U.S.), Danfoss A/S (Denmark), SWEP International AB (Sweden), Tranter, Inc. (U.S.), API Heat Transfer Inc. (U.S.), Koch Heat Transfer Company, LP (U.S.), Funke Wärmeaustauscher Apparatebau GmbH (Germany), HRS Heat Exchangers Ltd. (U.K.), BORSIG GmbH (Germany), Holtec International, Inc. (U.S.), Enerquip, LLC (U.S.), and Brask Inc. (U.S.), among others.

The global industrial heat exchanger market is expected to reach USD 31.1 billion by 2036 from an estimated USD 18.6 billion in 2026, at a CAGR of 5.2% during the forecast period 2026–2036.

In 2026, the shell and tube heat exchangers segment is expected to hold the largest share of this market, driven by its established suitability for high-pressure, high-temperature industrial applications in oil and gas refining, chemical processing, and power generation sectors.

The plate heat exchangers segment is expected to register the highest CAGR during the forecast period 2026–2036, driven by the accelerating displacement of shell and tube configurations in new installations, growing adoption of fully welded and brazed plate designs in high-pressure applications, and the favourable total cost of ownership profile of plate designs in food, pharmaceutical, and chemical manufacturing environments.

In 2026, the carbon steel segment is expected to hold the largest share of this market, reflecting its dominant position in large-scale oil and gas, power generation, and chemical processing heat exchanger applications where moderate-corrosivity service conditions allow cost-effective carbon steel construction.

In 2026, the oil and gas segment is expected to hold the largest share of this market, reflecting the dominant heat exchanger intensity of petroleum refining, upstream production, and midstream gas processing operations and the large installed base of heat exchanger assets across global oil and gas infrastructure.

North America is expected to account for the largest share of the global industrial heat exchanger market in 2026, driven by the presence of the world's largest refining and petrochemical complex, a large installed base of aging heat exchanger infrastructure requiring replacement and upgrade, and the most actively enforced industrial energy efficiency regulatory environment.

The growth of this market is primarily driven by the tightening of industrial energy efficiency regulations globally, including the EU Energy Efficiency Directive, U.S. DOE industrial efficiency programs supported by Inflation Reduction Act funding, and China's and India's energy conservation mandates; rapid industrial capacity expansion in Asia Pacific and the Middle East; the ongoing displacement of shell and tube configurations by advanced compact plate heat exchanger designs in new installations; the growing adoption of IoT-enabled performance monitoring platforms; and sustained capital investment in pharmaceutical, food processing, and specialty chemical manufacturing infrastructure.

Key players in the global industrial heat exchanger market include Alfa Laval AB (Sweden), Kelvion Holdings GmbH (Germany), GEA Group AG (Germany), Chart Industries, Inc. (U.S.), Danfoss A/S (Denmark), SWEP International AB (Sweden), Tranter, Inc. (U.S.), API Heat Transfer Inc. (U.S.), Koch Heat Transfer Company, LP (U.S.), Funke Wärmeaustauscher Apparatebau GmbH (Germany), HRS Heat Exchangers Ltd. (U.K.), BORSIG GmbH (Germany), Holtec International, Inc. (U.S.), Enerquip, LLC (U.S.), and Brask Inc. (U.S.).

Asia Pacific is expected to register the highest growth rate in the global industrial heat exchanger market during the forecast period 2026–2036, driven by accelerating industrial capacity expansion in refining, chemical, power generation, pharmaceutical, and food processing sectors across China, India, South Korea, Japan, and Southeast Asia, alongside tightening industrial energy efficiency and air quality regulations that are compelling widespread heat exchanger system investment across the region.

Published Date: Oct-2025

Published Date: Sep-2025

Published Date: Jul-2025

Published Date: Jul-2025

Published Date: May-2025

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates