Resources

About Us

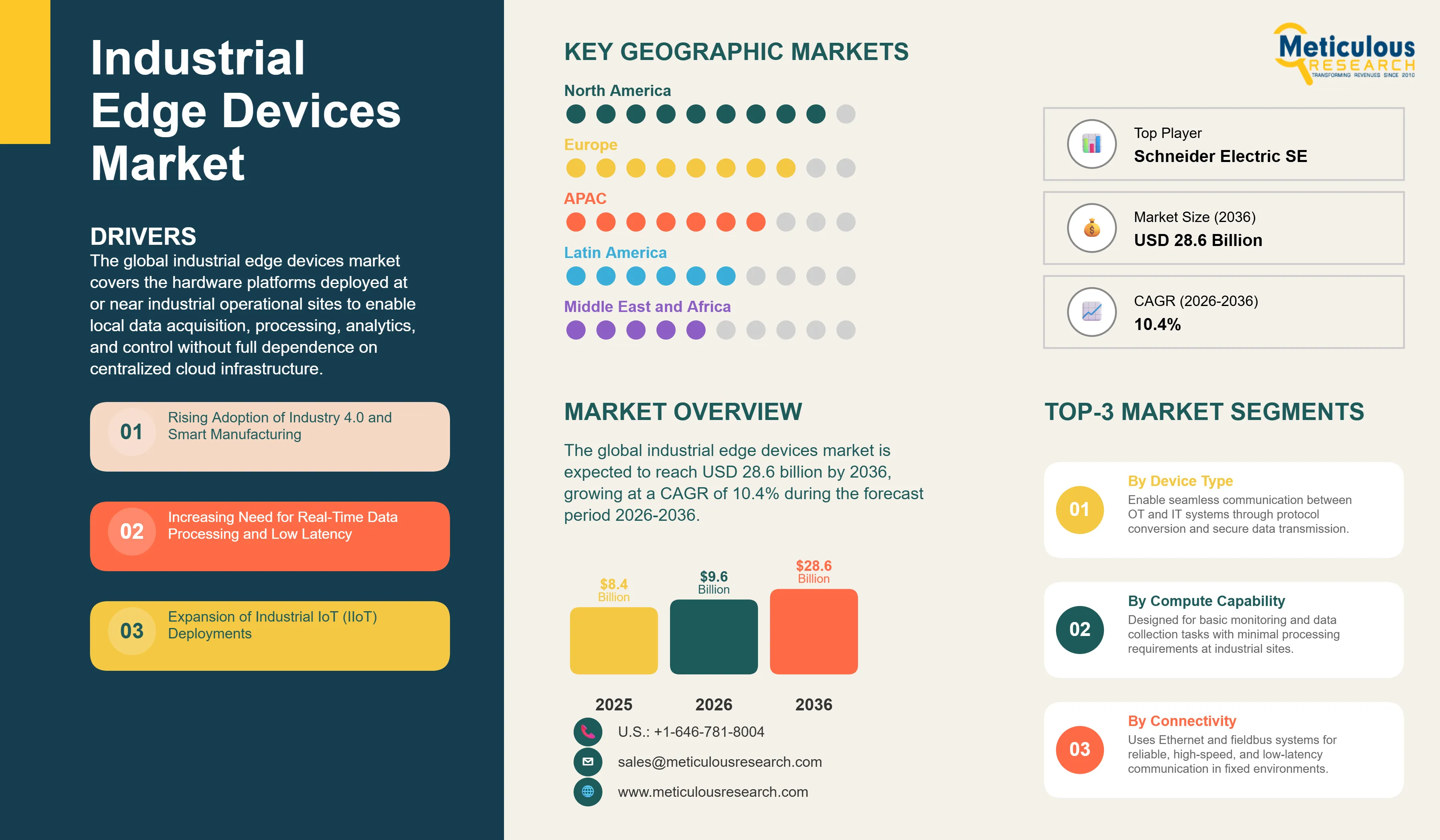

The global industrial edge devices market was valued at USD 8.4 billion in 2025. This market is expected to reach USD 28.6 billion by 2036 from an estimated USD 9.6 billion in 2026, growing at a CAGR of 10.4% during the forecast period 2026-2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global industrial edge devices market covers the hardware platforms deployed at or near industrial operational sites to enable local data acquisition, processing, analytics, and control without full dependence on centralized cloud infrastructure. The market encompasses edge gateways that bridge operational technology and information technology networks, edge controllers including programmable logic controllers and programmable automation controllers, industrial edge computers and rugged servers, smart sensors and data acquisition systems, and edge AI devices including AI accelerators and vision processing units. These devices collectively serve manufacturing, energy, oil and gas, transportation, healthcare, and warehouse automation applications where low-latency decision-making, network resilience, and data sovereignty requirements make on-premises edge compute essential.

The market's growth is anchored in the accelerating adoption of Industry 4.0 frameworks across global manufacturing, with industrial enterprises investing in edge devices as the foundational data layer for predictive maintenance, quality inspection, autonomous robotics, and real-time process optimization. The convergence of edge compute with embedded AI inference capabilities is transforming edge devices from passive data collectors to active intelligence nodes capable of executing machine learning models locally, enabling applications such as computer vision-based defect detection, anomaly detection in rotating machinery, and automated process control that require sub-millisecond response times incompatible with cloud-round-trip latency.

Despite strong growth fundamentals, the market faces structural constraints. High upfront capital expenditure for edge device deployment, particularly for large-scale IIoT rollouts across distributed industrial sites, limits adoption velocity among cost-sensitive manufacturers and small to medium enterprises. Integration of new edge devices with decades-old operational technology infrastructure, including legacy programmable logic controllers, SCADA systems, and proprietary industrial communication protocols, requires significant engineering effort and system integration expertise that prolongs deployment timelines and increases total cost of ownership.

These constraints are progressively being addressed. Standardization around open protocols including OPC UA over TSN, MQTT, and containerized edge software frameworks such as AWS Greengrass, Azure IoT Edge, and Linux Foundation's LF Edge is reducing interoperability friction. The growing availability of managed edge-as-a-service offerings from Siemens, Rockwell Automation, and Schneider Electric is lowering the operational burden on industrial customers without deep edge compute expertise, making broader deployment economically viable across the SME segment for the first time.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 28.6 Billion |

|

Market Size in 2026 |

USD 9.6 Billion |

|

Market Size in 2025 |

USD 8.4 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 10.4% |

|

Dominating Device Type |

Edge Gateways |

|

Fastest Growing Device Type |

Edge AI Devices |

|

Dominating Compute Capability |

Medium-Compute Devices |

|

Fastest Growing Compute Capability |

High-Compute Devices (AI/ML) |

|

Dominating Connectivity |

Wired Connectivity (Ethernet, Fieldbus) |

|

Fastest Growing Connectivity |

Cellular Connectivity (4G, 5G) |

|

Dominating Deployment Mode |

On-Premises Edge Deployment |

|

Fastest Growing Deployment Mode |

Hybrid Edge-Cloud Deployment |

|

Dominating Application |

Manufacturing and Smart Factories |

|

Fastest Growing Application |

Transportation and Logistics |

|

Dominating End User |

Large Enterprises |

|

Fastest Growing End User |

Small and Medium Enterprises (SMEs) |

|

Dominating Industry Vertical |

Automotive |

|

Fastest Growing Industry Vertical |

Pharmaceuticals |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Rising Adoption of Industry 4.0 and Smart Manufacturing

The global rollout of Industry 4.0 frameworks across discrete and process manufacturing is the primary structural driver of industrial edge device demand. Smart factory initiatives at automotive OEMs, electronics manufacturers, and heavy industry operators require a dense network of edge devices to collect, process, and act on production data in real time. Siemens' Industrial Metaverse program, Rockwell Automation's Connected Enterprise, and Schneider Electric's EcoStruxure architecture all position edge devices as the essential on-premises infrastructure layer enabling digital twin synchronization, closed-loop quality control, and autonomous production scheduling. Government manufacturing competitiveness programs including Germany's Platform Industrie 4.0, China's Made in China 2025, and the U.S. Department of Energy's Manufacturing USA network are co-funding smart factory deployments that directly drive industrial edge hardware procurement across their respective national manufacturing bases.

Industrial applications including robotic motion control, machine vision quality inspection, process safety interlocks, and autonomous guided vehicle navigation require deterministic response times of less than one millisecond that cannot be achieved through cloud-dependent architectures. Edge devices process sensor and machine data locally at the point of generation, enabling control loop response within the microsecond to millisecond range required for these applications without network round-trip delay. The deployment of time-sensitive networking standards including IEEE 802.1 TSN across industrial Ethernet infrastructure is enabling edge devices to guarantee deterministic latency across multi-node industrial networks, supporting synchronized multi-axis motion control and real-time safety system applications that previously required proprietary fieldbus architectures.

Expansion of Edge AI and Machine Learning

The integration of dedicated AI inference accelerator hardware, including NVIDIA Jetson compute modules, Intel Movidius VPUs, and Qualcomm AI 100 edge processors, into industrial edge devices is creating a substantial new market tier of high-compute edge AI devices that can execute convolutional neural networks, transformer models, and anomaly detection algorithms locally on the factory floor. Edge AI enables applications including visual defect inspection at production line speeds, predictive failure detection from vibration and thermal sensor data, and natural language process command interfaces for industrial equipment that require machine learning inference at latencies incompatible with cloud processing. The addressable market for edge AI devices in manufacturing, energy, and logistics is projected to expand significantly as AI model deployment at the edge transitions from pilot projects to production-scale rollouts through the forecast period.

Growth in 5G-Enabled Industrial Applications

The deployment of private 5G networks at industrial facilities by automotive manufacturers, port operators, and mining companies is creating demand for 5G-connected industrial edge devices that combine cellular connectivity with local compute for mobile robotics, autonomous vehicle guidance, and distributed sensor networks that cannot be served by fixed wired infrastructure. Private 5G networks offer deterministic sub-10 millisecond latency, high device density support exceeding one million connections per square kilometer, and network slicing capabilities that allow industrial applications to reserve guaranteed bandwidth separate from general enterprise traffic. Siemens, Ericsson, and Nokia are jointly deploying private 5G and industrial edge compute infrastructure at automotive and manufacturing facilities, with the edge device serving as the compute and control node that processes 5G sensor and camera feeds locally before transmitting aggregated results to enterprise systems.

Convergence of Edge Compute and AI Inference at the Device Level

The progressive integration of dedicated AI inference silicon directly into industrial edge devices is transforming the competitive landscape, as vendors including Siemens, Advantech, and Rockwell Automation embed NVIDIA, Intel, and custom AI processors into gateway and controller form factors. Edge AI devices are displacing previous generations of cloud-dependent analytics by enabling model inference at the point of data generation, reducing bandwidth costs and enabling real-time closed-loop control based on AI-derived insights. The growing catalog of pre-trained industrial AI models for predictive maintenance, quality inspection, and energy optimization that can be deployed to standard edge hardware through containerized software frameworks is accelerating edge AI adoption beyond early adopter manufacturers.

Migration from Proprietary to Open and Interoperable Edge Architectures

Industrial customers are increasingly demanding edge devices built on open hardware and software standards that reduce vendor lock-in and simplify integration across multi-vendor operational technology environments. The adoption of OPC UA over TSN as the dominant industrial communication standard, Linux-based operating systems on edge controllers, and container-based software deployment through Kubernetes and Docker across edge compute nodes is enabling customers to select best-of-breed hardware and software components independently. Established industrial automation vendors including Siemens, Schneider Electric, and ABB are adapting their edge device portfolios to support open interfaces while defending differentiation through application software, domain expertise, and support service ecosystems.

Rapid Growth of Edge-as-a-Service Consumption Models

The availability of industrial edge infrastructure on managed service and subscription models from major technology and industrial automation vendors is expanding edge device adoption into SME manufacturers that cannot justify large upfront capital expenditure for edge hardware. Dell Technologies' APEX for Manufacturing, HPE GreenLake for edge, and Siemens' SieEdge managed service offerings allow customers to consume edge compute capacity as an operational expense with vendor-managed hardware lifecycle, software updates, and security patching. This shift reduces the barrier to entry for mid-market industrial IoT deployments and is expected to accelerate SME segment growth significantly through the forecast period.

Increasing Focus on Edge Cybersecurity and Zero-Trust Architectures

The proliferation of internet-connected industrial edge devices at operational technology network boundaries is elevating cybersecurity from an afterthought to a primary design criterion for edge device procurement. Industrial buyers are increasingly requiring edge devices with hardware-rooted trust, secure boot, encrypted storage, and built-in network segmentation capabilities aligned with IEC 62443 industrial cybersecurity standards and NIST SP 800-82 guidelines for industrial control system security. Vendors including Cisco, Fortinet, and Palo Alto Networks are developing industrial-grade edge security appliances that combine connectivity gateway functions with next-generation firewall and zero-trust network access capabilities purpose-built for operational technology environments.

Sustainability and Energy Efficiency Requirements Driving Edge Hardware Innovation

The tightening energy efficiency mandates applied to industrial facilities under EU taxonomy regulations, the U.S. Department of Energy's industrial efficiency programs, and corporate net-zero manufacturing commitments are creating demand for edge devices with lower power consumption, thermal management optimization, and energy-aware compute scheduling capabilities. Edge device vendors are responding with silicon architectures optimized for performance per watt, power gating and sleep state management for intermittently active sensor nodes, and software-defined power management frameworks that allow edge compute resources to be dynamically scaled to match workload demand, reducing idle power consumption at facilities with variable production schedules.

By Device Type: In 2026, Edge Gateways to Dominate

Based on device type, the global industrial edge devices market is segmented into edge gateways, edge controllers, industrial edge computers, edge sensors and data acquisition devices, edge AI devices, and other industrial edge devices. In 2026, the edge gateways segment is expected to account for the largest share of the market. Edge gateways serve as the universal connectivity and protocol translation layer bridging operational technology equipment using legacy industrial protocols including Modbus, PROFIBUS, EtherNet/IP, and HART with IP-based enterprise and cloud networks. Their role as the entry point for IIoT connectivity deployments across installed base manufacturing equipment makes them the most broadly deployed industrial edge device category, with near-universal adoption across greenfield and brownfield industrial IoT projects. Leading gateway suppliers including Advantech, Moxa, Cisco, and Siemens serve millions of installed units across automotive, process industry, and utility sector deployments.

Edge AI devices is projected to register the highest CAGR during the forecast period. The deployment of AI inference accelerator hardware for visual inspection, predictive maintenance, and autonomous guidance applications is expanding the edge AI device market rapidly as AI model development tools, pre-trained industrial model libraries, and edge AI deployment frameworks mature, reducing the development burden for industrial customers deploying AI at the edge for the first time.

By Compute Capability: In 2026, Medium-Compute Devices to Hold the Largest Share

Based on compute capability, the global industrial edge devices market is segmented into low-compute devices, medium-compute devices, and high-compute devices. In 2026, the medium-compute devices segment is expected to account for the largest share, reflecting the broad deployment of edge gateways and industrial PCs capable of real-time data processing, protocol translation, and lightweight analytics across the majority of industrial IoT applications that do not require dedicated AI inference silicon. Medium-compute platforms from Advantech, Kontron, and Beckhoff address the mainstream industrial computing market with sufficient processing capability for most data aggregation, visualization, and condition monitoring applications.

High-compute devices (AI/ML processing) is projected to register the highest CAGR, driven by the structural adoption of edge AI inference for machine vision, predictive analytics, and autonomous control applications that require GPU, VPU, or custom AI accelerator processing capability not available in conventional embedded industrial compute platforms.

By Connectivity: In 2026, Wired Connectivity to Hold the Largest Share

Based on connectivity, the global industrial edge devices market is segmented into wired connectivity (Ethernet, Fieldbus), wireless connectivity (Wi-Fi, Bluetooth), cellular connectivity (4G, 5G), and LPWAN technologies. In 2026, the wired connectivity segment is expected to account for the largest share, reflecting the dominance of Industrial Ethernet including PROFINET, EtherNet/IP, and EtherCAT as the primary connectivity standard for deterministic, high-bandwidth machine control and data acquisition in fixed industrial plant environments where wired infrastructure provides reliability, latency, and bandwidth advantages over wireless alternatives.

Cellular connectivity (4G, 5G) is projected to register the highest CAGR, driven by the deployment of private 5G networks at automotive, mining, and port facilities enabling mobile industrial edge applications including autonomous guided vehicles, remote-operated equipment, and distributed sensor networks that require cellular connectivity to serve mobile or geographically dispersed asset monitoring applications.

By Deployment Mode: In 2026, On-Premises Edge Deployment to Hold the Largest Share

Based on deployment mode, the global industrial edge devices market is segmented into on-premises edge deployment, hybrid edge-cloud deployment, and cloud-integrated edge. In 2026, the on-premises deployment segment is expected to account for the largest share, driven by industrial customers' operational continuity requirements, data sovereignty regulations, and the latency-critical nature of real-time process control applications that mandate local processing independent of internet connectivity availability. Process industries including oil and gas, chemicals, and power generation favor pure on-premises edge architectures for safety-critical control loop applications.

Hybrid edge-cloud deployment is projected to register the highest CAGR as cloud-connected edge architectures mature, enabling customers to run time-critical control and safety applications locally while offloading historical data storage, advanced analytics, digital twin synchronization, and fleet-level predictive maintenance model training to cloud platforms, achieving the operational benefits of both local and cloud computing within a unified architecture.

By Application: In 2026, Manufacturing and Smart Factories to Hold the Largest Share

Based on application, the global industrial edge devices market is segmented into manufacturing and smart factories, energy and utilities, oil and gas, transportation and logistics, healthcare, retail and warehousing, and others. In 2026, the manufacturing and smart factories segment is expected to account for the largest share of the market. Manufacturing represents the broadest and most mature deployment domain for industrial edge devices, encompassing discrete manufacturing for automotive, electronics, and aerospace as well as process manufacturing for chemicals, food and beverage, and pharmaceuticals. The density of edge device deployments per factory floor, combined with the large global installed base of manufacturing facilities undergoing smart factory transformation, makes manufacturing the dominant application segment by both device unit volume and revenue value.

Transportation and logistics is projected to register the highest CAGR during the forecast period, driven by the deployment of edge intelligence for autonomous port operations, smart railway infrastructure, connected vehicle telematics, and warehouse automation including autonomous mobile robot fleets that require real-time edge compute at distributed logistics nodes.

By End User: In 2026, Large Enterprises to Hold the Largest Share

Based on end user, the global industrial edge devices market is segmented into large enterprises and small and medium enterprises. In 2026, the large enterprises segment is expected to account for the largest share of the market, reflecting the concentration of industrial edge device procurement at global manufacturers, utilities, and oil and gas majors with the capital budgets, IT/OT integration teams, and organizational scale required to deploy edge infrastructure across multi-site production networks. Large enterprises including Toyota, BASF, Siemens Energy, and BP are deploying edge compute at hundreds to thousands of facilities simultaneously, generating procurement volumes that dominate market revenue.

The SME segment is projected to register the highest CAGR during the forecast period, driven by the proliferation of affordable, simplified edge device platforms and managed service consumption models that are progressively making industrial edge compute accessible to smaller manufacturers previously priced out of enterprise-grade edge infrastructure.

By Industry Vertical: In 2026, Automotive to Hold the Largest Share

Based on industry vertical, the global industrial edge devices market is segmented into automotive, electronics and semiconductor, food and beverage, pharmaceuticals, mining and metals, chemicals, and others. In 2026, the automotive segment is expected to account for the largest share of the market. Automotive manufacturing plants deploy some of the highest densities of industrial edge devices globally, spanning programmable logic controllers for robotic welding and assembly lines, edge vision systems for quality inspection, edge compute nodes for autonomous guided vehicle fleets, and private 5G gateways for mobile manufacturing applications. The automotive industry's advanced Industry 4.0 adoption maturity and high capital investment capacity make it the dominant industry vertical by edge device deployment scale and spend. This segment is particularly important for demand mapping given its high edge device intensity per production facility and the ongoing retooling of automotive manufacturing for electric vehicle production.

Pharmaceuticals is projected to register the highest CAGR during the forecast period, driven by the pharmaceutical industry's accelerating adoption of digital manufacturing frameworks under the FDA's Pharma 4.0 initiative and the European Medicines Agency's digital manufacturing guidance, which require real-time process analytical technology data collection, continuous process verification, and electronic batch record systems that depend on industrial edge infrastructure for low-latency data acquisition and process control at manufacturing critical quality attributes.

Industrial Edge Devices Market by Region: North America Leading by Share, Asia-Pacific by Growth

Based on geography, the global industrial edge devices market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

In 2026, North America is expected to account for the largest share of the global industrial edge devices market. The region's dominance reflects the concentration of leading industrial automation technology vendors, the advanced Industry 4.0 adoption maturity of U.S. and Canadian manufacturing, and the significant federal investment in industrial digitalization through the Department of Energy's Manufacturing USA institutes and the Department of Commerce's CHIPS Act-linked smart manufacturing programs. The United States hosts the largest installed base of connected industrial facilities outside of East Asia, with automotive, aerospace, oil and gas, and food and beverage manufacturers deploying edge infrastructure across hundreds of thousands of production sites. The presence of dominant market participants including Rockwell Automation, Cisco, Dell, HPE, Intel, Honeywell, and Emerson Electric in the United States creates a structurally strong domestic supply and systems integration ecosystem that accelerates enterprise edge adoption relative to other regions.

Europe represents the second largest regional market, anchored by Germany's world-leading industrial automation heritage and its structural position as the global center of Industry 4.0 technology development. German manufacturing conglomerates including Siemens, Bosch Rexroth, and Festo are among the most advanced adopters and developers of industrial edge infrastructure globally, and their supply to European and global customers creates substantial domestic market activity. The EU's European Green Deal industrial digitalization programs, the European Chips Act supporting domestic semiconductor and edge hardware manufacturing, and the strong manufacturing bases of Germany, France, Italy, the Netherlands, and Sweden collectively make Europe a high-value market for premium edge device solutions with strong regulatory compliance and cybersecurity requirements under the EU Cyber Resilience Act applicable to industrial connected devices from 2027.

However, Asia-Pacific is expected to grow at the fastest CAGR during the forecast period. China's enormous manufacturing base undergoing continuous smart factory transformation under national industrial policy programs, Japan's strong industrial automation culture and the domestic edge device ecosystem centered on Mitsubishi Electric, Yokogawa, and Keyence, South Korea's advanced electronics and automotive manufacturing sectors, and India's rapidly expanding manufacturing investment under the Production Linked Incentive scheme collectively create the region's dominant growth dynamic. The concentration of global electronics manufacturing in China, South Korea, Taiwan, and increasingly Vietnam and Thailand is driving high-volume edge device deployments for machine vision, quality control, and automated material handling applications that are expanding the Asia-Pacific addressable market at above-global-average growth rates through the forecast period.

The global industrial edge devices market features a competitive ecosystem spanning established industrial automation conglomerates with broad edge device portfolios, technology infrastructure companies extending enterprise compute platforms into industrial environments, and specialized edge hardware vendors serving specific industrial application segments. Competition is structured across device categories, with industrial automation incumbents competing primarily on operational technology domain expertise, protocol breadth, and system integration capability while technology platform vendors compete on compute performance, cloud integration depth, and software ecosystem breadth.

Siemens AG leads the market with its SIMATIC industrial edge portfolio, encompassing edge gateways, industrial PCs, and the SINUMERIK edge platform for machine tool connectivity, backed by the MindSphere industrial IoT platform and Siemens' dominant position in European and Asian manufacturing automation. Rockwell Automation's Logix-based edge controllers and FactoryTalk Analytics Edge platform serve the North American discrete manufacturing market with strong integration across Allen-Bradley programmable logic controller installed bases. Schneider Electric's EcoStruxure Edge platforms serve energy, grid, and building automation applications with particular strength in utility and oil and gas sectors. Cisco provides industrial networking and edge compute infrastructure through its Catalyst Industrial Ethernet switches and IOx application hosting framework. Advantech is the leading purpose-built industrial edge computer vendor globally, with the broadest catalog of embedded edge computers, IoT gateways, and industrial PCs spanning a wide performance and price range. Dell Technologies and HPE serve the high-compute rugged edge server tier through their respective APEX and GreenLake edge platforms. Intel provides the underlying compute silicon for the majority of industrial edge devices through its Core, Xeon, and Atom processor families alongside the OpenVINO edge AI framework. ABB, Honeywell, Emerson, Mitsubishi Electric, Bosch Rexroth, and Yokogawa each serve their respective domain applications across process automation, discrete manufacturing, power, and oil and gas with integrated edge device and software platform offerings.

Key players operating in the global industrial edge devices market include Siemens AG (Germany), Rockwell Automation Inc. (U.S.), Schneider Electric SE (France), Cisco Systems Inc. (U.S.), Advantech Co. Ltd. (Taiwan), Dell Technologies Inc. (U.S.), Hewlett Packard Enterprise (U.S.), IBM Corporation (U.S.), Intel Corporation (U.S.), ABB Ltd. (Switzerland), Honeywell International Inc. (U.S.), Emerson Electric Co. (U.S.), Mitsubishi Electric Corporation (Japan), Bosch Rexroth AG (Germany), and Yokogawa Electric Corporation (Japan), among others.

The global industrial edge devices market is expected to reach USD 28.6 billion by 2036 from an estimated USD 9.6 billion in 2026, at a CAGR of 10.4% during the forecast period 2026-2036.

In 2026, the edge gateways segment is expected to hold the largest share, driven by universal adoption as the connectivity and protocol translation layer for industrial IoT deployments across both greenfield and brownfield manufacturing environments.

Edge AI devices is expected to register the highest CAGR during the forecast period 2026-2036, driven by the rapid deployment of AI inference hardware for machine vision, predictive maintenance, and autonomous guidance applications across manufacturing and logistics.

The automotive segment holds the largest share and is the most important for demand mapping due to its high edge device intensity per production facility, advanced Industry 4.0 adoption maturity, and ongoing retooling of global automotive manufacturing for electric vehicle production that is driving large-scale edge infrastructure refresh investment.

Cellular connectivity (4G, 5G) is expected to register the highest CAGR during the forecast period, driven by private 5G network deployments at automotive, mining, and port facilities enabling mobile industrial edge applications for autonomous guided vehicles, remote equipment monitoring, and distributed sensor networks across geographically dispersed assets.

Growth is primarily driven by the accelerating global adoption of Industry 4.0 and smart manufacturing frameworks, the real-time low-latency requirements of industrial control and AI inference applications that mandate on-premises edge processing, the integration of AI inference capability directly into edge device hardware, and the deployment of private 5G networks enabling new categories of mobile and distributed industrial applications that require cellular-connected edge compute.

Asia-Pacific is expected to register the highest growth rate during the forecast period 2026-2036, driven by China's large-scale smart manufacturing transformation, Japan's advanced industrial automation ecosystem, South Korea's electronics and automotive manufacturing digitalization, and India's rapidly expanding manufacturing investment under national production incentive programs.

Key players are Siemens AG (Germany), Rockwell Automation Inc. (U.S.), Schneider Electric SE (France), Cisco Systems Inc. (U.S.), Advantech Co. Ltd. (Taiwan), Dell Technologies Inc. (U.S.), Hewlett Packard Enterprise (U.S.), IBM Corporation (U.S.), Intel Corporation (U.S.), ABB Ltd. (Switzerland), Honeywell International Inc. (U.S.), Emerson Electric Co. (U.S.), Mitsubishi Electric Corporation (Japan), Bosch Rexroth AG (Germany), and Yokogawa Electric Corporation (Japan), among others.

1. Introduction

1.1 Market Definition

1.2 Market Ecosystem

1.3 Currency and Limitations

1.3.1 Currency

1.3.2 Limitations

1.4 Key Stakeholders

2. Research Methodology

2.1 Research Approach

2.2 Data Collection and Validation Process

2.2.1 Secondary Research

2.2.2 Primary Research and Validation

2.2.2.1 Primary Interviews with Experts

2.2.2.2 Approaches for Country/Region-Level Analysis

2.3 Market Estimation

2.3.1 Bottom-Up Approach

2.3.2 Top-Down Approach

2.3.3 Growth Forecast

2.4 Data Triangulation

2.5 Assumptions for the Study

3. Executive Summary

4. Market Overview

4.1 Introduction

4.2 Market Dynamics

4.2.1 Drivers

4.2.2 Restraints

4.2.3 Opportunities

4.2.4 Challenges

4.3 Technology Landscape

4.3.1 Edge Computing Platforms

4.3.2 Edge AI and Machine Learning

4.3.3 Industrial IoT Protocols (OPC UA, MQTT)

4.3.4 5G and Wireless Connectivity

4.3.5 Containerization and Edge Software Frameworks

4.4 Industrial Edge Architecture (Critical Segmentation)

4.4.1 Edge Devices (Sensors, Gateways, Controllers)

4.4.2 Edge Servers and Compute Nodes

4.4.3 Connectivity Infrastructure

4.4.4 Edge Software and Analytics Platforms

4.4.5 Cloud Integration

4.5 Value Chain Analysis

4.5.1 Component Suppliers (Processors, Sensors, Modules)

4.5.2 Device Manufacturers

4.5.3 Software and Platform Providers

4.5.4 System Integrators

4.5.5 End Users

4.6 Regulatory and Standards Landscape

4.6.1 Industrial Communication Standards

4.6.2 Data Security and Privacy Regulations

4.6.3 Industry-Specific Compliance Standards

4.7 Porter's Five Forces Analysis

4.8 Investment and Industry Trends

4.8.1 Industrial Digitalization Investments

4.8.2 Partnerships between OEMs and Tech Providers

4.8.3 Expansion of Edge AI Ecosystems

4.9 Cost and Pricing Analysis

4.9.1 Pricing by Device Type

4.9.2 Hardware vs Software Cost Split

4.9.3 Edge Deployment Cost Models

5. Industrial Edge Devices Market, by Device Type (Primary Segmentation)

5.1 Introduction

5.2 Edge Gateways

5.2.1 Protocol Conversion Gateways

5.2.2 IoT Gateways

5.2.3 Industrial Communication Gateways

5.3 Edge Controllers

5.3.1 Programmable Logic Controllers (PLCs)

5.3.2 Distributed Control Systems (DCS) Edge Nodes

5.3.3 Programmable Automation Controllers (PACs)

5.4 Industrial Edge Computers

5.4.1 Embedded Edge Computers

5.4.2 Industrial PCs (IPCs)

5.4.3 Rugged Edge Servers

5.5 Edge Sensors and Data Acquisition Devices

5.5.1 Smart Sensors

5.5.2 Data Acquisition Systems (DAQ)

5.6 Edge AI Devices

5.6.1 AI Accelerators

5.6.2 Vision Processing Units (VPUs)

5.7 Other Industrial Edge Devices

6. Industrial Edge Devices Market, by Compute Capability

6.1 Introduction

6.2 Low-Compute Devices (Basic Monitoring)

6.3 Medium-Compute Devices (Real-Time Processing)

6.4 High-Compute Devices (AI/ML Processing)

7. Industrial Edge Devices Market, by Connectivity

7.1 Introduction

7.2 Wired Connectivity (Ethernet, Fieldbus)

7.3 Wireless Connectivity (Wi-Fi, Bluetooth)

7.4 Cellular Connectivity (4G, 5G)

7.5 LPWAN Technologies

8. Industrial Edge Devices Market, by Deployment Mode

8.1 Introduction

8.2 On-Premises Edge Deployment

8.3 Hybrid Edge-Cloud Deployment

8.4 Cloud-Integrated Edge

9. Industrial Edge Devices Market, by Application

9.1 Introduction

9.2 Manufacturing and Smart Factories

9.3 Energy and Utilities

9.4 Oil and Gas

9.5 Transportation and Logistics

9.6 Healthcare

9.7 Retail and Warehousing

9.8 Others

10. Industrial Edge Devices Market, by End User

10.1 Introduction

10.2 Large Enterprises

10.3 Small and Medium Enterprises (SMEs)

11. Industrial Edge Devices Market, by Industry Vertical (Advanced Segmentation)

11.1 Introduction

11.2 Automotive

11.3 Electronics and Semiconductor

11.4 Food and Beverage

11.5 Pharmaceuticals

11.6 Mining and Metals

11.7 Chemicals

11.8 Others

12. Industrial Edge Devices Market, by Geography

12.1 Introduction

12.2 North America

12.2.1 U.S.

12.2.2 Canada

12.3 Europe

12.3.1 Germany

12.3.2 U.K.

12.3.3 France

12.3.4 Italy

12.3.5 Spain

12.3.6 Netherlands

12.3.7 Sweden

12.3.8 Switzerland

12.3.9 Rest of Europe

12.4 Asia-Pacific

12.4.1 China

12.4.2 Japan

12.4.3 India

12.4.4 South Korea

12.4.5 Australia

12.4.6 Singapore

12.4.7 Malaysia

12.4.8 Thailand

12.4.9 Indonesia

12.4.10 Vietnam

12.4.11 Rest of Asia-Pacific

12.5 Latin America

12.5.1 Brazil

12.5.2 Mexico

12.5.3 Argentina

12.5.4 Chile

12.5.5 Colombia

12.5.6 Rest of Latin America

12.6 Middle East and Africa

12.6.1 UAE

12.6.2 Saudi Arabia

12.6.3 South Africa

12.6.4 Turkey

12.6.5 Israel

12.6.6 Rest of Middle East and Africa

13. Competitive Landscape

13.1 Overview

13.2 Key Growth Strategies

13.3 Competitive Benchmarking

13.4 Competitive Dashboard

13.4.1 Industry Leaders

13.4.2 Market Differentiators

13.4.3 Vanguards

13.4.4 Emerging Companies

13.5 Market Ranking/Positioning Analysis of Key Players, 2025

14. Company Profiles

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

14.1 Siemens AG

14.2 Rockwell Automation, Inc.

14.3 Schneider Electric SE

14.4 Cisco Systems, Inc.

14.5 Advantech Co., Ltd.

14.6 Dell Technologies Inc.

14.7 Hewlett Packard Enterprise (HPE)

14.8 IBM Corporation

14.9 Intel Corporation

14.10 ABB Ltd.

14.11 Honeywell International Inc.

14.12 Emerson Electric Co.

14.13 Mitsubishi Electric Corporation

14.14 Bosch Rexroth AG

14.15 Yokogawa Electric Corporation

15. Appendix

15.1 Additional Customization

15.2 Related Reports

Published Date: Oct-2025

Published Date: Jul-2024

Published Date: Jul-2024

Published Date: Jan-2024

Subscribe to get the latest industry updates