Resources

About Us

Data Center Optical Fiber Market by Fiber Type, Connectivity Architecture, Deployment Environment, Application, End User (Cloud Service Providers, Colocation Providers, Enterprises)- Global Forecast to 2036

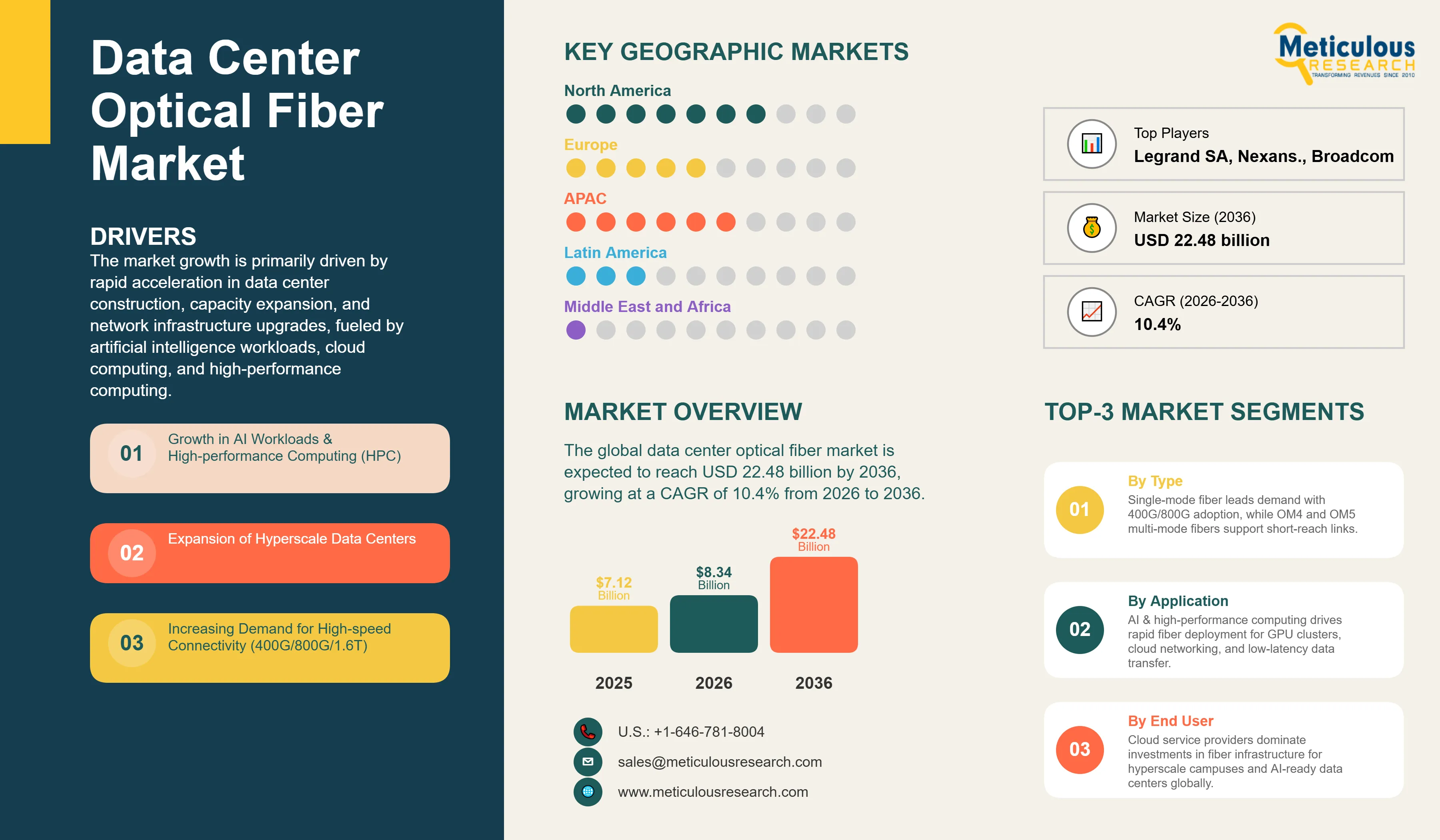

Report ID: MRICT - 1041992 Pages: 315 May-2026 Formats*: PDF Category: Information and Communications Technology Delivery: 24 to 72 Hours Download Free Sample ReportThe global data center optical fiber market was valued at USD 7.12 billion in 2025. This market is expected to reach USD 22.48 billion by 2036 from USD 8.34 billion in 2026, growing at a CAGR of 10.4% from 2026 to 2036.

The market growth is primarily driven by rapid acceleration in data center construction, capacity expansion, and network infrastructure upgrades, fueled by artificial intelligence workloads, cloud computing, and high-performance computing. According to the IEA's Energy and AI report published in April 2025, global data center electricity consumption has increased by approximately 12% annually since 2017, reaching about 415 terawatt-hours in 2024, representing roughly 1.5% of global electricity consumption. The IEA's April 2026 analysis confirmed that data center electricity demand rose by 17% in 2025, with AI-focused data centers expanding even more rapidly, increasing by 50% in the same year. The IEA projects that global data center electricity consumption will nearly double from 485 TWh in 2025 to 950 TWh by 2030, growing at an estimated 15% per year between 2024 and 2030. This rate is more than four times faster than the growth of total electricity consumption across all other sectors combined.

This trajectory of data center expansion directly increases demand for optical fiber infrastructure. Each megawatt of new data center capacity requires several kilometers of intra-data center fiber cabling, high-density patch panels, optical transceivers, and fiber management systems to connect servers, storage, and networking equipment. According to the IEA’s Energy and AI executive summary, global investment in data centers nearly doubled since 2022, reaching approximately half a trillion dollars in 2024. The IEA’s April 2026 analysis further indicated that the capital expenditure of five major technology companies exceeded USD 400 billion in 2025 and is projected to rise by an additional 75% in 2026. Meta, Amazon, Alphabet, and Microsoft collectively plan to spend about USD 320 billion in 2025, up from USD 230 billion in the previous year. A significant portion of this capital expenditure is allocated to fiber optic cabling and connectivity infrastructure, positioning the data center optical fiber market as a primary beneficiary of the AI-driven investment cycle.

Data center optical fiber infrastructure encompasses the complete ecosystem of fiber-optic cables, connectors, patch panels, transceivers, distribution frames, and management systems that provide the internal and external connectivity fabric of data center facilities. In a modern hyperscale or AI data center, optical fiber interconnects operate at multiple levels of the network hierarchy: intra-rack fiber connects servers and accelerators to top-of-rack switches; inter-rack and end-of-row fiber runs from top-of-rack switches to leaf-layer aggregation switches; spine-to-leaf fiber provides the north-south and east-west fabric interconnect of the data center network; and inter-building dark fiber runs between buildings within a campus, between data centers within a cluster, and between data center sites over regional or metropolitan distances. The total fiber count within a large hyperscale data center campus can exceed hundreds of millions of fiber-kilometers when all intra-building, inter-building, and campus interconnect runs are aggregated.

The IEA's Energy and AI report (April 2025) indicates that the United States accounted for 45% of global data center electricity consumption in 2024, with China at 25% and Europe at 15%. This geographic distribution of data center activity closely aligns with patterns of optical fiber infrastructure investment. North America is the largest market for data center optical fiber components and the primary location for hyperscale campus construction by Amazon, Microsoft, Google, and Meta. The DOE's Lawrence Berkeley National Laboratory 2024 Report on U.S. Data Center Energy Use found that data center load growth has tripled over the past decade and is expected to double or triple again by 2028. The Electric Power Research Institute projects that data centers could account for up to 9% of U.S. electricity generation annually by 2030, compared to 4% in 2023. Each additional megawatt of U.S. data center capacity requires a proportional investment in optical fiber infrastructure, making DOE and IEA data center growth projections essential for sizing the optical fiber market.

The competitive landscape of the data center optical fiber market includes fiber and cable manufacturers, transceiver and optical module providers, networking equipment vendors, and data center operators, all of whom collectively determine technology specifications and procurement volumes. Corning Incorporated, recognized as the world's leading optical fiber manufacturer and the inventor of silica optical fiber, maintains the strongest brand position in supplying optical fiber to data centers. Companies such as CommScope, Prysmian Group, Furukawa Electric, Sumitomo Electric, OFS Fitel, Legrand, and Nexans provide optical fiber cables and connectivity hardware, including patch panels, connectors, and fiber management systems. Coherent Corp., Broadcom, and Cisco are prominent suppliers of optical transceivers and silicon photonics-based optical modules. NVIDIA's networking division, following its acquisition of Mellanox, delivers InfiniBand and Ethernet interconnect solutions for AI data centers, thereby establishing high-speed fiber connectivity specifications for the broader ecosystem.

Migration to 800G and 1.6T Network Speeds Driving Complete Fiber Infrastructure Overhaul

The transition of hyperscale data center networks from 100G to 400G, and now to 800G, with 1.6T technology already in development and early deployment, is prompting a comprehensive overhaul of optical fiber infrastructure at the largest global data center facilities. This transition constitutes the most significant near-term revenue driver for suppliers of fiber, transceivers, and connectivity hardware. Each generational speed upgrade necessitates higher-performance optical modules, stricter fiber specifications, improved connector and splicing quality, and, in many cases, a shift from multi-mode to single-mode fiber to accommodate the extended reach and increased bandwidth density required by next-generation speeds. According to the IEA's Energy and AI analysis, AI-focused data centers can consume as much electricity as power-intensive factories. Their fiber interconnect requirements scale with the high-bandwidth, low-latency communication demands of AI training clusters, where thousands of GPUs and accelerators must exchange gradient updates and activation tensors continuously during training runs. NVIDIA's NVLink and InfiniBand interconnect specifications for AI compute clusters establish 400G and 800G per-lane optical interconnect requirements, which are driving the transceiver and fiber upgrade cycle at leading AI hyperscale operators.

AI Data Center Investment Cycle Creating Multi-year Structural Demand

The sustained, large-scale capital expenditures by the world's leading technology companies are generating a multi-year structural demand cycle for data center optical fiber, surpassing the typical equipment refresh cycles of conventional enterprise IT infrastructure. The IEA's April 2026 Key Questions on Energy and AI report states that the capital expenditure of five major technology companies exceeded USD 400 billion in 2025 and is projected to rise by an additional 75% in 2026. The IEA's Electricity Mid-Year Update 2025 further confirms that companies such as Meta, Amazon, Alphabet, and Microsoft have committed to spending USD 320 billion in 2025, an increase from USD 230 billion in the previous year. Additionally, the IEA's April 2025 Energy and AI report projects that electricity consumption in accelerated servers, primarily driven by AI adoption, will increase rapidly through 2030. The pipeline of conditional offtake agreements between data center operators and small modular reactor nuclear projects expanded from 25 gigawatts at the end of 2024 to 45 gigawatts as of April 2026, reflecting the long-term investment horizon of data center operators. Each new data center established during this investment cycle requires a complete optical fiber infrastructure installation, while existing data centers upgrading for AI workloads must transition from legacy 100G to current 400G or 800G fiber infrastructure specifications.

|

Parameter |

Details |

|

Market Size by 2036 |

USD 22.48 Billion |

|

Market Size in 2026 |

USD 8.34 Billion |

|

Market Size in 2025 |

USD 7.12 Billion |

|

Market Growth Rate (2026-2036) |

CAGR of 10.4% |

|

Dominating Region |

North America |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Fiber Type, Component, Connectivity Architecture, Deployment Environment, Application, End User, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Middle East & Africa, and Latin America |

Driver: AI Workload Expansion and Hyperscale Data Center Capacity Growth

The primary driver of the data center optical fiber market is the accelerating expansion of AI infrastructure and hyperscale data center capacity, which directly drives demand for fiber-optic cabling, transceivers, and connectivity hardware as the primary internal and external networking medium. According to the IEA's landmark Energy and AI report published in April 2025, global data center electricity consumption reached approximately 415 TWh in 2024 and grew at around 12% per year since 2017. The IEA's updated Key Questions on Energy and AI analysis published in April 2026 confirmed that data center electricity demand soared by 17% in 2025, with AI-focused data centers growing even faster at 50% in 2025. The IEA projects data center electricity consumption to roughly double from 485 TWh in 2025 to 950 TWh by 2030 in the base case, growing at approximately 15% per year. According to the DOE’s Lawrence Berkeley National Laboratory 2024 report on U.S. data center energy use, U.S. data center load growth has accelerated sharply over the past decade and is expected to continue rising through 2028. Separately, EPRI has estimated that data centers could consume up to 9% of U.S. electricity generation annually by 2030. The United States accounted for 45% of global data center electricity consumption in 2024 per the IEA, confirming the scale and geographic concentration of the data center infrastructure investment that drives optical fiber market demand.

Opportunity: Co-packaged Optics Enabling Next-generation Switch Radix and Bandwidth Density

Co-packaged optics (CPO) technology integrates optical transceiver functions directly with switching ASICs in a single package, rather than relying on pluggable optical modules connected through a PCB backplane. This approach presents a significant opportunity for optical fiber infrastructure suppliers, as hyperscale operators deploy next-generation Ethernet and InfiniBand switches with port counts and bandwidth densities that pluggable transceiver technology cannot efficiently support. The primary commercial implication for the fiber market is that CPO switches provide optical fiber connection points at the front panel, replacing electrical connection points and making fiber the required medium for all switch fabric connectivity, rather than copper for short distances. This shift eliminates the copper direct attach cable option that has served some short-reach data center connections in current-generation networks, thereby converting more connections to fiber. Major switch ASIC vendors, including Broadcom and Marvell, are developing ASIC designs with integrated photonic interfaces specifically for CPO deployment. NVIDIA's networking division and Cisco are also advancing CPO-based switch platforms for the AI data center market. The transition to CPO architecture is expected to accelerate during the forecast period as switch port speeds increase beyond 800G per lane toward 1.6T, creating a structural tailwind for investment in fiber connectivity hardware.

Why Does Single-mode Fiber Lead the Market?

By 2026, the single-mode fiber segment is projected to account for the largest share of the data center optical fiber market. The transition of hyperscale and artificial intelligence data center networks to 400G and 800G transmission speeds is accelerating the adoption of single-mode fiber across data center facilities. Single-mode fiber (SMF) offers the bandwidth capacity, low attenuation, and transmission distance necessary for these advanced speeds in both intra-campus and inter-data-center scenarios. OS2 single-mode fiber, the standard specification for data center applications, supports transmission distances up to 10 kilometers at 10G and can scale to 400G and 800G over relevant data center distances using either coherent or direct-detect optical transceiver technologies. Major hyperscale operators, such as Amazon, Google, Microsoft, and Meta, have standardized on single-mode fiber for campus interconnects, inter-building links, and increasingly for intra-building backbone cabling as 400G and 800G deployments expand from the spine layer to the leaf and top-of-rack layers. Leading commercial products in this segment include Corning's SMF-28 Ultra and related OS2 fiber products, Prysmian's BendBright SMF, and Sumitomo Electric's SMF offerings.

The multi-mode fiber segment continues to hold a significant market share and is expected to grow during the forecast period, particularly in short-reach applications within data center floors. OM4 and OM5 multi-mode fibers enable 100G and 400G transmission over distances of up to 100 to 150 meters using cost-effective VCSEL-based transceivers. This makes them suitable for top-of-rack to end-of-row and intra-rack applications in enterprise and colocation data centers, where the cost advantage of VCSEL transceivers over coherent single-mode modules offsets the shorter reach limitation. OM5 wideband multimode fiber, engineered to support short wavelength division multiplexing at four wavelengths from 850 to 953 nanometers, facilitates 400G transmission over 150 meters using SWDM4 transceivers. This extends the reach of multimode fiber for applications that might otherwise require single-mode solutions.

Why Do Optical Transceivers Lead the Component Market?

By 2026, the optical transceivers segment is projected to account for the largest share of the data center optical fiber market by component. Optical transceivers represent the highest per-unit-value component within the data center fiber infrastructure stack. For example, 400G QSFP-DD and OSFP modules are priced between USD 500 and USD 2,000 per unit, depending on reach and technology, while 800G modules, which are at higher price points, remain in the early stages of commercial deployment. The ongoing hyperscale data center upgrade cycle from 100G to 400G across millions of switch ports constitutes a multi-billion-dollar transceiver replacement initiative, serving as the primary revenue driver for this segment. Coherent Corp., Broadcom, and Cisco are the leading suppliers of transceivers for hyperscale data center applications. Silicon photonics-based optical engine technology enables the integration of multiple 100G lanes into compact module form factors, meeting the power and density requirements of next-generation switches. According to IEA projections, server electricity consumption is expected to increase by 30% annually through 2030. The AI clusters contributing to this growth require GPU-to-GPU interconnect bandwidths that necessitate high-speed optical transceiver deployment at every switch port within the AI fabric.

Despite the dominance of optical transceivers by market value, the optical fiber cables segment remains the foundational component category by volume. Patch panels and fiber management systems are experiencing rapid growth as the density of fiber connections per rack and per data center floor increases with each successive generation of higher-port-count switches and higher-fiber-count cable architectures. The shift toward ultra-high-density fiber management systems, which can support tens of thousands of fiber connections within a single rack unit of panel space, represents a significant product development trend. This trend is driven by the need to minimize the fiber management footprint in increasingly dense AI data center floor layouts.

Why Does Spine-Leaf Architecture Lead the Market?

In 2026, the spine-leaf architecture segment is projected to account for the largest share of the data center optical fiber market by connectivity architecture. Spine-leaf topology has become the standard among major hyperscale cloud providers and is prevalent in new AI data center designs. Its two-layer fabric delivers uniform low latency between any two endpoints, enables horizontal scaling by adding leaf switches without modifying the spine layer, and efficiently manages the intensive east-west traffic characteristic of distributed AI training workloads, where each accelerator communicates with multiple others simultaneously. In this architecture, each leaf switch connects to every spine switch with at least one fiber link, and the spine switches are fully interconnected. This configuration creates a full-mesh optical fiber connectivity pattern, maximizing the total fiber count per data center compared to hierarchical three-tier architectures. The transition from three-tier to spine-leaf architecture in new data center deployments directly increases optical fiber infrastructure investment per build, as the number of fiber runs per square meter of data center floor rises. According to the IEA, nearly half of data center capacity in the United States is concentrated in five regional clusters. These high-density campus environments are the primary locations for large-scale spine-leaf fabric deployment.

However, fabric-based architectures are anticipated to experience the fastest growth during the forecast period. Flat, non-blocking fabric topologies with direct interconnects between all servers and accelerators, such as those implemented in NVIDIA's NVLink domain and InfiniBand fat-tree designs for AI training clusters, currently represent the highest fiber density network topology in data centers. These AI fabric architectures require optical fiber interconnects for every GPU-to-GPU communication path beyond the NVLink domain boundary, resulting in fiber counts per rack that significantly exceed those of conventional spine-leaf Ethernet fabrics. This drives a higher per-rack optical fiber infrastructure investment in AI-optimized data centers.

Why Do Hyperscale Data Centers Lead the Market?

By 2026, hyperscale data centers are expected to command the largest share of the optical fiber market for data centers. Major operators like Amazon Web Services, Microsoft Azure, Google Cloud, Meta, and Apple lead the way with the biggest construction projects and the highest demand for optical fiber. The IEA's Energy and AI report notes that global investment in data centers almost doubled from 2022 to reach half a trillion dollars in 2024. In 2025, the top five tech companies spent over USD 400 billion on capital expenses. In 2024, the United States made up 45% of the world's data center electricity use, with nearly half of its capacity located in five main areas: northern Virginia, Phoenix, Dallas-Fort Worth, Silicon Valley, and Chicago. Each hyperscale campus in these regions includes several large buildings connected by dense fiber networks, with millions of fiber links supporting tens of thousands of servers and network devices.

However, edge data centers are expected to grow the fastest in the coming years. More edge centers are being built at telecom hubs, retail and business sites, and other locations closer to users. This growth is increasing the number of fiber-connected data centers worldwide, with each edge site needing a share of fiber investment for every megawatt of capacity. The IEA predicts that data center electricity use will rise by 15% each year through 2030. This includes both large, centralized hyperscale centers and the growing number of edge sites, as demand for low-latency AI and 5G services leads to more distributed computing at the network edge.

How Does Cloud Computing Infrastructure Lead the Application Market?

In 2026, the cloud computing infrastructure segment is projected to account for the largest share of the data center optical fiber market by application. Cloud computing is the primary driver of hyperscale data center expansion, leading to the highest volume of optical fiber procurement. The cloud infrastructures of Amazon Web Services, Microsoft Azure, Google Cloud Platform, and Alibaba Cloud together constitute the largest concentration of data center optical fiber infrastructure worldwide. Each cloud region comprises multiple data center facilities interconnected by dense fiber cable networks. According to the IEA's Energy and AI report, China accounted for 25% and Europe for 15% of global data center electricity consumption in 2024, with cloud computing infrastructure comprising the majority of data center electricity demand in both regions. The recurring revenue models of major cloud service providers enable sustained investment in infrastructure expansion, maintenance, and upgrades, thereby supporting ongoing high levels of optical fiber procurement.

However, the artificial intelligence (AI) and high-performance computing (HPC) segment is expected to grow the fastest over the forecast period. The IEA projects that electricity consumption in AI-driven accelerated servers will increase by 30% annually in the base case, compared with a 9% annual growth rate for conventional servers. According to IEA projections, accelerated servers are expected to account for nearly half of the net increase in global data center electricity consumption. Each AI training cluster, which consists of thousands of GPUs or other accelerators, requires a high-bandwidth, low-latency fiber interconnect fabric to enable extensive communication among GPUs. This results in fiber port counts per rack that are several times higher than those in conventional cloud compute racks. The combination of high fiber density per rack, large cluster scale, and a rapidly increasing number of clusters positions AI and HPC as the fastest-growing applications driving investment in optical fiber infrastructure.

Why Do Cloud Service Providers Lead the End User Market?

In 2026, the cloud service providers segment is projected to hold the largest share of the data center optical fiber market. Major cloud service providers, such as Amazon Web Services, Microsoft Azure, Google Cloud, Alibaba Cloud, and Meta, are the leading global procurers of optical fiber infrastructure. Each hyperscale operator maintains dedicated procurement programs for fiber cables, transceivers, patch panels, and connectivity hardware, acquiring these components at volumes that significantly exceed those of other end-user categories. According to the IEA, companies including Meta, Amazon, Alphabet, and Microsoft committed to spend USD 320 billion on data center capital expenditure in 2025, an increase from USD 230 billion the previous year. These commitments are driving the largest sustained optical fiber procurement program in the industry's history. The capital expenditure of five major technology companies is expected to increase by an additional 75% in 2026, according to the IEA's April 2026 analysis, which confirms the multi-year duration of this procurement cycle.

However, the colocation providers segment is anticipated to experience the fastest growth among established end-user categories during the forecast period. Colocation data center operators, such as Equinix, Digital Realty, CyberArk, NTT Data Centers, and Iron Mountain, are rapidly expanding their global data center portfolios to meet increasing enterprise and hyperscale colocation demand. These operators invest in optical fiber infrastructure for both customer connectivity within colocation facilities and for inter-facility dark fiber networks that link their campuses in major metropolitan markets. The trend of hyperscale cloud providers leasing colocation capacity from third-party operators, rather than constructing all capacity internally, is accelerating colocation operator investment.

How is North America Maintaining Market Leadership?

In 2026, North America is projected to account for the largest share of the global data center optical fiber market. The United States serves as the primary market, supported by its status as the largest global data center electricity consumer, representing 45% of total data center electricity consumption in 2024 according to the IEA. This dominance is further reinforced by the concentration of the world's largest hyperscale data center campuses operated by Amazon, Microsoft, Google, Meta, and Apple.

The IEA's Energy and AI report indicates that nearly half of U.S. data center capacity is concentrated within five regional clusters. U.S. data centers consumed approximately 180 TWh of electricity in 2024, as reported in the IEA's Electricity Mid-Year Update 2025. The DOE's LBNL 2024 Report on U.S. Data Center Energy Use projects that U.S. data center load growth will double or triple by 2028. Additionally, EPRI estimates that data centers could account for up to 9% of U.S. electricity generation by 2030. The IEA's April 2026 analysis confirms that data center capital expenditure is expected to increase by 75% in 2026, with the United States receiving the majority of this global investment. This trend is attributed to the country's available land, robust power infrastructure, skilled workforce, and established hyperscale operator presence, making it the preferred location for hyperscale AI training cluster deployment. Canada also contributes to regional demand through increased data center investment in Toronto, Vancouver, and Montreal, driven by favorable climate conditions for data center cooling, competitive energy prices, and proximity to major U.S. technology markets.

Which Factors Drive Asia-Pacific's Rapid Growth?

The Asia-Pacific region is projected to experience the most rapid growth in the data center optical fiber market in the coming years. This expansion is driven by the growth of China's data center industry, Singapore's emergence as a key hub for hyperscale facilities, increased investments in new data centers in India, and the implementation of advanced digital infrastructure projects in South Korea and Japan.

According to the IEA's Energy and AI report, China accounted for 25% of global data center electricity consumption in 2024, second only to the United States. Leading Chinese companies, including Alibaba Cloud, Tencent Cloud, Huawei Cloud, and ByteDance, are rapidly expanding their data center operations to meet increasing demand for AI and cloud computing, supported by significant government investment in digital infrastructure. Singapore possesses the highest concentration of hyperscale data center investments in Southeast Asia, with firms such as Equinix, Digital Realty, Google, Microsoft, and AWS constructing or operating large-scale facilities. This expansion is facilitated by the Singapore government's strategic resumption of data center approvals following a temporary pause. India's data center market is also expanding swiftly, with both international and domestic companies investing in new facilities in cities such as Mumbai, Chennai, Hyderabad, and Pune. The IEA projects that the Asia-Pacific region's share of global data center electricity consumption will continue to rise as digitalization and AI adoption accelerate, further stimulating investment in optical fiber infrastructure.

Some of the key companies operating in the global data center optical fiber market are Corning Incorporated, CommScope Holding Company Inc., Prysmian Group, Furukawa Electric Co. Ltd., Sumitomo Electric Industries Ltd., OFS Fitel LLC, Legrand SA, Nexans S.A., Amphenol Corporation, Molex LLC, Coherent Corp., Broadcom Inc., Cisco Systems Inc., NVIDIA Corporation (Networking Division), and Hengtong Group Co. Ltd.

The global data center optical fiber market is expected to grow from USD 8.34 billion in 2026 to USD 22.48 billion by 2036.

The global data center optical fiber market is projected to grow at a CAGR of 10.4% from 2026 to 2036.

The primary driver is the accelerating expansion of AI and hyperscale data center infrastructure. According to the IEA's April 2025 Energy and AI report, global data center electricity consumption grew 12% annually since 2017 to approximately 415 TWh in 2024, and the IEA's April 2026 update confirmed data center electricity demand soared 17% in 2025, with AI-focused data centers growing 50%. The IEA projects consumption to double to 950 TWh by 2030 at 15% annual growth. Each increment of this growth requires proportional optical fiber infrastructure investment.

The single-mode fiber segment is expected to dominate the overall market in 2026, as the migration to 400G and 800G speeds requires SMF's superior bandwidth and reach performance. Multi-mode fiber continues to serve short-reach intra-data-center applications with OM4 and OM5 fiber in enterprise and colocation environments where VCSEL transceiver cost advantages remain relevant.

The hyperscale data centers segment is expected to dominate the overall market in 2026, anchored by the 45% U.S. share of global data center electricity consumption per the IEA and the USD 400+ billion capital expenditure commitment of major technology companies in 2025. The edge data centers segment is expected to witness the fastest CAGR as AI inference, 5G hosting, and latency-sensitive workloads drive distributed compute deployment.

North America is expected to lead the global market in 2026, driven by the U.S. accounting for 45% of global data center electricity consumption per the IEA in 2024 and the concentration of hyperscale AI data center investment. Asia-Pacific is expected to witness the fastest CAGR, driven by China's 25% global share, Singapore's hyperscale hub status, and India's rapidly growing data center investment pipeline.

The major players are Corning, CommScope, Prysmian Group, Furukawa Electric, Sumitomo Electric, OFS Fitel, Legrand, Nexans, Amphenol, Molex, Coherent Corp., Broadcom, Cisco, NVIDIA Networking, and Hengtong Group.

Published Date: Apr-2026

Published Date: Apr-2026

Published Date: Feb-2026

Published Date: Oct-2024

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates