Resources

About Us

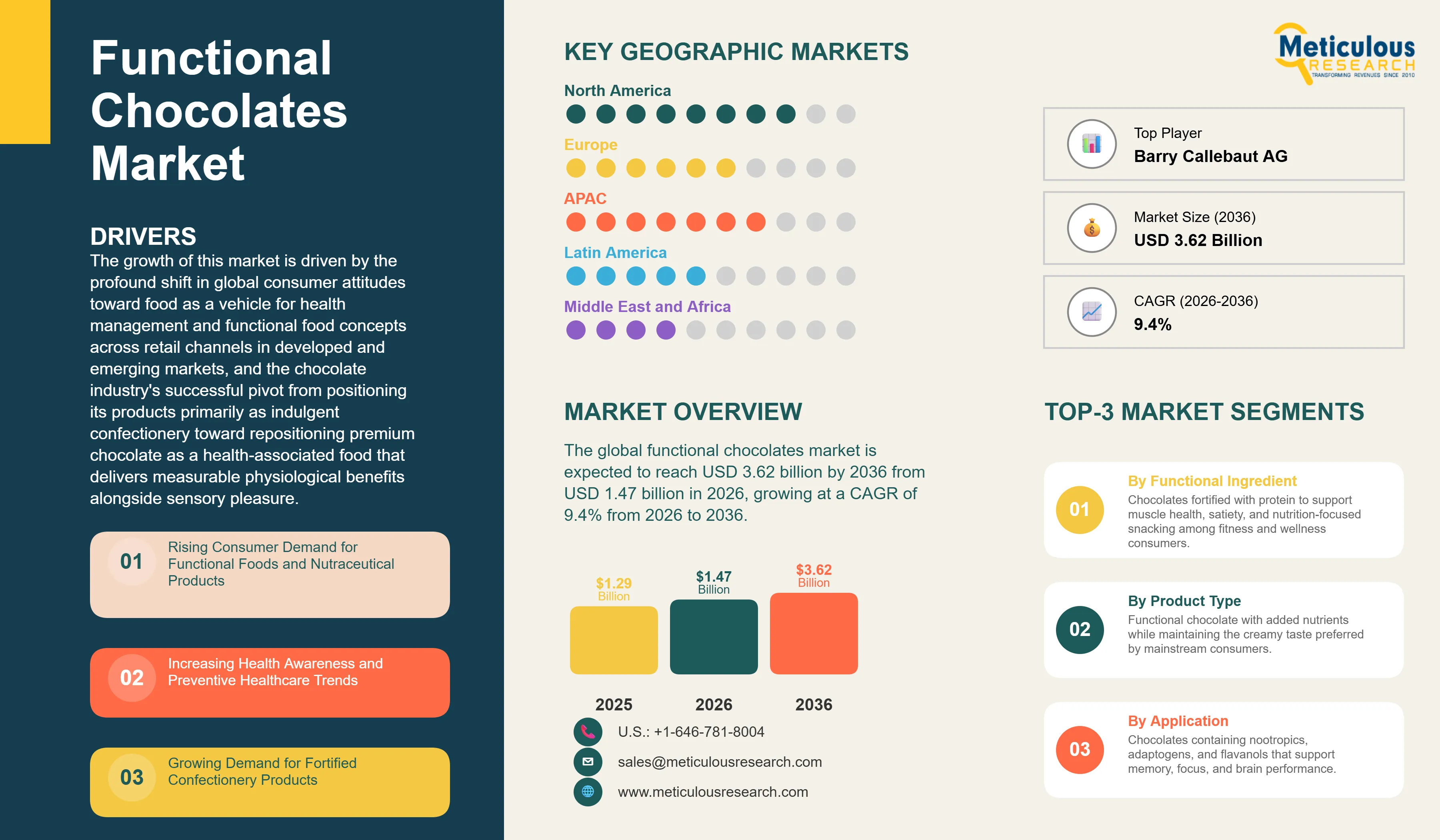

The global functional chocolates market was valued at USD 1.29 billion in 2025. This market is expected to reach USD 3.62 billion by 2036 from USD 1.47 billion in 2026, growing at a CAGR of 9.4% from 2026 to 2036.

The growth of this market is driven by the profound shift in global consumer attitudes toward food as a vehicle for health management, the accelerating mainstreaming of nutraceutical and functional food concepts across retail channels in developed and emerging markets, and the chocolate industry's successful pivot from positioning its products primarily as indulgent confectionery toward repositioning premium chocolate as a health-associated food that delivers measurable physiological benefits alongside sensory pleasure. Functional chocolates are confectionery products that combine a chocolate base — dark, milk, white, or sugar-free — with bioactive ingredients that provide specific health benefits beyond basic caloric nutrition, including proteins for muscle maintenance and satiety, probiotics and prebiotics for gut microbiome support, vitamins and minerals for micronutrient fortification, antioxidants for cellular protection, adaptogens and herbal extracts for stress modulation and cognitive support, and botanical ingredients including CBD for relaxation and wellness applications. The category encompasses both mass-market fortified chocolate products offered by large multinational confectionery companies and premium artisanal functional chocolate brands that command significant price premiums by emphasizing clean-label ingredient transparency, superfood inclusion, and evidence-based health positioning.

The functional chocolate category occupies a commercially compelling intersection between the established and growing global chocolate confectionery market, valued at over USD 130 billion, and the rapidly expanding functional food and nutraceutical market, which is driven by the same consumer health awareness trends that are reshaping food purchasing behavior across all categories. Chocolate's unique sensory properties — its creamy mouthfeel, complex flavor profile, and deeply established emotional associations with pleasure and reward — give it structural advantages as a delivery vehicle for functional ingredients relative to supplement formats such as capsules, tablets, and unflavored protein powders that many consumers find unappealing or inconvenient. The growing consumer willingness to pay premium prices for chocolate products that combine health benefits with the sensory experience of premium chocolate represents a fundamental market opportunity that has attracted investment from both established confectionery companies and a new generation of health-focused chocolate brands.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The functional chocolates market represents the convergence of two of the most dynamic consumer product categories of the past decade: premium chocolate confectionery and functional food and nutraceutical products. The category has evolved from its origins in simple vitamin-fortified chocolate products and sugar-free diabetic chocolates toward a sophisticated and rapidly diversifying landscape of products that integrate specific bioactive ingredient systems with premium chocolate platforms to deliver targeted health benefits that are communicated to consumers through transparent labeling, evidence-based marketing claims, and the credibility of established functional ingredient brands.

The technical foundation of functional chocolate product development is the successful incorporation of bioactive functional ingredients into chocolate matrices without compromising the taste, texture, and shelf stability that consumers expect from premium chocolate products. Chocolate is a complex colloidal system of cocoa butter, cocoa solids, sugar, and milk solids that is sensitive to temperature, moisture, and ingredient compatibility in ways that create genuine formulation challenges for functional ingredient integration. Proteins added to chocolate formulations must be selected and processed to avoid off-flavors, grittiness, and emulsification disruption that impair the eating experience. Probiotics incorporated into chocolate require microencapsulation protection systems that maintain viable bacterial counts through the high temperatures and humidity fluctuations of chocolate manufacturing, storage, and distribution. Water-soluble vitamins and minerals must be incorporated in forms that resist migration into the chocolate fat phase and maintain bioavailability. Adaptogens and botanical extracts must be introduced in flavor-compatible forms and concentrations that deliver effective doses without overwhelming the chocolate's flavor profile. The development of microencapsulation technologies, encapsulated probiotic preparations, and lipid-coated nutrient delivery systems specifically designed for confectionery matrices has been a critical enabling factor in the category's technical advancement.

The competitive landscape of the functional chocolates market spans three distinct segments that differ in scale, business model, and target consumer. Large multinational confectionery companies including Nestlé, Mars, Mondelez, Hershey, and Ferrero are addressing functional chocolate through product line extensions and acquisitions that add health-positioned variants to their established mainstream chocolate portfolios, targeting mass-market health-interested consumers through conventional grocery retail channels. Mid-tier premium chocolate companies including Lindt and Barry Callebaut are developing high-cacoa-content and functional ingredient enriched products that leverage their premium brand positioning to command higher price points in specialty and department store channels. A rapidly growing ecosystem of specialist functional chocolate brands including Hu Kitchen, Lily's Sweets, Alter Eco, Theo Chocolate, Goodio, and Love Cocoa are building direct-to-consumer and natural food retailer businesses around clean-label, organic, and specifically formulated functional chocolate products that prioritize ingredient transparency and health benefit specificity over broad mass-market distribution.

Growing Demand for Sugar-Free and Low-Sugar Functional Chocolates

The most broadly impactful trend reshaping functional chocolate product development and market growth is the rapid expansion of consumer demand for sugar-free and reduced-sugar chocolate options that maintain the sensory pleasure of conventional chocolate while eliminating or minimizing glycemic impact. The global rise in type 2 diabetes prevalence, which affects over 500 million adults worldwide with an additional estimated 400 million individuals in pre-diabetic states, is creating a large and growing consumer population with both medical motivation and personal lifestyle preference to reduce sugar consumption without abandoning chocolate enjoyment. The simultaneous mainstream adoption of low-carbohydrate dietary patterns including ketogenic, paleo, and general low-glycemic eating frameworks is extending the target consumer for sugar-free functional chocolate beyond clinical diabetic populations to include health-conscious mainstream consumers who have made reducing sugar intake a general wellness priority.

The commercial viability of sugar-free functional chocolate has been transformed by the maturation of alternative sweetener technology and the dramatic improvement in taste and texture quality achievable with erythritol, allulose, monk fruit extract, and stevia glycoside sweetener systems that have largely overcome the aftertaste and textural limitations of earlier-generation sugar alcohols and intense sweeteners. Lily's Sweets has built a successful brand specifically around stevia-sweetened dark and milk chocolate bars and chips that command premium positioning in natural food retail. Hu Kitchen's grain-free, refined-sugar-free chocolate has developed a loyal following among consumers seeking paleo and clean-label chocolate with functional ingredient additions. The combination of sugar reduction with specific functional ingredient fortification — protein, adaptogens, or probiotics — creates compound value propositions that appeal to consumers seeking multiple simultaneous health benefits from a single confectionery product.

Integration of Superfoods and Adaptogens in Chocolate Products

The incorporation of superfood ingredients and adaptogenic botanical extracts into functional chocolate formulations represents one of the most commercially dynamic and consumer-engaging trends in the category. Superfoods including matcha, turmeric, acai, spirulina, goji berry, and cacao nibs bring visible color differentiation, distinctive flavor profiles, and strong health-positive consumer associations to chocolate products that justify premium pricing and generate social media-driven discovery. Adaptogenic botanicals including ashwagandha, lion's mane mushroom, reishi mushroom, and rhodiola rosea are entering the mainstream functional food market from their origins in traditional herbal medicine and the dietary supplement industry, carried by consumer interest in stress management, mental clarity, and resilience that intensified significantly following the global pandemic period.

The chocolate delivery format is particularly well-suited to adaptogenic and superfood ingredient incorporation because the complex flavor profile of high-cocoa-content dark chocolate can accommodate the earthy, bitter, and botanical flavor notes that many adaptogenic extracts bring without creating the medicinal off-flavors that make the same ingredients unpalatable in other food matrices. Functional chocolate brands including Sakara Life, Foursigmatic's chocolate products, and Goodio have developed sophisticated multi-ingredient functional chocolate formulations that incorporate multiple adaptogenic and superfood ingredients alongside high-quality chocolate in products designed to appeal to premium wellness-oriented consumers. The premiumization dynamic in the functional chocolate category is reinforced by the high cost of premium adaptogenic ingredients, which justifies retail price points of USD 5 to 15 per bar that would be untenable for conventional chocolate but are accepted by health-focused consumers comparing the product to dietary supplement costs.

|

Parameter |

Details |

|

Market Size by 2036 |

USD 3.62 Billion |

|

Market Size in 2026 |

USD 1.47 Billion |

|

Market Size in 2025 |

USD 1.29 Billion |

|

Market Growth Rate (2026–2036) |

CAGR of 9.4% |

|

Dominating Region |

North America |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Functional Ingredient, Product Type, Application, Distribution Channel, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Rising Consumer Demand for Functional Foods and Nutraceutical Products

The primary driver of the functional chocolates market is the structural shift in global consumer food purchasing behavior toward products that deliver nutritional function and health benefits alongside conventional food enjoyment. The global functional food and nutraceutical market has grown from a niche category serving health-conscious early adopters to a mainstream consumer segment that encompasses billions of consumers across all income levels and geographic markets. This growth is driven by demographic aging in developed markets, where older consumers increasingly seek food products that support healthy aging, joint health, cardiovascular function, and cognitive maintenance. It is reinforced by the growing awareness among younger consumers that preventive nutrition practices implemented early in life contribute to long-term health outcomes, creating health-motivated food purchasing behavior across age cohorts rather than being concentrated among elderly populations.

Consumer research consistently demonstrates that the majority of consumers in North America and Europe, and a rapidly growing proportion in Asia-Pacific, actively seek out foods with functional health benefits and are willing to pay meaningful premiums for products that deliver credible health benefit claims backed by ingredient transparency. Chocolate, as one of the most universally beloved food categories globally, is uniquely positioned to benefit from this functional food demand growth, as the combination of established consumer affection for chocolate with the desire for health-beneficial eating creates a consumer acceptance advantage for functional chocolate products relative to functional food formats with lower baseline appeal.

Development of Plant-Based and Vegan Functional Chocolates

The intersection of plant-based eating trends and functional food demand is creating a significant growth opportunity for functional chocolate formulations that are entirely plant-based and vegan-certified, eliminating dairy milk solids from conventional milk chocolate formulations and replacing them with oat, almond, coconut, or cashew milk alternatives. The global plant-based food movement has developed a large and commercially attractive consumer segment that applies plant-based product preferences across all food categories including confectionery, and the combination of plant-based positioning with functional ingredient addition creates a compound value proposition that resonates strongly with health-and-sustainability-motivated consumer segments. Functional chocolate brands that can successfully develop plant-based milk chocolate formulations — historically challenging due to the technical difficulty of replicating the creaminess and mouthfeel of dairy milk chocolate with plant-based alternatives — will access the growing segment of consumers seeking plant-based confectionery with health benefits.

Integration of Superfoods and Adaptogens in Chocolate Products

The growing consumer familiarity with adaptogenic and superfood ingredients, driven by supplement market education, social media wellness culture, and health professional advocacy, is creating expanding demand for accessible and enjoyable food delivery formats for these ingredients. Functional chocolate's ability to mask the typically unpleasant taste of many adaptogenic botanicals while delivering them in a format that consumers actively enjoy consuming multiple times per week creates a frequency-of-use advantage over supplement capsule delivery formats that supports consistent ingredient intake and brand loyalty. The adaptogenic chocolate opportunity is particularly compelling because the consumer segments most interested in adaptogenic ingredients — urban millennials and Gen Z consumers focused on stress management, cognitive performance, and overall wellness — are also significant premium food and direct-to-consumer e-commerce consumers, making them accessible through the distribution channels most accessible to emerging functional chocolate brands.

How Do Protein-Enriched Chocolates Lead the Market?

In 2026, the protein-enriched chocolates segment is expected to hold the largest share of the functional chocolates market by functional ingredient. Protein-fortified chocolate products represent the most commercially mature and broadly distributed functional chocolate category, with established shelf presence in grocery, pharmacy, convenience, and sports nutrition retail channels and strong mainstream consumer recognition of protein content as a desirable nutritional attribute in snack foods. The sports nutrition channel, which encompasses protein bars, protein shakes, and protein-enriched snack products, has driven the development and consumer acceptance of high-protein chocolate-flavored and chocolate-coated products, creating an established consumer demand base that specialist functional chocolate brands have translated into premium whole-chocolate products with higher cocoa content and cleaner ingredient profiles. The macronutrient context of protein enrichment — supporting muscle maintenance, satiety, and metabolic health — resonates across a broad consumer base extending well beyond dedicated sports nutrition consumers to include weight management-motivated consumers, aging adults seeking to maintain muscle mass, and general health-conscious consumers who have incorporated higher protein intake as a dietary priority.

However, the probiotic and prebiotic chocolates segment is expected to witness the fastest growth during the forecast period. The gut health and microbiome wellness category has emerged as one of the highest-growth segments of the functional food and supplement market globally, driven by rapidly expanding consumer awareness of the gut microbiome's role in immune function, mental health through the gut-brain axis, metabolic health, and overall wellness. The successful translation of probiotic supplementation from yogurt and capsule formats into premium chocolate delivery systems addresses a genuine consumer desire for enjoyable, convenient, and consistent probiotic intake that yogurt cannot satisfy for consumers who dislike dairy or do not consume yogurt regularly, and that supplement capsules cannot deliver with the same daily compliance motivation as a premium chocolate product. Microencapsulation technology advances that maintain probiotic viability through chocolate manufacturing and extended shelf life are enabling the credible development of products with clinically relevant probiotic doses in chocolate formats, providing the technical foundation for rapid commercial expansion of this segment.

How Does Dark Chocolate Lead the Market?

In 2026, the dark chocolate segment is expected to hold the largest share of the functional chocolates market by product type. Dark chocolate's dominant position in the functional chocolate category reflects its established health-positive consumer image, grounded in well-publicized scientific research demonstrating that cocoa flavanols present at high concentrations in dark chocolate deliver clinically meaningful benefits for cardiovascular health through improved endothelial function and blood flow regulation, for cognitive function through cerebral blood flow enhancement and neuroprotective mechanisms, and for antioxidant protection against oxidative stress. This research-supported health positioning gives dark chocolate a natural credibility advantage as a base format for functional chocolate products that is not shared by milk chocolate or white chocolate, which contain lower or negligible cocoa flavanol concentrations. The compatibility of dark chocolate's intense and complex flavor profile with the earthy, bitter, and botanical flavor notes of adaptogenic and superfood functional ingredients — including mushroom extracts, ashwagandha, turmeric, and matcha — further reinforces dark chocolate's dominant position in the premium functional ingredient chocolate category.

However, the sugar-free chocolate segment is expected to witness the fastest growth during the forecast period. The convergence of rising diabetes prevalence, mainstream adoption of low-carbohydrate dietary patterns, and significant technical improvement in the taste quality of sugar-free chocolate formulations is driving rapid growth in consumer demand for sugar-free functional chocolate options. Brands including Lily's Sweets, ChocZero, and Hu Kitchen's sugar-free line have demonstrated the commercial viability of premium sugar-free functional chocolate at retail price points of USD 4 to 8 per bar, with strong repeat purchase rates indicating high consumer satisfaction with product quality. The combination of sugar-free formulation with functional ingredient addition — protein fortification for diabetic consumers managing both sugar intake and muscle mass, or adaptogen inclusion for consumers following ketogenic diets who seek stress and cognitive support — creates compound functional value propositions that justify the premium pricing of sugar-free functional chocolate products.

How Does the General Wellness Application Lead the Market?

In 2026, the general wellness segment is expected to hold the largest share of the functional chocolates market by application. General wellness-positioned functional chocolate products target the broadest and most commercially accessible consumer segment: health-conscious individuals who seek products that support their overall wellbeing without addressing a specific clinical condition or sports performance objective. This broad positioning is the most commercially practical approach for functional chocolate brands seeking significant retail distribution and mass consumer appeal, as it does not require consumers to self-identify with a specific health condition or nutrition protocol to consider the product relevant to their needs. Products positioned for general wellness leverage the established health associations of dark chocolate's cocoa flavanols, combined with broadly appealing functional additions such as vitamins, minerals, and general antioxidant-rich superfoods, to create health-positive products that health-conscious mainstream consumers can incorporate into their daily routines without requiring specific wellness knowledge or health objectives.

However, the cognitive health application is expected to witness the fastest growth during the forecast period. The rapid expansion of consumer interest in cognitive performance, mental focus, memory support, and long-term neuroprotection is creating strong demand for functional food products that credibly address these outcomes. Functional chocolate products incorporating cocoa flavanols at concentrations demonstrated in clinical studies to improve cerebral blood flow and cognitive test performance, combined with nootropic additives including lion's mane mushroom standardized extract, phosphatidylserine, bacopa monnieri, and citicoline, represent a compelling and differentiated product proposition that addresses growing consumer anxiety about cognitive health. The aging demographic in developed markets, where concerns about age-related cognitive decline are motivating active preventive nutrition strategies, and the performance-oriented millennial and Gen Z consumer segments seeking cognitive optimization products for professional and academic performance, represent a large and commercially attractive bimodal target audience for cognitive health functional chocolate products.

How Do Supermarkets and Hypermarkets Lead the Market?

In 2026, the supermarkets and hypermarkets segment is expected to hold the largest share of the functional chocolates market by distribution channel. Mass grocery retail remains the highest-volume distribution channel for chocolate confectionery globally, and functional chocolate products with sufficient brand recognition and mainstream consumer appeal to secure grocery retail shelf placement achieve the highest absolute sales volumes of any distribution channel. Large confectionery companies including Nestlé, Mars, Mondelez, and Hershey leverage their established retail relationships and trade marketing infrastructure to secure prominent shelf positioning for their functional chocolate product line extensions in mainstream grocery channels, reaching casual health-interested consumers who encounter functional chocolate products during routine grocery shopping rather than specifically seeking them out in specialty channels.

However, the online retail and e-commerce segment is expected to witness the fastest growth during the forecast period. The structural advantages of digital commerce for premium and specialist functional chocolate brands are compelling: direct-to-consumer online channels enable detailed product story communication about ingredient sourcing, functional benefits, and clinical evidence; they allow subscription commerce models that provide recurring revenue and high customer retention; they support targeted marketing to health-oriented consumer communities through social media, wellness influencer partnerships, and search engine marketing; and they provide access to national and international consumer audiences for brands that lack the scale to secure conventional retail distribution. The pandemic-driven acceleration of online grocery and specialty food purchasing created lasting behavioral changes in consumer willingness to purchase premium food products online, and functional chocolate brands have been among the principal beneficiaries of this behavioral shift.

How is North America Maintaining Market Leadership?

In 2026, North America is expected to hold the largest share of the global functional chocolates market. The United States is the primary driver of North American market leadership, representing the most commercially developed functional food market globally in terms of consumer awareness, retail infrastructure for specialty and premium functional products, and willingness to pay premium prices for health-positioned food innovations. The U.S. natural and specialty food retail channel, anchored by retailers including Whole Foods Market, Sprouts Farmers Market, and Natural Grocers, provides the retail infrastructure through which premium functional chocolate brands achieve their initial commercial traction and brand building before transitioning to broader conventional grocery distribution. The rapid growth of direct-to-consumer e-commerce for premium food products in the United States, combined with the country's sophisticated social media and wellness influencer marketing ecosystem, has enabled a generation of specialist functional chocolate brands to build significant consumer followings and revenue bases without the capital requirements of conventional retail distribution programs.

Canada contributes meaningfully to North American market leadership through its health-conscious consumer base, well-developed natural food retail channel, and growing direct-to-consumer digital commerce infrastructure for premium food products. Canadian consumers demonstrate strong alignment with U.S. functional food consumption trends, with comparable willingness to pay premium prices for clean-label, organic, and functional chocolate products, and the cross-border availability of major U.S. functional chocolate brands in Canadian natural food retail and e-commerce channels supports market development without the market entry investment requirements of genuinely separate international expansion.

Which Factors Drive Asia-Pacific's Rapid Growth?

Asia-Pacific is expected to witness the highest growth rate in the functional chocolates market during the forecast period. This growth is driven by the combination of rapidly rising premium food consumption in China, India, Japan, and South Korea, the strong cultural tradition of food-as-medicine thinking in Asian markets that creates favorable consumer receptivity to functional benefit claims on food products, and the explosive growth of health and wellness consumer segments in rapidly urbanizing middle-class populations across the region.

Japan represents the most commercially mature functional food market within Asia-Pacific, with a decades-long history of Foods for Specified Health Uses (FOSHU) and Foods with Functional Claims (FFC) regulatory frameworks that have established strong consumer familiarity with functional food concepts and health claim substantiation requirements. Japanese consumers demonstrate high willingness to pay premium prices for functional food products with credible health benefit claims, and the country's sophisticated confectionery market and strong premium chocolate culture create favorable conditions for functional chocolate market development. South Korea's highly health-conscious urban consumer base, driven by the country's strong beauty and wellness culture, is creating rapidly growing demand for functional food products including functional chocolates addressing skin health, weight management, and cognitive performance. China's functional food market is growing rapidly as rising incomes and health awareness among urban middle-class consumers drive demand for premium health-positioned food products, with functional chocolate benefiting from the premium positioning of chocolate confectionery among Chinese consumers for whom high-quality imported and domestic premium chocolate carries strong aspirational brand associations alongside health benefit communication. India's functional chocolate market is at an earlier stage of development but is growing rapidly among urban, educated, and health-conscious consumer segments, supported by the country's well-developed tradition of herbal and Ayurvedic functional ingredients — including ashwagandha and turmeric — that are increasingly incorporated into functional chocolate products targeting Indian consumers.

Some of the key companies operating in the global functional chocolates market are Nestlé S.A., Mars, Incorporated, Mondelez International, Lindt & Sprüngli, Barry Callebaut AG, Hershey Company, Ferrero Group, Hu Kitchen, Endangered Species Chocolate, Lily's Sweets, Alter Eco Foods, Theo Chocolate, Goodio Chocolate, Love Cocoa, and Taza Chocolate.

The global functional chocolates market is expected to grow from USD 1.47 billion in 2026 to USD 3.62 billion by 2036.

The global functional chocolates market is projected to grow at a CAGR of 9.4% from 2026 to 2036.

The protein-enriched chocolates segment is expected to dominate the overall market in 2026, reflecting the maturity and broad retail distribution of high-protein chocolate products in sports nutrition and mainstream grocery channels. However, the probiotic and prebiotic chocolates segment is expected to witness the fastest CAGR, driven by the explosive consumer interest in gut health and microbiome science and the successful development of viable probiotic chocolate formulations that deliver clinically relevant probiotic doses in premium chocolate formats.

The dark chocolate segment is expected to dominate the overall market in 2026, supported by dark chocolate's established health-positive consumer image and its natural compatibility with a wide range of premium functional ingredient additions. The sugar-free chocolate segment is expected to witness the fastest CAGR, driven by rising diabetes prevalence, the mainstreaming of low-carbohydrate dietary patterns, and the significant improvement in sugar-free chocolate taste quality through advanced alternative sweetener technologies.

The general wellness segment is expected to dominate the overall market in 2026, reflecting the broad consumer accessibility of general wellness-positioned functional chocolate products. The cognitive health segment is expected to witness the fastest CAGR, driven by growing consumer concern about cognitive performance and age-related cognitive decline, and the emergence of credible nootropic ingredient formulations incorporating lion's mane mushroom, phosphatidylserine, and high-flavanol cocoa in chocolate delivery formats.

The supermarkets and hypermarkets segment is expected to dominate the overall market in 2026, reflecting the high-volume distribution capability of mass grocery retail for mainstream and premium functional chocolate products. The online retail and e-commerce segment is expected to witness the fastest CAGR, driven by the structural advantages of direct-to-consumer digital channels for specialist functional chocolate brands and the pandemic-driven normalization of premium food purchases through online platforms.

North America is expected to lead the global market in 2026, supported by the United States' highly developed functional food market infrastructure, premium natural food retail channel, and direct-to-consumer e-commerce ecosystem for specialty food brands. Asia-Pacific is expected to witness the fastest CAGR, driven by rapid growth in premium food consumption, strong cultural alignment with functional food concepts, and the explosive expansion of health-conscious consumer segments in China, India, Japan, and South Korea.

The major players are Nestlé S.A., Mars, Incorporated, Mondelez International, Lindt & Sprüngli, Barry Callebaut AG, Hershey Company, Ferrero Group, Hu Kitchen, Endangered Species Chocolate, Lily's Sweets, Alter Eco Foods, Theo Chocolate, Goodio Chocolate, Love Cocoa, and Taza Chocolate.

1. Introduction

1.1. Market Definition

1.2. Market Ecosystem

1.3. Currency and Limitations

1.3.1. Currency

1.3.2. Limitations

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Data Collection & Validation Process

2.2.1. Secondary Research

2.2.2. Primary Research & Validation

2.2.2.1. Primary Interviews with Experts

2.2.2.2. Approaches for Country-/Region-Level Analysis

2.3. Market Estimation

2.3.1. Bottom-Up Approach

2.3.2. Top-Down Approach

2.3.3. Growth Forecast

2.4. Data Triangulation

2.5. Assumptions for the Study

3. Executive Summary

4. Market Overview

4.1. Introduction

4.2. Market Dynamics

4.2.1. Drivers

4.2.1.1. Rising Consumer Demand for Functional Foods and Nutraceutical Products

4.2.1.2. Increasing Health Awareness and Preventive Healthcare Trends

4.2.1.3. Growing Demand for Fortified Confectionery Products

4.2.1.4. Expansion of Premium and Specialty Chocolate Markets

4.2.2. Restraints

4.2.2.1. Higher Cost of Functional Ingredients

4.2.2.2. Regulatory Challenges for Health Claims in Food Products

4.2.2.3. Limited Consumer Awareness in Emerging Markets

4.2.3. Opportunities

4.2.3.1. Development of Plant-Based and Vegan Functional Chocolates

4.2.3.2. Integration of Superfoods and Adaptogens in Chocolate Products

4.2.3.3. Growth in Personalized Nutrition and Functional Snacking

4.2.3.4. Expansion of E-commerce and Direct-to-Consumer Sales Channels

4.2.4. Challenges

4.2.4.1. Maintaining Taste and Texture with Functional Ingredients

4.2.4.2. Shelf-Life Stability of Fortified Chocolate Products

4.3. Key Market Trends & Innovation Landscape

4.3.1. Growing Demand for Sugar-Free and Low-Sugar Functional Chocolates

4.3.2. Incorporation of Superfoods such as Matcha, Turmeric, and Acai

4.3.3. Expansion of Plant-Based and Vegan Chocolate Formulations

4.3.4. Development of High-Protein and Sports Nutrition Chocolates

4.3.5. Premiumization and Clean Label Chocolate Innovations

4.4. Product Innovation & Ingredient Technology Landscape

4.4.1. Functional Ingredient Fortification Technologies

4.4.2. Sugar Reduction and Alternative Sweetener Technologies

4.4.3. Microencapsulation Technologies for Nutrient Stability

4.4.4. Advanced Chocolate Processing Techniques

4.5. Regulatory and Standards Environment

4.5.1. Functional Food Regulations in North America

4.5.2. EFSA Health Claim Regulations in Europe

4.5.3. Functional Food Regulatory Landscape in Asia-Pacific

4.5.4. Labeling Requirements for Nutraceutical Food Products

4.6. Porter's Five Forces Analysis

4.7. Supply Chain & Ecosystem Analysis

4.7.1. Cocoa Suppliers

4.7.2. Functional Ingredient Suppliers

4.7.3. Chocolate Manufacturers

4.7.4. Retail and Distribution Channels

4.7.5. End Consumers

4.8. Strategic Developments & Investment Landscape

4.8.1. New Product Launches in Functional Chocolates

4.8.2. Investments in Functional Food Innovation

4.8.3. Partnerships Between Chocolate Brands and Nutraceutical Companies

4.8.4. Mergers & Acquisitions in the Functional Food Industry

4.9. Patent Landscape and Innovation Analysis

4.10. Pricing Analysis by Product Type and Region

5. Functional Chocolates Market, by Functional Ingredient

5.1. Introduction

5.2. Protein-Enriched Chocolates

5.3. Probiotic and Prebiotic Chocolates

5.4. Vitamin and Mineral Fortified Chocolates

5.5. Antioxidant-Enriched Chocolates

5.6. Adaptogen and Herbal Extract Chocolates

5.7. CBD and Botanical Infused Chocolates

6. Functional Chocolates Market, by Product Type

6.1. Introduction

6.2. Dark Chocolate

6.3. Milk Chocolate

6.4. White Chocolate

6.5. Sugar-Free Chocolate

6.6. High-Protein Chocolate

7. Functional Chocolates Market, by Application

7.1. Introduction

7.2. Sports Nutrition

7.3. Digestive Health

7.4. Cognitive Health

7.5. Immunity Boosting

7.6. Weight Management

7.7. General Wellness

8. Functional Chocolates Market, by Distribution Channel

8.1. Introduction

8.2. Supermarkets and Hypermarkets

8.3. Convenience Stores

8.4. Specialty Health Food Stores

8.5. Online Retail and E-commerce

8.6. Direct-to-Consumer Sales

9. Functional Chocolates Market, by Geography

9.1. Introduction

9.2. North America

9.2.1. U.S.

9.2.2. Canada

9.3. Europe

9.3.1. Germany

9.3.2. France

9.3.3. U.K.

9.3.4. Italy

9.3.5. Spain

9.3.6. Switzerland

9.3.7. Netherlands

9.3.8. Rest of Europe

9.4. Asia-Pacific

9.4.1. China

9.4.2. Japan

9.4.3. India

9.4.4. South Korea

9.4.5. Australia

9.4.6. Thailand

9.4.7. Indonesia

9.4.8. Vietnam

9.4.9. Rest of Asia-Pacific

9.5. Latin America

9.5.1. Brazil

9.5.2. Mexico

9.5.3. Argentina

9.5.4. Chile

9.5.5. Colombia

9.5.6. Rest of Latin America

9.6. Middle East & Africa

9.6.1. UAE

9.6.2. Saudi Arabia

9.6.3. South Africa

9.6.4. Turkey

9.6.5. Rest of Middle East & Africa

10. Competitive Landscape

10.1. Overview

10.2. Key Growth Strategies

10.3. Competitive Benchmarking

10.4. Competitive Dashboard

10.4.1. Industry Leaders

10.4.2. Market Differentiators

10.4.3. Vanguards

10.4.4. Emerging Companies

10.5. Market Ranking/Positioning Analysis of Key Players, 2025

11. Company Profiles

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

11.1. Nestlé S.A.

11.2. Mars, Incorporated

11.3. Mondelez International

11.4. Lindt & Sprüngli

11.5. Barry Callebaut AG

11.6. Hershey Company

11.7. Ferrero Group

11.8. Hu Kitchen

11.9. Endangered Species Chocolate

11.10. Lily's Sweets

11.11. Alter Eco Foods

11.12. Theo Chocolate

11.13. Goodio Chocolate

11.14. Love Cocoa

11.15. Taza Chocolate

12. Appendix

12.1. Additional Customization

12.2. Related Report

Published Date: Feb-2026

Published Date: Jan-2025

Published Date: Nov-2022

Published Date: Jun-2023

Subscribe to get the latest industry updates