Resources

About Us

Ambient Food Packaging Market Size, Share & Trends Analysis by Material (Plastic, Paper & Paperboard, Metal, Glass), Packaging Type (Rigid, Flexible, Semi-Rigid), Technology (Aseptic Processing, Retort, MAP, Active, Intelligent/Smart, Vacuum), Application, and Geography — Global Opportunity Analysis and Industry Forecast (2026–2036)

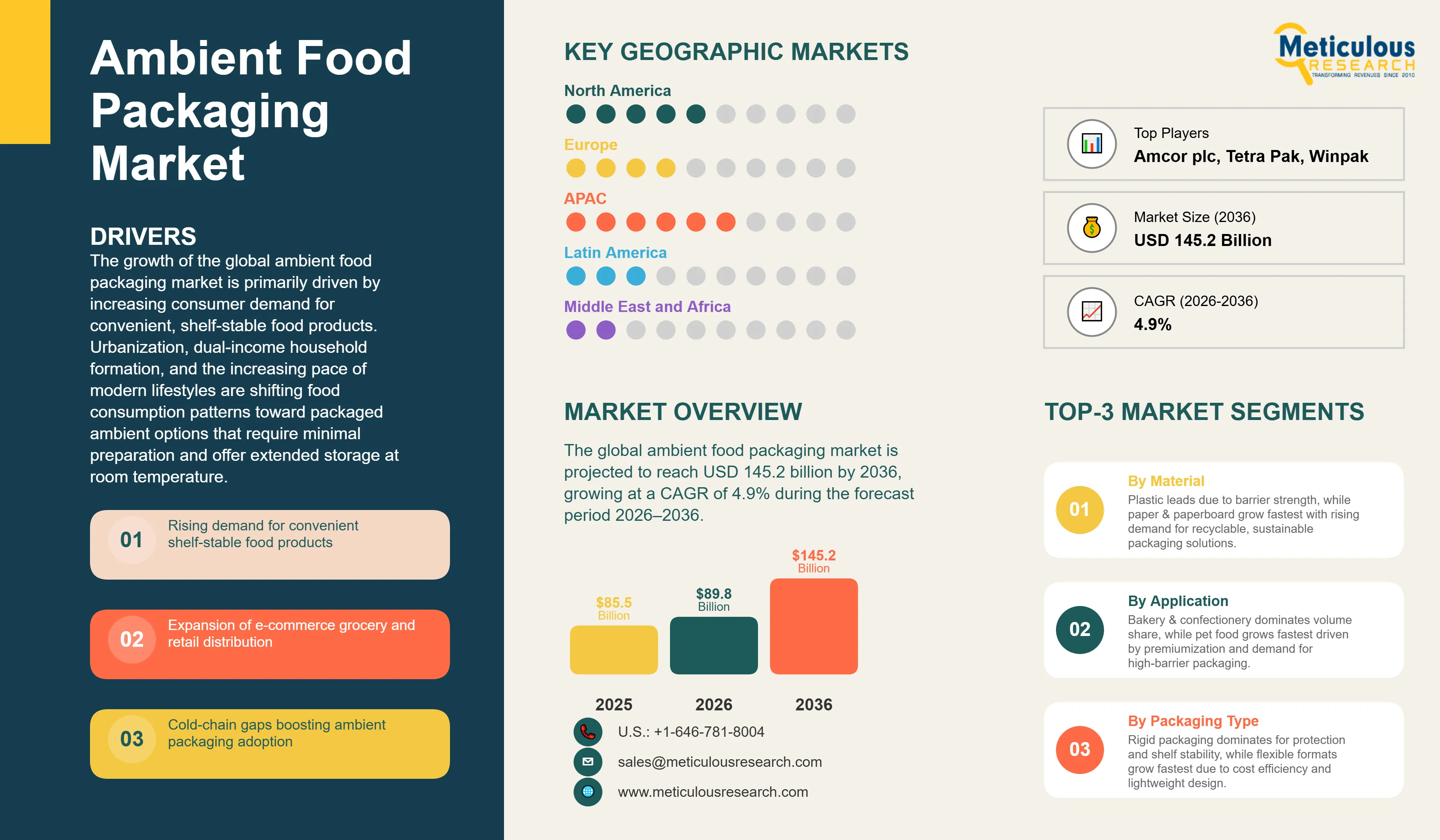

Report ID: MRFB - 1041919 Pages: 280 Apr-2026 Formats*: PDF Category: Food and Beverages Delivery: 24 to 72 Hours Download Free Sample ReportThe global ambient food packaging market was valued at USD 85.5 billion in 2025. The market is projected to reach USD 145.2 billion by 2036 from an estimated USD 89.8 billion in 2026, growing at a CAGR of 4.9% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

The global ambient food packaging market covers the packaging solutions designed to protect, preserve, and present food products that can be stored at room temperature without refrigeration. These are products whose shelf stability is achieved through thermal processing techniques, including aseptic processing, retort sterilization, and pasteurization, or through physical and chemical barriers that prevent microbial growth, oxidative deterioration, and moisture ingress. The market covers packaging materials including plastic (PET, PP, LDPE, multilayer films), paper and paperboard (including fiber-based aseptic cartons), metal (tinplate and aluminum cans, aerosol containers), and glass (jars, bottles), as well as the full range of rigid, semi-rigid, and flexible packaging formats used across dry foods, canned goods, snacks, sauces, condiments, ready-to-eat meals, pet food, beverages, and bakery products.

These packaging systems collectively serve as the primary enabler of long-distance food supply chains, pantry-stocking consumer behavior, food security in regions without consistent cold-chain infrastructure, and the expanding global e-commerce grocery sector.

The growth of the global ambient food packaging market is primarily driven by increasing consumer demand for convenient, shelf-stable food products. Urbanization, dual-income household formation, and the increasing pace of modern lifestyles are shifting food consumption patterns toward packaged ambient options that require minimal preparation and offer extended storage at room temperature.

The United Nations estimated the global urban population at approximately 4.4 billion around 2020, with this share projected to reach about 68% of the total global population by 2050, according to the UN Department of Economic and Social Affairs’ World Urbanization Prospects. This sustained urbanization trend directly expands the consumer base for packaged ambient foods and their packaging requirements.

Cold‑chain infrastructure gaps in developing and emerging markets remain a significant driver of the growth of the ambient packaging market. In rural and semi‑urban regions of South Asia, Southeast Asia, Sub‑Saharan Africa, and Latin America, limited refrigeration infrastructure at the retail and household level makes ambient food packaging not merely convenient but essential for safe food distribution and storage. The Food and Agriculture Organization of the United Nations (FAO) has estimated that approximately one‑third of all food produced globally for human consumption—around 1.3 billion metric tons per year—is lost or wasted, with a substantial share linked to inadequate packaging and cold‑chain failures in developing markets. Ambient packaging addresses this challenge directly by enabling temperature‑independent shelf‑life extension across distribution chains of variable quality.

The global e‑commerce grocery sector is also a significant growth driver for the ambient food packaging market. Online grocery shopping requires formats that can withstand mechanical stresses during automated picking, transit in distribution networks, and last‑mile delivery without compromising product integrity. Major retailers such as Walmart and Amazon Fresh have expanded their ambient shelf‑stable meal and snack offerings, driving higher demand for ambient packaging solutions that support the cost and reliability requirements of online grocery logistics.

At the same time, the market faces several notable restraints. The substantial use of single‑use plastic packaging in the ambient food sector has attracted mounting regulatory and consumer pressure across key regions. The EU Packaging and Packaging Waste Regulation (PPWR, Regulation (EU) 2025/40), which entered into force on 11 February 2025 and will generally apply from 12 August 2026, mandates that all packaging placed on the EU market must be recyclable by 2030 and introduces binding minimum recycled‑plastic content requirements, including 30% recycled content in PET packaging by 2030. These compliance obligations are generating substantial reformulation and capital‑investment needs for ambient food packaging manufacturers and brand owners, with associated risk of market disruption for packaging formats that cannot meet recyclability “grade C” or higher by the 2030 deadline.

Despite these challenges, the market offers substantial growth opportunities through the development and scaling of sustainable and bio‑based packaging materials. Consumer demand for packaging that is clearly recyclable, biodegradable, or made from post‑consumer recycled content is rising across major markets, pushing leading packaging companies to invest heavily in paper‑based, mono‑material plastic, and bio‑based alternatives to conventional multilayer structures.

A key market trend is the ongoing consolidation of the global packaging industry, with one of the most significant recent developments being the completed combination of Amcor and Berry Global in April–May 2025. The all‑stock transaction, valued at approximately USD 8.4 billion, created a packaging entity with combined annual revenues around USD 24 billion, operations in over 140 countries, and roughly 400 production facilities worldwide. This consolidation is expected to reshape competitive dynamics in the ambient food packaging market by integrating Amcor’s leadership in flexible films with Berry Global’s strengths in rigid containers and closures, forming a global packaging leader with unmatched scale and breadth across both rigid and flexible ambient packaging formats.

EU Packaging and Packaging Waste Regulation (PPWR) Reshaping Material and Design Strategies

One of the key trends shaping the global ambient food packaging market is the full implementation of the European Union’s Packaging and Packaging Waste Regulation (PPWR, Regulation (EU) 2025/40). Published in the Official Journal of the European Union in January 2025, entering into force on 11–12 February 2025, and applying broadly from 12 August 2026, the PPWR represents the most comprehensive overhaul of packaging legislation in the EU’s history and introduces directly binding standards across all 27 member states, replacing the previous Packaging Directive 94/62/EC.

For ambient food packaging specifically, the PPWR introduces several transformative requirements. All packaging placed on the EU market must be recyclable, with a de‑facto cut‑off defined by the recyclability grading system (A–C), such that grades A, B, and C are acceptable by 2030, while grade C will be phased out by 2038. Plastic packaging is subject to mandatory minimum recycled‑content requirements, including 30% recycled content in PET contact‑sensitive packaging (excluding single‑use plastic beverage bottles) by 2030, with further increases toward 2040. PFAS (per‑ and polyfluoroalkyl substances) are prohibited in food‑contact packaging from August 2026. Single‑use plastic packaging for individual portions of condiments and sauces for the HORECA sector is banned from 2030, a provision with direct implications for the large ambient condiment and sauce packaging segment. Mandatory harmonized labeling identifying material composition and recycling disposal instructions is required from 2026.

These requirements are driving significant near‑term investment by ambient food packaging manufacturers in material reformulation, packaging redesign, and recyclability‑assessment processes. Packaging companies serving the European market must now carry out formal conformity assessments, draw up EU declarations of conformity, and maintain technical documentation for five years for single‑use packaging. The PPWR’s scope extends to non‑EU exporters, requiring suppliers of packaged food to the EU market based outside the EU to ensure packaging compliance by established deadlines. This extraterritorial reach is creating compliance‑investment requirements across ambient food packaging manufacturers in Asia, North America, and Latin America that supply European retail chains, amplifying the regulation’s global market impact.

The PPWR is serving as a powerful driver of the shift toward paper‑based, monomaterial, and fully recyclable packaging innovations within the ambient food sector. In 2024, Danone introduced an ambient yogurt line in fiber‑based containers across several EU markets, aligning with the region’s evolving recyclability expectations and broader regulatory pressure on plastic‑heavy packaging formats. In 2024, Tesco collaborated with regional material‑science startups to develop home‑compostable ambient snack packaging while expanding its ambient vegan‑meal category, as part of a broader push to reduce hard‑to‑recycle plastics in its value chain. The Mondi Group, in February 2025, strengthened its partnership with the UN World Food Programme to deliver durable, transit‑ready packaging solutions, reflecting the intersection of stricter packaging‑regulation‑style expectations and broader humanitarian food‑security objectives.

Industry Consolidation and Strategic M&A Reshaping the Competitive Landscape

Another major trend in the global ambient food packaging market is the increasing wave of strategic mergers, acquisitions, and consolidation activity among leading packaging manufacturers. The most significant transaction has been the combination of Amcor plc with Berry Global, which was successfully completed in April 2025. The all-stock transaction, valued at approximately USD 8.4 billion, created a global packaging leader with combined annual revenues of around USD 24 billion, adjusted EBITDA of approximately USD 4.3 billion, operations across ~140 countries, and a manufacturing footprint of approximately 400 facilities worldwide. The combined company has identified USD 650 million in annual synergies to be realized by the end of the third year following the transaction.

This consolidation trend reflects the capital-intensive and scale-driven economics of the ambient food packaging industry, where sustained investment in sustainable materials R&D, aseptic filling technologies, recyclability-driven reformulation, and global supply chain infrastructure increasingly favors large, integrated players. As a result, smaller and regional packaging manufacturers are facing rising competitive pressure to consolidate, expand strategically, or focus on high-value niche applications in order to remain competitive against global leaders such as Mondi Group, Sealed Air Corporation, Huhtamäki Oyj, and SIG Group AG.

In parallel, strategic partnerships between packaging manufacturers and food brands are becoming increasingly important, particularly in the development of recyclable, paper-based, and sustainability-led packaging formats. These collaborations highlight the growing integration of packaging innovation into branded food manufacturers’ sustainability, compliance, and supply chain strategies.

|

Parameters |

Details |

|---|---|

|

Market Size by 2036 |

USD 145.2 Billion |

|

Market Size in 2026 |

USD 89.8 Billion |

|

Market Size in 2025 |

USD 85.5 Billion |

|

Revenue Growth Rate (2026–2036) |

CAGR of 4.9% |

|

Dominating Material |

Plastic |

|

Fastest Growing Material |

Paper & Paperboard |

|

Dominating Packaging Type |

Rigid Packaging |

|

Fastest Growing Packaging Type |

Flexible Packaging |

|

Dominating Technology |

Aseptic Processing & Packaging |

|

Fastest Growing Technology |

Active & Intelligent Packaging |

|

Dominating Application |

Bakery & Confectionery |

|

Fastest Growing Application |

Pet Food |

|

Dominating Geography |

Asia Pacific |

|

Fastest Growing Geography |

North America |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

By Material: In 2026, Plastic to Dominate the Global Ambient Food Packaging Market

Based on material, the global ambient food packaging market is segmented into plastic, paper & paperboard, metal, glass, and other materials. In 2026, the plastic segment is expected to account for the largest share of the overall ambient food packaging market.

The large share of this segment is primarily attributed to the superior barrier performance of plastic materials against moisture, oxygen, light, and microbial contamination. Materials such as PET (polyethylene terephthalate) and PP (polypropylene) continue to remain the dominant plastic substrates in ambient food packaging applications due to their strong gas barrier properties, thermal processing compatibility, and versatility across both rigid and flexible packaging formats. Plastic continues to account for the largest share of the broader food packaging material market, reflecting its established functional and cost advantages across shelf-stable food applications.

The dominance of plastic is further supported by its compatibility with aseptic filling lines, retort sterilization processes, and modified atmosphere packaging (MAP) systems. In addition, multilayer plastic films incorporating high-barrier layers such as EVOH (ethylene vinyl alcohol) are widely used in ambient packaging formats for sauces, ready-to-eat meals, meat products, and pet food, where extended shelf life at room temperature is a critical performance requirement.

However, the Paper & Paperboard segment is projected to register the highest CAGR during the forecast period. The strong growth of this segment is primarily driven by the increasing shift toward fiber-based packaging solutions as brands and retailers respond to sustainability targets, consumer preferences, and tightening regulatory requirements. The EU Packaging and Packaging Waste Regulation (PPWR) requires all packaging placed on the market to be recyclable by 2030, which is significantly increasing investment in paper-based alternatives across ambient food applications.

Key innovations include high-barrier coated paper packaging, fiber-based aseptic cartons for beverages and soups, and paperboard trays with sealed lidding films for ready meals. Continued advancements in mineral-coated and bio-based barrier technologies are expected to further improve the commercial viability of paper-based ambient packaging formats.

By Packaging Type: In 2026, Rigid Packaging to Account for the Largest Share

Based on packaging type, the global ambient food packaging market is segmented into Rigid Packaging (including cans, bottles, jars, cartons, trays, and pots), flexible packaging (including pouches, sachets, films, wraps, and bags), and semi-rigid packaging. In 2026, the Rigid Packaging segment is expected to account for the largest share of the global ambient food packaging market in value terms.

The large share of this segment is primarily attributed to the established position of rigid formats, including metal cans, glass jars, PET bottles, and multilayer cartons, across high-value ambient food categories such as canned vegetables, fruits, meat and fish products, shelf-stable beverages, sauces and condiments, and ambient soups. Rigid packaging provides superior product protection, tamper evidence, and structural integrity throughout storage and transportation, making it the preferred format across premium and high-shelf-life applications.

Aseptic multilayer cartons, supplied by leading players such as Tetra Pak and SIG Group AG, represent a particularly significant sub-segment within rigid ambient packaging. These systems combine thermal processing, sterile filling, and hermetic sealing to enable the ambient distribution of soups, juices, plant-based beverages, and dairy alternatives without refrigeration.

However, the flexible packaging segment is projected to register the highest CAGR during the forecast period. The strong growth of this segment is primarily driven by material efficiency advantages, lower transportation weight, improved sustainability economics, and increasing consumer preference for resealable stand-up pouches and retort pouches across ready meals, sauces, and pet food applications.

By Technology: In 2026, Aseptic Processing & Packaging to Hold the Largest Share

Based on technology, the global ambient food packaging market is segmented into aseptic processing & packaging, retort processing, modified atmosphere packaging (MAP), active packaging, intelligent packaging, and vacuum packaging. In 2026, the aseptic processing & packaging segment is expected to account for the largest share of the global ambient food packaging market.

The large share of this segment is primarily driven by its established position as the dominant commercial technology for shelf-stable ambient food and beverage products globally. Aseptic processing involves the separate sterilization of the product and packaging material, followed by filling and sealing under sterile conditions. This process eliminates the need for post-fill thermal treatment and enables better preservation of nutritional content, color, texture, and organoleptic quality compared with conventional retort processing.

This performance advantage has made aseptic technology the preferred production method across liquid and semi-liquid ambient food categories, including soups, sauces, juices, plant-based beverages, dairy alternatives, and baby food. The growth of this segment is further driven by the large installed base of aseptic filling lines worldwide and the dominant market positions of Tetra Pak and SIG Group AG in integrated carton and filling-line systems, which continue to drive large-scale adoption across shelf-stable food and beverage applications.

However, the active & intelligent packaging market is poised to grow at the fastest CAGR during the forecast period. The strong growth of this segment is primarily driven by increasing deployment of oxygen scavengers, antimicrobial films, moisture-control systems, freshness indicators, RFID tags, and NFC-enabled traceability solutions across premium ambient food applications.

The commercial case for this segment is further strengthened by the need to reduce food loss and waste across long supply chains. According to the FAO, approximately 1.3 billion metric tons of food are lost or wasted annually worldwide, creating a strong economic and sustainability-driven case for packaging technologies that improve shelf life, freshness monitoring, and traceability.

By Application: In 2026, Bakery & Confectionery to Hold the Largest Share

Based on application, the global ambient food packaging market is segmented into bakery & confectionery, sauces, dressings & condiments, snacks & savory, ready-to-eat meals & soups, fruits & vegetables, meat, fish & poultry, pet food, and other applications. In 2026, the bakery & confectionery segment is expected to account for the largest share of the global ambient food packaging market.

The large share of this segment is primarily attributed to the substantial global consumption volume of packaged biscuits, cookies, crackers, chocolates, candies, cereal bars, and packaged cakes, the majority of which are distributed in ambient shelf-stable formats. Bakery and confectionery products represent one of the most widely consumed packaged food categories globally, with strong demand across both developed and emerging markets.

This segment utilizes a broad range of ambient packaging materials and formats, including flexible multilayer films and flow-wraps for biscuits and chocolates, rigid cartons and trays for premium confectionery products, and paper-based wraps for snack bars and bakery items. The high frequency of purchase, large SKU variety, and strong retail shelf presence collectively support the dominant market position of this segment.

The sauces, dressings & condiments segment is another major application area, driven by the wide use of glass jars, PET bottles, sachets, stand-up pouches, and portion-controlled packs across retail and foodservice channels. Ambient stability in this segment is commonly achieved through hot-fill, aseptic, and high-barrier packaging solutions.

However, the pet food segment is projected to register the highest CAGR during the forecast period. The strong growth of this segment is primarily driven by the rapid premiumization and humanization of pet food products, with increasing demand for high-protein, natural-ingredient, and premium packaged formats.

This trend is driving the adoption of high-barrier flexible pouches, retort pouches, and premium rigid packaging solutions that enhance shelf life, preserve nutritional quality, and support premium brand positioning. Growth in pet ownership, particularly across Asia Pacific and Latin America, is expected to further support demand for ambient pet food packaging over the forecast period.

Based on geography, the global ambient food packaging market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. In 2026, the Asia Pacific is expected to account for the largest share of the global ambient food packaging market.

Asia Pacific’s dominant position is primarily driven by its role as both one of the world’s largest food production regions and the largest consumer base for packaged ambient foods. The strong market position of this region is driven by large-scale food manufacturing, rapid urbanization, expanding modern retail and e-commerce grocery channels, and the continued need for shelf-stable food distribution across markets with uneven cold-chain infrastructure.

China, Japan, and India are the three major countries within the region, each supported by distinct demand drivers. China ambient food packaging market is driven by large-scale packaged food manufacturing, rapid growth in organized retail and digital grocery channels, and extensive distribution across urban and rural geographies, where ambient packaging remains the most practical preservation format. Japan is a premium and innovation-led market with strong adoption of aseptic cartons, retort pouches, and intelligent packaging solutions. India is emerging as a high-growth market for ambient food packaging, driven by rapid urbanization, rising middle-class consumption, retail formalization, and continued limitations in rural cold-chain penetration, making ambient packaging critical to nationwide food distribution.

However, North America ambient food packaging market is expected to register the fastest growth rate during the forecast period. The strong growth of North America is primarily driven by the continued expansion of e-commerce grocery retail and rising demand for packaging formats optimized for automated fulfillment, transportation durability, and shelf stability. According to the U.S. Census Bureau, total U.S. retail e-commerce sales exceeded USD 1.19 trillion in 2024, reflecting strong growth in online retail demand, including food and beverage categories. This continues to create strong incremental demand for ambient packaging solutions across ready meals, snacks, sauces, and shelf-stable beverages.

The region is also witnessing growing adoption of sustainable packaging materials, driven by state-level packaging legislation in California, Colorado, and other jurisdictions, as well as sustainability commitments from major retailers and food brands.

Europe is the most regulatory-intensive ambient food packaging market globally, with the EU Packaging and Packaging Waste Regulation (PPWR) entering into force in February 2025 and driving investment in recyclability-led redesign, material substitution, and extended producer responsibility (EPR) compliance systems. Countries such as Germany, France, and the U.K. continue to lead the region in sustainable ambient packaging adoption and eco-friendly material innovation.

The global ambient food packaging market is characterized by a moderately consolidated competitive landscape comprising large-scale integrated packaging companies with multi-material and multi-format capabilities, specialized aseptic and retort system providers, metal can and rigid container manufacturers, flexible packaging leaders, and emerging sustainable packaging innovators.

Competition in this market is primarily driven by scale advantages in raw material procurement, capital investment in filling-line and converting technologies, sustainability-led material innovation, and long-standing customer relationships with leading food and beverage brands.

Amcor plc remains one of the most prominent players in the market following the completion of its combination with Berry Global in 2025. The combined entity, with annual revenues of approximately USD 24 billion and operations across more than 140 countries, has further strengthened its position across flexible and specialty packaging solutions for ambient food applications. The company continues to invest in recyclable and high-barrier paper-based alternatives such as its AmFiber portfolio.

Tetra Pak and SIG Group AG are the leading players in aseptic carton packaging systems and integrated filling-line technologies, serving major global food and beverage brands across soups, sauces, dairy alternatives, juices, and baby food categories. Their integrated systems model creates strong long-term customer relationships and high switching barriers.

Mondi Group, Huhtamäki Oyj, Constantia Flexibles, and ProAmpac are key players across flexible and fiber-based packaging solutions, with increasing focus on recyclable and sustainability-driven packaging innovations.

The market also includes the strong presence of Crown Holdings, Inc. in metal cans, Silgan Holdings Inc. in rigid food containers, Sonoco Products Company and Graphic Packaging Holding Company in fiber-based packaging, Smurfit Kappa Group in paperboard solutions, and DuPont de Nemours, Inc. in high-barrier material technologies.

The report offers a comprehensive competitive analysis based on the assessment of leading players’ product portfolios, geographic presence, strategic initiatives, sustainability investments, and key growth strategies adopted over the past few years.

This report provides market size estimates and forecasts for each segment and sub-segment at the global, regional, and country levels. The report further offers an in-depth analysis of the latest industry trends, market dynamics, technological advancements, regulatory developments, and key strategic initiatives across each sub-segment for the forecast period 2026–2036.

For the purpose of this study, the global ambient food packaging market has been segmented based on material, packaging type, technology, application, and geography.

|

Segment |

Sub-Segments |

|---|---|

|

By Material |

Plastic, Paper & Paperboard, Metal, Glass, Other Materials |

|

By Packaging Type |

Rigid Packaging (Cans, Bottles, Jars, Trays, Cartons), Flexible Packaging (Pouches, Sachets, Films, Wraps), Semi-Rigid Packaging |

|

By Technology |

Aseptic Processing & Packaging, Retort Processing, Modified Atmosphere Packaging (MAP), Active Packaging, Intelligent / Smart Packaging, Vacuum Packaging |

|

By Application |

Bakery & Confectionery, Sauces, Dressings & Condiments, Snacks & Savory, Ready-to-Eat Meals & Soups, Fruits & Vegetables, Meat, Fish & Poultry, Pet Food, Other Applications |

|

By Geography |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

By Material (Revenue, USD Billion, 2026–2036)

By Packaging Type (Revenue, USD Billion, 2026–2036)

By Technology (Revenue, USD Billion, 2026–2036)

By Application (Revenue, USD Billion, 2026–2036)

By Geography (Revenue, USD Billion, 2026–2036)

The global ambient food packaging market is expected to reach USD 145.2 billion by 2036 from an estimated USD 89.8 billion in 2026, at a CAGR of 4.9% during the forecast period 2026–2036.

In 2026, plastic is expected to hold the largest market share, driven by its superior barrier properties against moisture, gases, and contaminants, its compatibility with all major ambient packaging formats and thermal processing technologies, and its established cost efficiency across global ambient food packaging applications.

Paper & paperboard is expected to register the highest CAGR during the forecast period 2026–2036, driven by the accelerating adoption of fiber-based alternatives to plastic packaging across global food brands and the binding mandates of the EU Packaging and Packaging Waste Regulation (PPWR, EU 2025/40).

In 2026, the rigid packaging segment is expected to hold the largest market share, driven by the dominant commercial position of cans, bottles, jars, and aseptic cartons across high-value ambient food categories including canned goods, beverages, sauces, and ready-to-eat meals.

In 2026, the aseptic processing and packaging segment is expected to hold the largest market share of the global ambient food packaging market, driven by its established dominance as the primary production technology for shelf-stable ambient liquid foods and beverages globally.

The growth of this market is primarily driven by increasing global demand for convenient, shelf-stable food products fueled by urbanization and busy consumer lifestyles; cold-chain infrastructure gaps in developing markets that make ambient packaging essential for safe food distribution; the rapid expansion of e-commerce grocery retail requiring robust ambient packaging; the premiumization of pet food and snack categories; and continuous technological advancement in barrier materials, aseptic processing, and active and intelligent packaging that extends shelf life and reduces food waste.

Key players in the global ambient food packaging market include Amcor plc (Switzerland/Australia), Tetra Pak International S.A. (Switzerland), Mondi Group (South Africa/UK), SIG Group AG (Switzerland), Sealed Air Corporation (U.S.), Huhtamäki Oyj (Finland), Constantia Flexibles (Austria), Crown Holdings, Inc. (U.S.), Sonoco Products Company (U.S.), Graphic Packaging Holding Company (U.S.), Smurfit Kappa Group (Ireland), DuPont de Nemours, Inc. (U.S.), Silgan Holdings Inc. (U.S.), ProAmpac Holdings Inc. (U.S.), and Winpak Ltd. (Canada).

North America is expected to register the highest growth rate in the global ambient food packaging market during the forecast period 2026–2036, driven by e-commerce grocery expansion, accelerating adoption of sustainable ambient packaging materials, and private-label ambient food growth across major retail channels.

Published Date: Feb-2026

Published Date: Nov-2024

Published Date: Feb-2026

Published Date: Jan-2025

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates