Resources

About Us

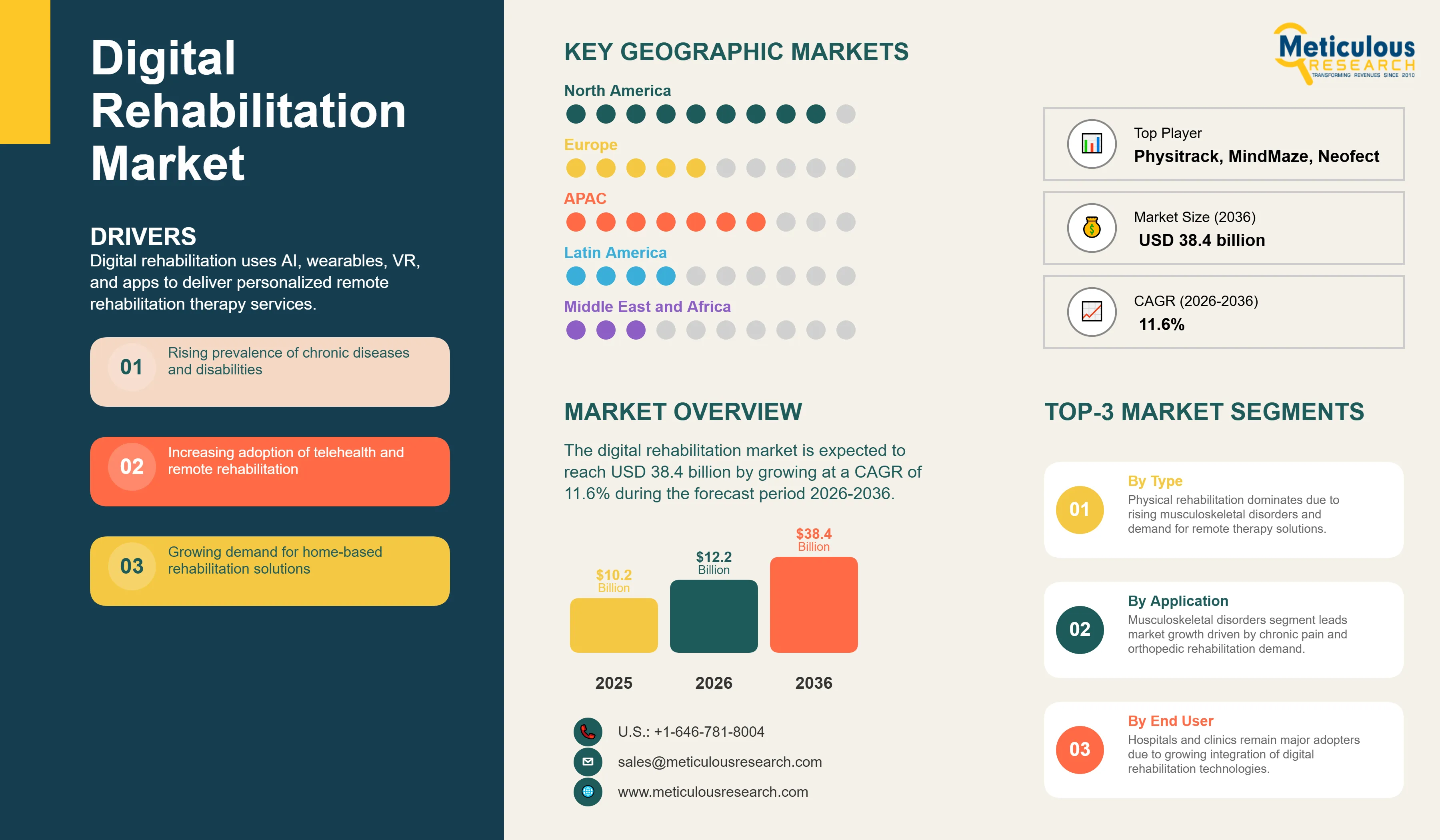

The global digital rehabilitation market was valued at USD 10.2 billion in 2025. This market is expected to reach USD 38.4 billion by 2036 from an estimated USD 12.8 billion in 2026, growing at a CAGR of 11.6% during the forecast period 2026-2036. According to the World Health Organization's World Report on Disability, approximately 1.3 billion people globally, representing 16% of the world's population, live with some form of significant disability and many of these individuals require rehabilitation services at some point in their lives. The WHO further estimates that more than 2.4 billion people globally live with a health condition that could benefit from rehabilitation, yet the majority lack access to adequate rehabilitation care, establishing both the scale of clinical need and the commercial opportunity for digital solutions that extend rehabilitation access.

Market Overview and Insights

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Digital rehabilitation refers to the use of digital technologies including software platforms, wearable sensors, virtual reality headsets, artificial intelligence, and mobile applications to deliver, monitor, and personalize rehabilitation therapy outside of or in addition to traditional in-person clinical settings. Where conventional rehabilitation requires a patient to travel to a clinic or hospital for each therapy session under the direct supervision of a physiotherapist, occupational therapist, or speech-language pathologist, digital rehabilitation enables therapy sessions to be conducted remotely via video consultation, guided exercise programs delivered through smartphone apps, motion analysis performed by wearable sensors worn at home, and cognitive training administered through gamified digital platforms that can adapt in real time to patient performance.

The market is growing rapidly because the unmet need for rehabilitation is extraordinary in scale. According to the WHO's Rehabilitation in Health Systems guidance, about 2.4 billion people globally could benefit from rehabilitation, and it emphasizes that access remains insufficient in many countries, especially low- and middle-income settings. In developed markets, rehabilitation waiting times at major healthcare systems have been growing as the volume of patients requiring rehabilitation post-surgery, post-stroke, post-COVID, and for chronic musculoskeletal conditions grows faster than therapist and facility capacity. According to Hinge Health's 2025 employer benefits report, musculoskeletal conditions are the leading cost driver in U.S. employer healthcare spending, accounting for approximately USD 380 billion in annual costs, and digital musculoskeletal rehabilitation programs delivered to employees at home have demonstrated clinically meaningful pain reduction and return-to-work improvements in multiple published studies.

Two developments are defining the market's current growth phase. The sustained post-pandemic expansion of telehealth reimbursement in the United States and Europe has created the billing infrastructure through which digital rehabilitation programs can be commercially sustained at scale, with the Centers for Medicare and Medicaid Services maintaining expanded telehealth coverage for rehabilitation therapy services that were introduced as temporary pandemic measures and made permanent or extended through subsequent legislation. Simultaneously, the clinical validation of AI-driven personalized rehabilitation programs, which adapt exercise intensity, progression, and content based on patient performance data analyzed in real time, is generating outcomes evidence that is progressively satisfying payer evidence standards for coverage decisions.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 38.4 Billion |

|

Market Size in 2026 |

USD 12.8 Billion |

|

Market Size in 2025 |

USD 10.2 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 11.6% |

|

Dominating Therapy Type |

Physical Rehabilitation |

|

Fastest Growing Therapy Type |

Cognitive Rehabilitation |

|

Dominating Technology Type |

Tele-rehabilitation Platforms |

|

Fastest Growing Technology Type |

VR/AR-based Rehabilitation Systems |

|

Dominating Delivery Mode |

Home-based Rehabilitation |

|

Fastest Growing Delivery Mode |

Home-based Rehabilitation |

|

Dominating Application |

Musculoskeletal Disorders |

|

Fastest Growing Application |

Neurological Disorders (Stroke) |

|

Dominating End User |

Hospitals & Clinics |

|

Fastest Growing End User |

Home Care Settings |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Hinge Health and Sword Health Demonstrating the Commercial Scale of Digital MSK Rehabilitation

The musculoskeletal digital rehabilitation market has been defined commercially by the rapid growth of two U.S.-based digital health companies that have demonstrated employer-funded digital MSK programs can achieve both clinical outcomes and financial returns that justify large-scale deployment. Hinge Health, which provides digital physical therapy programs for back, hip, and knee conditions through employer health benefits, raised capital at a valuation exceeding USD 6 billion in 2021 and filed for an initial public offering in 2025, representing one of the largest digital health companies globally. According to Hinge Health's 2025 clinical evidence publications, its digital MSK program demonstrated significant pain reduction and functional improvement in a randomized controlled trial compared with usual care, providing the clinical evidence that justifies employer and payer coverage.

Sword Health, a Portuguese-founded digital physical therapy company, reported strong clinical and operational outcomes in 2025, including reduced work interruption, avoided in-person care time, and fewer surgeries, reinforcing the value of home-based digital MSK rehabilitation, and has expanded its platform to include digital physical therapy, pelvic health, and a bloom women's health program. Together, Hinge Health and Sword Health have collectively deployed digital MSK rehabilitation to tens of millions of employees through large U.S. employer health benefit programs including several Fortune 500 companies, establishing employer-funded digital MSK rehabilitation as the largest single commercial deployment channel in the digital rehabilitation market. The commercial success of this model is attracting additional investment and competitors across multiple MSK subspecialties.

VR Rehabilitation Achieving Clinical Validation for Neurological and Orthopedic Applications

Virtual reality (VR)-based rehabilitation has transitioned from a research-driven concept to a clinically validated approach in neurological and orthopedic care. Supported by a growing body of randomized controlled trial evidence and regulatory clearances, VR systems are increasingly being integrated into routine rehabilitation practice. Their clinical effectiveness is rooted in the ability to stimulate neuroplasticity through immersive, interactive environments that provide real-time multisensory feedback. This enables higher patient engagement, increased therapy intensity, and task-specific training that closely mirrors real-world functional activities—particularly beneficial in conditions such as stroke and musculoskeletal disorders.

Leading companies such as MindMaze, Hocoma AG, Tyromotion GmbH, and Neofect are advancing the commercialization of VR rehabilitation solutions, reflecting growing demand from clinical centers for evidence-based technologies. Research published in journals like the Journal of NeuroEngineering and Rehabilitation further supports the effectiveness of VR interventions in improving motor outcomes. At the same time, advancements in VR hardware affordability and usability are lowering adoption barriers, enabling broader integration of VR into rehabilitation workflows and positioning it as a key component of next-generation therapy models.

AI-driven Personalized Rehabilitation Improving Outcomes and Adherence

Artificial intelligence-powered rehabilitation platforms that automatically adjust therapy content, exercise progression, and session duration based on continuous analysis of patient performance data are demonstrating meaningful improvements in both clinical outcomes and patient adherence compared with static protocol-based digital programs. In conventional home exercise programs, the most significant clinical problem is that patients perform exercises incorrectly without real-time feedback from a therapist, developing compensatory movement patterns that reduce therapeutic benefit or cause injury. AI-powered motion analysis systems, which use camera-based or wearable sensor-based computer vision to track joint angles and movement quality during exercises and provide real-time corrective feedback, are addressing this limitation.

Kaia Health's AI-driven digital musculoskeletal therapy platform uses motion analysis through a smartphone camera to assess exercise form and automatically adjusts programs based on patient performance, and according to Kaia Health's 2025 published clinical evidence, its platform demonstrated significant improvements in both pain reduction and patient adherence compared with control groups. Physitrack, which is used by over 12,000 healthcare professionals according to its 2025 platform statistics, provides therapist-prescribed home exercise programs with outcome tracking that enables therapists to monitor patient progress between sessions and adjust programs remotely. The integration of AI into rehabilitation platforms is also enabling more precise risk stratification, identifying patients at highest risk of non-adherence or adverse events for proactive therapist outreach, improving the efficiency of therapist time across large patient panels.

Rising Prevalence of Chronic Diseases and Disabilities

According to the WHO's World Report on Disability, approximately 1.3 billion people globally live with significant disability, and more than 2.4 billion people have health conditions that would benefit from rehabilitation. The prevalence of the conditions that most commonly require rehabilitation is growing: according to the American Heart Association's 2025 Heart Disease and Stroke Statistics Update, approximately 795,000 Americans experience a new stroke each year, with the majority requiring rehabilitation for motor, cognitive, or speech deficits. The American Academy of Orthopaedic Surgeons reported that musculoskeletal conditions affect over 150 million Americans and result in over 130 million physician visits annually according to their 2025 data, with post-surgical and chronic pain rehabilitation representing very large and growing rehabilitation service demands. The global aging population trend, with the WHO projecting that the number of people aged 60 and above will reach 2.1 billion by 2050, will sustain long-term rehabilitation demand growth as older adults have higher rates of stroke, joint replacement, and functional decline requiring rehabilitation.

Increasing Adoption of Telehealth and Remote Care

The telehealth expansion triggered by the COVID-19 pandemic permanently elevated the baseline of digital care delivery in healthcare systems globally, and rehabilitation was one of the most actively adopted telehealth modalities. According to the American Hospital Association's 2025 Telehealth Report, telehealth utilization in the United States remained at levels multiple times above pre-pandemic baselines in 2024, with physical therapy and rehabilitation representing one of the highest-volume telehealth service categories. The CMS's extension of telehealth reimbursement for rehabilitation therapy through the Consolidated Appropriations Act 2023 and subsequent extensions, which maintained the expanded Medicare coverage for telehealth PT, OT, and speech therapy that was introduced as pandemic emergency measures, provided the reimbursement foundation that digital rehabilitation companies needed to build commercially sustainable business models in the U.S. market. European healthcare systems have similarly expanded telerehabilitation coverage through national digital health strategies, with Germany's Digital Care Act and France's digital health strategy both including telerehabilitation as covered services.

Expansion of Remote Monitoring and AI-driven Therapy

Remote patient monitoring integrated with rehabilitation program delivery is creating a new tier of digital rehabilitation capability that provides continuous between-session visibility into patient activity, recovery progress, and potential complications that conventional once or twice-weekly clinic visits cannot capture. Wearable sensors worn throughout the day can track joint range of motion, gait parameters, activity levels, and pain-associated behaviors that provide rehabilitation therapists with a far richer picture of patient recovery than the in-clinic snapshot of a scheduled appointment. According to a 2025 report by the American Physical Therapy Association, digital rehabilitation platforms with integrated remote monitoring are demonstrating improved clinical outcomes and higher patient satisfaction compared with conventional rehabilitation in studies across orthopedic, neurological, and cardiopulmonary rehabilitation, creating a growing evidence base that is supporting payer coverage decisions.

Growth in Aging Population

The global aging population creates one of the most sustained and predictable long-term demand drivers for digital rehabilitation, as older adults have the highest rates of conditions requiring rehabilitation including hip and knee replacement surgery, stroke, Parkinson's disease, and fall-related injuries. According to the WHO's World Ageing Population 2024 report, the global population aged 65 and above reached approximately 703 million in 2023 and is projected to more than double to approximately 1.6 billion by 2050. In Japan, where 29% of the population was aged 65 and above per the Statistics Bureau of Japan's 2025 data, the demand for rehabilitation services is already among the world's highest per capita, and home-based digital rehabilitation is particularly valuable for this demographic because it eliminates the transportation and mobility barriers that make clinic attendance difficult for older adults with limited mobility. Digital geriatric rehabilitation programs specifically addressing fall prevention, balance training, and post-hip-replacement recovery are among the fastest-growing product categories in the digital rehabilitation market.

By Therapy Type: In 2026, Physical Rehabilitation to Hold the Largest Share

Based on therapy type, the global digital rehabilitation market is segmented into physical rehabilitation, cognitive rehabilitation, speech and language therapy, occupational therapy, and other therapies. In 2026, the physical rehabilitation segment is expected to account for the largest share of the global digital rehabilitation market. Physical rehabilitation for musculoskeletal conditions, post-surgical recovery, and neurological motor deficits represents by far the largest rehabilitation service category by patient volume globally, and the digital physical therapy market has been validated commercially by the large-scale employer deployment of Hinge Health and Sword Health programs reaching tens of millions of employees. According to Hinge Health's 2025 employer benefits data, musculoskeletal conditions are the leading driver of U.S. employer healthcare costs at approximately USD 380 billion annually, making digital physical therapy the highest-value digital rehabilitation investment for payers and employers.

However, the cognitive rehabilitation segment is projected to register the highest CAGR during the forecast period. The growing global prevalence of dementia, traumatic brain injury, stroke-related cognitive deficits, and the emerging recognition of post-COVID cognitive impairment as a significant and lasting condition in a substantial proportion of COVID-19 survivors are all driving growing demand for cognitive rehabilitation. According to Alzheimer's Disease International's World Alzheimer Report 2024, approximately 55 million people (can rise to 139 million by 2050) globally live with dementia, with 10 million new cases diagnosed annually, establishing cognitive rehabilitation as one of the fastest-growing rehabilitation need categories and driving investment in digital cognitive therapy platforms.

By Technology Type: In 2026, Tele-rehabilitation Platforms to Hold the Largest Share

Based on technology type, the global digital rehabilitation market is segmented into tele-rehabilitation platforms, VR/AR-based rehabilitation systems, AI-based rehabilitation systems, wearable and sensor-based systems, and mobile applications. In 2026, the tele-rehabilitation platforms segment is expected to account for the largest share of the global digital rehabilitation market. Tele-rehabilitation platforms that enable video-based therapist consultation, exercise prescription, home exercise program delivery, and patient-therapist communication represent the most broadly deployed digital rehabilitation technology, having been rapidly adopted by rehabilitation providers during the COVID-19 pandemic and sustained at high utilization rates by both therapist preference and patient demand since. Physitrack, Sword Health's clinical platform, and Hinge Health's provider tools are all tele-rehabilitation platform examples with large commercial deployments.

However, the VR/AR-based rehabilitation systems segment is projected to register the highest CAGR during the forecast period. The combination of growing clinical evidence from randomized controlled trials, FDA clearances for specific VR rehabilitation indications, and the rapidly declining cost of VR hardware is driving accelerating adoption of VR rehabilitation systems in neurological and orthopedic rehabilitation settings. The 2025 meta-analysis in the Journal of NeuroEngineering and Rehabilitation confirming VR superiority over conventional therapy for stroke upper limb rehabilitation at matched therapy time is a key evidence foundation for growing clinical and payer acceptance of VR rehabilitation investment.

By Delivery Mode: In 2026, Home-based Rehabilitation to Hold the Largest Share and Grow the Fastest

Based on delivery mode, the global digital rehabilitation market is segmented into home-based rehabilitation, clinic-based digital rehabilitation, and hybrid models. In 2026, the home-based rehabilitation segment is expected to account for the largest share of the global digital rehabilitation market and is also projected to register the highest CAGR during the forecast period, making it the dominant segment on both measures simultaneously. Home-based digital rehabilitation is the application that most directly and uniquely exploits the value proposition of digital technology: extending therapy access to patients who cannot or prefer not to attend clinic-based sessions. According to the American Hospital Association's 2025 data, home-based care continues to grow as both patients and payers recognize the cost and convenience advantages of managing rehabilitation in the home environment. Hinge Health's and Sword Health's multi-billion dollar commercial valuations are built entirely on home-based digital rehabilitation delivered to employees' homes without requiring any clinic visit for the majority of their patient population.

Clinic-based digital rehabilitation, where digital technologies including VR systems, robotic rehabilitation devices, and AI-powered motion analysis are deployed within clinical rehabilitation facilities, represents a complementary segment that benefits from the clinical environment's ability to support more complex technology deployments and more intensive supervision. Hybrid models that combine initial clinic-based assessment and setup with ongoing home-based digital monitoring are expected to become the mainstream delivery approach for complex rehabilitation programs as the evidence base and reimbursement infrastructure for digital rehabilitation matures.

By Application: In 2026, Musculoskeletal Disorders to Hold the Largest Share

Based on application, the global digital rehabilitation market is segmented into neurological disorders (stroke rehabilitation, Parkinson's disease, and multiple sclerosis), musculoskeletal disorders (orthopedic rehabilitation and sports injury rehabilitation), cardiopulmonary rehabilitation, pediatric rehabilitation, geriatric rehabilitation, and other applications. In 2026, the musculoskeletal disorders segment is expected to account for the largest share of the global digital rehabilitation market. MSK conditions including back pain, osteoarthritis, rotator cuff injuries, and post-joint-replacement recovery represent the highest-volume rehabilitation indication category globally, and the large-scale commercial validation of digital MSK rehabilitation through employer-funded Hinge Health and Sword Health programs has established this as the most commercially mature digital rehabilitation application. According to Hinge Health's 2025 employer data, MSK conditions affect approximately 1 in 3 U.S. adults and account for the largest single category of employer healthcare costs.

However, the neurological disorders segment, particularly stroke rehabilitation, is projected to register the highest CAGR during the forecast period. The very large global stroke incidence, with the American Heart Association's 2025 update documenting approximately 795,000 new U.S. strokes annually and the WHO estimating approximately 12 million stroke events globally per year, combined with the growing clinical evidence for VR and AI-assisted neurological rehabilitation superiority over conventional care, is driving rapid investment and adoption in digital neurological rehabilitation. The 2025 Journal of NeuroEngineering and Rehabilitation meta-analysis confirming VR efficacy in stroke rehabilitation is a key driver of neurological application adoption.

By End User: In 2026, Hospitals & Clinics to Hold the Largest Share

Based on end user, the global digital rehabilitation market is segmented into hospitals and clinics, rehabilitation centers, home care settings, and research institutes. In 2026, the hospitals and clinics segment is expected to account for the largest share of the global digital rehabilitation market. Hospitals and healthcare systems represent the largest institutional purchasers of digital rehabilitation platforms and devices because they serve the broadest patient population across all rehabilitation indications and are the primary entry point for patients requiring rehabilitation following surgery, stroke, injury, or acute illness. Hospital systems are also the leading adopters of VR rehabilitation systems and robotic rehabilitation devices due to the capital investment involved. Major hospital systems including Mayo Clinic, Cleveland Clinic, and the NHS have all announced digital rehabilitation strategy programs that incorporate multiple digital rehabilitation technologies.

However, the home care settings segment is projected to register the highest CAGR during the forecast period. The sustained shift of rehabilitation care toward home settings, supported by telehealth reimbursement infrastructure, patient preference for home-based care, and payer preference for lower-cost care settings, is driving home care as the fastest-growing end user category. According to the CMS's 2025 Home Health Agency Data, home health visits incorporating rehabilitation therapy grew at above-average rates in 2024, and the integration of digital rehabilitation platforms into home health agency workflows is a growing commercial priority for digital rehabilitation companies.

Digital Rehabilitation Market by Region: North America Leading by Share, Asia-Pacific by Growth

Based on geography, the global digital rehabilitation market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

In 2026, North America is expected to account for the largest share of the global digital rehabilitation market. The United States is the world's most commercially advanced digital rehabilitation market, home to the leading digital MSK rehabilitation companies Hinge Health and Sword Health, and benefiting from the most developed telehealth reimbursement infrastructure of any major healthcare system. According to the American Hospital Association's 2025 Telehealth Report, telehealth utilization in the U.S. remained at levels multiple times above pre-pandemic baselines in 2024, providing the access and billing infrastructure through which digital rehabilitation is delivered and reimbursed. The CMS's extension of telehealth coverage for rehabilitation therapy services provides the Medicare reimbursement framework that enables digital rehabilitation providers to serve the large and growing U.S. older adult population. The U.S. employer health benefits market represents a particularly large and growing digital rehabilitation procurement channel, with major self-insured employers including large technology, financial, and manufacturing companies integrating digital MSK programs into their health benefits offerings through partnerships with Hinge Health, Sword Health, and competing platforms. According to the International Foundation of Employee Benefit Plans' 2025 survey, digital musculoskeletal rehabilitation was the most commonly adopted digital health benefit among large U.S. employers in 2024.

However, the Asia-Pacific digital rehabilitation market is expected to grow at the fastest CAGR during the forecast period. Asia-Pacific has the world's largest aging population by absolute number and carries a very large rehabilitation service demand that is substantially unmet by conventional clinic-based rehabilitation systems. According to the WHO's Global Rehabilitation Needs Assessment 2024, Asia-Pacific has the world's largest rehabilitation need gap, with a very large proportion of people who need rehabilitation unable to access it due to geographic distance, cost, and workforce shortages. Japan's exceptional aging demographics, with 29% of its population aged 65 and above per the Statistics Bureau of Japan's 2025 data, and its well-developed national health insurance system that is progressively covering digital health services, make Japan a strong early-adopter market for digital geriatric rehabilitation. China is investing heavily in digital health infrastructure through its Healthy China 2030 initiative, which specifically addresses the need to expand rehabilitation services through digital means to address the country's growing chronic disease and disability burden. South Korea's advanced digital health ecosystem and high smartphone penetration create favorable conditions for mobile rehabilitation app adoption, and Australia's significant digital health investment through its My Health Record infrastructure and National Telehealth initiatives supports digital rehabilitation growth.

Key Players in the Global Digital Rehabilitation Market

The digital rehabilitation market is served by digital health platform companies providing software-based rehabilitation programs, medical device and robotics companies developing technology-enhanced rehabilitation equipment, and traditional rehabilitation technology companies adding digital capabilities to their product portfolios. Competition varies significantly by segment: in digital MSK rehabilitation, competition is primarily among software platform companies on clinical outcomes evidence, user experience, and employer and payer relationships; in robotic and VR rehabilitation, competition is primarily on clinical efficacy evidence, device performance, and clinical service support.

The report provides a comprehensive competitive analysis based on a thorough review of leading players' clinical evidence portfolios, product capabilities, commercial deployments, and recent strategic developments. Some of the key players operating in the global digital rehabilitation market include Reflexion Health (U.S.), Hinge Health (U.S.), Sword Health (U.S.), Kaia Health (Germany/U.S.), RehabGuru (Australia), Physitrack (UK/Australia), MIRA Rehab (UK), MindMaze (Switzerland), Hocoma AG (Switzerland), Ekso Bionics (U.S.), Neofect (South Korea/U.S.), Tyromotion GmbH (Austria), Bioness Inc. (U.S.), and Motek Medical (Netherlands), among others.

The global digital rehabilitation market is expected to reach USD 38.4 billion by 2036 from an estimated USD 12.8 billion in 2026, at a CAGR of 11.6% during the forecast period 2026-2036.

In 2026, the physical rehabilitation segment is expected to hold the largest share, anchored by digital MSK rehabilitation being the most commercially validated digital rehabilitation modality, with Hinge Health and Sword Health having collectively deployed to tens of millions of employees and with MSK conditions accounting for approximately USD 380 billion in annual U.S. employer healthcare costs per Hinge Health's 2025 data.

The VR/AR-based rehabilitation systems segment is projected to register the highest CAGR, driven by a 2025 meta-analysis in the Journal of NeuroEngineering and Rehabilitation confirming VR superiority over conventional therapy for stroke upper limb rehabilitation, FDA clearances for multiple VR rehabilitation systems, and rapidly declining VR hardware costs making clinical deployment financially viable.

Home-based rehabilitation is both the largest segment and the fastest-growing segment simultaneously, reflecting that the fundamental commercial value proposition of digital rehabilitation is extending therapy access to patients' homes, removing travel and schedule barriers, and reducing costs versus clinic-based care. CMS 2025 Home Health Agency Data confirming above-average growth in rehabilitation-incorporating home health visits supports this dominance.

The market is primarily driven by the WHO's World Report on Disability documenting that more than 2.4 billion people globally have conditions benefiting from rehabilitation with majority lacking access, creating an enormous unmet need that digital solutions uniquely address, combined with the sustained post-pandemic telehealth reimbursement infrastructure and the commercial validation of digital MSK rehabilitation at scale through Hinge Health and Sword Health's multi-billion-dollar employer deployments.

Key players are Reflexion Health (U.S.), Hinge Health (U.S.), Sword Health (U.S.), Kaia Health (Germany/U.S.), RehabGuru (Australia), Physitrack (UK/Australia), MIRA Rehab (UK), MindMaze (Switzerland), Hocoma AG (Switzerland), Ekso Bionics (U.S.), Neofect (South Korea/U.S.), Tyromotion GmbH (Austria), Bioness Inc. (U.S.), and Motek Medical (Netherlands), among others.

Asia-Pacific is expected to register the highest growth rate in the global digital rehabilitation market during the forecast period. The region’s growth is driven by a significant unmet need for rehabilitation services, as highlighted by the World Health Organization, which identifies Asia-Pacific as having one of the largest gaps between rehabilitation demand and service availability. This creates strong momentum for scalable, technology-enabled rehabilitation solutions.

1. Introduction

1.1 Market Definition

1.2 Scope

1.3 Market Ecosystem

1.4 Currency and Limitations

1.4.1 Currency

1.4.2 Limitations

1.5 Key Stakeholders

2. Research Methodology

2.1 Research Approach

2.2 Data Collection & Validation

2.2.1 Secondary Research

2.2.2 Primary Research

2.3 Market Estimation

2.3.1 Bottom-Up Approach

2.3.2 Top-Down Approach

2.3.3 Forecast Modelling

2.4 Data Triangulation

2.5 Assumptions

3. Executive Summary

4. Market Overview

4.1 Introduction

4.2 Market Dynamics

4.2.1 Drivers

4.2.1.1 Rising Prevalence of Chronic Diseases and Disabilities

4.2.1.2 Increasing Adoption of Telehealth and Remote Care

4.2.1.3 Growing Demand for Home-based Rehabilitation

4.2.1.4 Advancements in AI, VR, and Wearable Technologies

4.2.2 Restraints

4.2.2.1 Limited Reimbursement Policies

4.2.2.2 Digital Literacy Barriers

4.2.2.3 High Initial Setup Costs

4.2.3 Opportunities

4.2.3.1 Expansion of Remote Monitoring and AI-driven Therapy

4.2.3.2 Integration with Wearables and IoT Devices

4.2.3.3 Growth in Aging Population

4.2.3.4 Emerging Markets Adoption

4.2.4 Challenges

4.2.4.1 Data Privacy and Security Concerns

4.2.4.2 Clinical Validation and Adoption

4.3 Technology Landscape

4.3.1 Tele-rehabilitation Platforms

4.3.2 Virtual Reality (VR) & Augmented Reality (AR) Rehabilitation

4.3.3 AI-based Therapy & Motion Tracking Systems

4.3.4 Wearable Devices & Sensors

4.3.5 Mobile Health (mHealth) Applications

4.4 Digital Rehabilitation Ecosystem

4.4.1 Digital Health Platform Providers

4.4.2 Medical Device & Wearable Manufacturers

4.4.3 Healthcare Providers & Rehab Centers

4.4.4 Payers & Insurance Providers

4.4.5 Patients & Caregivers

4.5 Value Chain Analysis

4.5.1 Platform Development

4.5.2 Device Integration

4.5.3 Therapy Delivery

4.5.4 Monitoring & Data Analytics

4.5.5 Outcome Assessment

4.6 Regulatory Landscape

4.6.1 Digital Health Regulations (FDA, CE)

4.6.2 Telehealth Guidelines

4.6.3 Data Privacy Regulations (HIPAA, GDPR)

4.7 Industry Trends

4.7.1 Shift Toward Home-based Rehabilitation

4.7.2 Rise of AI-driven Personalized Therapy

4.7.3 Integration with Wearables & Remote Monitoring

4.7.4 Growth in Gamification and VR-based Rehab

4.8 Cost and Pricing Analysis

4.8.1 Cost Comparison: Traditional vs Digital Rehabilitation

4.8.2 Pricing Models (Subscription, Pay-per-use)

4.8.3 Reimbursement Trends

5. Digital Rehabilitation Market, by Therapy Type

5.1 Introduction

5.2 Physical Rehabilitation (Largest Segment)

5.3 Cognitive Rehabilitation

5.4 Speech & Language Therapy

5.5 Occupational Therapy

5.6 Other Therapies

6. Digital Rehabilitation Market, by Technology Type

6.1 Introduction

6.2 Tele-rehabilitation Platforms

6.3 VR/AR-based Rehabilitation Systems

6.4 AI-based Rehabilitation Systems

6.5 Wearable & Sensor-based Systems

6.6 Mobile Applications

7. Digital Rehabilitation Market, by Delivery Mode

7.1 Home-based Rehabilitation

7.2 Clinic-based Digital Rehabilitation

7.3 Hybrid Models

8. Digital Rehabilitation Market, by Application

8.1 Introduction

8.2 Neurological Disorders

8.2.1 Stroke Rehabilitation

8.2.2 Parkinson's Disease

8.2.3 Multiple Sclerosis

8.3 Musculoskeletal Disorders

8.3.1 Orthopedic Rehabilitation

8.3.2 Sports Injury Rehabilitation

8.4 Cardiopulmonary Rehabilitation

8.5 Pediatric Rehabilitation

8.6 Geriatric Rehabilitation

8.7 Other Applications

9. Digital Rehabilitation Market, by End User

9.1 Hospitals & Clinics

9.2 Rehabilitation Centers

9.3 Home Care Settings

9.4 Research Institutes

10. Digital Rehabilitation Market, by Geography

10.1 Introduction

10.2 North America

10.2.1 U.S.

10.2.2 Canada

10.3 Europe

10.3.1 Germany

10.3.2 U.K.

10.3.3 France

10.3.4 Italy

10.3.5 Spain

10.3.6 Netherlands

10.3.7 Sweden

10.3.8 Switzerland

10.3.9 Rest of Europe

10.4 Asia-Pacific

10.4.1 China

10.4.2 Japan

10.4.3 India

10.4.4 South Korea

10.4.5 Australia

10.4.6 Singapore

10.4.7 Rest of Asia-Pacific

10.5 Latin America

10.5.1 Brazil

10.5.2 Mexico

10.5.3 Rest of Latin America

10.6 Middle East & Africa

10.6.1 UAE

10.6.2 Saudi Arabia

10.6.3 South Africa

10.6.4 Rest of MEA

11. Competitive Landscape

11.1 Overview

11.2 Key Growth Strategies

11.3 Competitive Benchmarking

11.4 Competitive Dashboard

11.4.1 Industry Leaders

11.4.2 Market Differentiators

11.4.3 Emerging Players

11.5 Market Ranking/Positioning Analysis

12. Company Profiles (Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

12.1 Reflexion Health

12.2 Hinge Health

12.3 Sword Health

12.4 SWORD Health

12.5 Kaia Health

12.6 RehabGuru

12.7 Physitrack

12.8 MIRA Rehab

12.9 MindMaze

12.10 Hocoma AG

12.11 Ekso Bionics

12.12 Neofect

12.13 Tyromotion GmbH

12.14 Bioness Inc.

12.15 Motek Medical

13. Appendix

13.1 Customization Options

13.2 Related Reports

Published Date: May-2026

Published Date: Nov-2025

Published Date: May-2024

Published Date: Jun-2026

Published Date: May-2026

Subscribe to get the latest industry updates