Resources

About Us

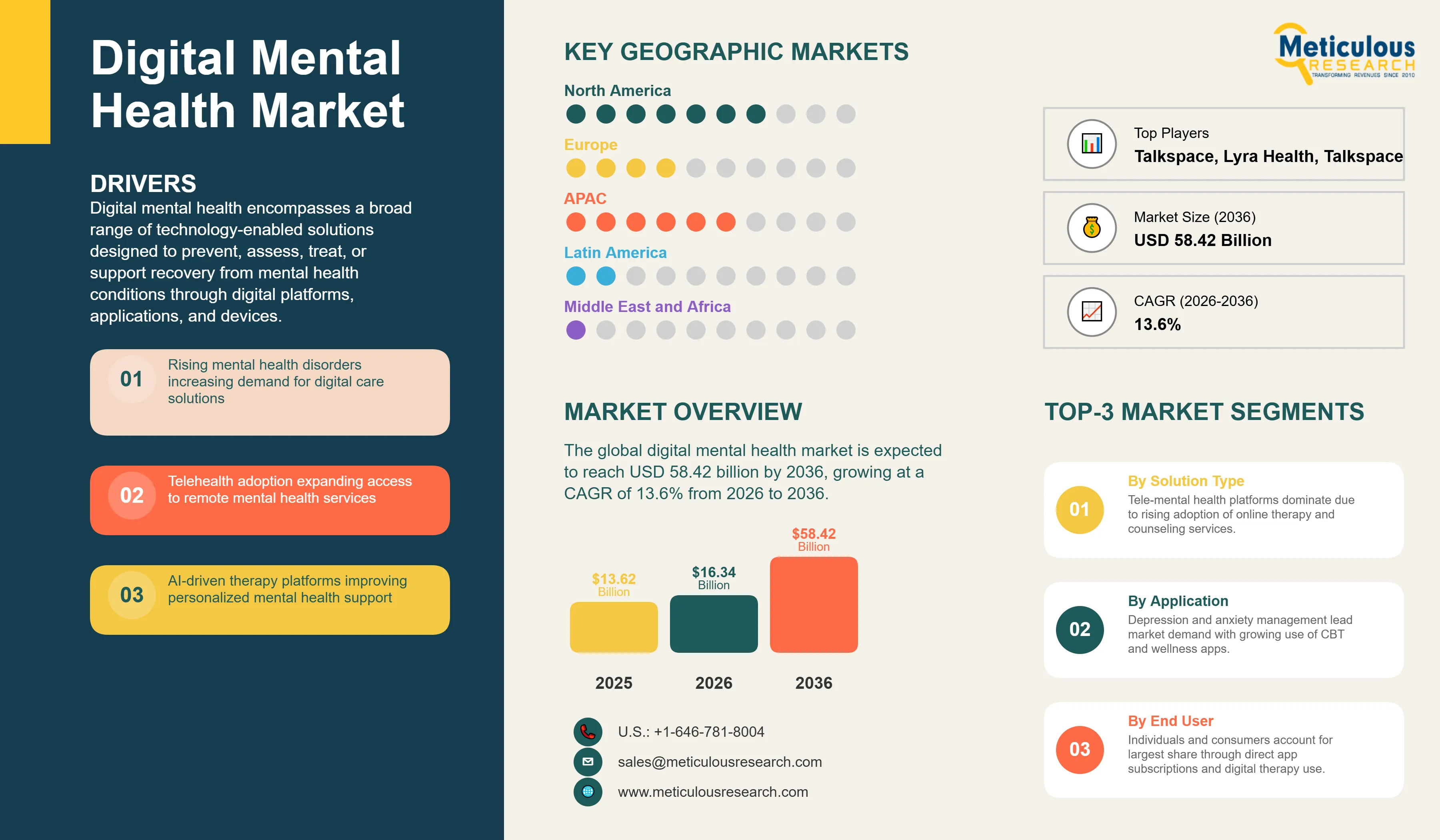

The global digital mental health market was valued at USD 13.62 billion in 2025. This market is expected to reach USD 58.42 billion by 2036 from USD 16.34 billion in 2026, growing at a CAGR of 13.6% from 2026 to 2036.

The growth of this market is driven by the scale and unmet need of the global mental health burden, the accelerating adoption of digital health platforms across telehealth, mobile applications, and AI-driven therapeutics, and the structural inadequacy of traditional mental health care systems to meet rising demand. According to the World Health Organization's Mental Health Atlas 2024 and the World Mental Health Today report, released in September 2025, over one billion people are currently living with a mental health condition worldwide. Mental health conditions are among the leading causes of disability globally, yet most affected individuals do not receive adequate care. According to the WHO, approximately two in three people experiencing mental health conditions globally do not receive any treatment at all, representing the most significant unmet need in global healthcare and the primary structural driver of demand for scalable digital alternatives to traditional in-person care.

The economic burden of the treatment gap is substantial. WHO estimates that depression and anxiety together cost the global economy about USD 1 trillion annually, mainly through productivity losses and absenteeism. WHO’s Mental Health Atlas 2024 also shows that mental health still receives only about 2% of health budgets in most countries, with spending per person varying sharply across income groups. This chronic underinvestment in traditional mental health infrastructure, combined with the scale of unmet need, creates a compelling structural case for digital mental health solutions that can be delivered at a fraction of the cost of in-person care, at scale, and without the geographic constraints of therapist-dependent service models.

Digital mental health encompasses a broad range of technology-enabled solutions designed to prevent, assess, treat, or support recovery from mental health conditions through digital platforms, applications, and devices. The product landscape spans tele-mental health platforms that connect patients with licensed therapists through secure video and messaging systems; mental health applications that deliver guided meditation, cognitive behavioral therapy exercises, mood tracking, and psychoeducation content to consumers on a self-directed basis; digital therapeutics that are clinically validated, evidence-based software interventions for specific mental health diagnoses; AI-powered chatbots and virtual therapists that provide on-demand conversational support using natural language processing; and wearable-integrated platforms that use physiological data including heart rate variability, sleep patterns, and galvanic skin response to monitor mental wellness and trigger intervention.

The scale of the underlying need driving this market is documented by the world's leading health authorities. According to the WHO's fact sheet on mental disorders, approximately 970 million people globally were living with a mental disorder in 2019, with the number increasing significantly through the COVID-19 pandemic period. The WHO's World Mental Health Today report (September 2025) updated this figure to over one billion. According to WHO, over 280 million people worldwide live with depression and 301 million live with anxiety disorders. WHO’s Mental Health Atlas 2024 also shows that mental health workforce capacity remains extremely limited, with especially severe shortages in low- and middle-income countries. In the United States, according to the SAMHSA National Survey on Drug Use and Health released in July 2025, 23.4% of U.S. adults, equivalent to 61.5 million people, experienced a mental health condition in the past year, and 5.6% of U.S. adults experienced a serious mental illness that substantially interfered with daily life. According to the CDC's 2024 data, only 14% of U.S. adults reported receiving counseling or therapy from a mental health professional in the past year, confirming the vast treatment gap that digital mental health solutions are positioned to address.

The competitive landscape of the digital mental health market encompasses tele-therapy platforms, consumer wellness app developers, digital therapeutics companies, AI mental health solution providers, and large health technology companies entering through acquisition or organic investment. Teladoc Health, through its BetterHelp and Teladoc Mental Health divisions, is the largest single player by revenue in the consumer and enterprise digital mental health segments. Lyra Health and Spring Health serve the employer-sponsored mental health benefits market, connecting employees with therapists and digital wellness tools through workforce mental health platforms. Consumer wellness app leaders Calm and Headspace Health address the self-directed mental wellness market. Woebot Health and SilverCloud Health represent the evidence-based digital therapeutic and CBT-based platform segment. Akili Interactive and Pear Therapeutics have developed FDA-regulated digital therapeutic products validated through randomized controlled trials.

Integration of Artificial Intelligence for Personalized and Scalable Mental Health Support

The integration of artificial intelligence across digital mental health platforms is the most broadly impactful technology trend shaping the market. AI capabilities including natural language processing, conversational agents, machine learning-based mood and risk assessment, and personalized content recommendation are being embedded into products across every segment of the digital mental health landscape. AI-powered chatbots such as Woebot, which uses conversational AI to deliver structured cognitive behavioral therapy techniques through a mobile chat interface, address a specific and documented access problem: the WHO's Mental Health Atlas 2024 confirms a global median of just 13 mental health workers per 100,000 people, a workforce gap that no recruitment program could realistically close within a generation. AI-driven systems that can provide consistent, evidence-based therapeutic support to millions of users simultaneously represent the only technically feasible path to closing the treatment gap identified by the WHO at scale.

Beyond conversational interfaces, AI is enabling passive monitoring approaches where machine learning models analyze patterns in how users type, speak, or move as captured through smartphone sensors to infer mental state changes that may indicate emerging depression or anxiety episodes. This passive sensing capability is being incorporated into platforms including Mindstrong Health, which analyzes smartphone usage patterns as digital biomarkers of cognitive and emotional health. The regulatory and clinical validation landscape for AI-driven mental health tools is also evolving, with the FDA's Digital Health Center of Excellence developing frameworks for reviewing AI-based software as a medical device in mental health applications. These regulatory developments, combined with growing clinical evidence for AI-based mental health interventions from NIH-funded research programs, are improving the credibility and payer acceptance of AI-driven digital mental health tools.

Employer-sponsored Mental Health Programs Expanding the Payer Base

The rapid growth of employer-sponsored mental health benefit programs is creating a large and commercially attractive distribution channel for digital mental health platforms that extends beyond the direct-to-consumer market. U.S. employers have increasingly recognized mental health conditions as a primary driver of employee absenteeism, presenteeism, and workforce turnover, with the economic burden falling directly on employer productivity and healthcare benefit costs. According to the SAMHSA 2024 National Survey on Drug Use and Health, released in July 2025, 23.4% of U.S. adults experienced a mental health condition in the past year, representing a substantial portion of any employer's workforce. Companies including Lyra Health, Spring Health, and Modern Health have built B2B mental health benefit platforms specifically designed for employer procurement, offering employees access to digital mental health tools, therapist matching, and medication management through a single integrated platform funded entirely by the employer as a benefit.

The employer channel provides digital mental health companies with several structural commercial advantages over direct-to-consumer models. Employer contracts provide predictable per-employee-per-month recurring revenue that is not subject to the high consumer churn rates that challenge direct-to-consumer subscription apps. Employer-funded platforms eliminate the cost barrier that the CDC identified as the obstacle cited by 52% of Americans who do not seek mental health care, allowing employees to access services without personal financial commitment. The growing regulatory and legal pressure on employers in the European Union under workplace mental health provisions of the EU Strategic Framework on Health and Safety at Work 2021-2027, and in the United Kingdom under Health and Safety Executive guidance on work-related stress, is also expanding the employer mental health benefit market beyond the United States.

|

Parameter |

Details |

|

Market Size by 2036 |

USD 58.42 Billion |

|

Market Size in 2026 |

USD 16.34 Billion |

|

Market Size in 2025 |

USD 13.62 Billion |

|

Market Growth Rate (2026-2036) |

CAGR of 13.6% |

|

Dominating Region |

North America |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Solution Type, Technology, Delivery Mode, Application, End User, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Driver: Escalating Global Prevalence of Mental Health Disorders and Critical Treatment Gaps

The most fundamental driver of the digital mental health market is the documented and growing scale of untreated mental health conditions globally, which creates an addressable need that traditional healthcare systems are structurally unable to meet. According to the World Health Organization's World Mental Health Today report (September 2025), over one billion people are currently living with a mental health condition worldwide, yet most do not receive adequate care. The WHO reports that approximately two in three people experiencing mental health conditions globally receive no treatment. According to the WHO's Mental Health Atlas 2024, the global median mental health workforce stands at just 13 workers per 100,000 people, and mental health spending accounts for only 2% of national health budgets globally, unchanged since 2017. In the United States, according to the SAMHSA 2024 National Survey on Drug Use and Health (released July 2025), 23.4% of U.S. adults, or 61.5 million people, experienced a mental health condition in the past year, including 14.6 million adults with serious mental illness. The CDC's 2024 data confirms that only 14% of U.S. adults reported receiving counseling or therapy in the past year, confirming that the vast majority of those affected are not receiving professional mental health support. This structural gap between prevalence and treatment access is the primary demand driver for digital mental health platforms that can reach underserved populations at scale, at lower cost, and without the geographic constraints of in-person therapist-dependent care models.

Opportunity: FDA-authorized Digital Therapeutics and Clinical Integration

The emergence of FDA-authorized digital therapeutic products for specific mental health conditions represents a significant opportunity to expand digital mental health beyond the consumer wellness market into the regulated clinical care and insurance reimbursement market. Digital therapeutics differ from general wellness apps in that they are evidence-based software interventions validated through randomized controlled trials, regulated by the FDA as software as a medical device, and designed to treat, manage, or prevent a specific medical condition under clinician supervision. Akili Interactive received FDA authorization for EndeavorRx, a video game-based digital therapeutic for attention-deficit hyperactivity disorder in children, marking a significant regulatory milestone for the category. Big Health's Sleepio and Daylight programs have received FDA Breakthrough Device designation for insomnia and generalized anxiety disorder, respectively. The FDA's Digital Health Center of Excellence has been actively developing regulatory frameworks for digital health technologies including software as a medical device, providing increasing regulatory clarity that supports clinical adoption and payer reimbursement of validated digital therapeutics. As more digital therapeutic products accumulate the clinical evidence required for FDA authorization and payer coverage decisions, the total addressable market for digital mental health expands from the discretionary consumer wellness spending segment into the significantly larger clinical care and insurance-reimbursed treatment market.

Why Do Tele-mental Health Platforms Lead the Market?

In 2026, the tele-mental health platforms segment is expected to hold the largest share of the digital mental health market. Tele-mental health platforms are the most commercially mature category in digital mental health, with live therapist-connected video and messaging services generating the highest per-user revenue of any digital mental health product through ongoing subscription or per-session billing. BetterHelp, operated by Teladoc Health, is the largest consumer tele-therapy platform globally, providing subscribers with unlimited messaging and weekly video sessions with licensed therapists at a monthly subscription rate that is substantially lower than the out-of-pocket cost of traditional in-person therapy in most markets. Talkspace serves both individual consumers and enterprise clients with a similar therapist-matched subscription model. These platforms address the documented access barriers to traditional therapy: according to a CDC survey cited in 2024, 52% of Americans who do not seek mental health care cite cost as the primary obstacle, and 42% cite difficulty finding a provider, both of which tele-therapy platforms directly address through lower-cost subscription access and expanded therapist network reach.

However, the digital therapeutics segment is expected to witness the fastest growth during the forecast period. Digital therapeutics represent the highest-value and highest-clinical-credibility segment within digital mental health because they are developed with the same evidence standards as pharmaceutical products, including randomized controlled trial validation, and are regulated by the FDA as software as a medical device. As FDA-authorized digital therapeutic products for depression, anxiety, insomnia, and substance use disorders gain insurance coverage from major U.S. payers and integration into clinical prescribing workflows, they are accessing the significantly larger reimbursed treatment market rather than competing in the discretionary consumer wellness spending segment. The FDA's Digital Health Center of Excellence regulatory frameworks are providing increasing clarity for digital therapeutic developers, and the growing number of products with FDA Breakthrough Device designation or authorization is creating a validated product pipeline that supports payer coverage expansion.

How Does AI and Machine Learning Lead the Technology Market?

In 2026, the AI and machine learning segment is expected to hold the largest share of the digital mental health market by technology. AI capabilities are embedded across the majority of digital mental health products in operation, from the conversational therapy chatbots of Woebot Health and SilverCloud Health to the personalized content recommendation engines of Calm and Headspace and the risk stratification algorithms that tele-therapy platforms use to match users with appropriate care pathways. The pervasiveness of AI as an enabling technology across all digital mental health product categories makes it the largest technology segment by revenue attribution. The foundational justification for AI in mental health is the documented workforce gap: the WHO's Mental Health Atlas 2024 confirms a global median of just 13 mental health workers per 100,000 people, with the most severe shortages in low- and middle-income countries. AI-driven systems that deliver consistent, evidence-based therapeutic content at scale are the only technically feasible approach to closing this gap without a generational workforce expansion program that no country has the budget to undertake.

However, the virtual reality and augmented reality segment is expected to witness the fastest growth during the forecast period. VR-based exposure therapy for PTSD, phobias, and social anxiety is accumulating clinical evidence and transitioning from research settings to commercially available treatment tools. Oxford VR and Limbix have developed VR therapy products targeting anxiety and phobia treatment, and the U.S. Department of Veterans Affairs has been an active funder of VR-based PTSD treatment research, providing clinical validation data that is supporting broader clinical adoption. The declining cost of VR headsets and the emergence of standalone wireless VR platforms such as Meta Quest reduce the hardware barrier for VR mental health therapy in clinical settings.

Why Does On-demand Self-guided Lead the Market?

In 2026, the on-demand self-guided segment is expected to hold the largest share of the digital mental health market. Self-guided apps represent the largest consumer-facing segment of the digital mental health market by user volume, with platforms including Calm, Headspace, and Woebot collectively serving tens of millions of monthly active users. The self-guided delivery mode removes the scheduling, cost, and access barriers associated with therapist-dependent delivery, allowing users to engage with mental health content at their own pace, at any time, and from any location with a smartphone. According to the SAMHSA 2024 NSDUH released July 2025, 23.4% of U.S. adults experienced a mental health condition in the past year, representing a population of 61.5 million people, the vast majority of whom do not currently have a regular therapist relationship. The self-guided app model is the most scalable approach to reaching this large population with mental health support, even if the depth of clinical intervention is more limited than therapist-guided alternatives.

However, the hybrid models segment is expected to witness the fastest growth during the forecast period. Hybrid models that combine on-demand digital tools with periodic therapist check-ins are gaining clinical and payer acceptance because they provide a more sustainable cost structure than fully therapist-led models while maintaining a level of clinical oversight that pure self-guided apps cannot offer. Employers and insurance payers are increasingly specifying hybrid model delivery in their digital mental health benefit procurement because hybrid platforms can demonstrate clinical outcomes data that supports the cost-of-care reduction arguments needed to justify benefit investment. Spring Health and Lyra Health both operate hybrid delivery models that route employees through digital screening tools and self-guided content while connecting higher-acuity cases with therapists, creating an efficient stepped-care architecture that matches intervention intensity to clinical need.

Why Does Depression and Anxiety Management Lead the Application Market?

In 2026, the depression and anxiety management segment is expected to hold the largest share of the digital mental health market. Depression and anxiety are the most prevalent mental health conditions globally and represent the primary clinical focus of the majority of digital mental health products across tele-therapy, apps, and digital therapeutics. According to the World Health Organization, over 280 million people worldwide suffer from depression and 301 million from anxiety disorders. According to the SAMHSA 2024 National Survey on Drug Use and Health released in July 2025, 21.4 million U.S. adults experienced a major depressive episode in the past year, and among those aged 18 to 25, 15.9% had a major depressive episode, nearly double the overall adult rate. The CDC's 2024 data shows that 19% of U.S. adults have been told by a healthcare professional that they have a depression disorder. The concentration of both prevalence and digital mental health product development activity in the depression and anxiety category makes it the dominant application segment by revenue.

However, the sleep disorders segment is expected to witness the fastest growth during the forecast period. Digital therapeutics for insomnia and sleep disorders have accumulated some of the strongest clinical evidence in the digital mental health field. Big Health's Sleepio, a digital cognitive behavioral therapy for insomnia program, has received FDA Breakthrough Device designation and has been validated in multiple randomized controlled trials. Sleep conditions affect a large population and are closely linked to depression and anxiety, creating significant co-morbidity-driven demand. Payers and employers are increasingly covering digital CBT-I products as a first-line insomnia treatment because they are more effective than sleep medications in long-term outcomes and avoid the side effects and dependency risks of pharmacological alternatives.

Why Do Individuals and Consumers Lead the End User Market?

In 2026, the individuals and consumers segment is expected to hold the largest share of the digital mental health market. Direct-to-consumer digital mental health platforms represent the broadest distribution channel by user volume and the largest aggregate revenue segment. Consumer-facing tele-therapy platforms including BetterHelp and Talkspace, wellness apps including Calm and Headspace, and AI chatbot platforms including Woebot collectively reach tens of millions of paying subscribers and free users who access mental health support independently rather than through employer or payer channels. The consumer segment benefits from the documented prevalence of mental health conditions: according to SAMHSA's 2024 NSDUH released in July 2025, 61.5 million U.S. adults experienced a mental health condition in the past year, representing a large addressable market for consumer mental health tools. The relatively low barrier to downloading and subscribing to consumer apps makes the individual consumer the most accessible and fastest-to-acquire customer segment for digital mental health companies.

However, the employers and corporate wellness programs segment is expected to witness the fastest growth during the forecast period. Employers are becoming an increasingly important procurement channel as they recognize the direct financial impact of employee mental health on productivity, absenteeism, and healthcare costs. According to the WHO, depression and anxiety alone cost up to USD 1 trillion per year globally in lost productivity, a figure that resonates with CFOs and HR leadership evaluating the business case for mental health benefit investment. Specialist employer mental health benefit platforms including Lyra Health, Spring Health, and Modern Health have grown rapidly by helping employers offer structured, clinically rigorous mental health benefits that go beyond traditional employee assistance programs. The growing legal and regulatory pressure on employers in Europe under EU workplace mental health provisions and in the UK under HSE guidance is expanding employer-driven digital mental health adoption beyond North America.

How is North America Maintaining Market Leadership?

In 2026, North America is expected to hold the largest share of the global digital mental health market. The United States is the primary market, driven by the high documented prevalence of mental health conditions, the rapid adoption of telehealth enabled by regulatory flexibilities introduced during the COVID-19 public health emergency, and the large and growing employer-sponsored mental health benefit market.

According to the SAMHSA 2024 National Survey on Drug Use and Health, released in July 2025, 23.4% of U.S. adults, equivalent to 61.5 million people, experienced a mental health condition in the past year. Of these, only 14% of U.S. adults reported receiving counseling or therapy from a mental health professional in the past year, according to the CDC's 2024 data. This gap between prevalence and treatment access is the most significant demand driver for digital mental health in the U.S. market. The CDC also confirmed in 2024 that 52% of Americans who do not seek mental health care cite cost as the primary barrier, which digital subscription platforms and employer-funded benefit programs are positioned to address. The U.S. telehealth regulatory environment, which was expanded significantly by the Centers for Medicare and Medicaid Services during the COVID-19 public health emergency, has maintained key telehealth provisions that have supported the continued growth of tele-therapy services. Canada contributes to regional demand through provincial mental health digital health initiatives and the adoption of employer-sponsored mental health benefit platforms by Canadian employers.

Which Factors Drive Asia-Pacific's Rapid Growth?

Asia-Pacific is expected to witness the highest growth rate in the digital mental health market during the forecast period. This growth is driven by the large and substantially underserved mental health burden across the region, rapid mobile health adoption, and government-supported digital health expansion programs.

According to the WHO's World Mental Health Today report (September 2025), mental health conditions affect over one billion people globally, with low- and middle-income countries bearing a disproportionate share of the burden and facing the most severe workforce and infrastructure shortages. The WHO's Mental Health Atlas 2024 documents that mental health spending in low-income countries averages just USD 0.04 per person per year, compared with USD 65 in high-income countries, confirming the scale of the investment gap in the region. China represents the largest individual market in Asia-Pacific, with a substantial and growing mental health burden and a national digital health policy framework that is supporting mobile health adoption. The Chinese government's Healthy China 2030 plan explicitly includes mental health as a priority area, creating a policy environment supportive of digital mental health solution deployment. India's large population, rapidly expanding smartphone penetration, and severe shortage of mental health professionals create a compelling environment for mobile-first digital mental health platforms. Australia's national digital mental health strategy and government-funded platforms including Beyond Blue and Lifeline have established a foundation of consumer familiarity with digital mental health services that is supporting broader adoption of commercial digital mental health products.

Some of the key companies operating in the global digital mental health market are Teladoc Health, Inc., Amwell (American Well Corporation), BetterHelp (Teladoc Health), Talkspace, Inc., Headspace Health, Calm.com, Inc., Woebot Health, Spring Health, Lyra Health, Mindstrong Health, Pear Therapeutics, Happify Health, SilverCloud Health, Big Health, and Akili Interactive.

The global digital mental health market is expected to grow from USD 16.34 billion in 2026 to USD 58.42 billion by 2036.

The global digital mental health market is projected to grow at a CAGR of 13.6% from 2026 to 2036.

The tele-mental health platforms segment is expected to dominate the overall market in 2026. However, the digital therapeutics segment is expected to witness the fastest CAGR, as FDA-authorized and clinically validated digital therapeutic products gain insurance reimbursement and clinical integration across depression, anxiety, insomnia, and substance use disorder treatment pathways.

The depression and anxiety management segment is expected to dominate the overall market in 2026, reflecting its position as the most prevalent mental health condition category globally, as documented by the WHO with over 280 million people affected by depression and 301 million by anxiety disorders. However, the sleep disorders segment is expected to witness the fastest CAGR, driven by the strong clinical evidence base for digital CBT-I products and growing payer coverage.

The individuals and consumers segment is expected to dominate the overall market in 2026. However, the employers and corporate wellness programs segment is expected to witness the fastest CAGR, driven by growing recognition of the productivity impact of employee mental health and expanding employer procurement of structured digital mental health benefit platforms across North America and Europe.

North America is expected to lead the global market in 2026. However, Asia-Pacific is expected to witness the fastest CAGR, driven by the large underserved mental health burden documented by the WHO, government-supported digital health expansion programs, and rapid mobile health adoption across China, India, and Southeast Asia.

The major players are Teladoc Health, Amwell, BetterHelp, Talkspace, Headspace Health, Calm.com, Woebot Health, Spring Health, Lyra Health, Mindstrong Health, Pear Therapeutics, Happify Health, SilverCloud Health, Big Health, and Akili Interactive.

1. Introduction

1.1. Market Definition

1.2. Scope

1.3. Market Ecosystem

1.4. Currency and Limitations

1.4.1. Currency

1.4.2. Limitations

1.5. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Data Collection & Validation

2.2.1. Secondary Research

2.2.2. Primary Research

2.3. Market Estimation

2.3.1. Bottom-Up Approach

2.3.2. Top-Down Approach

2.3.3. Forecast Modeling

2.4. Data Triangulation

2.5. Assumptions

3. Executive Summary

4. Market Overview

4.1. Introduction

4.2. Market Dynamics

4.2.1. Drivers

4.2.1.1. Rising Prevalence of Mental Health Disorders

4.2.1.2. Increasing Adoption of Telehealth and Remote Care

4.2.1.3. Growing Awareness and Reduced Stigma

4.2.1.4. Expansion of Employer-sponsored Mental Health Programs

4.2.2. Restraints

4.2.2.1. Data Privacy and Security Concerns

4.2.2.2. Limited Reimbursement in Some Regions

4.2.2.3. Clinical Validation Challenges

4.2.3. Opportunities

4.2.3.1. Integration of AI and Personalized Therapy

4.2.3.2. Expansion in Emerging Markets

4.2.3.3. Growth in Preventive Mental Health Solutions

4.2.3.4. Partnerships with Healthcare Systems and Employers

4.2.4. Challenges

4.2.4.1. User Engagement and Retention

4.2.4.2. Regulatory Compliance and Standardization

4.3. Technology Landscape

4.3.1. Tele-mental Health Platforms (Video/Chat-based Therapy)

4.3.2. Mobile Mental Health Applications

4.3.3. AI-based Chatbots and Virtual Therapists

4.3.4. Digital Therapeutics (DTx)

4.3.5. Wearables and Biosensors for Mental Health Monitoring

4.4. Digital Mental Health Ecosystem

4.4.1. Digital Health and App Developers

4.4.2. Healthcare Providers and Therapists

4.4.3. Employers and Payers

4.4.4. Pharmaceutical and Research Organizations

4.4.5. Patients and Consumers

4.5. Value Chain Analysis

4.5.1. Platform Development

4.5.2. Service Delivery

4.5.3. Data Collection and Monitoring

4.5.4. Analytics and Personalization

4.5.5. Outcome Measurement

4.6. Regulatory Landscape

4.6.1. Digital Health and Telemedicine Regulations

4.6.2. Data Privacy (HIPAA, GDPR)

4.6.3. Digital Therapeutics Approvals

4.7. Industry Trends

4.7.1. Rise of AI-driven Mental Health Solutions

4.7.2. Growth of Employer and Insurance-driven Models

4.7.3. Increasing Use of Digital Therapeutics

4.7.4. Integration with Wearables and Remote Monitoring

4.8. Cost and Pricing Analysis

4.8.1. Subscription-based Models

4.8.2. Pay-per-session Models

4.8.3. Reimbursement and Coverage Trends

5. Digital Mental Health Market, by Solution Type

5.1. Introduction

5.2. Tele-mental Health Platforms

5.3. Mental Health Apps (Meditation, CBT, Mood Tracking)

5.4. Digital Therapeutics (DTx)

5.5. AI-based Mental Health Solutions

5.6. Other Solutions

6. Digital Mental Health Market, by Technology

6.1. AI and Machine Learning

6.2. Cloud-based Platforms

6.3. Mobile Health (mHealth)

6.4. Wearable Integration

6.5. Virtual Reality (VR) and Augmented Reality (AR)

7. Digital Mental Health Market, by Delivery Mode

7.1. On-demand (Self-guided Apps)

7.2. Therapist-guided

7.3. Hybrid Models

8. Digital Mental Health Market, by Application

8.1. Introduction

8.2. Depression and Anxiety Management

8.3. Stress Management and Wellness

8.4. Substance Use Disorder Treatment

8.5. PTSD and Trauma Management

8.6. Sleep Disorders

8.7. Other Mental Health Conditions

9. Digital Mental Health Market, by End User

9.1. Individuals and Consumers

9.2. Healthcare Providers (Hospitals, Clinics)

9.3. Employers and Corporate Wellness Programs

9.4. Payers and Insurance Providers

10. Digital Mental Health Market, by Geography

10.1. Introduction

10.2. North America

10.2.1. U.S.

10.2.2. Canada

10.3. Europe

10.3.1. Germany

10.3.2. U.K.

10.3.3. France

10.3.4. Italy

10.3.5. Spain

10.3.6. Netherlands

10.3.7. Sweden

10.3.8. Switzerland

10.3.9. Rest of Europe

10.4. Asia-Pacific

10.4.1. China

10.4.2. Japan

10.4.3. India

10.4.4. South Korea

10.4.5. Australia

10.4.6. Singapore

10.4.7. Rest of Asia-Pacific

10.5. Latin America

10.5.1. Brazil

10.5.2. Mexico

10.5.3. Rest of Latin America

10.6. Middle East and Africa

10.6.1. UAE

10.6.2. Saudi Arabia

10.6.3. South Africa

10.6.4. Rest of MEA

11. Competitive Landscape

11.1. Overview

11.2. Key Growth Strategies

11.3. Competitive Benchmarking

11.4. Competitive Dashboard

11.4.1. Industry Leaders

11.4.2. Market Differentiators

11.4.3. Emerging Players

11.5. Market Ranking/Positioning Analysis

12. Company Profiles

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

12.1. Teladoc Health, Inc.

12.2. Amwell (American Well Corporation)

12.3. BetterHelp (Teladoc Health)

12.4. Talkspace, Inc.

12.5. Headspace Health

12.6. Calm.com, Inc.

12.7. Woebot Health

12.8. Spring Health

12.9. Lyra Health

12.10. Mindstrong Health

12.11. Pear Therapeutics

12.12. Happify Health

12.13. SilverCloud Health

12.14. Big Health

12.15. Akili Interactive

13. Appendix

13.1. Customization Options

13.2. Related Reports

Published Date: Jun-2026

Published Date: Nov-2025

Published Date: May-2024

Published Date: May-2024

Published Date: Apr-2023

Subscribe to get the latest industry updates