Resources

About Us

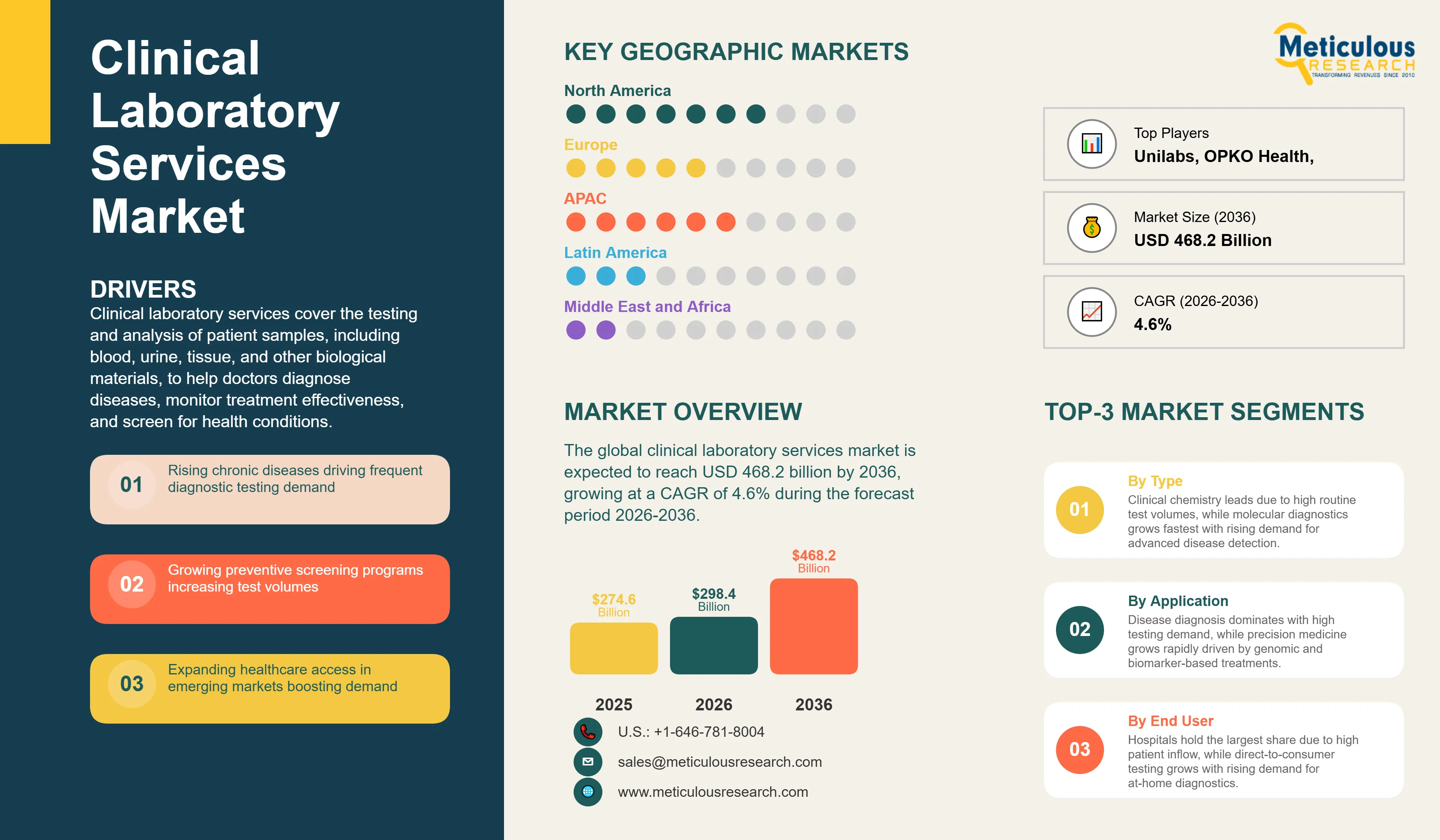

The global clinical laboratory services market was valued at USD 274.6 billion in 2025. This market is expected to reach USD 468.2 billion by 2036 from an estimated USD 298.4 billion in 2026, growing at a CAGR of 4.6% during the forecast period 2026-2036.

Click here to: Get Free Sample Pages of this Report

Clinical laboratory services cover the testing and analysis of patient samples, including blood, urine, tissue, and other biological materials, to help doctors diagnose diseases, monitor treatment effectiveness, and screen for health conditions. These services are delivered through hospital labs, large independent diagnostic chains, physician office labs, and increasingly through at-home testing kits. Laboratory test results inform an estimated 70% of all clinical decisions, making this one of the most essential and high-volume components of the global healthcare system.

The market is growing because chronic diseases including diabetes, cardiovascular conditions, and cancer are increasing globally, each requiring regular laboratory monitoring. Rising awareness of preventive health screening and the growth of annual health checkup programs are generating higher test volumes. Government health programs in emerging markets are significantly expanding access to diagnostic services for previously underserved populations. The post-COVID period has also reinforced the critical role of diagnostics in public health management, driving sustained investment in laboratory capacity globally.

Two significant opportunities are shaping the market's next phase. Automation and AI are transforming laboratory workflows by reducing manual processing time, improving accuracy, and enabling labs to handle far higher test volumes without proportional staffing increases. Simultaneously, the rapid expansion of genomic and molecular diagnostics for cancer detection, infectious disease identification, and precision medicine is creating a high-growth, high-value segment that is broadening the total addressable market well beyond traditional biochemistry and blood count testing.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 468.2 Billion |

|

Market Size in 2026 |

USD 298.4 Billion |

|

Market Size in 2025 |

USD 274.6 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 4.6% |

|

Dominating Test Type |

Clinical Chemistry Tests |

|

Fastest Growing Test Type |

Molecular Diagnostics |

|

Dominating Service Provider |

Hospital-Based Laboratories |

|

Fastest Growing Service Provider |

Independent and Reference Laboratories |

|

Dominating Application |

Disease Diagnosis |

|

Fastest Growing Application |

Personalized and Precision Medicine |

|

Dominating End User |

Hospitals |

|

Fastest Growing End User |

Patients (Direct-to-Consumer Testing) |

|

Dominating Mode of Testing |

Centralized Laboratory Testing |

|

Fastest Growing Mode of Testing |

At-Home Testing |

|

Dominating Technology Type |

Automated Testing |

|

Fastest Growing Technology Type |

AI-Enabled and Digital Diagnostics |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Consolidation Creating Large National and Global Laboratory Networks

One of the key trends in the clinical laboratory services market is the ongoing consolidation of independent and regional laboratory operators into large national and multinational networks through acquisition. Quest Diagnostics and Labcorp have built the world's two largest clinical laboratory businesses in the U.S. through decades of targeted acquisitions, and European counterparts including Eurofins Scientific, SYNLAB, and Sonic Healthcare have followed similar consolidation strategies across multiple national markets.

Consolidation delivers competitive advantages in purchasing power for reagents and equipment, the ability to spread capital investment in automation across a larger test volume base, more efficient routing of complex specialty tests to dedicated centers of excellence, and the scale to invest in digital infrastructure and data analytics. Smaller independent labs that cannot match the cost efficiency and service breadth of consolidated players are increasingly becoming acquisition targets, and this trend is expected to continue driving market concentration through the forecast period.

Molecular and Genomic Testing Reshaping the High-Value End of the Market

The fastest-growing segment of the clinical laboratory market is molecular and genomic testing, which uses DNA and RNA analysis to detect diseases at the molecular level with far greater sensitivity and specificity than conventional biochemical tests. Molecular testing has become standard for infectious disease identification following the mass adoption of PCR testing during the COVID-19 pandemic, which exposed millions of patients and clinicians globally to the speed and accuracy advantages of molecular methods. This familiarity is driving adoption of molecular approaches for applications where they were previously used only in specialized reference labs.

Next-generation sequencing is expanding into oncology as a standard tool for tumor profiling that guides treatment selection, into rare disease diagnosis for previously unresolvable cases, and into prenatal screening for chromosomal abnormalities. Companion diagnostic testing that identifies which patients will respond to specific targeted therapies is growing rapidly in parallel with the expanding pipeline of targeted cancer drugs. These applications command significantly higher per-test revenue than routine chemistry and hematology testing, making molecular and genomic services an increasingly important driver of revenue growth for laboratory service providers that have invested in the required sequencing and bioinformatics capabilities.

At-Home and Direct-to-Consumer Testing Expanding the Market's Reach

A growing segment of the clinical laboratory market is direct-to-consumer testing, where patients order laboratory tests themselves through online platforms and either collect samples at home using mail-in kits or visit a nearby collection center without a physician referral. Companies including Everlywell, LetsGetChecked, and the consumer health divisions of Quest Diagnostics offer panels covering everything from hormones and vitamins to sexually transmitted infection screening and cardiovascular risk markers directly to consumers who want healthcare information without a physician visit.

At-home testing experienced extraordinary growth during the COVID-19 pandemic and has retained a significantly larger consumer base than existed before 2020. The convenience of collecting a finger-prick blood sample or saliva swab at home and receiving results digitally within days is particularly appealing to working-age adults who value time efficiency and privacy for certain health topics. As at-home testing technology improves and as direct-to-consumer health awareness continues growing, this channel is expected to capture a progressively larger share of total testing volumes, particularly for wellness, preventive screening, and chronic disease monitoring applications.

Rising Prevalence of Chronic and Infectious Diseases

Chronic diseases including diabetes, cardiovascular disease, chronic kidney disease, and cancer require ongoing laboratory monitoring as essential components of patient management. The global diabetes population alone exceeds 530 million people, each requiring regular blood glucose monitoring, HbA1c testing, and kidney and cholesterol panels. Cancer incidence is growing globally, and each new cancer patient generates significant laboratory testing demand for initial diagnosis, treatment monitoring, and follow-up surveillance. The growing burden of chronic disease is therefore creating a structurally growing demand for laboratory services that increases proportionally with patient populations and extends over multi-year or lifetime treatment journeys rather than requiring only single-episode testing.

Expansion of Preventive Healthcare and Screening Programs

Government health agencies and private payers are increasingly recognizing that investing in preventive screening programs reduces the long-term cost of treating advanced disease. National cancer screening programs for colorectal, cervical, and breast cancer across developed markets generate very large volumes of laboratory tests annually, and the expansion of these programs to additional cancer types and to broader population age groups is growing test volumes progressively. Annual health checkup programs, employer wellness programs, and the growing consumer culture of proactive health monitoring are further expanding the population of people undergoing routine laboratory testing beyond the traditional patient-with-symptoms customer base.

Adoption of Automation and AI in Laboratory Testing

Laboratory automation, including total laboratory automation systems that handle sample receipt, processing, testing, and result reporting with minimal human intervention, is transforming the cost and capacity profile of large clinical laboratories. Automated labs can process significantly more samples with fewer staff, reduce turnaround times, eliminate manual handling errors, and operate continuously without shift constraints. For large reference laboratories processing tens of thousands of samples daily, total lab automation provides a transformative operational advantage. AI applications including automated image analysis for pathology slides, intelligent quality control monitoring, and predictive maintenance for laboratory instruments are adding further efficiency and accuracy improvements that compound the benefits of hardware automation.

Growth in Genomic and Molecular Diagnostics

The rapid reduction in the cost of DNA sequencing, from roughly USD 1 billion per genome in 2001 to under USD 200 today, has made genomic testing commercially viable across a much wider range of applications than was previously possible. Liquid biopsy tests that detect cancer-related DNA circulating in the bloodstream are enabling earlier cancer detection and treatment monitoring with a simple blood draw. Pharmacogenomic testing that identifies how individual patients metabolize specific drugs is improving prescribing decisions and reducing adverse drug reactions. The expanding clinical utility of genomic information across oncology, rare diseases, infectious disease, and reproductive medicine is creating a large and rapidly growing market for laboratory providers with the sequencing, bioinformatics, and clinical interpretation capabilities to deliver these high-complexity tests.

By Test Type: In 2026, Clinical Chemistry Tests to Dominate

Based on test type, the global clinical laboratory services market is segmented into clinical chemistry tests, immunology and serology tests, molecular diagnostics, hematology tests, microbiology tests, genetic and genomic testing, toxicology and drug testing, and other tests. In 2026, the clinical chemistry tests segment is expected to account for the largest share of the global clinical laboratory services market. Clinical chemistry testing, covering metabolic panels, lipid profiles, liver function tests, kidney function markers, and blood glucose, is by far the highest-volume test category because virtually every clinical encounter involving a blood test includes at least one chemistry panel. The extremely high test frequency, driven by chronic disease monitoring and routine annual health checkups, makes this the largest segment by total test volumes and revenue.

However, the molecular diagnostics segment is projected to register the highest CAGR during the forecast period. The proven value of molecular methods for infectious disease detection, oncology profiling, and precision medicine applications, combined with continuing reductions in the cost of molecular testing platforms and expanding clinical guidelines that recommend molecular testing for an increasing range of conditions, is driving double-digit growth in molecular diagnostics volumes across both developed and emerging markets.

By Service Provider: In 2026, Hospital-Based Laboratories to Hold the Largest Share

Based on service provider, the global market for clinical laboratory services is segmented into hospital-based laboratories, independent and reference laboratories, physician office laboratories, and public health laboratories. In 2026, the hospital-based laboratories segment is expected to account for the largest share of the global clinical laboratory services market. Hospital labs serve the largest concentration of high-acuity patients requiring immediate test results for clinical decision-making, covering emergency, inpatient, and outpatient testing within the hospital system. The combination of high test volumes per facility and the essential role of on-site lab services for urgent clinical needs makes hospital-based labs the largest segment by revenue.

However, the independent and reference laboratories segment is projected to register the highest CAGR during the forecast period. Large independent lab networks including Quest, Labcorp, Eurofins, and their equivalents in other markets are capturing an increasing share of routine outpatient and specialty testing as they offer lower costs through automation and scale, broader test menus including rare and specialized assays that most hospital labs cannot economically offer, and faster turnaround for many non-urgent tests through optimized logistics and high-capacity processing facilities.

By Application: In 2026, Disease Diagnosis to Hold the Largest Share

Based on application, the global market for clinical laboratory services is segmented into disease diagnosis, preventive screening, drug development and clinical trials, personalized and precision medicine, and other applications. In 2026, the disease diagnosis segment is expected to account for the largest share of the global clinical laboratory services market. Diagnosing infectious and chronic diseases is the most common and highest-volume reason patients undergo laboratory testing globally. From confirming a bacterial infection to diagnosing diabetes or detecting cancer, disease diagnosis drives the majority of total test volumes and represents the established core of the clinical laboratory business.

However, the personalized and precision medicine segment is projected to register the highest CAGR during the forecast period. Genomic profiling for cancer treatment selection, pharmacogenomic testing for drug dosing optimization, and biomarker testing for targeted therapy eligibility are all growing rapidly as oncology and other specialties adopt individualized treatment approaches that depend on high-complexity laboratory tests. These tests command significantly higher per-test pricing than routine diagnostics, making precision medicine an increasingly important revenue growth driver for leading laboratory providers.

By End User: In 2026, Hospitals to Hold the Largest Share

Based on end user, the global clinical laboratory services market is segmented into hospitals, clinics, pharmaceutical and biotechnology companies, research institutions, and patients (direct-to-consumer testing). In 2026, the hospitals segment is expected to account for the largest share of the global clinical laboratory services market. Hospitals are the single largest source of laboratory test orders globally, generating very high test volumes from inpatient, outpatient, and emergency patients who require comprehensive diagnostic work-ups as part of their clinical care. The combination of 24/7 testing requirements, high per-patient test intensity, and the large number of hospitals globally makes this the dominant end-user category by revenue.

However, the patients (direct-to-consumer testing) segment is projected to register the highest CAGR during the forecast period. The COVID-19 pandemic normalized direct laboratory test ordering by consumers, and the growing availability of convenient at-home sample collection kits and digital results delivery platforms is sustaining consumer demand for testing outside the traditional physician-ordered model. Wellness monitoring, preventive screening, and sensitive health topics are driving consumers to bypass traditional healthcare channels for laboratory testing.

By Mode of Testing: In 2026, Centralized Laboratory Testing to Hold the Largest Share

Based on mode of testing, the global clinical laboratory services market is segmented into centralized laboratory testing, point-of-care testing, and at-home testing. In 2026, the centralized laboratory testing segment is expected to account for the largest share of the global clinical laboratory services market. Centralized labs in hospitals and large independent reference facilities process the vast majority of clinical test volumes, offering the highest analytical accuracy, the broadest test menus, and the most cost-efficient processing for large sample batches. The infrastructure investment in high-throughput analyzers, quality control systems, and skilled staff makes centralized testing the current standard for most diagnostic applications.

However, the at-home testing segment is projected to register the highest CAGR during the forecast period. The combination of improved at-home sample collection technology, digital connectivity for result reporting, and growing consumer preference for convenient and private health monitoring is driving rapid growth in this newer channel from a smaller current base. Regulatory frameworks are progressively adapting to enable more test types to be performed using at-home sample collection, expanding the addressable market for this segment.

Clinical Laboratory Services Market by Region: North America Leading by Share, Asia-Pacific by Growth

Based on geography, the global market for clinical laboratory services is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

In 2026, North America is expected to account for the largest share of the global clinical laboratory services market. The United States has the world's largest clinical laboratory industry, anchored by Quest Diagnostics and Labcorp which together process billions of tests annually from their networks of patient service centers, hospital laboratory management contracts, and reference testing facilities. The U.S. laboratory market benefits from high healthcare spending per capita, the CLIA regulatory framework that establishes quality standards and patient confidence, robust health insurance coverage that reimburses most standard diagnostic tests, and a large and growing chronic disease patient population that generates sustained high test volumes. The U.S. is also the most advanced market for molecular and genomic testing adoption, with Mayo Clinic Laboratories, ARUP Laboratories, and several specialty molecular diagnostics companies offering highly differentiated test menus that serve both domestic and international physician customers. Canada's universal healthcare system generates significant laboratory test volumes through provincial laboratory networks and contracted independent labs.

However, the Asia-Pacific clinical laboratory services market is expected to grow at the fastest CAGR during the forecast period. The region combines the world's two most populous countries in China and India with rapidly growing middle classes that are increasing their healthcare utilization and awareness, governments investing in healthcare infrastructure expansion, and large and worsening chronic disease burdens that are driving demand for diagnostic services. India is one of the most dynamic laboratory services markets in the world, with major domestic chains including Dr. Lal PathLabs, Metropolis Healthcare, and SRL Diagnostics serving hundreds of millions of patients through hub-and-spoke collection networks across the country. China's laboratory services market is large and growing, driven by the country's enormous population, rapidly expanding urban healthcare infrastructure, and significant government investment in primary healthcare capacity. Japan, South Korea, and Australia have sophisticated laboratory industries with high per-capita test utilization and growing adoption of advanced molecular and genomic testing.

Europe is a large and mature clinical laboratory market with distinctive national characteristics shaped by the healthcare systems of individual countries. Germany, France, the UK, and Italy all have large laboratory service industries covering both public health system testing and privately funded diagnostics. The European market has seen significant consolidation, with Eurofins Scientific having built a pan-European and global reference laboratory network through over 900 acquisitions, and SYNLAB becoming one of Europe's leading clinical laboratory networks. The growth of specialist and molecular testing, the aging of European populations driving higher chronic disease management test volumes, and the ongoing expansion of cancer screening programs are all supporting sustained market growth. Latin America and the Middle East and Africa are growing markets with significant investment in healthcare infrastructure and diagnostic services capacity building underway.

The clinical laboratory services industry ranges from large global and national diagnostic chains serving millions of patients annually through extensive collection networks, to specialist reference laboratories offering highly complex molecular, genomic, and esoteric testing unavailable at most routine labs, to hospital-based laboratory networks managing on-site testing for major health systems. Competition is based on test menu breadth, turnaround time, analytical accuracy and quality credentials, geographic accessibility of collection points, pricing competitiveness, and digital result delivery and integration capabilities.

Quest Diagnostics and Labcorp are the world's two largest independent clinical laboratory companies by revenue and test volume, each serving hundreds of millions of patients annually through their U.S. networks and international operations. Sonic Healthcare is the world's third-largest clinical laboratory company with leading positions in Australia, Germany, the UK, Switzerland, and several other markets. Eurofins Scientific has built a unique pan-European and global reference laboratory network covering both clinical diagnostics and life sciences testing. SYNLAB is a major European clinical laboratory network operating across more than 30 countries. Mayo Clinic Laboratories and ARUP Laboratories are leading U.S. reference and specialty testing laboratories serving physicians nationwide with highly complex and specialized test menus. Dr. Lal PathLabs and Metropolis Healthcare are the leading listed clinical laboratory companies in India, each operating national collection and testing networks.

The report provides a comprehensive competitive analysis based on a thorough review of leading players' service portfolios, geographic footprint, technology capabilities, and recent strategic developments. Some of the key players operating in the global clinical laboratory services market include Quest Diagnostics Incorporated (U.S.), Laboratory Corporation of America Holdings/Labcorp (U.S.), Sonic Healthcare Limited (Australia), Eurofins Scientific SE (Luxembourg), SYNLAB International GmbH (Germany), BioReference Laboratories Inc. (U.S.), Mayo Clinic Laboratories (U.S.), ARUP Laboratories (U.S.), Unilabs (Sweden), Cerba HealthCare (France), Exact Sciences Corporation (U.S.), Fulgent Genetics Inc. (U.S.), OPKO Health Inc. (U.S.), Metropolis Healthcare Ltd. (India), and Dr. Lal PathLabs Limited (India), among others.

The global clinical laboratory services market is expected to reach USD 468.2 billion by 2036 from an estimated USD 298.4 billion in 2026, at a CAGR of 4.6% during the forecast period 2026-2036.

In 2026, the clinical chemistry tests segment is expected to hold the largest share of the global market, driven by the extremely high frequency of metabolic panel and blood chemistry testing for chronic disease management and routine health monitoring generating the highest aggregate test volumes of any category.

The molecular diagnostics segment is expected to register the highest CAGR during the forecast period 2026-2036, driven by expanding clinical adoption of PCR, NGS, and liquid biopsy technologies for infectious disease, oncology, and precision medicine applications alongside continued cost reductions in molecular testing platforms.

In 2026, the disease diagnosis segment is expected to hold the largest share of the global clinical laboratory services market, reflecting disease diagnosis being the primary reason patients undergo laboratory testing globally and generating the highest total test volumes across all application categories.

The at-home testing segment is projected to register the highest CAGR during the forecast period, driven by the sustained consumer adoption of direct-to-consumer testing that accelerated during the COVID-19 pandemic and the growing availability of convenient at-home collection kits for a widening range of diagnostic applications.

The market is primarily driven by rising global chronic disease prevalence creating sustained high-volume testing demand for ongoing disease monitoring, and by the rapid adoption of molecular and genomic diagnostics for precision medicine applications that command significantly higher per-test revenue and are expanding the market's total addressable value well beyond traditional routine testing.

Key players are Quest Diagnostics Incorporated (U.S.), Laboratory Corporation of America Holdings/Labcorp (U.S.), Sonic Healthcare Limited (Australia), Eurofins Scientific SE (Luxembourg), SYNLAB International GmbH (Germany), BioReference Laboratories Inc. (U.S.), Mayo Clinic Laboratories (U.S.), ARUP Laboratories (U.S.), Unilabs (Sweden), Cerba HealthCare (France), Exact Sciences Corporation (U.S.), Fulgent Genetics Inc. (U.S.), OPKO Health Inc. (U.S.), Metropolis Healthcare Ltd. (India), and Dr. Lal PathLabs Limited (India), among others.

Asia-Pacific is expected to register the highest growth rate in the global clinical laboratory services market during the forecast period 2026-2036, driven by India's rapidly expanding diagnostic chains serving its large and growing patient population, China's healthcare infrastructure investment, and the region's very large and increasing chronic disease burden creating sustained demand for diagnostic services.

1. Introduction

1.1. Market Definition

1.2. Market Ecosystem

1.3. Currency and Limitations

1.3.1. Currency

1.3.2. Limitations

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Data Collection & Validation Process

2.2.1. Secondary Research

2.2.2. Primary Research & Validation

2.2.2.1. Primary Interviews with Experts

2.2.2.2. Approaches for Country-/Region-Level Analysis

2.3. Market Estimation

2.3.1. Bottom-Up Approach

2.3.2. Top-Down Approach

2.3.3. Growth Forecast

2.4. Data Triangulation

2.5. Assumptions for the Study

3. Executive Summary

4. Market Overview

4.1. Introduction

4.2. Market Dynamics

4.2.1. Drivers

4.2.1.1. Rising Prevalence of Chronic and Infectious Diseases

4.2.1.2. Increasing Demand for Early and Accurate Diagnosis

4.2.1.3. Growth in Personalized and Precision Medicine

4.2.1.4. Expansion of Preventive Healthcare and Screening Programs

4.2.2. Restraints

4.2.2.1. High Cost of Advanced Diagnostic Tests

4.2.2.2. Reimbursement Challenges

4.2.2.3. Shortage of Skilled Laboratory Professionals

4.2.3. Opportunities

4.2.3.1. Adoption of Automation and AI in Laboratory Testing

4.2.3.2. Growth in Genomic and Molecular Diagnostics

4.2.3.3. Expansion in Emerging Markets

4.2.3.4. Integration with Digital Health and Telemedicine

4.2.4. Challenges

4.2.4.1. Regulatory Compliance and Quality Standards

4.2.4.2. Data Management and Interoperability Issues

4.3. Technology Landscape

4.3.1. Clinical Chemistry and Immunoassay Platforms

4.3.2. Molecular Diagnostics and PCR Technologies

4.3.3. Next-Generation Sequencing (NGS)

4.3.4. Laboratory Automation and Robotics

4.3.5. Digital Pathology and AI Integration

4.4. Clinical Laboratory Ecosystem

4.4.1. Sample Collection and Logistics

4.4.2. Laboratory Testing and Analysis

4.4.3. Data Interpretation and Reporting

4.4.4. Digital Integration and Health IT Systems

4.4.5. End-User Delivery Channels

4.5. Value Chain Analysis

4.5.1. Reagent and Equipment Suppliers

4.5.2. Diagnostic Laboratory Service Providers

4.5.3. Healthcare Providers (Hospitals/Clinics)

4.5.4. Payers and Insurance Providers

4.5.5. Patients and End Users

4.6. Regulatory and Standards Landscape

4.6.1. CLIA Regulations (U.S.)

4.6.2. ISO and Laboratory Accreditation Standards

4.6.3. Data Privacy Regulations (HIPAA, GDPR)

4.7. Porter's Five Forces Analysis

4.8. Investment and Industry Trends

4.8.1. Consolidation of Laboratory Service Providers

4.8.2. Growth in Specialty and Esoteric Testing

4.8.3. Expansion of At-Home Testing Services

4.9. Cost and Pricing Analysis

4.9.1. Pricing by Test Type

4.9.2. Reimbursement Models

4.9.3. Cost Efficiency through Automation

5. Clinical Laboratory Services Market, by Test Type

5.1. Introduction

5.2. Clinical Chemistry Tests

5.3. Immunology and Serology Tests

5.4. Molecular Diagnostics

5.4.1. PCR-Based Testing

5.4.2. Next-Generation Sequencing (NGS)

5.5. Hematology Tests

5.6. Microbiology Tests

5.7. Genetic and Genomic Testing

5.8. Toxicology and Drug Testing

5.9. Other Tests

6. Clinical Laboratory Services Market, by Service Provider

6.1. Introduction

6.2. Hospital-Based Laboratories

6.3. Independent and Reference Laboratories

6.4. Physician Office Laboratories

6.5. Public Health Laboratories

7. Clinical Laboratory Services Market, by Application

7.1. Introduction

7.2. Disease Diagnosis (Largest Segment)

7.2.1. Infectious Diseases

7.2.2. Chronic Diseases (Diabetes, Cardiovascular, Cancer)

7.3. Preventive Screening

7.3.1. Routine Health Checkups

7.3.2. Cancer Screening Programs

7.4. Drug Development and Clinical Trials

7.4.1. Biomarker Testing

7.4.2. Companion Diagnostics

7.5. Personalized and Precision Medicine

7.5.1. Genomic Profiling

7.5.2. Targeted Therapy Selection

7.6. Other Applications

8. Clinical Laboratory Services Market, by End User

8.1. Introduction

8.2. Hospitals

8.3. Clinics

8.4. Pharmaceutical and Biotechnology Companies

8.5. Research Institutions

8.6. Patients (Direct-to-Consumer Testing)

9. Clinical Laboratory Services Market, by Mode of Testing

9.1. Introduction

9.2. Centralized Laboratory Testing

9.3. Point-of-Care Testing (POCT)

9.4. At-Home Testing

10. Clinical Laboratory Services Market, by Technology Type

10.1. Introduction

10.2. Manual Testing

10.3. Automated Testing

10.4. AI-Enabled and Digital Diagnostics

11. Clinical Laboratory Services Market, by Geography

11.1. Introduction

11.2. North America

11.2.1. U.S.

11.2.2. Canada

11.3. Europe

11.3.1. Germany

11.3.2. U.K.

11.3.3. France

11.3.4. Italy

11.3.5. Spain

11.3.6. Netherlands

11.3.7. Sweden

11.3.8. Switzerland

11.3.9. Rest of Europe

11.4. Asia-Pacific

11.4.1. China

11.4.2. India

11.4.3. Japan

11.4.4. South Korea

11.4.5. Australia

11.4.6. Singapore

11.4.7. Thailand

11.4.8. Indonesia

11.4.9. Vietnam

11.4.10. Rest of Asia-Pacific

11.5. Latin America

11.5.1. Brazil

11.5.2. Mexico

11.5.3. Argentina

11.5.4. Chile

11.5.5. Colombia

11.5.6. Rest of Latin America

11.6. Middle East & Africa

11.6.1. Saudi Arabia

11.6.2. UAE

11.6.3. South Africa

11.6.4. Israel

11.6.5. Turkey

11.6.6. Rest of Middle East & Africa

12. Competitive Landscape

12.1. Overview

12.2. Key Growth Strategies

12.3. Competitive Benchmarking

12.4. Competitive Dashboard

12.4.1. Industry Leaders

12.4.2. Market Differentiators

12.4.3. Vanguards

12.4.4. Emerging Companies

12.5. Market Ranking/Positioning Analysis of Key Players, 2025

13. Company Profiles

(Business Overview, Financial Overview, Service Portfolio, Strategic Developments, SWOT Analysis)

13.1. Quest Diagnostics Incorporated

13.2. Laboratory Corporation of America Holdings (Labcorp)

13.3. Sonic Healthcare Limited

13.4. Eurofins Scientific SE

13.5. SYNLAB International GmbH

13.6. BioReference Laboratories, Inc.

13.7. Mayo Clinic Laboratories

13.8. ARUP Laboratories

13.9. Unilabs

13.10. Cerba HealthCare

13.11. Exact Sciences Corporation

13.12. Fulgent Genetics, Inc.

13.13. OPKO Health, Inc.

13.14. Metropolis Healthcare Ltd.

13.15. Dr. Lal PathLabs Limited

14. Appendix

14.1. Additional Customization

14.2. Related Reports

Published Date: Jan-2025

Published Date: Jan-2025

Published Date: Jun-2024

Published Date: Jun-2024

Published Date: Jan-2024

Subscribe to get the latest industry updates