Resources

About Us

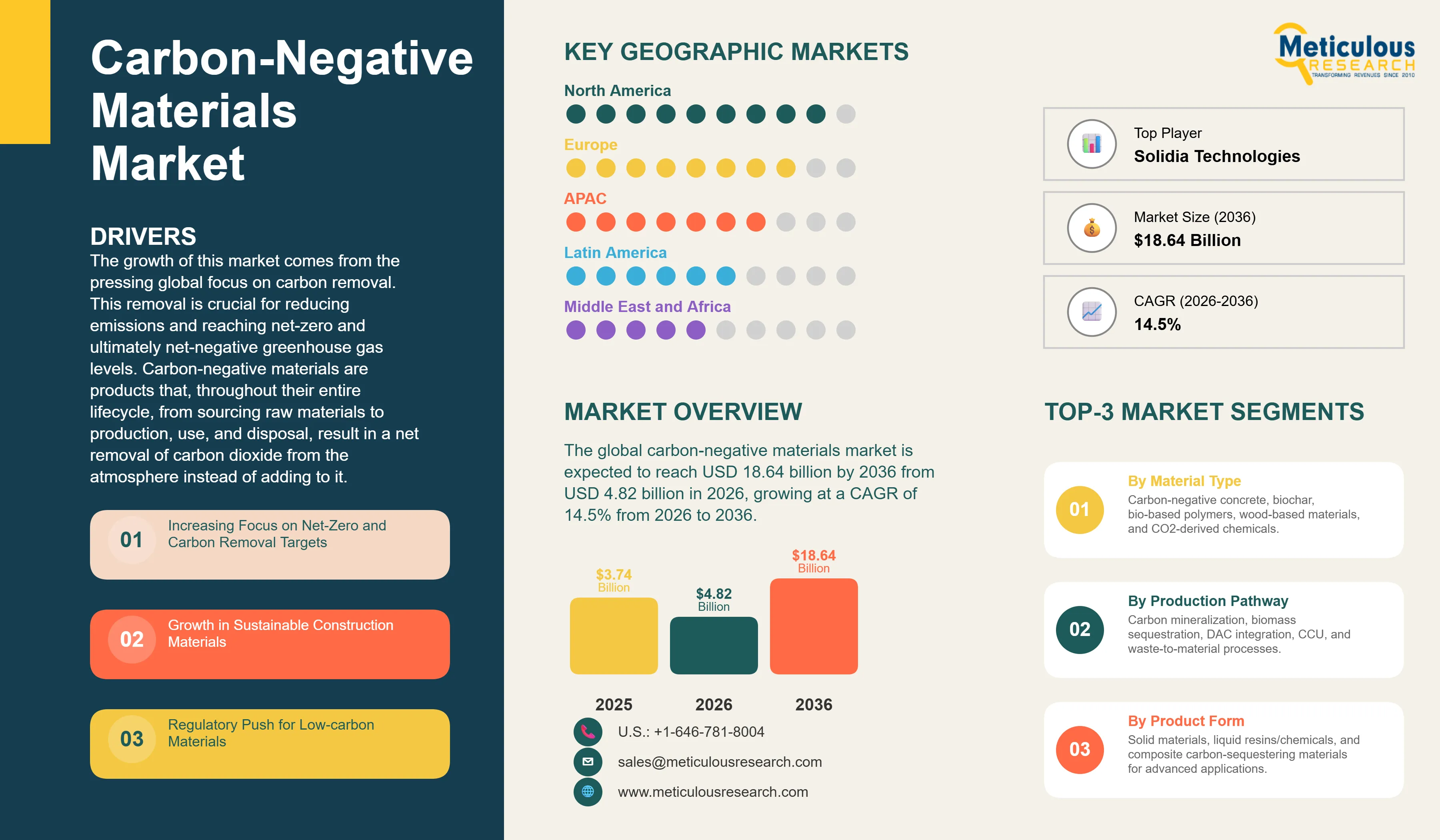

The global carbon-negative materials market was valued at USD 3.74 billion in 2025. This market is expected to reach USD 18.64 billion by 2036 from USD 4.82 billion in 2026, growing at a CAGR of 14.5% from 2026 to 2036.

The growth of this market comes from the pressing global focus on carbon removal. This removal is crucial for reducing emissions and reaching net-zero and ultimately net-negative greenhouse gas levels. Carbon-negative materials are products that, throughout their entire lifecycle, from sourcing raw materials to production, use, and disposal, result in a net removal of carbon dioxide from the atmosphere instead of adding to it. This occurs through various methods. These include permanently turning CO2 into construction materials, producing biochar that holds biogenic carbon in a solid form for centuries, creating bio-based polymers and engineered wood products that store carbon captured during photosynthesis, and using captured CO2 as a raw material for chemicals, materials, and fuels.

According to the IPCC Special Report on Global Warming of 1.5 degrees Celsius, nearly all pathways examined for limiting warming to 1.5 degrees Celsius depend on carbon removal methods to achieve net negative emissions. The IEA has found that agriculture, forestry, and land-use practices that use carbon-negative materials could remove between 1 billion and 11 billion tonnes of CO2 annually by 2050 in pathways that limit warming to 1.5 degrees. Meanwhile, the IEA's Breakthrough Agenda Report 2024 on Cement states that total CO2 emissions from the cement sector are now higher than in 2015. This sector contributes about 7% of global CO2 emissions, making it a key area for using carbon-negative construction materials. The IEA estimates that production costs for early commercial plants making near-zero emission cement with carbon capture and storage are 75-150% higher than those of today’s conventional plants. This shows both the size of the commercial opportunity and the higher prices that carbon-negative cement producers can obtain.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Carbon-negative materials are defined by their lifecycle carbon accounting. The net CO2 removed from the atmosphere during the material's entire lifecycle exceeds the CO2 emitted during its production, transportation, use, and disposal. This definition sets carbon-negative materials apart from low-carbon or carbon-neutral products, which lower emissions compared to traditional standards but do not achieve net carbon removal. Various mechanisms contribute to the carbon-negative outcome. In carbon mineralization, CO2 binds chemically into the crystalline structure of calcium carbonate or similar minerals within construction materials. This process permanently stores atmospheric or captured industrial CO2 in a stable solid form. In biomass-based sequestration, carbon captured through plant photosynthesis gets incorporated into biochar, engineered timber, or bio-based plastics, where it can be stored for decades to centuries. In direct air capture systems, CO2 removed from the air by mechanical systems is used as a feedstock for material production instead of being stored underground.

The market includes five main material categories. Carbon-negative concrete and cement feature products like CarbonCure's recarbonation concrete technology. This technology injects CO2 captured from industrial sources into fresh concrete, where it mineralizes permanently into calcium carbonate. Solidia Technologies uses a low-temperature cement formulation that cures by absorbing CO2. CarbiCrete has created cement-free concrete using steel slag as the binder, which cures with CO2. Blue Planet Systems mineralizes CO2 into synthetic limestone aggregate. Biochar-based materials involve char created by pyrolyzing biomass without oxygen. This process stores the biogenic carbon of the original plant material in a stable form with a lifespan of centuries to millennia in soil. Bio-based plastics use atmospheric CO2 from plant biomass as the carbon source for production. Engineered wood products, such as cross-laminated timber and glued laminated timber, structurally store the biogenic carbon captured during forest growth. Companies like LanzaTech, Twelve Benefit Corporation, and Novomer create CO2-derived chemicals and materials using captured CO2 as a feedstock for fuels, plastics, and specialty chemicals.

The competitive landscape for carbon-negative materials includes materials science startups with new production technologies, large construction companies developing low-carbon products, and carbon credit market players who capitalize on the carbon removal value of certified carbon-negative materials. CarbonCure Technologies is the most widely deployed company, with its CO2 mineralization technology licensed to many concrete producers. Cemex, one of the largest cement producers globally, is developing carbon-negative concrete products and aims for carbon neutrality. Climeworks, the leading direct air capture company, may supply upstream CO2 for carbon-negative materials production. Made of Air GmbH produces biochar-based thermoplastic materials from pyrolyzed biomass. Charm Industrial transforms plant biomass into bio-oil for permanent geological storage, generating revenue from carbon removal credits. According to the IEA's Breakthrough Agenda Report 2025 on Cement and Concrete, the Netherlands, Sweden, Germany, France, the United Kingdom, and the United States lead in adopting regulations on low-carbon concrete and construction as well as implementing supportive public procurement initiatives, pinpointing the main commercial markets for carbon-negative construction materials.

Government Procurement Mandates Creating Direct Demand for Carbon-Negative Construction Materials

The adoption of embodied carbon requirements in public infrastructure procurement specifications by national and regional governments is the most impactful near-term factor driving demand for carbon-negative construction materials. Public procurement is the largest category of concrete and structural material purchasing in most economies. When governments require low-carbon or carbon-negative material specifications, they create immediate demand that ensures revenue for producers and speeds up adoption.

According to the IEA's Breakthrough Agenda Report 2024 on Cement, governments and industry should work together through existing forums and with international standards bodies. They need to implement priority revisions by the end of 2025 to ensure the interoperability and net-zero compatibility of cement and concrete emissions accounting methods. Governments should also clarify principles for near-zero and low-emission cement and concrete definitions and commit to adopting these definitions within national policies by the end of 2025.

The IEA specifically named the Netherlands, Sweden, Germany, France, the United Kingdom, and the United States as leaders in regulating low-carbon concrete and construction and in supporting public procurement schemes. In the United States, the Inflation Reduction Act's Environmental Product Declaration requirements for federal procurement and Buy Clean provisions for low-embodied-carbon construction materials in federally funded projects are creating the most significant government procurement mandate for low-carbon construction materials implemented so far. This is directly increasing demand for carbon-negative concrete and engineered timber products in U.S. infrastructure investment.

IPCC and IEA Recognition of Carbon Removal Materials as Essential Net-Zero Pathway Elements

The IPCC and IEA recognize that removing carbon dioxide from the atmosphere is crucial for keeping global warming to 1.5 degrees Celsius. This recognition boosts credibility for the carbon-negative materials market and draws interest from policymakers, private investors, and companies. The IEA's report, Going Carbon Negative: What Are the Technology Options, shows that nearly all pathways examined by IPCC authors depend on carbon removal methods to reach net negative emissions. The IPCC Special Report on Global Warming of 1.5 Degrees Celsius noted that agriculture, forestry, and land-use strategies could remove between 1 billion and 11 billion tonnes of CO2 per year by 2050 under scenarios compatible with the 1.5-degree target. Improved land management techniques, including deploying biochar, contribute to this removal potential. The IPCC held its first Expert Meeting on Carbon Dioxide Removal Technologies in Vienna in July 2024. This meeting was the first step in preparing a Methodology Report on CDR technologies for acceptance by the IPCC Panel. This confirms the agency's commitment to creating strong measurement, reporting, and verification systems for carbon removal, which will support carbon credit certification and promote carbon-negative materials markets worldwide.

|

Parameter |

Details |

|

Market Size by 2036 |

USD 18.64 Billion |

|

Market Size in 2026 |

USD 4.82 Billion |

|

Market Size in 2025 |

USD 3.74 Billion |

|

Market Growth Rate (2026-2036) |

CAGR of 14.5% |

|

Dominating Region |

North America |

|

Fastest Growing Region |

Europe |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Material Type, Production Pathway, Product Form, Application, End User, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Driver: Mandatory Decarbonization of the Construction Sector and Cement Industry

The main factor driving the carbon-negative materials market is the required decarbonization path for the construction sector. This sector is responsible for about 40% of global energy-related CO2 emissions, as reported by the IEA. The cement industry alone accounts for around 7% of global CO2 emissions and is the second-largest industrial CO2 emitter in the world. The IEA's Breakthrough Agenda Report 2024 on Cement shows that total CO2 emissions from this sector are now higher than in 2015. Both the IEA's Net Zero Emissions by 2050 Scenario and the Paris Agreement goals demand a reduction of approximately 20% in cement sector emissions by 2030 from current levels. The IEA's Breakthrough Agenda Report 2025 on Cement and Concrete confirmed that total CO2 emissions are still higher than in 2015 and that the direct CO2 emissions intensity has not changed. This indicates that traditional cement production is not decarbonizing on its own. Regulatory action and alternative material solutions are necessary. The IEA's Net Zero Emissions scenario emphasizes that carbon capture and storage (CCS) must play a significant role in reducing emissions in the cement sector. Producing carbon-negative cement through CO2 mineralization, supplementary cementitious materials, and carbon capture integration addresses this regulatory need, creating lasting demand for carbon-negative concrete and cement products.

Opportunity: Carbon Credit Market Monetization of Carbon Removal Value

The rise of effective carbon credit markets for removing carbon dioxide is creating an important new source of income for producers of carbon-negative materials. These producers can generate verified, permanent carbon removal credits from their processes. Carbon removal credits certify that a specific amount of CO2 has been permanently removed from the atmosphere. This ensures that it will not re-enter the carbon cycle within a set timeframe. These credits often receive higher price premiums compared to regular carbon offset credits. Companies like Charm Industrial convert biomass into bio-oil for permanent geological storage while selling carbon removal credits to tech firms like Stripe, Google, and Microsoft. They show that revenue from carbon removal credits can either help support or even drive the economic viability of carbon-negative materials businesses.

In July 2024, the IPCC will hold an Expert Meeting on CDR Methodology in Vienna. This will kick off the creation of an IPCC Methodology Report on carbon dioxide removal technologies. This move highlights the growing commitment from the scientific and policy communities to develop solid measurement and verification systems that will support reliable carbon removal credit markets. As these systems improve and offer more certainty to businesses buying carbon removal credits, the size and activity of both voluntary and compliance carbon removal credit markets are expected to increase significantly. This growth will enhance the economic viability of producing carbon-negative materials over the coming years.

Why Does Carbon-Negative Concrete and Cement Lead the Market?

In 2026, the carbon-negative concrete and cement segment is expected to have the largest share of the global market. Concrete is the most commonly used construction material in the world. The cement industry contributes about 7% of global CO2 emissions according to the IEA. This makes it the biggest carbon emitter in the materials sector and the greatest opportunity for using carbon-negative materials as substitutes. The IEA's Breakthrough Agenda Report 2024 states that total CO2 emissions from the cement sector are now higher than they were in 2015. This highlights the urgent need for decarbonization and the business potential for low-carbon and carbon-negative alternatives. CarbonCure Technologies injects captured CO2 into fresh concrete, where it permanently mineralizes into calcium carbonate. It has achieved the widest commercial use of any carbon-negative construction material technology, with its systems in hundreds of concrete producers in North America and around the world. Solidia Technologies, CarbiCrete, and Prometheus Materials are some of the companies developing additional carbon-negative cement and concrete technologies for different market segments.

On the other hand, the biochar-based materials segment is expected to grow the fastest during the forecast period. Biochar is made by heating biomass without oxygen in a process called pyrolysis. This process turns the easily decomposed biogenic carbon from the original plant into a stable aromatic carbon form, which can last in soil for hundreds to thousands of years. The IPCC recognizes biochar as an established method for removing greenhouse gases in its assessment reports. The IEA also notes that biochar is a land management approach that boosts soil carbon content and helps reduce CO2 levels in the atmosphere. A peer-reviewed study in Nature Communications (Deng et al., February 2024) found that biochar could potentially remove up to 0.92 billion tonnes of CO2 each year in China, with an average net cost of USD 90 per tonne of CO2. This confirms biochar's significant potential for carbon removal in one of the world's largest economies.

How Does Carbon Mineralization Lead the Production Pathway Market?

In 2026, the carbon mineralization segment is expected to have the largest share of the market for carbon-negative materials by production pathway. Carbon mineralization converts CO2 into stable solid carbonate minerals through chemical reactions with calcium- or magnesium-rich materials. This method permanently sequesters carbon in a geologically stable form that does not break down or release the stored carbon under normal conditions. This production pathway is commercially validated at scale through CarbonCure Technologies' platform and Blue Planet Systems' synthetic limestone aggregate technology. Carbon mineralization is particularly appealing because it can fit into existing concrete production systems without requiring entirely new manufacturing processes. This reduces the barrier for concrete producers to adopt it. The IEA's Net Zero Emissions scenario highlights carbon capture and storage, which carbon mineralization addresses in a materials context, as a crucial part of the emissions reductions needed in the cement sector to reach net zero. This provides strong policy support for carbon mineralization.

On the other hand, the direct air capture integration segment is expected to grow the fastest during the forecast period. DAC-integrated carbon-negative materials represent the most reliable carbon removal pathway. The CO2 used in material production comes directly from the air through mechanical capture. This offers additionality that is easy to verify and certify for carbon credit purposes. As DAC costs continue to drop due to learning curves and increased scale, and as government incentives like the U.S. Inflation Reduction Act's Section 45Q tax credit for direct air capture provide financial support, the cost of DAC-sourced CO2 as a feedstock for carbon-negative materials is expected to improve compared to conventional CO2 sources. This will expand the commercial viability of DAC-integrated material production during the forecast period.

Why Do Solid Materials Lead the Product Form Market?

In 2026, the solid materials segment is expected to have the largest share of the carbon-negative materials market by product form. Solid carbon-negative materials, including concrete blocks and panels, biochar, cross-laminated timber, and carbon-mineralized aggregates, represent the most widely used and highest-volume category of carbon-negative materials. The construction sector is the main application for carbon-negative materials, which is why solid product forms are so prevalent. Building and infrastructure construction mainly relies on solid structural and cladding materials. The durability and longevity of solid carbon-negative materials also make for a clear case for carbon sequestration claims. The carbon stored in a concrete block or timber beam is likely to stay sequestered for the life of the building or infrastructure, usually lasting 50 to 100 years or more.

However, the composite materials segment is expected to grow the fastest during this period. New composite materials that use carbon-negative matrix materials or reinforcing components are being developed for automotive, aerospace, and infrastructure applications where high performance and carbon negativity must go together. Made of Air GmbH's biochar-based thermoplastic composites use pyrolyzed biomass char in polymer matrices to create carbon-negative structural and aesthetic materials. This represents a new category of high-value composite carbon-negative materials that sell for a premium in automotive interiors, architectural projects, and consumer products.

Why Does Construction and Infrastructure Lead the Application Market?

In 2026, the construction and infrastructure sector is predicted to have the largest share of the carbon-negative materials market. The built environment is responsible for about 40% of global energy-related CO2 emissions, according to the IEA. This makes it a key target for reducing carbon through materials. The cement industry alone contributes about 7% of global CO2 emissions and must cut emissions by around 20% by 2030 to meet net-zero goals, according to the IEA's Breakthrough Agenda Report on Cement and the IEA Net Zero scenario. The construction sector’s high material use, the lengthy lifespan of buildings and infrastructure that allow for long-term carbon storage, and increasing regulations for reducing embodied carbon in buildings all make construction the leading area for carbon-negative materials. The IEA points out that the Netherlands, Sweden, Germany, France, the United Kingdom, and the United States are leading in setting regulations for low-carbon concrete construction. This shows that public procurement requirements for carbon-negative construction materials are developing most quickly in these major markets.

On the other hand, the agriculture and soil enhancement segment is expected to experience the fastest growth during the forecast period. The use of biochar in agricultural soils is quickly gaining regulatory support and commercial use as a method that captures biogenic carbon in stable soil form while also improving soil fertility, water retention, and microbial activity. The IPCC recognizes biochar as a valid technique for removing greenhouse gases. The IPCC will start working on methodology for carbon removal technologies in 2024, creating a scientific basis that will help with policy incentives and carbon credit certification for agricultural biochar use. Countries like the United Kingdom are considering biochar as part of their greenhouse gas removal strategies under their legally binding Net Zero commitments.

Why Do Construction and Infrastructure Companies Lead the End User Market?

In 2026, the construction and infrastructure companies segment is expected to hold the largest share of the carbon-negative materials market. Major construction firms, real estate developers, and public infrastructure owners are the main buyers of carbon-negative concrete, engineered timber, and other carbon-sequestering building materials. This demand is driven by voluntary green building certification, mandatory embodied carbon specifications in public procurement, and corporate net-zero commitments that include Scope 3 supply chain emissions from construction materials. The IEA Breakthrough Agenda Report 2024 confirms that governments in the Netherlands, Sweden, Germany, France, the United Kingdom, and the United States are implementing procurement schemes that specifically require low-carbon and near-zero-emission concrete and construction materials. These measures create mandatory procurement demand from the public construction sector in these leading markets. Corporate real estate developers and construction companies with science-based targets under the Science Based Targets initiative increasingly need to address embodied carbon in their building portfolios. This need drives the voluntary procurement of carbon-negative materials, independent of regulatory mandates.

However, the government and public sector end-user segment is projected to see the fastest growth during the forecast period. Government bodies at national, regional, and municipal levels are becoming the most important buyers in the carbon-negative materials market. Public infrastructure procurement represents the largest category of construction material purchases. Additionally, government procurement mandates create market demand that speeds up private sector adoption. The IEA's recommendation in its Breakthrough Agenda Report 2024 suggests that governments should implement high-quality, multi-year advance purchase commitments and policy support for near-zero emission cement and concrete. This highlights the strategic role of government procurement in developing the market for carbon-negative construction materials. In the United States, the Inflation Reduction Act's Buy Clean provisions and Environmental Product Declaration requirements for federally funded construction are setting up the most significant and measurable government procurement mandate for low-carbon construction materials in the world.

How is North America Maintaining Market Leadership?

In 2026, North America is expected to have the largest share of the global carbon-negative materials industry. The United States is the main market, pushed by the presence of key technology companies in carbon-negative materials, strong federal policy support from the Inflation Reduction Act, and the increasing adoption of embodied carbon requirements in public infrastructure procurement.

The United States is home to the most widely used carbon-negative concrete technology in the world through CarbonCure Technologies' platform, which many concrete producers across North America have adopted. The IEA has recognized the United States as one of six leading countries in creating regulations for low-carbon concrete and in supporting public procurement schemes. The Section 45Q tax credit in the Inflation Reduction Act gives financial support for direct air capture and carbon storage, including the production of carbon-negative materials that integrate DAC technology. Additionally, the Buy Clean provisions in the Act for federal procurement of low-embodied-carbon construction materials are generating demand for carbon-negative concrete and timber in U.S. infrastructure projects. Canada also helps meet regional demand through government carbon pricing under the federal carbon levy, which encourages the procurement of carbon-negative materials to avoid carbon costs. Furthermore, there is active commercial deployment of CarbonCure's technology in producing concrete in Canada.

Which Factors Drive Europe's Rapid Growth?

Europe is expected to grow the fastest in the carbon-negative materials market during the forecast period. This growth comes from the European Climate Law's firm commitment to net-zero emissions by 2050 and net-negative emissions afterward. The EU is taking the lead in creating rules for low-carbon and carbon-negative construction materials. The IEA has identified the Netherlands, Sweden, Germany, France, and the United Kingdom as leaders in adopting regulations for low-carbon concrete and supporting public procurement programs.

According to the IEA Breakthrough Agenda Report 2024 on Cement, the IEA suggests that governments share best practices and speed up changes to building codes and public procurement practices by the end of 2025. This aims to maximize the use of supplementary cementitious materials and near-zero emission cement. Several European countries are already putting these suggestions into action. Sweden has some of the world’s most progressive procurement requirements for low-embodied-carbon construction materials in public buildings. The Netherlands' Green Deal for concrete promotes a shift to low-carbon and carbon-negative concrete formulations. The European Union’s Innovation Fund, backed by income from the EU Emissions Trading System, has committed billions of euros to large-scale demonstrations of groundbreaking low-carbon and carbon-negative industrial technologies. This includes projects for carbon-negative cement and concrete in Germany, the Netherlands, and other EU member countries. The United Kingdom's legally binding net-zero target under the Climate Change Act, along with the UK government's Greenhouse Gas Removal program that supports biochar and other carbon removal technologies, is driving regulatory and research investment in carbon-negative materials in the UK construction and agricultural sectors.

Some of the key companies operating in the global carbon-negative materials industry are CarbonCure Technologies, Solidia Technologies, Blue Planet Systems, Climeworks AG, Charm Industrial, LanzaTech Global Inc., Twelve Benefit Corporation, Novomer Inc., CarbiCrete Inc., Prometheus Materials, Biochar Now LLC, Made of Air GmbH, Mineral Carbonation International, Cemex S.A.B. de C.V., and CarbonBuilt.

The global carbon-negative materials market is expected to grow from USD 4.82 billion in 2026 to USD 18.64 billion by 2036.

The global carbon-negative materials market is projected to grow at a CAGR of 14.5% from 2026 to 2036.

The carbon-negative concrete and cement segment is expected to dominate the overall market in 2026, anchored by the cement industry's 7% share of global CO2 emissions identified by the IEA and the commercial deployment of CarbonCure's CO2 mineralization technology. However, the biochar-based materials segment is expected to witness the fastest CAGR, supported by IPCC recognition of biochar as an established greenhouse gas removal method and growing government and corporate procurement of biochar carbon removal credits.

The construction and infrastructure segment is expected to dominate the overall market in 2026, driven by the built environment's 40% share of global energy-related CO2 emissions per the IEA and mandatory low-carbon procurement requirements in leading markets. However, the agriculture and soil enhancement segment is expected to witness the fastest CAGR, driven by biochar's dual agricultural and carbon sequestration benefits and the IPCC's advancing methodology for carbon removal verification.

North America is expected to lead the global market in 2026, supported by U.S. federal policy through the IRA's Buy Clean provisions and Section 45Q tax credit. However, Europe is expected to witness the fastest CAGR, driven by the EU Climate Law's net-negative emissions mandate and the IEA's identification of five European countries as frontrunners in low-carbon concrete regulation and procurement.

The major players are CarbonCure Technologies, Solidia Technologies, Blue Planet Systems, Climeworks AG, Charm Industrial, LanzaTech Global, Twelve Benefit Corporation, Novomer, CarbiCrete, Prometheus Materials, Biochar Now, Made of Air GmbH, Mineral Carbonation International, Cemex, and CarbonBuilt.

1. Introduction

1.1 Market Definition (Carbon-Negative Materials & Carbon-Sequestering Products)

1.2 Scope (Construction Materials, Polymers, Bio-based Materials, Carbon Mineralization)

1.3 Market Ecosystem

1.4 Currency and Limitations

1.4.1 Currency

1.4.2 Limitations

1.5 Key Stakeholders

2. Research Methodology

2.1 Research Approach

2.2 Data Collection & Validation

2.2.1 Secondary Research

2.2.2 Primary Research (Material Scientists, Climate-tech Firms, Construction Companies)

2.3 Market Estimation

2.3.1 Bottom-Up Approach

2.3.2 Top-Down Approach

2.3.3 Forecast Modeling

2.4 Data Triangulation

2.5 Assumptions

3. Executive Summary

4. Market Overview

4.1 Introduction

4.2 Market Dynamics

4.2.1 Drivers

4.2.1.1 Increasing Focus on Net-Zero and Carbon Removal Targets

4.2.1.2 Growth in Sustainable Construction Materials

4.2.1.3 Regulatory Push for Low-carbon Materials

4.2.1.4 Corporate ESG Commitments

4.2.2 Restraints

4.2.2.1 High Production Costs

4.2.2.2 Limited Commercial-scale Deployment

4.2.2.3 Lack of Standardized Carbon Accounting

4.2.3 Opportunities

4.2.3.1 Development of Carbon Mineralization Technologies

4.2.3.2 Integration with Carbon Capture and Storage (CCS)

4.2.3.3 Expansion in Infrastructure and Construction

4.2.3.4 Growth in Carbon Credit Markets

4.2.4 Challenges

4.2.4.1 Scalability and Supply Chain Constraints

4.2.4.2 Verification of Carbon-Negative Claims

4.3 Technology & Production Landscape

4.3.1 Carbon Mineralization Technologies

4.3.2 Bio-based Material Production (Biomass, Algae-based)

4.3.3 Carbon Capture Utilization (CCU) Integration

4.3.4 Biochar Production

4.3.5 Advanced Polymer Synthesis (CO2-based Polymers)

4.3.6 Industrial Waste Utilization

4.4 Carbon-Negative Materials Ecosystem

4.4.1 Material Manufacturers

4.4.2 Construction & Infrastructure Companies

4.4.3 Carbon Capture Technology Providers

4.4.4 Government & Regulatory Bodies

4.4.5 Carbon Credit Market Participants

4.5 Value Chain Analysis

4.5.1 Raw Material Sourcing (CO2, Biomass, Industrial Waste)

4.5.2 Material Processing & Production

4.5.3 Product Manufacturing

4.5.4 Distribution & Deployment

4.5.5 Carbon Accounting & Certification

4.6 Regulatory Landscape

4.6.1 Carbon Emission Regulations

4.6.2 Green Building Standards

4.6.3 Carbon Credit Certification Frameworks

4.7 Industry Trends

4.7.1 Rise of Carbon-Negative Concrete & Cement

4.7.2 Increasing Investment in Climate-tech Startups

4.7.3 Integration with Circular Economy Models

4.7.4 Expansion of Carbon Credit Markets

4.8 Cost and Pricing Analysis

4.8.1 Cost by Material Type

4.8.2 Cost vs Traditional Materials Comparison

4.8.3 Carbon Credit Monetization

5. Carbon-Negative Materials Market, by Material Type

5.1 Introduction

5.2 Carbon-Negative Concrete & Cement

5.3 Biochar-based Materials

5.4 Bio-based Polymers & Plastics

5.5 Wood-based Engineered Materials

5.6 CO2-derived Chemicals & Materials

5.7 Other Materials

6. Carbon-Negative Materials Market, by Production Pathway

6.1 Carbon Mineralization

6.2 Biomass-based Sequestration

6.3 Direct Air Capture (DAC) Integration

6.4 Industrial Carbon Capture Utilization (CCU)

6.5 Waste-to-material Processes

7. Carbon-Negative Materials Market, by Product Form

7.1 Solid Materials (Concrete, Panels, Blocks)

7.2 Liquid Materials (Resins, Chemicals)

7.3 Composite Materials

8. Carbon-Negative Materials Market, by Application

8.1 Introduction

8.2 Construction & Infrastructure

8.2.1 Residential Construction

8.2.2 Commercial Construction

8.2.3 Public Infrastructure

8.3 Packaging & Consumer Goods

8.4 Automotive & Transportation

8.5 Energy & Industrial Applications

8.6 Agriculture & Soil Enhancement (Biochar)

9. Carbon-Negative Materials Market, by End User

9.1 Construction & Infrastructure Companies

9.2 Manufacturing & Industrial Sector

9.3 Packaging Industry

9.4 Automotive Industry

9.5 Government & Public Sector

10. Carbon-Negative Materials Market, by Geography

10.1 Introduction

10.2 North America

10.2.1 U.S.

10.2.2 Canada

10.3 Europe

10.3.1 Germany

10.3.2 U.K.

10.3.3 France

10.3.4 Netherlands

10.3.5 Sweden

10.3.6 Rest of Europe

10.4 Asia-Pacific

10.4.1 China

10.4.2 India

10.4.3 Japan

10.4.4 South Korea

10.4.5 Australia

10.4.6 Southeast Asia

10.4.7 Rest of Asia-Pacific

10.5 Latin America

10.5.1 Brazil

10.5.2 Mexico

10.5.3 Rest of Latin America

10.6 Middle East & Africa

10.6.1 UAE

10.6.2 Saudi Arabia

10.6.3 South Africa

10.6.4 Rest of MEA

11. Competitive Landscape

11.1 Overview

11.2 Key Growth Strategies

11.3 Competitive Benchmarking

11.4 Competitive Dashboard

11.4.1 Industry Leaders

11.4.2 Technology Innovators

11.4.3 Emerging Startups

11.5 Market Ranking/Positioning Analysis

12. Company Profiles

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

12.1 CarbonCure Technologies

12.2 Solidia Technologies

12.3 Blue Planet Systems

12.4 Climeworks AG

12.5 Charm Industrial

12.6 LanzaTech Global Inc.

12.7 Twelve Benefit Corporation

12.8 Novomer Inc.

12.9 CarbiCrete Inc.

12.10 Prometheus Materials

12.11 Biochar Now LLC

12.12 Hempcrete companies

12.13 Made of Air GmbH

12.14 Mineral Carbonation International

12.15 Cemex S.A.B. de C.V.

13. Appendix

13.1 Customization Options

13.2 Related Reports

Published Date: Apr-2026

Published Date: Feb-2025

Published Date: Sep-2024

Published Date: May-2024

Published Date: Apr-2024

Subscribe to get the latest industry updates