Resources

About Us

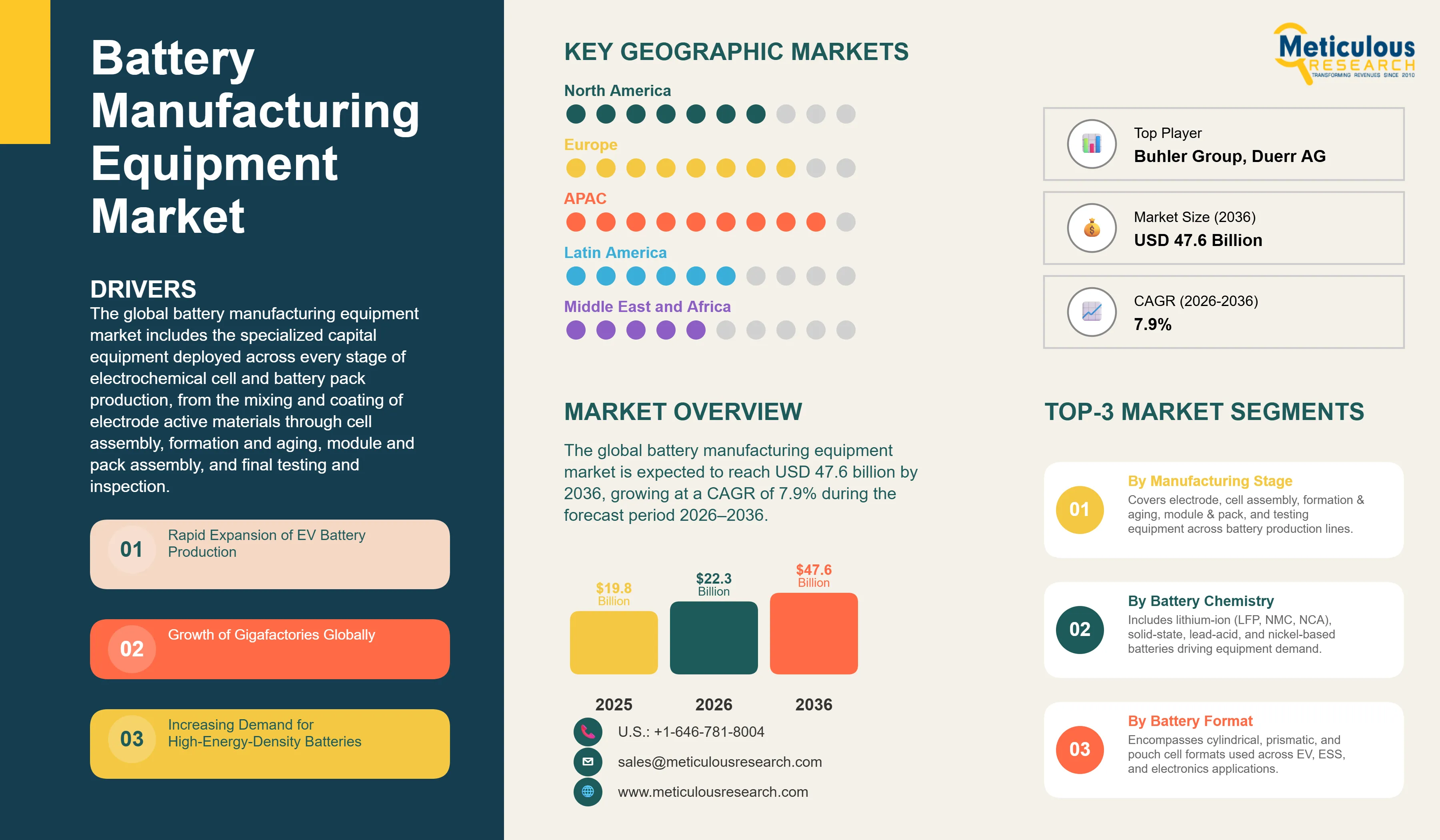

The global battery manufacturing equipment market was valued at USD 19.8 billion in 2025. This market is expected to reach USD 47.6 billion by 2036 from an estimated USD 22.3 billion in 2026, growing at a CAGR of 7.9% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global battery manufacturing equipment market includes the specialized capital equipment deployed across every stage of electrochemical cell and battery pack production, from the mixing and coating of electrode active materials through cell assembly, formation and aging, module and pack assembly, and final testing and inspection. This market serves the production of lithium-ion batteries in cylindrical, prismatic, and pouch cell formats across the LFP, NMC, and NCA chemistry platforms, as well as the emerging solid-state battery manufacturing segment, lead-acid battery production, and nickel-based battery manufacturing. End users of battery manufacturing equipment include large-scale lithium-ion cell producers operating gigafactories, module and pack assembly specialists, automotive OEMs establishing in-house battery production operations, and research and development laboratories developing next-generation battery technologies and manufacturing processes.

The growth of the global battery manufacturing equipment market is primarily driven by the extraordinary global expansion of battery cell production capacity necessitated by the rapid scaling of electric vehicle manufacturing and the accelerating deployment of grid-scale energy storage systems. Global EV sales exceeded 17 million units in 2024 and are projected to reach 40 to 50 million units annually by the mid-2030s, each vehicle requiring battery packs containing 50 to 100 kilograms of battery cells manufactured on equipment that must achieve micron-level precision across coating, assembly, and formation processes at production throughputs measured in millions of cells per day. The response to this demand—the global gigafactory buildout encompassing over 200 announced or under-construction large-format battery manufacturing facilities representing more than 5,000 GWh of planned production capacity—is generating an equipment procurement wave of extraordinary scale that is the fundamental structural driver of the battery manufacturing equipment market throughout the forecast period.

Two transformative opportunities are defining the market's long-term trajectory. The commercial development of solid-state battery technology requires an entirely new generation of manufacturing equipment adapted to the material properties, processing requirements, and cell architectures of solid-state cell formats, creating a new and high-value equipment market segment as solid-state battery production scales from pilot to commercial volumes over the forecast period. Simultaneously, the progressive automation and digitalization of battery manufacturing—driven by the need to achieve automotive-grade production quality at gigafactory throughput scales while reducing direct labor costs and minimizing material waste—is driving sustained capital investment in advanced robotics, machine vision inspection systems, AI-powered process control platforms, and digital twin simulation tools that are transforming battery manufacturing from a labor-intensive process into a highly automated precision manufacturing discipline.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 47.6 Billion |

|

Market Size in 2026 |

USD 22.3 Billion |

|

Market Size in 2025 |

USD 19.8 Billion |

|

Revenue Growth Rate (2026–2036) |

CAGR of 7.9% |

|

Dominating Manufacturing Stage |

Electrode Manufacturing Equipment |

|

Fastest Growing Manufacturing Stage |

Formation & Aging Equipment |

|

Dominating Battery Chemistry |

Lithium-ion Batteries |

|

Fastest Growing Battery Chemistry |

Solid-State Batteries |

|

Dominating Battery Format |

Prismatic Cells |

|

Fastest Growing Battery Format |

Cylindrical Cells |

|

Dominating Application |

Electric Vehicles (EVs) |

|

Fastest Growing Application |

Energy Storage Systems (ESS) |

|

Dominating Automation Level |

Semi-Automated Equipment |

|

Fastest Growing Automation Level |

Fully Automated Production Lines |

|

Dominating End User |

Battery Manufacturers (Cell Producers) |

|

Fastest Growing End User |

OEMs |

|

Dominating Geography |

Asia-Pacific |

|

Fastest Growing Geography |

Europe |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Automation and Digitalization of Battery Production

The progressive transformation of battery cell manufacturing from semi-automated processes requiring substantial direct labor input toward highly automated, digitally integrated production lines is the defining operational trend in the global battery manufacturing equipment market, driven by the imperative to achieve automotive-grade product consistency at gigafactory production scales while managing labor costs at the hundreds of billions of cells per year throughput volumes that the global EV and energy storage markets demand. The technical requirements of lithium-ion cell manufacturing—electrode coating thickness uniformity within plus or minus one micrometer across web widths exceeding one meter, cell assembly tolerance control at the ten-micrometer level, and formation protocol execution with millivolt-level precision across millions of simultaneously cycled cells—are fundamentally incompatible with manual process execution at gigafactory throughput and are driving the adoption of fully automated production lines from electrode mixing through end-of-line pack testing.

Battery manufacturing equipment suppliers are integrating advanced automation capabilities across their product portfolios, including multi-axis robotic cell handling systems that manage fragile electrode foils and assembled cells without contact damage, machine vision inspection systems deploying high-resolution cameras and AI image analysis algorithms to detect coating defects, electrode misalignment, and contamination events at production line speeds of several meters per second, and intelligent process control systems that adjust coating weight, calendering pressure, and formation current in real time based on in-process measurement feedback. Equipment leaders including Wuxi Lead Intelligent Equipment, Manz, and KUKA are developing integrated automation platforms that manage the full production line as a connected system rather than a series of discrete process steps, enabling the statistical process control and predictive maintenance capabilities that gigafactory operators require to maintain consistent cell quality across multi-billion-cell annual production volumes.

AI and Digital Twin Integration in Battery Manufacturing

The integration of artificial intelligence and digital twin simulation technology into battery manufacturing equipment and process control systems is advancing from experimental pilot programs toward mainstream commercial deployment, creating a new tier of intelligent manufacturing capability that enables battery producers to optimize process parameters, predict and prevent yield losses, and compress new product introduction timelines through virtual commissioning and process development that reduces dependence on physical trial production runs. Digital twin models of individual equipment units and complete production lines—built from equipment design data, process physics models, and real-time sensor data streams—enable battery manufacturers to simulate the impact of process parameter changes, raw material variability, and equipment maintenance events on cell quality and production yield before implementing changes on physical production lines, reducing the risk and time cost of process optimization and new product qualification.

AI-powered predictive maintenance applications are generating significant commercial value for battery manufacturers by analyzing the sensor data streams—current, voltage, temperature, vibration, and acoustic signatures—of coating machines, calendering rolls, formation cyclers, and assembly robots to identify early-stage equipment degradation signatures that predict impending failures hours or days before production-disrupting breakdowns would otherwise occur. The commercial case for predictive maintenance in battery manufacturing is compelling: electrode coating machine downtime at a gigafactory producing 20 GWh annually can generate production losses of USD 500,000 or more per unplanned production day, making the ROI of AI-powered maintenance prediction systems highly favorable relative to the sensor instrumentation and software investment required. Equipment manufacturers including Manz and Duerr are incorporating AI process analytics platforms as standard features of their next-generation equipment offerings, positioning digital intelligence as a core equipment value differentiator.

Development of Solid-State Battery Manufacturing Equipment

The accelerating commercial development of solid-state battery technology is creating a new and strategically important equipment market segment, as the material properties and process requirements of solid-state cell manufacturing differ fundamentally from liquid-electrolyte lithium-ion cell production in ways that necessitate new equipment designs, deposition processes, and assembly technologies. Solid-state batteries eliminate the liquid electrolyte of conventional lithium-ion cells by replacing it with a solid ionic conductor—either sulfide-based, oxide-based, or polymer-based—that requires deposition as a thin, uniform, defect-free layer onto the electrode structure using processes including physical vapor deposition, atomic layer deposition, tape casting, or hot pressing that have no direct equivalent in current lithium-ion production equipment. The simultaneous requirement for lithium metal anode integration in most solid-state cell architectures adds further process complexity, as lithium metal is highly reactive with moisture and oxygen and requires deposition and handling in rigorously controlled dry-room environments with dew points below minus 40 degrees Celsius.

Equipment manufacturers are investing in solid-state manufacturing process development programs in partnership with solid-state battery developers, with Toyota's commitment to solid-state vehicle production launch in the late 2020s, Samsung SDI's 2027 solid-state commercial production target, and QuantumScape and Solid Power's pilot production scaling programs collectively establishing a commercial equipment demand timeline that is driving process equipment development investment. The solid-state battery manufacturing equipment market is expected to remain in a pre-commercial development phase through the late 2020s before transitioning to rapid commercial volume growth in the early 2030s as multiple solid-state battery manufacturers scale production, creating a high-value equipment opportunity for suppliers that establish solid-state process expertise and customer relationships during the current technology development window.

Rapid Expansion of EV Battery Production

The rapid global expansion of electric vehicle adoption is generating battery cell production demand at an extraordinary scale that is the primary structural driver of the battery manufacturing equipment market, as every additional gigawatt-hour of annual battery cell production capacity requires capital investment in electrode manufacturing, cell assembly, formation, and testing equipment that collectively represents several hundred million dollars per GWh of new capacity at current automation levels. Global announced battery production capacity exceeds 5,000 GWh across all planned and under-construction gigafactory projects as of 2025, representing multi-hundred-billion-dollar aggregate equipment procurement requirements that will be executed progressively through the forecast period as gigafactory construction and commissioning timelines are realized. CATL's planned capacity expansion to over 1,000 GWh annually, BYD's vertical integration of cell production for its own EV manufacturing at a scale exceeding 400 GWh, LG Energy Solution's global manufacturing network spanning Asia, North America, and Europe, and the concurrent equipment procurement programs of dozens of additional battery manufacturers collectively constitute the largest sustained capital equipment purchasing program in the history of the global manufacturing equipment industry.

Growth of Gigafactories Globally

The emergence of the gigafactory as the defining production architecture of the battery manufacturing industry—characterized by single-site manufacturing complexes producing 10 GWh or more of battery cells annually in highly automated, vertically integrated production facilities—is creating a structural shift in the scale, specification, and procurement dynamics of the battery manufacturing equipment market that is generating sustained revenue expansion for equipment suppliers capable of serving multi-GWh production line requirements. Gigafactory-scale production is fundamentally different from the smaller-scale battery manufacturing operations that characterized the industry before the EV era, requiring equipment designed for continuous high-throughput operation at precision tolerances across production lines hundreds of meters in length, integrated process control and quality management systems capable of managing the statistical complexity of producing billions of cells per year, and equipment supply chain management at a global scale as battery manufacturers source electrode coating machines, winding systems, formation equipment, and testing lines from multiple specialized suppliers across Asia, Europe, and North America.

Development of Solid-State Battery Manufacturing Equipment

The commercial development of solid-state battery manufacturing processes represents the highest-value near-to-medium-term equipment opportunity in the battery manufacturing equipment market, as solid-state cell production requires entirely new equipment platforms for solid electrolyte deposition, lithium metal anode handling, and high-pressure cell assembly that cannot be adapted from existing lithium-ion equipment designs and therefore represent greenfield equipment development and commercialization opportunities for both established battery equipment manufacturers and specialist thin-film deposition and precision material processing equipment companies. The addressable solid-state battery equipment market is expected to grow from a pre-commercial base of pilot production tooling in the late 2020s to a commercially significant revenue segment in the early-to-mid 2030s as solid-state battery manufacturers including Toyota, Samsung SDI, QuantumScape, and Solid Power scale their production programs. Equipment suppliers that invest in solid-state manufacturing process development during the current pre-commercial phase—through R&D partnerships with solid-state battery developers, pilot line equipment installations, and process intellectual property development—will be positioned to capture the first-mover advantages of established customer relationships and process expertise when the solid-state battery equipment market transitions to commercial volume procurement.

Automation and Digitalization of Battery Production

The sustained capital investment in automation upgrades and digital manufacturing platform integration by battery manufacturers seeking to improve production yield, reduce direct labor costs, and achieve automotive-grade quality management at gigafactory scale represents a large and continuously expanding opportunity for battery equipment manufacturers that offer intelligent automation solutions beyond their core process equipment capabilities. The economics of battery manufacturing automation are compelling: electrode coating yield improvements of one to two percentage points at a 20 GWh facility can generate annual material cost savings of USD 20 to 50 million, making the ROI calculation for advanced process control and inspection equipment highly favorable relative to capital cost. The transition from semi-automated to fully automated production lines across the battery manufacturing industry—which is accelerating as labor costs in China's battery manufacturing heartland increase and as automotive OEM quality requirements mandate defect detection capabilities beyond human visual inspection—is driving sustained demand for advanced robotic handling systems, AI-powered inspection platforms, and integrated manufacturing execution systems from equipment suppliers including Wuxi Lead, KUKA, and Manz.

By Manufacturing Stage: In 2026, Electrode Manufacturing Equipment to Dominate

Based on manufacturing stage, the global battery manufacturing equipment market is segmented into electrode manufacturing equipment, cell assembly equipment, formation and aging equipment, module and pack assembly equipment, testing and inspection equipment, and other equipment. In 2026, the electrode manufacturing equipment segment is expected to account for the largest share of the global battery manufacturing equipment market. The dominant position of electrode manufacturing equipment reflects the critical technical importance and high capital cost of electrode coating and drying processes in lithium-ion cell manufacturing, where the slot-die coating of cathode and anode slurries onto copper and aluminum current collector foils at uniform thickness tolerances of plus or minus one micrometer across web widths of one meter or more represents the single most precision-demanding and capital-intensive process step in lithium-ion cell production. High-throughput electrode coating lines from leading suppliers including Hirano Tecseed, Buhler, and Wuxi Lead are among the highest unit-value individual equipment categories in the battery manufacturing equipment market, and the multiple coating lines required to support gigafactory electrode production volumes generate substantial aggregate equipment revenue. The ancillary electrode manufacturing equipment categories of calendering, which compresses coated electrodes to optimize active material density, and slitting, which cuts broad electrode web rolls into narrow strips matched to cell format dimensions, add further capital equipment procurement requirements to the electrode manufacturing stage.

However, the formation and aging equipment segment is poised to register the highest CAGR during the forecast period. Formation systems—which execute the precisely controlled electrochemical charge and discharge cycles that activate newly assembled battery cells by forming the solid electrolyte interphase layer on the anode surface—represent an exceptionally capital-intensive equipment category because every cell produced must individually undergo multi-hour formation protocols, requiring formation chamber capacity scaled to the millions of cells in simultaneous formation at any time across a gigafactory's production output. The growth of gigafactory production capacity is generating proportional growth in formation equipment procurement requirements, and the technical advancement of formation protocols toward higher-speed formation processes that reduce the time and equipment capital required per cell is a major R&D focus for both battery manufacturers and formation equipment suppliers that is attracting significant investment.

By Battery Chemistry: In 2026, Lithium-ion Batteries to Hold the Largest Share

Based on battery chemistry, the global battery manufacturing equipment market is segmented into lithium-ion batteries (LFP, NMC, NCA), solid-state batteries, lead-acid batteries, nickel-based batteries, and other chemistries. In 2026, the lithium-ion batteries segment is expected to account for the largest share of the global battery manufacturing equipment market. Lithium-ion battery manufacturing represents the overwhelming majority of current global battery production capacity investment, with LFP chemistry gaining significant share in EV and energy storage applications due to its compelling combination of low cost, excellent cycle life, and thermal stability, while NMC and NCA chemistries maintain strong positions in premium EV applications where high energy density and driving range justify their cost premium over LFP. The equipment requirements across LFP, NMC, and NCA lithium-ion cell production are broadly similar at the electrode coating, cell assembly, and testing stages, with chemistry-specific differences in slurry formulation, calendering pressure requirements, and formation protocol parameters that require equipment parameter adjustments rather than fundamentally different equipment platforms.

However, the solid-state batteries segment is projected to register the highest CAGR during the forecast period. The high growth rate of this segment—from a very low base of pilot production equipment in 2026—reflects the advancing commercial development timelines of solid-state battery programs at Toyota, Samsung SDI, QuantumScape, Solid Power, and multiple Chinese solid-state battery developers, each of which requires specialized solid electrolyte deposition, lithium metal anode processing, and high-pressure cell assembly equipment that represents entirely new equipment procurement categories with no equivalent in current lithium-ion production.

By Battery Format: In 2026, Prismatic Cells to Hold the Largest Share

Based on battery format, the global battery manufacturing equipment market is segmented into cylindrical cells, prismatic cells, and pouch cells. In 2026, the prismatic cells segment is expected to account for the largest share of the global battery manufacturing equipment market. Prismatic cell format adoption has accelerated significantly driven by CATL's large-format prismatic LFP cell platform, including the CTP (cell-to-pack) and Qilin battery architectures, that has achieved broad OEM adoption across the global EV market, BYD's blade battery prismatic format that has established a strong market position in both its own EV lineup and third-party OEM supply programs, and the broad preference for prismatic format in energy storage system applications where the rigid cell housing facilitates modular pack assembly and thermal management. Prismatic cell manufacturing requires stacking equipment for electrode assembly inside the rigid housing, laser welding systems for top-cap sealing, and precisely controlled electrolyte filling systems, each representing significant per-line capital equipment requirements.

However, the cylindrical cells segment is projected to register the highest CAGR during the forecast period. Tesla's strategic commitment to the large-format 4680 cylindrical cell validated the cylindrical format's long-term competitive position in the EV market and stimulated substantial manufacturing equipment investment. The 4680 cell format requires new-generation winding equipment capable of handling the wider electrode widths and higher mechanical stresses of the larger format cell, and multiple battery manufacturers beyond Tesla including Panasonic, Samsung SDI, and Chinese producers are establishing 4680 production programs that are generating cylindrical equipment procurement growth.

By Application: In 2026, Electric Vehicles to Hold the Largest Share

Based on application, the global battery manufacturing equipment market is segmented into electric vehicles, energy storage systems, consumer electronics, industrial applications, and aerospace and defense. In 2026, the electric vehicles segment is expected to account for the largest share of the global battery manufacturing equipment market. EV battery production constitutes the dominant end-use application driving global gigafactory capacity expansion and associated battery manufacturing equipment procurement, as passenger EV battery packs requiring 50 to 100 kWh of cell capacity represent the single largest and fastest-growing demand category for lithium-ion cells globally. The global EV market's continued strong growth trajectory, supported by government combustion engine phase-out mandates in the EU and U.K., the U.S. IRA's EV tax credit structure, and the improving price competitiveness of EVs relative to internal combustion vehicles, is translating directly into sustained gigafactory construction and equipment procurement programs by battery manufacturers and automotive OEMs establishing battery production capacity to serve their EV manufacturing operations.

However, the energy storage systems segment is projected to register the highest CAGR during the forecast period. Grid-scale battery energy storage deployment is accelerating globally as renewable energy penetration increases and grid operators require battery storage to provide frequency regulation, peak capacity, and renewable firming services. The IEA projects that installed global battery storage capacity needs to grow from approximately 85 GWh in 2024 to over 1,500 GWh by 2030 to support net-zero energy transition pathways, implying battery cell production volume growth for energy storage applications that will generate substantial incremental manufacturing equipment demand across the forecast period.

By Automation Level: In 2026, Semi-Automated Equipment to Hold the Largest Share

Based on automation level, the global battery manufacturing equipment market is segmented into manual equipment, semi-automated equipment, and fully automated production lines. In 2026, the semi-automated equipment segment is expected to account for the largest share of the global battery manufacturing equipment market. The large installed base of semi-automated production lines across established battery manufacturing facilities in China, South Korea, and Japan constitutes the majority of current global battery production capacity by line count and represents the equipment configuration of choice for the large number of mid-scale battery manufacturers producing below 5 GWh annually where the capital cost of full automation is not yet justified by production volume. Semi-automated lines provide a practical balance of production consistency, flexibility for product mix changes, and capital investment efficiency for battery manufacturers scaling from pilot to initial commercial production volumes.

However, the fully automated production lines segment is projected to register the highest CAGR during the forecast period. The economic imperative of gigafactory-scale production—where direct labor cost reduction, consistent quality across billions of cells, and throughput maximization at 24-hour production schedules drive the business case for full automation—is accelerating the adoption of end-to-end automated production lines that eliminate manual material handling and inspection operations throughout the electrode manufacturing, cell assembly, formation, and pack assembly process. Leading battery manufacturers including CATL, LG Energy Solution, and Panasonic are specifying fully automated production lines as the standard configuration for new gigafactory phases, and automotive OEMs establishing in-house battery manufacturing operations are investing in full automation from the outset to achieve the quality and cost targets required for competitive EV battery production.

By End User: In 2026, Battery Manufacturers (Cell Producers) to Hold the Largest Share

Based on end user, the global battery manufacturing equipment market is segmented into battery manufacturers (cell producers), module and pack manufacturers, OEMs, and R&D laboratories. In 2026, the battery manufacturers (cell producers) segment is expected to account for the largest share of the global battery manufacturing equipment market. Cell-level battery manufacturers—including the world's largest producers CATL, BYD, LG Energy Solution, Panasonic, Samsung SDI, SK On, CALB, and EVE Energy—represent the primary direct buyers of battery manufacturing equipment across the full production process spectrum from electrode manufacturing through cell assembly, formation, and testing, as cell production encompasses the most capital-intensive and technically demanding process stages of the battery manufacturing value chain. These manufacturers' ongoing gigafactory expansion programs generate the majority of global battery manufacturing equipment procurement by both value and volume, with CATL alone estimated to procure several billion dollars of manufacturing equipment annually across its global expansion program.

However, the OEMs segment is projected to register the highest CAGR during the forecast period. Automotive OEMs including Volkswagen Group (through PowerCo), General Motors (through Ultium Cells), Stellantis, and Toyota are establishing in-house battery cell manufacturing capabilities for the first time, driven by strategic imperatives to control battery supply chain costs, secure battery supply for their EV production programs, and develop proprietary battery technology differentiation. These OEM-owned or joint venture cell manufacturing operations represent entirely new equipment procurement programs for companies with no prior battery manufacturing equipment purchasing experience, and their ambitious production scale targets—PowerCo targets 240 GWh of annual production capacity by 2030—imply large and rapidly growing equipment investment programs.

Battery Manufacturing Equipment Market by Region: Asia-Pacific Leading by Share, Europe by Growth

Based on geography, the global battery manufacturing equipment market is segmented into Asia-Pacific, Europe, North America, Latin America, and the Middle East and Africa.

In 2026, Asia-Pacific is expected to account for the largest share of the global battery manufacturing equipment market. The overwhelming dominance of Asia-Pacific in the global battery manufacturing equipment market reflects China's position as both the world's largest battery cell production center and the home of the world's largest concentration of battery manufacturing equipment manufacturers. China's battery manufacturing equipment industry, anchored by Wuxi Lead Intelligent Equipment, Shenzhen Yinghe Technology, Shenzhen Geesun, and dozens of additional specialized equipment producers, supplies the majority of equipment deployed in Chinese gigafactories and is increasingly competing for international gigafactory equipment contracts in Europe and North America. South Korea's battery equipment industry, supplying precision equipment to LG Energy Solution, Samsung SDI, and SK On's global manufacturing networks, contributes significant advanced equipment technology to the regional market. Japan's battery equipment manufacturing heritage provides precision manufacturing equipment for the Japanese battery industry and selective international customers.

However, the European battery manufacturing equipment market is expected to grow at the fastest CAGR during the forecast period. Europe's rapid growth is driven directly by the unprecedented gigafactory investment wave that is constructing the European battery manufacturing base to serve the continent's large and rapidly growing EV demand. The pipeline of announced and under-construction European gigafactories encompasses Northvolt's established Vasteras facility and planned expansions in Germany and other EU locations, ACC's facilities in France (Billy-Berclau) and Germany (Kaiserslautern), AESC's Sunderland Gigaplant, and the European manufacturing operations of CATL, Samsung SDI, SK On, and Envision AESC that collectively represent the largest sustained battery manufacturing investment program in European industrial history. Each gigafactory requires hundreds of millions of euros of manufacturing equipment procurement, and the European equipment market is attracting both Asian equipment suppliers establishing European sales and service operations and European industrial equipment companies that are investing in battery manufacturing equipment product lines to serve the growing domestic customer base.

North America is establishing a rapidly expanding battery manufacturing equipment market, driven by the U.S. Inflation Reduction Act's domestic manufacturing requirements that are stimulating unprecedented gigafactory investment across the United States, Canada, and Mexico. The U.S. battery manufacturing capacity pipeline encompasses the Ultium Cells joint venture plants of General Motors and LG Energy Solution, Toyota's battery plant in North Carolina, Panasonic's facilities in Kansas and Nevada, and the battery manufacturing programs of multiple additional cell producers establishing North American production to qualify for IRA domestic content incentives. Canada's battery manufacturing investment includes Volkswagen's PowerCo gigafactory in St. Thomas, Ontario—one of the largest planned battery manufacturing investments in North American history—and Stellantis and LG Energy Solution's NextStar Energy plant in Windsor, Ontario, establishing Canada as a significant and rapidly growing battery equipment procurement market.

The global battery manufacturing equipment market is highly fragmented at the individual equipment category level, with specialized suppliers holding leading positions in specific process stages—electrode coating, cell winding or stacking, formation systems, or vision inspection—while few suppliers offer comprehensive end-to-end production line solutions across the full battery manufacturing process. Chinese equipment manufacturers have achieved significant market share gains over the past decade, with Wuxi Lead Intelligent Equipment and Shenzhen Yinghe Technology emerging as leading suppliers of integrated electrode manufacturing and cell assembly equipment to Chinese and international battery producers. Competition is focused on equipment throughput performance, process precision and yield, automation integration capability, service and spare parts support across global manufacturing locations, and the ability to co-develop equipment platforms aligned with customers' proprietary cell designs and manufacturing process specifications.

The report provides a comprehensive competitive analysis based on an extensive assessment of leading players' equipment portfolios, production technology capabilities, customer bases, geographic market presence, and key strategic developments. Some of the key players operating in the global battery manufacturing equipment market include Wuxi Lead Intelligent Equipment Co., Ltd. (China), Manz AG (Germany), Buhler Group (Switzerland), Hitachi High-Tech Corporation (Japan), PNT Co., Ltd. (South Korea), Shenzhen Yinghe Technology Co., Ltd. (China), CIS Co., Ltd. (South Korea), CKD Corporation (Japan), Hirano Tecseed Co., Ltd. (Japan), Sovema Group (Italy), Komax Holding AG (Switzerland), KUKA AG (Germany), Duerr AG (Germany), Nordson Corporation (U.S.), and Hanwha Corporation (South Korea), among others.

The global battery manufacturing equipment market is expected to reach USD 47.6 billion by 2036 from an estimated USD 22.3 billion in 2026, at a CAGR of 7.9% during the forecast period 2026–2036.

In 2026, the electrode manufacturing equipment segment is expected to hold the largest share of the global battery manufacturing equipment market, driven by the high unit value and critical technical importance of precision electrode coating and calendering equipment that constitutes the most capital-intensive process stage in lithium-ion cell production.

The formation and aging equipment segment is expected to register the highest CAGR during the forecast period 2026–2036, driven by the proportional scaling of formation system capacity requirements with growing gigafactory cell production volumes and the high aggregate capital investment in formation equipment necessitated by the multi-hour formation protocol durations that require large per-cell equipment capacity.

In 2026, the lithium-ion batteries segment is expected to hold the largest share of the global battery manufacturing equipment market, reflecting lithium-ion technology's established commercial dominance across EV, energy storage, and consumer electronics battery production and the very large installed and planned production capacity base generating equipment procurement demand.

In 2026, the prismatic cells segment is expected to hold the largest share of the global battery manufacturing equipment market, driven by the broad adoption of large-format prismatic LFP cell platforms by CATL and BYD that have achieved dominant market positions in both EV and energy storage applications globally.

The growth of this market is primarily driven by the extraordinary global expansion of EV battery production capacity necessitating unprecedented gigafactory investment and equipment procurement, the sustained growth of grid-scale energy storage deployment creating additional large-scale battery production demand, government policies including the U.S. IRA and EU Battery Regulation mandating battery supply chain localization that are accelerating gigafactory construction in North America and Europe, and the progressive automation and digitalization of battery manufacturing that is driving sustained investment in advanced robotic production lines and AI-powered process control systems.

Key players are Wuxi Lead Intelligent Equipment Co., Ltd. (China), Manz AG (Germany), Buhler Group (Switzerland), Hitachi High-Tech Corporation (Japan), PNT Co., Ltd. (South Korea), Shenzhen Yinghe Technology Co., Ltd. (China), CIS Co., Ltd. (South Korea), CKD Corporation (Japan), Hirano Tecseed Co., Ltd. (Japan), Sovema Group (Italy), Komax Holding AG (Switzerland), KUKA AG (Germany), Duerr AG (Germany), Nordson Corporation (U.S.), and Hanwha Corporation (South Korea), among others.

Europe is expected to register the highest growth rate in the global battery manufacturing equipment market during the forecast period 2026–2036, driven by the unprecedented gigafactory investment wave encompassing Northvolt, ACC, AESC, and the European manufacturing programs of CATL, Samsung SDI, SK On, and Volkswagen's PowerCo that collectively represent over 400 GWh of planned production capacity requiring comprehensive manufacturing equipment procurement.

1. Introduction

1.1 Market Definition

1.2 Market Ecosystem

1.3 Currency and Limitations

1.3.1 Currency

1.3.2 Limitations

1.4 Key Stakeholders

2. Research Methodology

2.1 Research Approach

2.2 Data Collection & Validation Process

2.2.1 Secondary Research

2.2.2 Primary Research & Validation

2.2.2.1 Primary Interviews with Experts

2.2.2.2 Approaches for Country-/Region-Level Analysis

2.3 Market Estimation

2.3.1 Bottom-Up Approach

2.3.2 Top-Down Approach

2.3.3 Growth Forecast

2.4 Data Triangulation

2.5 Assumptions for the Study

3. Executive Summary

4. Market Overview

4.1 Introduction

4.2 Market Dynamics

4.2.1 Drivers

4.2.1.1 Rapid Expansion of EV Battery Production

4.2.1.2 Growth of Gigafactories Globally

4.2.1.3 Increasing Demand for High-Energy-Density Batteries

4.2.1.4 Government Support for Localized Battery Manufacturing

4.2.2 Restraints

4.2.2.1 High Capital Investment for Equipment

4.2.2.2 Supply Chain Constraints for Key Components

4.2.2.3 Technology Standardization Challenges

4.2.3 Opportunities

4.2.3.1 Development of Solid-State Battery Manufacturing Equipment

4.2.3.2 Automation and Digitalization of Battery Production

4.2.3.3 Expansion in Emerging Markets

4.2.3.4 Recycling and Second-Life Battery Equipment

4.2.4 Challenges

4.2.4.1 Yield Optimization and Quality Control

4.2.4.2 Rapid Technology Evolution

4.3 Technology Landscape

4.3.1 Lithium-ion Battery Manufacturing Technologies

4.3.2 Solid-State Battery Manufacturing

4.3.3 Automation and Robotics in Battery Production

4.3.4 AI and Digital Twin Integration

4.4 Battery Manufacturing Process Flow (Critical Segmentation)

4.4.1 Electrode Preparation

4.4.2 Cell Assembly

4.4.3 Formation & Aging

4.4.4 Module & Pack Assembly

4.4.5 Testing & Quality Control

4.5 Value Chain Analysis

4.5.1 Raw Material Suppliers

4.5.2 Equipment Manufacturers

4.5.3 Battery Manufacturers (Cell/Module/Pack)

4.5.4 Integrators and Automation Providers

4.5.5 End Users

4.6 Regulatory and Standards Landscape

4.6.1 Battery Safety Standards (IEC, UL)

4.6.2 EV and Energy Storage Regulations

4.6.3 Environmental and Recycling Regulations

4.7 Porter's Five Forces Analysis

5. Battery Manufacturing Equipment Market, by Manufacturing Stage (Primary Segmentation)

5.1 Introduction

5.2 Electrode Manufacturing Equipment

5.2.1 Mixing Equipment

5.2.2 Coating Equipment

5.2.3 Drying Equipment

5.2.4 Calendering Equipment

5.2.5 Slitting Equipment

5.3 Cell Assembly Equipment

5.3.1 Stacking Equipment

5.3.2 Winding Equipment

5.3.3 Electrolyte Filling Equipment

5.3.4 Sealing Equipment

5.4 Formation & Aging Equipment

5.4.1 Formation Systems

5.4.2 Aging Systems

5.4.3 Grading & Sorting Equipment

5.5 Module & Pack Assembly Equipment

5.5.1 Welding Equipment

5.5.2 Assembly Lines

5.5.3 Battery Management System (BMS) Integration Equipment

5.6 Testing & Inspection Equipment

5.6.1 Electrical Testing

5.6.2 Safety Testing

5.6.3 Vision Inspection Systems

5.6.4 End-of-Line Testing

5.7 Other Equipment

6. Battery Manufacturing Equipment Market, by Battery Chemistry

6.1 Introduction

6.2 Lithium-ion Batteries

6.2.1 LFP

6.2.2 NMC

6.2.3 NCA

6.3 Solid-State Batteries

6.4 Lead-Acid Batteries

6.5 Nickel-Based Batteries

6.6 Other Chemistries

7. Battery Manufacturing Equipment Market, by Battery Format

7.1 Introduction

7.2 Cylindrical Cells

7.3 Prismatic Cells

7.4 Pouch Cells

8. Battery Manufacturing Equipment Market, by Application

8.1 Introduction

8.2 Electric Vehicles (EVs)

8.3 Energy Storage Systems (ESS)

8.4 Consumer Electronics

8.5 Industrial Applications

8.6 Aerospace & Defense

9. Battery Manufacturing Equipment Market, by Automation Level

9.1 Introduction

9.2 Manual Equipment

9.3 Semi-Automated Equipment

9.4 Fully Automated Production Lines

10. Battery Manufacturing Equipment Market, by End User

10.1 Introduction

10.2 Battery Manufacturers (Cell Producers)

10.3 Module & Pack Manufacturers

10.4 OEMs

10.5 R&D Laboratories

11. Battery Manufacturing Equipment Market, by Geography

11.1 Introduction

11.2 Asia-Pacific

11.2.1 China

11.2.2 South Korea

11.2.3 Japan

11.2.4 India

11.2.5 Taiwan

11.2.6 Singapore

11.2.7 Malaysia

11.2.8 Thailand

11.2.9 Vietnam

11.2.10 Indonesia

11.2.11 Rest of Asia-Pacific

11.3 Europe

11.3.1 Germany

11.3.2 France

11.3.3 U.K.

11.3.4 Sweden

11.3.5 Norway

11.3.6 Italy

11.3.7 Spain

11.3.8 Netherlands

11.3.9 Poland

11.3.10 Rest of Europe

11.4 North America

11.4.1 U.S.

11.4.2 Canada

11.5 Latin America

11.5.1 Brazil

11.5.2 Mexico

11.5.3 Argentina

11.5.4 Chile

11.5.5 Colombia

11.5.6 Rest of Latin America

11.6 Middle East & Africa

11.6.1 UAE

11.6.2 Saudi Arabia

11.6.3 South Africa

11.6.4 Turkey

11.6.5 Israel

11.6.6 Rest of Middle East & Africa

12. Competitive Landscape

12.1 Overview

12.2 Key Growth Strategies

12.3 Competitive Benchmarking

12.4 Competitive Dashboard

12.4.1 Industry Leaders

12.4.2 Market Differentiators

12.4.3 Vanguards

12.4.4 Emerging Companies

12.5 Market Ranking/Positioning Analysis of Key Players, 2025

13. Company Profiles

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

13.1 Wuxi Lead Intelligent Equipment Co., Ltd.

13.2 Manz AG

13.3 Buhler Group

13.4 Hitachi High-Tech Corporation

13.5 PNT (PNT Co., Ltd.)

13.6 Shenzhen Yinghe Technology Co., Ltd.

13.7 CIS Co., Ltd.

13.8 CKD Corporation

13.9 Hirano Tecseed Co., Ltd.

13.10 Sovema Group

13.11 Komax Holding AG

13.12 KUKA AG

13.13 Durr AG

13.14 Nordson Corporation

13.15 Hanwha Corporation

14. Appendix

14.1 Additional Customization

14.2 Related Reports

Published Date: Apr-2026

Subscribe to get the latest industry updates