Resources

About Us

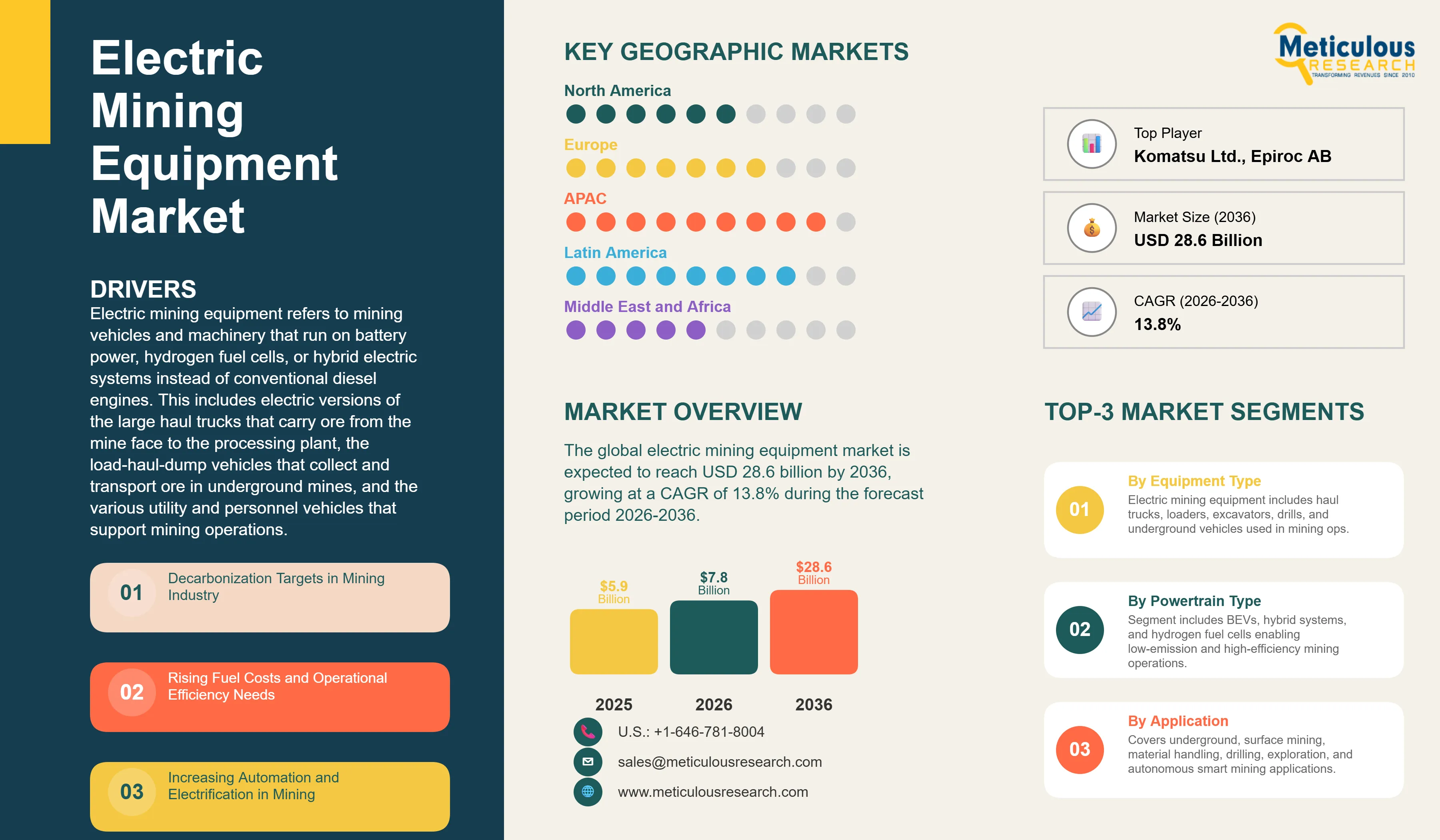

Electric Mining Equipment Market Size, Share & Trends Analysis by Equipment Type (Electric Haul Trucks, Loaders/LHD, Excavators), Application (Underground Mining, Surface Mining), End User, and Battery Type - Global Opportunity Analysis & Industry Forecast (2026-2036)

Report ID: MRAUTO - 1041925 Pages: 290 Apr-2026 Formats*: PDF Category: Automotive and Transportation Delivery: 24 to 72 Hours Download Free Sample ReportThe global electric mining equipment market was valued at USD 5.9 billion in 2025. This market is expected to reach USD 28.6 billion by 2036 from an estimated USD 7.8 billion in 2026, growing at a CAGR of 13.8% during the forecast period 2026-2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Electric mining equipment refers to mining vehicles and machinery that run on battery power, hydrogen fuel cells, or hybrid electric systems instead of conventional diesel engines. This includes electric versions of the large haul trucks that carry ore from the mine face to the processing plant, the load-haul-dump vehicles that collect and transport ore in underground mines, excavators, drilling rigs, and the various utility and personnel vehicles that support mining operations. Replacing diesel equipment with electric equivalents in a mine eliminates diesel exhaust and significantly reduces heat generation, which is particularly valuable in underground mines where ventilation is expensive, difficult to maintain, and limited in what it can safely remove. Diesel exhaust in an underground mine requires enormous ventilation systems that consume large amounts of energy and represent a significant share of the mine's total operating cost, so switching to electric equipment reduces ventilation requirements directly and saves money on energy that would otherwise go to pushing clean air through kilometers of underground tunnels.

The market is growing strongly because several powerful forces are pushing the mining industry toward electrification at the same time. Mining companies have made public net-zero emission commitments that require them to reduce or eliminate diesel combustion across their operations. Diesel fuel is one of the largest operating cost items for most mines, and rising fuel prices are making electric equipment increasingly attractive on purely financial grounds as battery costs fall. Regulators in major mining jurisdictions including Canada, Australia, and the European Union are tightening underground air quality standards, creating compliance requirements that are more cost-effectively met through electrification than through increasingly expensive diesel emission control technology. And the pioneering mines that have already deployed battery electric underground equipment from Epiroc, Sandvik, and other manufacturers are reporting real operational cost savings that are proving the business case to the broader industry.

Two significant opportunities are shaping the next phase of market development. The combination of electric mining equipment with on-site renewable energy microgrids is emerging as a very compelling package for remote mines that currently pay very high prices for diesel fuel that must be transported long distances. A mine that installs solar panels and battery storage to generate its own electricity and uses that electricity to power its mining fleet can dramatically reduce its total operating cost while eliminating the carbon emissions and logistical complexity of diesel supply. This renewable plus electric mining model is attracting strong interest from mining operators in sun-rich and remote locations including Australia, Chile, and parts of Africa. In addition, the combination of electric drivetrains with autonomous vehicle technology is creating a new generation of fully autonomous electric mining fleets that can operate continuously without shift changes, human fatigue constraints, or the ventilation requirements of crewed diesel equipment, potentially transforming the productivity economics of mining operations.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 28.6 Billion |

|

Market Size in 2026 |

USD 7.8 Billion |

|

Market Size in 2025 |

USD 5.9 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 13.8% |

|

Dominating Equipment Type |

Electric Haul Trucks |

|

Fastest Growing Equipment Type |

Electric Drilling Equipment |

|

Dominating Powertrain Type |

Battery Electric Vehicles (BEVs) |

|

Fastest Growing Powertrain Type |

Hydrogen Fuel Cell Vehicles |

|

Dominating Application |

Underground Mining |

|

Fastest Growing Application |

Surface Mining |

|

Dominating End User |

Metal Mining Companies |

|

Fastest Growing End User |

Contractors and Mining Service Providers |

|

Dominating Battery Type |

Lithium-Ion Batteries |

|

Fastest Growing Battery Type |

Solid-State Batteries |

|

Dominating Autonomy Level |

Semi-Autonomous Systems |

|

Fastest Growing Autonomy Level |

Fully Autonomous Systems |

|

Dominating Geography |

Asia-Pacific |

|

Fastest Growing Geography |

Latin America |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Underground Mining Leading the Electric Transition Because the Benefits Are Clearest

While electric mining equipment is being developed for both underground and surface applications, the adoption of battery electric equipment has advanced much further in underground mining because the operational benefits of eliminating diesel equipment underground are immediate, substantial, and measurable in ways that directly affect the mine's bottom line. An underground mine ventilation system needs to move enough fresh air to dilute diesel exhaust to safe levels for the miners working in the tunnels, and the energy required to run the ventilation fans is typically 40 to 50% of the total energy consumption at a deep underground mine. Replacing diesel vehicles with electric ones eliminates the exhaust that the ventilation system is designed to handle, which means ventilation requirements can be reduced significantly, cutting energy costs on a recurring basis. When Goldcorp and then Newmont implemented battery electric fleets at their Borden mine in Ontario, Canada, the elimination of diesel exhaust allowed them to substantially reduce ventilation requirements and cut energy costs in ways that helped justify the higher upfront cost of the electric equipment.

The underground advantage is also driving rapid product development from the major equipment manufacturers. Epiroc and Sandvik, both Swedish companies with deep roots in underground mining equipment, were among the first to bring commercially viable battery electric underground loaders and drill rigs to market and have established strong positions in the underground electric equipment segment. Their Scooptram ST7 Battery electric loader and Sandvik's LH514E loader are deployed in operating mines and generating real performance data that is validating the technology for broader adoption. The improving energy density of lithium-ion batteries, which allows longer operating times between charges, and the development of fast charging and battery swapping systems that minimize equipment downtime during recharging, are progressively removing the operational limitations that previously made battery electric underground equipment less practical than diesel alternatives.

Major Mining Companies Making Fleet Electrification Commitments

A growing number of the world's largest mining companies have made formal public commitments to electrifying their mining fleets as part of their broader climate and sustainability strategies, and these commitments are translating into large equipment procurement programs that are driving the commercial scale-up of the electric mining equipment market. BHP has committed to eliminating diesel from its mining operations and has run battery electric truck trials at its Olympic Dam mine in Australia. Anglo American is deploying its nuGen zero-emission haul truck prototype, which uses a hydrogen fuel cell and battery hybrid powertrain, at its Mogalakwena platinum mine in South Africa. Newmont has committed to net-zero scope 1 and scope 2 emissions from its operations by 2050 with a near-term target of 30% reduction by 2030, requiring significant fleet electrification. Glencore, Rio Tinto, and Vale have all made similar public commitments with specific fleet electrification targets.

These commitments are commercially significant because they create defined and time-bounded procurement demand that equipment manufacturers can plan production capacity around. When a major mining company announces that it will electrify a specific percentage of its fleet by a specific year, that commitment represents a known quantity of future equipment orders that gives Caterpillar, Komatsu, Epiroc, and Sandvik confidence to invest in scaling up their electric equipment manufacturing capacity and supply chains. The combination of regulatory pressure, fuel cost economics, and public sustainability commitments is creating a durable and growing demand signal that is transforming electric mining equipment from a niche innovation into a mainstream procurement category for the global mining industry.

Autonomous Electric Equipment Creating the Next Generation of Mining Productivity

The combination of electric drivetrains with autonomous vehicle technology is emerging as the most transformative development in mining equipment design, creating a new generation of vehicles that can operate continuously around the clock without the constraints of human operators. Conventional diesel mining equipment in underground mines requires continuous ventilation, creates significant heat, and can only be operated safely when the mine environment meets air quality standards. Electric autonomous equipment eliminates all of these constraints: no diesel exhaust means ventilation requirements are much lower, the reduced heat output from electric motors means the underground temperature is easier to manage, and fully autonomous vehicles can work through shift changes and breaks without stopping.

Komatsu's AHS autonomous haulage system for surface mines and Epiroc's Scooptram ST1030 autonomous loader represent the current frontier of autonomous electric mining equipment, but both major and smaller specialized manufacturers are investing heavily in this category. The financial case for autonomous electric equipment is compelling because the reduction in operating labor costs at a mine where most of the fleet runs autonomously can be hundreds of millions of dollars per year at a large mine, which makes the premium cost of autonomous electric equipment easy to justify. Sandvik's Artisan Vehicles division, which was acquired specifically for its battery electric mining vehicle technology, is developing the next generation of battery electric underground equipment specifically designed for integration with autonomous operation systems, positioning this segment as one of the highest-growth areas in the broader electric mining equipment market.

Decarbonization Targets in Mining Industry

The primary driver of the electric mining equipment market is the mining industry's growing pressure to reduce its greenhouse gas emissions in response to the climate commitments of individual mining companies, the requirements of investors and lenders who are applying increasingly strict ESG criteria to mining sector financing, and the regulatory requirements of governments in major mining jurisdictions. Mining is an emissions-intensive industry because it uses enormous quantities of diesel fuel to power its heavy equipment fleets, with diesel combustion accounting for 30 to 50% of scope 1 emissions at most surface and underground mines. For mining companies that have committed to net-zero operations by 2050 or to 30 to 50% emission reductions by 2030, fleet electrification is not an optional sustainability improvement but a mathematically necessary component of their climate strategy because no other available technology can reduce diesel combustion emissions at the scale that electrification can deliver. BHP, Newmont, Anglo American, Glencore, and Rio Tinto have all made public emission reduction commitments that require significant fleet electrification, and these commitments create the durable and time-bounded demand for electric mining equipment that is driving rapid market growth.

Rising Fuel Costs and Operational Efficiency Needs

Diesel fuel represents 20 to 35% of the total operating cost at most large mines, making it one of the most controllable and financially impactful cost categories that mine operators can address through equipment investment. Switching from diesel to battery electric equipment eliminates the direct fuel cost entirely, replacing it with electricity costs that are typically 40 to 70% lower per unit of energy for mines that can source electricity from the grid or from on-site renewable generation. For a large open-pit copper mine consuming several hundred million dollars of diesel fuel annually, the operating cost savings from fleet electrification can justify the higher upfront cost of electric equipment within a few years and generate substantial ongoing savings for the remaining equipment lifetime. This strong financial return from reduced fuel costs, combined with the lower maintenance costs of electric drivetrains which have fewer moving parts and do not require oil changes, exhaust system maintenance, or diesel engine overhauls, means that the total cost of ownership of electric mining equipment is increasingly competitive with diesel alternatives even before accounting for the carbon-related benefits of electrification.

Integration with Renewable Energy Microgrids

The combination of on-site renewable energy generation with battery electric mining equipment is a particularly compelling opportunity for remote mines that currently pay very high prices for diesel fuel that must be transported by road, pipeline, or in some cases by helicopter or barge to the mine site. The fully loaded cost of diesel at remote mining locations can be three to five times the wholesale market price, making the economics of renewable plus electric mining exceptionally favorable in these locations. A mine that can generate most of its electricity needs from solar panels and battery storage during the day and use that electricity to power and charge its electric fleet has dramatically lower energy costs than a diesel-dependent mine and is also much less exposed to fuel supply disruptions. Fortescue, one of the world's largest iron ore producers, has announced plans to convert its entire Pilbara mining fleet to renewable energy-powered electric equipment by 2030, representing one of the most ambitious fleet electrification programs in the industry and a model that other large mining companies in sun-rich locations are studying closely.

Electrification of Underground Mining Operations

The specific operational and economic advantages of battery electric equipment in underground mines represent a very large opportunity for equipment manufacturers and mining operators because underground mines have the clearest and most immediate financial case for electrification, and the large global inventory of underground mines represents a substantial potential replacement market for diesel equipment. The combination of reduced ventilation energy costs, which can save USD 5 million to USD 50 million per year at a deep underground mine depending on its size and depth, with eliminated diesel fuel costs and lower maintenance expenses creates a total cost of ownership advantage for battery electric underground equipment that is becoming financially compelling at current battery prices and will improve further as battery costs continue to fall. Epiroc and Sandvik's proven products in this space, the growing number of mines with operating experience that validates the technology, and the large number of underground mines that have not yet electrified their fleets represent a large near-term commercial opportunity for underground electric mining equipment across the gold, copper, nickel, and base metals mining sectors globally.

By Equipment Type: In 2026, Electric Haul Trucks to Dominate

Based on equipment type, the global electric mining equipment market is segmented into electric haul trucks, electric loaders (LHD), electric excavators, electric drilling equipment, electric underground mining vehicles, and other electric mining equipment. In 2026, the electric haul trucks segment is expected to account for the largest share of the global electric mining equipment market. Haul trucks are the single most expensive and fuel-consuming piece of equipment at most surface mines and represent the highest-value electrification opportunity on a per-unit basis. A large mining haul truck consumes several hundred liters of diesel per hour and costs USD 3 million to USD 5 million per unit, meaning that electric haul trucks also command the highest per-unit revenues in the equipment market. The development of trolley-assisted electric haul trucks that run on overhead wires on the main haul roads and switch to battery for off-road sections, as demonstrated by programs at BHP and Anglo American, provides a practical interim solution for large surface mines while fully battery-electric trucks are developed.

However, the electric drilling equipment segment is projected to register the highest CAGR during the forecast period. Electric drill rigs for both underground and surface mining are at an earlier stage of commercial adoption than loaders and haul trucks, meaning the growth rate from a smaller current base is expected to be higher. The advantage of electric drilling equipment in underground mines, where diesel fume generation from drill rigs in confined headings is a significant air quality challenge, is creating strong demand for commercial electric drill rig products from Epiroc, Sandvik, and smaller specialists.

By Powertrain Type: In 2026, Battery Electric Vehicles to Hold the Largest Share

Based on powertrain type, the global electric mining equipment market is segmented into battery electric vehicles, hybrid electric vehicles, and hydrogen fuel cell vehicles. In 2026, the battery electric vehicles segment is expected to account for the largest share of the global electric mining equipment market. Battery electric technology is the most commercially mature and most widely deployed electric powertrain in the mining equipment market, with multiple commercially available battery electric loaders, drill rigs, utility vehicles, and haul truck prototypes from established equipment manufacturers. The falling cost of lithium-ion batteries, the improving energy density that is extending the operating time between charges, and the proven operational performance of BEV equipment across multiple mining sites globally make battery electric the current dominant commercial technology choice.

However, the hydrogen fuel cell vehicles segment is projected to register the highest CAGR during the forecast period. Anglo American's nuGen demonstration truck and several other hydrogen fuel cell mining vehicle development programs indicate that the mining industry sees hydrogen as an important long-term solution for very large haul trucks where battery weight and charging time present practical challenges. Hydrogen fuel cell trucks can refuel as quickly as diesel trucks and do not require the very large and heavy battery packs that would be needed for multi-hundred-tonne haul trucks in long-shift operation, making hydrogen a more practical powertrain solution for the largest and most demanding mining applications as the technology develops.

By Application: In 2026, Underground Mining to Hold the Largest Share

Based on application, the global electric mining equipment market is segmented into underground mining, surface mining, material handling and transportation, drilling and blasting operations, exploration activities, and emerging applications. In 2026, the underground mining segment is expected to account for the largest share of the global electric mining equipment market. As discussed above, underground mining has the clearest and most immediately compelling financial case for electrification due to the very large savings from reduced ventilation requirements, and the commercial deployment of battery electric underground equipment is further advanced than any other application category. Epiroc and Sandvik have commercially available battery electric underground loaders and drill rigs that are operating productively in multiple mines, and the growing list of mines reporting positive experiences is accelerating adoption across the underground mining sector.

However, the surface mining segment is projected to register the highest CAGR during the forecast period. While the first commercial battery electric surface haul trucks are just beginning to enter the market, the very large number of surface mines globally and the enormous fleet replacement opportunity represented by the existing diesel haul truck inventory means that even modest adoption of electric haul trucks at surface mines represents very large total equipment market value growth. The development of electric haul truck solutions by Komatsu, Caterpillar, Hitachi, and Liebherr targeting the massive surface mining market is expected to drive rapid revenue growth in the surface mining application category through the forecast period.

By End User: In 2026, Metal Mining Companies to Hold the Largest Share

Based on end user, the global electric mining equipment market is segmented into coal mining companies, metal mining companies, mineral mining companies, and contractors and mining service providers. In 2026, the metal mining companies segment is expected to account for the largest share of the global electric mining equipment market. Metal miners including copper, gold, nickel, iron ore, and platinum producers are the most active adopters of electric mining equipment for two reasons: first, many of the world's most economically important metal mines are underground operations where the ventilation savings from electrification are most valuable; and second, the major metal mining companies including BHP, Rio Tinto, Anglo American, Newmont, and Barrick have made the strongest public sustainability commitments that translate into concrete fleet electrification procurement programs.

However, the contractors and mining service providers segment is projected to register the highest CAGR during the forecast period. As electric mining equipment becomes more commercially mainstream, the large contract mining companies that operate equipment on behalf of mine owners will increasingly need to offer electric equipment options to win contracts at mines that have made electrification commitments. Companies like Thiess, Macmahon, and African Mining Services that operate large fleets of mining equipment are beginning to acquire electric equipment for their fleets, and this trend is expected to accelerate as more mine owners require electric equipment from their contractors as part of their own scope 3 emission reduction strategies.

Electric Mining Equipment Market by Region: Asia-Pacific Leading by Share, Latin America by Growth

Based on geography, the global electric mining equipment market is segmented into Asia-Pacific, North America, Europe, Latin America, and the Middle East and Africa.

In 2026, Asia-Pacific is expected to account for the largest share of the global electric mining equipment market. The region's market dominance reflects the very large mining sectors of Australia, China, Indonesia, and India, which collectively account for a very large share of global mining output and equipment consumption. Australia is one of the most active markets for electric mining equipment adoption, driven by some of the world's largest iron ore, gold, and nickel mines that have made strong public electrification commitments, favorable solar energy conditions that support renewable energy integration with electric equipment, and a forward-thinking regulatory environment that encourages sustainable mining practices. Fortescue's commitment to eliminate diesel from its entire Pilbara iron ore mining fleet by 2030 is the most ambitious electrification program of any major mining company globally and represents an extraordinary procurement opportunity for electric haul truck suppliers. China's large and active mining equipment sector includes both major domestic manufacturers and significant adoption programs at Chinese mines operated by companies including China Shenhua and Zijin Mining. Australia also hosts the world's most advanced underground electric mining programs with several mines operating all-electric underground fleets in gold, nickel, and base metals mining.

However, the Latin American electric mining equipment market is expected to grow at the fastest CAGR during the forecast period. Latin America, particularly Chile and Peru, is home to some of the world's most important copper mines and is attracting very large investment in mine electrification driven by the combination of strong corporate ESG commitments from the major copper producers, the very high diesel costs in remote Andean mining locations that make the economic case for electrification extremely compelling, and the exceptional solar energy potential in the Atacama Desert that makes renewable energy integration with electric mining equipment highly practical and economical. Chile's major copper producers including Codelco, Antofagasta Minerals, and Anglo American Chile are all running electric equipment trials and developing fleet electrification roadmaps. Brazil's large iron ore and nickel mining sectors operated by Vale represent an additional major Latin American market for electric equipment adoption. The region's large number of high-altitude mines where diesel engine performance is degraded and ventilation is even more challenging than at sea-level underground mines adds further economic motivation for electrification in the Andean mining belt.

Europe is a significant and technologically leading market for electric mining equipment, driven primarily by Sweden and Finland where Epiroc and Sandvik are headquartered and where the Nordic mining sectors have been the earliest and most enthusiastic adopters of battery electric underground mining equipment. LKAB, the Swedish state-owned iron ore producer, has committed to fully electric operations at its underground mines and is a reference customer for Epiroc and Sandvik's electric equipment programs. The Scandinavian mines that were among the first to deploy commercial battery electric underground equipment have now accumulated years of operating experience that is providing the performance data and operational learnings that are informing the industry's broader electric adoption plans. North America is a growing market with active electric equipment programs at Canadian mines including the Borden gold mine and several nickel and base metals mines in Ontario and Quebec, driven by Canada's strong emission reduction policies, the high cost of underground mine ventilation in deep cold-climate mines, and the presence of major equipment manufacturers and technology developers in the region.

The electric mining equipment market includes the world's largest mining equipment manufacturers who are developing electric versions of their established diesel product lines, specialist underground mining equipment companies that were early leaders in battery electric technology, and smaller specialist companies developing purpose-built electric mining vehicles. Competition is based on equipment performance and productivity, battery technology capability, charging solution availability, total cost of ownership, the breadth of the electric product portfolio, and the ability to provide comprehensive operational support and service at remote mine sites.

Epiroc AB leads the underground electric mining equipment market with the broadest commercially available portfolio of battery electric underground loaders, drill rigs, and support vehicles, backed by operational experience at dozens of mines globally and a strong service network. Sandvik AB is Epiroc's closest competitor in underground electric equipment, with its LH514E electric loader and Rock Pulse battery technology platform, and has acquired Artisan Vehicles specifically to strengthen its electric underground equipment capabilities. Caterpillar is the world's largest mining equipment manufacturer and is developing electric haul trucks and surface equipment through its Cat Electric portfolio, with trolley-assist electric haul trucks already operating at BHP's Escondida mine. Komatsu is developing fully electric and fuel cell haul trucks through its P&H and Joy Global mining equipment brands. ABB and Siemens provide the electrical systems, drives, and power management infrastructure that support electric mining operations rather than the vehicles themselves.

The report provides a comprehensive competitive analysis based on a thorough review of leading players' product portfolios, operational deployment experience, customer relationships, geographic presence, and recent strategic developments. Some of the key players operating in the global electric mining equipment market include Caterpillar Inc. (U.S.), Komatsu Ltd. (Japan), Epiroc AB (Sweden), Sandvik AB (Sweden), Hitachi Construction Machinery Co. Ltd. (Japan), Liebherr Group (Germany/Switzerland), Volvo Construction Equipment (Sweden), ABB Ltd. (Switzerland), Siemens AG (Germany), Komatsu Mining Corporation (U.S.), Normet Group (Finland), MacLean Engineering (Canada), Artisan Vehicles/Sandvik (U.S./Sweden), Rokion Inc. (Canada), and MEDATech Engineering Services (Canada), among others.

The global electric mining equipment market is expected to reach USD 28.6 billion by 2036 from an estimated USD 7.8 billion in 2026, at a CAGR of 13.8% during the forecast period 2026-2036.

In 2026, the electric haul trucks segment is expected to hold the largest share of the global electric mining equipment market, driven by haul trucks representing the highest-value and highest fuel-consuming equipment category at surface mines and the largest per-unit revenue opportunity in the electric mining equipment market.

The electric drilling equipment segment is expected to register the highest CAGR during the forecast period 2026-2036, driven by the significant air quality advantages of eliminating diesel drill rigs in underground mining environments and the earlier-stage commercial development that supports higher percentage growth from a smaller current base.

In 2026, the underground mining segment is expected to hold the largest share of the global electric mining equipment market, reflecting underground mines having the most immediate and financially compelling case for electrification due to the very large ventilation energy savings that battery electric equipment enables.

Asia-Pacific is expected to dominate the global electric mining equipment market in 2026, driven by Australia's very large mining sector with strong electrification commitments from major producers, China's large mining equipment consumption, and the active electric equipment programs at Australasian iron ore, gold, and nickel mines.

The market is primarily driven by mining companies' formal decarbonization commitments requiring fleet electrification as the primary pathway to reducing diesel combustion emissions, and by the strong financial case for electrification driven by diesel fuel cost savings and underground ventilation energy cost reductions that make electric equipment increasingly competitive with diesel alternatives on total cost of ownership.

Key players are Caterpillar Inc. (U.S.), Komatsu Ltd. (Japan), Epiroc AB (Sweden), Sandvik AB (Sweden), Hitachi Construction Machinery Co. Ltd. (Japan), Liebherr Group (Germany/Switzerland), Volvo Construction Equipment (Sweden), ABB Ltd. (Switzerland), Siemens AG (Germany), Komatsu Mining Corporation (U.S.), Normet Group (Finland), MacLean Engineering (Canada), Artisan Vehicles/Sandvik (U.S./Sweden), Rokion Inc. (Canada), and MEDATech Engineering Services (Canada), among others.

Latin America is expected to register the highest growth rate in the global electric mining equipment market during the forecast period 2026-2036, driven by Chile's world-class copper mines committing to fleet electrification, the very high diesel costs in remote Andean mining locations that strengthen the economic case for electric equipment, and the exceptional solar energy potential in the Atacama Desert supporting renewable energy integration.

Published Date: May-2024

Published Date: Apr-2024

Published Date: Jan-2024

Published Date: Feb-2026

Published Date: Jul-2022

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates