Resources

About Us

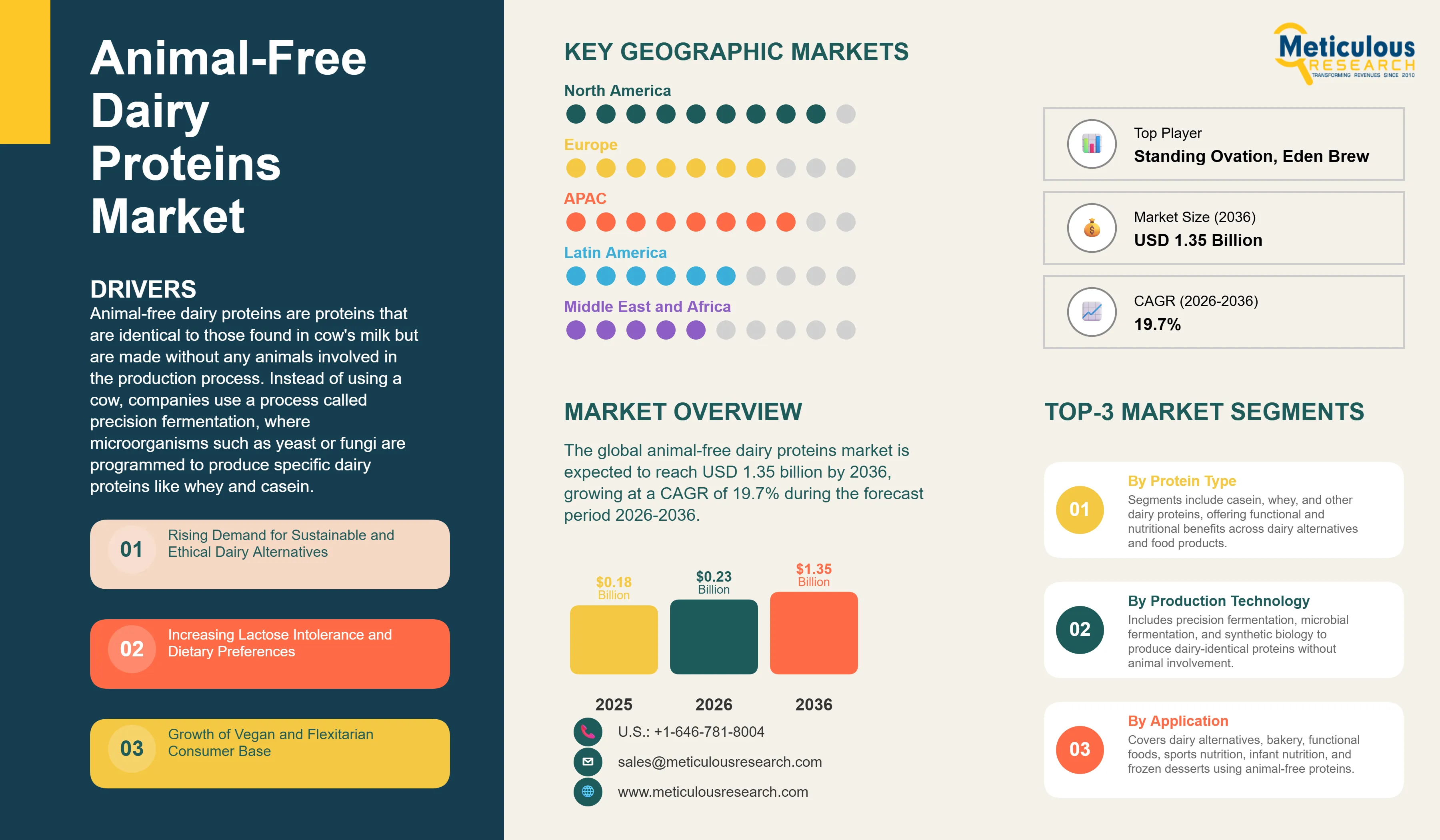

The global animal-free dairy proteins market was valued at USD 0.18 billion in 2025. This market is expected to reach USD 1.35 billion by 2036 from an estimated USD 0.23 billion in 2026, growing at a CAGR of 19.7% during the forecast period 2026-2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Animal-free dairy proteins are proteins that are identical to those found in cow's milk but are made without any animals involved in the production process. Instead of using a cow, companies use a process called precision fermentation, where microorganisms such as yeast or fungi are programmed to produce specific dairy proteins like whey and casein. The result is a protein that is chemically the same as conventional dairy protein but is produced sustainably, without livestock, and without the environmental impact associated with traditional dairy farming. These proteins can then be used by food companies to make products including cheese, yogurt, ice cream, and protein drinks that taste and behave like conventional dairy products but carry a clean and animal-free ingredient story.

The market is growing rapidly because a significant number of consumers around the world want the taste, nutrition, and functionality of dairy products but are concerned about animal welfare, environmental sustainability, or personal dietary reasons such as lactose intolerance. Plant-based dairy alternatives like oat milk and almond milk have grown enormously but many consumers find that these products do not taste or perform quite the same as conventional dairy. Animal-free dairy proteins offer a potential solution to this problem because they are the actual proteins found in real dairy, so they deliver the same taste, melt, stretch, and nutritional content that consumers expect from real dairy products, while being made through a process that does not require animals.

Two significant opportunities are shaping the market going forward. As fermentation technology improves and production scales up, the cost of making these proteins is falling steadily, and the point where animal-free dairy proteins can compete on price with conventional dairy is getting closer. Companies that establish strong brand and customer relationships now, while the market is still small, will be well positioned when that cost parity is achieved and mass-market adoption becomes possible. In addition, the growing consumer interest in high-protein, clean-label, and functional food and beverage products is creating strong demand for premium protein ingredients with clear sustainability stories, which animal-free dairy proteins are very well placed to provide.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 1.36 Billion |

|

Market Size in 2026 |

USD 0.23 Billion |

|

Market Size in 2025 |

USD 0.18 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 19.7% |

|

Dominating Protein Type |

Whey Proteins |

|

Fastest Growing Protein Type |

Casein Proteins |

|

Dominating Production Technology |

Precision Fermentation |

|

Fastest Growing Production Technology |

Synthetic Biology-Based Production |

|

Dominating Application |

Dairy Alternatives (Milk, Cheese, Yogurt) |

|

Fastest Growing Application |

Sports Nutrition |

|

Dominating End User |

Food & Beverage Manufacturers |

|

Fastest Growing End User |

Nutraceutical Companies |

|

Dominating Distribution Channel |

Direct B2B Sales |

|

Fastest Growing Distribution Channel |

Online Channels |

|

Dominating Functionality |

Nutritional Enhancement |

|

Fastest Growing Functionality |

Gelation |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Perfect Day's Commercial Launch Proving the Business Model Works

The most important commercial development in the animal-free dairy proteins market has been Perfect Day's successful launch of whey proteins produced through precision fermentation and their licensing to consumer food brands including Archer Daniels Midland, Graeter's Ice Cream, Bored Cow, and the Nick's brand, which demonstrated for the first time that fermentation-derived dairy proteins can be used in real commercial food products sold at retail. Perfect Day's approach of selling its protein as a branded ingredient to established food companies rather than trying to build its own consumer brand directly has proven to be an effective commercial strategy because it allows the company to leverage the distribution networks, marketing capabilities, and retail relationships of partners who already know how to sell food products to consumers.

This partnership and licensing model has become a template that other animal-free dairy protein companies are following. Rather than requiring consumers to buy products from unknown startup brands, the ingredient licensing approach puts animal-free dairy proteins inside familiar products from brands that consumers already trust. A well-known ice cream company making its premium product with animal-free whey protein can introduce this ingredient to millions of consumers who would never seek out a specialty protein supplement. This approach is significantly accelerating consumer exposure to animal-free dairy proteins and building the consumer awareness and acceptance that will be necessary for mass-market adoption as costs come down.

Cheese Is Emerging as the Highest-Value Target Application

While whey protein has been the first animal-free dairy protein to reach commercial scale, cheese is widely seen as the most commercially attractive target application for animal-free casein proteins. Conventional cheese alternatives made from nuts, oats, or other plant sources generally fail to melt, stretch, or brown the way real cheese does. These functional properties of real cheese come from casein proteins, which form a specific network structure when heated that gives cheese its characteristic melt and stretch behavior. Plant-based ingredients cannot replicate this because they do not have casein. Animal-free casein proteins produced through precision fermentation have exactly the same molecular structure as dairy casein, which means they can deliver the melt, stretch, and flavor of real cheese in a product made entirely without animals.

Companies including New Culture, Formo, and Change Foods are specifically targeting the cheese application, developing animal-free mozzarella and other cheese varieties using precision fermentation casein. The commercial potential of the cheese market is very large because cheese is one of the most consumed dairy products globally and conventional cheese alternatives have historically disappointed consumers with poor sensory performance. A genuinely dairy-equivalent cheese made without animals and with a strong sustainability story could command significant premium pricing and capture a substantial share of the growing dairy-free and flexitarian consumer segment that has been underserved by existing plant-based cheese products.

Large Food Companies Forming Strategic Partnerships to Secure Ingredient Access

Established food and ingredient companies are increasingly forming partnerships with animal-free dairy protein startups rather than waiting for the technology to mature and then competing with their own products. Companies like Archer Daniels Midland, Ingredion, and several large dairy cooperatives have made investments and partnership agreements with precision fermentation protein companies, recognizing that animal-free dairy proteins are likely to be an important ingredient category in future food production and that securing early access to the technology and production capacity is strategically valuable. The Nature's Fynd investment by Blackstone, ADM's partnership with Perfect Day, and the Series B and C funding rounds that multiple animal-free protein companies have completed from strategic food industry investors all reflect this growing recognition that the technology is real, the consumer demand is genuine, and early-mover partnerships are commercially important.

This strategic investment trend is accelerating the scaling of production capacity for animal-free dairy proteins by connecting startup technology developers with the capital and industry expertise of established food companies. The startups provide the biotechnology knowledge and product innovation while the established food industry partners provide distribution, customer relationships, food safety expertise, and access to capital markets. For investors and market participants assessing the commercial trajectory of animal-free dairy proteins, the quality and scale of these strategic partnerships is one of the most reliable indicators of which technologies and companies are likely to achieve significant commercial scale over the forecast period.

Rising Demand for Sustainable and Ethical Dairy Alternatives

The dairy industry is one of the most significant contributors to greenhouse gas emissions, water use, and land use in the global food system. A growing number of consumers, particularly among younger age groups in North America and Europe, are actively looking to reduce their consumption of conventional dairy products for environmental reasons. At the same time, animal welfare concerns about dairy farming practices are influencing purchasing decisions for a significant minority of consumers who want to continue enjoying dairy-taste products without the ethical compromises of conventional dairy production. Animal-free dairy proteins offer a compelling answer to both concerns because they deliver the actual proteins of dairy, with all their taste and nutritional benefits, through a production process that uses no animals and has a much smaller environmental footprint than conventional dairy farming. This combination of environmental and ethical positioning gives animal-free dairy proteins a strong value proposition that goes beyond simple dietary preference and taps into deeper consumer values that are becoming increasingly mainstream in developed market food purchasing decisions.

Technological Advancements in Precision Fermentation

Precision fermentation has become significantly more capable and more affordable over the past five years as a result of advances in synthetic biology, improvements in fermentation strain engineering, and the scaling of industrial bioreactor infrastructure. The cost of producing a kilogram of fermentation-derived protein has fallen substantially as fermentation yields have improved through better strain development and process optimization, and as production facilities have moved from pilot scale to commercial scale with the associated efficiency gains. Companies including Perfect Day and Remilk have demonstrated commercial-scale production of dairy proteins through precision fermentation and are actively working to reduce costs further through continued fermentation process improvements and facility scale-up. As production costs continue to fall along a trajectory similar to other biotechnology-derived ingredients, the price gap between animal-free dairy proteins and conventional dairy proteins is expected to narrow significantly through the forecast period, progressively opening up lower-priced mass-market food applications to animal-free dairy proteins alongside the premium-priced specialty products that currently constitute the majority of the market.

Expansion in Functional and High-Protein Food Products

The booming market for high-protein, functional food and beverage products represents an immediately accessible commercial opportunity for animal-free dairy proteins that does not depend on achieving full cost parity with conventional dairy. Consumers seeking high-quality protein for sports nutrition, general wellness, and weight management are already paying premium prices for protein bars, protein shakes, and high-protein dairy products. An animal-free whey or casein protein ingredient positioned as a premium, sustainable, and animal-free alternative to conventional whey protein concentrate can command a price premium that makes it financially viable in these applications at current production costs. The existing premium protein supplement market is therefore a strong near-term revenue opportunity for animal-free dairy protein companies that allows them to build revenue and production scale while continuing to reduce costs toward the price points required for mainstream dairy alternative applications.

Partnerships with Food & Beverage Brands

The most effective way for animal-free dairy protein ingredient companies to reach consumers at scale is to supply their proteins to established food and beverage brands that already have the distribution networks, consumer trust, and marketing resources to bring products to mass market. For an ingredient company, securing a supply agreement with a major dairy company, a leading ice cream brand, or a large nutritional products company gives access to the established partner's entire customer base and retail distribution, which would take years and hundreds of millions of dollars to build from scratch. For the established brand, offering an animal-free dairy protein version of an existing product with a strong sustainability story can attract new customers from the growing segment of consumers who want dairy-quality products without animal sourcing. Both sides benefit, making these partnerships commercially attractive for food brands and essential to the commercial growth of animal-free dairy protein ingredient companies. Establishing more of these high-profile brand partnerships is therefore the most important commercial priority for animal-free dairy protein companies over the forecast period.

By Protein Type: In 2026, Whey Proteins to Dominate

Based on protein type, the global animal-free dairy proteins market is segmented into casein proteins, whey proteins, and other dairy proteins. In 2026, the whey proteins segment is expected to account for the largest share of the global animal-free dairy proteins market. Whey proteins are currently the most commercially advanced animal-free dairy protein category, primarily because Perfect Day has achieved commercial-scale production of fermentation-derived whey protein and has multiple licensed products sold at retail. Whey proteins are also the most familiar and commercially established protein ingredient in the sports nutrition and functional food markets, where buyers and consumers are already comfortable paying premium prices for high-quality whey protein. This existing market familiarity means animal-free whey protein can be introduced with relatively little consumer education required, making it the natural first commercial entry point for the animal-free dairy protein industry.

However, the casein proteins segment is poised to register the highest CAGR during the forecast period. Casein is the protein responsible for the distinctive melting, stretching, and texture properties of real cheese, and it is the primary target for companies trying to make genuinely dairy-equivalent cheese without animals. Because no good plant-based substitute for casein exists, the commercial opportunity for animal-free casein in the large cheese market is very large, and the companies successfully developing commercial-scale casein production will unlock access to a much larger total market than whey alone. Investment in casein protein development is growing rapidly, and the first commercial launches of casein-based animal-free cheese products are expected within the forecast period.

By Production Technology: In 2026, Precision Fermentation to Hold the Largest Share

Based on production technology, the global animal-free dairy proteins market is segmented into precision fermentation, microbial fermentation, and synthetic biology-based production. In 2026, the precision fermentation segment is expected to account for the largest share of the global animal-free dairy proteins market. Precision fermentation is the process of programming a microorganism such as yeast, fungi, or bacteria to produce a specific protein by inserting the relevant gene sequence into the microorganism's DNA. The microorganism then acts as a tiny factory, producing the desired protein as it grows and reproduces in a fermentation tank. This technology has been used in the food industry for decades to produce enzymes, vitamins, and food additives such as rennet for cheese making, and applying it to dairy proteins is a natural extension of established industrial biotechnology. Perfect Day and Remilk have both demonstrated commercial-scale precision fermentation production of dairy proteins, establishing this as the current commercial standard for the industry.

However, the synthetic biology-based production segment is projected to register the highest CAGR during the forecast period. Synthetic biology goes beyond inserting single genes into existing microorganisms to designing entirely new biosynthetic pathways and even entirely engineered microorganism genomes optimized for the most efficient possible protein production. While more complex to develop, synthetic biology approaches offer the potential for significantly higher production yields and lower costs at scale compared with conventional precision fermentation, and the falling cost of DNA synthesis and genome engineering tools is making synthetic biology increasingly accessible to food protein companies. Companies at the frontier of synthetic biology applied to food protein production may achieve production cost structures that make cost parity with conventional dairy proteins achievable faster than current precision fermentation technology alone would allow.

By Application: In 2026, Dairy Alternatives to Hold the Largest Share

Based on application, the global animal-free dairy proteins market is segmented into dairy alternatives (milk, cheese, and yogurt), bakery and confectionery, functional foods and beverages, sports nutrition, infant nutrition, and ice cream and frozen desserts. In 2026, the dairy alternatives segment is expected to account for the largest share of the global animal-free dairy proteins market. Dairy alternative products such as animal-free milk, cheese, yogurt, and ice cream are the most direct and obvious application for animal-free dairy proteins, as these products are designed to replace conventional dairy products with something that looks, tastes, and functions the same way. The large and rapidly growing market for dairy-free products, driven by veganism, lactose intolerance, and general health and sustainability preferences, provides the consumer demand that makes dairy alternative applications the primary commercial focus for animal-free dairy protein companies.

However, the sports nutrition segment is projected to register the highest CAGR during the forecast period. Sports nutrition consumers are already highly educated about protein quality, are accustomed to paying significant premiums for better protein ingredients, and many are actively looking for clean, sustainable protein options that align with their health and values. This combination of price-tolerance, product sophistication, and sustainability awareness makes sports nutrition an ideal early commercial market for animal-free dairy proteins where premium positioning can be justified without requiring the broad mass-market consumer education that lower-margin applications would need. Several sports nutrition brands have already begun incorporating or announcing plans to incorporate animal-free dairy proteins into their product lines, and this segment is expected to be one of the fastest-growing in the market.

By End User: In 2026, Food & Beverage Manufacturers to Hold the Largest Share

Based on end user, the global animal-free dairy proteins market is segmented into food and beverage manufacturers, nutraceutical companies, the food service industry, and retail consumers. In 2026, the food and beverage manufacturers segment is expected to account for the largest share of the global animal-free dairy proteins market. Large food and beverage manufacturers represent the primary direct customer for animal-free dairy proteins at the ingredient level, buying proteins in bulk to incorporate into their branded consumer products. The licensing and supply agreements that animal-free protein companies have established with food manufacturers are the primary revenue channel for the industry, and the growing number of established food companies adding animal-free dairy protein products to their portfolios is the clearest indicator of the market's commercial momentum. When a large food manufacturer adopts an animal-free dairy protein ingredient, it can generate very significant ingredient procurement volumes that help drive production scale and cost reduction.

However, the nutraceutical companies segment is projected to register the highest CAGR during the forecast period. Nutraceutical and supplement companies that formulate protein-rich health products are among the most commercially ready customers for premium animal-free dairy proteins because their customers already expect to pay above-average prices for high-quality protein ingredients with strong health and sustainability credentials. The nutraceutical channel is therefore one of the fastest pathways to commercial adoption for animal-free dairy proteins, and the growth of this segment will be an important contributor to the revenue scaling that enables animal-free protein companies to reduce costs through higher production volumes.

By Distribution Channel: In 2026, Direct B2B Sales to Hold the Largest Share

Based on distribution channel, the global animal-free dairy proteins market is segmented into direct B2B sales, retail channels, and online channels. In 2026, the direct B2B sales segment is expected to account for the largest share of the global animal-free dairy proteins market. Because animal-free dairy proteins are primarily sold as bulk ingredients to food and beverage manufacturers rather than directly to consumers, direct business-to-business sales to food companies are the dominant revenue channel. Ingredient supply agreements, licensing arrangements, and long-term supply contracts with food manufacturers, nutraceutical companies, and food service operators constitute the primary commercial activity of the market's leading companies. These B2B relationships are typically the highest-volume and most commercially significant transactions in the animal-free dairy proteins supply chain.

However, the online channels segment is projected to register the highest CAGR during the forecast period. As consumer-facing animal-free dairy protein products including branded protein powders, health supplements, and specialty food items become more widely available, online direct-to-consumer sales through brand websites, Amazon, and specialty health and wellness e-commerce platforms are growing rapidly. Online channels are particularly important for reaching the early-adopter consumers who are actively seeking out animal-free and sustainable products and who are comfortable purchasing specialty items online that may not yet be widely available in conventional retail stores.

Animal-Free Dairy Proteins Market by Region: North America Leading by Share, Asia-Pacific by Growth

Based on geography, the global animal-free dairy proteins market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

In 2026, North America is expected to account for the largest share of the global animal-free dairy proteins market. The United States is home to the majority of the world's leading animal-free dairy protein companies, including Perfect Day, New Culture, Helaina, Change Foods, TurtleTree, and Nobell Foods, many of which are based in the San Francisco Bay Area where the intersection of food-tech innovation and venture capital funding has created a strong startup ecosystem for alternative protein technology. The U.S. Food and Drug Administration has provided regulatory clearance for several precision fermentation dairy proteins including Perfect Day's whey protein, which is classified as Generally Recognized as Safe, giving American companies a clearer regulatory pathway for commercial product launches than exists in some other markets. The large and affluent U.S. consumer market for premium, sustainable, and health-oriented food products provides strong demand for animal-free dairy products at the premium price points that current production costs require. Canada's growing food-tech sector and its strong dairy industry create interesting conditions for both innovation and eventual mainstream adoption.

However, the Asia-Pacific animal-free dairy proteins market is expected to grow at the fastest CAGR during the forecast period. Asia-Pacific is home to the world's largest population of lactose-intolerant consumers, particularly across East and Southeast Asia where the majority of adults cannot comfortably digest conventional dairy. This creates a very large base of consumers who would benefit from dairy-quality products made with animal-free proteins that deliver the nutritional and functional benefits of dairy without the digestive discomfort. China's rapidly growing middle class with increasing interest in premium health food products, Japan's advanced functional food market and consumers' strong affinity for high-quality protein products, South Korea's dynamic food innovation sector, and Australia's active food-tech startup scene all contribute to the region's growth potential. Singapore has emerged as a particularly important hub for alternative protein investment and innovation in Asia, with government support programs specifically targeting precision fermentation and alternative protein technologies as strategic industries.

Europe is a significant and well-developed market for animal-free dairy proteins, with a strong regulatory framework being developed through the EU Novel Food regulation, active food-tech startup activity particularly in Germany, the Netherlands, Denmark, and the UK, and a large consumer base that is broadly receptive to sustainable food innovations. Formo in Germany and Better Dairy in the UK are among the most active European precision fermentation dairy protein companies. The European market's strong sustainability orientation and its large dairy consumption per capita create a compelling consumer market for animal-free dairy products that can deliver the dairy experience without the environmental impact. The European Food Safety Authority's evaluation process for novel food approvals provides a clear but time-consuming pathway for commercializing animal-free dairy proteins in Europe, and several companies are actively working through this process.

The animal-free dairy proteins market is composed primarily of well-funded technology startups that have developed precision fermentation and synthetic biology platforms for producing dairy proteins, alongside a smaller number of established ingredient companies beginning to enter the space. Competition is based on the quality and efficiency of fermentation technology, the range of proteins that can be produced, the regulatory clearances secured, the quality of brand partnerships and customer agreements, and the ability to scale production to reduce costs toward conventional dairy price levels.

The report provides a comprehensive competitive analysis based on a thorough review of leading players' technology platforms, protein portfolios, regulatory status, commercial partnerships, and recent strategic developments. Some of the key players operating in the global animal-free dairy proteins market include Perfect Day Inc. (U.S.), Remilk Ltd. (Israel), Formo Bio GmbH (Germany), Change Foods (U.S./Australia), TurtleTree Labs (Singapore), Imagindairy Ltd. (Israel), New Culture (U.S.), Standing Ovation (France), Zero Cow Factory (India), Nobell Foods (U.S.), Better Dairy (UK), All G Foods (Australia), Eden Brew (Australia), Wilk Technologies Ltd. (Israel), and Helaina Inc. (U.S.), among others.

The global animal-free dairy proteins market is expected to reach USD 1.36 billion by 2036 from an estimated USD 0.23 billion in 2026, at a CAGR of 19.7% during the forecast period 2026-2036.

In 2026, the whey proteins segment is expected to hold the largest share of the global animal-free dairy proteins market, driven by whey being the first animal-free dairy protein to achieve commercial scale through Perfect Day's production and the multiple licensed consumer product launches using fermentation-derived whey.

The casein proteins segment is expected to register the highest CAGR during the forecast period 2026-2036, driven by casein being the key protein required to make genuinely dairy-equivalent cheese with real melt and stretch properties, unlocking access to the much larger cheese market as commercial casein production scales up.

In 2026, the dairy alternatives segment is expected to hold the largest share of the global animal-free dairy proteins market, reflecting dairy alternative products including animal-free milk, cheese, yogurt, and ice cream being the primary and most direct application for animal-free dairy proteins.

The sports nutrition segment is projected to register the highest CAGR during the forecast period, driven by sports nutrition consumers already being accustomed to paying premium prices for high-quality protein and actively seeking sustainable and clean-label options that align with their health and values.

The market is primarily driven by the growing number of consumers who want dairy-quality products without the animal welfare and environmental impact of conventional dairy, and by the significant progress being made in reducing the cost of precision fermentation production as technology improves and production facilities scale up, making commercial viability across more food applications increasingly achievable.

Key players are Perfect Day Inc. (U.S.), Remilk Ltd. (Israel), Formo Bio GmbH (Germany), Change Foods (U.S./Australia), TurtleTree Labs (Singapore), Imagindairy Ltd. (Israel), New Culture (U.S.), Standing Ovation (France), Zero Cow Factory (India), Nobell Foods (U.S.), Better Dairy (UK), All G Foods (Australia), Eden Brew (Australia), Wilk Technologies Ltd. (Israel), and Helaina Inc. (U.S.), among others.

Asia-Pacific is expected to register the highest growth rate in the global animal-free dairy proteins market during the forecast period 2026-2036, driven by the very large population of lactose-intolerant consumers across East and Southeast Asia, the rapidly growing middle-class demand for premium health food products, and active government support for precision fermentation food technology particularly in Singapore and Australia.

1.Introduction

1.1 Market Definition

1.2 Market Ecosystem

1.3 Currency and Limitations

1.3.1 Currency

1.3.2 Limitations

1.4 Key Stakeholders

2.Research Methodology

2.1 Research Approach

2.2 Data Collection & Validation Process

2.2.1 Secondary Research

2.2.2 Primary Research & Validation

2.2.2.1 Primary Interviews with Experts

2.2.2.2 Approaches for Country-/Region-Level Analysis

2.3 Market Estimation

2.3.1 Bottom-Up Approach

2.3.2 Top-Down Approach

2.3.3 Growth Forecast

2.4 Data Triangulation

2.5 Assumptions for the Study

3.Executive Summary

4.Market Overview

4.1 Introduction

4.2 Market Dynamics

4.2.1 Drivers

4.2.1.1 Rising Demand for Sustainable and Ethical Dairy Alternatives

4.2.1.2 Increasing Lactose Intolerance and Dietary Preferences

4.2.1.3 Growth of Vegan and Flexitarian Consumer Base

4.2.1.4 Technological Advancements in Precision Fermentation

4.2.2 Restraints

4.2.2.1 High Production Costs

4.2.2.2 Regulatory Uncertainty for Novel Proteins

4.2.2.3 Limited Consumer Awareness in Emerging Markets

4.2.3 Opportunities

4.2.3.1 Expansion in Functional and High-Protein Food Products

4.2.3.2 Partnerships with Food & Beverage Brands

4.2.3.3 Scaling of Fermentation Technologies

4.2.3.4 Growth in Clean-Label and Sustainable Ingredients

4.2.4 Challenges

4.2.4.1 Achieving Cost Parity with Conventional Dairy

4.2.4.2 Scaling Manufacturing Infrastructure

4.3 Technology Landscape

4.3.1 Precision Fermentation Technology

4.3.2 Microbial Fermentation Platforms (Yeast, Fungi, Bacteria)

4.3.3 Synthetic Biology and Protein Engineering

4.3.4 Downstream Processing and Purification

4.3.5 Scale-Up and Bioreactor Technologies

4.4 Animal-Free Dairy Protein Architecture (Critical Segmentation)

4.4.1 Casein Proteins

4.4.2 Whey Proteins

4.4.3 Milk Fat Proteins and Functional Lipids

4.4.4 Functional and Specialty Proteins

4.5 Value Chain Analysis

4.5.1 Feedstock and Raw Material Suppliers

4.5.2 Fermentation Technology Providers

4.5.3 Ingredient Manufacturers

4.5.4 Food & Beverage Companies

4.5.5 Distribution Channels and End Consumers

4.6 Regulatory and Standards Landscape

4.6.1 Novel Food Regulations (FDA, EFSA, etc.)

4.6.2 Labeling and Claims (Dairy vs Non-Dairy)

4.6.3 Food Safety and Quality Standards

4.7 Porter's Five Forces Analysis

4.8 Investment and Industry Trends

4.8.1 Venture Capital Investments in Food-Tech Startups

4.8.2 Strategic Partnerships with Dairy Companies

4.8.3 Expansion of Precision Fermentation Facilities

4.9 Cost and Pricing Analysis

4.9.1 Cost Structure of Fermentation-Based Proteins

4.9.2 Price Comparison vs Conventional Dairy Proteins

4.9.3 Scaling Impact on Pricing

5.Animal-Free Dairy Proteins Market, by Protein Type

5.1 Introduction

5.2 Casein Proteins

5.2.1 Alpha-Casein

5.2.2 Beta-Casein

5.2.3 Kappa-Casein

5.3 Whey Proteins

5.3.1 Beta-Lactoglobulin

5.3.2 Alpha-Lactalbumin

5.4 Other Dairy Proteins

6.Animal-Free Dairy Proteins Market, by Production Technology

6.1 Introduction

6.2 Precision Fermentation

6.3 Microbial Fermentation

6.4 Synthetic Biology-Based Production

7.Animal-Free Dairy Proteins Market, by Application

7.1 Introduction

7.2 Dairy Alternatives (Milk, Cheese, Yogurt)

7.3 Bakery and Confectionery

7.4 Functional Foods and Beverages

7.5 Sports Nutrition

7.6 Infant Nutrition

7.7 Ice Cream and Frozen Desserts

8.Animal-Free Dairy Proteins Market, by End User

8.1 Introduction

8.2 Food & Beverage Manufacturers

8.3 Nutraceutical Companies

8.4 Food Service Industry

8.5 Retail Consumers

9.Animal-Free Dairy Proteins Market, by Distribution Channel

9.1 Introduction

9.2 Direct B2B Sales

9.3 Retail Channels

9.4 Online Channels

10.Animal-Free Dairy Proteins Market, by Functionality

10.1 Introduction

10.2 Emulsification

10.3 Foaming

10.4 Gelation

10.5 Nutritional Enhancement

11.Animal-Free Dairy Proteins Market, by Geography

11.1 Introduction

11.2 North America

11.2.1 U.S.

11.2.2 Canada

11.2.3 Mexico

11.3 Europe

11.3.1 Germany

11.3.2 U.K.

11.3.3 France

11.3.4 Netherlands

11.3.5 Denmark

11.3.6 Sweden

11.3.7 Switzerland

11.3.8 Italy

11.3.9 Spain

11.3.10 Rest of Europe

11.4 Asia-Pacific

11.4.1 China

11.4.2 India

11.4.3 Japan

11.4.4 South Korea

11.4.5 Australia

11.4.6 Singapore

11.4.7 Indonesia

11.4.8 Thailand

11.4.9 Vietnam

11.4.10 Rest of Asia-Pacific

11.5 Latin America

11.5.1 Brazil

11.5.2 Mexico

11.5.3 Argentina

11.5.4 Chile

11.5.5 Colombia

11.5.6 Rest of Latin America

11.6 Middle East & Africa

11.6.1 UAE

11.6.2 Saudi Arabia

11.6.3 Israel

11.6.4 South Africa

11.6.5 Turkey

11.6.6 Rest of Middle East & Africa

12.Competitive Landscape

12.1 Overview

12.2 Key Growth Strategies

12.3 Competitive Benchmarking

12.4 Competitive Dashboard

12.4.1 Industry Leaders

12.4.2 Market Differentiators

12.4.3 Vanguards

12.4.4 Emerging Companies

12.5 Market Ranking/Positioning Analysis of Key Players, 2025

13.Company Profiles

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

13.1 Perfect Day, Inc.

13.2 Remilk Ltd.

13.3 Formo Bio GmbH

13.4 Change Foods

13.5 TurtleTree Labs

13.6 Imagindairy Ltd.

13.7 New Culture

13.8 Standing Ovation

13.9 Zero Cow Factory

13.10 Nobell Foods

13.11 Better Dairy

13.12 All G Foods

13.13 Eden Brew

13.14 Wilk Technologies Ltd.

13.15 Helaina Inc.

14.Appendix

14.1 Additional Customization

14.2 Related Reports

Published Date: May-2025

Published Date: Jan-2025

Published Date: Nov-2024

Published Date: Aug-2024

Published Date: Aug-2024

Subscribe to get the latest industry updates