Resources

About Us

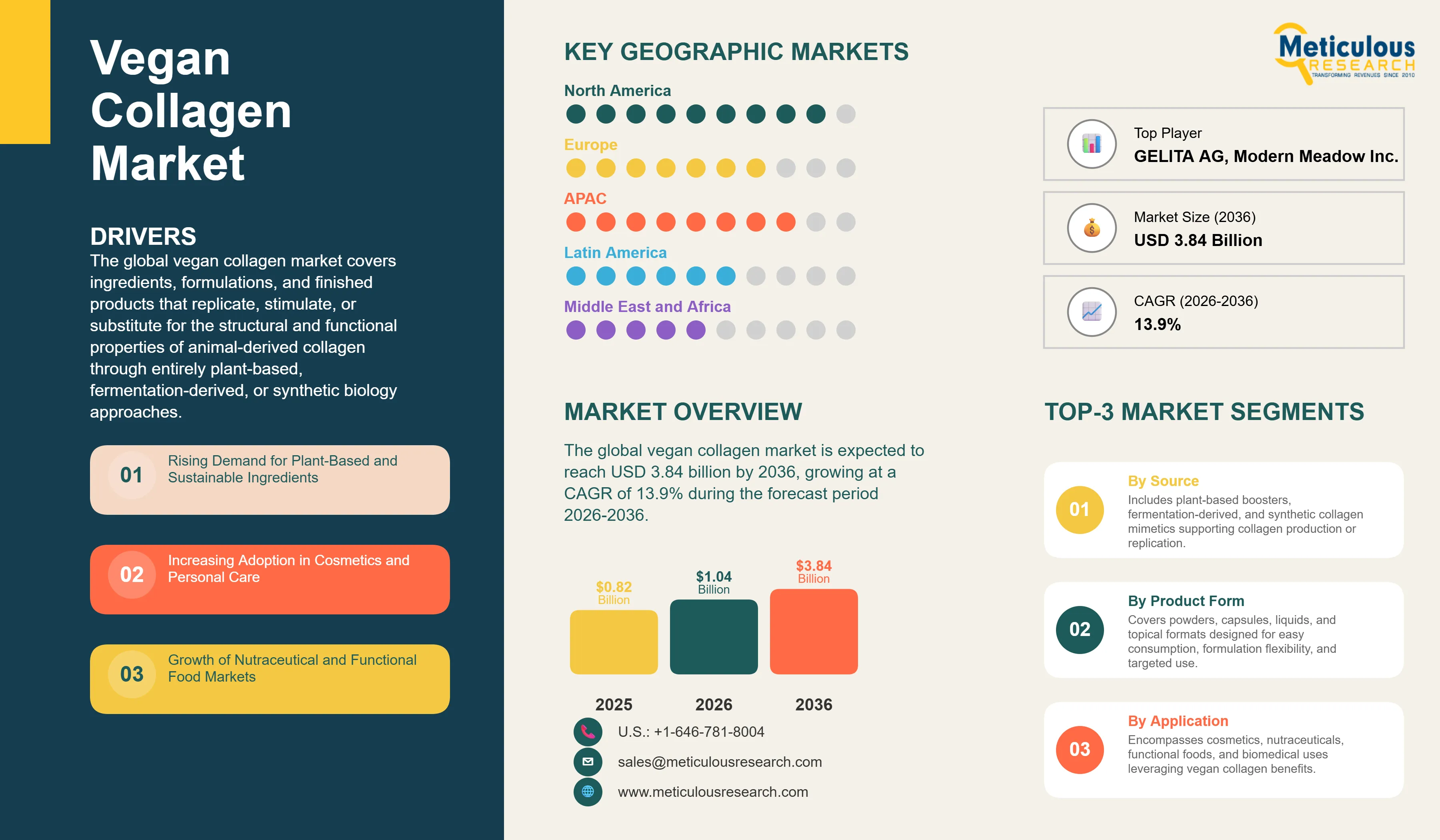

The global vegan collagen market was valued at USD 0.82 billion in 2025. This market is expected to reach USD 3.84 billion by 2036 from an estimated USD 1.04 billion in 2026, growing at a CAGR of 13.9% during the forecast period 2026-2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global vegan collagen market covers ingredients, formulations, and finished products that replicate, stimulate, or substitute for the structural and functional properties of animal-derived collagen through entirely plant-based, fermentation-derived, or synthetic biology approaches. This encompasses plant-based collagen booster blends combining amino acids such as glycine, proline, hydroxyproline, and lysine with cofactor vitamins including C and B vitamins that support the body's endogenous collagen synthesis pathways, fermentation-derived recombinant collagen proteins produced through precision fermentation using genetically engineered yeast or bacteria expressing human or plant collagen gene sequences, and biomimetic synthetic collagen peptide structures designed to mimic the triple-helix structural properties of natural collagen across skincare, nutraceutical, dietary supplement, functional food, and biomedical application segments.

The growth of the global vegan collagen market is primarily driven by the rapid mainstream adoption of vegan, plant-based, and cruelty-free product preferences across cosmetics, personal care, and nutritional supplement consumer segments, which is progressively shifting purchasing decisions away from conventional marine and bovine collagen products toward plant-based and biotechnology-derived alternatives that align with ethical consumption values. The cosmetics and personal care industry's accelerating clean beauty movement, which prioritizes vegan certification, sustainable ingredient sourcing, and transparency about ingredient origins, is creating strong brand-driven demand for vegan collagen ingredients from formulators seeking to remove animal-derived collagen from their product formulations without compromising efficacy claims.

Two significant opportunities are shaping the market's long-term trajectory. The commercial maturation of precision fermentation technology for recombinant human collagen production, demonstrated by Geltor's successful commercialization of fermentation-derived human collagen proteins for cosmetic applications, is opening a pathway to functionally superior vegan collagen ingredients that replicate the exact molecular structure of human collagen rather than simply stimulating endogenous collagen synthesis, addressing the functional performance gap between current plant-based booster formulations and genuine collagen replacement. The expansion of vegan collagen applications into biomedical uses including tissue engineering scaffolds, wound dressings, and drug delivery matrices represents a high-value frontier market where the regulatory acceptance and clinical validation advantages of recombinant human collagen over xenogeneic animal collagen are driving strong institutional demand from pharmaceutical and medical device companies.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 3.84 Billion |

|

Market Size in 2026 |

USD 1.04 Billion |

|

Market Size in 2025 |

USD 0.82 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 13.9% |

|

Dominating Source/Technology |

Plant-Based Collagen Boosters |

|

Fastest Growing Source/Technology |

Fermentation-Derived Collagen |

|

Dominating Product Form |

Powders |

|

Fastest Growing Product Form |

Liquid Formulations |

|

Dominating Application |

Cosmetics & Personal Care |

|

Fastest Growing Application |

Nutraceuticals & Dietary Supplements |

|

Dominating End User |

Cosmetics Manufacturers |

|

Fastest Growing End User |

Pharmaceutical & Biotech Companies |

|

Dominating Distribution Channel |

Online Channels |

|

Fastest Growing Distribution Channel |

Direct Sales (B2B) |

|

Dominating Functionality |

Skin Health & Anti-Aging |

|

Fastest Growing Functionality |

Joint & Bone Health |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Precision Fermentation Transforming the Commercial Vegan Collagen Landscape

The commercial emergence of precision fermentation as a production platform for recombinant human collagen proteins represents the most technically transformative trend in the vegan collagen market, enabling the production of structurally authentic human collagen sequences in microbial fermentation systems rather than the approximate collagen stimulation provided by plant-based amino acid blends. Geltor has demonstrated the commercial viability of fermentation-derived collagen at cosmetic ingredient scale, receiving industry recognition and securing major cosmetic brand partnerships for its HumaColl21 human collagen and N-Collage fermentation collagen products that offer vegan certification alongside the structural authenticity of actual collagen protein rather than collagen precursor supplementation. Modern Meadow, CollPlant Biotechnologies, and Jellatech are advancing parallel fermentation-derived collagen programs targeting cosmetic, nutraceutical, and biomedical applications.

The precision fermentation approach creates vegan collagen ingredients with a fundamentally superior functional proposition relative to plant-based booster blends, as recombinant collagen proteins can be applied topically or ingested as structured collagen peptides that interact directly with skin fibroblasts and connective tissue rather than relying on endogenous biosynthesis stimulation from amino acid precursors. The production cost of fermentation-derived collagen has been declining as fermentation strain optimization, bioprocess scaling, and downstream purification efficiency improvements advance, and the trajectory toward cost-competitive fermentation collagen production at ingredient scale is a defining commercial development that will progressively expand the accessible market for precision fermentation vegan collagen products.

Beauty-from-Within and Ingestible Beauty Driving Nutraceutical Vegan Collagen Growth

The rapidly growing beauty-from-within and ingestible beauty market category, which applies nutritional supplement approaches to skin, hair, and nail health, is creating strong and fast-growing demand for vegan collagen supplement products in powder, capsule, liquid shot, and functional beverage formats targeted at health-conscious and vegan consumers seeking collagen supplementation benefits without animal-derived ingredients. The global collagen supplement market is one of the largest and fastest-growing nutraceutical categories globally, and the progressive shift of supplement-consuming consumers toward vegan and plant-based dietary frameworks is creating a natural demand pull for vegan collagen supplement alternatives to the bovine and marine collagen hydrolysate products that currently dominate the category.

Consumer brands including Vital Proteins' vegan collagen booster line, Ancient Nutrition's Plant Collagen, Garden of Life's myKind Organics Collagen Builder, and numerous direct-to-consumer vegan supplement brands have developed commercially successful vegan collagen supplement products that are building the consumer awareness and category legitimacy required for mainstream retail distribution. The clinical research base supporting plant-based collagen booster efficacy through vitamin C, silica, and amino acid supplementation for endogenous collagen synthesis enhancement is growing progressively, providing the evidence-based marketing claims required for premium product positioning in the increasingly scientifically literate nutritional supplement consumer audience.

Clean Beauty and Ethical Consumerism Accelerating Cosmetic Vegan Collagen Adoption

The clean beauty movement's progressive mainstreaming from niche natural and organic beauty channels into mass-market retail is creating structural and sustained demand for vegan collagen cosmetic ingredients across skincare formulation categories spanning serums, moisturizers, eye creams, sheet masks, and anti-aging treatment products. Major prestige and mass-market cosmetic brands including L'Oreal, Shiseido, Unilever, and Procter & Gamble are accelerating their investments in vegan ingredient alternatives to meet the vegan and cruelty-free certification requirements that growing proportions of their consumer base are applying to purchasing decisions. The Vegan Society and PETA's cruelty-free certification programs, whose certified product databases have grown to encompass tens of thousands of products from hundreds of brands, are establishing vegan collagen ingredient adoption as a mainstream cosmetic industry practice rather than a niche specialty.

Asia-Pacific markets, particularly South Korea, Japan, and China, are important and growing drivers of cosmetic vegan collagen demand as the region's large and highly engaged premium skincare consumer base combines strong interest in collagen-based anti-aging cosmetics with growing awareness of animal welfare and sustainability considerations in ingredient sourcing. South Korea's beauty industry, as the global leader in skincare innovation and the K-beauty export ecosystem, is developing vegan collagen formulation capabilities at an accelerating pace as its cosmetic export market faces increasing European and North American retailer requirements for vegan certification.

Rising Demand for Plant-Based and Sustainable Ingredients

The primary driver of the global vegan collagen market is the structural shift in consumer product purchasing preferences toward plant-based, sustainably sourced, and ethically produced ingredients across cosmetics, dietary supplements, and functional food categories that is progressively displacing conventional animal-derived collagen ingredients from formulations targeting health-conscious and ethically motivated consumer segments. The global vegan product market has grown from a niche alternative food and lifestyle category to a mainstream consumer preference dimension that influences purchasing decisions across beauty, nutrition, and functional food categories for a consumer population estimated at hundreds of millions globally. Conventional collagen derived from bovine hides, porcine skin, and marine sources carries inherent ethical and sustainability objections for vegan and flexitarian consumers that are creating product reformulation pressure on brands seeking to address this consumer segment, driving demand for the vegan collagen ingredients that enable cruelty-free collagen benefit claims on reformulated products. The documented environmental impact of animal agriculture on greenhouse gas emissions, land use, and water consumption is further reinforcing the sustainability positioning of vegan collagen as a lower-impact alternative to conventional animal-derived collagen.

Increasing Adoption in Cosmetics and Personal Care

The cosmetics and personal care industry's rapid adoption of vegan collagen ingredients across prestige, mass-market, and direct-to-consumer brand formulations is the largest and most commercially developed demand channel for vegan collagen ingredients, as the industry's established collagen skin benefit claims, well-developed consumer understanding of collagen's role in skin firmness and anti-aging, and the large and premium-priced anti-aging skincare segment collectively create a natural commercial context for premium vegan collagen ingredient products. The EU's expanding regulatory pressure on animal testing in cosmetics and the progressive adoption of vegan certification by major European and Asian beauty retailers as a shelf listing requirement for new products are creating compliance-driven adoption incentives that extend vegan collagen adoption beyond voluntary sustainability commitments into commercially mandatory positioning. Brand investments in vegan collagen product lines from L'Oreal, Shiseido, Croda International, and Symrise are demonstrating the category's commercial viability at scale and establishing the ingredient supply chain relationships required for broad formulator adoption.

Advancements in Precision Fermentation Technologies

The rapid advancement of precision fermentation technology platforms for recombinant collagen protein production represents the highest-value commercial development opportunity in the vegan collagen market, as successful commercialization at competitive production costs will enable the first functionally equivalent vegan collagen ingredients that replicate the molecular structure of natural collagen rather than simply stimulating its biosynthesis. Geltor's demonstrated commercial production of fermentation-derived human and designer collagen proteins for cosmetic applications establishes the technical proof of concept, and the progressive improvement of fermentation strain productivity, bioprocess efficiency, and downstream purification economics that is being driven by the broader industrial biotechnology sector's investment in fermentation scale-up is progressively improving the economics of precision fermentation collagen production. Equipment and process improvements at precision fermentation collagen producers through 2026 to 2036 are projected to reduce production costs to levels that enable competitive positioning against premium marine collagen ingredients, opening the large premium supplement and cosmetic ingredient market segments to fermentation-derived vegan collagen products.

Expansion in Anti-Aging and Beauty-from-Within Products

The global anti-aging skincare and beauty supplement market, representing one of the largest and fastest-growing consumer product categories globally at over USD 60 billion annually, provides an enormous addressable market opportunity for vegan collagen products that can credibly communicate anti-aging and skin health benefit claims to the large and premium-spending consumer audience prioritizing skin appearance as a quality of life and wellness objective. The beauty-from-within segment specifically, which combines the nutricosmetics and ingestible beauty product categories, is projected to grow rapidly through the forecast period as consumer understanding of the relationship between nutritional supplementation and skin quality deepens and as the product format landscape for beauty supplements expands from traditional capsule and powder formats into functional beverages, gummies, and beauty-focused functional food products that command mainstream retail distribution and broader consumer reach. Vegan collagen supplement products that can demonstrate efficacy evidence through clinical or consumer perception studies are positioned to command significant retail price premiums over conventional collagen supplements while accessing the larger and faster-growing vegan supplement consumer segment.

By Source/Technology: In 2026, Plant-Based Collagen Boosters to Dominate

Based on source/technology, the global vegan collagen market is segmented into fermentation-derived collagen, plant-based collagen boosters, synthetic/biomimetic collagen, and other technologies. In 2026, the plant-based collagen boosters segment is expected to account for the largest share of the global vegan collagen market. The large share of this segment is attributed to plant-based collagen booster formulations combining vitamin C, glycine, proline, lysine, silica, and other collagen-supportive nutrients representing the most commercially established, most widely distributed, and most affordable category of vegan collagen products currently available, with broad retail presence across supplement, natural beauty, and functional food channels globally. The accessibility and cost-effectiveness of plant-based collagen booster formulations relative to fermentation-derived recombinant collagen, combined with the established consumer familiarity with vitamin C and amino acid supplementation for collagen synthesis support, have made this the entry-point segment for most brands entering the vegan collagen market.

However, the fermentation-derived collagen segment is poised to register the highest CAGR during the forecast period. The high growth of this segment is attributed to the commercial momentum of precision fermentation vegan collagen companies including Geltor and Modern Meadow securing major cosmetic brand partnerships, the progressive improvement in fermentation collagen production economics creating competitive pricing trajectories, and the superior functional differentiation of recombinant collagen proteins relative to collagen booster blends that positions fermentation-derived products as the premium tier of the vegan collagen market capable of commanding the highest per-unit value.

By Product Form: In 2026, Powders to Hold the Largest Share

Based on product form, the global vegan collagen market is segmented into powders, capsules and tablets, liquid formulations, and topical formulations including creams and serums. In 2026, the powders segment is expected to account for the largest share of the global vegan collagen market. The dominance of powders reflects the format's versatility across supplement, functional food, and ingredient supply applications, its cost-efficiency in production and packaging relative to liquid and topical formats, and the established consumer adoption of collagen powder supplements that has driven the development of smoothie-compatible, flavorless, and flavored vegan collagen powder products by a large number of direct-to-consumer and retail supplement brands. The B2B ingredient supply application of vegan collagen powders to food, beverage, and supplement formulators represents a large and volume-efficient demand channel that reinforces the segment's market size dominance.

However, the liquid formulations segment is projected to register the highest CAGR during the forecast period. This growth is driven by the rapidly growing consumer preference for convenience-oriented beauty supplement formats including single-serve liquid shots, ready-to-drink collagen beauty beverages, and liquid collagen drops that deliver premium supplement experiences with high perceived bioavailability that commands higher retail price points than equivalent powder or capsule formats.

By Application: In 2026, Cosmetics & Personal Care to Hold the Largest Share

Based on application, the global vegan collagen market is segmented into cosmetics and personal care (skincare and haircare), nutraceuticals and dietary supplements, functional food and beverages, and biomedical applications (tissue engineering and wound care). In 2026, the cosmetics and personal care segment is expected to account for the largest share of the global vegan collagen market. This dominance reflects cosmetics' position as the most established and highest-value application channel for vegan collagen ingredients, driven by the large global anti-aging skincare market's well-developed collagen benefit communication framework, the premium pricing achievable for vegan-certified collagen skincare formulations, and the broad formulator adoption of vegan collagen ingredient options by prestige and mass-market cosmetic brands as a clean beauty ingredient substitution for animal-derived collagen.

However, the nutraceuticals and dietary supplements segment is projected to register the highest CAGR during the forecast period. This growth is driven by the rapid mainstream adoption of vegan dietary supplement lifestyles across the key supplement-consuming demographics in North America, Europe, and Asia-Pacific, the explosive growth of the beauty-from-within supplement category creating a large new consumer market for ingestible vegan collagen products, and the improving product quality and efficacy communication of vegan collagen supplement brands that is converting conventional collagen supplement users.

By End User: In 2026, Cosmetics Manufacturers to Hold the Largest Share

Based on end user, the global vegan collagen market is segmented into cosmetics manufacturers, food and beverage companies, pharmaceutical and biotech companies, and contract manufacturers. In 2026, the cosmetics manufacturers segment is expected to account for the largest share of the global vegan collagen market. Cosmetic companies represent the primary and most commercially mature end-user segment for vegan collagen ingredients, with vegan collagen ingredient procurement driven by the clean beauty reformulation programs of prestige brands including L'Oreal, Shiseido, and Unilever alongside the proliferating direct-to-consumer vegan beauty brands that have specifically built their brand identities around vegan collagen formulations. The high per-unit value of premium skincare products containing vegan collagen ingredients generates strong purchasing motivation that supports premium ingredient pricing, making cosmetics manufacturers the highest-value customer segment for vegan collagen ingredient suppliers.

However, the pharmaceutical and biotech companies segment is projected to register the highest CAGR during the forecast period. This growth is driven by the growing pharmaceutical industry interest in recombinant human collagen proteins for drug delivery matrices, tissue engineering scaffolds, wound healing products, and regenerative medicine applications where the regulatory and safety profile advantages of human-sequence recombinant collagen over xenogeneic animal collagen are compelling, and by the biomedical research community's rapidly expanding use of fermentation-derived collagen proteins as defined and reproducible research tools replacing variable animal-derived collagen preparations.

By Distribution Channel: In 2026, Online Channels to Hold the Largest Share

Based on distribution channel, the global vegan collagen market is segmented into direct sales (B2B), retail stores, and online channels. In 2026, the online channels segment is expected to account for the largest share of the global vegan collagen market. The dominance of online channels reflects both the strong direct-to-consumer e-commerce business model adopted by most vegan collagen consumer brand companies, which leverage digital marketing, social media health and beauty communities, and subscription commerce to build consumer bases without the slotting fee and minimum volume requirements of conventional retail, and the large B2B ingredient e-commerce platforms that increasingly facilitate vegan collagen ingredient procurement by smaller cosmetic, supplement, and food formulators who lack direct supplier relationship infrastructure. Amazon, Thrive Market, iHerb, and brand-direct websites collectively represent the largest retail revenue channels for vegan collagen consumer products.

However, the direct sales (B2B) segment is projected to register the highest CAGR during the forecast period. This growth is driven by the expanding commercial-scale ingredient procurement programs of major cosmetic and supplement companies establishing direct supply agreements with vegan collagen ingredient producers as they scale vegan reformulation programs across their product portfolios, creating large-volume B2B ingredient purchase relationships that represent the highest-value and most strategically important revenue streams for vegan collagen ingredient manufacturers.

Vegan Collagen Market by Region: North America Leading by Share, Asia-Pacific by Growth

Based on geography, the global vegan collagen market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

In 2026, North America is expected to account for the largest share of the global vegan collagen market. The largest share of this region is mainly due to the concentration of leading precision fermentation and synthetic biology vegan collagen technology companies including Geltor, Modern Meadow, Jellatech, and Amyris in the United States, the large and highly developed vegan supplement and clean beauty consumer markets in the U.S. and Canada that represent the largest addressable consumer demand bases for vegan collagen products globally, and the advanced early-adoption culture of the North American natural products and wellness retail channels that has established vegan collagen as a mainstream supplement category ahead of other regional markets. The U.S. natural and specialty food and supplement retail ecosystem anchored by Whole Foods Market, Sprouts, and iHerb, combined with the very large direct-to-consumer digital supplement market, provides the distribution infrastructure through which vegan collagen brands including Vital Proteins, Garden of Life, and numerous emerging brands have built commercially meaningful businesses. The biotechnology investment ecosystem of Silicon Valley and the Boston-Cambridge biotech cluster is providing the venture capital and strategic partnership infrastructure supporting the leading fermentation-derived vegan collagen companies whose commercial development represents the market's highest-value near-term growth trajectory.

However, the Asia-Pacific vegan collagen market is expected to grow at the fastest CAGR during the forecast period. The region's rapid growth is driven by the extraordinary scale and innovation intensity of the South Korean K-beauty industry's adoption of vegan collagen formulations for its global export product lines, the very large and rapidly growing premium skincare consumer market in China where both ethical consumption awareness and anti-aging skincare spending are rising simultaneously among urban middle-class consumers, Japan's well-established and scientifically sophisticated beauty and nutraceutical supplement culture that is progressively adopting vegan alternatives to its traditional marine collagen supplement category, and the rapidly developing vegan lifestyle consumer segments in Australia, Singapore, and India that are generating growing demand for vegan-certified personal care and supplement products incorporating plant-based or fermentation-derived collagen alternatives.

Europe represents an important and growing vegan collagen market with a strong policy and regulatory foundation for market development, anchored by the EU's comprehensive vegan and cruelty-free cosmetic ingredient regulatory framework, the EFSA's novel food assessment process for fermentation-derived collagen proteins, and the strong vegan consumer culture of the U.K., Germany, Netherlands, and Sweden that generates high per-capita demand for vegan-certified beauty and supplement products. European ingredient companies including Evonik, DSM-Firmenich, Symrise, Croda International, and BASF are developing vegan collagen ingredient portfolios for the European cosmetic and supplement formulation market, creating a European supply chain that reduces import dependence and enables EFSA-compliant novel ingredient development.

The global vegan collagen market is characterized by a highly dynamic competitive landscape spanning dedicated precision fermentation biotechnology companies developing recombinant collagen proteins, established specialty ingredient companies developing plant-based collagen booster formulations, and major consumer goods companies investing in vegan collagen formulation capabilities for their cosmetic and supplement brand portfolios. Competition is focused on technical ingredient differentiation, clinical or consumer evidence supporting efficacy claims, vegan and clean label certification credentials, production scalability, and the brand partnership relationships that drive commercial ingredient adoption.

The report provides a comprehensive competitive analysis based on an extensive assessment of leading players' product portfolios, technology platforms, geographic presence, and key strategic developments. Some of the key players operating in the global vegan collagen market include Geltor Inc. (U.S.), Evonik Industries AG (Germany), DSM-Firmenich (Switzerland/Netherlands), Amyris Inc. (U.S.), Modern Meadow Inc. (U.S.), Jellatech Inc. (U.S.), CollPlant Biotechnologies Ltd. (Israel), GELITA AG (Germany), Symrise AG (Germany), Croda International Plc (U.K.), BASF SE (Germany), L'Oreal S.A. (France), Shiseido Company Limited (Japan), Unilever PLC (U.K./Netherlands), and Procter & Gamble Company (U.S.), among others.

The global vegan collagen market is expected to reach USD 3.84 billion by 2036 from an estimated USD 1.04 billion in 2026, at a CAGR of 13.9% during the forecast period 2026-2036.

In 2026, the plant-based collagen boosters segment is expected to hold the largest share of the global vegan collagen market, reflecting this segment's established commercial presence, broad retail distribution, and cost-accessible formulation positioning relative to fermentation-derived alternatives.

The fermentation-derived collagen segment is expected to register the highest CAGR during the forecast period 2026-2036, driven by the commercial advancement of precision fermentation vegan collagen companies, improving production economics, and the superior functional differentiation of recombinant collagen proteins that enables premium positioning and cosmetic brand partnership development.

In 2026, the cosmetics and personal care segment is expected to hold the largest share of the global vegan collagen market, driven by the well-established collagen ingredient market in premium anti-aging skincare and the accelerating vegan reformulation programs of major cosmetic brands.

The nutraceuticals and dietary supplements segment is projected to register the highest CAGR during the forecast period, driven by the rapid mainstream adoption of vegan dietary supplement lifestyles and the explosive growth of the beauty-from-within supplement category creating large new consumer demand for ingestible vegan collagen products.

The growth of this market is primarily driven by the structural shift in consumer product purchasing toward plant-based, sustainably sourced, and cruelty-free ingredients across cosmetics and supplement categories compelling brands to adopt vegan collagen ingredient alternatives, and the commercial advancement of precision fermentation technology enabling the production of structurally authentic recombinant human collagen proteins that address the functional performance limitations of conventional plant-based collagen booster formulations.

Key players are Geltor Inc. (U.S.), Evonik Industries AG (Germany), DSM-Firmenich (Switzerland/Netherlands), Amyris Inc. (U.S.), Modern Meadow Inc. (U.S.), Jellatech Inc. (U.S.), CollPlant Biotechnologies Ltd. (Israel), GELITA AG (Germany), Symrise AG (Germany), Croda International Plc (U.K.), BASF SE (Germany), L'Oreal S.A. (France), Shiseido Company Limited (Japan), Unilever PLC (U.K./Netherlands), and Procter & Gamble Company (U.S.), among others.

Asia-Pacific is expected to register the highest growth rate in the global vegan collagen market during the forecast period 2026-2036, driven by the South Korean K-beauty industry's rapid vegan collagen formulation adoption, China's growing premium skincare and ethical consumption markets, and Japan's large and scientifically sophisticated beauty supplement culture transitioning toward vegan alternatives.

1. Introduction

1.1 Market Definition

1.2 Market Ecosystem

1.3 Currency and Limitations

1.3.1 Currency

1.3.2 Limitations

1.4 Key Stakeholders

2. Research Methodology

2.1 Research Approach

2.2 Data Collection & Validation Process

2.2.1 Secondary Research

2.2.2 Primary Research & Validation

2.2.2.1 Primary Interviews with Experts

2.2.2.2 Approaches for Country-/Region-Level Analysis

2.3 Market Estimation

2.3.1 Bottom-Up Approach

2.3.2 Top-Down Approach

2.3.3 Growth Forecast

2.4 Data Triangulation

2.5 Assumptions for the Study

3. Executive Summary

4. Market Overview

4.1 Introduction

4.2 Market Dynamics

4.2.1 Drivers

4.2.1.1 Rising Demand for Plant-Based and Sustainable Ingredients

4.2.1.2 Increasing Adoption in Cosmetics and Personal Care

4.2.1.3 Growth of Nutraceutical and Functional Food Markets

4.2.1.4 Ethical and Environmental Concerns with Animal-Derived Collagen

4.2.2 Restraints

4.2.2.1 High Production Cost Compared to Animal Collagen

4.2.2.2 Limited Consumer Awareness

4.2.2.3 Functional Performance Limitations

4.2.3 Opportunities

4.2.3.1 Advancements in Precision Fermentation Technologies

4.2.3.2 Expansion in Anti-Aging and Beauty-from-Within Products

4.2.3.3 Growth in Clean Label and Vegan Product Trends

4.2.3.4 Increasing Use in Biomedical Applications

4.2.4 Challenges

4.2.4.1 Scalability of Production

4.2.4.2 Regulatory Approval for Novel Ingredients

4.3 Technology Landscape

4.3.1 Precision Fermentation (Recombinant Collagen Production)

4.3.2 Plant-Based Collagen Boosters (Amino Acid Blends)

4.3.3 Synthetic Biology Approaches

4.3.4 Tissue Engineering and Biomaterial Applications

4.4 Vegan Collagen Production Pathways

4.4.1 Fermentation-Derived Collagen Proteins

4.4.2 Plant-Based Collagen Precursors

4.4.3 Biomimetic Collagen Peptides

4.5 Value Chain Analysis

4.5.1 Raw Material Suppliers (Sugars, Amino Acids, Microbial Strains)

4.5.2 Biotechnology and Ingredient Manufacturers

4.5.3 Formulators and Brand Owners

4.5.4 Distribution Channels

4.5.5 End Consumers

4.6 Regulatory and Standards Landscape

4.6.1 Food and Nutraceutical Regulations (FDA, EFSA)

4.6.2 Cosmetic Ingredient Regulations

4.6.3 Novel Food and Biotechnology Approvals

4.7 Porter's Five Forces Analysis

4.8 Investment and Industry Trends

4.8.1 Venture Funding in Synthetic Biology

4.8.2 Strategic Partnerships with FMCG and Cosmetic Brands

4.8.3 Expansion of Vegan and Clean Beauty Markets

4.9 Cost and Pricing Analysis

4.9.1 Production Cost Comparison (Vegan vs Animal Collagen)

4.9.2 Pricing by Product Type

4.9.3 Premium Positioning in End Markets

5. Vegan Collagen Market, by Source/Technology (Primary Segmentation)

5.1 Introduction

5.2 Fermentation-Derived Collagen

5.2.1 Recombinant Collagen Proteins

5.2.2 Engineered Microbial Production

5.3 Plant-Based Collagen Boosters

5.3.1 Amino Acid Blends

5.3.2 Vitamin-Enriched Formulations

5.4 Synthetic/Biomimetic Collagen

5.5 Other Technologies

6. Vegan Collagen Market, by Product Form

6.1 Introduction

6.2 Powders

6.3 Capsules & Tablets

6.4 Liquid Formulations

6.5 Topical Formulations (Creams, Serums)

7. Vegan Collagen Market, by Application

7.1 Introduction

7.2 Cosmetics & Personal Care

7.2.1 Skincare

7.2.2 Haircare

7.3 Nutraceuticals & Dietary Supplements

7.4 Functional Food & Beverages

7.5 Biomedical Applications

7.5.1 Tissue Engineering

7.5.2 Wound Care

8. Vegan Collagen Market, by End User (B2B)

8.1 Introduction

8.2 Cosmetics Manufacturers

8.3 Food & Beverage Companies

8.4 Pharmaceutical & Biotech Companies

8.5 Contract Manufacturers

9. Vegan Collagen Market, by Distribution Channel

9.1 Introduction

9.2 Direct Sales (B2B)

9.3 Retail Stores

9.4 Online Channels

10. Vegan Collagen Market, by Functionality

10.1 Introduction

10.2 Skin Health & Anti-Aging

10.3 Joint & Bone Health

10.4 Hair & Nail Health

10.5 General Wellness

11. Vegan Collagen Market, by Geography

11.1 Introduction

11.2 North America

11.2.1 U.S.

11.2.2 Canada

11.3 Europe

11.3.1 Germany

11.3.2 U.K.

11.3.3 France

11.3.4 Italy

11.3.5 Spain

11.3.6 Netherlands

11.3.7 Sweden

11.3.8 Switzerland

11.3.9 Rest of Europe

11.4 Asia-Pacific

11.4.1 China

11.4.2 Japan

11.4.3 India

11.4.4 South Korea

11.4.5 Australia

11.4.6 Thailand

11.4.7 Indonesia

11.4.8 Vietnam

11.4.9 Malaysia

11.4.10 Singapore

11.4.11 Rest of Asia-Pacific

11.5 Latin America

11.5.1 Brazil

11.5.2 Mexico

11.5.3 Argentina

11.5.4 Chile

11.5.5 Colombia

11.5.6 Rest of Latin America

11.6 Middle East & Africa

11.6.1 UAE

11.6.2 Saudi Arabia

11.6.3 South Africa

11.6.4 Turkey

11.6.5 Israel

11.6.6 Rest of Middle East & Africa

12. Competitive Landscape

12.1 Overview

12.2 Key Growth Strategies

12.3 Competitive Benchmarking

12.4 Competitive Dashboard

12.4.1 Industry Leaders

12.4.2 Market Differentiators

12.4.3 Vanguards

12.4.4 Emerging Companies

12.5 Market Ranking/Positioning Analysis of Key Players, 2025

13. Company Profiles

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

13.1 Geltor, Inc.

13.2 Evonik Industries AG

13.3 DSM-Firmenich

13.4 Amyris, Inc.

13.5 Modern Meadow, Inc.

13.6 Jellatech, Inc.

13.7 CollPlant Biotechnologies Ltd.

13.8 GELITA AG (Plant-based initiatives)

13.9 Symrise AG

13.10 Croda International Plc

13.11 BASF SE

13.12 L'Oreal S.A. (Biotech collaborations)

13.13 Shiseido Company, Limited

13.14 Unilever PLC

13.15 Procter & Gamble Company

14. Appendix

14.1 Additional Customization

14.2 Related Reports

Published Date: Feb-2025

Published Date: Oct-2024

Published Date: Aug-2024

Published Date: Jul-2024

Published Date: Jun-2024

Subscribe to get the latest industry updates