Resources

About Us

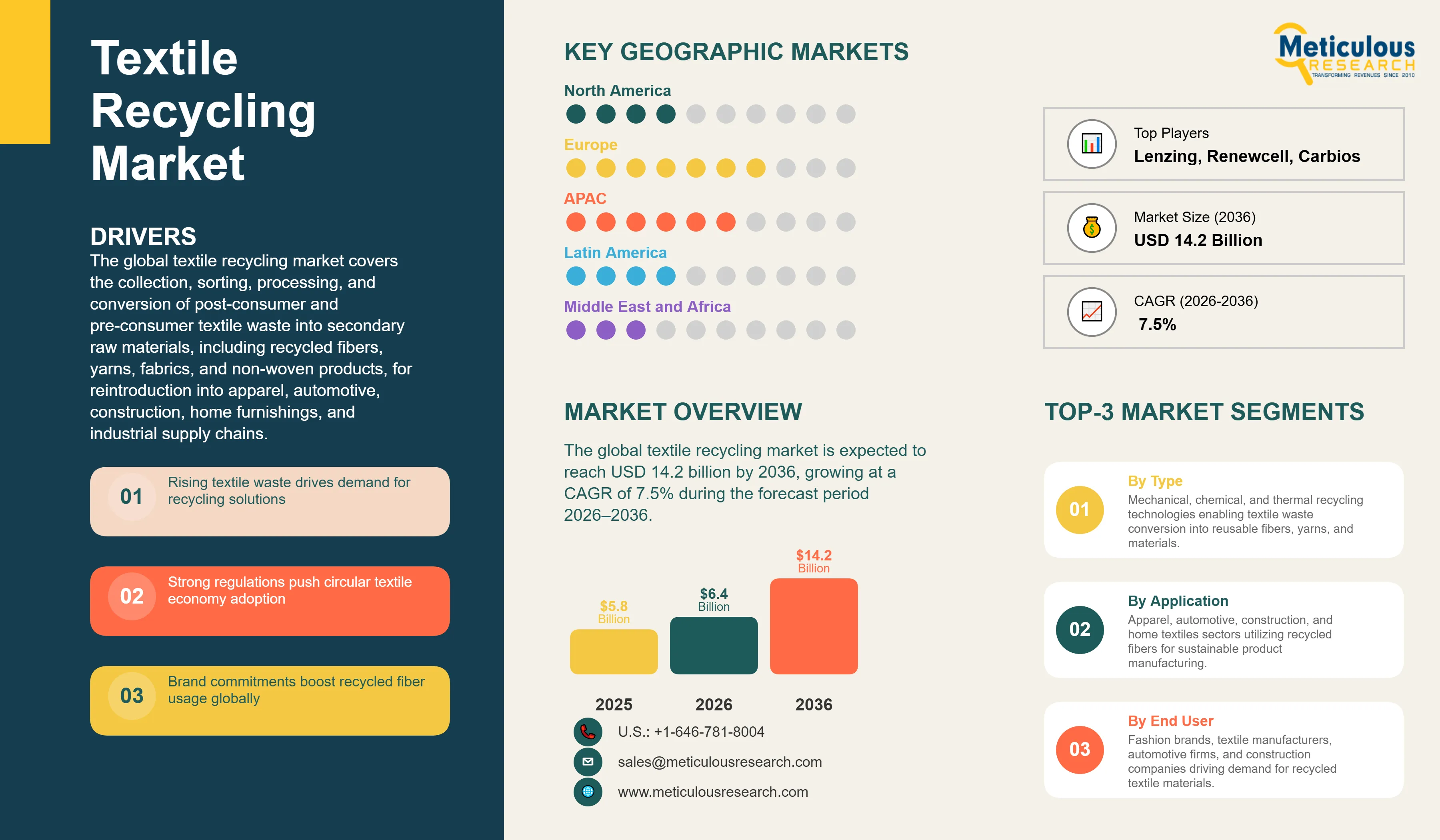

The global textile recycling market was valued at USD 5.8 billion in 2025. This market is expected to reach USD 14.2 billion by 2036 from an estimated USD 6.4 billion in 2026, growing at a CAGR of 7.5% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

The global textile recycling market covers the collection, sorting, processing, and conversion of post-consumer and pre-consumer textile waste into secondary raw materials, including recycled fibers, yarns, fabrics, and non-woven products, for reintroduction into apparel, automotive, construction, home furnishings, and industrial supply chains. The market encompasses the full spectrum of recycling technologies, including mechanical shredding and re-spinning, chemical depolymerization and dissolution, thermal energy recovery, and emerging enzymatic bio-based pathways, as well as the supporting infrastructure of waste collection networks, automated sorting facilities, and fiber regeneration and re-spinning capacity that collectively constitute the textile recycling value chain.

The growth of the global textile recycling market is primarily driven by the accelerating legislative pressure on fashion brands and textile manufacturers to incorporate recycled fiber content into their products and to finance end-of-life collection and recycling infrastructure through extended producer responsibility programs. The European Union’s revised Waste Framework Directive mandating separate collection of textile waste across all member states by January 2025, the French AGEC law requiring minimum recycled content in certain textile product categories, and the escalating corporate commitments of major apparel brands including H&M, Zara parent Inditex, Nike, and Adidas to achieve specific recycled fiber content targets by 2030 are collectively creating mandated demand that is stimulating investment in recycling technology development and infrastructure capacity expansion at unprecedented scale.

However, the market faces meaningful structural constraints. The complex blended fiber composition of the majority of post-consumer garments, which typically combine cotton, polyester, elastane, and multiple synthetic components in proportions that vary continuously across product lines and vintages, presents a fundamental technical challenge for both mechanical and chemical recycling processes that are most efficient when processing homogeneous single-fiber streams. The collection and sorting infrastructure required to aggregate, transport, grade, and prepare post-consumer textile waste for commercial recycling processes represents a significant cost burden that currently makes post-consumer textile recycling economically unviable in most geographies without policy support or brand subsidy.

Despite these challenges, the market outlook is strongly positive. The rapid advancement of chemical recycling technologies, particularly the dissolution-based cellulosic fiber recycling platforms developed by Renewcell, Infinited Fiber Company, and Circulose, and the depolymerization technologies for polyester recycling advanced by Eastman Chemical’s molecular recycling program and Carbios’ enzymatic PET depolymerization, is progressively extending the range of textile waste streams that can be recycled into near-virgin quality fiber feedstocks. The scaling of automated near-infrared sorting systems by Valvan Baling Systems, PICVISA, and Tomra is resolving the input quality bottleneck that has historically limited chemical recycling process efficiency.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 14.2 Billion |

|

Market Size in 2026 |

USD 6.4 Billion |

|

Market Size in 2025 |

USD 5.8 Billion |

|

Revenue Growth Rate (2026–2036) |

CAGR of 7.5% |

|

Dominating Recycling Process |

Mechanical Recycling |

|

Fastest Growing Recycling Process |

Chemical Recycling |

|

Dominating Material Type |

Polyester |

|

Fastest Growing Material Type |

Blended Fabrics |

|

Dominating Source |

Post-Consumer Textile Waste |

|

Fastest Growing Source |

Pre-Consumer (Manufacturing) Waste |

|

Dominating End Product |

Fibers and Yarns |

|

Fastest Growing End Product |

Non-Woven Textiles |

|

Dominating End-Use Industry |

Apparel & Fashion |

|

Fastest Growing End-Use Industry |

Automotive |

|

Dominating Fiber-to-Fiber Type |

Open-Loop Recycling |

|

Fastest Growing Fiber-to-Fiber Type |

Closed-Loop Recycling |

|

Dominating Geography |

Europe |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Shift Toward Closed-Loop Textile Recycling

The progressive transition of the textile recycling industry from open-loop recovery toward closed-loop fiber-to-fiber recycling that returns recovered material to garment-quality fiber feedstock is the defining structural trend reshaping the competitive and commercial dynamics of the market. Closed-loop recycling preserves the maximum economic and environmental value of textile waste by producing fiber outputs that can directly substitute for virgin cotton, polyester, or viscose in apparel manufacturing, enabling circular supply chain models that are the stated ambition of major fast fashion and sportswear brands. Renewcell’s Circulose dissolving pulp technology, which converts cotton-rich post-consumer denim and textile waste into a certified recycled cellulosic dissolving pulp that Lenzing and other viscose producers use as a direct substitute for virgin wood pulp, represents the commercial model for closed-loop textile recycling at industrial scale.

The H&M Group’s strategic investment in Renewcell and its commitment to source Circulose for Conscious Collection garment lines, Inditex’s partnership with Infinited Fiber Company for cellulosic staple fiber supply, and the Adidas and Stella McCartney commitments to Evrnu’s NuCycl regenerated cellulose fiber collectively represent the brand-level demand pull that is enabling closed-loop recycling technology companies to justify the capital investment required to scale from pilot to commercial production. The growing availability of Global Recycled Standard and Recycled Claim Standard certification for closed-loop recycled fiber products is enabling brands to make credible and verifiable recycled content claims that support premium pricing and meet regulatory minimum content requirements.

Increasing Investment in Chemical Recycling Startups

The surge of venture capital, corporate strategic investment, and public funding into chemical textile recycling technology companies represents a defining commercial development that is advancing the technology readiness level and reducing the capital cost of next-generation fiber-to-fiber recycling platforms at a pace that is compressing development timelines from the decade-scale of previous industrial process innovations. Chemical recycling addresses the fundamental limitation of mechanical recycling by breaking down textile polymers to their molecular building blocks and reconstituting near-virgin quality fiber. Carbios raised EUR 114 million in 2021 for the industrial demonstration of its enzymatic PET depolymerization technology, securing licensing agreements with Salomon, On, Patagonia, and PVH as sustainability-committed offtake partners. Worn Again Technologies secured GBP 20 million from H&M Group and Sulzer for its solvent-based polyester and cellulose separation and recovery technology. Circ, formerly Tyton BioSciences, completed a Series B financing round backed by PVH Corp to advance its hydrothermal process for separating and recycling polyester-cotton blend garments.

The concentration of chemical recycling investment in cellulosic and polyester pathways reflects the dominance of cotton and polyester as the two largest fiber categories in the global textile waste stream, and the high commercial value of near-virgin cellulosic dissolving pulp and recycled PET as substitutes for virgin wood pulp and petroleum-derived terephthalic acid respectively. The projected commercial scale-up of five or more chemical recycling technology platforms from pilot to industrial demonstration scale during the 2026 to 2030 portion of the forecast period is expected to materially expand the volume of post-consumer textile waste that can be processed into near-virgin quality recycled fiber.

Adoption of AI-Based Textile Sorting Technologies

The deployment of automated textile sorting systems combining near-infrared spectroscopy, hyperspectral imaging, and machine learning classification algorithms represents a critical enabling technology trend that is resolving the input quality bottleneck limiting the commercial viability of chemical textile recycling at scale. Post-consumer textile waste arriving at sorting facilities exhibits enormous variability in fiber composition, color, contamination level, and blending complexity that makes manual sorting to the fiber purity specifications required by chemical recycling processes impractical at commercial throughput rates. Automated NIR-based sorting systems from Valvan Baling Systems and PICVISA can identify and sort textile waste by fiber type at throughput rates of up to 1,000 kilograms per hour, achieving fiber composition identification accuracy above 90% for single-fiber streams and enabling the creation of sorted fiber fractions with sufficient purity to serve as chemical recycling process inputs.

The European Union’s Sorting for Recycling project, supported by the Waste and Resources Action Programme, and the AATCC Foundation’s automated sorting research program are funding the development and validation of automated sorting technologies specifically optimized for textile waste at commercial scale. The combination of automated NIR sorting with digital product passport data, which the EU’s Ecodesign for Sustainable Products Regulation is expected to mandate for textile products sold in European markets from 2027, will enable sorting systems to access detailed fiber composition information encoded at point of manufacture, substantially improving sorting efficiency and reducing contamination in recycled fiber output streams.

Rising Textile Waste and Landfill Pressure

The escalating global volume of post-consumer textile waste is the foundational structural driver underpinning long-term demand growth in the textile recycling market. The Ellen MacArthur Foundation estimates that more than 92 million tonnes of textile waste are generated globally each year, with less than 1% currently recycled into fiber of equivalent quality, and the remainder predominantly directed to landfill or incineration. The growth of fast fashion business models—which have increased average clothing purchase frequency while reducing average garment lifespan—has accelerated the volume and velocity of post-consumer textile waste generation in major consumption markets including the United States, the European Union, and China. The progressive exhaustion of landfill capacity in densely populated European nations and the escalating gate fees for textile waste landfill disposal are creating economic pressure on municipal waste authorities and brand take-back programs to divert textile waste toward recycling processing as the lowest-cost alternative to disposal, providing a volume and cost incentive for recycling infrastructure investment.

Increasing Regulations on Circular Economy and Waste Management

The accelerating adoption of binding circular economy and extended producer responsibility legislation across the European Union, the United Kingdom, France, and several U.S. states is creating mandatory structural demand for textile recycling infrastructure by requiring brands and importers to finance end-of-life collection and recycling of the textiles they place on the market. The EU Waste Framework Directive’s mandatory separate textile waste collection requirement, effective January 2025, is obligating member states to establish collection infrastructure capable of diverting post-consumer textiles from municipal solid waste streams into dedicated recycling processing channels. France’s REFASHION extended producer responsibility scheme for textiles, covering apparel, household linens, and footwear, collected approximately 235,000 tonnes of used textiles in 2023 and is scaling collection and sorting infrastructure investment under a mandatory eco-contribution framework paid by producers. The anticipated expansion of EPR frameworks for textiles to additional EU member states, and the separate textile waste legislative proposals in Germany, the Netherlands, and Sweden, will substantially expand the geographic scope and financial scale of brand-financed textile recycling infrastructure over the forecast period.

Growth of Fiber-to-Fiber Recycling

The commercial scale-up of fiber-to-fiber recycling technologies capable of producing near-virgin quality recycled fiber outputs from post-consumer textile waste represents the highest-value opportunity in the textile recycling market and the primary destination for the substantial technology investment and brand partnership activity characterizing the market’s current development phase. Fiber-to-fiber recycling creates recycled fiber products commanding price premiums of 20 to 50% above mechanically recycled fiber outputs and approaching parity with virgin fiber pricing in certain product categories, substantially improving the economic returns of recycling operations relative to downcycling alternatives. The certification infrastructure for fiber-to-fiber recycled content—including the Global Recycled Standard, Recycled Claim Standard, and the EU Ecolabel’s textile recycled content criteria—is enabling brands to make differentiated and verifiable sustainability claims for garments incorporating fiber-to-fiber recycled content, creating commercial market access for the premium-priced outputs of advanced recycling technology platforms.

Advancements in Chemical Recycling Technologies

The accelerating advancement of chemical recycling technology across multiple molecular pathways is progressively expanding the range of textile waste compositions addressable by closed-loop recycling and improving the fiber quality achievable from chemically recycled feedstocks. Carbios’ enzymatic PET depolymerization technology, which uses an engineered thermostable PETase enzyme to convert PET textile and packaging waste to its BHET monomer building blocks for repolymerization to near-virgin PET fiber, achieved its first industrial-scale demonstration at a 50,000-tonne-per-year capacity facility in Clermont-Ferrand, France in 2025, establishing the proof of concept for enzymatic chemical textile recycling at commercial scale. Eastman Chemical’s Renew molecular recycling technology, which uses methanolysis to depolymerize polyester waste to its DMT and MEG monomer components, is operating at commercial scale in Kingsport, Tennessee and is establishing the replicable commercial technology blueprint for polyester textile chemical recycling.

By Recycling Process: In 2026, Mechanical Recycling to Dominate

Based on recycling process, the global textile recycling market is segmented into mechanical recycling, chemical recycling (encompassing depolymerization, dissolution-based recycling, and enzymatic recycling), and thermal recycling (energy recovery). In 2026, the mechanical recycling segment is expected to account for the largest share of the global textile recycling market. The large share of this segment is attributed to mechanical recycling’s status as the most established and commercially scaled textile recycling process, the extensive installed base of mechanical shredding and garnetting equipment across Europe, South Asia, and East Asia that currently processes the majority of collected textile waste, and the lower capital investment requirement of mechanical recycling relative to chemical processes that enables smaller-scale and geographically dispersed processing operations aligned with current textile waste collection infrastructure capacity. Mechanical recycling’s low processing cost per tonne—typically USD 100 to 300 per tonne depending on facility scale and input quality—provides the baseline commercial viability for textile waste processing that is supporting the functioning of current collection infrastructure economics across most markets.

However, the chemical recycling segment is poised to register the highest CAGR during the forecast period. The high growth of this segment is attributed to the technology maturation and commercial scale-up of multiple chemical recycling platforms targeting the large unaddressed market of blended fiber and complex composite textile waste that mechanical recycling cannot effectively process, the substantial venture capital and corporate investment being deployed into chemical recycling technology developers, and the brand demand for near-virgin quality fiber-to-fiber recycled content that only chemical recycling can consistently deliver from post-consumer waste feedstocks.

By Material Type: In 2026, Polyester to Hold the Largest Share

Based on material type, the global textile recycling market is segmented into cotton, polyester, nylon, wool, blended fabrics, and other fibers. In 2026, the polyester segment is expected to account for the largest share of the global textile recycling market. This dominance reflects polyester’s position as the largest single fiber type in global textile production—representing approximately 54% of total fiber output—and the commercial maturity of mechanical recycled polyester production from post-consumer PET bottle feedstocks, which has established large-scale rPET fiber manufacturing capacity and brand adoption infrastructure that is being progressively extended to textile-to-textile recycled polyester pathways. The availability of a well-developed commercial market for recycled PET fiber through Unifi’s REPREVE brand and multiple Asian rPET producers provides the revenue infrastructure for expanding polyester textile recycling volumes.

However, the blended fabrics segment is projected to register the highest CAGR during the forecast period. This growth is driven by the development of chemical recycling technologies specifically targeting blended fiber waste streams, which represent the majority of post-consumer garment waste by volume, and the consequent expansion of the commercially addressable blended textile waste stream as blend-capable recycling technology platforms approach commercial scale over the forecast period.

By Source: In 2026, Post-Consumer Textile Waste to Hold the Largest Share

Based on source, the global textile recycling market is segmented into pre-consumer textile waste (manufacturing waste) and post-consumer textile waste (encompassing apparel waste, home textiles, and industrial textiles). In 2026, the post-consumer textile waste segment is expected to account for the largest share of the global textile recycling market. This dominance reflects the substantially larger absolute volume of post-consumer textile waste generated globally relative to pre-consumer manufacturing waste, the focus of EPR policy frameworks on post-consumer waste management responsibilities, and the consumer-facing sustainability narrative that drives brand investment in post-consumer collection and recycling infrastructure.

The pre-consumer textile waste segment is projected to grow at an above-average rate during the forecast period as the near-shore proximity of large-volume pre-consumer waste streams to garment manufacturing clusters enables lower-cost collection and higher-purity fiber fraction inputs that chemical recycling technology platforms can efficiently process.

By End Product: In 2026, Fibers and Yarns to Hold the Largest Share

Based on end product, the global textile recycling market is segmented into fibers and yarns, fabrics, non-woven textiles, insulation materials, industrial applications, and others. In 2026, the fibers and yarns segment is expected to account for the largest share of the global textile recycling market. This dominance reflects the concentration of current textile recycling output in the form of recycled fiber and yarn intermediates for downstream garment, home textiles, and technical textiles manufacturing, the high commercial value of recycled fiber and yarn relative to other recycled textile product forms, and the direct alignment of fiber and yarn outputs with the supply chain requirements of apparel brands incorporating recycled content into their product lines.

However, the non-woven textiles segment is projected to register the highest CAGR during the forecast period. This growth is driven by the expanding automotive industry demand for recycled fiber non-woven materials for vehicle interior insulation, sound dampening, and trunk lining applications, the construction industry’s adoption of recycled textile non-wovens for building thermal and acoustic insulation, and the growing use of recycled textile fiber in geotextile applications for civil engineering and landscaping.

By End-Use Industry: In 2026, Apparel & Fashion to Hold the Largest Share

Based on end-use industry, the global textile recycling market is segmented into apparel and fashion, automotive (upholstery and insulation), construction (insulation materials), home furnishings, packaging, and others. In 2026, the apparel and fashion segment is expected to account for the largest share of the global textile recycling market. This dominance reflects the apparel industry’s role as the primary driver of commercial demand for recycled fiber through brand sustainability commitments, consumer preference for recycled content products, and the regulatory minimum content requirements beginning to emerge in European markets. The apparel and fashion industry’s scale provides a vast addressable demand pool for recycled fiber supply even at modest recycled content penetration rates.

However, the automotive segment is projected to register the highest CAGR during the forecast period. This growth is driven by the automotive industry’s progressive adoption of recycled textile fiber non-wovens and technical textiles for interior trim, trunk liner, underbody shield, and acoustic insulation applications, the regulatory pressure on automotive manufacturers to demonstrate recycled content in vehicle components under EU end-of-life vehicle regulations, and the cost competitiveness of recycled textile fiber non-wovens relative to petroleum-derived synthetic fiber alternatives in automotive interior applications.

By Fiber-to-Fiber Recycling Type: In 2026, Open-Loop to Hold the Largest Share

Based on fiber-to-fiber recycling type, the global textile recycling market is segmented into open-loop recycling and closed-loop recycling. In 2026, the open-loop recycling segment is expected to account for the largest share of the global textile recycling market. This dominance reflects the current commercial maturity stage of the industry, in which the majority of textile waste recycling produces lower-grade fiber outputs for non-apparel end uses including industrial wipers, insulation products, and automotive interior components rather than garment-quality fiber for direct reintroduction into apparel supply chains. Open-loop recycling’s lower processing cost and lower input quality requirements accommodate the heterogeneous post-consumer textile waste streams accessible under current collection infrastructure, enabling commercial viability at the current scale of market development.

However, the closed-loop recycling segment is projected to register the highest CAGR during the forecast period. This growth is driven by the commercial scale-up of fiber-to-fiber recycling technology platforms targeting near-virgin quality fiber outputs, the brand demand for closed-loop recycled content claims supported by chain-of-custody certification, and the superior environmental credentials of closed-loop recycling relative to downcycling that are increasingly required to satisfy brand science-based targets and EU Taxonomy alignment requirements.

Textile Recycling Market by Region: Europe Leading by Share, Asia-Pacific by Growth

Based on geography, the global textile recycling market is segmented into Europe, North America, Asia-Pacific, Latin America, and the Middle East and Africa.

In 2026, Europe is expected to account for the largest share of the global textile recycling market. The largest share of this region is mainly due to Europe’s comprehensive and advanced regulatory framework for textile waste management and circular economy, the mandatory separate textile waste collection requirement under the EU Waste Framework Directive in effect from January 2025, and the established national EPR frameworks for textiles in France, Germany, the Netherlands, and Sweden that are providing structured financial flows for collection and recycling infrastructure investment. Europe’s first-mover advantage in chemical textile recycling technology development is anchored by the commercial operations of Renewcell in Sweden, Infinited Fiber Company in Finland, and the industrial demonstration of Carbios’ enzymatic recycling technology in France, which collectively represent the world’s most advanced commercial fiber-to-fiber recycling capability cluster. The U.K.’s WRAP Textiles 2030 initiative, Germany’s Biotexfuture program funding bio-based textile recycling research, and the Netherlands’ Fashion for Good innovation accelerator represent additional policy and institutional enablers of the European textile recycling ecosystem’s leadership position.

However, the Asia-Pacific textile recycling market is expected to grow at the fastest CAGR during the forecast period. The region’s rapid growth is driven by the concentration of global textile manufacturing in China, Bangladesh, Vietnam, and India—which collectively produce approximately 65% of global apparel output—creating vast and geographically concentrated pre-consumer manufacturing waste streams that represent the most accessible and cost-effective feedstock for textile recycling investment in the near term. China’s national circular economy policy framework, which identifies textile recycling as a priority sector for industrial policy support, is stimulating investment in recycled fiber manufacturing capacity and textile waste collection infrastructure at a scale commensurate with China’s position as the world’s largest single textile producer and consumer. South Korea’s Hyosung TNC has established global leadership in nylon fiber recycling through its regen brand of recycled nylon and polyester, while Japan’s advanced industrial ecology culture and Extended Producer Responsibility frameworks for textiles are supporting above-average textile recycling rates relative to regional peers.

North America is establishing an expanding textile recycling commercial presence concentrated in the United States, where the Inflation Reduction Act’s advanced manufacturing tax credits and the EPA’s National Recycling Strategy are providing policy support for domestic recycled fiber manufacturing investment. Unifi’s REPREVE recycled polyester fiber production from its Yadkinville, North Carolina manufacturing facility represents the most commercially established U.S. textile recycling operation, with over 35 billion PET bottles converted to recycled fiber since the program’s inception. The emerging U.S. textile EPR legislative proposals in California, New York, and Colorado, if enacted, would create the structural framework for substantially expanded post-consumer textile collection and recycling infrastructure investment over the second half of the forecast period.

The global textile recycling market is characterized by a heterogeneous competitive ecosystem spanning four distinct competitive tiers: established industrial recycling and waste management companies with large-scale collection and processing infrastructure; specialty chemical companies providing novel fiber-to-fiber recycling technology platforms; vertically integrated fiber manufacturers incorporating recycled feedstocks into their manufacturing operations; and pure-play recycling technology startups advancing proprietary chemical or biological recycling processes from pilot to commercial scale. Competition across tiers is currently less focused on traditional market share metrics and more oriented toward technology differentiation, supply chain partnership quality, sustainability certification depth, and the credibility of recycled fiber content claims that brands require to support their sustainability marketing and regulatory compliance objectives.

Renewcell AB leads the cellulosic fiber-to-fiber recycling segment with its Circulose dissolving pulp technology, operating a 120,000-tonne-per-year commercial production facility in Sundsvall, Sweden and supplying Circulose to Lenzing, Aditya Birla, and other viscose producers for incorporation into branded recycled fiber products. Infinited Fiber Company is advancing its Infinna cellulosic staple fiber technology, targeting a 30,000-tonne-per-year commercial facility with secured offtake agreements from Inditex and PVH. Carbios has achieved commercial demonstration of its enzymatic PET depolymerization technology and is licensing the process to INDORAMA Ventures, Swissaustral, and other PET fiber producers. Worn Again Technologies, Circ, Evrnu, and Ambercycle represent the leading next-generation chemical recycling startups advancing proprietary platforms across cellulosic and synthetic fiber pathways toward commercial scale. Unifi, Inc.’s REPREVE franchise represents the world’s largest branded recycled performance fiber program. Lenzing AG’s ECOVERO and REFIBRA recycled cellulosic fiber brands leverage post-consumer cotton waste as a partial feedstock input. Eastman Chemical Company’s Renew molecular recycling technology at commercial scale in Kingsport, Tennessee establishes the U.S. benchmark for polyester textile chemical recycling. Veolia Environnement and Suez SA provide industrial-scale textile waste collection, sorting, and mechanical recycling processing services across European markets.

The report provides a comprehensive competitive analysis based on an extensive assessment of leading players’ technology platforms, product portfolios, geographic presence, capacity expansion programs, and key strategic developments. Key players operating in the global textile recycling market include Lenzing AG (Austria), Renewcell AB (Sweden), Infinited Fiber Company (Finland), Worn Again Technologies (U.K.), Evrnu Inc. (U.S.), Carbios (France), Ambercycle (U.S.), Circ/Tyton BioSciences (U.S.), Unifi Inc. (U.S.), Birla Cellulose (India), Hyosung TNC (South Korea), Eastman Chemical Company (U.S.), BASF SE (Germany), Veolia Environnement (France), and Suez SA (France), among others.

The global textile recycling market is expected to reach USD 14.2 billion by 2036 from an estimated USD 6.4 billion in 2026, at a CAGR of 7.5% during the forecast period 2026–2036.

In 2026, the mechanical recycling segment is expected to hold the largest share of the global textile recycling market, driven by the technology’s commercial maturity, the extensive installed base of mechanical processing equipment globally, and the lower capital cost relative to chemical recycling that enables broad geographic deployment.

The chemical recycling segment is expected to register the highest CAGR during the forecast period 2026–2036, driven by the commercial scale-up of fiber-to-fiber recycling technology platforms targeting blended and complex textile waste streams, the substantial investment in chemical recycling startups, and the brand demand for near-virgin quality recycled fiber outputs achievable only through chemical processing.

In 2026, the polyester segment is expected to hold the largest share of the global textile recycling market, reflecting polyester’s dominance as the largest global fiber type, the commercial maturity of rPET fiber production from post-consumer PET bottle feedstocks, and the large installed base of recycled polyester fiber manufacturing capacity in Asia and North America.

The closed-loop recycling segment is expected to register the highest CAGR during the forecast period, driven by the commercial scale-up of fiber-to-fiber recycling technology platforms, the brand demand for closed-loop recycled content claims with chain-of-custody certification, and the superior environmental and regulatory credentials of closed-loop recycling relative to downcycling alternatives. This segment is particularly critical for sustainability-focused clients seeking supply chain circularity.

The growth of this market is primarily driven by rising global textile waste volumes and increasing landfill pressure, the accelerating adoption of binding EPR legislation and circular economy regulations mandating separate textile waste collection and brand financial responsibility for end-of-life management, growing consumer and brand demand for verified recycled fiber content, and the commercial scale-up of chemical recycling technologies enabling near-virgin quality fiber-to-fiber recycling from post-consumer waste feedstocks.

The automotive segment is expected to register the highest CAGR during the forecast period, driven by the automotive industry’s adoption of recycled textile fiber non-wovens for interior insulation and acoustic dampening applications, EU end-of-life vehicle recycled content regulations, and the cost competitiveness of recycled textile non-wovens relative to virgin synthetic alternatives in automotive interior manufacturing.

Key players are Lenzing AG (Austria), Renewcell AB (Sweden), Infinited Fiber Company (Finland), Worn Again Technologies (U.K.), Evrnu Inc. (U.S.), Carbios (France), Ambercycle (U.S.), Circ/Tyton BioSciences (U.S.), Unifi Inc. (U.S.), Birla Cellulose (India), Hyosung TNC (South Korea), Eastman Chemical Company (U.S.), BASF SE (Germany), Veolia Environnement (France), and Suez SA (France), among others.

Asia-Pacific is expected to register the highest growth rate in the global textile recycling market during the forecast period 2026–2036, driven by the concentration of global textile manufacturing and pre-consumer waste in China, Bangladesh, Vietnam, and India; China’s national circular economy policy support for textile recycling; South Korea’s advanced nylon and polyester fiber recycling capabilities; and the expanding regulatory pressure on textile producers across the region to address end-of-life textile waste management obligations.

1. Introduction

1.1. Market Definition

1.2. Market Ecosystem

1.3. Currency and Limitations

1.3.1. Currency

1.3.2. Limitations

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Data Collection & Validation Process

2.2.1. Secondary Research

2.2.2. Primary Research & Validation

2.3. Market Estimation

2.3.1. Bottom-Up Approach

2.3.2. Top-Down Approach

2.3.3. Growth Forecast

2.4. Data Triangulation

2.5. Assumptions for the Study

3. Executive Summary

4. Market Overview

4.1. Introduction

4.2. Market Dynamics

4.2.1. Drivers

4.2.2. Restraints

4.2.3. Opportunities

4.2.4. Challenges

4.3. Key Market Trends

4.4. Technology Landscape

4.5. Textile Recycling Process Architecture

4.6. Value Chain Analysis

4.7. Regulatory and Policy Landscape

4.8. Porter’s Five Forces Analysis

4.9. Investment and Capacity Expansion Landscape

4.10. Cost and Pricing Analysis

5. Textile Recycling Market, by Recycling Process

5.1. Introduction

5.2. Mechanical Recycling

5.3. Chemical Recycling

5.3.1. Depolymerization (Polyester, Nylon)

5.3.2. Dissolution-Based Recycling (Cellulosic Fibers)

5.3.3. Enzymatic Recycling

5.4. Thermal Recycling (Energy Recovery)

6. Textile Recycling Market, by Material Type

6.1. Introduction

6.2. Cotton

6.3. Polyester

6.4. Nylon

6.5. Wool

6.6. Blended Fabrics

6.7. Other Fibers

7. Textile Recycling Market, by Source

7.1. Introduction

7.2. Pre-Consumer Textile Waste (Manufacturing Waste)

7.3. Post-Consumer Textile Waste

7.3.1. Apparel Waste

7.3.2. Home Textiles

7.3.3. Industrial Textiles

8. Textile Recycling Market, by End Product

8.1. Introduction

8.2. Fibers and Yarns

8.3. Fabrics

8.4. Non-Woven Textiles

8.5. Insulation Materials

8.6. Industrial Applications

8.7. Others

9. Textile Recycling Market, by End-Use Industry

9.1. Introduction

9.2. Apparel & Fashion

9.3. Automotive (Upholstery, Insulation)

9.4. Construction (Insulation Materials)

9.5. Home Furnishings

9.6. Packaging

9.7. Others

10. Textile Recycling Market, by Fiber-to-Fiber Recycling Type

10.1. Introduction

10.2. Open-Loop Recycling

10.3. Closed-Loop Recycling

11. Textile Recycling Market, by Geography

11.1. Introduction

11.2. Europe

11.2.1. Germany

11.2.2. France

11.2.3. U.K.

11.2.4. Italy

11.2.5. Spain

11.2.6. Netherlands

11.2.7. Sweden

11.2.8. Rest of Europe

11.3. North America

11.3.1. U.S.

11.3.2. Canada

11.4. Asia-Pacific

11.4.1. China

11.4.2. India

11.4.3. Bangladesh

11.4.4. Vietnam

11.4.5. Japan

11.4.6. South Korea

11.4.7. Rest of Asia-Pacific

11.5. Latin America

11.5.1. Brazil

11.5.2. Mexico

11.5.3. Argentina

11.5.4. Chile

11.5.5. Rest of Latin America

11.6. Middle East & Africa

11.6.1. UAE

11.6.2. Saudi Arabia

11.6.3. South Africa

11.6.4. Turkey

11.6.5. Rest of Middle East & Africa

12. Competitive Landscape

12.1. Overview

12.2. Key Growth Strategies

12.3. Competitive Benchmarking

12.4. Competitive Dashboard

12.4.1. Industry Leaders

12.4.2. Market Differentiators

12.4.3. Vanguards

12.4.4. Emerging Companies

12.5. Market Ranking/Positioning Analysis of Key Players, 2025

13. Company Profiles

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

13.1. Lenzing AG

13.2. Renewcell AB

13.3. Infinited Fiber Company

13.4. Worn Again Technologies

13.5. Evrnu Inc.

13.6. Carbios

13.7. Ambercycle

13.8. Circ (Tyton BioSciences)

13.9. Unifi, Inc.

13.10. Birla Cellulose

13.11. Hyosung TNC

13.12. Eastman Chemical Company

13.13. BASF SE

13.14. Veolia Environnement

13.15. Suez SA

14. Appendix

14.1. Additional Customization

14.2. Related Reports

Published Date: Apr-2026

Published Date: Mar-2026

Subscribe to get the latest industry updates