Resources

About Us

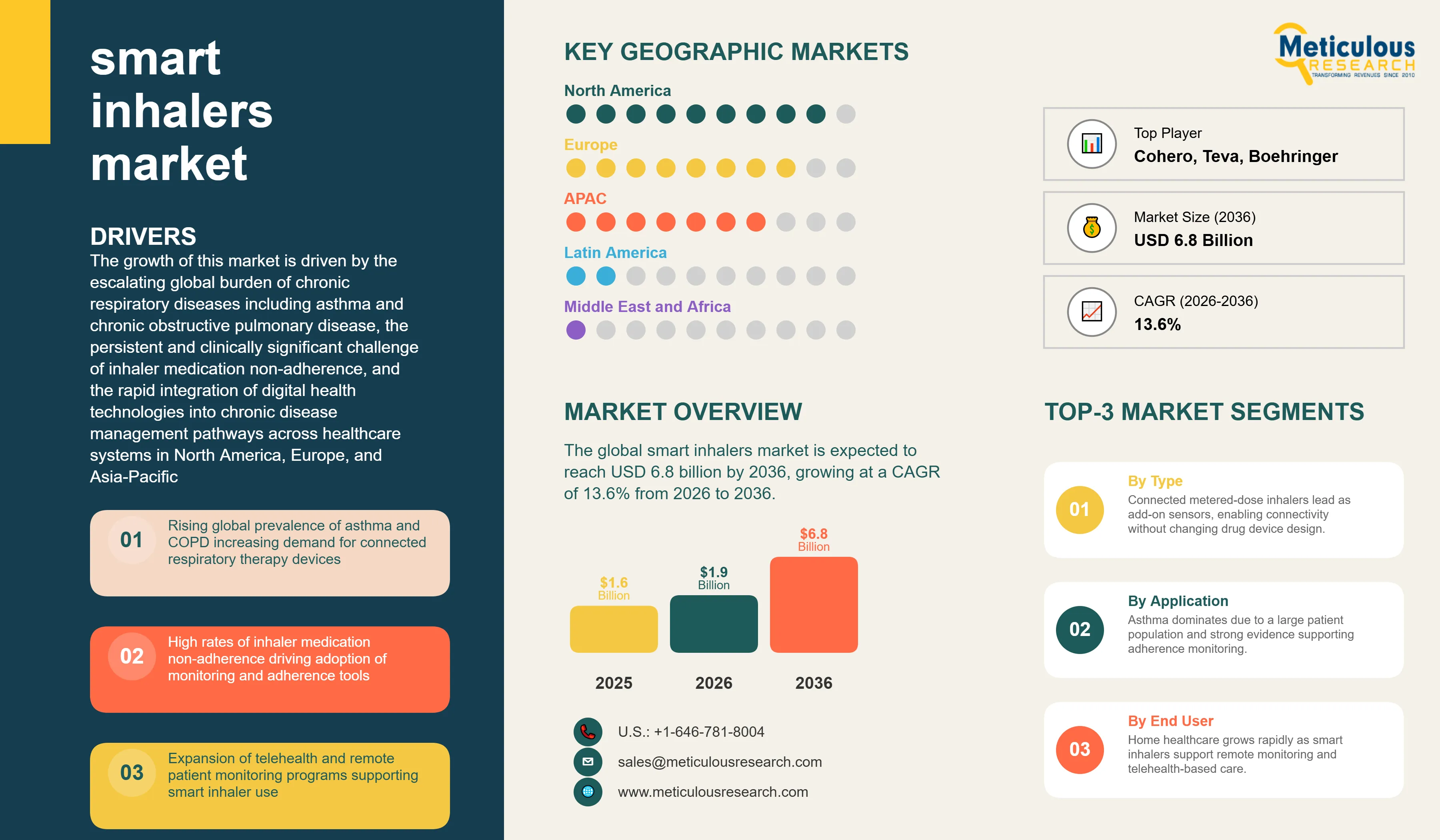

The global smart inhalers market was valued at USD 1.6 billion in 2025. This market is expected to reach USD 6.8 billion by 2036 from USD 1.9 billion in 2026, growing at a CAGR of 13.6% from 2026 to 2036.

The growth of this market is driven by the escalating global burden of chronic respiratory diseases including asthma and chronic obstructive pulmonary disease, the persistent and clinically significant challenge of inhaler medication non-adherence, and the rapid integration of digital health technologies into chronic disease management pathways across healthcare systems in North America, Europe, and Asia-Pacific. A smart inhaler system is a connected drug delivery device that combines a conventional inhalation therapy platform — whether a metered-dose inhaler, dry powder inhaler, soft mist inhaler, or nebulizer — with embedded electronic sensors, wireless communication modules, and linked mobile application and cloud analytics software that together capture detailed data on inhaler actuation timing, technique quality, inhalation flow rate, and environmental context. This data is transmitted to patient-facing mobile applications and clinician dashboards that provide adherence feedback, technique coaching, exacerbation risk alerts, and longitudinal therapy performance reporting.

The fundamental clinical problem that smart inhaler systems address is inhaler medication non-adherence, which affects an estimated 50 to 60 percent of patients with asthma and COPD globally and is directly associated with increased rates of acute exacerbations, unplanned emergency department visits, hospitalizations, and disease-related mortality. Conventional adherence monitoring approaches based on patient self-report and prescription refill records are widely recognized as inaccurate, and clinical studies using electronic monitoring have demonstrated that patients' actual inhaler use patterns differ dramatically from their self-reported behavior. Smart inhaler systems provide objective, timestamped records of every inhaler actuation that enable clinicians to identify specific adherence failure patterns, distinguish between non-adherence and poor inhaler technique as causes of inadequate disease control, and design targeted behavioral interventions that have been shown in randomized controlled trials to significantly improve adherence rates and clinical outcomes.

Click here to: Get Free Sample Pages of this Report

Smart inhaler systems represent the convergence of established pharmaceutical inhaled drug delivery technology with miniaturized consumer electronics, wireless communication, mobile health application software, and cloud-based data analytics platforms. The core hardware innovation enabling smart inhalers is the development of sensor and electronics modules sufficiently small, energy-efficient, and cost-effective to be incorporated either within new inhaler device designs by pharmaceutical manufacturers or as retrofit attachments that clip onto existing conventional inhaler canisters or caps. These sensor modules detect inhaler use events through one or more physical sensing modalities including acoustic microphones that detect the characteristic sound signature of drug canister actuation, airflow sensors that measure the inhalation flow rate through the inhaler mouthpiece, MEMS accelerometers that detect the orientation and movement patterns characteristic of inhaler use, and capacitive or optical sensors that detect the position of the inhaler dose counter or actuator. The combination of multiple sensing modalities in advanced smart inhaler designs enables the system to detect not only that an inhaler was used but also to assess whether the inhalation technique was adequate — specifically whether the patient's inspiratory flow rate was within the range required for effective drug deposition in the lungs for the specific device type.

The wireless data transmission layer of smart inhaler systems has largely standardized on Bluetooth Low Energy protocols that enable timestamped inhaler event data to be transmitted from the inhaler to the patient's smartphone automatically at the time of inhaler use or through periodic synchronization sessions. Smartphone-based mobile applications serve as the primary patient interface, presenting adherence tracking information in visualizations designed to motivate consistent use, providing inhalation technique feedback based on sensor data, sending programmed reminder notifications when scheduled doses are missed, and enabling patients to log symptom reports and environmental exposure data that contextualizes their inhaler use patterns. Cloud analytics platforms aggregate data from large patient populations to generate population-level adherence metrics and predictive exacerbation risk models that health system and payer customers use to identify high-risk patients requiring clinical intervention.

The market ecosystem includes three distinct business model approaches. Pharmaceutical companies including AstraZeneca, GSK, Boehringer Ingelheim, and Novartis are pursuing connectivity as a product differentiator, embedding smart features into new inhaler device platforms or partnering with specialist digital health companies to create connected versions of existing marketed drugs. Digital health platform companies including Propeller Health (acquired by ResMed), Adherium, and Cohero Health provide drug-agnostic smart inhaler add-on devices and analytics platforms that connect to multiple different pharmaceutical companies' inhaler products, selling adherence management services to health systems, payers, and pharmaceutical companies. Integrated care organizations and pharmacy benefit managers are increasingly procuring smart inhaler programs as disease management services where the adherence improvement and exacerbation prevention outcomes provide demonstrable return on investment through reduced emergency department and hospitalization costs.

Pharmaceutical Company-Digital Health Company Partnerships Accelerating Connected Inhaler Commercialization

The most commercially significant trend shaping the smart inhalers market is the active pursuit of strategic partnerships between major pharmaceutical companies with established inhaled respiratory drug franchises and specialist digital health companies with connected device and analytics platform capabilities. Pharmaceutical companies recognize that adding connectivity to marketed or pipeline inhaler products can differentiate their devices in a competitive inhaler market where multiple equivalent drug formulations exist across similar device platforms, support premium pricing through demonstrated clinical outcomes improvement, and enable real-world evidence generation that supports market access negotiations with payers. Digital health companies, for their part, benefit from pharmaceutical partnership access to large established patient populations, co-marketing resources, and regulatory expertise that would be difficult to access independently.

GSK's multi-year collaboration with Propeller Health to develop connected versions of its Ellipta DPI platform for severe asthma and COPD therapy represents one of the most advanced examples of this partnership model, with the integrated smart inhaler system progressing through clinical validation studies and commercial rollout programs across the United States and European markets. AstraZeneca has similarly partnered with Adherium to develop the Smartinhaler product platform for connected versions of its Symbicort and Pulmicort inhaler products. Boehringer Ingelheim has invested in developing proprietary connectivity for its Respimat SMI platform, targeting COPD patients managed under its Spiolto, Stiolto, and Ofev therapy programs. These pharmaceutical-led partnership programs are creating a pipeline of regulatory-cleared connected inhaler products with established commercial distribution channels and clinical evidence bases that independent smart inhaler companies would face significant barriers to replicate.

AI-Powered Predictive Analytics Transforming Adherence Programs into Exacerbation Prevention Platforms

The evolution of smart inhaler analytics platforms from retrospective adherence reporting tools toward prospective exacerbation prediction systems is significantly expanding the clinical and economic value proposition of smart inhaler programs for health system and payer customers. Early smart inhaler analytics platforms provided primarily historical visualizations of inhaler use frequency and timing patterns that were useful for clinical review consultations but did not enable proactive intervention before clinical deterioration occurred. Advanced AI-based analytics platforms now integrate smart inhaler adherence data with additional data streams including environmental air quality monitoring, symptom diary entries, physical activity data from wearables, and weather forecast data to build multi-variable predictive models that identify individual patient-specific patterns associated with elevated exacerbation risk several days before the clinical event would manifest.

Propeller Health's platform, operating across a patient population of hundreds of thousands of asthma and COPD patients in the United States, has demonstrated the ability to identify geographic clusters of elevated rescue inhaler use that correlate with local air quality deterioration events, enabling public health alerts and preemptive clinical outreach to high-risk patients. Cohero Health's BreatheSmart platform uses machine learning models trained on longitudinal patient data to generate individual exacerbation risk scores that care coordinators use to prioritize outreach calls to patients at elevated risk. Clinical study data from programs including the STAAR trial in the United Kingdom demonstrated that smart inhaler-based adherence programs supported by proactive clinical intervention protocols reduced asthma-related emergency department attendances by over 50 percent compared with usual care over a 12-month program period, providing the health economic evidence that is driving commissioning decisions by NHS and European health system purchasers.

|

Parameter |

Details |

|

Market Size by 2036 |

USD 6.8 Billion |

|

Market Size in 2026 |

USD 1.9 Billion |

|

Market Size in 2025 |

USD 1.6 Billion |

|

Market Growth Rate (2026–2036) |

CAGR of 13.6% |

|

Dominating Region |

North America |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Product Type, Technology, Indication, Distribution Channel, End User, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Driver: Rising Global Burden of Chronic Respiratory Diseases and Medication Non-Adherence

The primary driver of the smart inhalers market is the growing global prevalence of asthma and COPD combined with the persistent and clinically consequential failure of conventional inhaler therapy delivery to achieve adequate medication adherence in the patient populations affected by these conditions. The World Health Organization estimates that over 330 million people worldwide currently live with asthma, and approximately 480 million with COPD, with both disease burdens continuing to grow due to urbanization, air pollution, tobacco use in developing countries, and the aging of global populations. These two conditions together account for substantial direct healthcare expenditure through emergency department visits, hospitalizations, and intensive care admissions associated with acute exacerbations, the majority of which are considered preventable through adequate maintenance therapy adherence.

The clinical and economic consequences of inhaler non-adherence are well-documented. Studies conducted across multiple healthcare systems consistently demonstrate that patients with poorly controlled asthma who are classified as treatment-refractory frequently improve substantially when objective adherence monitoring reveals and addresses underlying non-adherence, rather than requiring treatment escalation to more expensive biologic therapies. For payers, the cost of a single COPD exacerbation requiring hospitalization in the United States ranges from USD 20,000 to USD 50,000, creating strong incentives to fund adherence management programs that can prevent even a small fraction of exacerbation events across a managed patient population. Smart inhaler systems that provide objective adherence data and enable targeted clinical intervention represent a clinically credible and increasingly cost-effective mechanism for addressing this adherence gap.

Opportunity: Integration with Telehealth and Remote Patient Monitoring Reimbursement Programs

The rapid expansion of telehealth and remote patient monitoring (RPM) reimbursement frameworks in the United States and Europe is creating a significant commercial opportunity for smart inhaler systems vendors. The Centers for Medicare and Medicaid Services in the United States established RPM billing codes that allow healthcare providers to bill for the time spent reviewing and managing data from connected patient monitoring devices, including smart inhalers, when used in a structured clinical program. Private payers including Cigna, Aetna, and UnitedHealth Group have developed value-based respiratory care programs that incorporate smart inhaler adherence monitoring as a clinical data source for outcome-based contracting arrangements with hospital systems and physician groups.

The alignment between smart inhaler system capabilities and the data requirements of remote patient monitoring reimbursement frameworks is creating a commercial pathway that did not exist before 2019, when CMS established the initial RPM billing codes that have since been progressively expanded in scope. Healthcare providers who enroll COPD and asthma patients in RPM programs using smart inhalers as the connected monitoring device can generate recurring monthly billing revenue for clinical time spent on data review and patient communication, creating a sustainable practice economics model that supports the clinician engagement required to realize the clinical benefits of smart inhaler programs. This reimbursement infrastructure is expected to significantly accelerate U.S. market adoption as healthcare providers develop systematic smart inhaler program enrollment and management workflows integrated with their existing chronic disease management capabilities.

How Do Connected Metered-Dose Inhalers Lead the Market?

In 2026, the connected metered-dose inhalers (cMDI) segment is expected to hold the largest share of the smart inhalers market. Pressurized metered-dose inhalers remain the most widely prescribed inhaler format globally for both asthma rescue therapy and maintenance therapy, with billions of units dispensed annually across North America, Europe, and Asia. The retrofit add-on sensor attachment model developed by Propeller Health and Adherium enables smart inhaler connectivity to be applied to existing marketed MDI products without requiring changes to the drug formulation or canister, which in many regulatory jurisdictions avoids the need for full device combination product reapproval. This approach has enabled rapid commercial scaling by allowing pharmaceutical companies to offer connected versions of their existing MDI products with relatively low incremental development investment, and has allowed smart inhaler platform companies to support multiple different pharmaceutical companies' products on a single sensor and analytics platform.

The cDPI segment, however, is expected to witness the fastest growth during the forecast period. This growth is driven by the progressive clinical shift toward DPI-based maintenance therapy platforms for severe asthma and COPD, where the Ellipta and Turbuhaler DPI device families from GSK and AstraZeneca respectively hold dominant market positions. As pharmaceutical companies integrate connectivity directly into next-generation DPI device designs rather than relying on retrofit attachments, the sensor and analytics capabilities available for DPI-delivered maintenance therapies will surpass those achievable with add-on approaches, and the seamless patient experience of a fully integrated smart DPI is expected to drive adoption in the high-value severe disease patient segments where smart inhaler programs generate the greatest clinical and economic returns.

How Does the Asthma Indication Lead the Market?

In 2026, the asthma indication segment is expected to hold the largest share of the smart inhaler systems market. Asthma is the most prevalent chronic respiratory condition globally among both adults and children, and the smart inhaler market for asthma management has benefited from the earliest and most extensive clinical evidence base demonstrating the adherence improvement and outcome benefits of connected inhaler programs. The availability of multiple validated smart inhaler products specifically developed and regulatory-cleared for asthma management, including Propeller Health's connected platform for Ventolin and QVAR, Adherium's Smartinhaler for Symbicort and Foster, and Cohero Health's mSpirometer and connected inhaler system, provides commercial choice for health systems and payers seeking to implement asthma adherence programs. The strong pediatric asthma segment within the overall indication, where parents are particularly motivated to engage with digital tools that provide reassurance about their child's medication adherence and technique, is a commercially attractive subsegment for smart inhaler vendors offering child-friendly device designs and family engagement application features.

However, the COPD indication is expected to witness the fastest growth during the forecast period. COPD affects a predominantly elderly and often less digitally confident patient population, which has historically made mobile application-based adherence programs more challenging to deploy successfully in COPD than in asthma. However, the particularly strong health economic case for adherence improvement in COPD, where exacerbation costs are high and maintenance therapy adherence rates are very low, is motivating health systems and payers to invest in implementation support infrastructure including device onboarding support, simplified application interfaces, and care coordinator-mediated program enrollment that addresses the usability barriers for older COPD patients. The multiple device burden common in severe COPD, where patients manage two or three concurrent inhaler devices with different usage schedules and techniques, creates a compelling use case for smart inhaler monitoring that distinguishes non-adherence from technique errors and device confusion as causes of inadequate disease control.

How Do Hospital Pharmacies Lead the Market?

In 2026, the hospital pharmacies segment is expected to hold the largest share of the smart inhaler systems market. Hospital pharmacies serve as the primary dispensing channel for smart inhaler systems in European markets where national health service procurement programs are the dominant commercial pathway, and in the United States where specialty hospital-based respiratory disease management programs incorporate smart inhalers as a standard component of discharge planning for patients admitted with severe asthma or COPD exacerbations. Hospital-based pulmonology programs that prescribe smart inhaler systems as part of structured respiratory disease management pathways benefit from the clinical infrastructure to provide device onboarding, patient education, and systematic adherence data review, which are the implementation requirements that determine whether smart inhaler programs achieve their full clinical benefit potential.

However, the online and e-commerce channels segment is expected to witness the fastest growth during the forecast period, reflecting the broader trend toward direct-to-consumer health product purchasing and the increasing availability of smart inhaler add-on devices as over-the-counter consumer health products in some markets. The ability to purchase smart inhaler sensor attachments directly and link them to manufacturer-provided mobile applications without a clinical prescription is expanding the accessible patient population for smart inhaler benefits beyond the healthcare system-enrolled population, creating a consumer health market segment alongside the established clinical program market.

How is North America Maintaining Market Leadership?

In 2026, North America is expected to hold the largest share of the global smart inhalers market. The United States is the largest and most commercially advanced national market for smart inhaler systems, supported by the combination of high asthma and COPD disease burden, sophisticated payer infrastructure that has established reimbursement frameworks for digital therapeutics and remote patient monitoring services incorporating smart inhaler data, and the commercial leadership of Propeller Health, Adherium's U.S. operations, and pharmaceutical company digital health initiatives including AstraZeneca's AMAZE and CONNECT studies that have generated the clinical evidence base required for payer contracting.

The United Kingdom contributes significantly to North American market leadership by demonstrating through NHS commissioning of smart inhaler programs that health system-level smart inhaler deployment at population scale is operationally and economically feasible. NHS Scotland's national smart inhaler initiative and NHS England's integrated care system respiratory digital health programs have provided real-world outcome data that health systems in North America and across Europe are using to justify their own commissioning decisions. Canada's provincial health system interest in smart inhaler programs for Indigenous and remote community respiratory disease management, where in-person clinical access is limited, represents a growing market segment for connected inhaler and telehealth-integrated respiratory care solutions.

Which Factors Drive Asia-Pacific's Rapid Growth?

Asia-Pacific is expected to witness the highest growth rate in the smart inhalers market during the forecast period. This growth is driven by the convergence of rapidly growing respiratory disease burden attributable to urban air quality deterioration in China and India, expanding smartphone and mobile health infrastructure enabling digital adherence platforms, and growing health system investment in chronic disease management technologies in Japan, South Korea, Singapore, and Australia.

China represents the largest growth opportunity within Asia-Pacific, with an estimated COPD patient population of over 100 million and urban air pollution levels that drive high rates of asthma exacerbation in major cities. The Chinese government's digital health infrastructure investment, including national electronic health record standardization programs and provincial telemedicine network development, is creating the connectivity infrastructure that smart inhaler analytics platforms require to deliver their full value to clinical and public health system users. India's large and underdiagnosed COPD population, estimated to exceed 55 million patients, combined with rapidly growing smartphone penetration among working-age adults, creates a large addressable market for smart inhaler programs delivered through primary care digital health platforms. Australia's strong digital health infrastructure, well-developed telehealth reimbursement framework, and highly active respiratory research community, including the Woolcock Institute of Medical Research and multiple university clinical trials programs, are supporting both commercial smart inhaler market development and the generation of real-world clinical evidence that informs global market adoption.

Some of the key companies operating in the global smart inhalers market are AstraZeneca PLC, GlaxoSmithKline PLC (GSK), Boehringer Ingelheim GmbH, Novartis AG, Teva Pharmaceutical Industries Ltd., Propeller Health (a ResMed company), Adherium Ltd., 3M Health Care (Kindeva Drug Delivery), Philips Respironics, PARI Medical Holding GmbH, Cohero Health Inc., Vectura Group PLC, Respira Therapeutics, Voluntis SA, and Gridscape Solutions Inc.

The global smart inhalers market is expected to grow from USD 1.9 billion in 2026 to USD 6.8 billion by 2036.

The global smart inhalers market is projected to grow at a CAGR of 13.6% from 2026 to 2036.

The connected metered-dose inhalers (cMDI) segment is expected to dominate the overall market in 2026. However, the connected dry powder inhalers (cDPI) segment is expected to witness the fastest CAGR, driven by pharmaceutical company integration of connectivity into new-generation DPI device platforms, the growing clinical preference for DPI-delivered maintenance therapies in severe asthma and COPD, and the superior patient experience and environmental profile of DPI systems relative to propellant-based pMDI platforms.

The asthma segment is expected to dominate the overall market in 2026. However, the COPD segment is expected to witness the fastest CAGR, driven by the very high economic cost of preventable COPD exacerbations that motivates payer investment in adherence programs, the large and underserved global COPD patient population, and improving smart inhaler usability design for the elderly patient population where COPD is most prevalent.

The hospitals and tertiary care centers segment is expected to dominate the overall market in 2026. However, the home healthcare settings segment is expected to witness the fastest CAGR, as telehealth and remote patient monitoring reimbursement models enable smart inhaler programs to be delivered outside clinical settings, expanding access to the large and growing population of patients managing chronic respiratory disease independently at home.

North America is expected to lead the global market in 2026. However, Asia-Pacific is expected to witness the fastest CAGR, driven by China's rapidly growing respiratory disease burden and digital health infrastructure investment, India's large underserved COPD patient population, and Japan's and Australia's advanced digital health ecosystems and health system investment in connected chronic disease management technologies.

The major players are AstraZeneca PLC, GlaxoSmithKline PLC (GSK), Boehringer Ingelheim GmbH, Novartis AG, Teva Pharmaceutical Industries Ltd., Propeller Health (ResMed), Adherium Ltd., Philips Respironics, PARI Medical Holding GmbH, Cohero Health Inc., and Vectura Group PLC.

1. Introduction

1.1 Market Definition

1.2 Market Scope

1.2.1 Inclusions & Exclusions

1.2.2 Geographic Coverage

1.3 Research Methodology

1.3.1 Primary Research

1.3.2 Secondary Research

1.3.3 Data Triangulation Approach

1.4 Assumptions & Limitations

2. Executive Summary

2.1 Market Snapshot

2.2 Key Findings by Segment

2.3 Strategic Recommendations

3. Market Overview

3.1 Introduction

3.2 Market Dynamics

3.2.1 Drivers

3.2.1.1 Rising Global Burden of Chronic Respiratory Diseases

3.2.1.2 Medication Non-Adherence and Clinical Outcomes Gap

3.2.1.3 Digital Health Integration and Remote Patient Monitoring Adoption

3.2.1.4 Payer and Health System Incentives for Adherence Management

3.2.2 Restraints

3.2.2.1 High Device Cost and Reimbursement Uncertainty

3.2.2.2 Patient Data Privacy Concerns and Regulatory Complexity

3.2.2.3 Interoperability Challenges Across Health IT Ecosystems

3.2.3 Opportunities

3.2.3.1 Pediatric and Elderly Population-Specific Smart Inhaler Development

3.2.3.2 AI-Driven Personalized Therapy Adjustment Platforms

3.2.3.3 Integration with Electronic Health Records and Telehealth Platforms

3.2.3.4 Expansion in Emerging Markets with High COPD Prevalence

3.2.4 Challenges

3.2.4.1 Clinical Evidence Requirements for Reimbursement Approval

3.2.4.2 Device Usability and Patient Acceptance in Low-Literacy Populations

3.3 Technology Landscape

3.3.1 Sensor Technologies: Acoustic, Flow, Accelerometer, and Optical

3.3.2 Wireless Communication: Bluetooth LE, NFC, Wi-Fi, and Cellular

3.3.3 Cloud Analytics and AI-Based Adherence Algorithms

3.3.4 Mobile Application Platforms and Patient Engagement Interfaces

3.3.5 Integration with Wearables and Continuous Monitoring Devices

3.4 Regulatory and Standards Environment

3.4.1 FDA Digital Health Guidance and De Novo Classification Framework

3.4.2 EMA Connected Device Regulatory Pathways in Europe

3.4.3 ISO 13485, IEC 62133, and Medical Device Software (MDSW) Standards

3.4.4 HIPAA, GDPR, and Cross-Border Patient Data Compliance

3.5 Porter's Five Forces Analysis

3.6 Value Chain Analysis

3.6.1 Component Suppliers

3.6.2 Device Manufacturers

3.6.3 Software and Platform Developers

3.6.4 Distribution and Pharmacy Networks

3.6.5 End Users and Payers

3.7 Patent Landscape and IP Analysis

3.8 Pricing Analysis by Product Type and Region

4. Global Smart Inhalers Market, by Product Type

4.1 Introduction

4.2 Connected Metered-Dose Inhalers (cMDI)

4.2.1 Standard Pressurized cMDI

4.2.2 Breath-Actuated Pressurized cMDI

4.3 Connected Dry Powder Inhalers (cDPI)

4.3.1 Single-Dose cDPI

4.3.2 Multi-Dose Reservoir cDPI

4.3.3 Multi-Dose Blister Strip cDPI

4.4 Connected Soft Mist Inhalers (cSMI)

4.5 Connected Nebulizers

4.5.1 Jet Nebulizers

4.5.2 Ultrasonic Nebulizers

4.5.3 Mesh Nebulizers

4.6 Smart Spacers and Valved Holding Chambers

4.6.1 Adult Smart Spacers

4.6.2 Pediatric Smart Spacers

5. Global Smart Inhalers Market, by Technology

5.1 Introduction

5.2 Bluetooth and Bluetooth Low Energy (BLE)

5.3 Near Field Communication (NFC)

5.4 Wi-Fi Enabled Smart Inhalers

5.5 Cellular-Enabled Smart Inhalers

5.6 Hybrid Connectivity Platforms

5.7 Embedded Sensor Technologies

6. Global Smart Inhalers Market, by Indication

6.1 Introduction

6.2 Asthma

6.3 Chronic Obstructive Pulmonary Disease (COPD)

6.4 Cystic Fibrosis

6.5 Pulmonary Arterial Hypertension (PAH)

6.6 Bronchiectasis

6.7 Other Respiratory Indications

7. Global Smart Inhalers Market, by Drug Type

7.1 Introduction

7.2 Short-Acting Beta-2 Agonists (SABA)

7.3 Long-Acting Beta-2 Agonists (LABA)

7.4 Inhaled Corticosteroids (ICS)

7.5 ICS/LABA Fixed-Dose Combinations

7.6 Long-Acting Muscarinic Antagonists (LAMA)

7.7 LAMA/LABA Fixed-Dose Combinations

7.8 Triple Therapy (ICS/LABA/LAMA)

7.9 Mucolytics and Other Inhaled Agents

8. Global Smart Inhalers Market, by Component

8.1 Introduction

8.2 Hardware

8.3 Software

8.4 Cloud and Data Services

8.5 Connectivity Infrastructure

9. Global Smart Inhalers Market, by Distribution Channel

9.1 Introduction

9.2 Hospital Pharmacies

9.3 Retail and Community Pharmacies

9.4 Online and E-Commerce Channels

9.5 Specialty Respiratory Clinics and Direct Provider Supply

9.6 Government and Tender-Based Procurement

10. Global Smart Inhalers Market, by End User

10.1 Introduction

10.2 Hospitals and Tertiary Care Centers

10.2.1 Pulmonology and Respiratory Medicine Departments

10.2.2 Intensive Care Units and Emergency Departments

10.2.3 Pediatric Respiratory Units

10.3 Ambulatory and Outpatient Clinics

10.3.1 Respiratory Specialty Outpatient Clinics

10.3.2 Allergy and Immunology Clinics

10.3.3 Primary Care and General Practice Clinics

10.4 Home Healthcare Settings

10.4.1 Self-Managed Chronic Respiratory Disease Patients

10.4.2 Home Healthcare Agency-Managed Patients

10.4.3 Telehealth-Enrolled Patients

10.5 Long-Term Care and Rehabilitation Facilities

10.5.1 Skilled Nursing Facilities

10.5.2 Pulmonary Rehabilitation Centers

10.6 Research Institutions and Clinical Trial Settings

10.6.1 Academic Medical Centers Conducting Respiratory Trials

10.6.2 CRO-Managed Clinical Trials

11. Global Smart Inhalers Market, by Age Group

11.1 Introduction

11.2 Pediatric (0–11 Years)

11.3 Adolescent (12–17 Years)

11.4 Adult (18–64 Years)

11.5 Geriatric (65 Years and Above)

12. Global Smart Inhalers Market, by Geography

12.1 Introduction

12.2 North America

12.2.1 U.S.

12.2.2 Canada

12.3 Europe

12.3.1 Germany

12.3.2 United Kingdom

12.3.3 France

12.3.4 Italy

12.3.5 Spain

12.3.6 Netherlands

12.3.7 Belgium

12.3.8 Sweden

12.3.9 Denmark

12.3.10 Switzerland

12.3.11 Austria

12.3.12 Rest of Europe

12.4 Asia-Pacific

12.4.1 China

12.4.2 Japan

12.4.3 India

12.4.4 South Korea

12.4.5 Australia

12.4.6 Singapore

12.4.7 Thailand

12.4.8 Malaysia

12.4.9 Indonesia

12.4.10 Rest of Asia-Pacific

12.5 Latin America

12.5.1 Brazil

12.5.2 Mexico

12.5.3 Argentina

12.5.4 Colombia

12.5.5 Chile

12.5.6 Rest of Latin America

12.6 Middle East & Africa

12.6.1 UAE

12.6.2 Saudi Arabia

12.6.3 South Africa

12.6.4 Turkey

12.6.5 Egypt

12.6.6 Rest of Middle East & Africa

13. Competitive Landscape

13.1 Overview

13.2 Key Growth Strategies

13.2.1 Product Launches and Pipeline

13.2.2 Partnerships, Collaborations, and Licensing Agreements

13.2.3 Mergers and Acquisitions

13.2.4 Geographic Expansion

13.3 Competitive Benchmarking

13.4 Competitive Dashboard

13.4.1 Industry Leaders

13.4.2 Market Differentiators

13.4.3 Vanguards

13.4.4 Emerging Companies

13.5 Market Ranking/Positioning Analysis of Key Players, 2025

14. Company Profiles

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

14.1 AstraZeneca PLC (Adherium Partnership)

14.2 GlaxoSmithKline PLC (GSK — Propeller Health Partnership)

14.3 Boehringer Ingelheim GmbH

14.4 Novartis AG

14.5 Teva Pharmaceutical Industries Ltd.

14.6 Propeller Health (ResMed Company)

14.7 Adherium Ltd.

14.8 3M Health Care (Kindeva Drug Delivery)

14.9 Philips Respironics

14.10 PARI Medical Holding GmbH

14.11 Cohero Health Inc.

14.12 Smartinhaler (Adherium)

14.13 Vectura Group PLC

14.14 Respira Therapeutics

14.15 Voluntis SA

15. Appendix

15.1 Questionnaire

15.2 Related Reports

15.3 Available Customization

Published Date: Jan-2025

Published Date: Aug-2024

Subscribe to get the latest industry updates