Resources

About Us

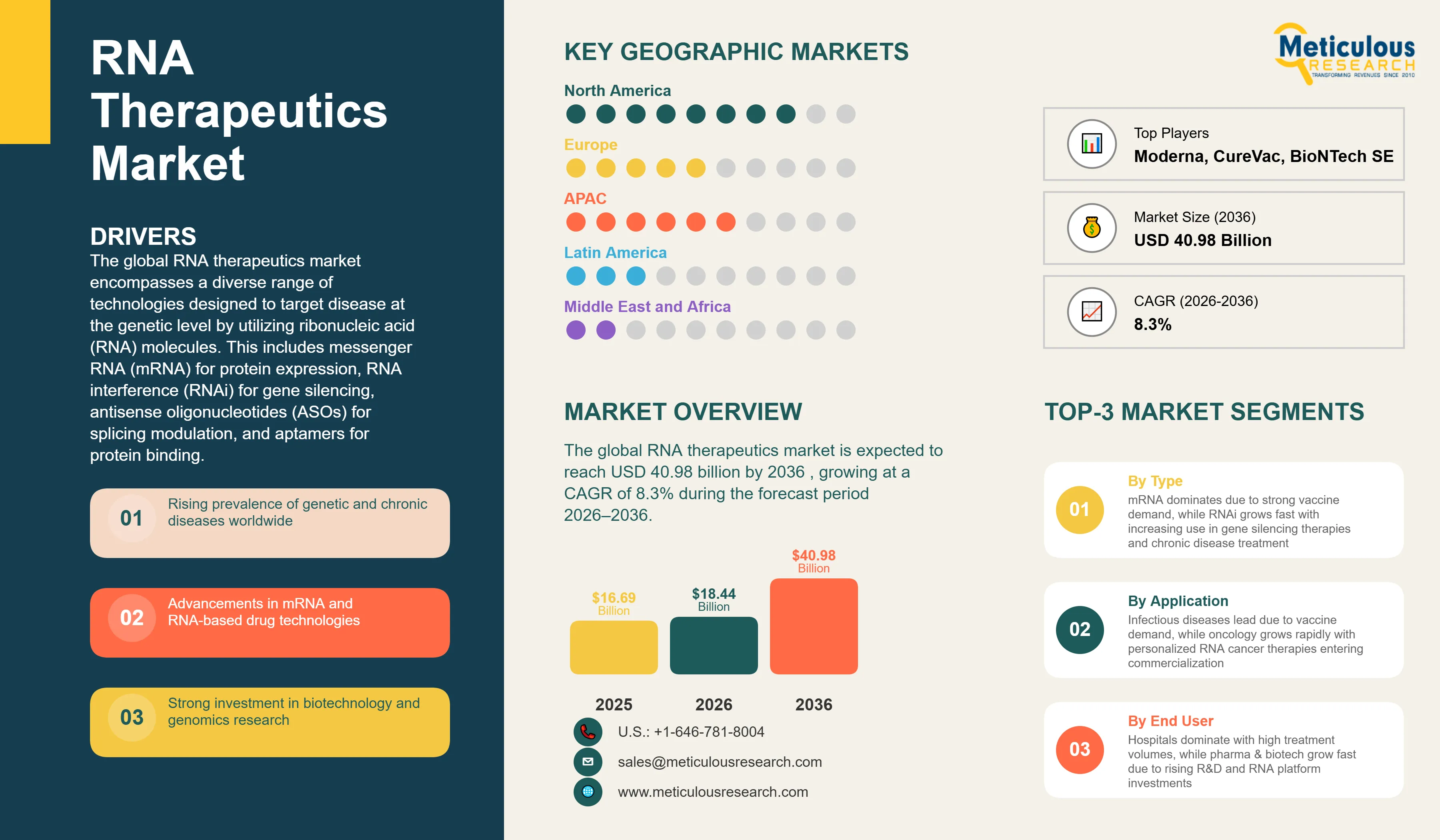

The global RNA therapeutics market was valued at USD 16.69 billion in 2025. This market is expected to reach USD 40.98 billion by 2036 from an estimated USD 18.44 billion in 2026, growing at a CAGR of 8.3% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

The global RNA therapeutics market encompasses a diverse range of technologies designed to target disease at the genetic level by utilizing ribonucleic acid (RNA) molecules. This includes messenger RNA (mRNA) for protein expression, RNA interference (RNAi) for gene silencing, antisense oligonucleotides (ASOs) for splicing modulation, and aptamers for protein binding. These therapies represent a paradigm shift in medicine, moving from traditional small molecules and biologics to programmable genetic medicines.

RNA therapeutics function as a versatile platform capable of addressing "undruggable" targets, enabling the treatment of rare genetic disorders, complex cancers, and infectious diseases. The market is characterized by rapid technological evolution, particularly in delivery systems like Lipid Nanoparticles (LNPs) and GalNAc conjugates, which have overcome historical challenges related to RNA stability and cellular uptake.

The growth of the global RNA therapeutics market is primarily driven by the increasing prevalence of chronic and genetic diseases, coupled with the validated success of mRNA technology during the pandemic. The ability to rapidly design and manufacture RNA-based candidates makes them ideal for personalized medicine and rapid response to emerging pathogens. Furthermore, significant venture capital and institutional investment in the biotechnology sector are accelerating the clinical pipeline.

However, the market faces constraints such as high development and manufacturing costs, particularly for personalized therapies. Delivery remains a challenge for extra-hepatic tissues, and the complex regulatory landscape for gene-based therapies can lead to extended approval timelines. Additionally, the requirement for ultra-cold chain logistics for certain mRNA products poses a barrier in developing regions.

Despite these challenges, opportunities abound in the expansion of RNA therapies into oncology and cardiovascular diseases. The development of next-generation delivery platforms, such as exosomes and circular RNA (circRNA), promises improved stability and tissue specificity. Strategic collaborations between big pharma and nimble biotech firms are also expected to drive market expansion through the forecast period.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 40.98 Billion |

|

Market Size in 2026 |

USD 18.44 Billion |

|

Market Size in 2025 |

USD 16.69 Billion |

|

Revenue Growth Rate (2026–2036) |

CAGR of 8.3% |

|

Dominating Technology Type |

mRNA Therapeutics |

|

Fastest Growing Technology Type |

RNA Interference (RNAi) |

|

Dominating Indication |

Infectious Diseases |

|

Fastest Growing Indication |

Oncology |

|

Dominating Delivery Platform |

Lipid Nanoparticles (LNPs) |

|

Fastest Growing Delivery Platform |

Conjugate-Based Delivery (GalNAc) |

|

Dominating End User |

Hospitals and Clinics |

|

Fastest Growing End User |

Pharmaceutical & Biotech Companies |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Expansion of mRNA-Based Therapeutics Beyond Vaccines into Oncology

The most significant trend in the RNA therapeutics market is the pivot of mRNA technology from prophylactic vaccines to therapeutic applications, particularly in oncology. Companies like Moderna and BioNTech are advancing personalized cancer vaccines that encode patient-specific neoantigens to trigger a targeted immune response. This shift is transforming the oncology landscape, offering a highly precise alternative to traditional chemotherapy and even existing immunotherapies. The integration of mRNA with checkpoint inhibitors is showing promising results in clinical trials for melanoma and non-small cell lung cancer, signaling a new era of "programmable" cancer treatment.

Advancements in Extra-Hepatic Delivery Technologies

While the liver has been the primary target for RNA therapies due to the natural accumulation of delivery vehicles like LNPs and GalNAc conjugates, a major trend is the development of technologies for extra-hepatic delivery. Researchers and companies are engineering novel ligands and viral-like particles to target the lungs, central nervous system (CNS), and heart. This expansion is critical for treating neurological disorders like Alzheimer’s and Huntington’s disease, as well as cystic fibrosis. The move toward tissue-specific delivery is expected to significantly expand the addressable market for RNA therapeutics over the next decade.

Rise of RNA Interference (RNAi) for Chronic Disease Management

RNA interference (RNAi) is transitioning from a tool for rare disease treatment to a mainstream platform for chronic disease management. The approval of siRNA drugs for conditions like primary hyperoxaluria and hereditary transthyretin-mediated amyloidosis has paved the way for targeting more common conditions. A key trend is the development of long-acting RNAi therapies for cardiovascular health, such as Inclisiran for LDL cholesterol reduction, which requires only twice-yearly dosing. This "vaccine-like" approach to chronic disease management is expected to drive high volume adoption and market growth.

By Technology Type: In 2026, the mRNA Segment to Dominate the Global RNA Therapeutics Market

Based on technology type, the global RNA therapeutics market is segmented into mRNA, RNAi, ASO, and aptamers. In 2026, the mRNA therapeutics segment is expected to account for the largest share of RNA therapeutics market. The large share of this segment is attributed to the high capital expenditure cycle in mRNA manufacturing and the broad clinical pipeline targeting both infectious diseases and oncology. The hardware and infrastructure for mRNA production are in active large-volume procurement across global biopharmaceutical hubs.

However, the RNA interference (RNAi) segment is poised to grow at the highest CAGR of during the forecast period. The high growth of this segment is attributed to the growing adoption of GalNAc-conjugation for liver targeting, the increasing deployment of siRNA for chronic metabolic disorders, and the rising number of clinical milestones in the RNAi pipeline.

By Indication: In 2026, Infectious Diseases to Hold the Largest Share

Based on indication, the market is segmented into oncology, infectious diseases, rare genetic disorders, cardiovascular diseases, and others. In 2026, the infectious diseases segment is expected to account for the largest share of RNA therapeutics market. The large share of this segment is attributed to the continued demand for mRNA-based respiratory vaccines and the active development of next-generation candidates for HIV, Zika, and malaria.

The oncology segment is poised to grow at the highest CAGR of during the forecast period. This growth is fueled by the transition of several personalized mRNA cancer vaccines and RNAi-based tumor suppressors into late-stage clinical trials. The ability of RNA therapies to target previously "undruggable" oncogenes and modulate the tumor microenvironment positions this segment for explosive growth.

By Delivery Platform: In 2026, Lipid Nanoparticles (LNPs) to Dominate the Global Market

Based on delivery platform, the global RNA therapeutics market is segmented into LNPs, conjugate-based delivery (e.g., GalNAc), viral vectors, and polymer-based systems. In 2026, the Lipid Nanoparticles (LNPs) segment is expected to account for the largest share of RNA therapeutics market. The large share of this segment is attributed to the high volume of mRNA vaccines utilizing LNP technology and the established safety and efficacy profile of LNPs in global clinical applications.

However, the Conjugate-Based Delivery (e.g., GalNAc) segment is poised to grow at the highest CAGR of during the forecast period. The high growth of this segment is attributed to the superior stability and tissue-specific targeting of GalNAc for liver-based therapies, which reduces off-target effects and enables subcutaneous administration, improving patient compliance.

By End User: In 2026, Hospitals and Clinics to Hold the Largest Share

Based on end user, the market is segmented into hospitals and clinics, research institutes, and pharmaceutical & biotechnology companies. In 2026, the hospitals and clinics segment is expected to account for the largest share of RNA therapeutics market. The large share of this segment is attributed to the high volume of vaccine administration and the increasing integration of RNA-based therapies into standard clinical practice for rare and chronic diseases.

The pharmaceutical and biotechnology companies segment is poised to grow at the highest CAGR of during the forecast period. This growth is attributed to the rapid expansion of internal R&D programs, the increasing number of strategic collaborations for RNA platform development, and the rising investment in proprietary manufacturing facilities to secure supply chains.

By Geography: North America to Dominate; Asia Pacific to Grow Fastest

North America is expected to account for the largest share of RNA therapeutics market. The large share of this region is attributed to the presence of industry giants like Moderna and Alnylam, a high concentration of research universities, and a supportive ecosystem for orphan drug development. The U.S. FDA’s proactive stance on advanced therapy medicinal products (ATMPs) further bolsters this region.

Asia Pacific is poised to grow at the highest CAGR of during the forecast period. This growth is driven by massive investments in biotechnology by the Chinese government, the expansion of CDMO services in India and South Korea, and an increasing focus on addressing the regional burden of infectious and metabolic diseases. The region is also becoming a hub for clinical trials due to its large patient populations and improving regulatory standards.

The global RNA therapeutics market is highly competitive and rapidly evolving, with competition focused on delivery platform efficiency, clinical pipeline depth, intellectual property strength, and the ability to scale manufacturing for global distribution.

Moderna and BioNTech lead the mRNA segment, leveraging their massive commercial success from COVID-19 vaccines to fund expansive pipelines in oncology and rare diseases. Alnylam Pharmaceuticals maintains a dominant position in the RNAi space with its proprietary GalNAc-conjugate technology and a growing portfolio of approved siRNA therapies. Ionis Pharmaceuticals competes through its extensive antisense oligonucleotide (ASO) platform and strategic partnerships with major pharmaceutical companies like Biogen and AstraZeneca.

The report provides a comprehensive competitive analysis based on an extensive assessment of leading players’ product portfolios, geographic presence, and key strategic developments over the past few years. Some of the key players operating in the global RNA therapeutics market include Moderna, Inc. (U.S.), BioNTech SE (Germany), Alnylam Pharmaceuticals, Inc. (U.S.), Ionis Pharmaceuticals, Inc. (U.S.), Sarepta Therapeutics, Inc. (U.S.), Arrowhead Pharmaceuticals, Inc. (U.S.), CureVac N.V. (Germany), Translate Bio (Sanofi) (France), Silence Therapeutics plc (U.K.), and CRISPR Therapeutics AG (Switzerland), among others.

The global RNA therapeutics market is expected to reach USD 40.98 billion by 2036 from an estimated USD 18.44 billion in 2026, at a CAGR of 8.3% during the forecast period 2026–2036.

In 2026, the mRNA therapeutics segment is expected to hold the largest share of the global RNA therapeutics market, driven by the high volume of vaccine sales and emerging oncology applications.

The RNA interference (RNAi) segment is expected to register a high CAGR during the forecast period 2026–2036, fueled by the expansion of siRNA therapies into high-prevalence chronic diseases.

In 2026, the infectious diseases segment is expected to hold the largest share of the global RNA therapeutics market.

The oncology segment is projected to witness the highest growth rate during the forecast period, as personalized RNA cancer vaccines enter the commercial phase.

The growth of this market is primarily driven by the increasing prevalence of genetic and chronic diseases, advancements in RNA delivery technologies (like LNPs and GalNAc), and the validated success of mRNA platforms in global health.

Key players include Moderna, Inc., BioNTech SE, Alnylam Pharmaceuticals, Inc., Ionis Pharmaceuticals, Inc., and Sarepta Therapeutics, Inc., among others.

Asia Pacific is expected to register the highest growth rate in the global RNA therapeutics market during the forecast period 2026–2036.

1. Introduction

1.1 Market Definition

1.2 Market Ecosystem

1.3 Currency and Limitations

1.3.1 Currency

1.3.2 Limitations

1.4 Key Stakeholders

2. Research Methodology

2.1 Research Approach

2.2 Data Collection & Validation Process

2.2.1 Secondary Research

2.2.2 Primary Research & Validation

2.2.2.1 Primary Interviews with Experts

2.2.2.2 Approaches for Country-/Region-Level Analysis

2.3 Market Estimation

2.3.1 Bottom-Up Approach

2.3.2 Top-Down Approach

2.3.3 Growth Forecast

2.4 Data Triangulation

2.5 Assumptions for the Study

3. Executive Summary

4. Market Overview

4.1 Introduction

4.2 Market Dynamics

4.2.1 Drivers

4.2.1.1 Increasing Prevalence of Genetic and Chronic Diseases

4.2.1.2 Advancements in RNA-Based Drug Technologies

4.2.1.3 Success of mRNA Vaccines Accelerating Adoption

4.2.1.4 Growing Investment in Biotechnology and Genomics

4.2.2 Restraints

4.2.2.1 High Development and Manufacturing Costs

4.2.2.2 Delivery Challenges for RNA Molecules

4.2.2.3 Regulatory and Clinical Trial Complexities

4.2.3 Opportunities

4.2.3.1 Expansion of RNA Therapeutics in Oncology

4.2.3.2 Development of Personalized Medicine

4.2.3.3 Emerging Applications in Rare Diseases

4.2.3.4 Advancements in RNA Delivery Technologies

4.2.4 Challenges

4.2.4.1 Stability and Storage Issues

4.2.4.2 Immunogenicity and Off-Target Effects

4.3 Key Market Trends

4.3.1 Expansion of mRNA-Based Therapeutics Beyond Vaccines

4.3.2 Growth of RNA Interference (RNAi) Therapies

4.3.3 Increasing Use of Lipid Nanoparticle (LNP) Delivery Systems

4.3.4 Rise of Personalized and Precision Medicine

4.3.5 Increasing Strategic Collaborations in RNA Therapeutics

4.4 Technology Landscape

4.4.1 mRNA Technologies

4.4.2 RNA Interference (RNAi) Technologies

4.4.3 Antisense Oligonucleotide (ASO) Technologies

4.4.4 Aptamer-Based Therapeutics

4.4.5 CRISPR and Gene Editing Integration

4.5 Delivery Technology Landscape (Critical Segment)

4.5.1 Lipid Nanoparticles (LNPs)

4.5.2 Polymer-Based Delivery Systems

4.5.3 Viral Vectors

4.5.4 Conjugate-Based Delivery (GalNAc, etc.)

4.5.5 Other Delivery Platforms

4.6 Regulatory and Clinical Landscape

4.6.1 FDA and EMA Approval Pathways

4.6.2 Clinical Trial Trends in RNA Therapeutics

4.6.3 Regulatory Guidelines for Gene-Based Therapies

4.7 Porter’s Five Forces Analysis

4.8 Value Chain & Ecosystem Analysis

4.8.1 Raw Material and Reagent Suppliers

4.8.2 RNA Therapeutics Developers

4.8.3 Contract Development & Manufacturing Organizations (CDMOs)

4.8.4 Clinical Research Organizations (CROs)

4.8.5 Healthcare Providers and Patients

4.9 Strategic Developments & Investment Landscape

4.9.1 Investments in RNA-Based Drug Development

4.9.2 Strategic Partnerships and Collaborations

4.9.3 Mergers and Acquisitions

4.9.4 Pipeline Expansion and Clinical Milestones

5. RNA Therapeutics Market, by Technology Type

5.1 Introduction

5.2 mRNA Therapeutics

5.2.1 Vaccines

5.2.2 Therapeutic Proteins

5.3 RNA Interference (RNAi)

5.3.1 siRNA

5.3.2 miRNA

5.4 Antisense Oligonucleotides (ASO)

5.5 Aptamer-Based Therapeutics

5.6 Other RNA Technologies

6. RNA Therapeutics Market, by Indication

6.1 Introduction

6.2 Oncology

6.3 Infectious Diseases

6.4 Rare Genetic Disorders

6.5 Cardiovascular Diseases

6.6 Neurological Disorders

6.7 Metabolic Disorders

6.8 Other Indications

7. RNA Therapeutics Market, by Delivery Platform

7.1 Introduction

7.2 Lipid Nanoparticles (LNPs)

7.3 Conjugate-Based Delivery (e.g., GalNAc)

7.4 Viral Vector-Based Delivery

7.5 Polymer-Based Delivery Systems

7.6 Other Delivery Platforms

8. RNA Therapeutics Market, by End User

8.1 Introduction

8.2 Hospitals and Clinics

8.3 Research Institutes and Academic Organizations

8.4 Pharmaceutical and Biotechnology Companies

8.5 Other End Users

9. RNA Therapeutics Market, by Geography

9.1 Introduction

9.2 North America

9.2.1 U.S.

9.2.2 Canada

9.3 Europe

9.3.1 Germany

9.3.2 U.K.

9.3.3 France

9.3.4 Italy

9.3.5 Spain

9.3.6 Switzerland

9.3.7 Sweden

9.3.8 Rest of Europe

9.4 Asia-Pacific

9.4.1 China

9.4.2 Japan

9.4.3 India

9.4.4 South Korea

9.4.5 Australia

9.4.6 Singapore

9.4.7 Rest of Asia-Pacific

9.5 Latin America

9.5.1 Brazil

9.5.2 Mexico

9.5.3 Argentina

9.5.4 Chile

9.5.5 Colombia

9.5.6 Rest of Latin America

9.6 Middle East & Africa

9.6.1 UAE

9.6.2 Saudi Arabia

9.6.3 South Africa

9.6.4 Israel

9.6.5 Turkey

9.6.6 Rest of Middle East & Africa

10. Competitive Landscape

10.1 Overview

10.2 Key Growth Strategies

10.3 Competitive Benchmarking

10.4 Competitive Dashboard

10.4.1 Industry Leaders

10.4.2 Market Differentiators

10.4.3 Vanguards

10.4.4 Emerging Companies

10.5 Market Ranking/Positioning Analysis of Key Players, 2025

11. Company Profiles

(Business Overview, Financial Overview, Pipeline/Products, Strategic Developments, SWOT Analysis)

11.1 Moderna, Inc.

11.2 BioNTech SE

11.3 CureVac N.V.

11.4 Alnylam Pharmaceuticals, Inc.

11.5 Ionis Pharmaceuticals, Inc.

11.6 Arrowhead Pharmaceuticals, Inc.

11.7 Regulus Therapeutics Inc.

11.8 Arbutus Biopharma Corporation

11.9 Translate Bio (Sanofi)

11.10 Sarepta Therapeutics, Inc.

11.11 Silence Therapeutics plc

11.12 Dicerna Pharmaceuticals (Novo Nordisk)

11.13 Beam Therapeutics Inc.

11.14 Intellia Therapeutics, Inc.

11.15 CRISPR Therapeutics AG

12. Appendix

12.1 Additional Customization

12.2 Related Reports

Published Date: Mar-2026

Published Date: Nov-2024

Published Date: Sep-2024

Published Date: Aug-2024

Published Date: Mar-2024

Subscribe to get the latest industry updates