Resources

About Us

Microbiome Therapeutics Market by Product Type (Live Biotherapeutic Products, Prebiotics & Synbiotics), Indication (Gastrointestinal Disorders, Oncology, CNS/Neurological Disorders), End-User, Technology (Next-Generation Sequencing, Metagenomics) - Global Forecast to 2036

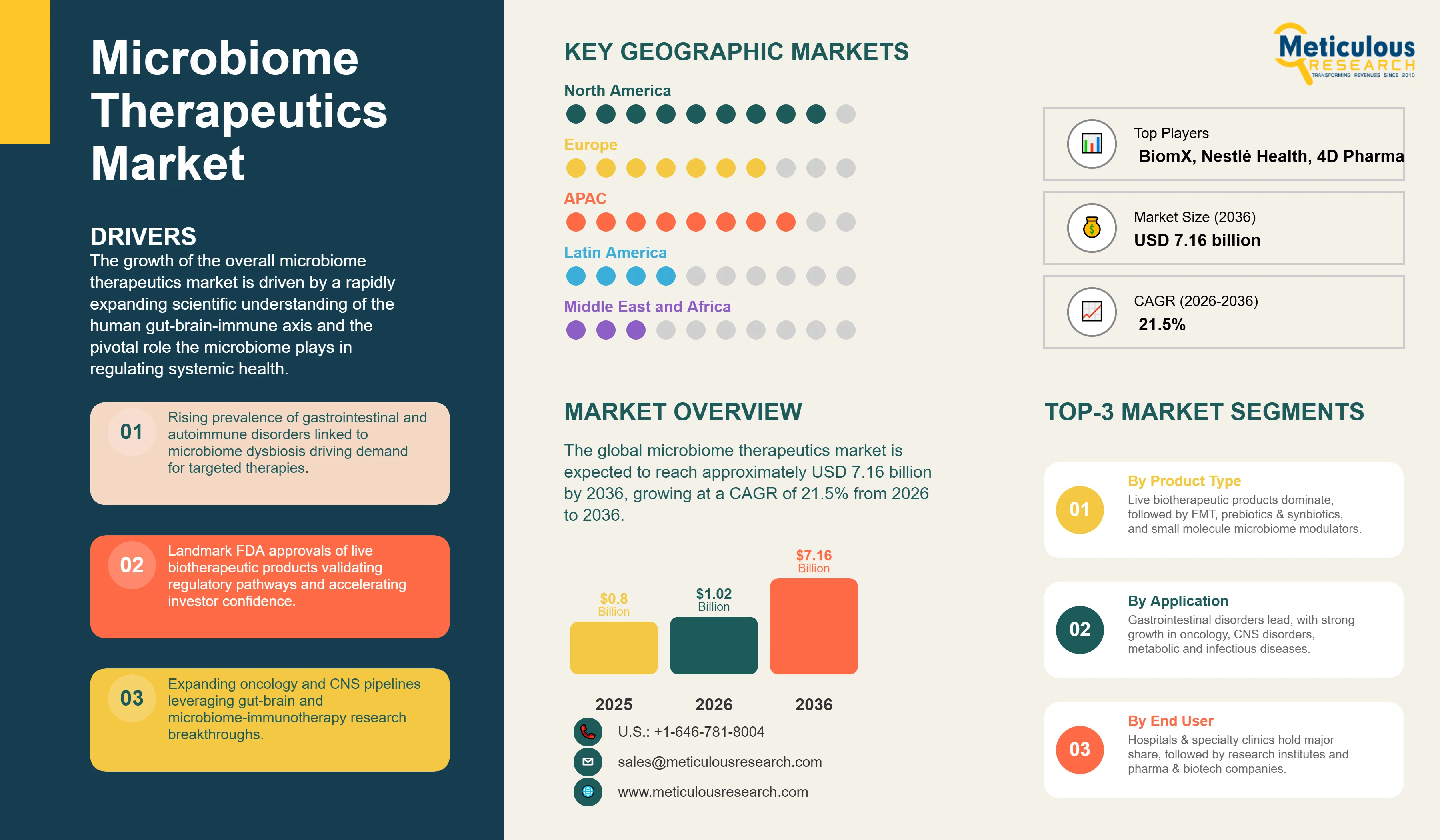

Report ID: MRHC - 1041825 Pages: 295 Mar-2026 Formats*: PDF Category: Healthcare Delivery: 24 to 72 Hours Download Free Sample ReportThe global microbiome therapeutics market was valued at USD 0.80 billion in 2025. The market is expected to reach approximately USD 7.16 billion by 2036 from USD 1.02 billion in 2026, growing at a CAGR of 21.5% from 2026 to 2036. The growth of the overall microbiome therapeutics market is driven by a rapidly expanding scientific understanding of the human gut-brain-immune axis and the pivotal role the microbiome plays in regulating systemic health. As biopharmaceutical companies and academic institutions accelerate translational research converting microbiome discoveries into clinically validated therapeutic candidates, the sector is witnessing unprecedented investment from both private venture capital and public funding agencies. The recent landmark regulatory approvals of live biotherapeutic products — including the first FDA-approved fecal microbiota products for recurrent Clostridioides difficile infection — have fundamentally validated the therapeutic approach and opened the commercial pathway for next-generation microbiome-based medicines targeting a broad spectrum of conditions from inflammatory bowel disease to oncology and neurological disorders.

Microbiome therapeutics encompass a diverse class of interventions designed to modulate the composition, diversity, and functional capacity of microbial communities — primarily the gut microbiome — to prevent, treat, or manage human disease. These products range from live biotherapeutic products (LBPs) containing defined microbial strains with demonstrated mechanisms of action, to fecal microbiota transplantation (FMT) procedures transferring complete donor microbiome ecosystems, prebiotic and synbiotic formulations selectively nourishing beneficial microbial populations, and small molecule drugs targeting host-microbiome signaling pathways. The market is characterized by sophisticated platforms integrating next-generation sequencing, metagenomics, and computational biology to identify disease-associated microbiome signatures, engineer targeted microbial therapies, and predict patient response based on baseline microbiome composition — collectively enabling precision medicine approaches unachievable with conventional pharmaceutical modalities.

The scientific foundation of microbiome therapeutics rests on compelling evidence linking dysbiosis — disruption of healthy microbial community structure — to a remarkably broad spectrum of diseases extending far beyond gastrointestinal conditions. Clinical and preclinical research has established microbiome involvement in immune system calibration, metabolic regulation, central nervous system function through the gut-brain axis, cancer immunotherapy response, and susceptibility to infectious diseases. This breadth of therapeutic opportunity creates multi-indication development strategies for leading companies, as core microbiome manufacturing and characterization platforms can be adapted across diverse disease areas. The convergence of advanced microbial genomics, anaerobic microbiology techniques enabling culture of previously unculturable gut anaerobes, and sophisticated regulatory frameworks specifically designed for LBPs creates a uniquely favorable environment for commercial translation.

The competitive landscape is bifurcated between pharmaceutical companies pursuing single-strain or defined-consortium LBPs with conventional drug development pathways — clinical trials, regulatory submissions, prescription distribution — and biotechnology innovators exploring FMT standardization, synthetic microbiome reconstruction, and engineered microbial strains with enhanced therapeutic properties including oxygen tolerance, targeted colonization, and programmable metabolite production. Strategic partnerships between large pharmaceutical corporations and specialized microbiome companies accelerate development timelines, providing manufacturing scale-up capabilities, regulatory expertise, and commercial infrastructure that early-stage microbiome startups typically lack. Simultaneously, the diagnostic microbiome market — companion diagnostics identifying patients likely to respond to specific microbiome interventions — represents rapidly growing complementary revenue opportunity reinforcing therapeutic product positioning.

Expansion Beyond Gastrointestinal Indications into Oncology and CNS Applications

The most transformative trend reshaping the microbiome therapeutics market is rapid pipeline expansion from gastrointestinal strongholds into oncology, neurology, and metabolic medicine. Landmark research demonstrating that gut microbiome composition profoundly influences response rates to immune checkpoint inhibitor therapies in melanoma, lung cancer, and renal cell carcinoma has catalyzed major pharmaceutical investment in microbiome-oncology combination programs. Companies including Seres Therapeutics, Microbiotica, and Vedanta Biosciences are pursuing clinical programs combining LBPs with PD-1/PD-L1 inhibitors, with preliminary evidence suggesting microbiome modulation can convert immunotherapy non-responders into responders — potentially expanding patient populations benefiting from immunotherapy by 20-40%. The gut-brain axis represents equally compelling territory, with clinical trials exploring microbiome interventions for Parkinson's disease, Alzheimer's disease, autism spectrum disorders, and treatment-resistant depression, based on mechanistic evidence that gut microbial metabolites including short-chain fatty acids, tryptophan derivatives, and enteroendocrine signaling molecules directly influence neuroinflammation, neurotransmitter synthesis, and blood-brain barrier integrity.

Regulatory Pathway Maturation and First-Generation Product Approvals Catalyzing Investment

The 2022-2023 FDA approvals of Rebyota (fexapotamide) from Ferring Pharmaceuticals and Vowst (formerly SER-109) from Seres Therapeutics represent watershed commercial milestones validating microbiome therapeutics as a legitimate pharmaceutical category rather than emerging science. These approvals established critical regulatory precedents — clinical trial endpoints, safety monitoring requirements, manufacturing standards for LBPs — that substantially reduce regulatory uncertainty for subsequent pipeline products. The FDA's framework for LBP development, outlined in industry guidance documents, clarifies the distinction between LBPs and conventional biologics, enabling developers to design fit-for-purpose clinical programs rather than adapting existing regulatory pathways imperfectly suited to living microbial medicines. European Medicines Agency and regulatory bodies in Japan, Australia, and China are developing analogous frameworks, creating global regulatory infrastructure supporting international market access for approved products. This maturation reduces investment risk sufficiently to attract major pharmaceutical companies previously observing from the periphery, dramatically increasing capital availability and partnership opportunities for pure-play microbiome biotechnology companies.

|

Market Size by 2036 |

USD 7.16 Billion |

|

Market Size in 2026 |

USD 1.02 Billion |

|

Market Size in 2025 |

USD 0.80 Billion |

|

Market Growth Rate (2026–2036) |

CAGR of 21.5% |

|

Dominating Region |

North America |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Product Type, Indication, End-User, Technology, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Drivers: Rising Prevalence of Gastrointestinal and Autoimmune Disorders

The primary driver of microbiome therapeutics market growth is the escalating global burden of conditions pathophysiologically linked to microbiome dysbiosis. Inflammatory bowel diseases — Crohn's disease and ulcerative colitis — affect over 10 million patients globally with incidence rising particularly in newly industrialized regions of Asia, Latin America, and the Middle East, where adoption of Western dietary patterns and antibiotic overuse are driving microbiome disruption at population scale. Clostridioides difficile infection causes approximately 500,000 cases and 30,000 deaths annually in the United States alone, with recurrence rates of 25-65% following antibiotic treatment representing a massive unmet need directly addressable by microbiome restoration therapies. Irritable bowel syndrome affects 10-15% of global population creating a large addressable market for microbiome-modulating interventions even before extending to systemic indications. Simultaneously, autoimmune diseases including rheumatoid arthritis, multiple sclerosis, and type 1 diabetes demonstrate compelling microbiome associations, expanding the potential patient population for microbiome therapeutics to hundreds of millions globally.

Opportunity: Precision Medicine Integration and Companion Diagnostics

The integration of microbiome diagnostics with therapeutic programs represents transformative commercial opportunity creating companion diagnostic-therapeutic product pairings analogous to oncology precision medicine paradigms. Companies developing microbiome characterization platforms capable of predicting patient response to specific microbial interventions — identifying the subset of IBD patients, cancer patients, or metabolic syndrome patients most likely to benefit from particular LBP compositions — create substantial competitive advantages through enriched clinical trial populations demonstrating superior efficacy signals, improved regulatory success rates, and premium pricing justification. The convergence of decreasing next-generation sequencing costs enabling routine clinical microbiome profiling, artificial intelligence platforms identifying complex microbiome biomarker signatures from large patient datasets, and increasing payer interest in precision medicine approaches reducing trial-and-error prescribing creates favorable market dynamics for integrated diagnostic-therapeutic platforms. Companies including Microba Life Sciences, uBiome's successor entities, and major clinical laboratory networks are building the commercial infrastructure for clinical microbiome testing, creating diagnostic market revenue while simultaneously generating the patient datasets necessary to refine therapeutic response prediction algorithms.

Why Do Live Biotherapeutic Products Lead the Market?

The live biotherapeutic products segment accounts for approximately 55-60% of total market revenue in 2026, reflecting the segment's combination of strongest clinical validation, regulatory framework clarity, and commercial product launches. LBPs — ranging from single well-characterized strains including Lactobacillus and Bifidobacterium species with clinical evidence in specific conditions, to complex defined consortia of 3-30 microbial strains designed to reconstitute specific functional niches in the dysbiotic microbiome — represent the segment most directly paralleling conventional pharmaceutical development paradigms. The recent commercial launches of Rebyota and Vowst in C. difficile infection demonstrate viable commercialization pathways and create market precedents informing reimbursement negotiations for subsequent LBPs. The pipeline breadth is substantial, with over 100 LBPs in clinical development targeting IBD, cancer, autoimmune disorders, metabolic diseases, and neurological conditions across multiple geographies. However, the FMT segment demonstrates the highest growth potential at approximately 22-25% CAGR, driven by expanding clinical evidence in conditions beyond C. difficile including IBD, graft-versus-host disease, and metabolic syndrome, concurrent with standardization efforts addressing the quality control and safety concerns that have historically limited FMT adoption to specialized centers.

How Does the Gastrointestinal Segment Maintain Dominance?

The gastrointestinal disorders segment represents approximately 60-65% of total microbiome therapeutics market in 2026, anchored by C. difficile infection (CDI) as the most clinically validated and commercially proven microbiome therapeutic indication. The compelling efficacy of microbiome restoration therapies in preventing CDI recurrence — with FMT demonstrating 80-90% success rates versus 30-40% for antibiotic retreatment — establishes an irrefutable clinical and economic case for microbiome intervention. IBD represents the second major gastrointestinal indication with multiple late-stage clinical programs exploring LBPs as induction and maintenance therapies, either as standalone treatments or combination partners for existing biologics and small molecules. Irritable bowel syndrome, small intestinal bacterial overgrowth, and antibiotic-associated diarrhea constitute additional GI indications with active development programs. The oncology segment demonstrates the highest projected growth at 25-28% CAGR, reflecting intense industry investment in microbiome-immunotherapy combination strategies following compelling clinical evidence that gut microbiome diversity and specific microbial signatures significantly predict and potentially modulate response to checkpoint inhibitor immunotherapy across multiple tumor types.

Why Do Hospitals & Clinics Command Market Leadership?

Hospitals and specialty clinics command approximately 65-70% of the microbiome therapeutics market in 2026, reflecting the prescription-only regulatory status of approved LBPs, the clinical supervision requirements for FMT procedures, and the concentration of specialized gastroenterology, oncology, and infectious disease practices within hospital settings. Academic medical centers and teaching hospitals are particularly important early adopters, combining clinical expertise in microbiome-associated conditions with research infrastructure enabling participation in clinical trials that generate real-world evidence supporting broader adoption. Inflammatory bowel disease centers, oncology departments initiating checkpoint inhibitor programs, and infectious disease specialists managing recurrent CDI represent the primary prescriber segments driving initial commercial uptake. Research institutes represent the fastest-growing end-user segment at 18-22% CAGR, as fundamental microbiome science continues advancing across academic institutions globally, fueling both basic science discovery pipelines and translational programs bridging laboratory findings to clinical candidates. Pharmaceutical and biotechnology companies constitute substantial end-users through contract manufacturing, formulation development, and analytical services supporting the growing LBP development pipeline.

How is Next-Generation Sequencing Transforming Microbiome Therapeutics?

Next-generation sequencing technologies — encompassing 16S rRNA amplicon sequencing for community profiling, whole-genome shotgun metagenomics for functional characterization, and metatranscriptomics for active metabolic pathway analysis — represent the foundational analytical infrastructure enabling microbiome therapeutics development. NGS platforms dominate the technology segment with approximately 45-50% market share, providing the microbiome characterization capabilities essential for patient stratification in clinical trials, quality control of LBP manufacturing processes, and identification of therapeutic targets through disease-microbiome association studies. Long-read sequencing technologies from Oxford Nanopore Technologies and Pacific Biosciences are increasingly enabling complete microbial genome assembly and real-time microbiome surveillance, enhancing resolution beyond short-read platforms. Metagenomics represents the second major technology segment, particularly valuable for functional microbiome profiling identifying metabolic pathways, antimicrobial resistance genes, and virulence factors rather than purely taxonomic community composition. Advanced microbial culture technology — specifically high-throughput anaerobic cultivation platforms enabling isolation and characterization of previously unculturable gut microbiome members — represents critical enabling technology for LBP development, with companies investing substantially in proprietary culture libraries providing competitive moats through access to unique microbial strains with validated therapeutic activities.

How is North America Maintaining Market Leadership?

North America holds approximately 48-52% of global microbiome therapeutics market in 2026, sustained by concentration of leading microbiome biotechnology companies, most advanced clinical pipeline globally, largest venture capital investment in the sector, and most mature regulatory framework for LBP development. The United States hosts the majority of Phase 2 and Phase 3 microbiome therapeutics trials globally, reflecting both scientific leadership at major academic medical centers and favorable FDA engagement with microbiome therapeutic development teams. Two commercial product launches — Rebyota and Vowst — represent North American first-mover advantages in the LBP commercial market, establishing reimbursement precedents and physician awareness ahead of competitors in other geographies. Canadian academic centers contribute significantly to global microbiome science, particularly at institutions including the University of Toronto, McMaster University, and University of Calgary which host internationally recognized microbiome research programs generating both basic science insights and clinical trial leadership.

Which Factors Drive Asia-Pacific's Rapid Growth?

Asia-Pacific demonstrates the highest regional growth rate at 22-25% CAGR, driven by China's aggressive national microbiome research investment, Japan's advanced clinical development programs paralleling Western pipeline development, South Korea's sophisticated biotechnology infrastructure pursuing microbiome commercialization, and India's large patient populations with high GI disease burden creating significant clinical opportunity. China's National Key R&D Program has designated microbiome research as a national priority, with substantial funding flowing to Chinese Academy of Sciences institutes, major medical universities, and domestic biotechnology companies developing microbiome therapeutics tailored to Asian gut microbiome compositions that differ meaningfully from Western populations. Japan's regulatory agency (PMDA) has developed specific guidance for microbiome therapeutics development aligned with international frameworks, enabling Japanese companies including Ajinomoto and academic spin-outs to pursue regulatory submissions for domestically developed LBPs. The regional market also benefits from high C. difficile infection burden in hospital settings with antibiotic overuse, strong consumer acceptance of probiotic products creating awareness of microbiome health concepts, and growing medical tourism infrastructure in Singapore, Thailand, and India supporting access to cutting-edge microbiome therapies.

The leading companies in the global microbiome therapeutics market include Seres Therapeutics, Inc. (SER-109/Vowst), Ferring Pharmaceuticals (Rebyota), Vedanta Biosciences, Inc. (VE303), and Finch Therapeutics Group, Inc. (CP101), which lead through clinically validated products, late-stage pipelines, and established manufacturing capabilities for complex microbial consortia. 4D Pharma plc, Evelo Biosciences, Inc., Assembly Biosciences, and Axial Therapeutics strengthen market presence through diverse therapeutic area pipelines spanning IBD, oncology, CNS, and infectious disease applications. Emerging players including Microbiotica Limited, Pendulum Therapeutics, Prolacta Bioscience, Eligo Bioscience (phage-based microbiome editing), and BiomX Inc. are advancing innovative platform technologies including synthetic microbiome reconstruction, targeted phage therapies, and engineered LBPs with enhanced colonization and therapeutic properties that differentiate from first-generation microbiome products. Major pharmaceutical companies including Nestlé Health Science, Johnson & Johnson, and Pfizer have established strategic partnerships and acquisitions to build microbiome capabilities, signaling the sector's maturation from niche biotechnology into mainstream pharmaceutical development.

The global microbiome therapeutics market is expected to grow from USD 1.02 billion in 2026 to USD 7.16 billion by 2036.

The global microbiome therapeutics market is projected to grow at a CAGR of 21.5% from 2026 to 2036.

Live biotherapeutic products dominate the market representing 55-60% of revenue as the most clinically validated product category with commercial approvals. However, FMT-based products demonstrate fastest growth at 22-25% CAGR driven by expanding indications and standardization initiatives.

Next-generation sequencing and metagenomics enable comprehensive microbiome profiling for patient stratification in clinical trials, quality control of LBP manufacturing, identification of therapeutic targets through disease association studies, and development of companion diagnostic tools predicting patient response to specific microbiome interventions.

North America holds 48-52% of global market driven by leading biotechnology companies, most advanced clinical pipeline, and first commercial LBP approvals. Asia-Pacific demonstrates fastest growth at 22-25% CAGR propelled by national research investment, large GI disease burden, and rapidly advancing regulatory frameworks.

The leading companies include Seres Therapeutics, Ferring Pharmaceuticals, Vedanta Biosciences, 4D Pharma, Evelo Biosciences, Assembly Biosciences, Microbiotica, and Finch Therapeutics, with major pharmaceutical companies including Nestlé Health Science, J&J, and Pfizer increasingly building microbiome capabilities through partnerships and acquisitions.

Published Date: Apr-2026

Published Date: Nov-2024

Published Date: Jan-2023

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates