Resources

About Us

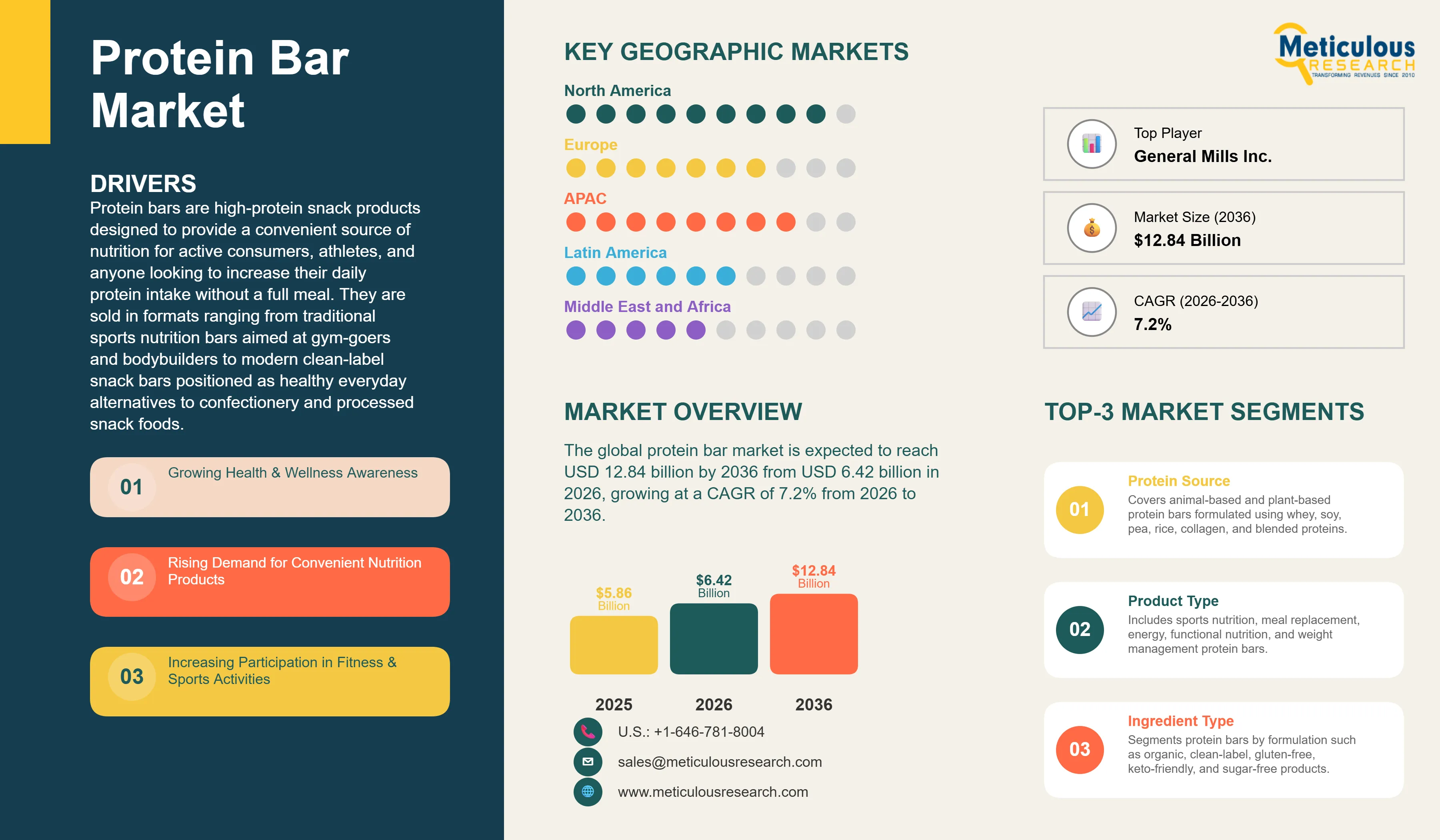

The global protein bar market was valued at USD 5.86 billion in 2025. This market is expected to reach USD 12.84 billion by 2036 from USD 6.42 billion in 2026, growing at a CAGR of 7.2% from 2026 to 2036.

Protein bars are high-protein snack products designed to provide a convenient source of nutrition for active consumers, athletes, and anyone looking to increase their daily protein intake without a full meal. They are sold in formats ranging from traditional sports nutrition bars aimed at gym-goers and bodybuilders to modern clean-label snack bars positioned as healthy everyday alternatives to confectionery and processed snack foods. The market has broadened significantly over the past decade as brands have moved beyond the niche sports nutrition channel into mass retail, convenience stores, and online subscription services, reaching a much wider consumer base.

The growth of this market is supported by clear and widely documented public health trends. According to the CDC, only one in four U.S. adults fully meets the physical activity guidelines for both aerobic and muscle-strengthening activity. The CDC notes that about one in two U.S. adults lives with a chronic disease and that getting enough physical activity could prevent many of these conditions. This large gap between recommended and actual physical activity levels creates a consumer base that is health-conscious but time-poor, making convenient, nutritious, on-the-go food products such as protein bars an appealing practical option. At the same time, CDC’s updated Adult Obesity Prevalence Maps (2024), every U.S. state and territory had an adult obesity prevalence of at least 25%, meaning at least one in four adults was living with obesity in each state. This drives growing consumer interest in high-protein snack products that support weight management and a higher-protein dietary approach.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Protein bars are manufactured food products containing elevated protein content, typically between 10 and 30 grams per bar, derived from one or more protein sources including whey, casein, soy, pea, rice, or collagen. They are sold in bar form as a portable, shelf-stable, and ready-to-eat alternative to other high-protein food sources such as chicken breast, eggs, or protein shakes. The product category spans a wide range of formulations and positioning, from high-protein, low-sugar sports performance bars aimed at competitive athletes through to more mainstream snack bars with 10 to 15 grams of protein that are positioned as a healthier alternative to candy bars and biscuits for everyday health-conscious consumers.

The category has gone through significant evolution over the past two decades. Early protein bars were heavily associated with bodybuilding and sports nutrition and were sold primarily through specialist supplement retailers. They were often criticized for poor taste, high sugar content, or the inclusion of artificial sweeteners and additives. The commercial breakthrough of brands including Quest Nutrition, which launched in 2010 with a formula based on high protein content, fiber, and minimal sugar using sugar alcohols as sweeteners, showed that consumers would prioritize nutritional profiles over traditional confectionery taste profiles. RXBAR's 2012 launch with a minimal ingredient list displayed prominently on the packaging established the clean-label format as a major commercial direction. These innovations shifted protein bars from a niche supplement product into a mainstream functional food category sold in supermarkets, convenience stores, and coffee chains alongside conventional snacks.

The competitive landscape of the protein bar market is a mix of large food companies that have entered through acquisition, specialist nutrition brands, and newer direct-to-consumer entrants. Mars Incorporated owns the ONE Bar and KIND Protein Bar brands. General Mills owns EPIC. Kellanova owns RXBAR. Nestle and Glanbia each have strong positions through their nutrition divisions. Quest Nutrition, the market leader by volume in the U.S. premium protein bar segment, is owned by The Simply Good Foods Company. Grenade from the UK and Barebells from Sweden have built strong brand followings in European markets and are expanding internationally. David Protein, founded in 2024 and positioning itself on an exceptionally high protein-to-calorie ratio, represents the newer generation of entrants competing aggressively on nutritional credentials rather than taste profile.

Plant-based Protein Bars Growing Rapidly as Consumer Diets Evolve

The shift toward plant-based protein sources in protein bars is one of the most commercially significant trends in the market. Growing numbers of consumers are adopting vegan, flexitarian, or reduced-meat diets for health, environmental, and ethical reasons, and they are looking for protein bar products that fit these dietary preferences without sacrificing protein content or taste quality. Pea protein has emerged as the leading plant-based protein ingredient in bars due to its relatively neutral flavor, high protein content of approximately 80% protein concentrate, and good amino acid profile. Brands including Aloha Foods, Garden of Life, and Orgain have built entire product lines around plant-based protein formulations. Established animal-protein-focused brands including Quest and Clif Bar have launched plant-based variants of their core products to retain consumers who are shifting their diets.

The market opportunity in plant-based protein bars is supported by consumer survey data and supermarket purchasing trends showing meaningful increases in plant-based food purchases. The WHO has consistently recommended that healthy diets include a variety of plant-based protein sources, and national dietary guidelines in several major markets have been updated in recent years to emphasize plant protein diversity. This institutional endorsement of plant-forward diets reinforces the commercial direction that protein bar brands are pursuing with their plant-based product development investment.

Clean-label and Minimal-ingredient Formats Reshaping the Category

Consumers are paying more attention to ingredient labels on food products than at any previous point, and protein bars are no exception to this scrutiny. The success of RXBAR, which displays its full ingredient list prominently on the front of the pack under the heading of what is in the bar and what is not, demonstrated that a significant segment of protein bar buyers will choose products based on ingredient transparency over taste or cost. This trend has pushed the entire category toward cleaner formulations, with brands removing artificial sweeteners such as sucralose and acesulfame potassium, synthetic colors, and preservatives from their formulations and replacing them with natural alternatives such as dates, honey, and natural flavor extracts. The regulatory environment supports this direction: the FDA's labeling requirements for food products require accurate declaration of all ingredients, and organic certification programs administered by the USDA under the National Organic Program provide a recognized standard for consumers seeking products made from organically grown ingredients. Brands that have invested in USDA Organic certification for their protein bar products can access a consumer segment willing to pay a meaningful premium for certified organic nutrition products.

|

Parameter |

Details |

|

Market Size by 2036 |

USD 12.84 Billion |

|

Market Size in 2026 |

USD 6.42 Billion |

|

Market Size in 2025 |

USD 5.86 Billion |

|

Market Growth Rate (2026-2036) |

CAGR of 7.2% |

|

Dominating Region |

North America |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Protein Source, Product Type, Ingredient Type, Distribution Channel, Application, End User, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Driver: Growing Consumer Focus on Health, Fitness, and High-protein Diets

The most important driver of the protein bar market is the growing number of consumers who are actively paying attention to their dietary protein intake and seeking convenient ways to meet their daily protein targets without cooking or meal preparation. According to the CDC's About Physical Activity page updated in August 2025, only one in four U.S. adults fully meets both the aerobic and muscle-strengthening components of the physical activity guidelines. The CDC's Active People, Healthy Nation initiative is working to help 27 million Americans become more physically active by 2027. As more people engage in strength training, running, cycling, and other fitness activities, awareness of protein's role in muscle repair, recovery, and maintenance increases, driving demand for convenient high-protein food products that can be consumed immediately after exercise or as part of a fitness-focused dietary routine.

The obesity data also supports this demand. According to the CDC's Adult Obesity Prevalence Maps updated in December 2025, in 2024 all U.S. states and territories had an adult obesity prevalence of 25% or higher, and at least one in five adults in every U.S. state is living with obesity. This large population of weight-management-focused consumers creates significant demand for protein-rich snack options that are more satiating than carbohydrate-heavy conventional snacks, support lean muscle mass during calorie-restricted diets, and fit into popular dietary frameworks including high-protein, low-carb, and ketogenic eating plans that have become mainstream consumer weight management approaches.

Opportunity: Direct-to-Consumer and Subscription Models Expanding Brand Reach

The continued growth of direct-to-consumer (DTC) e-commerce channels presents a significant opportunity for protein bar manufacturers to strengthen customer relationships, improve brand loyalty, and increase profit margins by reducing dependence on traditional retail channels. DTC platforms enable brands to collect valuable consumer insights, launch new products more efficiently, and offer personalized purchasing experiences. The increasing adoption of subscription-based purchasing models is further supporting recurring revenue streams and improving customer retention through scheduled product deliveries and loyalty programs.

The rapid expansion of online grocery and health-focused e-commerce is accelerating this trend. According to the U.S. Census Bureau, U.S. e-commerce sales exceeded USD 1.3 trillion in 2025, reflecting continued growth in online consumer purchasing. Leading protein bar brands, including Quest Nutrition, RXBAR, and David Protein, have leveraged DTC channels alongside retail distribution to expand market reach and engage directly with consumers. In addition, online marketplaces such as Amazon, brand-owned websites, and nutrition-focused subscription services provide emerging brands with cost-effective market access without the shelf-space constraints of traditional retail stores. The DTC model also supports product personalization through customized flavor assortments, variety packs, and targeted nutrition offerings, helping brands better align products with evolving consumer preferences.

Why Do Animal-based Protein Bars Lead the Market?

In 2026, the animal-based protein bars segment is expected to hold the largest share of the protein bar market. Whey protein, which is derived from milk as a byproduct of cheese production, is the most widely used ingredient in protein bars. It is valued by consumers and formulation scientists for its high protein concentration, complete amino acid profile including all nine essential amino acids, fast absorption rate that supports post-workout muscle recovery, and relatively neutral flavor that is easy to work with in bar formulations. Whey protein's decades of use in sports nutrition and the large body of research supporting its effectiveness for muscle protein synthesis have established it as the default protein source for sports nutrition bars. Major brands including Quest Nutrition, Grenade, and Barebells base their core products on whey protein or combinations of whey and casein. Casein protein, also derived from milk, is slower digesting than whey and is used in bars marketed for overnight muscle recovery or as a more sustained protein source between meals. Collagen protein, which has grown significantly in use as a functional protein ingredient in bars marketed for skin, hair, joint, and gut health, is another animal-based protein source gaining commercial traction outside traditional sports nutrition.

However, the plant-based protein bars segment is expected to witness the fastest growth during the forecast period. Pea protein, soy protein, rice protein, and blended plant protein formulations are being adopted by a growing range of brands serving vegan, flexitarian, and allergy-conscious consumers. Pea protein has become the most popular plant-based protein in bars because it provides high protein content, neutral flavor, and good texture in finished bars, with fewer allergen concerns than soy. Aloha Foods, Garden of Life, and Orgain are among the leading brands competing in this segment.

Why Do Sports Nutrition Bars Lead the Market?

In 2026, the sports nutrition bars segment is expected to hold the largest share of the protein bar market by product type. Sports nutrition bars were the original form of the protein bar category and continue to generate the largest revenue share through their strong presence in specialty nutrition retail, online sports nutrition channels, and gym retail. These products are typically formulated with 20 grams or more of protein, low sugar content, and specific macronutrient profiles designed to support athletic performance, muscle building, or post-exercise recovery. Quest Bar, the leading product in this segment in the U.S. market, built its reputation on a 20-gram protein, high-fiber, low-sugar formulation that appealed directly to gym-going consumers seeking a guilt-free high-protein snack. Grenade's Carb Killa bar has achieved a similar position in the UK and European markets.

However, the functional nutrition bars segment is expected to witness the fastest growth during the forecast period. Functional bars go beyond protein content to include additional active ingredients such as probiotics, adaptogens, collagen, vitamins, or botanical extracts that address specific health goals beyond muscle building. This product format is appealing to a broader consumer base that includes wellness-focused buyers who are not primarily motivated by sports performance but want their snacks to contribute to digestive health, stress management, skin health, or immune function. The functional bar format commands higher retail prices than standard sports bars, supporting revenue growth even at moderate volume growth rates.

How Do Conventional Protein Bars Lead the Market?

In 2026, the conventional protein bars segment is expected to hold the largest share of the protein bar market by ingredient type. Conventional protein bars using standard food-grade ingredients including whey protein concentrate, sugar alcohols such as maltitol and erythritol, artificial sweeteners, and standard binding agents represent the broadest product base in the market and include the highest-volume selling products including Quest Bar, ONE Bar, and Grenade Carb Killa. These products are widely available across all distribution channels and have the lowest retail price points within the protein bar category, making them accessible to the largest number of buyers.

However, the clean-label protein bars segment is expected to witness the fastest growth during the forecast period. Clean-label products that use short, transparent ingredient lists with recognizable whole food ingredients, and that avoid artificial sweeteners, synthetic preservatives, and modified food starches, are attracting the highest price premiums in the market and commanding premium shelf placement. The FDA's food labeling regulations require brands to list all ingredients in descending order of weight, enabling consumers to directly compare ingredient quality across products, which clean-label brands exploit commercially by making their short ingredient lists a front-of-pack marketing feature.

Why Do Supermarkets and Hypermarkets Lead the Market?

In 2026, the supermarkets and hypermarkets segment is expected to hold the largest share of the protein bar market by distribution channel. The expansion of protein bars from specialist nutrition retailers into mainstream supermarket shelves is one of the defining commercial developments of the past decade, bringing the category to the much larger consumer population that shops for everyday groceries at Walmart, Kroger, Tesco, Carrefour, and similar mass retail chains. Brands that achieved supermarket distribution including Quest, RXBAR, Kind, and Clif Bar accessed significantly larger consumer volumes than were available through specialist channels alone. Supermarket shelf placement in the snack or health food aisle puts protein bars in front of millions of shoppers who were not actively looking for a protein supplement product but find it a convenient and appealing snack option when confronted with it alongside conventional bars and biscuits.

However, the online retail and e-commerce segment is expected to witness the fastest growth during the forecast period. Online purchasing of protein bars is growing rapidly as consumers appreciate the price advantages of buying in bulk, the wider product variety available compared with physical retail, and the convenience of home delivery. Amazon is the largest single online retailer for protein bars in North America, and brand-owned DTC websites are growing in importance as brands invest in direct consumer relationships. Subscription box services for protein bars and nutrition products are also expanding. The FDA's food labeling requirements apply equally to online product listings, and brands selling through Amazon and other online platforms must ensure their product pages accurately reflect ingredients and nutritional content, maintaining the same transparency standards as physical retail.

Why Does Sports and Fitness Nutrition Lead the Application Market?

In 2026, the sports and fitness nutrition segment is expected to hold the largest share of the protein bar market by application. Protein bars were created for athletes and fitness enthusiasts and this consumer base remains the core of the market. According to the CDC's Active People, Healthy Nation initiative, the CDC is working to help 27 million additional Americans become more physically active by 2027, with physical activity participation already substantial across the U.S. population. Every person who participates in regular gym, running, cycling, or team sport activity is a potential consumer of sports nutrition bars as a convenient way to meet elevated protein requirements without meal preparation. The sports fitness application benefits from clear, well-understood consumer motivation: protein supports muscle recovery and growth, and bars provide that protein in a format that can be eaten immediately after a workout without refrigeration or preparation.

However, the general wellness and healthy snacking segment is expected to witness the fastest growth during the forecast period. The expansion of protein bars into mainstream snacking is converting a much larger population of non-athlete consumers who simply want a more nutritious, more satiating alternative to conventional biscuits, chocolate bars, and crisps. These consumers are not primarily motivated by sports performance but by general health consciousness, weight management interest, or a preference for snacks with a better nutritional profile. This broader wellness application represents a much larger potential consumer base than the sports nutrition segment alone, and brands that successfully position their products for everyday snacking rather than just post-workout use are accessing this larger opportunity.

Why Do Athletes and Bodybuilders Lead the End User Market?

In 2026, the athletes and bodybuilders segment is expected to hold the largest share of the protein bar market by end user. This group has the highest per-capita protein bar consumption, buys the most frequently, has the strongest brand loyalty to specialist sports nutrition brands, and is willing to pay the highest prices for products with strong nutritional credentials. Athletes and bodybuilders are also the most knowledgeable buyers, reading ingredient labels and nutritional panels carefully and making purchasing decisions based on protein content, amino acid profile, and macronutrient ratios. Their buying behavior is less sensitive to price per bar than other consumer segments, and they are more likely to purchase in bulk packs of 12, 24, or even larger box formats rather than single bars.

However, the lifestyle and wellness consumers segment is expected to witness the fastest growth during the forecast period. This is the largest and fastest-growing end-user group by head count, encompassing the broad population of health-conscious consumers who have begun eating protein bars as part of a general effort to improve their diet, manage their weight, or simply make better snacking choices. According to the CDC's obesity data, at least one in five adults in every U.S. state is living with obesity, and broader weight management interest extends well beyond the clinically obese population to a large group of consumers who are actively managing their diet and snack choices. This lifestyle wellness consumer group is accessible through supermarkets, convenience stores, online channels, and increasingly coffee shops and petrol station forecourts, making it the most commercially broad and commercially important growth end-user segment for the protein bar market over the forecast period.

How is North America Maintaining Market Leadership?

In 2026, North America is expected to hold the largest share of the global protein bar market. The United States is by far the largest individual market, with the highest per-capita consumption of protein bars globally, the most developed sports nutrition retail infrastructure, and the deepest brand portfolio in the category.

The U.S. market benefits from a large, fitness-conscious consumer population and a well-established retail ecosystem that includes specialist sports nutrition chains such as GNC and Vitamin Shoppe alongside mainstream supermarkets and convenience stores that carry a wide range of protein bar brands. According to the CDC, the CDC is actively working to increase physical activity participation among Americans through its Active People, Healthy Nation initiative targeting 27 million additional active Americans by 2027, and one in four U.S. adults currently meets the full physical activity guidelines for both aerobic and muscle-strengthening activity. The large and growing number of Americans who are engaged in regular physical activity, combined with the equally large number who are health-conscious but not currently meeting activity guidelines, collectively represents the largest national consumer base for protein bars globally. Canada contributes to regional demand through a similar fitness and health culture, with major U.S. protein bar brands widely available through Canadian retail channels.

Which Factors Drive Asia-Pacific's Rapid Growth?

Asia-Pacific is expected to witness the highest growth rate in the protein bar market during the forecast period. This growth is driven by rapidly expanding gym culture and fitness participation in China, India, South Korea, and Australia, rising disposable incomes among young urban consumers, and the growing availability of protein bar products through e-commerce platforms and modern retail formats.

China is the largest individual market in Asia-Pacific for protein bars, with a rapidly growing fitness and bodybuilding culture in major cities, a large young working population interested in health and wellness products, and major domestic e-commerce platforms providing easy access to both international and domestic protein bar brands. India's growing urban middle class, rapidly expanding gym network, and rising protein awareness among young consumers are creating a fast-growing protein supplement and protein snack market that international brands are beginning to address seriously. South Korea's highly developed health and beauty consumer culture, strong gym participation rates, and sophisticated e-commerce infrastructure make it one of the most commercially attractive markets in Asia-Pacific for premium protein bar brands. Australia has a well-established sports nutrition market with high per-capita fitness participation, and is a key market for brands including Grenade, Barebells, and international whey protein products.

Some of the key companies operating in the global protein bar market are Quest Nutrition, Mars Incorporated (ONE Brands, KIND Protein Bars), General Mills Inc. (EPIC Protein Bars), The Simply Good Foods Company (Quest and Atkins), Nestle S.A., Clif Bar and Company, Grenade (UK) Ltd., Barebells Functional Foods, BellRing Brands Inc., Glanbia plc, Herbalife Ltd., Abbott Laboratories, RXBAR (Kellanova), David Protein, and Aloha Foods Co.

The global protein bar market is expected to grow from USD 6.42 billion in 2026 to USD 12.84 billion by 2036.

The global protein bar market is projected to grow at a CAGR of 7.2% from 2026 to 2036.

Animal-based protein bars, particularly whey-based products, are expected to dominate the overall market in 2026. However, plant-based protein bars are expected to witness the fastest growth during the forecast period, driven by growing consumer adoption of vegan and flexitarian diets and improving product quality in pea, soy, and blended plant protein formulations.

The functional nutrition bars segment is expected to witness the fastest growth by product type, as brands add probiotics, adaptogens, collagen, and other active ingredients to command premium pricing from wellness-focused consumers. The clean-label protein bars segment is expected to witness the fastest growth by ingredient type, driven by growing consumer preference for products with short, transparent, whole-food ingredient lists.

Online retail and e-commerce is expected to witness the fastest growth during the forecast period, as subscription purchasing, bulk buying, and DTC brand strategies expand the online channel's share relative to traditional physical retail.

North America is expected to lead the global market in 2026, supported by the large U.S. sports nutrition consumer base and the CDC's documentation that one in four U.S. adults meets full physical activity guidelines with a much larger group health-conscious and actively managing their diet. Asia-Pacific is expected to witness the fastest CAGR, driven by rapidly growing fitness culture and rising health awareness in China, India, South Korea, and Australia.

The major players are Quest Nutrition, Mars (ONE Bar, KIND Protein), General Mills (EPIC), The Simply Good Foods Company, Nestle, Clif Bar, Grenade, Barebells, BellRing Brands, Glanbia, Herbalife, Abbott Laboratories, RXBAR (Kellanova), David Protein, and Aloha Foods.

1. Introduction

1.1 Market Definition (Protein Bars & High-Protein Nutrition Bars)

1.2 Scope (Sports Nutrition, Meal Replacement, Functional Nutrition, Healthy Snacking)

1.3 Market Ecosystem

1.4 Currency and Limitations

1.4.1 Currency

1.4.2 Limitations

1.5 Key Stakeholders

2. Research Methodology

2.1 Research Approach

2.2 Data Collection & Validation

2.2.1 Secondary Research

2.2.2 Primary Research (Manufacturers, Retailers, Nutrition Experts, Consumers)

2.3 Market Estimation

2.3.1 Bottom-Up Approach

2.3.2 Top-Down Approach

2.3.3 Forecast Modeling

2.4 Data Triangulation

2.5 Assumptions

3. Executive Summary

4. Market Overview

4.1 Introduction

4.2 Market Dynamics

4.2.1 Drivers

4.2.1.1 Growing Health & Wellness Awareness

4.2.1.2 Rising Demand for Convenient Nutrition Products

4.2.1.3 Increasing Participation in Fitness & Sports Activities

4.2.1.4 Growing Consumer Preference for High-Protein Diets

4.2.2 Restraints

4.2.2.1 High Product Prices Compared to Conventional Snacks

4.2.2.2 Taste and Texture Challenges

4.2.2.3 Regulatory Requirements for Health Claims

4.2.3 Opportunities

4.2.3.1 Growth of Plant-based Protein Bars

4.2.3.2 Expansion in Emerging Markets

4.2.3.3 Functional & Personalized Nutrition Trends

4.2.3.4 Clean-label and Organic Product Development

4.2.4 Challenges

4.2.4.1 Raw Material Price Volatility

4.2.4.2 Product Differentiation in a Competitive Market

4.3 Industry Trends

4.3.1 Rise of Plant-based Protein Bars

4.3.2 Sugar-free and Low-carb Formulations

4.3.3 Functional Ingredients (Collagen, Probiotics, Adaptogens)

4.3.4 Sustainable & Eco-friendly Packaging

4.3.5 Personalized Nutrition Products

4.4 Protein Bar Ecosystem

4.4.1 Ingredient Suppliers

4.4.2 Contract Manufacturers

4.4.3 Protein Bar Brands

4.4.4 Retailers & Distributors

4.4.5 End Consumers

4.5 Value Chain Analysis

4.5.1 Raw Material Procurement

4.5.2 Formulation & Product Development

4.5.3 Manufacturing & Packaging

4.5.4 Distribution & Retail

4.5.5 Consumer Purchase & Consumption

4.6 Regulatory Landscape

4.6.1 Food Safety Regulations

4.6.2 Nutritional Labeling Requirements

4.6.3 Protein Content & Health Claims Regulations

4.6.4 Organic & Clean-label Certifications

4.7 Pricing Analysis

4.7.1 Pricing by Protein Source

4.7.2 Premium vs Mass-market Products

4.7.3 Regional Pricing Trends

5. Protein Bar Market, by Protein Source

5.1 Introduction

5.2 Animal-based Protein Bars

5.2.1 Whey Protein Bars

5.2.2 Milk Protein Bars

5.2.3 Casein Protein Bars

5.2.4 Collagen Protein Bars

5.3 Plant-based Protein Bars

5.3.1 Soy Protein Bars

5.3.2 Pea Protein Bars

5.3.3 Rice Protein Bars

5.3.4 Mixed Plant Protein Bars

6. Protein Bar Market, by Product Type

6.1 Sports Nutrition Bars

6.2 Meal Replacement Bars

6.3 Energy Bars

6.4 Functional Nutrition Bars

6.5 Weight Management Bars

7. Protein Bar Market, by Ingredient Type

7.1 Conventional Protein Bars

7.2 Organic Protein Bars

7.3 Clean-label Protein Bars

7.4 Gluten-free Protein Bars

7.5 Keto-friendly Protein Bars

7.6 Sugar-free Protein Bars

8. Protein Bar Market, by Distribution Channel

8.1 Supermarkets & Hypermarkets

8.2 Convenience Stores

8.3 Specialty Nutrition Stores

8.4 Pharmacies & Drug Stores

8.5 Online Retail & E-commerce

8.6 Direct-to-Consumer (DTC)

9. Protein Bar Market, by Application

9.1 Introduction

9.2 Sports & Fitness Nutrition (Largest Segment)

9.3 Meal Replacement

9.4 Weight Management

9.5 General Wellness & Healthy Snacking

9.6 Clinical & Medical Nutrition

10. Protein Bar Market, by End User

10.1 Athletes & Bodybuilders

10.2 Fitness Enthusiasts

10.3 Weight Management Consumers

10.4 Lifestyle & Wellness Consumers

10.5 Medical & Clinical Nutrition Users

11. Protein Bar Market, by Geography

11.1 Introduction

11.2 North America

11.2.1 U.S.

11.2.2 Canada

11.3 Europe

11.3.1 Germany

11.3.2 U.K.

11.3.3 France

11.3.4 Italy

11.3.5 Spain

11.3.6 Netherlands

11.3.7 Rest of Europe

11.4 Asia-Pacific

11.4.1 China

11.4.2 Japan

11.4.3 India

11.4.4 Australia

11.4.5 South Korea

11.4.6 Southeast Asia

11.4.7 Rest of Asia-Pacific

11.5 Latin America

11.5.1 Brazil

11.5.2 Mexico

11.5.3 Argentina

11.5.4 Chile

11.5.5 Colombia

11.5.6 Peru

11.5.7 Rest of Latin America

11.6 Middle East & Africa

11.6.1 UAE

11.6.2 Saudi Arabia

11.6.3 South Africa

11.6.4 Rest of MEA

12. Competitive Landscape

12.1 Overview

12.2 Key Growth Strategies

12.3 Competitive Benchmarking

12.4 Competitive Dashboard

12.4.1 Market Leaders

12.4.2 Premium Brands

12.4.3 Emerging & Disruptive Brands

12.5 Market Share Analysis

12.6 Brand Positioning Analysis

13. Company Profiles

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

13.1 Quest Nutrition

13.2 Mars, Incorporated (ONE Brands, KIND Protein Bars)

13.3 General Mills, Inc. (EPIC Protein Bars)

13.4 The Simply Good Foods Company (Quest & Atkins)

13.5 Nestle S.A.

13.6 Clif Bar & Company

13.7 Grenade (UK) Ltd.

13.8 Barebells Functional Foods

13.9 BellRing Brands, Inc.

13.10 Glanbia plc

13.11 Herbalife Ltd.

13.12 Abbott Laboratories

13.13 RXBAR (Kellanova)

13.14 David Protein

13.15 Aloha Foods Co.

13.16 Other Companies

14. Appendix

14.1 Customization Options

14.2 Related Reports

Published Date: Mar-2026

Published Date: May-2025

Published Date: Feb-2025

Published Date: Jan-2025

Published Date: Aug-2024

Subscribe to get the latest industry updates