Resources

About Us

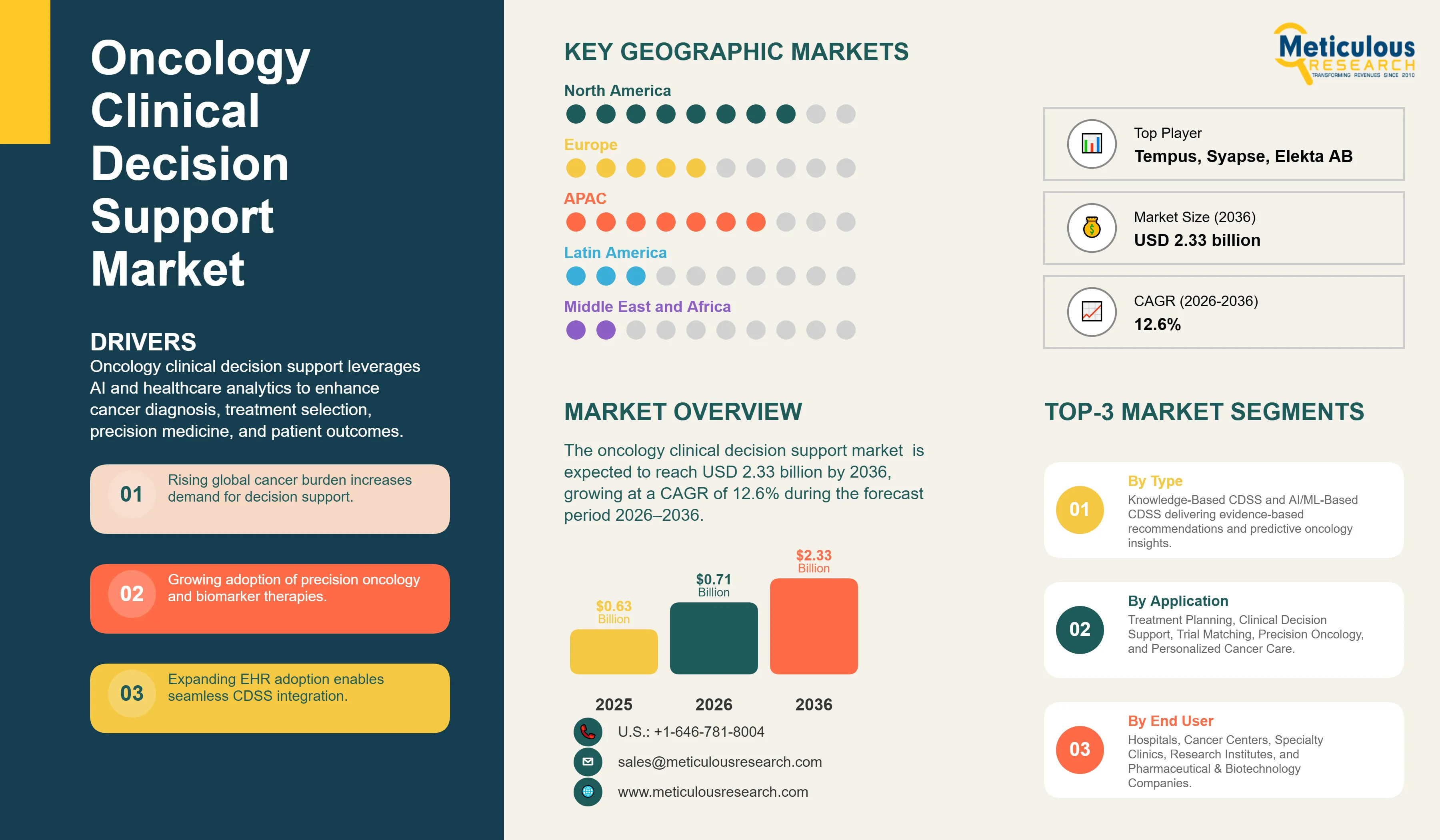

The global oncology clinical decision support market was valued at USD 0.71 billion in 2026. This market is expected to reach USD 2.33 billion by 2036, growing at a CAGR of 12.6% during the forecast period 2026–2036.

Market Overview and Insights

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global oncology clinical decision support market is experiencing a transformative evolution, driven by the convergence of advanced healthcare IT and rapid advancements in precision medicine. As the complexity of cancer care intensifies, oncology decision support systems have become indispensable tools for clinicians, enabling them to navigate the vast and continuously expanding landscape of clinical guidelines, genomic data, biomarker information, and therapeutic options. These systems leverage sophisticated algorithms to provide evidence-based recommendations, ensuring that cancer clinical decision support is integrated seamlessly into the physician's workflow. The market's robust growth is fundamentally anchored by the escalating global cancer burden. According to the International Agency for Research on Cancer, approximately 20 million new cancer cases and 9.7 million cancer-related deaths were reported globally in 2022, while the global cancer burden is projected to increase by 77% by 2050, reaching more than 35 million new cases annually. This rising disease burden, coupled with the increasing adoption of precision oncology and biomarker-driven therapies, is creating significant demand for advanced clinical decision support solutions that can assist clinicians in delivering personalized cancer care.

The integration of AI in oncology is a primary catalyst for market expansion, enabling the interpretation of complex multi-omics data that was previously beyond the reach of manual analysis. Oncology decision support software now incorporates machine learning models that can predict treatment responses and toxicity risks with high accuracy. Precision oncology decision support tools are particularly critical in the era of targeted therapies, where matching a patient's unique genetic profile to the most effective drug is paramount. By reducing diagnostic errors and improving adherence to clinical guidelines by over 30%, these systems are significantly enhancing patient outcomes and reducing the overall cost of cancer care.

Technological innovation is further stimulated by the shift toward cloud-based SaaS models, which offer the scalability and interoperability needed for modern cancer treatment decision support. While knowledge-based systems following established clinical pathways remain the current standard, the fastest growth is observed in non-knowledge based systems that utilize deep learning to uncover novel clinical insights. The competitive landscape is characterized by the presence of global tech giants and specialized oncology informatics firms, all of whom are investing heavily in interoperable platforms that can aggregate data from diverse sources, including EMRs, pathology reports, and liquid biopsy results.

Geographically, North America leads the global market in 2026. This dominance is driven by high healthcare IT spending, a robust ecosystem of oncology research, and favorable government policies promoting the use of digital health tools. However, the Asia-Pacific region is projected to witness the fastest growth, as countries like China and India rapidly modernize their healthcare infrastructure and adopt AI-driven solutions to manage their massive cancer burdens. As precision medicine becomes the standard of care, the oncology clinical decision support market is poised for sustained, double-digit growth through 2036.

The primary driver for the oncology clinical decision support market is the increasing complexity of cancer treatment pathways, which increasingly rely on biomarker-driven therapies, companion diagnostics, immunotherapies, and precision medicine approaches. According to the International Agency for Research on Cancer, approximately 20 million new cancer cases and 9.7 million cancer-related deaths were reported globally in 2022, while the global cancer burden is projected to increase by 77% by 2050, reaching more than 35 million new cases annually. As oncology care becomes more personalized, clinicians must evaluate growing volumes of genomic, clinical, and treatment data, creating significant demand for advanced clinical decision support tools.

Furthermore, the widespread adoption of electronic health records (EHRs) has established the digital infrastructure necessary for CDSS deployment. According to the Office of the National Coordinator for Health Information Technology, nearly 96% of non-federal acute care hospitals and approximately 78% of office-based physicians in the United States have adopted certified EHR systems. Government initiatives supporting precision medicine and healthcare digitalization are also accelerating market growth. For example, the National Institutes of Health continues to invest through programs such as the All of Us Research Program, which has enrolled more than 1 million participants to advance personalized healthcare and precision medicine. The growing need to improve diagnostic accuracy, treatment selection, and patient safety in oncology is driving the widespread implementation of clinical decision support solutions across healthcare systems.

Restraint

A major restraint is the high initial cost and technical complexity of implementing advanced oncology decision support software, which can be prohibitive for smaller community oncology practices. Concerns regarding data privacy and the security of sensitive patient and genomic information also pose significant challenges. Furthermore, the lack of standardized interoperability across different healthcare IT platforms can hinder the seamless exchange of data, limiting the effectiveness of decision support tools in multidisciplinary care settings.

Significant opportunities exist in the integration of multi-omics data—including genomics, proteomics, and metabolomics—into cancer treatment decision support platforms. The expansion of these tools into emerging markets, where healthcare infrastructure is rapidly digitizing, presents a massive growth path. Furthermore, the development of clinical trial matching algorithms that can connect patients with appropriate trials in real-time offers high potential for both clinical research and pharmaceutical development. The use of AI to predict long-term survivorship and manage post-treatment care also represents a major unmet need.

A key challenge is overcoming physician skepticism and 'alert fatigue,' which can occur if decision support tools are not seamlessly integrated into clinical workflows or if they provide excessive or irrelevant notifications. Ensuring the clinical validity and transparency of AI-driven 'black box' algorithms is also critical for gaining clinician trust. Furthermore, manufacturers must navigate the complex and evolving regulatory landscapes for medical software and prove the long-term cost-effectiveness of their systems to secure broad adoption and reimbursement.

There is a clear trend toward the adoption of cloud-based oncology decision support software, which offers lower upfront costs and easier integration with diverse data sources. This model allows for real-time updates to clinical guidelines and provides the scalability needed to manage the massive volumes of data generated in modern cancer care.

The integration of AI in oncology is no longer a futuristic concept but a practical necessity. Machine learning models are being increasingly used to identify 'super-responders' and predict adverse events, enabling a level of precision in cancer treatment decision support that was previously unattainable. This trend is driving a wave of innovation in non-knowledge based systems that can uncover hidden patterns in clinical data.

Based on product, the market is segmented into On-premise Software, Cloud-based Software, and Services. In 2026, the Cloud-based Software segment is expected to hold the largest share of the market. This dominance is driven by the scalability, ease of implementation, and lower total cost of ownership associated with SaaS models, making them the preferred choice for modern oncology practices.

The Cloud-based Software segment is also projected to witness the fastest growth during the forecast period, as more institutions move away from legacy on-premise systems to more flexible and interoperable digital platforms.

Based on type, the market is segmented into Knowledge-Based CDSS and Non-Knowledge Based CDSS (AI/ML). In 2026, the Knowledge-Based CDSS segment is expected to hold the largest share of the market. These systems, which utilize rule-based algorithms following established clinical guidelines like NCCN, are the current standard of care and provide a high degree of transparency.

The Non-Knowledge Based CDSS (AI/ML) segment is projected to witness the fastest growth. As the volume of genomic data increases, the need for machine learning models that can interpret complex biological patterns is becoming critical for precision oncology.

North America is expected to hold the largest share of the global oncology clinical decision support market in 2026, accounting for approximately 48% of the total revenue. This is due to high healthcare IT spending, a robust ecosystem of oncology research, and the presence of major industry players like Oracle, IBM (Merative), and Epic. The region's early adoption of precision medicine and favorable regulatory environment are also key drivers.

Asia-Pacific is projected to witness the fastest growth during the forecast period. The region is modernizing its healthcare infrastructure at an unprecedented pace, with countries like China and India investing heavily in AI-driven healthcare solutions. The rising incidence of cancer and the need for efficient data management in large-scale clinical settings are the primary growth drivers. Key companies operating in the Asia-Pacific market include major global vendors and emerging local tech firms.

The global oncology clinical decision support market is characterized by intense competition between global healthcare IT giants and specialized oncology informatics firms. Oracle (Cerner) and IBM (Merative) maintain a strong presence through their comprehensive EHR-integrated platforms, while firms like Flatiron Health (Roche) and Tempus lead the way in data-driven precision oncology. Competition is focused on interoperability, the clinical validity of AI models, and the ability to provide actionable insights at the point of care.

Strategic partnerships between software vendors and diagnostic companies are critical for integrating genomic and pathology data into decision support platforms. Companies are also investing in cloud-native architectures to improve the speed and scalability of their offerings. Key players in the global market include IBM Corporation (Merative), Oracle Corporation (Cerner), Flatiron Health (Roche), Tempus, GE HealthCare, Siemens Healthineers (Varian), Philips Healthcare, Elekta AB, Epic Systems, and Wolters Kluwer Health.

The market is projected to reach USD 2.33 million by 2036, growing at a CAGR of 12.6% from 2026 to 2036.

AI enables the interpretation of complex genomic data and predicts treatment responses, allowing for more precise and personalized care.

Cloud-based software offers lower upfront costs, real-time updates, and the scalability needed for modern data-heavy cancer care.

The Asia-Pacific region is projected to witness the fastest growth due to rapid modernization and adoption of AI healthcare.

By improving therapy matching and avoiding ineffective treatments, these systems can reduce overall cancer care costs by 15-20%.

The market is expected to grow at a CAGR of 12.6% during the forecast period 2026–2036.

Knowledge-based CDSS, which utilizes rule-based clinical guidelines, currently holds the largest share.

The high implementation cost and technical complexity are the main restraints for smaller oncology practices.

It matches a patient's genetic profile to the most effective targeted therapies, optimizing treatment outcomes.

The market is led by Oracle (Cerner), IBM (Merative), Flatiron Health, Tempus, and GE HealthCare.

1. Market Definition & Scope

1.1. Market Definition

1.2. Market Ecosystem

1.3. Currency Considered

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Process of Data Collection and Validation

2.2.1. Secondary Research

2.2.2. Primary Research/Interviews with Key Opinion Leaders

2.3. Market Sizing and Forecast

2.3.1. Market Size Estimation Approach

2.3.1.1. Bottom-Up Approach

2.3.1.2. Top-Down Approach

2.3.2. Growth Forecast Approach

2.3.3. Assumptions for the Study

3. Executive Summary

3.1. Overview

3.2. Segmental Analysis

3.2.1. Market Analysis, by Product & Service

3.2.2. Market Analysis, by Type

3.2.3. Market Analysis, by Application

3.2.4. Market Analysis, by End User

3.2.5. Market Analysis, by Geography

3.3. Competitive Analysis

4. Market Insights

4.1. Overview

4.2. Factors Affecting Market Growth

4.2.1. Drivers

4.2.1.1. Rising Complexity of Cancer Treatment Pathways and Personalized Medicine

4.2.1.2. Rapid Adoption of EHR/EMR Systems and Foundational Digital Health Infrastructure

4.2.1.3. Government Initiatives and Funding for Precision Oncology and Health IT

4.2.2. Restraints

4.2.2.1. High Implementation Costs and Technical Complexity for Smaller Practices

4.2.2.2. Data Privacy and Security Concerns Regarding Sensitive Genomic Information

4.2.3. Opportunities

4.2.3.1. Integration of Multi-Omics Data for Superior Clinical Decision Support

4.2.3.2. Expansion of AI-Driven Tools into Rapidly Modernizing Emerging Markets

4.2.4. Challenges

4.2.4.1. Overcoming Physician Skepticism and 'Alert Fatigue' in Clinical Workflows

4.2.4.2. Navigating Complex and Evolving Global Regulatory Landscapes for Medical Software

4.2.5. Trends

4.2.5.1. Shift Toward Cloud-Based SaaS Models for Scalability and Interoperability

4.2.5.2. Increasing Use of AI to Identify 'Super-Responders' and Predict Adverse Events

4.3. Porter’s Five Forces Analysis

4.4. Regulatory Landscape

4.5. Value Chain Analysis

5. Global Oncology Clinical Decision Support Market, by Product & Service

5.1. Overview

5.2. Software

5.2.1. On-premise Software

5.2.2. Cloud-based Software (SaaS)

5.3. Services

5.3.1. Consulting & Implementation

5.3.2. Training & Maintenance

6. Global Oncology Clinical Decision Support Market, by Type

6.1. Overview

6.2. Knowledge-Based CDSS

6.3. Non-Knowledge Based CDSS (AI/ML)

7. Global Oncology Clinical Decision Support Market, by Application

7.1. Overview

7.2. Diagnosis & Screening Support

7.3. Treatment Planning

7.4. Drug Dosing & Management

7.5. Clinical Trial Matching

7.6. Others

8. Global Oncology Clinical Decision Support Market, by End User

8.1. Overview

8.2. Hospitals & Specialty Clinics

8.3. Research Institutes & Academic Centers

8.4. Pharmaceutical & Biotech Companies

9. Global Oncology Clinical Decision Support Market, by Geography

9.1. Overview

9.2. North America

9.2.1. U.S. (Stats: ~48% Global Market Share)

9.2.2. Canada

9.3. Europe

9.3.1. Germany (Stats: Strong Focus on Digital Health and Cancer Research)

9.3.2. U.K. (Stats: NHS Investment in AI for Oncology Care)

9.3.3. France

9.3.4. Netherlands

9.3.5. Italy

9.3.6. Rest of Europe

9.4. Asia-Pacific

9.4.1. China (Stats: Fastest Growth Due to Heavy Investment in AI Healthcare)

9.4.2. Japan

9.4.3. India

9.4.4. South Korea

9.4.5. Rest of Asia-Pacific

9.5. Latin America

9.5.1. Brazil

9.5.2. Mexico

9.5.3. Rest of Latin America

9.6. Middle East & Africa

10. Competitive Landscape

10.1. Overview

10.2. Key Growth Strategies

10.3. Competitive Dashboard

10.4. Vendor Market Positioning

10.5. Market Share Analysis, 2025

11. Company Profiles

11.1. IBM Corporation (Merative)

11.2. Oracle Corporation (Cerner)

11.3. Flatiron Health (Roche)

11.4. Tempus

11.5. GE HealthCare Technologies Inc.

11.6. Siemens Healthineers AG (Varian)

11.7. Philips Healthcare

11.8. Elekta AB

11.9. Epic Systems Corporation

11.10. McKesson Corporation

11.11. Wolters Kluwer Health

11.12. Elsevier (ClinicalKey)

11.13. ZS Associates

11.14. SOPHiA GENETICS

11.15. Syapse

12. Appendix

Published Date: Apr-2026

Published Date: Mar-2026

Published Date: Feb-2026

Published Date: Jan-2025

Published Date: Jun-2024

Subscribe to get the latest industry updates