Resources

About Us

Precision Oncology Market by Component (Diagnostics & Biomarker Testing, Targeted Therapies), Technology, Cancer Type (Non-Small Cell Lung Cancer, Breast Cancer, Colorectal Cancer, Melanoma, Leukemia & Lymphoma), End-User - Global Forecast to 2036

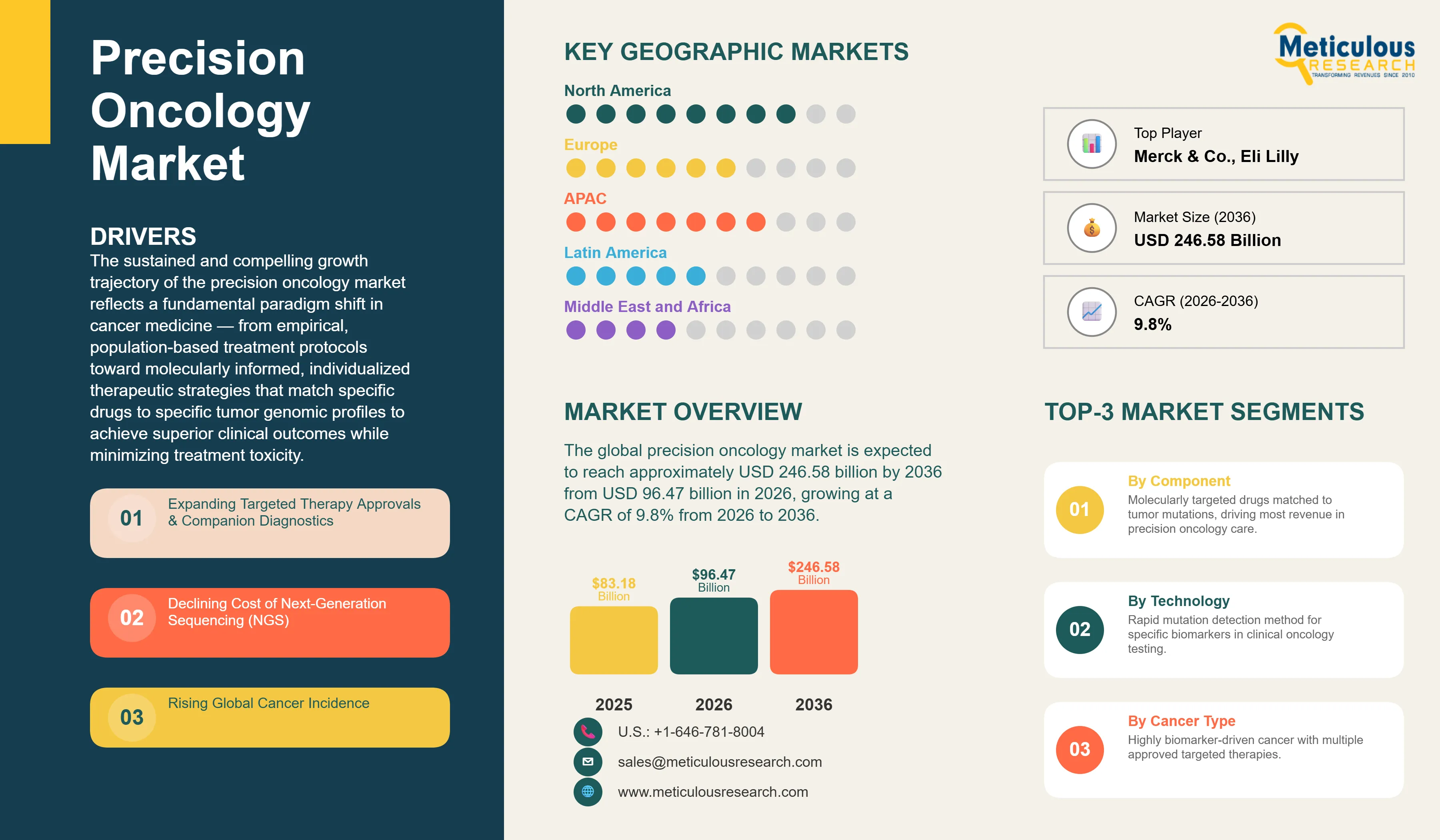

Report ID: MRHC - 1041829 Pages: 288 Mar-2026 Formats*: PDF Category: Healthcare Delivery: 24 to 72 Hours Download Free Sample ReportThe global precision oncology market was valued at USD 83.18 billion in 2025. The market is expected to reach approximately USD 246.58 billion by 2036 from USD 96.47 billion in 2026, growing at a CAGR of 9.8% from 2026 to 2036. The sustained and compelling growth trajectory of the precision oncology market reflects a fundamental paradigm shift in cancer medicine — from empirical, population-based treatment protocols toward molecularly informed, individualized therapeutic strategies that match specific drugs to specific tumor genomic profiles to achieve superior clinical outcomes while minimizing treatment toxicity. Precision oncology integrates comprehensive genomic profiling of tumor and germline DNA, RNA expression analysis, proteomic characterization, and increasingly epigenomic and metabolomic data into a multi-dimensional molecular portrait of each patient's cancer that guides selection among an expanding arsenal of targeted therapies, checkpoint immunotherapy combinations, and antibody-drug conjugates designed to exploit specific molecular vulnerabilities. The convergence of next-generation sequencing cost reductions — with comprehensive tumor profiling costs declining from tens of thousands to hundreds of dollars over the past decade — rapidly expanding FDA and EMA approvals of companion diagnostic-linked targeted therapies, and the demonstrated superiority of biomarker-selected patient populations in clinical trial outcomes has transformed precision oncology from an academic aspiration into the dominant commercial paradigm driving pharmaceutical R&D investment, oncology practice guidelines, and healthcare reimbursement policy globally. AI-driven drug discovery platforms, liquid biopsy technologies enabling non-invasive tumor genomic monitoring, and the first generation of tumor-agnostic therapies approved based on molecular biomarkers rather than tissue of origin collectively demonstrate how rapidly the precision oncology landscape continues to evolve beyond its already transformative initial impact on cancer treatment outcomes.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Precision oncology represents the clinical application of genomic, molecular, and increasingly multi-omic data to individualize cancer treatment decisions, replacing the traditional approach of selecting therapy primarily based on cancer tissue of origin and histological subtype with a molecularly informed strategy that matches patients to therapies based on the specific genetic alterations driving their tumor's growth and survival. The conceptual foundation of precision oncology rests on the recognition that cancers of the same tissue type — for example, lung adenocarcinomas — are actually diverse collections of molecularly distinct diseases unified by organ location but driven by heterogeneous genetic alterations with fundamentally different drug sensitivities and clinical behaviors. By characterizing these molecular differences through comprehensive biomarker testing, oncologists can select therapies with dramatically higher probability of benefit for genomically defined patient subgroups — exemplified by EGFR-mutated NSCLC patients who achieve progression-free survival of 18-24 months on osimertinib versus 8-12 months on platinum-based chemotherapy, or HER2-positive breast cancer patients for whom trastuzumab-based regimens transformed a previously poor-prognosis subtype into one with excellent long-term outcomes.

The precision oncology ecosystem encompasses the full value chain from biomarker discovery through therapeutic development and clinical deployment. The diagnostic component — spanning next-generation sequencing-based comprehensive genomic profiling, liquid biopsy assays detecting circulating tumor DNA, immunohistochemistry and fluorescence in situ hybridization for protein expression and gene rearrangement detection, and increasingly digital pathology platforms applying AI to predict molecular phenotypes from tissue morphology — generates the molecular intelligence that drives treatment selection decisions. The therapeutic component encompasses the rapidly expanding portfolio of targeted agents including tyrosine kinase inhibitors, PARP inhibitors, CDK inhibitors, KRAS inhibitors, antibody-drug conjugates, bispecific antibodies, and cancer vaccines, alongside the immuno-oncology agents including checkpoint inhibitors and cellular therapies that are increasingly deployed in biomarker-selected populations for optimal benefit. The data analytics and software component — encompassing clinical decision support platforms, genomic data interpretation tools, AI-powered drug response prediction systems, and real-world evidence platforms aggregating treatment outcomes across large patient populations — enables clinicians to navigate the exponentially expanding landscape of biomarker-therapy associations and translate genomic findings into actionable treatment recommendations.

The regulatory evolution enabling precision oncology commercialization has been as consequential as scientific advances. FDA's approval of pembrolizumab for TMB-high solid tumors in 2020 and larotrectinib for NTRK-fusion solid tumors established the tumor-agnostic indication paradigm — approving therapies based on molecular biomarkers present across cancer types rather than within a specific tissue of origin — representing a fundamental reorientation of oncology drug development and regulatory review toward biomarker-centric approval pathways. FDA's Breakthrough Therapy and Accelerated Approval designations have substantially compressed development timelines for precision oncology drugs with compelling early clinical data in biomarker-selected populations, with median approval times of 5.2 years for breakthrough-designated oncology agents compared to 8.1 years for standard-reviewed drugs. Companion diagnostic co-development and co-approval frameworks — requiring FDA approval of a specific diagnostic test as a prerequisite for prescribing the linked therapy — have created tight commercial integration between diagnostic and therapeutic companies, driving co-development partnerships and acquisitions that are reshaping the competitive landscape across both sectors.

Liquid Biopsy Transforming Tumor Genomic Monitoring from Invasive to Longitudinal

Liquid biopsy — the analysis of circulating tumor DNA, circulating tumor cells, exosomes, and other tumor-derived materials shed into peripheral blood — is emerging as one of the most transformative technology trends in precision oncology, enabling non-invasive genomic profiling of tumor molecular status that can be performed serially throughout the treatment course without the procedural complexity, cost, and sampling bias limitations of tissue biopsy. The clinical utility of liquid biopsy spans multiple precision oncology applications: initial tumor molecular profiling from plasma ctDNA analysis when tissue biopsy is inadequate or inaccessible, minimal residual disease detection following curative-intent surgery identifying patients at high risk of recurrence who require adjuvant therapy intensification, early detection of acquired resistance mutations enabling treatment adaptation before radiographic progression, and therapy response monitoring through ctDNA quantitative changes that precede imaging-detectable tumor burden changes by weeks to months. Guardant Health's Guardant360 CDx — approved as a companion diagnostic for multiple targeted therapies — and Foundation Medicine's FoundationOne Liquid CDx have established the commercial liquid biopsy market in companion diagnostic applications, while the emerging early cancer detection segment — exemplified by Grail's Galleri multi-cancer early detection test and Exact Sciences' Oncotype platform — potentially extends liquid biopsy utility to population-scale cancer screening where its minimally invasive nature enables compliance at scales impossible for tissue-based screening approaches. The technical evolution of liquid biopsy — with digital PCR, error-corrected next-generation sequencing, and methylation-based cancer signal detection achieving sensitivity for ctDNA fractions below 0.1% — continues expanding the clinical scenarios where liquid biopsy provides actionable information, with multi-analyte platforms simultaneously characterizing DNA mutations, copy number alterations, methylation patterns, and protein biomarkers from single blood draws approaching the comprehensive molecular characterization previously requiring fresh tissue samples.

AI and Machine Learning Revolutionizing Biomarker Discovery and Drug Development

The application of artificial intelligence and machine learning across the precision oncology value chain — from genomic data interpretation through clinical trial design, drug target identification, and treatment outcome prediction — is accelerating the pace of biomarker discovery and therapeutic development while enabling clinical translation of molecular complexity that exceeds human analytical capacity. Deep learning algorithms applied to digital pathology whole-slide images are demonstrating remarkable capability to predict molecular subtypes, tumor mutational burden, microsatellite instability status, and genomic alterations from hematoxylin and eosin stained tissue sections alone — potentially enabling precise molecular stratification from routine pathology without specialized molecular testing for certain applications. Companies including PathAI, Paige.AI, Owkin, and Tempus are commercializing AI pathology platforms that predict clinically actionable biomarker status from tissue morphology, with multiple FDA breakthrough designations and marketing authorizations for AI-based pathology applications validating regulatory acceptance of this technology paradigm. In drug discovery, AI platforms from companies including Recursion Pharmaceuticals, BenevolentAI, Exscientia, and Insilico Medicine are applying deep learning to multi-omic cancer datasets identifying novel drug targets, predicting drug-target interactions, and designing optimized molecular structures — dramatically compressing the pre-clinical drug discovery phase from years to months while simultaneously exploring vastly larger chemical space than conventional medicinal chemistry approaches can address. Real-world evidence platforms aggregating genomic and clinical data from tens of thousands of cancer patients — including Foundation Medicine's clinical genomics database, Tempus's multimodal oncology data platform, and Flatiron Health's electronic health record-derived real-world oncology database — provide unprecedented statistical power to identify biomarker-outcome associations that are not detectable in the smaller randomized controlled trial populations on which regulatory approvals are based.

|

Parameter |

Details |

|

Market Size by 2036 |

USD 246.58 Billion |

|

Market Size in 2026 |

USD 96.47 Billion |

|

Market Size in 2025 |

USD 83.18 Billion |

|

Market Growth Rate (2026-2036) |

CAGR of 9.8% |

|

Dominating Region |

North America |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Component, Technology, Cancer Type, End-User, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Drivers: Expanding Targeted Therapy Approvals and Companion Diagnostic Ecosystem

The primary market driver for precision oncology is the exponential expansion of FDA and EMA-approved targeted therapies linked to specific companion diagnostics, creating a self-reinforcing cycle where each new approval drives biomarker testing adoption which in turn generates commercial evidence supporting further investment in precision oncology drug development. The FDA approved over 70 oncology drug therapies between 2020 and 2025, with the majority featuring biomarker selection criteria, companion diagnostic requirements, or tumor-agnostic indications that explicitly require molecular testing before treatment initiation — creating contractually mandated diagnostic utilization tied to multi-billion dollar drug franchises. KRAS inhibitors represent the most recent major biomarker-drug class commercialization, with sotorasib and adagrasib targeting the previously undruggable KRAS G12C mutation present in approximately 13% of NSCLC and substantial proportions of colorectal and pancreatic cancers — creating large new biomarker testing markets for KRAS mutation detection that are expected to generate hundreds of millions in annual diagnostic revenue. The antibody-drug conjugate class — combining cancer cell-targeting antibody specificity with highly potent cytotoxic payload delivery — represents the fastest-growing therapeutic segment in precision oncology, with trastuzumab deruxtecan demonstrating unprecedented efficacy across HER2-expressing cancers regardless of tissue of origin and establishing HER2 expression quantitation as a critical companion biomarker across multiple tumor types beyond the historical HER2-amplified breast cancer indication. PARP inhibitors in BRCA-mutated and homologous recombination deficient cancers, RET inhibitors for RET-fusion lung and thyroid cancers, and FGFR inhibitors for FGFR-altered urothelial and cholangiocarcinoma cancers collectively represent the breadth of biomarker-therapy connections that are driving test ordering and diagnostic revenue growth across the oncology biomarker testing spectrum.

Opportunity: Multi-Cancer Early Detection and Population Screening Applications

The extension of precision oncology molecular technologies into early cancer detection and population-scale screening represents the largest potential market expansion opportunity in the sector, with multi-cancer early detection tests potentially creating a new paradigm of cancer care that identifies malignancies at curable early stages in asymptomatic individuals through routine blood tests. The clinical rationale is compelling: over 70% of cancer deaths occur from cancers that lack recommended screening tests, and most cancers presenting symptomatically are detected at advanced stages where curative treatment is substantially less feasible. Multi-cancer early detection assays analyzing circulating tumor DNA methylation patterns — with tissue-of-origin signal localization enabling direction of diagnostic workup when cancer signal is detected — are in advanced clinical validation, with Grail's Galleri test demonstrating 51.5% sensitivity across 50+ cancer types at 99.5% specificity in the PATHFINDER study and entering NHS England's largest-ever cancer trial program. The economic opportunity of MCED testing is transformative in scale: the US population aged 50 and above — the primary screening target — numbers approximately 100 million individuals, implying a potential annual testing market of tens of billions of dollars at price points of USD 300-1,000 per test if widespread clinical adoption and insurance reimbursement are achieved. Regulatory pathways for MCED tests are being established through FDA's breakthrough device designation framework, with clinical trial evidence requirements for sensitivity, specificity, and downstream clinical impact being defined through multi-year longitudinal studies. Commercial payer and CMS coverage decisions over the 2026-2030 period will determine the pace and scale of MCED market development, with positive coverage decisions potentially catalyzing the most significant market expansion in precision oncology history.

Why Do Targeted Therapies Lead the Market?

Targeted therapies command approximately 55-60% of total precision oncology market revenue in 2026, encompassing the large and rapidly expanding portfolio of molecularly targeted anticancer drugs that represent the therapeutic component of precision oncology workflows. The oncology targeted therapy market is dominated by blockbuster agents including osimertinib (Tagrisso, AstraZeneca) for EGFR-mutated NSCLC generating over USD 5 billion annually, palbociclib (Ibrance, Pfizer) and abemaciclib (Verzenio, Eli Lilly) targeting CDK4/6 in HR-positive HER2-negative breast cancer, ibrutinib and acalabrutinib targeting BTK in B-cell malignancies, trastuzumab deruxtecan across multiple HER2-expressing solid tumor types, and olaparib targeting BRCA-mutated ovarian, breast, prostate, and pancreatic cancers — collectively representing tens of billions in precision oncology therapeutic revenue. The immuno-oncology sub-segment — particularly checkpoint inhibitors including pembrolizumab, nivolumab, atezolizumab, and durvalumab deployed increasingly in biomarker-selected (high PD-L1, high TMB, MSI-high) patient populations — contributes massive revenue to the precision oncology therapeutics market, with pembrolizumab alone generating approximately USD 25 billion annually across its multiple biomarker-selected indications. The diagnostics component — encompassing next-generation sequencing panels, liquid biopsy tests, immunohistochemistry assays, FISH testing, and digital pathology — represents approximately 10-12% of total market revenue but serves as the enabling infrastructure for the entire precision oncology ecosystem, with companion diagnostic revenue growth closely tracking targeted therapy utilization expansion.

How Does Next-Generation Sequencing Dominate the Technology Landscape?

Next-generation sequencing represents approximately 42-46% of precision oncology technology market revenue in 2026, functioning as the foundational platform enabling comprehensive tumor molecular profiling that identifies the full landscape of actionable genomic alterations simultaneously from a single tissue or liquid biopsy sample. Comprehensive genomic profiling panels — including Foundation Medicine's FoundationOne CDx (324 genes), Tempus xT, Guardant360 CDx, and institutional NGS panels — are becoming standard of care biomarker testing in multiple advanced cancer settings, with National Comprehensive Cancer Network guidelines recommending broad molecular profiling for NSCLC, ovarian, prostate, colorectal, and multiple other cancer types at initial metastatic diagnosis to identify actionable alterations before treatment initiation. Whole exome sequencing and whole genome sequencing platforms are advancing toward clinical deployment, with falling sequencing costs approaching USD 200-500 per whole genome enabling increasingly comprehensive tumor characterization beyond targeted panel limitations, particularly for identifying tumor mutational burden, homologous recombination deficiency, and structural variants including complex genomic rearrangements that targeted panels may miss. Liquid biopsy NGS platforms are the fastest-growing NGS subsegment at approximately 16-18% CAGR, driven by both companion diagnostic applications for established targeted therapies and the emerging early cancer detection market. Illumina, Roche (AVENIO), Thermo Fisher Scientific (Ion Torrent), Qiagen, and Pacific Biosciences (long-read sequencing) lead the NGS platform market, with competitive intensity increasing from Oxford Nanopore Technologies advancing portable long-read sequencing applications in precision oncology molecular diagnostics.

Why Does Non-Small Cell Lung Cancer Lead the Market?

Non-small cell lung cancer commands approximately 22-26% of total precision oncology market revenue in 2026, reflecting the most extensively developed biomarker-targeted therapy ecosystem among all solid tumor types and the large global burden of lung cancer representing the world's leading cause of cancer mortality. NSCLC molecular profiling has become standard-of-care globally, with guidelines recommending testing for EGFR mutations (present in approximately 15% of Western and 40-50% of Asian NSCLC patients), ALK rearrangements (3-5%), ROS1 rearrangements (1-2%), BRAF V600E mutations (2-3%), MET exon 14 skipping mutations (3-4%), RET rearrangements (1-2%), NTRK fusions (< 1%), and KRAS G12C mutations (13%) — creating a rich and commercially valuable multi-biomarker testing mandate at NSCLC diagnosis. The therapeutic consequence of NSCLC molecular profiling is dramatic clinical impact: EGFR-mutated patients receiving osimertinib achieve median overall survival of approximately 38 months compared to historical platinum-chemotherapy outcomes of 12-18 months, with the magnitude of this benefit directly attributable to precision molecular matching enabled by biomarker testing. Breast cancer represents the second-largest cancer type segment in precision oncology revenue, encompassing HER2-targeted therapy for HER2-amplified tumors, PARP inhibitors for BRCA-mutated tumors, PI3K inhibitor alpelisib for PIK3CA-mutated HR-positive disease, and the expanding ADC portfolio targeting HER2-low and HER2-ultralow expression classifications that are dramatically expanding the biomarker-selected treatable population beyond the historical HER2-positive subset.

Why Do Hospitals and Cancer Centers Command Market Leadership?

Hospitals and cancer centers account for approximately 45-50% of precision oncology market revenue in 2026, serving as the primary sites where the full precision oncology care pathway — from molecular testing through therapy selection, treatment delivery, and response monitoring — is integrated and delivered to cancer patients. Comprehensive cancer centers — including NCI-designated cancer centers in the United States, European Organisation for Research and Treatment of Cancer network members, and equivalent designation programs in Japan, Australia, and other markets — have been the earliest adopters and most advanced implementers of precision oncology workflows, integrating molecular tumor boards that convene multidisciplinary experts to interpret comprehensive genomic profiling results and translate molecular findings into actionable treatment recommendations. Diagnostic laboratories represent the second-largest end-user segment, encompassing both hospital-based molecular pathology laboratories performing in-house NGS testing and independent reference laboratories including Quest Diagnostics, Laboratory Corporation (LabCorp), and specialized oncology diagnostics companies like NeoGenomics that process large volumes of oncology biomarker testing for community oncology practices lacking in-house genomic testing capabilities. Pharmaceutical and biotechnology companies constitute a critically important end-user category — leveraging precision oncology diagnostics, biomarker data platforms, and real-world evidence databases in drug development, companion diagnostic co-development, clinical trial patient selection, and regulatory submission contexts — with the global oncology pipeline of over 2,000 drugs in development creating sustained and growing demand for precision oncology tools and services throughout development programs.

How is North America Maintaining Market Leadership?

North America holds approximately 40-44% of the global precision oncology market in 2026, anchored by the United States' position as both the largest precision oncology drug market globally and the most advanced regulatory and reimbursement environment for precision oncology diagnostics and therapeutics. The FDA's oncology regulatory framework — including accelerated approval, breakthrough therapy designation, and companion diagnostic co-approval pathways — provides the world's fastest route to market for precision oncology innovations, attracting global pharmaceutical companies to prioritize US regulatory submissions and creating the most extensive portfolio of approved biomarker-linked therapies available to US oncologists. Medicare coverage for comprehensive genomic profiling panels including Foundation Medicine's FoundationOne CDx for certain solid tumors and liquid biopsy assays provides broad reimbursement access that has driven rapid NGS testing adoption across both academic medical centers and community oncology practices. Commercial insurance coverage for precision oncology diagnostics and therapeutics, while variable, has expanded substantially as clinical evidence demonstrating health economic value through improved outcomes and avoidance of ineffective therapies justifies coverage investment. Canada's government-funded provincial cancer agencies — including Ontario Health, BC Cancer, and Cancer Care Alberta — have implemented precision oncology programs with centralized genomic testing infrastructure providing equitable access to molecular profiling for cancer patients across the country.

Which Factors Drive Asia-Pacific's Rapid Growth?

Asia-Pacific demonstrates the highest regional growth rate at approximately 12-14% CAGR, driven by rapidly expanding precision oncology infrastructure across multiple high-population markets with large and growing cancer burdens where biomarker-guided therapy adoption is accelerating from a lower base. Japan's Cancer Genomic Medicine (CGM) program, launched in 2019, has established 11 core hospitals and approximately 200 affiliate hospitals equipped to perform comprehensive cancer genome profiling and present cases at molecular tumor boards, creating national infrastructure for precision oncology delivery that is driving systematic adoption of comprehensive genomic profiling and targeted therapy utilization. China's precision oncology market is growing at approximately 15-17% CAGR, driven by the world's largest cancer patient population — with approximately 4.6 million new cancer diagnoses annually — rapidly expanding domestic NGS testing infrastructure through companies including GenomiCare, Berry Oncology, Burning Rock Biotech, and Genetron Health, and growing availability of both imported targeted therapies and domestically developed precision oncology drugs from companies including BeiGene, Zymeworks, and Innovent Biologics. South Korea's advanced healthcare infrastructure, high molecular diagnostic adoption, and strong domestic genomics industry represented by companies including Macrogen and Theragen Bio create a sophisticated and rapidly growing precision oncology market. Australia's National Cancer Screening Programs and investment in ACRF Cancer Genomics Facility infrastructure are supporting population-level precision oncology implementation, with the Medical Services Advisory Committee providing coverage recommendations that are progressively expanding Medicare Benefits Schedule reimbursement for precision oncology diagnostics.

The global precision oncology market encompasses pharmaceutical companies, diagnostic platform providers, and enabling technology companies across interconnected market segments. In targeted therapies and immuno-oncology, Roche/Genentech (Tecentriq, Herceptin, Perjeta, FoundationOne diagnostics), AstraZeneca (Tagrisso, Lynparza, Imfinzi), Pfizer (Ibrance, Lorbrena, Xalkori), Bristol-Myers Squibb (Opdivo, Yervoy, Reblozyl), Merck & Co. (Keytruda across numerous biomarker-selected indications), Novartis (Kymriah CAR-T, Kisqali, Zykadia), Eli Lilly (Verzenio, Retevmo, selpercatinib), and Johnson & Johnson (Darzalex, Imbruvica, Rybrevant) are the dominant pharmaceutical revenue generators. In precision oncology diagnostics, Illumina (NovaSeq, MiSeq, TruSight Oncology), Thermo Fisher Scientific (Ion Torrent, Oncomine), Foundation Medicine (Roche subsidiary, FoundationOne CDx/Liquid CDx), Guardant Health (Guardant360 CDx, Guardant Reveal), Exact Sciences (Oncotype DX, multi-cancer early detection pipeline), Veracyte (Decipher, Afirma), NeoGenomics, and Tempus AI provide the diagnostic platforms and testing services driving biomarker-guided treatment selection. In AI and data analytics, Tempus AI, Flatiron Health (Roche subsidiary), IBM Watson Health (divested), and PathAI are building the data infrastructure and AI tools enabling precision oncology intelligence at scale. GRAIL (Illumina spin-off), Pacific Biosciences, and Oxford Nanopore represent emerging technology innovators expanding liquid biopsy and long-read sequencing capabilities.

The global precision oncology market is expected to grow from USD 96.47 billion in 2026 to USD 246.58 billion by 2036.

The global precision oncology market is projected to grow at a CAGR of 9.8% from 2026 to 2036.

Targeted therapies dominate the market representing 55-60% of revenue through the large portfolio of approved biomarker-linked drugs including EGFR inhibitors, HER2-targeted agents, CDK inhibitors, PARP inhibitors, and checkpoint immunotherapy in biomarker-selected populations. Diagnostics and biomarker testing demonstrate the fastest underlying growth driven by expansion of companion diagnostic requirements, liquid biopsy adoption, and multi-cancer early detection test commercialization.

Liquid biopsy enables non-invasive tumor molecular profiling from peripheral blood, supporting initial biomarker testing when tissue is insufficient, monitoring minimal residual disease after curative therapy to identify patients requiring treatment intensification, early detection of acquired resistance mutations enabling treatment adaptation before radiographic progression, and emerging multi-cancer early detection applications potentially transforming population-scale cancer screening.

North America leads with approximately 40-44% of global market driven by the most extensive portfolio of approved companion diagnostic-linked targeted therapies, advanced FDA regulatory and reimbursement frameworks, and highest genomic testing adoption. Asia-Pacific demonstrates the fastest growth at 12-14% CAGR driven by Japan's national Cancer Genomic Medicine program, China's large and growing cancer patient population with expanding domestic NGS infrastructure, and South Korea's advanced molecular diagnostics ecosystem.

The leading companies include Roche/Genentech (Foundation Medicine), AstraZeneca, Pfizer, Bristol-Myers Squibb, Merck & Co., Novartis, Eli Lilly, Illumina, Thermo Fisher Scientific, Guardant Health, Exact Sciences, Tempus AI, Flatiron Health, GRAIL, and NeoGenomics, spanning targeted therapy pharmaceuticals, NGS diagnostic platforms, liquid biopsy, and AI-driven precision oncology analytics.

Published Date: Apr-2026

Published Date: Feb-2026

Published Date: Jan-2025

Published Date: Mar-2016

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates