Resources

About Us

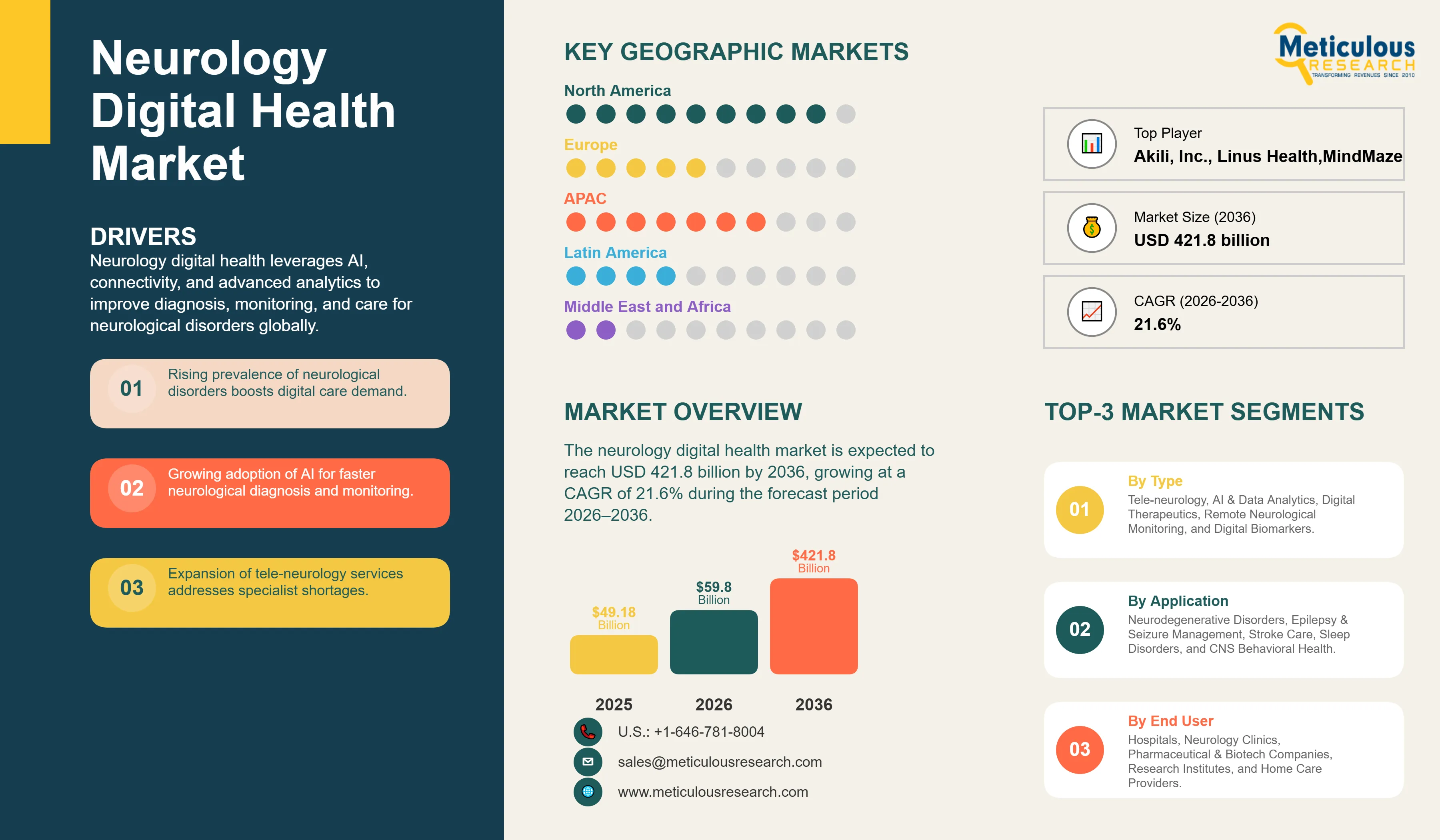

The global neurology digital health market was valued at USD 59.8 billion in 2026. This market is expected to reach USD 421.8 billion by 2036, growing at a CAGR of 21.6% during the forecast period 2026–2036.

Market Overview and Insights

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global neurology digital health market is undergoing a seismic transformation as the healthcare industry integrates advanced computing, artificial intelligence, and connectivity into the management of complex brain and nervous system disorders. Neurological conditions are currently the leading cause of disability-adjusted life years (DALYs) and the second leading cause of death globally, accounting for approximately 11 million deaths annually and more than 440 million DALYs worldwide, according to the World Health Organization and the Global Burden of Disease (GBD) study. Digital health in neurology offers a critical pathway to addressing the immense burden of conditions such as Alzheimer’s disease, Parkinson’s disease, epilepsy, and stroke. According to the World Health Organization, more than 3 billion people worldwide were living with a neurological condition in 2021, highlighting the urgent need for scalable and accessible neurological care solutions. By leveraging neurological health technology, providers can now offer decentralized, data-driven care that was previously impossible within the constraints of traditional clinical settings.

AI in neurology is the primary engine of innovation within this market, enabling the automated analysis of neuroimaging, EEG data, and complex behavioral patterns. These digital neurology solutions are significantly improving diagnostic accuracy and reducing the time to intervention, particularly in acute stroke care where every minute saved preserves brain tissue and improves long-term outcomes. Stroke remains a major healthcare burden, with approximately 12 million new stroke cases and 6.5 million stroke-related deaths occurring globally each year, according to the GBD study. Furthermore, the emergence of digital biomarkers in neurology is providing clinicians with objective, high-frequency metrics of disease progression, allowing for more precise treatment adjustments. The market is also being propelled by the rapid rise of neurology digital therapeutics (DTx), which provide software-based interventions for cognitive and behavioral disorders and are increasingly being incorporated into patient-centered care models.

Remote neurological monitoring is another pivotal segment, utilizing wearable sensors and mobile platforms to track gait, tremors, and seizure activity in real time. These tools are particularly valuable for patients with Parkinson’s disease and epilepsy. According to the World Health Organization, approximately 50 million people worldwide live with epilepsy, making it one of the most common neurological disorders globally. Additionally, the World Health Organization estimates that more than 55 million people are living with dementia worldwide, with nearly 10 million new cases diagnosed each year, creating substantial demand for continuous monitoring and digital disease management solutions. The integration of these technologies into the broader healthcare ecosystem is supported by favorable regulatory developments and the increasing use of digital endpoints in decentralized clinical trials.

Geographically, North America currently holds the largest share of the global market, supported by advanced digital health infrastructure, strong telehealth adoption, and favorable reimbursement policies. However, the Asia-Pacific region is projected to witness the fastest growth through 2036. China and Japan are expected to play pivotal roles, driven by aging populations and increasing investments in healthcare digitalization. According to the United Nations, the global population aged 65 years and older is projected to reach nearly 1.6 billion by 2050, significantly increasing the prevalence of age-related neurological disorders and reinforcing the need for scalable digital neurology solutions. As digital health becomes increasingly integrated into neurological care pathways, the market is poised for sustained long-term growth.

The primary driver for the neurology digital health market is the rising global prevalence of chronic neurological disorders. According to the World Health Organization, neurological conditions affect more than 3 billion people worldwide and are currently the leading cause of ill health and disability globally. Furthermore, more than 55 million people are living with dementia worldwide, and this number is projected to increase to approximately 139 million by 2050, driven largely by population aging. The growing burden of neurological diseases is creating an urgent need for scalable digital neurology solutions that support early detection, continuous monitoring, and long-term disease management.

Furthermore, advancements in AI and machine learning are enabling the analysis of complex neurological data, making digital health in neurology more reliable and actionable. The shift toward decentralized clinical trials by pharmaceutical companies is also a major driver, as digital tools allow for more frequent and accurate patient data collection.

A significant restraint is the inherent complexity of neurological data, where high variability in patient symptoms across conditions like Alzheimer’s and Parkinson’s makes standardized digital interventions difficult to implement. Additionally, regulatory hurdles for AI-based diagnostics and digital therapeutics remain high. The FDA and EMA require stringent clinical evidence for software-as-a-medical-device (SaMD) clearance, which can slow the time to market for innovative neurological health technology. The sensitive nature of brain health data also presents significant privacy and security concerns that must be addressed to gain broad patient and provider trust.

The emergence of precision neurology presents a massive opportunity, where digital biomarkers in neurology can be used to tailor treatments based on an individual's specific disease progression and behavioral metrics. This shift toward personalized care has the potential to significantly improve patient outcomes and reduce long-term healthcare costs. There is also significant growth potential in emerging markets in Asia-Pacific and Africa, where the severe shortage of neurology specialists makes tele-neurology and AI-driven triage tools highly valuable. Furthermore, the integration of digital neurology solutions into pharmaceutical drug development pipelines offers a significant path for commercial growth and innovation.

A key challenge is ensuring high patient adherence, particularly in populations with cognitive impairment or motor dysfunction. Designing user interfaces that are accessible and engaging for elderly patients with dementia or Parkinson’s is critical for the success of remote neurological monitoring. Interoperability also remains a technical hurdle, as diverse digital neurology data must be seamlessly integrated into disparate hospital IT systems and electronic health records. Furthermore, the industry must navigate the complex ethical implications of using AI for predicting neurological decline and ensure that these tools are deployed in a transparent and unbiased manner.

Digital therapeutics are moving from niche applications to mainstream clinical practice. FDA-cleared software for ADHD and chronic pain management are setting the stage for a broader wave of DTx targeting cognitive decline and behavioral symptoms in neurodegenerative diseases.

The use of digital biomarkers—collected via smartphones and wearables—is revolutionizing early detection. Subtle changes in speech, gait, and typing patterns are now being used to identify signs of Parkinson’s and Alzheimer’s years before clinical symptoms become apparent.

Based on technology, the market is segmented into Tele-neurology, AI & Data Analytics, Digital Therapeutics (DTx), Remote Neurological Monitoring, and Digital Biomarkers. In 2026, the Tele-neurology segment is expected to hold the largest share of the market. This is primarily due to the global shortage of neurologists and the rapid establishment of virtual care infrastructure during the COVID-19 pandemic, which has now become a standard of care.

The AI & Data Analytics segment is projected to witness the fastest growth, driven by the critical need for automated neuroimaging analysis and the increasing volume of longitudinal data from remote monitoring platforms.

Based on application, the market is segmented into Neurodegenerative Disorders, Epilepsy & Seizure Management, Mental & Behavioral Health (CNS-focused), Stroke & Acute Neurology, and Sleep Disorders. In 2026, the Neurodegenerative Disorders segment is expected to hold the largest share. Conditions like Alzheimer’s and Parkinson’s represent the largest and most costly long-term care burden in neurology.

The Epilepsy & Seizure Management segment is projected to witness the fastest growth, as patients and caregivers increasingly adopt real-time remote monitoring and logging tools to improve safety and treatment adherence.

North America is expected to hold the largest share of the global neurology digital health market in 2026, accounting for approximately 45% of total revenue. This dominance is driven by the region's advanced digital infrastructure, high concentration of leading health-tech firms, and favorable regulatory and reimbursement environments for digital therapeutics and remote monitoring.

Asia-Pacific is projected to witness the fastest growth during the forecast period. The region's aging population, particularly in Japan and China, is creating massive demand for brain health technology. Furthermore, the rapid digitization of healthcare systems in China and India is facilitating the broad rollout of tele-neurology and AI-driven diagnostic tools. Key companies operating in the Asia-Pacific market include global leaders and a growing number of local AI-focused startups.

The global neurology digital health market is highly competitive, featuring a mix of established medical technology giants, pharmaceutical companies with digital divisions, and specialized health-tech startups. Competition is increasingly focused on securing clinical validation for AI algorithms and digital therapeutics, as well as integrating diverse data sources into unified clinician portals. Strategic partnerships between pharmaceutical firms and digital health vendors are a key trend, aimed at combining pharmacological treatments with digital management tools.

Key players in the global market include Medtronic plc, Philips Healthcare, GE HealthCare, Siemens Healthineers, Abbott Laboratories, Biogen, Roche, Akili, Inc., Cogstate Ltd., Linus Health, Rune Labs, NeuroTrack Technologies, Click Therapeutics, MindMaze, Hinge Health, Empatica, Beacon Biosignals, and Ceribell, Inc.

The market is projected to reach USD 421.8 billion by 2036, growing at a CAGR of 21.6% from 2026 to 2036.

Digital biomarkers are software-based metrics of physiological and behavioral metrics that provide objective, high-frequency data for disease tracking and precision treatment.

AI-based diagnostic tools for neuroimaging can reduce diagnostic errors by 30% and decrease time to treatment for acute stroke patients by over 60 minutes.

The Asia-Pacific region is projected to witness the fastest growth due to its aging population and rapid healthcare digitization.

Neurology digital therapeutics provide software-based interventions for cognitive and behavioral disorders, often demonstrating significant clinical efficacy in decentralized settings.

The market is expected to grow at a CAGR of 21.6% during the forecast period 2026–2036.

Neurodegenerative Disorders hold the largest share, as conditions like Alzheimer’s represent the largest long-term care burden.

The rising prevalence of neurological disorders, advancements in AI, and the shift toward decentralized clinical trials are the primary drivers.

Designing accessible and engaging interfaces is critical for ensuring adherence among patients with dementia or motor dysfunction.

The market features leaders like Medtronic, Philips, GE HealthCare, Siemens Healthineers, Abbott, Biogen, and Roche.

1. Market Definition & Scope

1.1. Market Definition

1.2. Market Ecosystem

1.3. Currency Considered

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Process of Data Collection and Validation

2.2.1. Secondary Research

2.2.2. Primary Research/Interviews with Key Opinion Leaders

2.3. Market Sizing and Forecast

2.3.1. Market Size Estimation Approach

2.3.1.1. Bottom-Up Approach

2.3.1.2. Top-Down Approach

2.3.2. Growth Forecast Approach

2.3.3. Assumptions for the Study

3. Executive Summary

3.1. Overview

3.2. Segmental Analysis

3.2.1. Market Analysis, by Technology

3.2.2. Market Analysis, by Component

3.2.3. Market Analysis, by Application

3.2.4. Market Analysis, by End User

3.2.5. Market Analysis, by Geography

3.3. Competitive Analysis

4. Market Insights

4.1. Overview

4.2. Factors Affecting Market Growth

4.2.1. Drivers

4.2.1.1. Increasing Global Prevalence of Chronic Neurological Disorders

4.2.1.2. Rapid Advancements in AI and Machine Learning for Data Analysis

4.2.1.3. Increasing Shift Toward Decentralized Clinical Trials in Pharma

4.2.1.4. Rising Global Aging Population and Demand for Brain Health Tech

4.2.2. Restraints

4.2.2.1. Inherent Complexity and Variability of Neurological Data

4.2.2.2. Stringent Regulatory Hurdles for AI and Digital Therapeutics

4.2.3. Opportunities

4.2.3.1. Emergence of Precision Neurology and Personalized Treatment Models

4.2.3.2. High Unmet Need for Tele-neurology in Emerging APAC and African Markets

4.2.3.3. Integration into Pharmaceutical Drug Development Pipelines

4.2.4. Challenges

4.2.4.1. Ensuring Patient Adherence in Populations with Cognitive Impairment

4.2.4.2. Achieving Technical Interoperability with Disparate Hospital IT Systems

4.2.5. Trends

4.2.5.1. Mainstreaming of FDA-Cleared Neurology Digital Therapeutics (DTx)

4.2.5.2. Proliferation of Digital Biomarkers for Early Disease Detection

4.3. Porter’s Five Forces Analysis

4.4. Regulatory Landscape

4.5. Value Chain Analysis

5. Global Neurology Digital Health Market, by Technology

5.1. Overview

5.2. Tele-neurology

5.3. AI & Data Analytics

5.4. Digital Therapeutics (DTx)

5.5. Remote Neurological Monitoring

5.6. Digital Biomarkers

6. Global Neurology Digital Health Market, by Component

6.1. Overview

6.2. Software & Platforms

6.3. Hardware/Devices

6.4. Services

7. Global Neurology Digital Health Market, by Application

7.1. Overview

7.2. Neurodegenerative Disorders

7.2.1. Alzheimer’s Disease

7.2.2. Parkinson’s Disease

7.2.3. Others

7.3. Epilepsy & Seizure Management

7.4. Mental & Behavioral Health (CNS-focused)

7.5. Stroke & Acute Neurology

7.6. Sleep Disorders

8. Global Neurology Digital Health Market, by End User

8.1. Overview

8.2. Hospitals & Neurology Clinics

8.3. Pharmaceutical & Biotech Companies

8.4. Patients/Homecare

8.5. Payers

9. Global Neurology Digital Health Market, by Geography

9.1. Overview

9.2. North America

9.2.1. U.S. (Stats: ~45% Global Market Share)

9.2.2. Canada

9.3. Europe

9.3.1. Germany (Stats: Strong Focus on DiGA and Digital Health Apps)

9.3.2. U.K. (Stats: NHS Focus on AI-Driven Stroke Triage)

9.3.3. France

9.3.4. Italy

9.3.5. Spain

9.3.6. Rest of Europe

9.4. Asia-Pacific

9.4.1. China (Stats: Massive Investment in AI and Digital Infrastructure)

9.4.2. Japan (Stats: High Demand for Elderly and Dementia Care Tech)

9.4.3. India

9.4.4. Australia

9.4.5. Rest of Asia-Pacific

9.5. Latin America

9.5.1. Brazil

9.5.2. Mexico

9.5.3. Rest of Latin America

9.6. Middle East & Africa

10. Competitive Landscape

10.1. Overview

10.2. Key Growth Strategies

10.3. Competitive Dashboard

10.4. Vendor Market Positioning

10.5. Market Share Analysis, 2025

11. Company Profiles

11.1. Medtronic plc

11.2. Koninklijke Philips N.V.

11.3. GE HealthCare Technologies Inc.

11.4. Siemens Healthineers AG

11.5. Abbott Laboratories

11.6. Biogen Inc.

11.7. Roche Holding AG

11.8. Akili, Inc.

11.9. Cogstate Ltd.

11.10. Linus Health

11.11. Rune Labs

11.12. NeuroTrack Technologies, Inc.

11.13. Click Therapeutics, Inc.

11.14. MindMaze

11.15. Hinge Health

11.16. Empatica Inc.

11.17. Beacon Biosignals

11.18. Ceribell, Inc.

12. Appendix

Published Date: May-2026

Published Date: May-2026

Published Date: Nov-2025

Published Date: May-2024

Published Date: May-2024

Subscribe to get the latest industry updates