Resources

About Us

Medical Device Interoperability Market Size, Share & Trends Analysis by Component, Technology, Application, End User, and Geography - Global Opportunity Analysis and Industry Forecast (2026-2036)

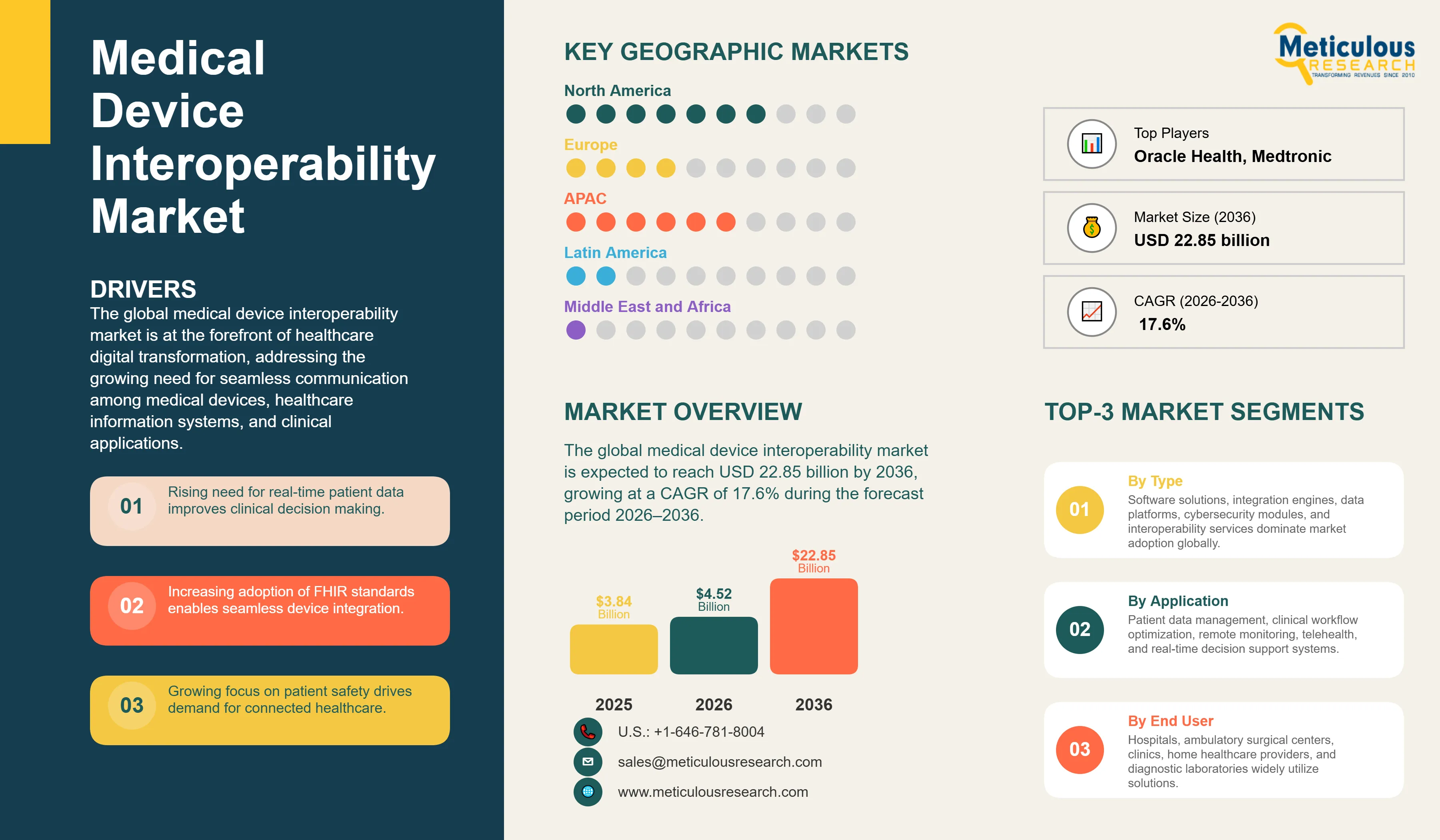

Report ID: MRHC - 1042062 Pages: 314 Jun-2026 Formats*: PDF Category: Healthcare Delivery: 24 to 72 Hours Download Free Sample ReportThe global medical device interoperability market is estimated to be USD 4.52 billion in 2026. This market is expected to reach USD 22.85 billion by 2036, growing at a CAGR of 17.6% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

The global medical device interoperability market is at the forefront of healthcare digital transformation, addressing the growing need for seamless communication among medical devices, healthcare information systems, and clinical applications. These solutions enable the safe and secure exchange of patient data across devices and electronic health records (EHRs), supporting more efficient clinical workflows and informed decision-making. According to the U.S. FDA, medical device interoperability refers to the ability of devices and systems to safely, securely, and effectively exchange and use information, making interoperability a critical requirement as healthcare environments become increasingly connected.

Growing adoption of connected monitoring devices, infusion systems, telehealth platforms, and remote patient monitoring solutions is increasing the volume of clinical data that must be integrated across disparate systems. Interoperable technologies help reduce manual documentation, improve patient safety, and support standardized data exchange through protocols such as ISO/IEEE 11073, DICOM, HL7, and FHIR. The FDA and standards organizations, including the Association for the Advancement of Medical Instrumentation (AAMI), have promoted the development of interoperability standards to facilitate safe device integration and cross-platform communication.

The importance of interoperability is further reinforced by its economic and operational benefits. The West Health Institute estimates that improved medical device interoperability could deliver more than USD 30 billion in annual healthcare savings through reductions in adverse events, workflow inefficiencies, and redundant clinical activities. As healthcare providers increasingly focus on connected care delivery, patient safety, and data-driven clinical operations, demand for robust interoperability software and services is expected to accelerate worldwide.

Drivers: Enhancing Patient Safety and Clinical Workflow through Seamless Device Integration

The primary drivers of the medical device interoperability market are the growing need to enhance patient safety, improve clinical workflow efficiency, and reduce healthcare costs. Seamless integration of medical devices with electronic health records (EHRs) and clinical information systems reduces manual data entry, minimizes the risk of human error, and enables healthcare professionals to devote more time to direct patient care. Improved interoperability has also been associated with significant cost savings through reductions in adverse events, duplicate procedures, and workflow inefficiencies, with industry estimates suggesting that enhanced interoperability could eliminate more than USD 30 billion in annual waste across the healthcare system.

The increasing adoption of Fast Healthcare Interoperability Resources (FHIR) standards is another major growth driver. Healthcare providers and technology vendors are increasingly leveraging FHIR-based frameworks to enable standardized and secure data exchange across disparate devices and information systems. The widespread implementation of FHIR-enabled electronic health records and the growing emphasis on connected care are accelerating the development of a more integrated healthcare ecosystem. As healthcare organizations continue to prioritize data accessibility, operational efficiency, and value-based care, demand for medical device interoperability solutions is expected to rise steadily worldwide.

Restraints: Integration Complexities and Cybersecurity Concerns

Despite the clear benefits, the market faces significant restraints, primarily related to the complexities of integrating diverse medical devices and the ever-present threat of cybersecurity breaches. The sheer volume and variety of legacy medical devices, each with proprietary communication protocols, pose substantial integration challenges. Developing universal interfaces that ensure secure and reliable data exchange is a complex and costly endeavor. Furthermore, as medical devices become increasingly connected, they become potential entry points for cyberattacks, threatening patient data privacy and device functionality. The EU Medical Device Regulation (MDR) and other global regulatory frameworks impose stringent requirements for data safety and quality assurance, adding to the development and compliance burden for manufacturers and healthcare providers.

Opportunities: IoMT Expansion and AI-Powered Predictive Analytics

Significant opportunities are emerging from the rapid expansion of the Internet of Medical Things (IoMT) and the increasing integration of AI-powered analytics into healthcare delivery. Connected medical devices, ranging from wearable sensors and remote patient monitoring systems to smart infusion pumps and bedside monitors, generate vast amounts of real-time clinical data. When supported by interoperable platforms, these data streams can be leveraged by AI algorithms to enable predictive diagnostics, personalized treatment strategies, and proactive patient monitoring.

The growing adoption of connected health technologies is accelerating the need for standardized data exchange across devices and healthcare information systems. At the same time, regulatory agencies are advancing frameworks for the safe and effective deployment of AI-enabled medical devices, fostering innovation in digital health. The convergence of IoMT and artificial intelligence is expected to transform healthcare delivery by supporting more preventive, data-driven, and personalized models of care. As healthcare providers increasingly embrace remote care, clinical decision support, and predictive analytics, demand for robust medical device interoperability solutions is expected to expand substantially.

Accelerated Adoption of FHIR Standards

A defining trend in 2026 is the rapid adoption of HL7 FHIR as the preferred framework for healthcare data exchange. The U.S. Office of the National Coordinator for Health Information Technology (ONC) and CMS interoperability regulations have accelerated the deployment of standardized APIs across healthcare systems. According to ONC, nearly all non-federal acute care hospitals have adopted certified EHR technology, creating a strong foundation for FHIR-based interoperability. The RESTful API architecture of FHIR simplifies integration between medical devices, EHRs, and digital health applications, enabling more efficient data sharing and supporting advanced analytics and connected care initiatives.

Rise of Vendor-Neutral Interoperability Platforms

The market is witnessing increasing adoption of vendor-neutral interoperability platforms capable of integrating devices from multiple manufacturers. This trend addresses longstanding challenges associated with proprietary systems and vendor lock-in. Industry standards organizations such as AAMI and HL7 have emphasized the importance of interoperable ecosystems to improve patient safety and clinical efficiency. Vendor-neutral platforms normalize data from bedside monitors, infusion pumps, ventilators, and other devices, creating a unified data layer for EHRs and clinical applications. As hospitals continue to expand connected care infrastructure and manage thousands of networked devices, these platforms are becoming essential for real-time clinical decision-making and maximizing the value of existing medical technology investments.

Analysis by Component

Based on component, the software segment is expected to hold the largest share in 2026. This dominance is driven by the increasing demand for sophisticated software solutions that can manage, process, and integrate data from a multitude of medical devices. These platforms often include data aggregation, normalization, and analytics capabilities. The services segment is projected to register the highest CAGR during the forecast period, reflecting the growing need for implementation, integration, and ongoing support services to navigate the complexities of medical device interoperability.

Analysis by Technology

By technology, the wired technology segment is expected to hold the largest share in 2026. This is primarily due to its inherent reliability, security, and high bandwidth capabilities, which are crucial for real-time data transmission in critical care environments. However, the wireless technology segment is projected to exhibit the fastest growth, driven by the increasing adoption of mobile health devices, wearables, and the flexibility offered by wireless connectivity in various clinical settings.

Analysis by Application

Based on application, the patient data management segment is expected to account for the largest share in 2026. This is driven by the critical need for comprehensive, real-time patient data from various devices to inform clinical decision-making, enhance patient safety, and support personalized care. The clinical workflow management segment is projected to register the highest CAGR, as healthcare organizations increasingly leverage interoperable devices to optimize operational efficiency, reduce manual tasks, and streamline care delivery processes.

Analysis by End User

By end user, hospitals are expected to hold the largest share in 2026. Hospitals are primary adopters due to the high volume and complexity of medical devices used in their facilities, coupled with the imperative to improve patient outcomes and operational efficiency. The home care settings segment is projected to witness the fastest growth, driven by the increasing shift towards remote patient monitoring and telehealth, which heavily rely on interoperable medical devices for continuous data collection and transmission.

North America

North America is expected to dominate the global medical device interoperability market in 2026, with an estimated market share of around 45%. The region's leadership is attributed to stringent regulatory mandates, such as those from the ONC and CMS promoting interoperability, and a high adoption rate of FHIR-enabled systems, with over 90% of U.S. hospitals already utilizing them (Source: Knowi). Significant investments in digital health infrastructure and the presence of key market players further solidify its market position. The region also benefits from a mature healthcare IT ecosystem and a strong focus on reducing medical errors and improving patient safety through integrated data.

Europe

Europe is projected to hold the second-largest market share, estimated at approximately 26% in 2026. The region's growth is driven by increasing regulatory emphasis on data exchange, such as the EU Medical Device Regulation (MDR), and initiatives like the European Health Data Space (EHDS) that aim to facilitate cross-border health data exchange. Countries like Germany and the UK are leading in the adoption of interoperable solutions to enhance their national health systems and improve patient care coordination.

Asia Pacific

The Asia Pacific region is projected to witness the fastest growth during the forecast period, with a CAGR exceeding 20%. This rapid expansion is fueled by significant investments in digital health transformation, increasing healthcare expenditure, and the growing adoption of advanced medical technologies in countries like China, India, and Australia. The rising prevalence of chronic diseases and the need for efficient healthcare delivery systems are driving the demand for interoperable medical devices to improve patient outcomes and operational efficiency.

Latin America

Latin America is an emerging market for medical device interoperability, driven by increasing healthcare digitalization initiatives and growing awareness of the benefits of integrated care. Countries like Brazil and Mexico are investing in modernizing their healthcare infrastructure, leading to a gradual adoption of interoperable solutions. The market growth is supported by efforts to improve patient safety and streamline clinical workflows in a cost-effective manner.

Middle East & Africa

The Middle East & Africa region is expected to witness steady growth in the medical device interoperability market. This growth is primarily driven by government initiatives to develop smart hospitals and healthcare cities, particularly in the UAE and Saudi Arabia. Increasing healthcare expenditure, coupled with a focus on adopting advanced medical technologies to enhance patient care and operational efficiency, contributes to the market expansion in this region.

The competitive landscape of the global medical device interoperability market is characterized by strategic alliances, partnerships, and continuous innovation aimed at developing robust and secure integration platforms. Leading players are focusing on enhancing their software capabilities to support a wider range of medical devices and adhere to evolving interoperability standards like FHIR. Acquisitions and collaborations are common strategies to expand market reach and integrate complementary technologies. The market is also seeing an influx of specialized startups offering niche solutions for specific device types or clinical workflows, contributing to a dynamic and evolving competitive environment in June 2026.

Philips Healthcare (including Capsule), GE HealthCare, Oracle Health (Cerner), Medtronic, Baxter International, Dräger, Masimo, Ascom, Stryker, Cisco Systems, Siemens Healthineers, Epic Systems, Nihon Kohden, Becton Dickinson (BD), Abbott, Spacelabs Healthcare, Mindray Medical, ICU Medical, Fresenius Medical Care, NantHealth.

The market is projected to reach USD 22.85 billion by 2036, growing at a CAGR of 17.6% from 2026 to 2036.

Medical device interoperability enhances patient safety, improves clinical workflow efficiency, and reduces healthcare costs by enabling seamless data exchange and minimizing manual data entry.

The wireless technology segment is projected to exhibit the fastest growth, driven by the increasing adoption of mobile health devices and wearables.

Over 90% of U.S. hospitals have adopted FHIR-enabled systems, with 85% adoption among institutions using major EHR vendors.

North America holds the largest share, estimated at around 45% in 2026, driven by stringent regulatory mandates and high FHIR adoption.

IoMT devices generate vast amounts of real-time data that, when interoperable, fuel AI algorithms for predictive diagnostics and personalized treatment plans.

Improved health data interoperability could eliminate more than USD 30 billion in annual healthcare waste through reductions in inefficiencies, duplicate testing, and medical errors.

Which end-user segment is the primary adopter of advanced medical device interoperability solutions?

Hospitals are the primary adopters due to the high volume and complexity of medical devices used, and the imperative to improve patient outcomes.

Stringent regulatory mandates, such as the EU MDR and ONC/CMS rules, drive the demand for compliant and secure interoperability solutions.

The top 5 players are Qualcomm Life, Inc., Capsule Technologies, Inc., Philips Healthcare, GE HealthCare Technologies Inc., and Oracle Health (Cerner).

Published Date: Jul-2026

Published Date: Jun-2026

Published Date: Jun-2026

Published Date: Apr-2026

Published Date: Feb-2026

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates