Resources

About Us

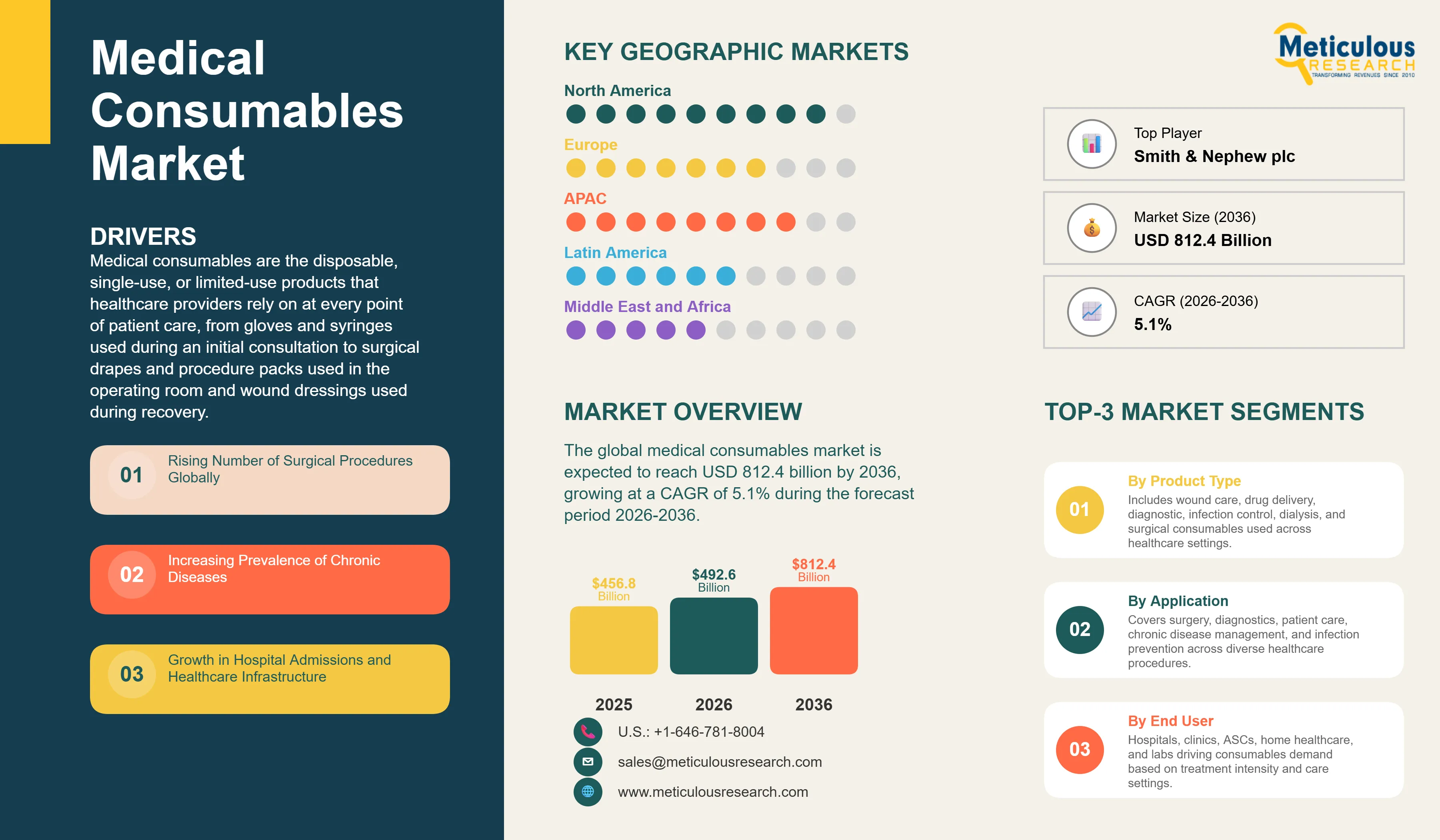

The global medical consumables market was valued at USD 456.8 billion in 2025. This market is expected to reach USD 812.4 billion by 2036 from an estimated USD 492.6 billion in 2026, growing at a CAGR of 5.1% during the forecast period 2026-2036. According to the World Health Organization, over 313 million surgical procedures are performed globally every year, each requiring a defined set of sterile single-use consumables, making surgical volume one of the most reliable and measurable demand indicators for this market.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Medical consumables are the disposable, single-use, or limited-use products that healthcare providers rely on at every point of patient care, from gloves and syringes used during an initial consultation to surgical drapes and procedure packs used in the operating room and wound dressings used during recovery. These products are replaced after each patient contact to prevent cross-infection and maintain the sterile conditions that modern medicine requires. According to Becton Dickinson, one of the world's largest medical device companies, approximately 16 billion injections are administered globally each year using disposable syringes and needles, a single product subcategory that illustrates the extraordinary scale of recurring demand in this market.

The market is growing because healthcare utilization is increasing across every major indicator. According to the World Health Organization, global surgical volumes are growing at approximately 5% annually in developing countries as healthcare infrastructure expands. The International Diabetes Federation reported in 2023 that 537 million adults globally are living with diabetes, a number projected to reach 783 million by 2045, with each patient requiring daily or weekly consumables for blood glucose monitoring, insulin delivery, and related care. The Global Kidney Health Atlas published by the International Society of Nephrology estimates that over 850 million people worldwide have some form of kidney disease, with approximately 3.5 million requiring regular dialysis that consumes significant volumes of dialysis-specific consumables per session. These chronic disease populations are growing every year, creating an ever-expanding baseline of recurring consumables demand that does not diminish between economic cycles.

Two key opportunities are reshaping the market's trajectory. Home healthcare is the fastest-growing care setting globally, with the American Hospital Association projecting that home-based care will account for a growing share of total healthcare delivery as payers and patients alike seek alternatives to costly hospital stays. This shift is driving demand for consumables specifically designed for patient self-administration including prefilled syringes, easy-to-use wound care kits, and continuous glucose monitoring supplies. In parallel, the healthcare industry's sustainability agenda is creating commercial pull for biodegradable and plant-based polymer consumables, with major hospital groups in Europe and North America issuing procurement sustainability requirements that are beginning to reshape material specifications across the supply chain.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 812.4 Billion |

|

Market Size in 2026 |

USD 492.6 Billion |

|

Market Size in 2025 |

USD 456.8 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 5.1% |

|

Dominating Product Type |

Infection Control Consumables |

|

Fastest Growing Product Type |

Diagnostic Consumables |

|

Dominating Application |

Surgery |

|

Fastest Growing Application |

Chronic Disease Management |

|

Dominating End User |

Hospitals |

|

Fastest Growing End User |

Home Healthcare |

|

Dominating Distribution Channel |

Distributors and Wholesalers |

|

Fastest Growing Distribution Channel |

Online Channels |

|

Dominating Material Type |

Plastics and Polymers |

|

Fastest Growing Material Type |

Nonwoven Materials |

|

Dominating Sterilization Type |

Pre-Sterilized Consumables |

|

Fastest Growing Sterilization Type |

Non-Sterilized Consumables |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Post-Pandemic Normalization Masking Structural Demand Growth

The medical consumables market went through an extraordinary boom in 2020 and 2021 as COVID-19 drove unprecedented demand for gloves, masks, gowns, and diagnostic test kits that dwarfed normal procurement volumes. According to the WHO, global PPE demand increased by as much as 40 times during the height of the pandemic, creating severe supply shortages and driving manufacturers to invest heavily in expanded capacity. The subsequent normalization of infection control consumables demand as pandemic protocols eased has created a misleading impression of a market in decline, when in reality the underlying structural drivers of non-pandemic consumables demand, including surgical volumes, chronic disease populations, and healthcare infrastructure expansion, have continued growing steadily.

The post-pandemic period has also resulted in permanent changes in infection control protocols in many healthcare settings. According to the Centers for Disease Control and Prevention, healthcare-associated infections affect approximately 1 in 31 hospital patients in the U.S. on any given day, and the heightened awareness of infection risks generated by the pandemic has reinforced compliance with PPE protocols and maintained elevated baseline demand for gloves, masks, and other infection control consumables above pre-pandemic levels in most markets. The market is therefore best characterized as returning to structural growth after an exceptional spike, with the long-term demand trajectory firmly upward.

Single-Use Medical Device Adoption Accelerating Across Endoscopy and Surgical Specialties

One of the most commercially significant structural shifts in the medical consumables market over the past five years has been the rapid acceleration of single-use device adoption in procedural medicine, particularly in flexible endoscopy. Conventional reusable endoscopes require complex multi-step reprocessing between patients that is time-consuming, expensive, and has been linked to pathogen transmission incidents. A 2018 investigation by the U.S. Food and Drug Administration identified duodenoscope contamination as a contributing factor in carbapenem-resistant Enterobacteriaceae outbreaks at multiple U.S. hospitals, accelerating regulatory and clinical interest in single-use alternatives.

Companies including Ambu, which pioneered single-use bronchoscopes and has rapidly expanded into colonoscopy and other endoscopy categories, and Boston Scientific, which has invested heavily in disposable endoscopy, have demonstrated strong commercial growth in this segment. According to Ambu's 2023 annual report, its single-use endoscope portfolio is growing revenue at double-digit rates annually as hospitals progressively adopt disposable scopes for an expanding range of procedures. This trend is extending beyond endoscopy into other procedure categories including surgical instruments, biopsy needles, and access systems, adding significant new product volume to the consumables market that was previously served by capital equipment.

Supply Chain Regionalization Following COVID-19 Disruptions

The COVID-19 pandemic revealed severe vulnerabilities in the globally concentrated supply chains for medical consumables, with a very large proportion of global glove, mask, and syringe production concentrated in a small number of countries. According to the U.S. Department of Health and Human Services, the United States was importing approximately 90% of its surgical gloves and over 70% of its N95 respirators from overseas at the start of the pandemic, creating critical supply failures when global demand surged simultaneously. This vulnerability prompted significant policy and commercial responses aimed at building more geographically diversified and regionally resilient supply chains.

The U.S. PREVENT Pandemics Act and the EU's Strategic Reserves program both include provisions for domestic manufacturing incentives and stockpiling requirements for critical medical consumables. Becton Dickinson has announced investments in U.S.-based manufacturing capacity for syringes and needles, and Cardinal Health has expanded its domestic distribution and sourcing footprint. In Europe, the EU's Health Emergency Preparedness and Response Authority has been established with a mandate to maintain strategic stockpiles of critical health products including consumables. These supply chain restructuring investments are creating new manufacturing and distribution capacity in North America and Europe that will support regional consumables supply chains through the forecast period.

Rising Number of Surgical Procedures Globally

According to the Lancet Commission on Global Surgery, approximately 313 million surgical procedures are performed worldwide each year, but the commission also estimates that at least 143 million additional procedures are needed annually to address unmet surgical need in low and middle-income countries. As healthcare infrastructure expands in these markets, the gap between current and needed surgical volumes will progressively narrow, driving significant increases in surgical consumables demand. In developed markets, the aging of populations is driving growing volumes of elective procedures including joint replacements, cataract surgeries, and cardiac procedures. According to the American Joint Replacement Registry, total hip and knee replacement procedures in the U.S. alone exceeded 1 million in 2022 and are projected to grow substantially through 2030 as the baby boomer generation ages into the peak age for these procedures. Each procedure consumes a substantial kit of single-use surgical consumables including drapes, gowns, prep kits, sutures, staples, and instrument covers.

Increasing Prevalence of Chronic Diseases

According to the International Diabetes Federation's Diabetes Atlas 2023, 537 million adults aged 20 to 79 years are currently living with diabetes, representing 10.5% of the adult population globally, and this number is expected to rise to 783 million by 2045. Each person with diabetes who uses insulin requires syringes, pen needles, or insulin pump infusion sets on a daily basis, and those who monitor their blood glucose require test strips or continuous glucose monitoring sensors on an ongoing basis. According to the World Health Organization's 2023 data, cardiovascular diseases remain the number one cause of death globally, accounting for approximately 17.9 million deaths per year, and the large patient population with cardiovascular disease consumes significant volumes of catheters, IV consumables, and monitoring consumables during hospitalization and ongoing care. The growing global chronic disease burden creates a permanent, recurring, and growing demand for consumables that persists throughout each patient's disease management journey.

Growth in Home Healthcare and Self-Care

The global home healthcare market is expanding rapidly as payers, providers, and patients increasingly recognize the cost and convenience advantages of managing chronic conditions and post-acute care at home rather than in clinical settings. According to McKinsey and Company's 2023 Future of Care report, up to USD 265 billion worth of care services currently delivered in traditional healthcare settings could be shifted to home settings in the U.S. alone by 2025. This shift creates direct demand for consumables specifically designed for home use, including prefilled autoinjector syringes for biologics self-administration, simplified wound care kits for post-surgical home recovery, portable dialysis supplies for home peritoneal dialysis, and continuous glucose monitoring supplies for diabetes management. Medical consumables manufacturers are responding with product lines specifically designed for patient self-use, featuring simplified application, enhanced safety features to prevent needlestick injuries, and connected digital elements that allow care teams to monitor patient compliance and outcomes remotely.

Innovations in Biodegradable and Sustainable Consumables

The healthcare sector generates an estimated 5.9 million tonnes of waste annually in the United States alone, according to the U.S. Environmental Protection Agency, with single-use medical consumables representing a significant fraction of this total. This environmental footprint is attracting growing regulatory and procurement attention, with several major health systems including the National Health Service in the United Kingdom having made explicit net-zero commitments that include reducing the carbon footprint and waste generation of medical supplies procurement. This is creating commercial demand for biodegradable polymers, plant-based nonwoven materials, and reduced-packaging consumables that meet the same clinical performance standards as conventional products while offering better environmental credentials. Companies including Medline and Cardinal Health have launched sustainability product lines, and several specialist startups are developing medical-grade biodegradable materials for gloves, drapes, and packaging that are beginning to reach clinical qualification.

By Product Type: In 2026, Infection Control Consumables to Dominate

Based on product type, the global medical consumables market is segmented into wound care consumables, drug delivery consumables, diagnostic consumables, infection control consumables, dialysis consumables, surgical consumables, and other consumables. In 2026, the infection control consumables segment is expected to account for the largest share of the global medical consumables market. Gloves, masks, gowns, and disinfectants are used in every clinical encounter across every healthcare setting globally, generating the highest aggregate consumption volumes of any consumables category. According to the World Health Organization's hand hygiene guidelines, healthcare workers are recommended to perform hand hygiene procedures up to 100 times per 12-hour shift in high-risk settings, and gloves are integral to many of these interactions. The sheer frequency and universality of infection control consumables use makes this the largest segment by volume and by revenue.

However, the diagnostic consumables segment is projected to register the highest CAGR during the forecast period. The expansion of molecular diagnostics, point-of-care testing, and direct-to-consumer testing is driving very rapid growth in test strips, sample collection kits, and reagent volumes. According to the In Vitro Diagnostics Association, the global IVD market is growing at approximately 5 to 6% annually, and diagnostic consumables represent the recurring revenue stream that supports this growth, as every diagnostic test consumes a defined quantity of single-use consumables regardless of the platform used.

By Application: In 2026, Surgery to Hold the Largest Share

Based on application, the global medical consumables market is segmented into surgery, patient care and monitoring, diagnostics and testing, chronic disease management, infection prevention and control, and other applications. In 2026, the surgery segment is expected to account for the largest share of the global medical consumables market. Surgical procedures are the highest-intensity consumers of single-use medical consumables, with a single complex surgical case consuming drapes, gowns, gloves, sutures, staples, surgical tapes, procedure packs, and numerous specialized consumables that together can represent several hundred dollars in consumables cost per procedure. According to the American College of Surgeons, hospital supply costs including consumables account for approximately 30 to 40% of total surgery costs, making surgical consumable spend a major component of hospital operating expenses and a large and stable demand segment.

However, the chronic disease management segment is projected to register the highest CAGR during the forecast period. The International Diabetes Federation's projection of 783 million people with diabetes by 2045, combined with the growing kidney disease patient population requiring dialysis, creates a very large and rapidly expanding recurring consumables demand base in this segment. Unlike surgical consumables that are consumed in discrete procedure episodes, chronic disease consumables generate daily or weekly recurring demand per patient across multi-year or lifetime disease management periods, making this an exceptionally durable and predictable growth segment.

By End User: In 2026, Hospitals to Hold the Largest Share

Based on end user, the global medical consumables market is segmented into hospitals, clinics, ambulatory surgical centers, home healthcare, and diagnostic laboratories. In 2026, the hospitals segment is expected to account for the largest share of the global medical consumables market. Hospitals are the most intensive users of medical consumables per facility, combining inpatient care, surgical suites, emergency departments, intensive care units, and diagnostic laboratories under one roof, each generating significant consumables consumption. According to the American Hospital Association, U.S. hospitals alone spent over USD 250 billion on supplies and services in 2022, with medical consumables representing a large share of this total. The global hospital sector, which includes over 140,000 hospitals worldwide according to WHO estimates, is the largest and most concentrated procurement channel in the market.

However, the home healthcare segment is projected to register the highest CAGR during the forecast period. The shift of care toward home settings, driven by the aging of populations, the preference of patients for home-based care, and payer pressure to reduce expensive hospitalization, is generating rapid growth in home-specific consumables from a smaller current base. The U.S. home health market is expected to grow at above-average rates through the forecast period according to the Centers for Medicare and Medicaid Services, driving corresponding growth in home healthcare consumables procurement.

Medical Consumables Market by Region: North America Leading by Share, Asia-Pacific by Growth

Based on geography, the global medical consumables market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

In 2026, North America is expected to account for the largest share of the global medical consumables market, led by the United States, which remains the world’s largest market for medical consumables. The U.S. continues to record the highest per-capita healthcare expenditure globally, exceeding $13,000 per capita in 2024, according to the Centers for Medicare & Medicaid Services, reflecting a highly intensive healthcare system with strong and recurring demand for consumables. The country is also home to leading medical device and consumables companies such as Becton Dickinson, Cardinal Health, Baxter International, and Medtronic, all of which generate significant revenues from consumables portfolios.

However, the Asia-Pacific medical consumables market is expected to grow at the fastest CAGR during the forecast period. According to the World Health Organization, the Asia-Pacific region accounts for nearly 60% of the global population and is witnessing rapid growth in healthcare utilization, driven by rising incomes, urbanization, and expanding healthcare infrastructure. In China, ongoing healthcare reforms continue to strengthen access and capacity; data from the National Health Commission of China indicates that the number of hospital beds exceeded 9.8 million by 2023, reflecting sustained infrastructure expansion and continuous demand for consumables.

In India, the Ayushman Bharat program remains a key growth driver, covering over 550 million beneficiaries as of 2024, according to the National Health Authority of India, significantly increasing hospitalization rates and demand for medical consumables. Furthermore, the International Diabetes Federation (IDF Atlas 2024) estimates that China and India remain the two largest diabetes populations globally, with approximately 148 million and 89 million adults respectively, creating a substantial and recurring demand for diabetes-related consumables such as test strips and insulin delivery devices. Japan also contributes significantly to regional demand due to its rapidly aging population; according to the Statistics Bureau of Japan, nearly 30% of the population is aged 65 years and above as of 2024, resulting in high per capita healthcare utilization and sustained consumption of medical supplies.

Europe is a large and well-established medical consumables market with high per-capita consumption, sophisticated procurement standards, and strong regulatory frameworks that ensure product quality and safety. Germany, France, the UK, and Italy are the largest European markets, each with universal or near-universal health insurance coverage that ensures broad access to hospital care and the associated consumables demand. The European medical device regulation that came into full effect in 2021 has significantly raised the clinical evidence and post-market surveillance requirements for medical consumables, increasing compliance costs but also raising quality standards. Latin America and the Middle East and Africa are earlier-stage but growing markets, with Brazil's large and growing healthcare sector, Saudi Arabia and UAE's healthcare infrastructure investment under Vision 2030, and South Africa's expanding private healthcare sector all contributing to growing regional consumables demand.

The report provides a comprehensive competitive analysis based on a thorough review of leading players' product portfolios, financial performance, geographic presence, and recent strategic developments. Some of the key players operating in the global medical consumables market include Medtronic plc (Ireland), Becton Dickinson and Company (U.S.), Cardinal Health Inc. (U.S.), 3M Company (U.S.), Baxter International Inc. (U.S.), B. Braun Melsungen AG (Germany), Johnson & Johnson/Ethicon (U.S.), Fresenius Medical Care AG & Co. KGaA (Germany), Smith & Nephew plc (UK), Boston Scientific Corporation (U.S.), Owens & Minor Inc. (U.S.), Terumo Corporation (Japan), Halyard Health/Owens & Minor (U.S.), Molnlycke Health Care AB (Sweden), and Ansell Limited (Australia), among others.

The global medical consumables market is expected to reach USD 812.4 billion by 2036 from an estimated USD 492.6 billion in 2026, at a CAGR of 5.1% during the forecast period 2026-2036.

In 2026, the infection control consumables segment is expected to hold the largest share of the global medical consumables market.

The diagnostic consumables segment is expected to register the highest CAGR during the forecast period 2026-2036, driven by the expansion of molecular diagnostics, point-of-care testing, and direct-to-consumer testing.

Diabetes is the largest single chronic disease driver of recurring consumables demand. The International Diabetes Federation's Diabetes Atlas 2023 reports that 537 million adults globally live with diabetes, a number projected to reach 783 million by 2045. Each insulin-dependent patient consumes daily drug delivery consumables, and glucose monitoring patients consume test strips or sensor consumables on an ongoing basis, creating enormous recurring procurement volumes.

The market is primarily driven by the growing global burden of chronic disease, with the IDF reporting 537 million diabetes patients and the WHO identifying cardiovascular disease as accounting for 17.9 million deaths annually, creating large and growing recurring consumables demand, combined with rising surgical volumes as healthcare access expands in developing markets where the Lancet Commission estimates 143 million additional surgical procedures are needed annually.

Key players are Medtronic plc (Ireland), Becton Dickinson and Company (U.S.), Cardinal Health Inc. (U.S.), 3M Company (U.S.), Baxter International Inc. (U.S.), B. Braun Melsungen AG (Germany), Johnson & Johnson/Ethicon (U.S.), Fresenius Medical Care AG & Co. KGaA (Germany), Smith & Nephew plc (UK), Boston Scientific Corporation (U.S.), Owens & Minor Inc. (U.S.), Terumo Corporation (Japan), Halyard Health/Owens & Minor (U.S.), Molnlycke Health Care AB (Sweden), and Ansell Limited (Australia), among others.

Asia-Pacific is expected to register the highest growth rate during the forecast period 2026-2036. According to the International Diabetes Federation's 2023 Atlas, China has 140 million and India has 77 million adult diabetes patients, the two largest national populations globally. Combined with India's Ayushman Bharat program covering approximately 500 million beneficiaries according to the National Health Authority of India, and China's hospital bed count exceeding 9 million per the National Health Commission, the region's healthcare utilization growth will drive consumables demand at above-average rates.

1. Introduction

1.1 Market Definition

1.2 Market Ecosystem

1.3 Currency and Limitations

1.3.1 Currency

1.3.2 Limitations

1.4 Key Stakeholders

2. Research Methodology

2.1 Research Approach

2.2 Data Collection & Validation Process

2.2.1 Secondary Research

2.2.2 Primary Research & Validation

2.2.2.1 Primary Interviews with Experts

2.2.2.2 Approaches for Country-/Region-Level Analysis

2.3 Market Estimation

2.3.1 Bottom-Up Approach

2.3.2 Top-Down Approach

2.3.3 Growth Forecast

2.4 Data Triangulation

2.5 Assumptions for the Study

3. Executive Summary

4. Market Overview

4.1 Introduction

4.2 Market Dynamics

4.2.1 Drivers

4.2.1.1 Rising Number of Surgical Procedures Globally

4.2.1.2 Increasing Prevalence of Chronic Diseases

4.2.1.3 Growth in Hospital Admissions and Healthcare Infrastructure

4.2.1.4 Rising Demand for Infection Control and Hygiene Products

4.2.2 Restraints

4.2.2.1 Cost Pressures and Reimbursement Challenges

4.2.2.2 Environmental Concerns Related to Disposable Waste

4.2.2.3 Supply Chain Disruptions

4.2.3 Opportunities

4.2.3.1 Growth in Home Healthcare and Self-Care

4.2.3.2 Increasing Adoption of Single-Use Medical Devices

4.2.3.3 Expansion in Emerging Markets

4.2.3.4 Innovations in Biodegradable and Sustainable Consumables

4.2.4 Challenges

4.2.4.1 Regulatory Compliance and Quality Standards

4.2.4.2 Counterfeit and Low-Quality Products

4.3 Technology and Product Landscape

4.3.1 Disposable Medical Products

4.3.2 Infection Prevention and Control Consumables

4.3.3 Minimally Invasive Procedure Consumables

4.3.4 Advanced Wound Care Materials

4.3.5 Smart and Connected Consumables

4.4 Medical Consumables Ecosystem

4.4.1 Raw Material Suppliers

4.4.2 Manufacturers

4.4.3 Distributors and Wholesalers

4.4.4 Healthcare Providers

4.4.5 Patients and End Users

4.5 Value Chain Analysis

4.5.1 Raw Material Procurement

4.5.2 Manufacturing and Packaging

4.5.3 Distribution and Logistics

4.5.4 End Use and Disposal

4.6 Regulatory and Standards Landscape

4.6.1 FDA, CE Marking, and Global Regulatory Frameworks

4.6.2 Sterilization and Quality Standards

4.6.3 Environmental and Waste Management Regulations

4.7 Porter's Five Forces Analysis

4.8 Investment and Industry Trends

4.8.1 Growth in Healthcare Infrastructure Investments

4.8.2 Increasing Mergers and Acquisitions

4.8.3 Expansion of Private Healthcare Providers

4.9 Cost and Pricing Analysis

4.9.1 Pricing by Product Category

4.9.2 Cost of Raw Materials

4.9.3 Reimbursement and Procurement Models

5. Medical Consumables Market, by Product Type

5.1 Introduction

5.2 Wound Care Consumables

5.2.1 Dressings (Advanced & Traditional)

5.2.2 Bandages

5.2.3 Sutures and Staples

5.2.4 Surgical Tapes

5.3 Drug Delivery Consumables

5.3.1 Syringes and Needles

5.3.2 IV Sets and Infusion Pump Consumables

5.3.3 Catheters

5.4 Diagnostic Consumables

5.4.1 Test Strips

5.4.2 Sample Collection Kits

5.4.3 Reagents and Assay Kits

5.5 Infection Control Consumables

5.5.1 Gloves

5.5.2 Masks and Respirators

5.5.3 Gowns and Drapes

5.5.4 Disinfectants and Sanitizers

5.6 Dialysis Consumables

5.6.1 Hemodialysis Consumables

5.6.2 Peritoneal Dialysis Consumables

5.7 Surgical Consumables

5.7.1 Surgical Kits

5.7.2 Disposable Instruments

5.7.3 Procedure Packs

5.8 Other Consumables

6. Medical Consumables Market, by Application

6.1 Introduction

6.2 Surgery

6.2.1 General Surgery

6.2.2 Orthopedic Surgery

6.2.3 Cardiovascular Surgery

6.3 Patient Care and Monitoring

6.3.1 ICU and Critical Care

6.3.2 Routine Patient Care

6.4 Diagnostics and Testing

6.5 Chronic Disease Management

6.5.1 Diabetes Care

6.5.2 Dialysis Care

6.6 Infection Prevention and Control

6.7 Other Applications

7. Medical Consumables Market, by End User

7.1 Introduction

7.2 Hospitals

7.3 Clinics

7.4 Ambulatory Surgical Centers (ASCs)

7.5 Home Healthcare

7.6 Diagnostic Laboratories

8. Medical Consumables Market, by Distribution Channel

8.1 Introduction

8.2 Direct Sales

8.3 Distributors and Wholesalers

8.4 Online Channels

9. Medical Consumables Market, by Material Type

9.1 Introduction

9.2 Plastics and Polymers

9.3 Nonwoven Materials

9.4 Rubber and Latex

9.5 Glass

9.6 Other Materials

10. Medical Consumables Market, by Sterilization Type

10.1 Introduction

10.2 Pre-Sterilized Consumables

10.3 Non-Sterilized Consumables

11. Medical Consumables Market, by Geography

11.1 Introduction

11.2 North America

11.2.1 U.S.

11.2.2 Canada

11.3 Europe

11.3.1 Germany

11.3.2 U.K.

11.3.3 France

11.3.4 Italy

11.3.5 Spain

11.3.6 Netherlands

11.3.7 Sweden

11.3.8 Switzerland

11.3.9 Rest of Europe

11.4 Asia-Pacific

11.4.1 China

11.4.2 India

11.4.3 Japan

11.4.4 South Korea

11.4.5 Australia

11.4.6 Indonesia

11.4.7 Thailand

11.4.8 Vietnam

11.4.9 Rest of Asia-Pacific

11.5 Latin America

11.5.1 Brazil

11.5.2 Mexico

11.5.3 Argentina

11.5.4 Chile

11.5.5 Colombia

11.5.6 Rest of Latin America

11.6 Middle East & Africa

11.6.1 Saudi Arabia

11.6.2 UAE

11.6.3 South Africa

11.6.4 Israel

11.6.5 Turkey

11.6.6 Rest of Middle East & Africa

12. Competitive Landscape

12.1 Overview

12.2 Key Growth Strategies

12.3 Competitive Benchmarking

12.4 Competitive Dashboard

12.4.1 Industry Leaders

12.4.2 Market Differentiators

12.4.3 Vanguards

12.4.4 Emerging Companies

12.5 Market Ranking/Positioning Analysis of Key Players, 2025

13. Company Profiles

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

13.1 Medtronic plc

13.2 Becton, Dickinson and Company (BD)

13.3 Cardinal Health, Inc.

13.4 3M Company

13.5 Baxter International Inc.

13.6 B. Braun Melsungen AG

13.7 Johnson & Johnson (Ethicon)

13.8 Fresenius Medical Care AG & Co. KGaA

13.9 Smith & Nephew plc

13.10 Boston Scientific Corporation

13.11 Owens & Minor, Inc.

13.12 Terumo Corporation

13.13 Halyard Health (Owens & Minor)

13.14 Molnlycke Health Care AB

13.15 Ansell Limited

14. Appendix

14.1 Additional Customization

14.2 Related Reports

Published Date: Feb-2026

Published Date: Jan-2025

Published Date: Jan-2025

Published Date: Jan-2025

Published Date: Jan-2025

Subscribe to get the latest industry updates