Resources

About Us

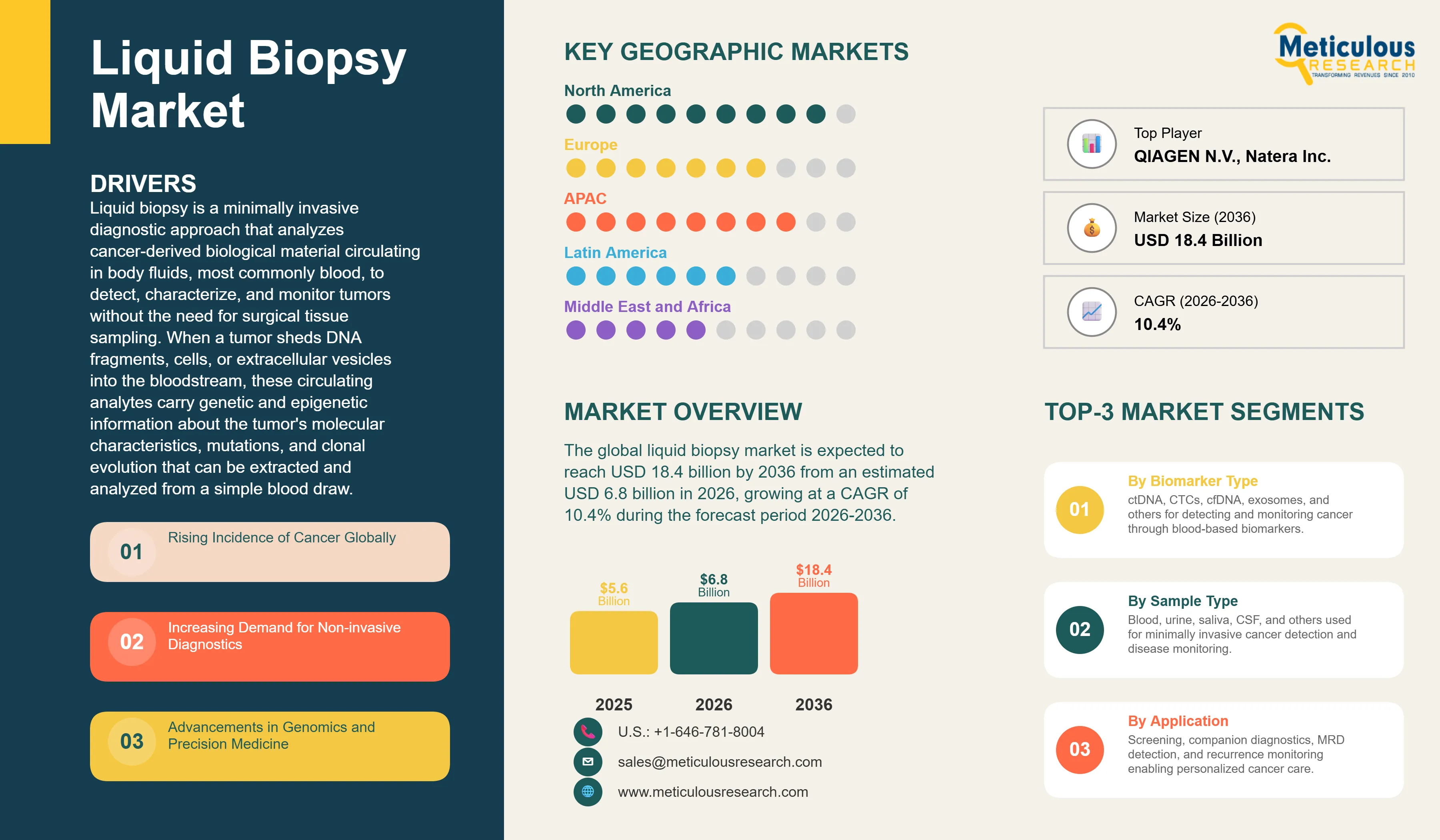

The global liquid biopsy market was valued at USD 5.6 billion in 2025. This market is expected to reach USD 18.4 billion by 2036 from an estimated USD 6.8 billion in 2026, growing at a CAGR of 10.4% during the forecast period 2026-2036. According to the World Health Organization's World Cancer Report 2024, cancer is the second leading cause of death globally and accounted for approximately 9.7 million deaths in 2022, with an estimated 20 million new cancer cases diagnosed that year. The burden is projected to rise to 35 million new cases by 2050, a 77% increase from 2022, largely driven by population aging and exposure to risk factors. This growing global cancer burden, combined with the compelling clinical case for earlier and less invasive cancer detection, is the fundamental driver of the liquid biopsy market's sustained and rapid growth.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Liquid biopsy is a minimally invasive diagnostic approach that analyzes cancer-derived biological material circulating in body fluids, most commonly blood, to detect, characterize, and monitor tumors without the need for surgical tissue sampling. When a tumor sheds DNA fragments, cells, or extracellular vesicles into the bloodstream, these circulating analytes carry genetic and epigenetic information about the tumor's molecular characteristics, mutations, and clonal evolution that can be extracted and analyzed from a simple blood draw. Compared with conventional tissue biopsy, liquid biopsy offers the ability to sample the tumor continuously over time, capture tumor heterogeneity across multiple metastatic sites simultaneously, detect minimal residual disease after treatment, and identify emerging resistance mutations that are driving tumor progression.

The market is growing rapidly because liquid biopsy has successfully transitioned from a research tool into a commercially deployed clinical diagnostic with multiple FDA-approved applications. Guardant Health's Guardant360 CDx was FDA-approved as a companion diagnostic for multiple targeted therapies in non-small cell lung cancer and other solid tumors. Foundation Medicine's FoundationOne Liquid CDx received FDA approval as a companion diagnostic across multiple tumor types using ctDNA from plasma. According to the FDA's oncology database, more than 30 companion diagnostic approvals currently reference liquid biopsy-based tests as the recommended testing approach, establishing liquid biopsy as a mainstream clinical workflow in oncology treatment selection. The global oncology diagnostics investment wave documented by the American Cancer Society's 2025 cancer statistics report, which identified approximately 2 million new cancer cases expected in the U.S. in 2025 alone, confirms the scale of the clinical opportunity.

The most transformative near-term growth opportunity is multi-cancer early detection, where a single blood test can simultaneously screen for signals of multiple cancer types years before symptoms appear. Grail's Galleri test, which uses methylation analysis of cell-free DNA to detect signals across more than 50 cancer types with a single blood draw, received FDA Breakthrough Device designation and has been commercially available in the United States since 2021. According to Grail's 2025 clinical update, large prospective studies including the NHS-Galleri trial in the UK, which enrolled approximately 140,000 participants, are generating the real-world evidence needed to support insurance coverage decisions and potential FDA approval. A positive outcome from these pivotal studies would represent the largest single commercial expansion event in the liquid biopsy market's history.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 18.4 Billion |

|

Market Size in 2026 |

USD 6.8 Billion |

|

Market Size in 2025 |

USD 5.6 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 10.4% |

|

Dominating Biomarker Type |

Circulating Tumor DNA (ctDNA) |

|

Fastest Growing Biomarker Type |

Extracellular Vesicles (Exosomes) |

|

Dominating Sample Type |

Blood (Plasma/Serum) |

|

Fastest Growing Sample Type |

Urine |

|

Dominating Application |

Therapy Selection/Companion Diagnostics |

|

Fastest Growing Application |

Cancer Screening & Early Detection (MCED) |

|

Dominating Cancer Type |

Lung Cancer |

|

Fastest Growing Cancer Type |

Pancreatic Cancer |

|

Dominating End User |

Diagnostic Laboratories |

|

Fastest Growing End User |

Pharmaceutical & Biotechnology Companies |

|

Dominating Technology |

NGS-based Testing |

|

Fastest Growing Technology |

Digital PCR (dPCR) |

|

Dominating Product Type |

Assays & Kits |

|

Fastest Growing Product Type |

Software & Services |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Multi-Cancer Early Detection Approaching Pivotal Regulatory and Coverage Milestones

Multi-cancer early detection tests represent the most commercially significant emerging application in the liquid biopsy market, with the potential to transform cancer diagnosis from a predominantly symptomatic disease discovery process into a population-level screening program that catches cancers years earlier than conventional diagnosis. The clinical rationale is compelling: the WHO's World Cancer Report 2024 notes that five-year survival rates for most cancers are dramatically higher when detected at Stage I versus Stage III or IV, and most cancers currently diagnosed in the symptomatic stage have already progressed beyond early intervention windows. An MCED test that can be ordered alongside a routine blood test offers the scalability and convenience that no imaging-based screening program can match.

The pivotal commercial moment for MCED will arrive with the results of the NHS-Galleri trial, which enrolled approximately 140,000 participants in the UK and is generating prospective data on whether Grail's Galleri test can reduce late-stage cancer diagnosis rates in a real-world population screening context. According to Grail's 2025 communications, interim data from the trial is expected to be published in high-impact medical journals through 2025 and 2026, with final results informing NHS coverage decisions and the FDA's regulatory review. Simultaneously, Exact Sciences, Illumina, and several other companies are developing competing MCED platforms, and the Chinese genomics leader BGI has been conducting MCED research programs in China's large population. A successful regulatory outcome for any major MCED product would dramatically expand the total addressable market for liquid biopsy beyond its current oncology treatment monitoring and companion diagnostic base into mass population screening.

Minimal Residual Disease Detection Becoming Standard of Care in Hematologic and Solid Tumors

Minimal residual disease detection using liquid biopsy, where ctDNA or circulating tumor cells are analyzed after treatment to determine whether the cancer has been completely eliminated or whether residual disease remains that could cause relapse, is transitioning from a research application to clinical standard of care across multiple tumor types. In hematological malignancies, MRD detection by sensitive molecular testing has been part of treatment monitoring protocols for years, and the extension of this capability to solid tumors through ctDNA liquid biopsy is one of the most clinically impactful recent developments in oncology diagnostics.

Natera's Signatera personalized ctDNA test, which is designed specifically for MRD detection in treated solid tumor patients, received Medicare coverage and has been commercially deployed across colorectal, breast, and lung cancer treatment monitoring programs. According to Natera's 2025 financial results, Signatera test volumes grew at above-average rates compared with the company's overall oncology testing portfolio, confirming the strong clinical adoption of ctDNA MRD monitoring in standard oncology practice. A landmark study published in the New England Journal of Medicine in 2024 demonstrated that ctDNA-guided adjuvant chemotherapy decisions in colorectal cancer resulted in equivalent outcomes with significantly less chemotherapy exposure in patients who were ctDNA-negative after surgery, providing clinical evidence that liquid biopsy MRD results can directly guide treatment escalation and de-escalation decisions that affect patient outcomes and healthcare costs.

NGS-Based Comprehensive Genomic Profiling Expanding Companion Diagnostic Applications

The approval of an increasing number of targeted cancer therapies has created corresponding demand for companion diagnostic tests that identify which patients carry the specific genomic alterations that make those therapies effective. Each new targeted therapy approval that specifies a companion diagnostic as the required patient selection method creates a recurring liquid biopsy testing requirement for every patient being considered for that therapy in clinical practice. According to the FDA's oncology database and Foundation Medicine's 2025 communications, Foundation One Liquid CDx is currently specified as a companion diagnostic for therapies targeting EGFR, ALK, ROS1, KRAS, and multiple other oncogenes across non-small cell lung cancer, colorectal cancer, ovarian cancer, and other tumor types, making it the most FDA-approved liquid biopsy companion diagnostic test globally.

Guardant Health reported revenues of approximately USD 687 million in 2024 per its annual report, with the majority derived from its Guardant360 CDx companion diagnostic platform serving oncologists selecting targeted therapies for patients with solid tumors. The company's precision oncology business grew above average in 2024, driven by both the increasing use of existing companion diagnostic approvals and the qualification of Guardant360 CDx for new therapy approvals. Illumina's oncology products division, which supplies the next-generation sequencing platforms underpinning many laboratory-developed liquid biopsy tests, reported continued strong demand from clinical and research laboratories expanding their ctDNA testing programs in 2025.

Rising Incidence of Cancer Globally

According to the World Health Organization's World Cancer Report 2024, approximately 20 million new cancer cases were diagnosed globally in 2022 and approximately 9.7 million cancer deaths occurred in that year. The WHO projects that the global cancer burden will continue growing, driven by aging populations, rising rates of lifestyle-associated risk factors, and improved cancer detection in previously underdiagnosed populations, with an estimated 35 million new cases projected annually by 2050. The American Cancer Society's Cancer Facts and Figures 2025 report estimates approximately 2 million new cancer cases and approximately 611,000 cancer deaths in the United States in 2025, sustaining the United States as the world's largest individual market for oncology diagnostics including liquid biopsy tests. Each new cancer diagnosis in principle represents a clinical need for liquid biopsy testing across multiple phases from initial genomic profiling for treatment selection through treatment monitoring and post-treatment MRD surveillance.

Advancements in Genomics and Precision Medicine

The commercial deployment of FDA-approved liquid biopsy companion diagnostics for an expanding portfolio of targeted therapies has created a self-reinforcing cycle of market growth: each new targeted therapy approval creates a companion diagnostic testing requirement, which generates commercial volume that funds further assay development, which supports additional clinical validation studies, which leads to further therapy approvals. According to the Pharmaceutical Research and Manufacturers of America's 2025 annual report, the oncology pipeline contains over 1,600 medicines/treatments in clinical development in the United States alone, a very large proportion of which are targeted therapies requiring molecular testing for patient selection. The progressive shift of oncology treatment from cytotoxic chemotherapy toward molecularly targeted agents and immunotherapies requiring biomarker selection is the fundamental commercial engine driving the companion diagnostic segment of the liquid biopsy market.

Expansion in Multi-cancer Early Detection (MCED)

Multi-cancer early detection using methylation analysis of cell-free DNA represents the largest single commercial expansion opportunity in the liquid biopsy market's history, with the potential total addressable market encompassing the entire adult population over specified age thresholds rather than the cancer patient population that comprises the current market. The clinical and economic case for MCED is anchored in the well-established correlation between cancer stage at detection and treatment outcomes and costs: Stage I cancers are typically curable at a fraction of the cost of treating Stage IV disease. The NHS-Galleri trial, which enrolled approximately 140,000 UK participants according to Grail's 2025 communications, is generating the prospective evidence base that regulators and payers require before approving coverage of population-level cancer screening with MCED tests. According to IQVIA's 2025 Oncology Trends report, the oncology diagnostics investment pipeline includes at least six commercial organizations developing MCED products that could reach clinical and regulatory maturity within the forecast period, indicating the scale of commercial interest in this segment.

Integration with AI and Genomic Analytics

The integration of artificial intelligence with liquid biopsy genomic data analysis is enabling new levels of diagnostic sensitivity and clinical insight that are expanding the utility of liquid biopsy across additional cancer types and clinical questions. AI algorithms trained on large datasets of ctDNA methylation patterns, copy number variations, and mutation signatures can detect cancer signals in cell-free DNA at concentrations too low for conventional analysis methods, improving the sensitivity of early detection tests in exactly the clinical context where sensitivity is most critical. According to Grail's published research validating its Galleri test methodology, the AI-based signal interpretation approach using methylation sequencing achieves a tissue of origin prediction accuracy above 90% when a cancer signal is detected, providing clinically actionable information about which cancer type to investigate further rather than just a positive or negative screening result. Foundation Medicine and Guardant Health have both disclosed investments in AI-based interpretation of liquid biopsy genomic data to improve the clinical actionability of their comprehensive genomic profiling results.

By Biomarker Type: In 2026, ctDNA to Hold the Largest Share

Based on biomarker type, the global liquid biopsy market is segmented into circulating tumor DNA, circulating tumor cells, cell-free DNA, extracellular vesicles (exosomes), and other biomarkers. In 2026, the circulating tumor DNA segment is expected to account for the largest share of the global liquid biopsy market. ctDNA analysis forms the technical foundation of the most commercially successful and FDA-approved liquid biopsy products, including Guardant360 CDx and Foundation One Liquid CDx for companion diagnostics and Natera's Signatera for MRD monitoring. The ctDNA segment benefits from the most extensive clinical validation evidence base, the largest number of FDA-approved companion diagnostic applications, and the most mature NGS and dPCR technology platforms for ctDNA analysis. Guardant Health's approximately USD 687 million in 2024 revenues, principally from ctDNA-based liquid biopsy, illustrates the commercial scale of the ctDNA market.

However, the extracellular vesicles (exosomes) segment is projected to register the highest CAGR during the forecast period. Exosomes carry RNA, proteins, and lipids in addition to DNA fragments, providing a richer biological information content than naked cfDNA, and their surface proteins may enable tissue-specific identification and earlier cancer detection than DNA-based approaches alone. While the exosome analysis field is earlier in clinical development than ctDNA, the growing research pipeline and commercial investment in exosome diagnostics platform companies is expected to drive above-average market growth as clinical evidence accumulates.

By Application: In 2026, Therapy Selection / Companion Diagnostics to Hold the Largest Share

Based on application, the global liquid biopsy market is segmented into cancer screening and early detection, therapy selection and companion diagnostics, treatment monitoring and MRD, and recurrence monitoring. In 2026, the therapy selection and companion diagnostics segment is expected to account for the largest share of the global liquid biopsy market. This application represents the most commercially mature and reimbursed segment of the liquid biopsy market, with over 30 FDA-approved companion diagnostic designations currently referencing liquid biopsy testing according to FDA's oncology database. Every patient with advanced non-small cell lung cancer, for example, requires molecular profiling including for EGFR, ALK, ROS1, KRAS G12C, and other targetable alterations, and liquid biopsy ctDNA testing is the clinically preferred approach when tissue is unavailable or insufficient for comprehensive molecular testing.

However, the cancer screening and early detection segment, particularly MCED, is projected to register the highest CAGR during the forecast period. The potential commercial impact of successful MCED regulatory approval and insurance coverage for population-level screening would be transformative for this segment, creating a total addressable market far larger than the treatment-setting applications that currently dominate the market. According to IQVIA's 2025 Oncology Trends report, multi-cancer screening is identified as the highest-priority growth vector in oncology diagnostics investment.

By Cancer Type: In 2026, Lung Cancer to Hold the Largest Share

Based on cancer type, the global liquid biopsy market is segmented into lung cancer, breast cancer, colorectal cancer, prostate cancer, liver cancer, pancreatic cancer, and other cancer types. In 2026, the lung cancer segment is expected to account for the largest share of the global liquid biopsy market. Lung cancer has the most extensive and clinically validated liquid biopsy companion diagnostic ecosystem of any cancer type, with multiple FDA-approved targeted therapies specifying ctDNA or tissue NGS as the required companion diagnostic approach for patient selection. According to the American Cancer Society's 2025 Cancer Facts and Figures, lung and bronchus cancer remains the leading cause of cancer death in the United States, with approximately 125,000 deaths estimated in 2025, sustaining its position as the highest-priority cancer type for advanced molecular diagnostics including liquid biopsy.

However, the pancreatic cancer segment is projected to register the highest CAGR during the forecast period. Pancreatic cancer has the lowest five-year survival rate of any major cancer type, at approximately 13% according to the American Cancer Society's 2025 data, largely because the vast majority of cases are diagnosed at advanced stages when curative treatment is no longer possible. The clinical urgency for early detection tools in pancreatic cancer is extreme, and liquid biopsy early detection research programs specifically targeting pancreatic cancer biomarkers are among the most intensively funded areas of the liquid biopsy research pipeline.

Liquid Biopsy Market by Region: North America Leading by Share, Asia-Pacific by Growth

Based on geography, the global liquid biopsy market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

In 2026, North America is expected to account for the largest share of the global liquid biopsy market. The United States is the world's most advanced liquid biopsy market by regulatory approvals, clinical adoption, and commercial revenue. According to the American Cancer Society's 2025 Cancer Facts and Figures, approximately 2 million new cancer cases were expected in the U.S. in 2025, providing the patient population foundation for the world's largest oncology diagnostics market. The FDA's oncology diagnostic approval process has produced more liquid biopsy companion diagnostic approvals than any other regulatory authority, with Guardant Health and Foundation Medicine's Roche having between them the largest number of approved companion diagnostic indications globally. Guardant Health reported revenues of approximately USD 687 million in 2024 per its annual report, with above-average revenue growth in its precision oncology segment driven by companion diagnostic volume expansion. The Centers for Medicare and Medicaid Services provides Medicare coverage for several liquid biopsy tests in oncology including the Foundation One Liquid CDx for patients with solid tumors and Natera's Signatera for colorectal cancer MRD monitoring, and this reimbursement coverage is a critical enabler of commercial adoption at scale.

However, the Asia-Pacific liquid biopsy market is expected to grow at the fastest CAGR during the forecast period. Asia-Pacific carries a very large share of the global cancer burden: according to the WHO's World Cancer Report 2024, Asia accounts for approximately 49% of global cancer cases and approximately 56% of global cancer deaths, driven by the region's large population and elevated rates of specific cancer types including liver, stomach, esophageal, and cervical cancer. China has the world's largest absolute cancer incidence and is experiencing rapid adoption of precision oncology diagnostics driven by growing clinical oncology infrastructure, favorable government policies for innovative diagnostics, and the commercial activities of domestic liquid biopsy companies including Berry Genomics and Burning Rock Biotech alongside global players including Roche, Illumina, and Thermo Fisher Scientific. According to Burning Rock Biotech's 2025 investor communications, the Chinese liquid biopsy market is growing rapidly as oncology treatment guidelines increasingly incorporate molecular testing requirements. Japan's well-developed oncology diagnostics infrastructure and high awareness of cancer screening, South Korea's advanced healthcare IT ecosystem, and Singapore's position as an Asia-Pacific clinical research hub all contribute to regional growth momentum.

The liquid biopsy market is served by specialist liquid biopsy diagnostics companies with dedicated ctDNA and cfDNA testing platforms, large diversified diagnostics and genomics companies with liquid biopsy products as part of their broader oncology portfolios, and platform technology companies whose sequencing and analysis instruments underpin many laboratory-developed liquid biopsy tests. Competition is based on analytical sensitivity and specificity across the cancer types and clinical applications being addressed, the number and breadth of FDA companion diagnostic approvals, reimbursement coverage depth, laboratory turnaround time and service quality, and the comprehensiveness of the genomic profiling information provided per test.

The report provides a comprehensive competitive analysis based on a thorough review of leading players' product approvals, clinical evidence portfolios, geographic presence, and recent strategic developments. Some of the key players operating in the global liquid biopsy market include Guardant Health Inc. (U.S.), Illumina Inc. (U.S.), Roche Diagnostics (Switzerland), Thermo Fisher Scientific Inc. (U.S.), Bio-Rad Laboratories Inc. (U.S.), QIAGEN N.V. (Netherlands), Exact Sciences Corporation (U.S.), Foundation Medicine/Roche (U.S.), NeoGenomics Laboratories (U.S.), Natera Inc. (U.S.), Freenome Holdings Inc. (U.S.), Grail Inc. (U.S.), Myriad Genetics Inc. (U.S.), Sysmex Corporation (Japan), and Menarini Silicon Biosystems (Italy), among others.

The global liquid biopsy market is expected to reach USD 18.4 billion by 2036 from an estimated USD 6.8 billion in 2026, at a CAGR of 10.4% during the forecast period 2026-2036.

In 2026, the circulating tumor DNA segment is expected to hold the largest share of the global liquid biopsy market.

The cancer screening and early detection segment, particularly multi-cancer early detection, is projected to register the highest CAGR during the forecast period.

The pancreatic cancer segment is projected to register the highest CAGR during the forecast period.

The NHS-Galleri trial, which enrolled approximately 140,000 UK participants according to Grail's 2025 communications, is the world's most important prospective validation study for multi-cancer early detection using liquid biopsy. Its results will directly inform NHS coverage decisions for MCED screening and the FDA's regulatory review pathway for Galleri and potentially competing MCED products, with a positive outcome representing the largest single commercial expansion event in the liquid biopsy market's history.

The market is primarily driven by the WHO's World Cancer Report 2024 documenting approximately 20 million new global cancer cases annually and the progressive expansion of FDA companion diagnostic approvals for liquid biopsy tests, with over 30 current approved applications creating mandatory clinical testing requirements. The American Cancer Society's 2025 report projecting approximately 2 million new U.S. cancer cases in 2025 confirms the sustained scale of clinical demand underpinning the market.

Key players are Guardant Health Inc. (U.S.), Illumina Inc. (U.S.), Roche Diagnostics (Switzerland), Thermo Fisher Scientific Inc. (U.S.), Bio-Rad Laboratories Inc. (U.S.), QIAGEN N.V. (Netherlands), Exact Sciences Corporation (U.S.), Foundation Medicine/Roche (U.S.), NeoGenomics Laboratories (U.S.), Natera Inc. (U.S.), Freenome Holdings Inc. (U.S.), Grail Inc. (U.S.), Myriad Genetics Inc. (U.S.), Sysmex Corporation (Japan), and Menarini Silicon Biosystems (Italy), among others.

Asia-Pacific is expected to register the highest growth rate in the global liquid biopsy market during the forecast period 2026-2036, driven by the WHO's World Cancer Report 2024 identifying Asia as carrying approximately 49% of global cancer cases, China's rapidly expanding precision oncology market, and the growing clinical adoption of companion diagnostics and molecular testing requirements across Japan, South Korea, and Singapore's advanced healthcare systems.

1. Introduction

1.1 Market Definition

1.2 Scope

1.3 Market Ecosystem

1.4 Currency and Limitations

1.4.1 Currency

1.4.2 Limitations

1.5 Key Stakeholders

2. Research Methodology

2.1 Research Approach

2.2 Data Collection & Validation

2.2.1 Secondary Research

2.2.2 Primary Research

2.3 Market Estimation

2.3.1 Bottom-Up Approach

2.3.2 Top-Down Approach

2.3.3 Forecast Modeling

2.4 Data Triangulation

2.5 Assumptions

3. Executive Summary

4. Market Overview

4.1 Introduction

4.2 Market Dynamics

4.2.1 Drivers

4.2.1.1 Rising Incidence of Cancer Globally

4.2.1.2 Increasing Demand for Non-invasive Diagnostics

4.2.1.3 Advancements in Genomics and Precision Medicine

4.2.1.4 Growing Adoption of Early Cancer Screening

4.2.2 Restraints

4.2.2.1 High Cost of Testing and Limited Reimbursement

4.2.2.2 Sensitivity and Accuracy Challenges

4.2.2.3 Regulatory and Clinical Validation Barriers

4.2.3 Opportunities

4.2.3.1 Expansion in Multi-cancer Early Detection (MCED)

4.2.3.2 Integration with AI and Genomic Analytics

4.2.3.3 Growth in Companion Diagnostics

4.2.3.4 Adoption in Emerging Markets

4.2.4 Challenges

4.2.4.1 Standardization of Testing Protocols

4.2.4.2 Clinical Adoption and Physician Awareness

4.3 Technology Landscape

4.3.1 Next-Generation Sequencing (NGS)

4.3.2 Polymerase Chain Reaction (PCR)-based Techniques

4.3.3 Digital PCR (dPCR)

4.3.4 Microarrays

4.3.5 Emerging Technologies (Single-cell analysis, AI-based analytics)

4.4 Liquid Biopsy Ecosystem

4.4.1 Diagnostic & Genomics Companies

4.4.2 Pharmaceutical & Biotechnology Firms

4.4.3 Clinical Laboratories

4.4.4 Research Institutes

4.4.5 Healthcare Providers

4.5 Value Chain Analysis

4.5.1 Sample Collection

4.5.2 Sample Processing

4.5.3 Biomarker Detection

4.5.4 Data Analysis

4.5.5 Clinical Reporting

4.6 Regulatory Landscape

4.6.1 FDA & Global Regulatory Approvals

4.6.2 Companion Diagnostics Guidelines

4.6.3 Reimbursement Policies

4.7 Industry Trends

4.7.1 Growth in Multi-cancer Screening

4.7.2 Rise of Personalized Medicine

4.7.3 Integration with Digital Health Platforms

4.7.4 Increasing Investment in Oncology Diagnostics

4.8 Cost and Pricing Analysis

4.8.1 Cost by Technology Type

4.8.2 Pricing Trends by Application

4.8.3 Reimbursement Landscape

5. Liquid Biopsy Market, by Biomarker Type

5.1 Introduction

5.2 Circulating Tumor DNA (ctDNA)

5.3 Circulating Tumor Cells (CTCs)

5.4 Cell-free DNA (cfDNA)

5.5 Extracellular Vesicles (Exosomes)

5.6 Other Biomarkers

6. Liquid Biopsy Market, by Sample Type

6.1 Blood (Plasma/Serum)

6.2 Urine

6.3 Saliva

6.4 Cerebrospinal Fluid (CSF)

6.5 Other Sample Types

7. Liquid Biopsy Market, by Application

7.1 Introduction

7.2 Cancer Screening & Early Detection

7.3 Therapy Selection / Companion Diagnostics

7.4 Treatment Monitoring & Minimal Residual Disease (MRD)

7.5 Recurrence Monitoring

8. Liquid Biopsy Market, by Cancer Type

8.1 Lung Cancer

8.2 Breast Cancer

8.3 Colorectal Cancer

8.4 Prostate Cancer

8.5 Liver Cancer

8.6 Pancreatic Cancer

8.7 Other Cancer Types

9. Liquid Biopsy Market, by End User

9.1 Hospitals & Clinics

9.2 Diagnostic Laboratories

9.3 Academic & Research Institutes

9.4 Pharmaceutical & Biotechnology Companies

10. Liquid Biopsy Market, by Technology

10.1 NGS-based Testing

10.2 PCR-based Testing

10.3 Digital PCR (dPCR)

10.4 Microarrays

10.5 Other Technologies

11. Liquid Biopsy Market, by Product Type

11.1 Assays & Kits

11.2 Instruments

11.3 Software & Services

12. Liquid Biopsy Market, by Geography

12.1 Introduction

12.2 North America

12.2.1 U.S.

12.2.2 Canada

12.3 Europe

12.3.1 Germany

12.3.2 U.K.

12.3.3 France

12.3.4 Italy

12.3.5 Spain

12.3.6 Netherlands

12.3.7 Sweden

12.3.8 Switzerland

12.3.9 Rest of Europe

12.4 Asia-Pacific

12.4.1 China

12.4.2 Japan

12.4.3 India

12.4.4 South Korea

12.4.5 Australia

12.4.6 Singapore

12.4.7 Rest of Asia-Pacific

12.5 Latin America

12.5.1 Brazil

12.5.2 Mexico

12.5.3 Rest of Latin America

12.6 Middle East & Africa

12.6.1 UAE

12.6.2 Saudi Arabia

12.6.3 South Africa

12.6.4 Rest of MEA

13. Competitive Landscape

13.1 Overview

13.2 Key Growth Strategies

13.3 Competitive Benchmarking

13.4 Competitive Dashboard

13.4.1 Industry Leaders

13.4.2 Market Differentiators

13.4.3 Emerging Players

13.5 Market Ranking/Positioning Analysis

14. Company Profiles

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

14.1 Guardant Health, Inc.

14.2 Illumina, Inc.

14.3 Roche Diagnostics

14.4 Thermo Fisher Scientific Inc.

14.5 Bio-Rad Laboratories, Inc.

14.6 QIAGEN N.V.

14.7 Exact Sciences Corporation

14.8 Foundation Medicine (Roche)

14.9 NeoGenomics Laboratories

14.10 Natera, Inc.

14.11 Freenome Holdings, Inc.

14.12 Grail, Inc.

14.13 Myriad Genetics, Inc.

14.14 Sysmex Corporation

14.15 Menarini Silicon Biosystems

15. Appendix

15.1 Customization Options

15.2 Related Reports

Published Date: Jun-2026

Published Date: Jun-2026

Published Date: Jun-2026

Published Date: Nov-2022

Subscribe to get the latest industry updates