Resources

About Us

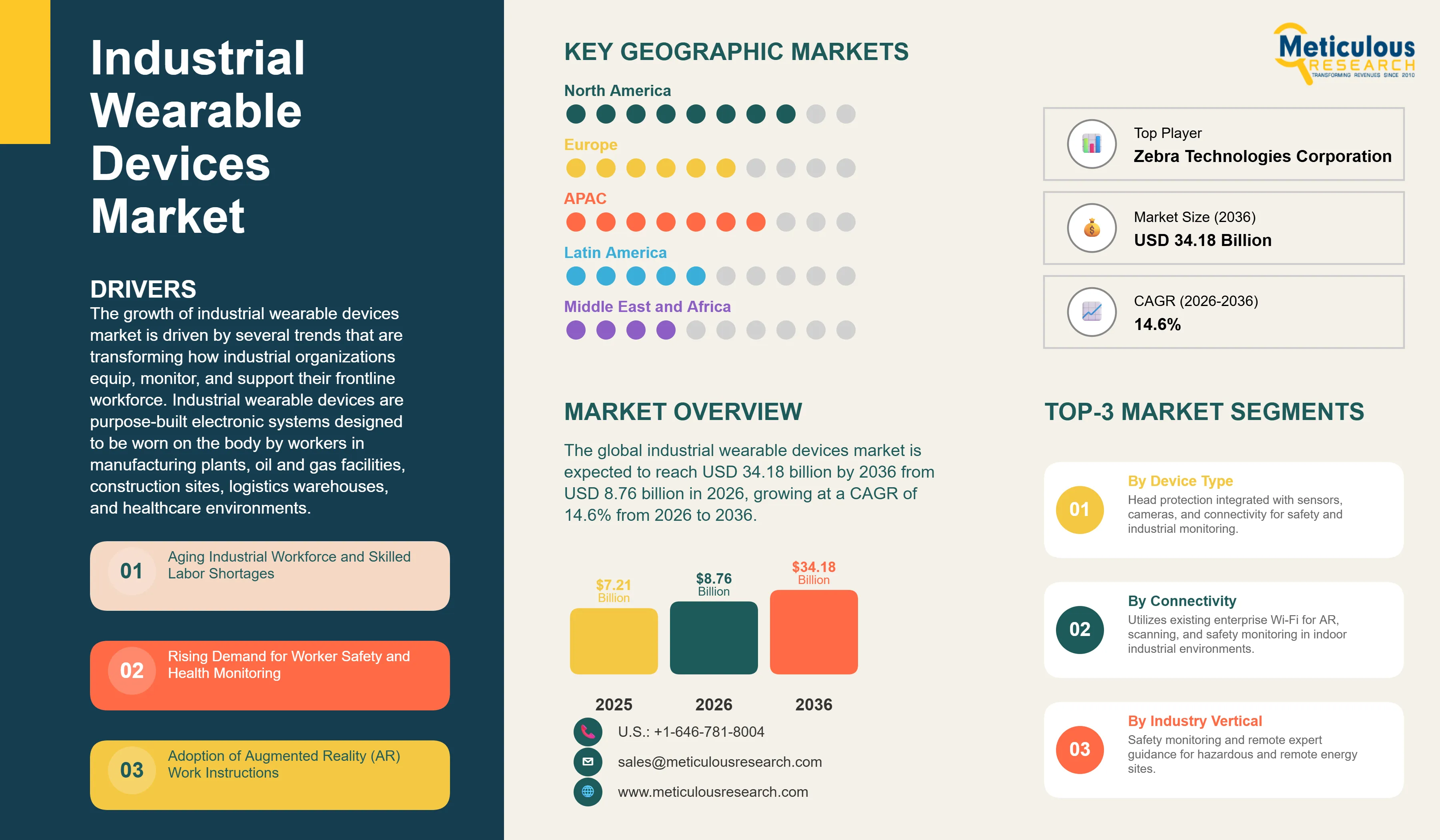

The global industrial wearable devices market was valued at USD 7.21 billion in 2025. This market is expected to reach USD 34.18 billion by 2036 from USD 8.76 billion in 2026, growing at a CAGR of 14.6% from 2026 to 2036.

The growth of this market is driven by several trends that are transforming how industrial organizations equip, monitor, and support their frontline workforce. Industrial wearable devices are purpose-built electronic systems designed to be worn on the body by workers in manufacturing plants, oil and gas facilities, construction sites, logistics warehouses, and healthcare environments. These devices differ fundamentally from consumer wearables in their design priorities: they are engineered for durability in harsh environments, compliance with occupational safety standards, all-day battery life under continuous use, compatibility with personal protective equipment, and integration with enterprise software platforms rather than consumer applications. Core product categories include smart glasses and augmented reality headsets that overlay digital information onto the worker's field of view, smart helmets that integrate sensors and communications into head protection, body-worn sensor systems that track physiological and environmental safety parameters, wrist-worn devices such as ruggedized smartwatches and wearable barcode scanners, and powered exoskeletons that reduce physical strain during manual handling tasks.

Several factors are driving the adoption of industrial wearables across key end markets. The aging of the skilled industrial workforce and the difficulty of retaining and training replacement workers is increasing the value of wearable-enabled remote expert guidance and step-by-step augmented reality work instructions that allow less experienced workers to perform complex tasks with fewer errors and less supervision. Industrial safety regulations in major markets are becoming increasingly data-driven, and wearable sensor platforms that continuously monitor worker vital signs, environmental gas concentrations, ergonomic risk, and proximity to hazardous equipment provide the real-time safety data that regulatory compliance programs and corporate safety management systems increasingly require. The rollout of private 5G networks in large industrial facilities is enabling a new generation of connected wearable applications that require low-latency, high-bandwidth wireless connectivity that previous Wi-Fi infrastructure could not reliably provide across large plant footprints.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Industrial wearable devices represent a distinct product category within the broader wearable technology market, defined by their design for use in physically demanding, safety-critical, and often hazardous industrial environments. The core technical requirements that differentiate industrial wearables from consumer wearables include ruggedization to IP65 or IP67 ingress protection ratings for dust and water resistance, compliance with relevant electrical safety standards for use in potentially explosive atmospheres, compatibility with hard hats, safety glasses, hearing protection, and gloves that workers in industrial settings are required to wear simultaneously, battery life sufficient for a full 8 to 12 hour work shift under continuous active use, and integration with enterprise resource planning, manufacturing execution, and industrial IoT platform software rather than consumer app ecosystems.

The industrial wearable device market encompasses five primary product categories that key players develop, brand, and sell as distinct product lines. Smart glasses and augmented reality headsets overlay digital information such as work instructions, equipment schematics, inventory data, and live video from remote experts onto the worker's field of view through a transparent display positioned in front of one or both eyes. Companies including RealWear with its HMT-1 and Navigator 500 head-mounted tablets, Google with Google Glass Enterprise Edition, and Honeywell with its Honeywell Intelligent Wearables platform lead this segment. Smart helmets integrate connectivity, cameras, sensors, and display capability into certified head protection, serving construction, mining, and energy sectors where head protection is mandatory and where the helmet provides a practical platform for sensor mounting. Body-worn sensors and safety wearables include clip-on gas detectors from Blackline Safety and MSA Safety, connected harness systems that detect falls, ergonomic monitoring bands from Kinetic and StrongArm Technologies that track unsafe movement patterns, and physiological monitoring devices that measure heart rate, core body temperature, and fatigue indicators. Wrist-worn devices encompass ruggedized smartwatches for worker communications and alert notification as well as wrist-mounted barcode and RFID scanners from Zebra Technologies and Honeywell that free warehouse workers' hands while maintaining scanning capability. Powered and passive exoskeletons from Ekso Bionics, SuitX, Ottobock, and Sarcos Technology support workers performing repetitive overhead assembly, heavy lifting, and prolonged standing by augmenting or offloading the physical effort required.

The competitive landscape of the industrial wearable devices market spans established industrial technology conglomerates, specialist wearable hardware developers, and enterprise software platform providers that increasingly bundle hardware and software into integrated solution offerings. Honeywell and Zebra Technologies represent the large industrial technology players that have built or acquired wearable product lines alongside their broader portfolio of industrial automation, safety, and data capture products. RealWear, Osterhout Design Group, and Vuzix are specialist AR headset developers focused exclusively on industrial head-worn computing. Blackline Safety, Guardhat, and Kenzen are specialist body-worn sensor and safety monitoring companies. Ekso Bionics and Sarcos compete in the emerging powered exoskeleton segment. Enterprise software companies including PTC with its Vuforia augmented reality platform and Scope AR provide the software layer that many hardware-agnostic industrial wearable deployments are built upon, creating a layered market structure where hardware and software are increasingly procured from different vendors and integrated by system integrators.

Augmented Reality Work Instructions Replacing Paper-Based Procedures

The replacement of paper-based work instructions, printed procedure manuals, and computer-terminal-based guidance systems with wearable augmented reality work instruction platforms is one of the most commercially significant trends driving the industrial wearable devices market. In manufacturing environments where assembly workers must execute complex, multi-step processes with precise specifications, the ability to display step-by-step visual instructions directly in the worker's field of view through AR headsets reduces reliance on memorized procedures and paper documents, decreases error rates, and reduces the time required for new worker training and certification. Boeing has publicly reported that AR-guided wire harness assembly reduced wiring production time by 25% and error rates to near zero in its commercial aircraft manufacturing operations. Companies including Airbus, BMW, General Electric, and Siemens have deployed AR work instruction platforms across assembly and maintenance operations with similar productivity and quality outcomes.

The commercial infrastructure supporting AR work instruction deployment has matured significantly. Software platforms from PTC Vuforia, Scope AR, Proceedix, and Apprentice.io enable industrial engineers to author AR work instruction content without specialized programming skills, using drag-and-drop tools that overlay 3D models, video clips, text annotations, and sensor data onto physical equipment and workstations. These platforms connect with existing PLM, ERP, and MES systems to pull current revision-controlled work instructions automatically, ensuring that workers always follow the most current procedure version. Hardware platforms including RealWear Navigator 500 and Google Glass Enterprise Edition 2 are optimized for this use case, with voice command interfaces that allow workers to navigate through procedure steps without removing gloves or interrupting their work.

Private 5G Networks Enabling a New Generation of Connected Wearable Applications

The deployment of private 5G networks in large manufacturing plants, oil refineries, mining sites, and port logistics facilities is enabling a new generation of industrial wearable applications that require connectivity performance levels that existing enterprise Wi-Fi infrastructure cannot reliably provide. Private 5G networks offer deterministic low latency, typically below 10 milliseconds, that is required for augmented reality applications where any perceptible lag between head movement and display update causes user discomfort and adoption resistance. They also provide reliable connectivity across large outdoor areas such as plant yards, port terminals, and open-pit mining sites where Wi-Fi access point density is impractical. Additionally, they support simultaneous high-bandwidth connections to hundreds of wearable devices without the performance degradation that occurs on shared Wi-Fi networks under high device loads.

Industrial enterprises are investing in private 5G infrastructure as a foundational connectivity layer for a range of Industry 4.0 applications, and industrial wearables are among the primary use cases that justify this investment. Samsung, Ericsson, Nokia, and Siemens are the primary suppliers of private 5G network equipment to industrial customers. Wearable device manufacturers are responding by developing 5G-capable variants of their core products: RealWear's next-generation headsets support 5G connectivity, Zebra Technologies has launched 5G-capable wrist-worn scanners, and specialized industrial 5G wearable communications devices from Guardhat integrate push-to-talk, location tracking, and sensor monitoring over private 5G networks. As private 5G deployment accelerates across major industrial facilities globally, it is expected to unlock wearable application categories that have been technically impractical on Wi-Fi, including real-time AR remote assistance for field technicians in outdoor and underground environments.

|

Parameter |

Details |

|

Market Size by 2036 |

USD 34.18 Billion |

|

Market Size in 2026 |

USD 8.76 Billion |

|

Market Size in 2025 |

USD 7.21 Billion |

|

Market Growth Rate (2026-2036) |

CAGR of 14.6% |

|

Dominating Region |

North America |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Device Type, Connectivity, Industry Vertical, Sales Channel, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Driver: Aging Industrial Workforce and Skilled Labor Shortages

A key driver of the industrial wearable devices market is the accelerating retirement of experienced skilled workers from manufacturing, energy, and infrastructure industries and the difficulty of recruiting and training replacement workers to equivalent skill levels within acceptable timeframes. In the United States, the manufacturing sector is projected to have more than 2 million unfilled jobs by 2030, according to industry estimates, with the skills gap driven by the retirement of experienced baby boomer generation workers who carry decades of tacit process knowledge. Similar demographics are affecting manufacturing and industrial sectors in Germany, Japan, South Korea, and other major industrial economies. Industrial wearable platforms directly address this challenge in two ways. AR-guided work instruction systems allow less experienced workers to perform complex tasks correctly by following visual step-by-step guidance overlaid on their actual work environment, reducing dependence on memorized procedural knowledge. Remote expert assistance platforms, where an experienced specialist can see what a field technician is seeing through the wearable device's camera and provide live visual guidance, allow one expert to support multiple less-experienced workers simultaneously across different locations, extending the productivity of the most experienced remaining workforce.

Opportunity: Industrial Safety Regulation and Worker Health Monitoring

Increasingly stringent occupational health and safety regulations and the growing corporate focus on worker wellbeing as a measurable business metric are creating a significant opportunity for body-worn safety monitoring wearables in the industrial market. Regulatory bodies including OSHA in the United States, the Health and Safety Executive in the United Kingdom, and their counterparts in Europe, Australia, and Asia are expanding requirements for real-time monitoring of environmental hazards such as gas concentrations, heat stress, and noise exposure in industrial workplaces. Traditional compliance approaches relying on periodic area monitoring and manual inspection are increasingly insufficient to meet these requirements. Continuous personal monitoring through wearable sensors worn by individual workers provides more accurate, worker-specific exposure data and enables real-time alerts when thresholds are exceeded, satisfying both regulatory compliance objectives and corporate duty-of-care obligations. Companies such as Blackline Safety, MSA Safety, Industrial Scientific, and Kenzen have developed connected wearable safety monitoring platforms that are sold directly to safety managers and procurement departments in oil and gas, mining, chemicals, and construction, representing a growing revenue channel that is expanding independently of the productivity-focused AR wearable market.

In 2026, the smart glasses and AR headsets segment is expected to hold the largest share of the industrial wearable devices market. This segment dominates because it addresses the most commercially validated and widely deployed industrial wearable use case: hands-free access to digital work instructions, equipment data, and remote expert video during physical work tasks. The hands-free capability is particularly important in industrial environments because workers are often wearing gloves and engaged in two-handed tasks where stopping to consult a phone, tablet, or printed document is time-consuming, disruptive, and sometimes unsafe. RealWear's HMT-1 and Navigator 500 head-mounted tablet devices, which use a display positioned below the eye rather than directly in the line of sight, have become the most widely deployed industrial AR headset platform globally, with more than 100,000 units deployed across customers including Shell, Merck, and Honeywell Process Solutions. Google Glass Enterprise Edition 2, distributed through Honeywell and other enterprise resellers, has achieved significant deployment in light manufacturing and logistics environments. The segment benefits from an established software ecosystem, with AR work instruction platforms from PTC Vuforia, Scope AR, and others providing proven enterprise deployments that reduce the technical risk of adoption for new customers.

However, the exoskeletons segment is expected to witness the fastest growth during the forecast period. This growth is driven by increasing recognition of musculoskeletal disorders as the leading category of occupational injury in manufacturing, logistics, and construction, combined with declining device costs as production volumes increase and design iterations reduce manufacturing complexity. Passive exoskeletons from companies including SuitX, Laevo, and Ottobock, which use springs and rigid frames to redistribute physical load without electronic components, have reached price points where large manufacturing and logistics operators are deploying them at scale. Powered exoskeletons from Ekso Bionics and Sarcos Technology, which use actuators and sensors to actively amplify worker strength, are being adopted for heavy-duty applications in automotive assembly and construction. Ford Motor Company and Boeing have publicly reported exoskeleton pilot programs in their assembly operations, and the involvement of major industrial employers in proving the business case for exoskeletons is accelerating broader adoption.

How Does Wi-Fi Connected Dominate the Market?

In 2026, the Wi-Fi connected segment is expected to hold the largest share of the industrial wearable devices market. Wi-Fi connectivity dominates because enterprise Wi-Fi infrastructure is already deployed across the majority of manufacturing plants, distribution centers, and healthcare facilities where industrial wearables are being adopted. For most initial industrial wearable deployments, connecting devices to the existing enterprise Wi-Fi network is the path of least resistance and avoids the cost and complexity of deploying separate wireless infrastructure. The 802.11ac and 802.11ax Wi-Fi standards provide sufficient bandwidth for AR video streaming and data transfer in most indoor factory environments, and Wi-Fi security frameworks including WPA3 and enterprise authentication protocols satisfy corporate IT security requirements. RealWear, Google Glass Enterprise Edition, Zebra Technologies, and most other major industrial wearable platforms are designed with Wi-Fi as the primary connectivity option, reflecting the reality of the enterprise network environments where they are deployed.

However, the cellular and 5G connected segment is expected to witness the fastest growth during the forecast period. As private 5G network deployment accelerates across large industrial facilities, oil and gas installations, mining sites, and port logistics terminals, cellular connectivity is becoming available in industrial environments that were previously served only by Wi-Fi or required standalone offline devices. The performance advantages of private 5G, including consistent low latency, outdoor coverage, and support for high device density, are unlocking wearable applications in field environments that Wi-Fi cannot reliably support. Major industrial operators including BP, Rio Tinto, and BMW have deployed or announced private 5G networks, and wearable device manufacturers are responding with 5G-capable product variants. In addition, the broader availability of LTE and 4G coverage in industrial areas means that cellular connectivity is increasingly practical for wearable deployments at smaller sites that cannot justify a private 5G investment.

Why Does Manufacturing Lead the Industry Vertical Market?

In 2026, the manufacturing segment is expected to hold the largest share of the industrial wearable devices market. Manufacturing has been the earliest and most active adopter of industrial wearable technology, particularly AR-guided assembly and quality inspection applications. The manufacturing environment provides favorable conditions for wearable adoption: facilities are typically indoors with established Wi-Fi infrastructure, workers perform repetitive complex tasks where AR guidance delivers measurable productivity gains, and the high cost of manufacturing defects provides a clear financial return on investment from error reduction. Automotive manufacturers including BMW, Ford, Volkswagen, and Toyota have been among the most public early adopters of AR wearables for assembly line worker guidance, quality inspection, and maintenance. Aerospace manufacturers including Boeing and Airbus have deployed AR wearables for complex wire harness assembly and aircraft maintenance procedures where paper documentation management is a significant challenge. Electronics manufacturers in Asia, particularly in China, South Korea, and Taiwan, are adopting wearable barcode scanners, AR inspection systems, and connected safety devices as part of smart factory initiatives supported by government-funded industrial upgrading programs.

However, the logistics and warehousing segment is expected to witness the fastest growth during the forecast period. The rapid growth of e-commerce has dramatically increased the volume and velocity of warehouse picking, packing, and sorting operations, creating strong demand for wearable devices that improve worker productivity and accuracy in these environments. Wrist-worn barcode scanners from Zebra Technologies and Honeywell allow warehouse workers to scan items and confirm picks hands-free, improving picking speed compared with handheld scanner workflows. AR-guided picking systems that display pick location and item information in the worker's field of view through smart glasses are being piloted by major logistics operators including DHL, UPS, and Amazon fulfillment network suppliers. The growth of same-day and next-day delivery commitments across e-commerce markets is increasing the productivity pressure on warehouse operations, making wearable tools that reduce pick time and error rates increasingly valuable. In addition, the logistics sector's high worker turnover rates make the training time reduction enabled by AR guidance systems particularly valuable for operators that must continuously onboard new workers.

How Do System Integrators and VARs Lead the Market?

In 2026, the system integrators and value-added resellers segment is expected to hold the largest share of the industrial wearable devices market. Industrial enterprises typically procure wearable solutions as part of broader digital transformation and Industry 4.0 projects rather than as standalone device purchases. These projects involve selection of hardware platforms, integration of wearable software with existing ERP, MES, and industrial IoT systems, change management programs for the workforce adopting new technology, and ongoing technical support. System integrators such as Accenture, Deloitte, Wipro, and specialized industrial IoT integrators manage these end-to-end deployments, selecting and procuring wearable hardware on behalf of their industrial clients and developing the custom software integrations that connect wearable platforms to enterprise systems. Value-added resellers that specialize in particular industries or technology platforms, such as RealWear's certified partner network or Zebra Technologies' PartnerConnect program, provide regional sales, implementation, and support services that hardware manufacturers rely upon to reach mid-market industrial customers that they cannot serve cost-effectively through direct sales teams alone.

However, the direct enterprise sales segment is expected to witness the fastest growth during the forecast period. As industrial wearable technology matures and procurement processes become more standardized, large industrial corporations are increasingly purchasing wearable platforms directly from manufacturers through enterprise software agreements that combine hardware, software licenses, cloud platform access, and support services in a single commercial relationship. Tesla Energy's model of selling Solar Roof directly to homeowners through its own installation network provides an analogy: as vendors develop proven, standardized solution packages for defined use cases, the need for system integrator involvement in every deployment is reduced and direct sales become more efficient. Honeywell's Intelligent Wearables platform, RealWear's enterprise subscription model, and Blackline Safety's connected safety platform are examples of vendor-managed solutions that include hardware, software, analytics, and support in integrated commercial packages designed for direct enterprise procurement.

How is North America Maintaining Market Leadership?

In 2026, North America is expected to hold the largest share of the global industrial wearable devices market. This leadership is primarily driven by the United States' position as the world's largest market for industrial AR and safety wearable deployments, supported by the presence of leading wearable technology developers, a large and technology-forward manufacturing and energy sector, and strong corporate investment in workforce productivity and safety technology.

The U.S. oil and gas industry has been an early and significant adopter of connected safety wearables and AR remote assistance platforms. Companies including Shell, Chevron, ExxonMobil, and BP have deployed wearable safety monitoring systems from Blackline Safety and MSA Safety across upstream operations, and AR remote expert platforms from RealWear and Librestream for maintenance support at refineries and offshore facilities. The U.S. manufacturing sector, particularly aerospace and defense manufacturers including Boeing, Lockheed Martin, and Raytheon, has deployed AR-guided assembly and maintenance wearable systems at scale, with these programs receiving significant public documentation that has established proof of concept for the broader manufacturing market. Canada's mining and oil sands sectors also contribute to regional demand through deployments of connected safety monitoring wearables in remote extraction environments.

Which Factors Drive Asia-Pacific's Rapid Growth?

Asia-Pacific is expected to witness the highest growth rate in the industrial wearable devices market during the forecast period. This growth is primarily driven by China's large-scale smart manufacturing initiatives, Japan's demographic-driven demand for workforce augmentation technology, and South Korea's and Australia's resource and advanced manufacturing sectors adopting wearable safety and productivity solutions.

China is the largest and fastest-growing individual market in the Asia-Pacific region for industrial wearables. The Chinese government's Made in China 2025 and subsequent smart manufacturing policy initiatives are driving investment in factory digitization, including connected worker technology programs that encompass AR work instruction systems, wearable quality inspection devices, and connected safety monitoring. Chinese industrial equipment manufacturers are also developing domestic wearable products targeting the large domestic manufacturing base, creating a competitive domestic supply base alongside imported solutions from international vendors.

Japan's industrial wearable market is driven by a particularly acute demographic challenge. Japan has the most rapidly aging industrial workforce globally, with the working-age population declining and the average age of skilled manufacturing and construction workers rising significantly. Exoskeletons that reduce physical strain and extend the working life of older workers are receiving significant government and corporate investment in Japan, with companies including Cyberdyne and Innophys developing domestically produced exoskeleton systems for manufacturing and nursing care applications. South Korea's semiconductor and electronics manufacturing sector is adopting AR inspection and quality monitoring wearables, and Australia's mining industry is deploying wearable safety systems for worker monitoring in remote surface and underground mining operations.

Some of the key companies operating in the global industrial wearable devices market are Honeywell International Inc., Zebra Technologies Corporation, RealWear Inc., Google LLC (Glass Enterprise Edition), Blackline Safety Corp., MSA Safety Incorporated, Ekso Bionics Holdings Inc., Sarcos Technology and Robotics Corporation, Kinetic Inc., StrongArm Technologies Inc., Guardhat Inc., Vuzix Corporation, PTC Inc. (Vuforia), Librestream Technologies Inc., and Kenzen Inc.

The global industrial wearable devices market is expected to grow from USD 8.76 billion in 2026 to USD 34.18 billion by 2036.

The global industrial wearable devices market is projected to grow at a CAGR of 14.6% from 2026 to 2036.

The smart glasses and AR headsets segment is expected to dominate the overall market in 2026. However, the exoskeletons segment is expected to witness the fastest CAGR, driven by growing recognition of musculoskeletal injury costs in manufacturing and logistics, declining device costs as production scales, and high-profile adoption programs at Ford, Boeing, and other major manufacturers establishing the business case for broader deployment.

The Wi-Fi connected segment is expected to dominate the overall market in 2026. However, the cellular and 5G connected segment is expected to witness the fastest CAGR, as private 5G network deployment in large industrial facilities unlocks wearable applications in outdoor, underground, and field environments where Wi-Fi coverage is impractical.

The manufacturing segment is expected to dominate the overall market in 2026. However, the logistics and warehousing segment is expected to witness the fastest CAGR, driven by the rapid growth of e-commerce increasing productivity pressure on warehouse operations and creating strong demand for wrist-worn scanning and AR-guided picking systems that reduce pick time and error rates.

North America is expected to lead the global market in 2026. However, Asia-Pacific is expected to witness the fastest CAGR, driven by China's smart manufacturing programs, Japan's demographic-driven exoskeleton and AR adoption, and South Korea's and Australia's resource and advanced manufacturing sectors expanding wearable deployments.

The major players are Honeywell International, Zebra Technologies, RealWear, Google (Glass Enterprise Edition), Blackline Safety, MSA Safety, Ekso Bionics, Sarcos Technology, Kinetic, StrongArm Technologies, Guardhat, Vuzix, PTC (Vuforia), Librestream Technologies, and Kenzen.

1. Introduction

1.1. Market Definition

1.2. Market Scope

1.3. Research Methodology

1.4. Assumptions & Limitations

2. Executive Summary

3. Market Overview

3.1. Introduction

3.2. Market Dynamics

3.2.1. Drivers

3.2.2. Restraints

3.2.3. Opportunities

3.2.4. Challenges

3.3. Technology Landscape: AR Optics, Sensor Integration, Edge AI, and Private 5G Enablement

3.4. Regulatory Environment: Occupational Safety Standards and Intrinsic Safety Certification

3.5. Porter's Five Forces Analysis

4. Global Industrial Wearable Devices Market, by Device Type

4.1. Introduction

4.2. Smart Glasses and AR Headsets

4.2.1. Monocular Head-Mounted Displays

4.2.2. Binocular and Full AR Headsets

4.2.3. Smart Glasses with Integrated Camera

4.3. Smart Helmets

4.3.1. Connected Safety Helmets with Sensor Integration

4.3.2. AR-Integrated Hard Hats for Construction and Mining

4.4. Body-worn Sensors and Safety Wearables

4.4.1. Connected Gas Detection and Environmental Monitors

4.4.2. Ergonomic Risk Monitoring Wearables

4.4.3. Physiological and Fatigue Monitoring Devices

4.4.4. Fall Detection and Lone Worker Safety Devices

4.5. Wrist-worn Devices

4.5.1. Wearable Barcode and RFID Scanners

4.5.2. Ruggedized Industrial Smartwatches and Wrist Computers

4.6. Exoskeletons

4.6.1. Passive Upper-Body Exoskeletons for Overhead Assembly

4.6.2. Passive Lower-Body and Back-Support Exoskeletons

4.6.3. Powered Full-Body Exoskeletons

5. Global Industrial Wearable Devices Market, by Connectivity

5.1. Introduction

5.2. Wi-Fi Connected

5.3. Cellular and 5G Connected

5.4. Bluetooth and Short-Range Wireless

5.5. Standalone and Offline

6. Global Industrial Wearable Devices Market, by Industry Vertical

6.1. Introduction

6.2. Manufacturing

6.2.1. Automotive and Heavy Equipment Assembly

6.2.2. Aerospace and Defense Manufacturing

6.2.3. Electronics and Semiconductor Manufacturing

6.2.4. Food and Beverage and Consumer Goods Manufacturing

6.3. Oil and Gas and Mining

6.3.1. Upstream Oil and Gas Exploration and Production

6.3.2. Refining, Petrochemicals, and Downstream Operations

6.3.3. Surface and Underground Mining

6.4. Construction

6.4.1. Commercial and Infrastructure Construction

6.4.2. Industrial Plant and Facility Construction

6.5. Logistics and Warehousing

6.5.1. E-commerce Fulfillment and Distribution Centers

6.5.2. Third-Party Logistics and Freight Handling

6.6. Healthcare and Pharmaceuticals

6.6.1. Hospital and Clinical Environment Wearables

6.6.2. Pharmaceutical and Life Sciences Manufacturing

7. Global Industrial Wearable Devices Market, by Sales Channel

7.1. Introduction

7.2. Direct Enterprise Sales

7.3. System Integrators and Value-Added Resellers

7.4. OEM and Platform Partnerships

8. Global Industrial Wearable Devices Market, by Region

8.1. Introduction

8.2. North America

8.2.1. U.S.

8.2.2. Canada

8.3. Europe

8.3.1. Germany

8.3.2. United Kingdom

8.3.3. France

8.3.4. Netherlands

8.3.5. Scandinavia (Norway, Sweden, Finland)

8.3.6. Rest of Europe

8.4. Asia-Pacific

8.4.1. China

8.4.2. Japan

8.4.3. South Korea

8.4.4. Australia

8.4.5. India

8.4.6. Rest of Asia-Pacific

8.5. Latin America

8.5.1. Brazil

8.5.2. Mexico

8.5.3. Chile

8.5.4. Rest of Latin America

8.6. Middle East & Africa

8.6.1. Saudi Arabia

8.6.2. UAE

8.6.3. South Africa

8.6.4. Rest of Middle East & Africa

9. Competitive Landscape

9.1. Overview

9.2. Key Growth Strategies

9.3. Competitive Benchmarking

9.4. Competitive Dashboard

9.4.1. Industry Leaders

9.4.2. Market Differentiators

9.4.3. Vanguards

9.4.4. Emerging Companies

9.5. Market Ranking/Positioning Analysis of Key Players, 2025

10. Company Profiles

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

10.1. Honeywell International Inc.

10.2. Zebra Technologies Corporation

10.3. RealWear Inc.

10.4. Google LLC (Glass Enterprise Edition)

10.5. Blackline Safety Corp.

10.6. MSA Safety Incorporated

10.7. Ekso Bionics Holdings Inc.

10.8. Sarcos Technology and Robotics Corporation

10.9. Kinetic Inc.

10.10. StrongArm Technologies Inc.

10.11. Guardhat Inc.

10.12. Vuzix Corporation

10.13. PTC Inc. (Vuforia AR Platform)

10.14. Librestream Technologies Inc.

10.15. Kenzen Inc.

11. Appendix

11.1. Questionnaire

11.2. Related Reports

Published Date: Mar-2026

Published Date: Feb-2026

Published Date: Sep-2024

Published Date: Jan-2023

Published Date: May-2026

Subscribe to get the latest industry updates