Resources

About Us

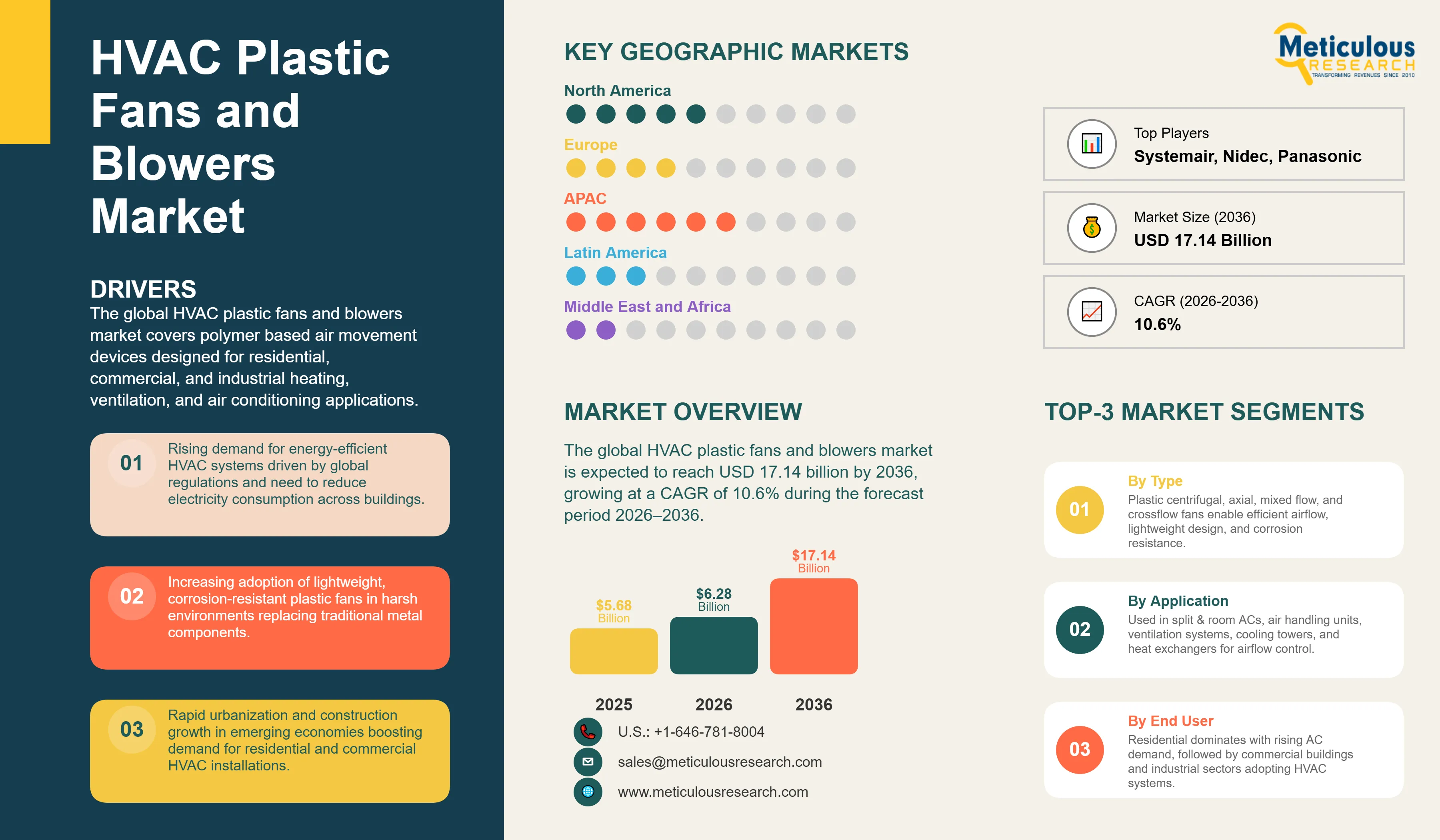

The global HVAC plastic fans and blowers market is estimated at USD 6.28 billion in 2026. This market is expected to reach USD 17.14 billion by 2036, growing at a CAGR of 10.6% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

The global HVAC plastic fans and blowers market covers polymer based air movement devices designed for residential, commercial, and industrial heating, ventilation, and air conditioning applications. These include plastic centrifugal fans, plastic axial fans, plastic mixed flow fans, plastic crossflow fans, and plastic centrifugal blowers manufactured from engineering grade thermoplastics and fiber reinforced composite materials, deployed across a broad range of HVAC configurations including split and room air conditioning systems, air handling units, energy recovery ventilation equipment, cooling towers, and industrial ventilation systems.

HVAC plastic fans and blowers use high performance polymers like glass fiber reinforced polyamide, flame retardant polypropylene, and advanced composites to offer benefits over traditional metal designs, including corrosion resistance, lighter weight, and improved aerodynamics through precise molding. These fans come in a variety of designs, from backward and forward curved centrifugal fans to tube and vane axial fans, crossflow units for compact residential air conditioners, and mixed flow fans for energy recovery and inline duct systems. The category is integrated with electronically commutated motors and variable frequency drives to meet energy efficiency and demand controlled ventilation standards set by regulations such as ASHRAE Standard 90.1, the EU Ecodesign Directive (Lot 30), and the U.S. DOE Fan Energy Index.

The growth of the overall HVAC plastic fans and blowers market is primarily driven by growing adoption of energy efficient ventilation systems authorised by regulatory frameworks that favor lightweight, aerodynamically optimized impeller geometries achievable through polymer molding processes. Rising utilization of corrosion resistant fan components in demanding operating environments such as coastal buildings, healthcare facilities, swimming pools, and industrial applications is also contributing to market expansion, as moisture and chemical exposure accelerate degradation of metal alternatives. Expanding construction activities across emerging economies indicate another key growth driver, with Asia expected to accommodate nearly 50% of global urban population growth by 2050 according to the United Nations Department of Economic and Social Affairs. Furthermore, fan systems account for approximately 9% of commercial building electricity consumption globally according to the International Energy Agency, and plastic impellers enabling 30 to 50% fan energy savings through variable speed operation are increasingly favored by facility managers targeting lifecycle energy cost reductions. The rapid growth of data center infrastructure further supports market demand, with global data center electricity consumption projected to nearly double from 415 TWh in 2024 to 945 TWh by 2030 amid accelerating AI infrastructure expansion.

However, the growth of this market is restrained by temperature limitations of engineering thermoplastics, with maximum continuous operating temperatures between 80°C and 120°C restricting suitability for high temperature industrial exhaust applications. Fire performance requirements imposed by stringent codes including UL 723 and EN 13501 can further restrict plastic fan use in certain occupancy spaces without specialized flame retardant formulations. Additionally, perception challenges regarding structural durability compared with metal alternatives and volatility in specialty polymer resin pricing pose further challenges for market stakeholders.

On the other hand, the development of smart and IoT enabled fan systems integrated with EC motors and digital control interfaces enabling remote monitoring, predictive maintenance, and demand responsive operation represents a significant growth opportunity, with IoT control alone estimated to achieve 15 to 30% energy savings. Rising demand for noise reduced and aerodynamically optimized designs enabled by advanced computational fluid dynamics tools offers additional market development potential. The ongoing expansion of data center cooling infrastructure and integration of HVAC systems with renewable energy platforms are further expected to generate new avenues for market participants throughout the forecast period.

EC Motor Integration Reshaping the Energy Efficiency Landscape in HVAC Fan Systems

The growing adoption of electronically commutated (EC) motors in plastic fan assemblies is one of the most significant near term trends in the HVAC fan and blower market. EC motors use electronic circuitry to drive brushless permanent magnets, offering energy savings of 30–50% compared with traditional AC motors. The light weight of plastic impellers lowers rotational inertia, making them ideal for EC motors and enabling precise, variable speed operation across the full airflow range, from 20% to 100% of capacity.

This combination is becoming popular in high performance commercial HVAC systems, where building owners and operators focus on reducing energy use over the system’s lifetime to meet sustainability goals and manage rising electricity costs. Pre engineered fan and motor assemblies that work with building automation protocols like BACnet and Modbus, along with advanced control interfaces, make EC motor plastic fans a top choice for projects aiming for LEED, BREEAM, or other green building certifications. Regulatory support is also driving adoption, as standards like ASHRAE 90.1 and the EU Ecodesign Directive are steering procurement toward electronically commutated, variable speed fan technologies in commercial and industrial settings.

Expanding Deployment of Energy Recovery Ventilation Driving Demand for Mixed Flow Plastic Fans

The growing regulatory emphasis on controlled mechanical ventilation and energy efficiency in residential and light commercial buildings is creating a sustained demand wave for plastic mixed flow fans integrated into energy recovery ventilation and heat recovery ventilation equipment. Mixed flow fans, combining the high volume airflow characteristics of axial designs with the pressure generation of centrifugal configurations, are widely deployed in inline duct ventilation systems and compact air handling units where moderate static pressure capability and high volume delivery are simultaneously required.

Energy recovery ventilation systems, which can capture 70–85% of thermal energy from exhaust air to boost heating and cooling efficiency, are increasingly being specified in residential and commercial projects across North America, Europe, and parts of Asia Pacific. Standards like ASHRAE 62.2 for residential ventilation feature the importance of controlled mechanical ventilation, creating a steady demand for mixed flow plastic fan assemblies. This trend is further strengthened by variable speed EC motor technology, which allows precise, demand based ventilation control, while the combination of aerodynamic efficiency and lightweight plastic construction meets the performance and cost requirements for high volume residential and light commercial applications.

IoT Enabled Smart Fan Systems Transitioning from Premium Specification to Mainstream Adoption

The digitalization of HVAC fan systems through IoT connectivity, smart sensor integration, and cloud based monitoring platforms is transitioning from a premium differentiating feature toward a mainstream product capability, driven by the growing demand for predictive maintenance, remote diagnostics, and demand responsive building operations. IoT enabled plastic fan assemblies providing real time performance data, fault detection, and automated alerting allow facility operators to reduce unplanned downtime and optimize maintenance schedules across large commercial and industrial installations.

The integration of smart control platforms compatible with BACnet, Modbus, and emerging open building automation standards enables HVAC fan systems to respond dynamically to real time occupancy patterns, indoor air quality measurements, and utility pricing signals, delivering the 15 to 30% energy savings attributed specifically to intelligent demand controlled ventilation strategies. Leading manufacturers including ebm papst Group and Delta Electronics are advancing integrated motor and fan platforms with embedded intelligence and digital communication capabilities, positioning IoT connectivity as a core design requirement rather than an optional feature for next generation HVAC plastic fan products targeting commercial, healthcare, and data center end use segments.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 17.14 Billion |

|

Market Size in 2026 |

USD 6.28 Billion |

|

Revenue Growth Rate (2026–2036) |

CAGR of 10.6% |

|

Dominating Product Type |

Plastic Centrifugal Fans |

|

Fastest Growing Product Type |

Plastic Mixed Flow Fans |

|

Dominating Technology |

AC Motor Fans |

|

Fastest Growing Technology |

EC Motor Fans |

|

Dominating Pressure Range |

Low Pressure |

|

Dominating Application |

Split & Room AC |

|

Dominating End Use |

Residential |

|

Dominating Geography |

Asia Pacific |

|

Fastest Growing Geography |

Asia Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

By Product Type: In 2026, the Plastic Centrifugal Fans Segment to Dominate the Global HVAC Plastic Fans and Blowers Market

Based on product type, the global HVAC plastic fans and blowers market is segmented into plastic centrifugal fans, plastic axial fans, plastic mixed flow fans, plastic crossflow fans, and plastic centrifugal blowers. The large share of this segment is attributed to the widespread deployment of backward curved centrifugal designs across commercial building air handling units, cooling tower applications, and industrial ventilation systems, driven by their ability to deliver high static pressure with improved aerodynamic performance and reduced motor power consumption. Building owners and facility managers increasingly emphasize minimizing lifecycle energy consumption to meet sustainability targets and mitigate rising electricity costs, driving adoption of optimized centrifugal fan technologies across commercial and industrial infrastructure.

However, the plastic mixed flow fans segment is projected to register the highest growth during the forecast period. The high growth of this segment is driven by increasing demand for compact and energy efficient ventilation systems across residential and commercial buildings, the widespread integration of mixed flow fans into energy recovery ventilation equipment recovering 70 to 85% of thermal energy from exhaust air streams, and the strong alignment of this product category with ASHRAE 62.2 residential ventilation mandates requiring controlled mechanical ventilation. Integration with variable speed EC motor technologies enables improved system efficiency and demand based ventilation control, allowing HVAC systems to adjust airflow from 20 to 100% capacity based on real time occupancy and ventilation requirements.

By Technology: In 2026, the AC Motor Fans Segment to Hold the Largest Share

Based on technology, the global HVAC plastic fans and blowers market is segmented into AC motor fans, EC motor fans, and DC motor fans. The large share of this segment is attributed to widespread deployment across residential split air conditioning systems, compact ventilation units, and cost sensitive commercial HVAC equipment where simplicity and price competitiveness remain primary selection criteria. AC motor driven plastic fans dominate the residential crossflow fan market used in wall mounted indoor units, representing the majority of global room air conditioner installations.

However, the EC motor fans segment is projected to register the highest growth during the forecast period, driven by superior energy efficiency, precise speed control capabilities, and alignment with global building performance regulations. EC motors integrate electronic commutation circuitry that enables brushless permanent magnet operation, delivering 30 to 50% energy savings compared to traditional AC motor platforms. The lightweight nature of plastic impellers reduces rotational inertia, making them well suited for variable speed operation with EC motor controls, while pre engineered motor and fan assemblies compatible with BACnet and Modbus protocols position EC motor plastic fans as the technology of choice for high performance commercial HVAC systems.

By Application: In 2026, the Split & Room AC Segment to Hold the Largest Share

Based on application, the global HVAC plastic fans and blowers market is segmented into split and room AC, air handling units, ventilation systems, heat exchangers, cooling towers, and other applications. The dominant share of this segment reflects the accelerating adoption of residential cooling systems across emerging markets in Asia Pacific, the Middle East, and Latin America experiencing sustained temperature increases, rising household incomes, and rapid urbanization. The International Energy Agency projects global installed air conditioning units to grow from approximately 2.5 billion in 2025 to more than 6 billion units by 2050, with nearly 70% of this increase driven by developing economies. Plastic crossflow fans enabling ultra compact indoor unit designs with 15 to 25% weight reduction dominate this application, while outdoor condensing units increasingly utilize plastic axial propeller fans for heat rejection.

Based on geography, the global HVAC plastic fans and blowers market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. The dominant position of this region is supported by its established role as the primary manufacturing hub for split and room air conditioning systems, with countries including China, India, Japan, and Thailand serving as major production centers for HVAC equipment that heavily utilizes plastic axial and crossflow fan assemblies. China alone represents the world's largest market for residential air conditioning with annual production exceeding 130 million room air conditioner units. The region benefits from large scale OEM concentration, cost competitive manufacturing infrastructure, and strong domestic demand driven by rapid urbanization and rising disposable incomes. Asia Pacific is also expected to witness the fastest growth during the forecast period, driven by accelerating air conditioner penetration in emerging economies across India and Southeast Asia that remain significantly underpenetrated in terms of residential cooling, and by government regulations promoting energy efficiency and EC motor integration encouraging technological upgrades in fan systems.

North America is expected to maintain a significant market share in 2026, driven by building retrofitting initiatives, high performance mechanical system adoption, and compliance requirements established by ASHRAE Standard 90.1. Europe accounts for 19.5% of the market in 2026, supported by the stringent requirements of the EU Ecodesign Directive and the widespread deployment of energy recovery ventilation systems across cold climate regions.

The competition within the global HVAC plastic fans and blowers market is primarily driven by technological innovation in motor and impeller design, manufacturing scalability across high volume residential and commercial product lines, product performance benchmarked against regulatory energy efficiency standards, and strategic collaborations across the HVAC original equipment manufacturer value chain.

ebm papst Group remains one of the leading players in the market, driven by its strong commercial presence across centrifugal and axial compact fan assemblies for HVAC applications and its significant investments in EC motor integration technology and IoT enabled control platforms supporting smart building automation protocols. Ziehl Abegg SE maintains a strong position through its ZAmid plastic impeller product portfolio and centrifugal fan solutions targeting commercial ventilation applications. Delta Electronics and Nidec Corporation also hold significant positions through their broad portfolios of EC and DC motor driven plastic fan and blower assemblies catering to HVAC and data center thermal management applications.

Some of the key players operating in the global HVAC plastic fans and blowers market include ebm papst Group (Germany), Ziehl Abegg SE (Germany), Nidec Corporation (Japan), Delta Electronics Inc. (Taiwan), Systemair AB (Sweden), FläktGroup Holding GmbH (Germany), Zhejiang Yilida Ventilator Co. Ltd. (China), Nisshinbo Holdings Inc. (Japan), Carrier Global Corporation (U.S.), Johnson Controls International plc (Ireland), Panasonic Corporation (Japan), Daikin Industries Ltd. (Japan), Greenheck Fan Corporation (U.S.), Nortek Global HVAC (U.S.), Regal Rexnord Corporation (U.S.), Midea Group (China), Gree Electric Appliances Inc. (China), Haier Group Corporation (China), and LG Electronics Inc. (South Korea), among others.

The global HVAC plastic fans and blowers market is estimated at USD 6.28 billion in 2026 and is expected to reach USD 17.14 billion by 2036, at a CAGR of 10.6% during the forecast period 2026–2036.

In 2026, the plastic centrifugal fans segment is expected to hold the largest share of the global HVAC plastic fans and blowers market, driven by the dominant commercial volume of backward curved centrifugal fan deployments across air handling units, cooling towers, and industrial ventilation systems.

The plastic mixed flow fans segment is expected to register the highest growth during the forecast period 2026–2036, driven by growing demand for compact and energy efficient inline duct ventilation solutions and the expanding deployment of energy recovery ventilation systems in residential and commercial buildings.

In 2026, the AC motor fans segment is expected to hold the largest share of the global HVAC plastic fans and blowers market, attributable to its dominant installed base across residential split air conditioning and cost sensitive commercial HVAC applications.

In 2026, the split and room AC segment is expected to hold the largest share of the global HVAC plastic fans and blowers market, driven by accelerating residential cooling adoption across emerging economies and the expanding global installed base of room air conditioning systems.

The growth of this market is primarily driven by increasing regulatory mandates for energy efficient ventilation systems, rising adoption of EC motor technology delivering 30 to 50% energy savings, expanding construction and cooling infrastructure across emerging economies, growing data center thermal management demand, and the lightweight and corrosion resistant properties of engineering grade polymers enabling cost effective high volume production for residential and commercial HVAC applications.

Key players operating in the global HVAC plastic fans and blowers market include ebm papst Group (Germany), Ziehl Abegg SE (Germany), Nidec Corporation (Japan), Delta Electronics Inc. (Taiwan), Systemair AB (Sweden), FläktGroup Holding GmbH (Germany), Zhejiang Yilida Ventilator Co. Ltd. (China), Nisshinbo Holdings Inc. (Japan), Carrier Global Corporation (U.S.), Johnson Controls International plc (Ireland), Panasonic Corporation (Japan), Daikin Industries Ltd. (Japan), Greenheck Fan Corporation (U.S.), Nortek Global HVAC (U.S.), Regal Rexnord Corporation (U.S.), Midea Group (China), Gree Electric Appliances Inc. (China), Haier Group Corporation (China), and LG Electronics Inc. (South Korea).

Asia Pacific is expected to register the highest growth rate in the global HVAC plastic fans and blowers market during the forecast period 2026–2036, driven by accelerating residential air conditioner penetration, expanding commercial infrastructure, and government driven energy efficiency mandates encouraging EC motor integration across the region's dominant HVAC manufacturing base.

1. Introduction

1.1. Market Definition & Scope

1.2. Currency & Limitations

2. Research Methodology

2.1. Research Approach

2.2. Data Collection & Validation

2.2.1. Secondary Research

2.2.2. Primary Research

2.3. Market Assessment

2.3.1. Market Size Estimation

2.3.2. Bottom-Up Approach

2.3.3. Top-Down Approach

2.3.4. Growth Forecast

2.4. Assumptions For The Study

3. Executive Summary

4. Market Insights

4.1. Overview

4.2. Factors Affecting Market Growth

4.2.1. Drivers

4.2.2. Regulatory Mandates Favoring Aerodynamically Optimized Fan Designs Driving Demand

4.2.3. Corrosion Resistance Requirements In Demanding Operating Environments Boosting Adoption

4.2.4. Lightweight Construction Enabling Motor Efficiency And System Integration

4.2.5. Expanding Construction Activities And Infrastructure Development

4.2.6. Stringent Regulations Promoting Energy Efficiency In HVAC Systems

4.3. Restraints

4.3.1. Temperature And Fire Performance Limitations Of Polymer Materials

4.3.2. Perception Challenges Regarding Structural Durability Versus Metal Alternatives

4.3.3. Fluctuating Raw Material Prices Affecting Profit Margins

4.3.4. Complexity In Retrofitting Existing HVAC Systems

4.4. Opportunities

4.4.1. Untapped Markets In Emerging Economies With Rapid Industrialization

4.4.2. Development Of Smart And IoT-Enabled Fan Systems

4.4.3. Expansion Of Data Center Cooling Applications

4.4.4. Integration With Renewable Energy Systems And Energy Storage

4.4.5. Rising Demand For Noise-Reduced And Aerodynamically Optimized Designs

4.5. Challenges

4.5.1. Technical Complexity In Custom Engineering Solutions

4.5.2. Long Product Development Cycles For Specialized Applications

4.5.3. Maintenance And Service Requirements In Remote Locations

4.6. Key Trends

4.6.1. Advanced Materials Including Lightweight Composites

4.6.2. Digitalization And Remote Monitoring Capabilities

4.6.3. Variable Frequency Drive (VFD) Integration

4.6.4. Sustainable Manufacturing Processes

4.7. Porter's Five Forces Analysis

4.7.1. Bargaining Power Of Buyers: High

4.7.2. Bargaining Power Of Suppliers: Moderate To High

4.7.3. Threat Of Substitutes: Moderate

4.7.4. Threat Of New Entrants: Low To Moderate

4.7.5. Degree Of Competition: High

5. Global HVAC Fans And Blowers Market, By Product Type

5.1. Overview

5.2. Plastic Centrifugal Fans

5.2.1. Plastic Backward Curved Centrifugal Fans

5.2.2. Plastic Forward Curved Centrifugal Fans

5.2.3. Plastic Radial Blade Centrifugal Fans

5.3. Plastic Axial Fans

5.3.1. Plastic Propeller Axial Fans

5.3.2. Plastic Tube Axial Fans

5.3.3. Plastic Vane Axial Fans

5.4. Plastic Mixed Flow Fans

5.5. Plastic Crossflow Fans

5.6. Plastic Centrifugal Blowers

6. Global HVAC Fans And Blowers Market, By Technology

6.1. Overview

6.2. AC Motor Fans

6.3. EC Motor Fans

6.4. DC Motor Fans

7. Global HVAC Fans And Blowers Market, By Pressure Range

7.1. Overview

7.2. Low Pressure Fans

7.3. Medium Pressure Fans

7.4. High Pressure Fans

8. Global HVAC Fans And Blowers Market, By Application

8.1. Overview

8.2. Air Handling Units

8.3. Cooling Towers

8.4. Heat Exchangers

8.5. Ventilation Systems

8.6. Split And Room Air Conditioners

8.7. Other Applications

9. Global HVAC Fans And Blowers Market, By End Use

9.1. Overview

9.2. Commercial

9.3. Industrial

9.4. Residential

10. HVAC Fans And Blowers Market Assessment, By Geography

10.1. Overview

10.2. North America

10.3. Europe

10.4. Asia-Pacific

10.4.1. China

10.4.2. Japan

10.4.3. India

10.4.4. Thailand

10.4.5. Rest Of Asia Pacific

10.5. Latin America

10.6. Middle East & Africa

11. Competitive Landscape

11.1. Introduction

11.2. Competitive Benchmarking

11.3. Competitive Dashboard

11.3.1. Industry Leaders

11.3.2. Market Differentiators

11.3.3. Vanguards

11.3.4. Emerging Companies

12. Company Profiles

12.1. Ebm-Papst Group

12.1.1. Company Overview

12.1.2. Product Portfolio

12.1.3. Strategic Developments

12.1.4. SWOT Analysis

12.2. Ziehl-Abegg SE

12.2.1. Company Overview

12.2.2. Product Portfolio

12.2.3. SWOT Analysis

12.3. Greenheck Fan Corporation

12.3.1. Company Overview

12.3.2. Product Portfolio

12.3.3. SWOT Analysis

12.4. Systemair AB

12.4.1. Company Overview

12.4.2. Product Portfolio

12.4.3. Financial Overview

12.4.4. Strategic Developments

12.4.5. SWOT Analysis

12.5. FläktGroup Holding GmbH

12.5.1. Company Overview

12.5.2. Product Portfolio

12.5.3. Strategic Developments

12.5.4. SWOT Analysis

12.6. Nidec Corporation

12.6.1. Company Overview

12.6.2. Product Portfolio

12.6.3. Financial Overview

12.6.4. SWOT Analysis

12.7. Delta Electronics, Inc.

12.7.1. Company Overview

12.7.2. Product Portfolio

12.7.3. Financial Overview

12.7.4. SWOT Analysis

12.8. Daikin Industries, Ltd.

12.8.1. Company Overview

12.8.2. Product Portfolio

12.8.3. Financial Overview

12.8.4. SWOT Analysis

12.9. Carrier Global Corporation

12.9.1. Company Overview

12.9.2. Product Portfolio

12.9.3. Financial Overview

12.9.4. SWOT Analysis

12.10. Johnson Controls International PLC

12.10.1. Company Overview

12.10.2. Product Portfolio

12.10.3. Financial Overview

12.10.4. SWOT Analysis

12.11. Munters Group AB

12.11.1. Company Overview

12.11.2. Product Portfolio

12.11.3. Financial Overview

12.11.4. SWOT Analysis

12.12. Nisshinbo Holdings Inc.

12.12.1. Company Overview

12.12.2. Product Portfolio

12.12.3. Financial Overview

12.12.4. SWOT Analysis

12.13. Zhejiang Yilida Ventilator Co., Ltd.

12.13.1. Company Overview

12.13.2. Product Portfolio

12.13.3. Financial Overview

12.13.4. SWOT Analysis

12.14. Panasonic Corporation

12.14.1. Company Overview

12.14.2. Product Portfolio

12.14.3. Financial Overview

12.14.4. SWOT Analysis

13. Appendix

13.1. Available Customization

13.2. Related Reports

LIST OF TABLES

Table 1. Global HVAC Fans and Blowers Market, By Product Type, 2025–2035 (USD Million)

Table 2. Global HVAC Plastic Fans and Blowers Market, By Product Type, 2026–2036 (Thousand Units)

Table 3. Global HVAC Plastic Centrifugal Fans Market, By Type, 2026–2036 (USD Million)

Table 4. Global HVAC Plastic Centrifugal Fans Market, By Type, 2026–2036 (Thousand Units)

Table 5. Global Plastic Centrifugal Fans Market, By Country/Region, 2026–2036 (USD Million)

Table 6. Global Plastic Centrifugal Fans Market, By Country/Region, 2026–2036 (Thousand Units)

Table 7. Global HVAC Plastic Backward Curved Fans Market, By Country/Region, 2026–2036 (USD Million)

Table 8. Global HVAC Plastic Backward Curved Fans Market, By Country/Region, 2026–2036 (Thousand Units)

Table 9. Global HVAC Plastic Forward Curved Fans Market, By Country/Region, 2026–2036 (USD Million)

Table 10. Global HVAC Plastic Forward Curved Fans Market, By Country/Region, 2026–2036 (Thousand Units)

Table 11. Global HVAC Plastic Radial Blade Fans Market, By Country/Region, 2026–2036 (USD Million)

Table 12. Global HVAC Plastic Radial Blade Fans Market, By Country/Region, 2026–2036 (Thousand Units)

Table 13. Global HVAC Plastic Axial Fans Market, By Type, 2026–2036 (USD Million)

Table 14. Global HVAC Plastic Axial Fans Market, By Type, 2026–2036 (Thousand Units)

Table 15. Global HVAC Plastic Axial Fans Market, By Country/Region, 2026–2036 (USD Million)

Table 16. Global HVAC Plastic Axial Fans Market, By Country/Region, 2026–2036 (Thousand Units)

Table 17. Global HVAC Plastic Propeller Fans Market, By Country/Region, 2026–2036 (USD Million)

Table 18. Global HVAC Plastic Propeller Fans Market, By Country/Region, 2026–2036 (Thousand Units)

Table 19. Global HVAC Plastic Tube Axial Fans Market, By Country/Region, 2026–2036 (USD Million)

Table 20. Global HVAC Plastic Tube Axial Fans Market, By Country/Region, 2026–2036 (Thousand Units)

Table 21. Global HVAC Plastic Vane Axial Fans Market, By Country/Region, 2026–2036 (USD Million)

Table 22. Global HVAC Plastic Vane Axial Fans Market, By Country/Region, 2026–2036 (Thousand Units)

Table 23. Global HVAC Plastic Mixed Flow Fans Market, By Country/Region, 2026–2036 (USD Million)

Table 24. Global HVAC Plastic Mixed Flow Fans Market, By Country/Region, 2026–2036 (Thousand Units)

Table 25. Global HVAC Plastic Crossflow Fans Market, By Country/Region, 2026–2036 (USD Million)

Table 26. Global HVAC Plastic Crossflow Fans Market, By Country/Region, 2026–2036 (Thousand Units)

Table 27. Global HVAC Plastic Centrifugal Blowers Market, By Country/Region, 2026–2036 (USD Million)

Table 28. Global HVAC Plastic Centrifugal Blowers Market, By Country/Region, 2026–2036 (Thousand Units)

Table 29. Global HVAC Fans and Blowers Market, By Technology, 2026–2036 (USD Million)

Table 30. Global HVAC Ac Motor Fans Market, By Country/Region, 2026–2036 (USD Million)

Table 31. Global HVAC Ec Motor Fans Market, By Country/Region, 2026–2036 (USD Million)

Table 32. Global HVAC Dc Motor Fans Market, By Country/Region, 2026–2036 (USD Million)

Table 33. Global HVAC Fans and Blowers Market, By Pressure Range, 2026–2036 (USD Million)

Table 34. Global HVAC Plastic Fans and Blowers Market for Low Pressure, By Country/Region, 2026–2036 (USD Million)

Table 35. Global HVAC Plastic Fans and Blowers Market for Medium Pressure, By Country/Region, 2026–2036 (USD Million)

Table 36. Global HVAC Plastic Fans and Blowers Market for High Pressure, By Country/Region, 2026–2036 (USD Million)

Table 37. Global HVAC Fans and Blowers Market, By Application, 2026–2036 (USD Million)

Table 38. Global HVAC Plastic Fans and Blowers Market for Air Handling Units, By Country/Region, 2026–2036 (USD Million)

Table 39. Global HVAC Plastic Fans and Blowers Market for Cooling Towers, By Country/Region, 2026–2036 (USD Million)

Table 40. Global HVAC Plastic Fans and Blowers Market for Heat Exchangers, By Country/Region, 2026–2036 (USD Million)

Table 41. Global HVAC Plastic Fans and Blowers Market for Ventilation Systems, By Country/Region, 2026–2036 (USD Million)

Table 42. Global HVAC Plastic Fans and Blowers Market for Split & Room Ac, By Country/Region, 2026–2036 (USD Million)

Table 43. Global HVAC Plastic Fans and Blowers Market for Other Applications, By Country/Region, 2026–2036 (USD Million)

Table 44. Global HVAC Fans and Blowers Market, By End Use, 2026–2036 (USD Million)

Table 45. Global HVAC Plastic Fans and Blowers Market for Commercial, By Country/Region, 2026–2036 (USD Million)

Table 46. Global HVAC Plastic Fans and Blowers Market for Industrial, By Country/Region, 2026–2036 (USD Million)

Table 47. Global HVAC Plastic Fans and Blowers Market for Residential, By Country/Region, 2026–2036 (USD Million)

Table 48. North America: HVAC Plastic Fans and Blowers Market, By Product Type, 2026–2036 (USD Million)

Table 49. North America: HVAC Plastic Fans and Blowers Market, By Product Type, 2026–2036 (Thousand Units)

Table 50. North America: HVAC Plastic Centrifugal Fans Market, By Type, 2026–2036 (USD Million)

Table 51. North America: HVAC Plastic Centrifugal Fans Market, By Type, 2026–2036 (Thousand Units)

Table 52. North America: HVAC Plastic Axial Fans Market, By Type, 2026–2036 (USD Million)

Table 53. North America: HVAC Plastic Axial Fans Market, By Type, 2026–2036 (Thousand Units)

Table 54. North America: HVAC Plastic Fans and Blowers Market, By Technology, 2026–2036 (USD Million)

Table 55. North America: HVAC Plastic Fans and Blowers Market, By Pressure Range, 2026–2036 (USD Million)

Table 56. North America: HVAC Plastic Fans and Blowers Market, By Application, 2026–2036 (USD Million)

Table 57. North America: HVAC Plastic Fans and Blowers Market, By End User, 2026–2036 (USD Million)

Table 58. Europe: HVAC Plastic Fans and Blowers Market, By Product Type, 2026–2036 (USD Million)

Table 59. Europe: HVAC Plastic Fans and Blowers Market, By Product Type, 2026–2036 (Thousand Units)

Table 60. Europe: HVAC Plastic Centrifugal Fans Market, By Type, 2026–2036 (USD Million)

Table 61. Europe: HVAC Plastic Centrifugal Fans Market, By Type, 2026–2036 (Thousand Units)

Table 62. Europe: HVAC Plastic Axial Fans Market, By Type, 2026–2036 (USD Million)

Table 63. Europe: HVAC Plastic Axial Fans Market, By Type, 2026–2036 (Thousand Units)

Table 64. Europe: HVAC Plastic Fans and Blowers Market, By Technology, 2026–2036 (USD Million)

Table 65. Europe: HVAC Plastic Fans and Blowers Market, By Pressure Range, 2026–2036 (USD Million)

Table 66. Europe: HVAC Plastic Fans and Blowers Market, By Application, 2026–2036 (USD Million)

Table 67. Europe: HVAC Plastic Fans and Blowers Market, By End User, 2026–2036 (USD Million)

Table 68. Asia-Pacific: HVAC Plastic Fans and Blowers Market, By Country, 2026–2036 (USD Million)

Table 69. Asia-Pacific: HVAC Plastic Fans and Blowers Market, By Product Type, 2026–2036 (USD Million)

Table 70. Asia-Pacific: HVAC Plastic Fans and Blowers Market, By Product Type, 2026–2036 (Thousand Units)

Table 71. Asia-Pacific: HVAC Plastic Centrifugal Fans Market, By Type, 2026–2036 (USD Million)

Table 72. Asia-Pacific: HVAC Plastic Centrifugal Fans Market, By Type, 2026–2036 (Thousand Units)

Table 73. Asia-Pacific: HVAC Plastic Axial Fans Market, By Type, 2026–2036 (USD Million)

Table 74. Asia-Pacific: HVAC Plastic Axial Fans Market, By Type, 2026–2036 (Thousand Units)

Table 75. Asia-Pacific: HVAC Plastic Fans and Blowers Market, By Technology, 2026–2036 (USD Million)

Table 76. Asia-Pacific: HVAC Plastic Fans and Blowers Market, By Pressure Range, 2026–2036 (USD Million)

Table 77. Asia-Pacific: HVAC Plastic Fans and Blowers Market, By Application, 2026–2036 (USD Million)

Table 78. Asia-Pacific: HVAC Plastic Fans and Blowers Market, By End User, 2026–2036 (USD Million)

Table 79. China: HVAC Plastic Fans and Blowers Market, By Product Type, 2026–2036 (USD Million)

Table 80. China: HVAC Plastic Fans and Blowers Market, By Product Type, 2026–2036 (Thousand Units)

Table 81. China: HVAC Plastic Centrifugal Fans Market, By Type, 2026–2036 (USD Million)

Table 82. China: HVAC Plastic Centrifugal Fans Market, By Type, 2026–2036 (Thousand Units)

Table 83. China: HVAC Plastic Axial Fans Market, By Type, 2026–2036 (USD Million)

Table 84. China: HVAC Plastic Axial Fans Market, By Type, 2026–2036 (Thousand Units)

Table 85. China: HVAC Plastic Fans and Blowers Market, By Technology, 2026–2036 (USD Million)

Table 86. China: HVAC Plastic Fans and Blowers Market, By Pressure Range, 2026–2036 (USD Million)

Table 87. China: HVAC Plastic Fans and Blowers Market, By Application, 2026–2036 (USD Million)

Table 88. China: HVAC Plastic Fans and Blowers Market, By End User, 2026–2036 (USD Million)

Table 89. Japan: HVAC Plastic Fans and Blowers Market, By Product Type, 2026–2036 (USD Million)

Table 90. Japan: HVAC Plastic Fans and Blowers Market, By Product Type, 2026–2036 (Thousand Units)

Table 91. Japan: HVAC Plastic Centrifugal Fans Market, By Type, 2026–2036 (USD Million)

Table 92. Japan: HVAC Plastic Centrifugal Fans Market, By Type, 2026–2036 (Thousand Units)

Table 93. Japan: HVAC Plastic Axial Fans Market, By Type, 2026–2036 (USD Million)

Table 94. Japan: HVAC Plastic Axial Fans Market, By Type, 2026–2036 (Thousand Units)

Table 95. Japan: HVAC Plastic Fans and Blowers Market, By Technology, 2026–2036 (USD Million)

Table 96. Japan: HVAC Plastic Fans and Blowers Market, By Pressure Range, 2026–2036 (USD Million)

Table 97. Japan: HVAC Plastic Fans and Blowers Market, By Application, 2026–2036 (USD Million)

Table 98. Japan: HVAC Plastic Fans and Blowers Market, By End User, 2026–2036 (USD Million)

Table 99. India: HVAC Plastic Fans and Blowers Market, By Product Type, 2026–2036 (USD Million)

Table 100. India: HVAC Plastic Fans and Blowers Market, By Product Type, 2026–2036 (Thousand Units)

Table 101. India: HVAC Plastic Centrifugal Fans Market, By Type, 2026–2036 (USD Million)

Table 102. India: HVAC Plastic Centrifugal Fans Market, By Type, 2026–2036 (Thousand Units)

Table 103. India: HVAC Plastic Axial Fans Market, By Type, 2026–2036 (USD Million)

Table 104. India: HVAC Plastic Axial Fans Market, By Type, 2026–2036 (Thousand Units)

Table 105. India: HVAC Plastic Fans and Blowers Market, By Technology, 2026–2036 (USD Million)

Table 106. India: HVAC Plastic Fans and Blowers Market, By Pressure Range, 2026–2036 (USD Million)

Table 107. India: HVAC Plastic Fans and Blowers Market, By Application, 2026–2036 (USD Million)

Table 108. India: HVAC Plastic Fans and Blowers Market, By End User, 2026–2036 (USD Million)

Table 109. Thailand: HVAC Plastic Fans and Blowers Market, By Product Type, 2026–2036 (USD Million)

Table 110. Thailand: HVAC Plastic Fans and Blowers Market, By Product Type, 2026–2036 (Thousand Units)

Table 111. Thailand: HVAC Plastic Centrifugal Fans Market, By Type, 2026–2036 (USD Million)

Table 112. Thailand: HVAC Plastic Centrifugal Fans Market, By Type, 2026–2036 (Thousand Units)

Table 113. Thailand: HVAC Plastic Axial Fans Market, By Type, 2026–2036 (USD Million)

Table 114. Thailand: HVAC Plastic Axial Fans Market, By Type, 2026–2036 (Thousand Units)

Table 115. Thailand: HVAC Plastic Fans and Blowers Market, By Technology, 2026–2036 (USD Million)

Table 116. Thailand: HVAC Plastic Fans and Blowers Market, By Pressure Range, 2026–2036 (USD Million)

Table 117. Thailand: HVAC Plastic Fans and Blowers Market, By Application, 2026–2036 (USD Million)

Table 118. Thailand: HVAC Plastic Fans and Blowers Market, By End User, 2026–2036 (USD Million)

Table 119. Rest Of Asia-Pacific: HVAC Plastic Fans and Blowers Market, By Product Type, 2026–2036 (USD Million)

Table 120. Rest Of Asia-Pacific: HVAC Plastic Fans and Blowers Market, By Product Type, 2026–2036 (Thousand Units)

Table 121. Rest Of Asia-Pacific: HVAC Plastic Centrifugal Fans Market, By Type, 2026–2036 (USD Million)

Table 122. Rest Of Asia-Pacific: HVAC Plastic Centrifugal Fans Market, By Type, 2026–2036 (Thousand Units)

Table 123. Rest Of Asia-Pacific: HVAC Plastic Axial Fans Market, By Type, 2026–2036 (USD Million)

Table 124. Rest Of Asia-Pacific: HVAC Plastic Axial Fans Market, By Type, 2026–2036 (Thousand Units)

Table 125. Rest Of Asia-Pacific: HVAC Plastic Fans and Blowers Market, By Technology, 2026–2036 (USD Million)

Table 126. Rest Of Asia-Pacific: HVAC Plastic Fans and Blowers Market, By Pressure Range, 2026–2036 (USD Million)

Table 127. Rest Of Asia-Pacific: HVAC Plastic Fans and Blowers Market, By Application, 2026–2036 (USD Million)

Table 128. Rest Of Asia-Pacific: HVAC Plastic Fans and Blowers Market, By End User, 2026–2036 (USD Million)

Table 129. Latin America: HVAC Plastic Fans and Blowers Market, By Product Type, 2026–2036 (USD Million)

Table 130. Latin America: HVAC Plastic Fans and Blowers Market, By Product Type, 2026–2036 (Thousand Units)

Table 131. Latin America: HVAC Plastic Centrifugal Fans Market, By Type, 2026–2036 (USD Million)

Table 132. Latin America: HVAC Plastic Centrifugal Fans Market, By Type, 2026–2036 (Thousand Units)

Table 133. Latin America: HVAC Plastic Axial Fans Market, By Type, 2026–2036 (USD Million)

Table 134. Latin America: HVAC Plastic Axial Fans Market, By Type, 2026–2036 (Thousand Units)

Table 135. Latin America: HVAC Plastic Fans and Blowers Market, By Technology, 2026–2036 (USD Million)

Table 136. Latin America: HVAC Plastic Fans and Blowers Market, By Pressure Range, 2026–2036 (USD Million)

Table 137. Latin America: HVAC Plastic Fans and Blowers Market, By Application, 2026–2036 (USD Million)

Table 138. Latin America: HVAC Plastic Fans and Blowers Market, By End User, 2026–2036 (USD Million)

Table 139. Middle East and Africa: HVAC Plastic Fans and Blowers Market, By Product Type, 2026–2036 (USD Million)

Table 140. Middle East and Africa: HVAC Plastic Fans and Blowers Market, By Product Type, 2026–2036 (Thousand Units)

Table 141. Middle East and Africa: HVAC Plastic Centrifugal Fans Market, By Type, 2026–2036 (USD Million)

Table 142. Middle East and Africa: HVAC Plastic Centrifugal Fans Market, By Type, 2026–2036 (Thousand Units)

Table 143. Middle East and Africa: HVAC Plastic Axial Fans Market, By Type, 2026–2036 (USD Million)

Table 144. Middle East and Africa: HVAC Plastic Axial Fans Market, By Type, 2026–2036 (Thousand Units)

Table 145. Middle East and Africa: HVAC Plastic Fans and Blowers Market, By Technology, 2026–2036 (USD Million)

Table 146. Middle East and Africa: HVAC Plastic Fans and Blowers Market, By Pressure Range, 2026–2036 (USD Million)

Table 147. Middle East and Africa: HVAC Plastic Fans and Blowers Market, By Application, 2026–2036 (USD Million)

Table 148. Middle East and Africa: HVAC Plastic Fans and Blowers Market, By End User, 2026–2036 (USD Million)

LIST OF FIGURES

Figure 1. Research Process

Figure 2. Key Secondary Sources

Figure 3. Primary Research Techniques

Figure 4. Key Executives Interviewed

Figure 5. Breakdown Of Primary Interviews (Supply-Side & Demand-Side)

Figure 6. Market Sizing and Growth Forecast Approach

Figure 7. Global HVAC Plastic Fans and Blowers Market, By Product Type, 2026 Vs. 2036 (Usd Million)

Figure 8. Global HVAC Plastic Fans and Blowers Market, By Technology, 2026 Vs. 2036 (Usd Million)

Figure 9. Global HVAC Plastic Fans and Blowers Market, By Pressure Range, 2026 Vs. 2036 (Usd Million)

Figure 10. Global HVAC Plastic Fans and Blowers Market, By Application, 2026 Vs. 2036 (Usd Million)

Figure 11. Global HVAC Plastic Fans and Blowers Market, By End User, 2026 Vs. 2036 (Usd Million)

Figure 12. HVAC Plastic Fans and Blowers Market, By Geography, 2026 Vs 2036

Figure 13. Factors Affecting Market Growth

Figure 14. Global HVAC Fans and Blowers Market, By Product Type, 2026 Vs. 2036 (Usd Million)

Figure 15. Global HVAC Fans and Blowers Market, By Product Type, 2026 Vs. 2036 (Thousand Units)

Figure 16. Global HVAC Fans and Blowers Market, By Technology, 2026 Vs. 2036 (Usd Million)

Figure 17. Global HVAC Fans and Blowers Market, By Pressure Range, 2026 Vs. 2036 (Usd Million)

Figure 18. Global HVAC Fans and Blowers Market, By Application, 2026 Vs. 2036 (Usd Million)

Figure 19. Global HVAC Fans and Blowers Market, By End Use, 2026 Vs. 2036 (Usd Million)

Figure 20. Global HVAC Fans and Blowers Market, By Region, 2026 Vs. 2036 (Usd Million)

Figure 21. North America: HVAC Plastic Fans and Blowers Market Snapshot

Figure 22. Europe: HVAC Plastic Fans and Blowers Market Snapshot

Figure 23. Asia-Pacific: HVAC Plastic Fans and Blowers Market Snapshot

Figure 24. Latin America: HVAC Plastic Fans and Blowers Market Snapshot

Figure 25. Middle East and Africa: HVAC Plastic Fans and Blowers Market Snapshot

Figure 26. HVAC Fans and Blowers Market: Competitive Benchmarking, By Region

Figure 27. Competitive Dashboard: HVAC Fans and Blowers Market

Figure 28. Systemair Ab: Financial Overview (2025)

Figure 29. Nidec Corporation: Financial Overview (2025)

Figure 30. Delta Electronics, Inc.: Financial Overview (2024)

Figure 31. Daikin Industries, Ltd.: Financial Overview (2024)

Figure 32. Carrier Global Corporation: Financial Overview (2024)

Figure 33. Johnson Controls International Plc: Financial Overview (2025)

Figure 34. Munters Group Ab: Financial Overview (2024)

Figure 35. Nisshinbo Holdings Inc.: Financial Overview (2024)

Figure 36. Zhejiang Yilida Ventilator Co., Ltd.: Financial Overview (2024)

Figure 37. Panasonic Corporation: Financial Overview (2024)

Published Date: Jul-2025

Published Date: Jul-2025

Subscribe to get the latest industry updates