Resources

About Us

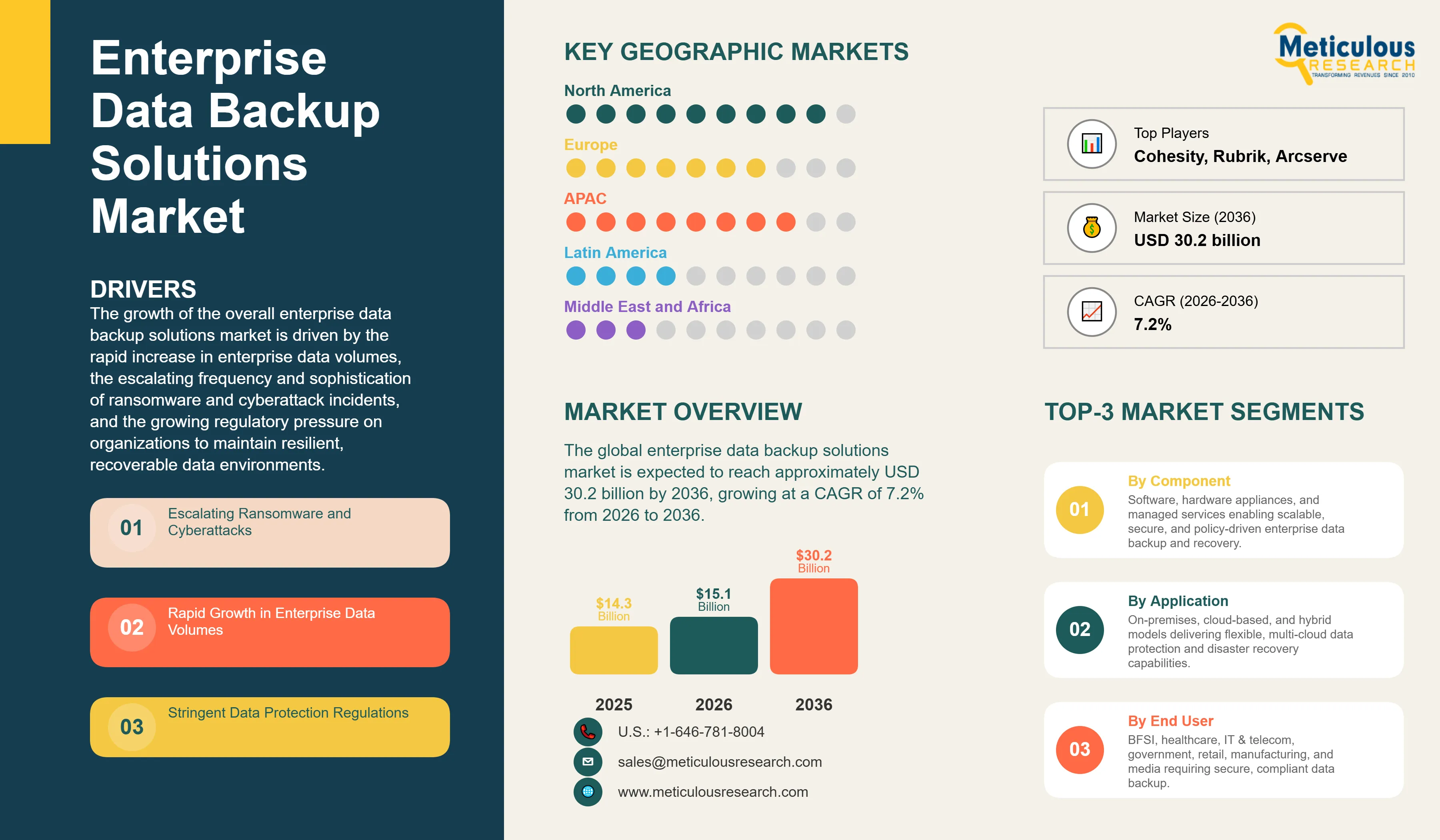

The global enterprise data backup solutions market was valued at USD 14.3 billion in 2025. The market is expected to reach approximately USD 30.2 billion by 2036 from USD 15.1 billion in 2026, growing at a CAGR of 7.2% from 2026 to 2036. The growth of the overall enterprise data backup solutions market is driven by the rapid increase in enterprise data volumes, the escalating frequency and sophistication of ransomware and cyberattack incidents, and the growing regulatory pressure on organizations to maintain resilient, recoverable data environments. As enterprises across industries seek to protect business-critical information and maintain operational continuity, data backup infrastructure has become a foundational element of broader IT resilience and risk management strategies. The accelerating shift toward cloud-native architectures, the growing complexity of hybrid IT environments, and the rising adoption of as-a-service delivery models continue to fuel significant growth of this market across all major geographic regions.

Click here to: Get Free Sample Pages of this Report

Enterprise data backup solutions are specialized technology platforms designed to capture, store, manage, and recover copies of business-critical data from diverse IT environments, including on-premises servers, virtual machines, cloud workloads, SaaS applications, and endpoints. These solutions encompass a broad set of capabilities such as incremental and continuous data protection, automated backup scheduling, deduplication and compression, encryption at rest and in transit, and granular recovery to ensure that organizations can restore operations quickly following data loss events. The market is shaped by innovations in immutable storage architecture, air-gapped backup vaults, and AI-driven anomaly detection, which substantially enhance the ability of enterprise IT teams to identify and respond to data threats before they escalate into full-scale incidents.

The market includes a wide spectrum of offerings, ranging from hardware-based backup appliances and tape library systems for air-gapped protection to software-defined backup platforms and fully managed cloud-based backup services. These solutions are increasingly integrated with workload-aware intelligence and policy-based automation to enable zero-touch backup operations, real-time recovery point monitoring, and compliance reporting across complex multi-cloud environments. The ability to deliver consistent recovery time objectives (RTOs) and recovery point objectives (RPOs) across heterogeneous data sources has made enterprise data backup solutions the cornerstone of IT infrastructure for organizations where data availability and regulatory compliance are business imperatives.

The global enterprise IT landscape is undergoing a fundamental shift, with organizations facing an unprecedented surge in structured and unstructured data generated by digital workloads, IoT devices, and AI-driven applications. This shift has placed enormous pressure on legacy backup architectures, accelerating the transition toward modern, cloud-integrated platforms that offer granular, application-aware protection. Simultaneously, the increasing adoption of zero-trust security frameworks and data sovereignty regulations is compelling enterprises to invest in backup solutions that offer comprehensive audit trails, geographic data residency controls, and end-to-end encryption, further broadening the addressable market for advanced backup and recovery technology providers.

Rise of Ransomware-Resilient Backup Architectures and Immutable Storage

Enterprise IT and security teams are rapidly transitioning away from traditional backup models toward ransomware-resilient architectures that incorporate immutable storage, air-gapped vaults, and multi-factor authentication for backup access. Vendors such as Cohesity and Rubrik have introduced purpose-built data security platforms that combine backup and recovery with threat intelligence, behavioral analytics, and automated clean-room recovery workflows. These platforms reduce recovery time from days to hours even in the wake of sophisticated ransomware attacks. The integration of cyber recovery vaults — isolated environments that store clean, validated backup copies — is gaining traction among BFSI and healthcare enterprises, where downtime and data loss carry direct regulatory and financial consequences. This shift is redefining the competitive landscape, pushing traditional backup vendors to embed security-first capabilities directly into their core backup workflows rather than treating them as add-on features.

Accelerating Adoption of Backup-as-a-Service and Cloud-Native Data Protection

The widespread migration of enterprise workloads to multi-cloud and hybrid cloud environments is fundamentally reshaping how backup solutions are architected, delivered, and consumed. Vendors including Veeam Software, Druva, and Commvault Systems are rapidly expanding their cloud-native portfolios to support workload-level protection across major hyperscaler platforms such as AWS, Microsoft Azure, and Google Cloud. The backup-as-a-service (BaaS) model is gaining significant adoption as it eliminates the capital expenditure associated with on-premises backup infrastructure while offering enterprises predictable, consumption-based pricing and seamless scalability. The growing need to protect SaaS application data — particularly from platforms like Microsoft 365, Salesforce, and Google Workspace — is creating a new and rapidly expanding category within the enterprise backup market, with vendors introducing lightweight, agentless connectors that integrate directly with SaaS APIs to deliver continuous, policy-driven data protection without impacting application performance.

|

Parameter |

Details |

|

Market Size by 2036 |

USD 30.2 Billion |

|

Market Size in 2026 |

USD 15.1 Billion |

|

Market Size in 2025 |

USD 14.3 Billion |

|

Market Growth Rate (2026-2036) |

CAGR of 7.2% |

|

Dominating Region |

North America |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Component, Deployment, Organization Size, End-use, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Drivers: Escalating Cyber Threats and Stringent Data Protection Regulations

A primary driver of the enterprise data backup solutions market is the dramatic rise in ransomware attacks, data breaches, and insider threats targeting enterprise IT environments. According to data published by the Cybersecurity and Infrastructure Security Agency (CISA) and cybersecurity firms such as Palo Alto Networks and CrowdStrike, ransomware incidents targeting enterprise infrastructure have grown significantly in frequency and financial impact over recent years, with attackers increasingly targeting backup repositories to prevent organizations from recovering without paying a ransom. This threat landscape is compelling enterprises across all sectors to invest in multi-layered backup strategies that incorporate immutable copies, offsite replication, and automated recovery testing. Simultaneously, regulations such as the EU General Data Protection Regulation (GDPR), the U.S. Health Insurance Portability and Accountability Act (HIPAA), and sector-specific mandates from bodies like the Prudential Regulation Authority (PRA) in the UK are imposing strict data retention, recovery, and auditability requirements on organizations, further accelerating investment in purpose-built enterprise backup platforms.

Opportunity: Proliferation of AI Workloads and Unstructured Data Protection

The rapid growth of artificial intelligence workloads, large language model training datasets, and unstructured data repositories across enterprise environments presents a significant opportunity for the enterprise data backup solutions market. As organizations build and expand AI infrastructure, the volume, diversity, and criticality of the data assets underpinning these systems are growing at an extraordinary pace. Traditional backup solutions were not designed to efficiently protect petabyte-scale unstructured data or the proprietary datasets used for model training and fine-tuning, creating a clear gap that modern backup vendors are actively moving to address. Vendors are introducing workload-aware backup policies, high-throughput data ingestion engines, and AI-optimized storage tiering to meet the specific recovery and retention needs of AI-driven enterprises. This emerging requirement is expected to drive a new wave of enterprise backup investments through 2036, particularly among technology, media, and financial services organizations with large-scale data science operations.

Why Does the Software Segment Lead the Market?

The software segment accounts for the largest share of the overall enterprise data backup solutions market in 2026. This dominance is primarily attributed to the central role that backup management software plays in orchestrating protection policies, scheduling jobs, managing data lifecycle, and enabling recovery across diverse and distributed IT environments. Enterprise software platforms from vendors such as Veritas Technologies, Commvault Systems, and Veeam Software offer broad workload coverage — spanning physical servers, virtual machines, cloud instances, databases, and SaaS applications — within a unified management console, making them the preferred choice for large enterprises seeking to consolidate their backup operations. The increasing need for policy-driven automation, compliance reporting, and integration with security information and event management (SIEM) tools is further reinforcing the primacy of software as the most value-generating component in the enterprise backup stack.

The services segment is expected to witness the fastest growth during the forecast period. As enterprises increasingly outsource backup management to reduce operational complexity and address internal skills shortages, managed backup services and professional implementation services from providers such as IBM and Dell Technologies are gaining rapid traction. The shift toward outcome-based service agreements — where vendors guarantee specific RTOs and RPOs as part of their managed service contracts — is significantly expanding the addressable market for backup services, particularly among mid-sized enterprises that lack the internal capacity to operate and maintain complex backup environments.

How Does the Cloud-based Segment Dominate?

Based on deployment, the cloud-based segment holds the largest share of the overall enterprise data backup solutions market in 2026. This is primarily driven by the accelerating migration of enterprise workloads to public and private cloud environments and the growing preference for backup-as-a-service delivery models that eliminate the capital expenditure and operational burden associated with on-premises backup infrastructure. Enterprises are increasingly drawn to cloud-based backup platforms for their ability to scale capacity on demand, replicate data across geographically distributed availability zones, and provide built-in disaster recovery capabilities without requiring a secondary physical site. Vendors such as Druva and Zerto (an HPE company) have built their entire product portfolios around cloud-native backup and disaster recovery, offering lightweight, agentless solutions that integrate directly with hyperscaler environments and eliminate the need for any on-premises backup hardware.

The hybrid deployment segment is expected to witness steady growth through 2036, as large enterprises operating complex IT environments with a mix of legacy on-premises infrastructure and modern cloud workloads seek unified backup platforms capable of managing protection policies across both environments from a single control plane.

Why Do Large Enterprises Lead Adoption?

The large enterprises segment holds the dominant share of the global enterprise data backup solutions market in 2026. This is primarily because large organizations manage significantly greater volumes of data across more diverse and geographically distributed IT environments, requiring sophisticated backup platforms capable of handling petabyte-scale workloads, enforcing complex retention policies, and supporting rapid recovery across multiple sites and cloud regions. Large enterprises in sectors such as BFSI, healthcare, and government are also subject to the most stringent regulatory requirements for data retention and recoverability, driving sustained investment in enterprise-grade backup infrastructure. Vendors such as Veritas Technologies and IBM have historically derived the majority of their backup revenue from large enterprise accounts, and continue to invest in capabilities — such as mainframe backup support, air-gapped vault integration, and advanced compliance reporting — that specifically address the needs of this segment.

The small and medium-sized enterprises (SMEs) segment, however, is expected to grow at the fastest CAGR during the forecast period. The availability of affordable, easy-to-deploy cloud-based backup solutions and the growing awareness of ransomware risks among smaller organizations are driving rapid adoption in this segment. Vendors such as Acronis and Arcserve are actively targeting the SME segment with simplified, cost-effective backup platforms that deliver enterprise-grade protection without requiring dedicated IT staff for management.

Why Does the BFSI Segment Lead the Market?

The BFSI segment commands the largest share of the global enterprise data backup solutions market in 2026. This dominance reflects the sector's exceptionally stringent regulatory obligations for data retention, operational resilience, and recovery capability, which are enforced by regulators including the U.S. Federal Financial Institutions Examination Council (FFIEC), the European Banking Authority (EBA), and the Bank of England's Prudential Regulation Authority (PRA). Financial institutions are required to maintain multiple copies of transactional data across geographically separated locations, perform regular recovery testing, and demonstrate the ability to restore critical systems within tightly defined timeframes following any disruption. These requirements make the BFSI sector a consistent and high-volume consumer of advanced enterprise backup solutions from vendors such as Commvault Systems and Cohesity.

The healthcare and life sciences segment, however, is poised for the fastest growth through 2036, fueled by the accelerating digitization of clinical data, the proliferation of electronic health records (EHR) systems, and the increasing targeting of healthcare organizations by ransomware threat actors. Healthcare providers and life sciences companies are investing heavily in ransomware-resilient backup architectures and air-gapped recovery environments to protect patient data and ensure compliance with regulations such as HIPAA in the U.S. and the EU Medical Device Regulation (MDR) in Europe.

How is North America Maintaining Dominance in the Global Enterprise Data Backup Solutions Market?

North America holds the largest share of the global enterprise data backup solutions market in 2026. This dominance is primarily attributed to the high concentration of large enterprises across sectors such as BFSI, healthcare, technology, and government, all of which operate at significant scale and face rigorous regulatory requirements for data protection and recoverability. The U.S. alone accounts for a substantial portion of global enterprise backup spending, supported by the presence of leading solution vendors including Veritas Technologies, Commvault Systems, Cohesity, Rubrik, and Druva, as well as a highly developed cloud infrastructure ecosystem anchored by AWS, Microsoft Azure, and Google Cloud. The ongoing wave of ransomware attacks targeting U.S. critical infrastructure and enterprises is further accelerating investment in advanced backup and cyber recovery platforms across the region.

Which Factors Support Europe and Asia-Pacific Market Growth?

Europe accounts for a significant share of the global enterprise data backup solutions market, driven primarily by the comprehensive data protection requirements established under the GDPR, which mandates that organizations implement technical and organizational measures to ensure the availability and resilience of processing systems and the ability to restore personal data in a timely manner following a physical or technical incident. Countries including Germany, the United Kingdom, France, and the Netherlands are at the forefront of enterprise backup adoption, with organizations across financial services, healthcare, and public sector verticals investing heavily in compliant, auditable backup architectures. The growing focus on digital sovereignty and the preference for data residency within national borders are also driving demand for private cloud and on-premises backup solutions across European enterprises.

Asia-Pacific is expected to record the fastest growth in the enterprise data backup solutions market during the forecast period. This growth is underpinned by the rapid pace of digital transformation across major economies including China, India, Japan, South Korea, and the emerging markets of Southeast Asia. The rapid expansion of cloud infrastructure, the growing adoption of data protection regulations such as India's Digital Personal Data Protection (DPDP) Act and China's Personal Information Protection Law (PIPL), and the increasing awareness of ransomware risks among enterprises across the region are collectively accelerating investment in enterprise-grade backup and recovery platforms. The presence of major regional IT service providers and system integrators is further supporting the deployment of complex backup environments across mid-sized and large enterprises throughout Asia-Pacific.

Companies such as Veritas Technologies LLC, Commvault Systems, Inc., Veeam Software Group GmbH, and Dell Technologies Inc. (Dell EMC) lead the global enterprise data backup solutions market with comprehensive portfolios spanning backup software, hardware appliances, and managed services, particularly for large-scale enterprise and multi-cloud environments. Meanwhile, players including IBM Corporation, Cohesity, Inc., Rubrik, Inc., and Druva Inc. focus on next-generation data security and cloud-native backup platforms targeting enterprises undergoing cloud transformation and those seeking ransomware-resilient data protection. Established and emerging players such as Acronis International GmbH, Arcserve (USA) LLC, Zerto (an HPE Company), and OpenText Corporation (Carbonite) are strengthening the market through innovations in backup-as-a-service delivery, SaaS data protection, and unified endpoint and server backup for mid-sized enterprises.

The global enterprise data backup solutions market is expected to grow from USD 14.5 billion in 2026 to USD 38.5 billion by 2036.

The global enterprise data backup solutions market is projected to grow at a CAGR of 10.3% from 2026 to 2036.

The software segment is expected to dominate the market in 2026 due to its central role in orchestrating backup policies, enabling multi-workload protection, and supporting compliance reporting across complex enterprise IT environments. However, the services segment is projected to be the fastest-growing segment, driven by the accelerating adoption of managed backup services and backup-as-a-service delivery models among enterprises seeking to reduce operational complexity.

The accelerating migration of enterprise workloads to multi-cloud environments is driving strong demand for cloud-native backup platforms and backup-as-a-service delivery models that offer scalable, pay-as-you-go data protection without on-premises infrastructure. Simultaneously, the surge in ransomware attacks is compelling organizations to adopt immutable storage, air-gapped vaults, and integrated cyber recovery workflows — fundamentally elevating backup from a routine IT function to a critical component of enterprise security and resilience strategy.

North America holds the largest share of the global enterprise data backup solutions market in 2026. This dominance is primarily attributed to the high concentration of large enterprises subject to stringent data protection regulations, the presence of leading backup solution vendors, and the advanced cloud infrastructure ecosystem in the U.S. and Canada.

The leading companies include Veritas Technologies LLC, Commvault Systems, Inc., Veeam Software Group GmbH, Dell Technologies Inc. (Dell EMC), IBM Corporation, Cohesity, Inc., Rubrik, Inc., and Druva Inc.

1. Introduction

1.1. Market Definition

1.2. Market Scope

1.3. Research Methodology

1.4. Assumptions & Limitations

2. Executive Summary

3. Market Overview

3.1. Introduction

3.2. Market Dynamics

3.2.1. Drivers

3.2.2. Restraints

3.2.3. Opportunities

3.2.4. Challenges

3.3. Impact of Cloud Adoption and Hybrid IT on Enterprise Data Backup

3.4. Regulatory Landscape & Data Protection Standards

3.5. Porter's Five Forces Analysis

4. Global Enterprise Data Backup Solutions Market, by Component

4.1. Introduction

4.2. Software

4.2.1. Backup Management & Orchestration Software

4.2.2. Data Deduplication & Compression Software

4.2.3. Backup Monitoring & Reporting Software

4.3. Hardware

4.3.1. Backup Appliances (Purpose-built Backup Appliances, Converged Backup Appliances)

4.3.2. Tape Library Systems

4.3.3. Disk-based Storage Systems (NAS/SAN for Backup)

4.4. Services

4.4.1. Professional Services (Consulting, Implementation & Integration, Training & Support)

4.4.2. Managed Backup Services / Backup-as-a-Service (BaaS)

5. Global Enterprise Data Backup Solutions Market, by Deployment

5.1. Introduction

5.2. On-premises

5.2.1. Physical Server-based Backup

5.2.2. Virtual Appliance-based Backup

5.3. Cloud-based

5.3.1. Public Cloud Backup

5.3.2. Private Cloud Backup

5.4. Hybrid

5.4.1. Hybrid Cloud Backup

5.4.2. Disaster Recovery as a Service (DRaaS)

6. Global Enterprise Data Backup Solutions Market, by Organization Size

6.1. Introduction

6.2. Large Enterprises

6.3. Small & Medium-sized Enterprises (SMEs)

7. Global Enterprise Data Backup Solutions Market, by End-use

7.1. Introduction

7.2. BFSI

7.2.1. Banking & Financial Services

7.2.2. Insurance

7.3. Healthcare & Life Sciences

7.3.1. Hospitals & Healthcare Providers

7.3.2. Pharmaceutical & Biotechnology Companies

7.4. IT & Telecom

7.4.1. IT Services & Software Companies

7.4.2. Telecommunications Operators

7.5. Government & Public Sector

7.5.1. Federal & Central Government

7.5.2. Defense & Intelligence

7.6. Retail & E-commerce

7.6.1. Retail Chains

7.6.2. E-commerce Platforms

7.7. Manufacturing

7.7.1. Discrete Manufacturing

7.7.2. Process Manufacturing

7.8. Media & Entertainment

7.8.1. Digital Content Producers

7.8.2. Streaming & Broadcasting Companies

7.9. Other End-users

8. Global Enterprise Data Backup Solutions Market, by Region

8.1. Introduction

8.2. North America

8.2.1. U.S.

8.2.2. Canada

8.3. Europe

8.3.1. Germany

8.3.2. United Kingdom

8.3.3. France

8.3.4. Netherlands

8.3.5. Italy

8.3.6. Spain

8.3.7. Rest of Europe

8.4. Asia-Pacific

8.4.1. China

8.4.2. India

8.4.3. Japan

8.4.4. South Korea

8.4.5. Southeast Asia

8.4.6. Australia

8.4.7. Rest of Asia-Pacific

8.5. Latin America

8.5.1. Brazil

8.5.2. Mexico

8.5.3. Rest of Latin America

8.6. Middle East & Africa

8.6.1. Saudi Arabia

8.6.2. UAE

8.6.3. South Africa

8.6.4. Rest of Middle East & Africa

9. Competitive Landscape

9.1. Overview

9.2. Key Growth Strategies

9.3. Competitive Benchmarking

9.4. Competitive Dashboard

9.4.1. Industry Leaders

9.4.2. Market Differentiators

9.4.3. Vanguards

9.4.4. Emerging Companies

9.5. Market Ranking / Positioning Analysis of Key Players, 2025

10. Company Profiles (Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

10.1. Veritas Technologies LLC

10.2. Commvault Systems, Inc.

10.3. Veeam Software Group GmbH

10.4. Dell Technologies Inc. (Dell EMC)

10.5. IBM Corporation

10.6. Cohesity, Inc.

10.7. Rubrik, Inc.

10.8. Druva Inc.

10.9. Acronis International GmbH

10.10. Arcserve (USA) LLC

10.11. Zerto (An HPE Company)

10.12. OpenText Corporation (Carbonite)

11. Appendix

11.1. Questionnaire

11.2. Related Reports

Published Date: Aug-2025

Published Date: Jan-2025

Published Date: Jan-2025

Published Date: Apr-2024

Subscribe to get the latest industry updates