Resources

About Us

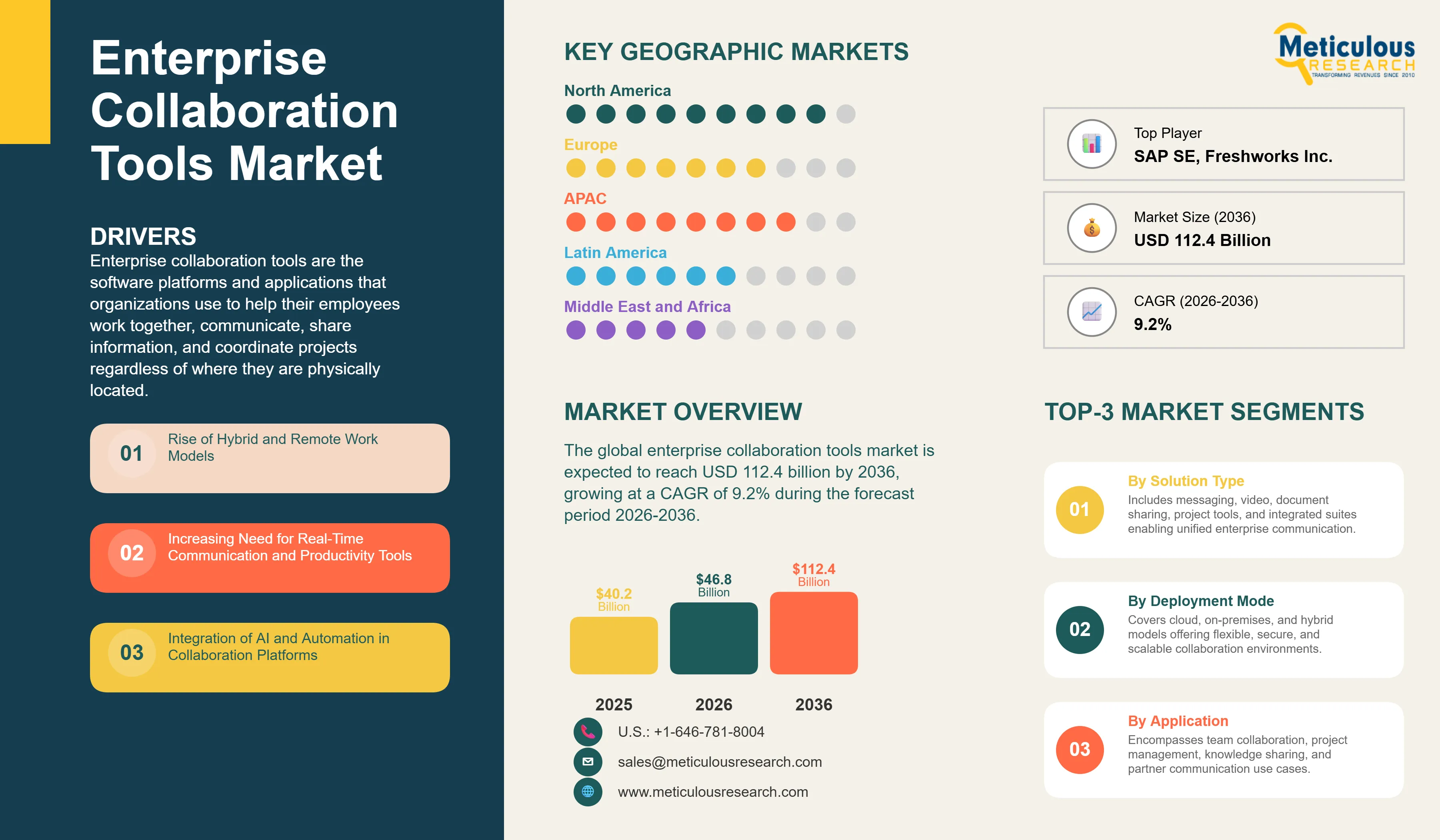

The global enterprise collaboration tools market was valued at USD 40.2 billion in 2025. This market is expected to reach USD 112.4 billion by 2036 from an estimated USD 46.8 billion in 2026, growing at a CAGR of 9.2% during the forecast period 2026-2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Enterprise collaboration tools are the software platforms and applications that organizations use to help their employees work together, communicate, share information, and coordinate projects regardless of where they are physically located. These tools range from chat and messaging applications like Microsoft Teams and Slack that allow colleagues to have instant conversations, to video conferencing platforms like Zoom that connect teams face-to-face across distances, to document sharing systems like Google Workspace and SharePoint that let multiple people work on the same file simultaneously, to project management tools like Asana and Monday.com that help teams track tasks, deadlines, and progress. Taken together, these tools form the digital workplace infrastructure that enables modern organizations to function effectively across offices, homes, and multiple countries.

The market is growing because the way people work has fundamentally changed, and there is no going back to purely office-based working for most knowledge workers. The COVID-19 pandemic accelerated a shift toward remote and hybrid working that was already underway, and the majority of knowledge workers now expect to have the flexibility to work from various locations as part of their employment package. Organizations that have discovered that remote and hybrid teams can maintain or even improve productivity with the right collaboration tools in place are not reverting to requiring full-time office attendance, meaning the demand for enterprise collaboration software is now structural and permanent rather than temporary. Additionally, the rapid integration of artificial intelligence into collaboration platforms is creating a new category of AI-assisted work that promises to automate routine tasks, summarize long conversation threads, generate meeting notes automatically, and provide intelligent assistance to workers across every type of collaboration activity, making these tools increasingly indispensable to daily work.

Two significant opportunities are shaping the next phase of market growth. The integration of AI copilot features into existing collaboration platforms, most visibly through Microsoft Copilot integrated with Teams and Office 365 and Google Gemini integrated with Google Workspace, is creating a compelling upgrade incentive for existing enterprise customers to move to higher-priced premium tiers that include AI features. This AI-driven upsell dynamic is already generating significant revenue growth at Microsoft and Google and is being rapidly replicated across the broader collaboration software market. In addition, the very large number of small and medium-sized enterprises globally that still rely on basic email and consumer-grade communication tools rather than purpose-built enterprise collaboration platforms represents a large and largely untapped market that is being addressed by more affordable cloud-based solutions and is expected to be a significant growth driver throughout the forecast period.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 112.4 Billion |

|

Market Size in 2026 |

USD 46.8 Billion |

|

Market Size in 2025 |

USD 40.2 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 9.2% |

|

Dominating Solution Type |

Integrated Collaboration Suites |

|

Fastest Growing Solution Type |

Project and Workflow Collaboration Tools |

|

Dominating Deployment Mode |

Cloud-Based |

|

Fastest Growing Deployment Mode |

Hybrid Deployment |

|

Dominating Application |

Internal Team Collaboration |

|

Fastest Growing Application |

Knowledge Sharing and Training |

|

Dominating Enterprise Size |

Large Enterprises |

|

Fastest Growing Enterprise Size |

Small & Medium Enterprises (SMEs) |

|

Dominating Industry Vertical |

IT & Telecommunications |

|

Fastest Growing Industry Vertical |

Healthcare |

|

Dominating Feature Type |

Real-Time Collaboration Features |

|

Fastest Growing Feature Type |

AI and Automation Features |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

AI Integration Transforming Collaboration Platforms into Intelligent Work Assistants

One of the most important trends in the enterprise collaboration tools market is the rapid integration of generative AI into leading platforms. Tools that were once used mainly for communication and coordination are now evolving into intelligent work assistants that help employees complete tasks more efficiently.

Microsoft’s Copilot for Microsoft 365, offered as a premium add-on to Microsoft Teams and Office 365, can generate meeting summaries, draft emails, create presentations from documents, and answer questions by searching across a user’s communications. Similarly, Google’s Gemini integration with Google Workspace provides advanced capabilities for users of Google Meet, Gmail, and Google Docs.

The business impact of these AI features is significant. Microsoft reports that enterprise users of Copilot save several hours each week on tasks like email management, meeting notes, and document creation. This leads to clear productivity gains, making the added subscription cost worthwhile and driving strong adoption among organizations.

At the same time, competition is intensifying. The advancements by Microsoft and Google are pushing other vendors to accelerate their AI development. Companies such as Zoom, Salesforce (Slack), Atlassian, and many smaller players are rapidly introducing features like automatic transcription, smart task suggestions, AI-generated summaries, and improved search.

This growing focus on AI is expanding the overall market for collaboration tools by increasing per-user value and revenue. It is also raising the barrier for new entrants, who must now offer not only a strong core platform but also advanced AI capabilities to remain competitive.

Platform Consolidation Reducing the Number of Tools Employees Use

Another key trend in collaboration software is the shift toward using fewer, more integrated tools. Between 2015 and 2022, companies adopted many specialized apps for messaging, video calls, documents, project management, and email. As a result, employees often had to switch between multiple tools throughout the day, creating confusion, reducing focus, and increasing workload.

To solve this, many organizations now prefer all-in-one platforms that bring most collaboration features into a single system. For example, Microsoft Teams combines chat, video meetings, file sharing, and app integrations in one place. Similarly, Google Workspace connects tools like Meet, Chat, Docs, Drive, and Gmail into a unified experience. This reduces the need to switch between apps and makes IT management and security easier.

This trend is also changing how companies spend on software. Many businesses are reducing their use of standalone tools like Zoom, Slack, and Dropbox, and instead expanding their contracts with major platforms like Microsoft or Google.

As a result, specialized vendors are under pressure to adapt. Some are improving integration with larger platforms to stay relevant, while others are focusing on niche areas where their unique features stand out. For example, Zoom is expanding beyond video meetings into services like Zoom Phone, Zoom Docs, and AI features to compete as a broader platform.

Overall, platform consolidation is simplifying workflows for employees while reshaping competition in the collaboration software market.

Rise of Hybrid and Remote Work Models

The most powerful and durable driver of the enterprise collaboration tools market is the structural shift to hybrid and remote working that has permanently changed how knowledge workers work and what technology they need to do so effectively. Before 2020, most organizations relied on physical proximity and in-person interaction as the primary mechanism for team coordination, with digital collaboration tools playing a supporting rather than central role. The COVID-19 pandemic forced essentially the entire global knowledge workforce to rely entirely on digital collaboration tools overnight, and the experience demonstrated that well-equipped remote teams could maintain productivity across most types of knowledge work. The result is that the majority of knowledge workers in developed markets now work in hybrid arrangements that combine some office time with regular remote working, and both organizations and employees expect the digital collaboration infrastructure to support seamless and effective work regardless of physical location. This expectation has raised the minimum acceptable standard for enterprise collaboration tooling across virtually every organization and is generating sustained investment in upgrading, expanding, and maintaining enterprise collaboration software as a core operational infrastructure rather than a discretionary technology.

Integration of AI and Automation in Collaboration Platforms

The integration of AI capabilities into enterprise collaboration platforms is creating the most significant product upgrade cycle in the market's history, as organizations that have already standardized on a collaboration platform are being presented with compelling AI-powered feature upgrades that justify moving to premium pricing tiers and accelerating platform adoption across their workforces. The productivity value of AI meeting summaries, intelligent email drafting, automated document generation, and smart search across organizational knowledge is measurable and significant, providing the ROI justification that enterprise procurement teams require for technology spending approvals. Microsoft's early commercial success with Copilot for Microsoft 365, which achieved USD 1 billion in annual revenue run rate faster than any other Microsoft product in the company's history, demonstrates the commercial appetite for AI-enhanced collaboration features among enterprise customers and is creating competitive urgency for every other collaboration platform to invest in equivalent AI capabilities.

AI Copilots and Smart Collaboration Assistants

The development and deployment of AI copilot capabilities within collaboration platforms represents the largest single commercial growth opportunity in the enterprise collaboration tools market over the forecast period, as AI features are driving per-user revenue increases across the existing installed base while simultaneously attracting new customers who select platforms based on the quality of their AI capabilities. The opportunity is not simply about adding AI as a feature but about fundamentally reimagining the value proposition of collaboration software: from a tool that connects people to one that actively helps people accomplish their work. An AI assistant that can attend a meeting on a user's behalf and produce an accurate summary with action items, that can draft a complex document based on a brief prompt drawing on relevant company knowledge, or that can monitor a project's communications and proactively flag risks or blockers before they become problems, provides a qualitatively different and substantially higher value than the underlying communication and coordination capabilities of the platform. Vendors that successfully demonstrate this higher-order value through their AI features will be able to command the premium pricing and long-term customer retention that builds highly profitable software businesses.

Expansion in SMEs and Emerging Markets

The large population of small and medium-sized enterprises globally that have not yet adopted purpose-built enterprise collaboration platforms represents a significant growth opportunity as cloud-based SaaS pricing models make professional-grade collaboration tools accessible at price points that fit smaller organization budgets. A ten-person company can now access Microsoft Teams, Google Workspace, or Zoho Cliq for a few dollars per user per month, compared with the enterprise software investments that were required to deploy comparable capabilities a decade ago. The SME market is particularly large in emerging economies including India, Southeast Asia, Latin America, and Africa where the business population is growing rapidly and where mobile-first cloud-based tools can reach customers who have never had access to enterprise software. Vendors with strong SME offerings including Zoho, Freshworks, and several regional specialists are building significant businesses in these markets, and the larger platforms including Microsoft and Google are also actively competing for SME customers through their freemium and entry-level pricing tiers.

By Solution Type: In 2026, Integrated Collaboration Suites to Dominate

Based on solution type, the global market for enterprise collaboration tools is segmented into communication and messaging tools, video conferencing and virtual meeting tools, content and document collaboration tools, project and workflow collaboration tools, enterprise social networks and engagement platforms, and integrated collaboration suites. In 2026, the integrated collaboration suites segment is expected to account for the largest share of the global enterprise collaboration tools market. Integrated suites including Microsoft 365 with Teams, Google Workspace, and Salesforce's integrated platform represent the highest-revenue category because they combine multiple collaboration capabilities in a single subscription, capture the entire collaboration budget of an enterprise rather than a single use case, and benefit from the consolidation trend that is directing enterprise spending toward fewer, more comprehensive platforms. Microsoft 365 and Google Workspace together serve hundreds of millions of users globally and represent by far the largest revenue pools in the collaboration software market.

However, the project and workflow collaboration tools segment is projected to register the highest CAGR during the forecast period. The explosion of knowledge work driven by digital transformation across all industries is creating growing demand for structured project management and workflow automation tools that help teams coordinate complex multi-step work more efficiently. Asana, Monday.com, and Atlassian's Jira and Confluence products are growing rapidly as organizations recognize that unstructured chat and document sharing tools are insufficient for managing complex cross-functional projects and need dedicated workflow and project coordination capabilities.

By Deployment Mode: In 2026, Cloud-Based to Hold the Largest Share

Based on deployment mode, the global market for enterprise collaboration tools is segmented into cloud-based, on-premises, and hybrid deployment. In 2026, the cloud-based segment is expected to account for the largest share of the global enterprise collaboration tools market. Cloud-based deployment is overwhelmingly the default choice for enterprise collaboration software in the current market, because collaboration tools fundamentally need to be accessible from anywhere and on any device, which is only practically achievable through cloud delivery. The continuous feature updates, automatic scaling, and global availability that cloud platforms deliver without customer-managed infrastructure maintenance have made on-premises alternatives progressively less competitive, and even large enterprises that were previously committed to on-premises IT are migrating their collaboration workloads to cloud platforms.

However, the hybrid deployment segment is projected to register the highest CAGR during the forecast period. Some regulated industries including financial services, healthcare, and government have data residency and sovereignty requirements that prevent them from storing all communications and documents in public cloud infrastructure, but want the user experience and features of cloud collaboration platforms. Hybrid deployments that store sensitive data on-premises or in private cloud environments while using cloud-delivered application interfaces are growing as a compromise that meets regulatory requirements without sacrificing user experience.

By Application: In 2026, Internal Team Collaboration to Hold the Largest Share

Based on application, the global market is segmented into internal team collaboration, customer and partner collaboration, project and program management, knowledge sharing and training, innovation and ideation platforms, and other applications. In 2026, the internal team collaboration segment is expected to account for the largest share of the global enterprise collaboration tools market. Internal team communication and coordination between colleagues is the most fundamental and highest-frequency use case for enterprise collaboration tools, covering the daily chat messages, video calls, document sharing, and meeting coordination that constitute the majority of collaboration activity across every organization. This is also the application where the network effects of having all employees on the same platform are strongest, creating winner-take-most dynamics that benefit the dominant platform providers.

However, the knowledge sharing and training segment is projected to register the highest CAGR during the forecast period. Organizations are increasingly recognizing that much of their institutional knowledge is trapped in individual employees' heads or in unstructured conversation threads, and that capturing and making this knowledge accessible through structured knowledge management and learning platforms has significant productivity and resilience value. The combination of AI-powered knowledge discovery, which can find relevant information from across an organization's communications and documents based on a natural language query, with formal learning management system capabilities is creating a new and fast-growing category of knowledge collaboration tools.

By Industry Vertical: In 2026, IT and Telecommunications to Hold the Largest Share

Based on industry vertical, the global market is segmented into IT and telecommunications, BFSI, healthcare, manufacturing, retail and e-commerce, education, government, and others. In 2026, the IT and telecommunications segment is expected to account for the largest share of the global enterprise collaboration tools market. Technology companies are the heaviest users of enterprise collaboration tools per employee, driven by the nature of software development and technology work which is inherently collaborative, project-based, and often distributed across global teams and time zones. The IT sector adopted cloud collaboration tools earliest and at highest penetration rates, and technology companies typically spend more per employee on collaboration software than any other industry vertical, making them the highest-revenue vertical despite not necessarily being the largest employer.

However, the healthcare segment is projected to register the highest CAGR during the forecast period. Healthcare organizations are undergoing significant digital transformation of their communication and coordination workflows, driven by the need to improve care coordination across multidisciplinary clinical teams, the challenge of connecting administrative staff working remotely with clinical staff on-site, and the growing use of telehealth that requires robust video communication capabilities. The complexity of healthcare compliance requirements, including HIPAA in the U.S. and equivalent regulations in other markets, creates demand for specialist healthcare collaboration platforms with built-in compliance features that support faster growth of purpose-built healthcare collaboration solutions.

Enterprise Collaboration Tools Market by Region: North America Leading by Share, Asia-Pacific by Growth

Based on geography, the global market for enterprise collaboration tools is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

In 2026, North America is expected to account for the largest share of the global enterprise collaboration tools market. The United States is home to virtually all of the world's leading enterprise collaboration software companies, including Microsoft, Google, Slack/Salesforce, Zoom, Atlassian, Asana, Monday.com, Dropbox, Box, and RingCentral, and the U.S. enterprise software market is the world's largest and most mature. American enterprises were among the first to broadly adopt cloud-based collaboration tools, and the U.S. knowledge worker population, which numbers in the tens of millions across technology, financial services, healthcare, professional services, and media industries, represents the highest-spending collaboration software customer base in the world. The strong culture of flexible and remote working in the U.S. technology sector, which has been a model for broader adoption across the economy, has maintained high levels of collaboration tool investment even as office attendance has partially recovered from pandemic lows. Canada's advanced technology sector in cities including Toronto, Vancouver, and Montreal contributes additional North American market demand, with strong Canadian adoption of U.S.-origin collaboration platforms.

However, the Asia-Pacific enterprise collaboration tools market is expected to grow at the fastest CAGR during the forecast period. Asia-Pacific is the world's largest and fastest-growing region for enterprise software adoption more broadly, and its diverse range of markets from the technologically sophisticated workforces of Japan, South Korea, Singapore, and Australia to the very large and rapidly digitalizing economies of India, China, Indonesia, and Vietnam collectively represent an enormous and growing addressable market for enterprise collaboration tools. India's very large and globally connected IT services industry, which provides software development and business process services to clients worldwide and employs millions of knowledge workers who work across time zones with distributed international teams, is one of the most intensive users of enterprise collaboration tools in the world and is a major demand driver for the Asia-Pacific market. China's large enterprise software market has significant domestic collaboration platform alternatives including DingTalk from Alibaba, WeCom from Tencent, and Feishu from ByteDance that compete with international platforms, but the growing international business activities of Chinese enterprises and the subsidiaries of multinational companies operating in China generate meaningful demand for global platform adoption. Southeast Asian economies including Indonesia, Vietnam, and Thailand are experiencing rapid enterprise software adoption as their business communities grow and digitalize.

Europe is a large and sophisticated enterprise collaboration tools industry with high adoption rates across the UK, Germany, France, the Netherlands, and Scandinavia. European enterprises were significant early adopters of cloud collaboration tools, particularly Zoom and Microsoft Teams during the pandemic, and the region's strong emphasis on data privacy under GDPR has created demand for collaboration platforms with strong data governance, geographic data residency options, and privacy-by-design features that European enterprises and regulators require. Several European countries including Germany and the Netherlands have strong digital workplace cultures that support high per-user collaboration software spending, and the European public sector including government ministries, healthcare systems, and educational institutions represents a large and growing customer base for compliant and security-certified collaboration platforms. Latin America and the Middle East and Africa are growing collaboration markets as enterprise software adoption accelerates alongside economic development in these regions.

The enterprise collaboration tools industry is highly concentrated at the top, with Microsoft and Google collectively serving the majority of enterprise collaboration users globally through their integrated productivity suites, alongside a competitive ecosystem of specialist vendors targeting specific collaboration use cases, industries, or customer segments. Competition is based on feature breadth and integration quality, AI capability leadership, security and compliance credentials, user experience and adoption rates, pricing flexibility, and the strength of the platform ecosystem and third-party integrations.

Microsoft is the dominant player in the enterprise collaboration market through Microsoft 365 and Teams, which combines chat, video meetings, file storage, and integration with the Office productivity suite in the most widely adopted enterprise collaboration platform globally. Google Workspace competes directly for the broad enterprise collaboration market with Gmail, Meet, Chat, Drive, and Docs, with particular strength in education and among tech-forward enterprises. Slack, now owned by Salesforce and integrated with Salesforce's CRM platform, is the leading specialist team messaging platform with strong adoption among technology companies and development teams. Zoom remains the leading dedicated video conferencing platform and is expanding into broader collaboration functionality. Atlassian provides the leading developer and technical team collaboration tools through Jira for project tracking and Confluence for knowledge management.

The report provides a comprehensive competitive analysis based on a thorough review of leading players' product portfolios, enterprise customer bases, AI capabilities, geographic presence, and recent strategic developments. Some of the key players operating in the global enterprise collaboration tools market include Microsoft Corporation (U.S.), Google LLC (U.S.), Slack Technologies/Salesforce (U.S.), Zoom Video Communications Inc. (U.S.), Cisco Systems Inc. (U.S.), Atlassian Corporation Plc (Australia/U.S.), Asana Inc. (U.S.), Monday.com Ltd. (Israel), Dropbox Inc. (U.S.), Box Inc. (U.S.), SAP SE (Germany), IBM Corporation (U.S.), RingCentral Inc. (U.S.), Zoho Corporation Pvt. Ltd. (India), and Freshworks Inc. (U.S./India), among others.

The global enterprise collaboration tools market is expected to reach USD 112.4 billion by 2036 from an estimated USD 46.8 billion in 2026, at a CAGR of 9.2% during the forecast period 2026-2036.

In 2026, the integrated collaboration suites segment is expected to hold the largest share of the global enterprise collaboration tools market, driven by Microsoft 365 with Teams and Google Workspace collectively serving hundreds of millions of enterprise users and capturing the full collaboration spending of enterprises rather than single use cases.

The project and workflow collaboration tools segment is expected to register the highest CAGR during the forecast period 2026-2036, driven by the growing recognition that unstructured messaging tools are insufficient for managing complex multi-step work and the rapid adoption of dedicated project management and workflow automation platforms across organizations of all sizes.

In 2026, the internal team collaboration segment is expected to hold the largest share of the global enterprise collaboration tools market, reflecting daily inter-colleague communication and coordination being the most fundamental and highest-frequency use case for enterprise collaboration software.

In 2026, the IT and telecommunications segment is expected to hold the largest share of the global enterprise collaboration tools market, driven by technology companies being the heaviest per-employee users of collaboration tools and the highest per-user spenders on collaboration software of any industry vertical.

The market is primarily driven by the structural and permanent shift to hybrid and remote working that has made cloud-based collaboration tools indispensable core infrastructure for knowledge worker organizations globally, and by the rapid integration of AI capabilities into collaboration platforms that is driving significant per-user revenue increases through premium AI feature tiers and creating compelling productivity ROI that justifies growing collaboration software investment.

Key players are Microsoft Corporation (U.S.), Google LLC (U.S.), Slack Technologies/Salesforce (U.S.), Zoom Video Communications Inc. (U.S.), Cisco Systems Inc. (U.S.), Atlassian Corporation Plc (Australia/U.S.), Asana Inc. (U.S.), Monday.com Ltd. (Israel), Dropbox Inc. (U.S.), Box Inc. (U.S.), SAP SE (Germany), IBM Corporation (U.S.), RingCentral Inc. (U.S.), Zoho Corporation Pvt. Ltd. (India), and Freshworks Inc. (U.S./India), among others.

Asia-Pacific is expected to register the highest growth rate in the global enterprise collaboration tools market during the forecast period 2026-2036, driven by the rapidly growing IT services industry in India, the large and digitalizing enterprise populations of Southeast Asia, and the sophisticated technology-driven business cultures of Japan, South Korea, Singapore, and Australia that are progressively increasing their enterprise software spending.

1. Introduction

1.1 Market Definition

1.2 Market Ecosystem

1.3 Currency and Limitations

1.3.1 Currency

1.3.2 Limitations

1.4 Key Stakeholders

2. Research Methodology

2.1 Research Approach

2.2 Data Collection & Validation Process

2.2.1 Secondary Research

2.2.2 Primary Research & Validation

2.2.2.1 Primary Interviews with Experts

2.2.2.2 Approaches for Country-/Region-Level Analysis

2.3 Market Estimation

2.3.1 Bottom-Up Approach

2.3.2 Top-Down Approach

2.3.3 Growth Forecast

2.4 Data Triangulation

2.5 Assumptions for the Study

3. Executive Summary

4. Market Overview

4.1 Introduction

4.2 Market Dynamics

4.2.1 Drivers

4.2.1.1 Rise of Hybrid and Remote Work Models

4.2.1.2 Increasing Need for Real-Time Communication and Productivity Tools

4.2.1.3 Integration of AI and Automation in Collaboration Platforms

4.2.1.4 Growing Demand for Cloud-Based Enterprise Solutions

4.2.2 Restraints

4.2.2.1 Data Security and Privacy Concerns

4.2.2.2 Integration Challenges with Legacy Systems

4.2.2.3 Tool Fragmentation Across Enterprises

4.2.3 Opportunities

4.2.3.1 AI Copilots and Smart Collaboration Assistants

4.2.3.2 Industry-Specific Collaboration Platforms

4.2.3.3 Expansion in SMEs and Emerging Markets

4.2.3.4 Integration with Workflow and Business Applications

4.2.4 Challenges

4.2.4.1 User Adoption and Change Management

4.2.4.2 Managing Collaboration Overload

4.3 Technology Landscape

4.3.1 Cloud-Based Collaboration Platforms

4.3.2 AI and Generative AI Integration

4.3.3 Unified Communication and UCaaS Platforms

4.3.4 Workflow Automation and Integration APIs

4.3.5 Security and Identity Management Technologies

4.4 Enterprise Collaboration Ecosystem

4.4.1 Communication Platforms

4.4.2 Content and Document Collaboration

4.4.3 Workflow and Project Collaboration

4.4.4 Integration and API Platforms

4.4.5 Security and Governance Solutions

4.5 Value Chain Analysis

4.5.1 Software Vendors

4.5.2 Cloud Infrastructure Providers

4.5.3 System Integrators

4.5.4 Enterprises and End Users

4.5.5 Managed Service Providers

4.6 Regulatory and Compliance Landscape

4.6.1 Data Privacy Regulations (GDPR, CCPA, etc.)

4.6.2 Enterprise Security Standards

4.6.3 Industry-Specific Compliance (HIPAA, FINRA, etc.)

4.7 Porter's Five Forces Analysis

4.8 Investment and Industry Trends

4.8.1 Growth of AI-Driven Collaboration

4.8.2 Mergers, Acquisitions, and Platform Consolidation

4.8.3 Expansion of Remote Work Infrastructure

4.9 Cost and Pricing Analysis

4.9.1 Subscription-Based Pricing Models

4.9.2 Pricing by Feature Tier

4.9.3 Enterprise Licensing Models

5. Enterprise Collaboration Tools Market, by Solution Type

5.1 Introduction

5.2 Communication and Messaging Tools

5.2.1 Instant Messaging Platforms

5.2.2 Team Chat Applications

5.2.3 Email Integration Tools

5.3 Video Conferencing and Virtual Meeting Tools

5.3.1 Video Meetings

5.3.2 Webinars and Virtual Events

5.3.3 Voice and VoIP Solutions

5.4 Content and Document Collaboration Tools

5.4.1 Document Sharing and Editing

5.4.2 File Storage and Management

5.4.3 Knowledge Management Systems

5.5 Project and Workflow Collaboration Tools

5.5.1 Task and Project Management

5.5.2 Agile Collaboration Tools

5.5.3 Workflow Automation Platforms

5.6 Enterprise Social Networks and Engagement Platforms

5.6.1 Internal Social Networks

5.6.2 Employee Engagement Tools

5.7 Integrated Collaboration Suites

5.7.1 Unified Collaboration Platforms

5.7.2 All-in-One Productivity Suites

6. Enterprise Collaboration Tools Market, by Deployment Mode

6.1 Introduction

6.2 Cloud-Based

6.3 On-Premises

6.4 Hybrid Deployment

7. Enterprise Collaboration Tools Market, by Application

7.1 Introduction

7.2 Internal Team Collaboration

7.2.1 Cross-Functional Team Collaboration

7.2.2 Remote Workforce Collaboration

7.3 Customer and Partner Collaboration

7.3.1 Client Communication

7.3.2 Vendor and Supply Chain Collaboration

7.4 Project and Program Management

7.4.1 IT and Software Development

7.4.2 Construction and Engineering Projects

7.5 Knowledge Sharing and Training

7.5.1 Corporate Learning Platforms

7.5.2 Knowledge Base and Documentation

7.6 Innovation and Ideation Platforms

7.7 Other Applications

8. Enterprise Collaboration Tools Market, by Enterprise Size

8.1 Introduction

8.2 Large Enterprises

8.3 Small & Medium Enterprises (SMEs)

9. Enterprise Collaboration Tools Market, by Industry Vertical

9.1 Introduction

9.2 IT & Telecommunications

9.3 BFSI

9.4 Healthcare

9.5 Manufacturing

9.6 Retail & E-commerce

9.7 Education

9.8 Government

9.9 Others

10. Enterprise Collaboration Tools Market, by Feature Type

10.1 Introduction

10.2 Real-Time Collaboration Features

10.3 AI and Automation Features

10.4 Security and Compliance Features

10.5 Integration and API Capabilities

11. Enterprise Collaboration Tools Market, by Geography

11.1 Introduction

11.2 North America

11.2.1 U.S.

11.2.2 Canada

11.3 Europe

11.3.1 U.K.

11.3.2 Germany

11.3.3 France

11.3.4 Netherlands

11.3.5 Sweden

11.3.6 Italy

11.3.7 Spain

11.3.8 Rest of Europe

11.4 Asia-Pacific

11.4.1 China

11.4.2 India

11.4.3 Japan

11.4.4 South Korea

11.4.5 Australia

11.4.6 Singapore

11.4.7 Indonesia

11.4.8 Vietnam

11.4.9 Rest of Asia-Pacific

11.5 Latin America

11.5.1 Brazil

11.5.2 Mexico

11.5.3 Argentina

11.5.4 Chile

11.5.5 Colombia

11.5.6 Rest of Latin America

11.6 Middle East & Africa

11.6.1 UAE

11.6.2 Saudi Arabia

11.6.3 South Africa

11.6.4 Israel

11.6.5 Turkey

11.6.6 Rest of Middle East & Africa

12. Competitive Landscape

12.1 Overview

12.2 Key Growth Strategies

12.3 Competitive Benchmarking

12.4 Competitive Dashboard

12.4.1 Industry Leaders

12.4.2 Market Differentiators

12.4.3 Vanguards

12.4.4 Emerging Companies

12.5 Market Ranking/Positioning Analysis of Key Players, 2025

13. Company Profiles

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

13.1 Microsoft Corporation

13.2 Google LLC

13.3 Slack Technologies (Salesforce)

13.4 Zoom Video Communications, Inc.

13.5 Cisco Systems, Inc.

13.6 Atlassian Corporation Plc

13.7 Asana, Inc.

13.8 Monday.com Ltd.

13.9 Dropbox, Inc.

13.10 Box, Inc.

13.11 SAP SE

13.12 IBM Corporation

13.13 RingCentral, Inc.

13.14 Zoho Corporation Pvt. Ltd.

13.15 Freshworks Inc.

14. Appendix

14.1 Additional Customization

14.2 Related Reports

Published Date: Aug-2025

Published Date: Aug-2025

Published Date: Apr-2024

Subscribe to get the latest industry updates