Resources

About Us

AI Copilot Solutions Market by Copilot Type (General Productivity Copilots, Developer Copilots), Deployment Mode (Cloud-Based, On-Premise, Hybrid), End-Use Industry (IT & Telecom, BFSI, Healthcare & Life Sciences, Retail & E-commerce), and Geography - Global Forecast to 2036

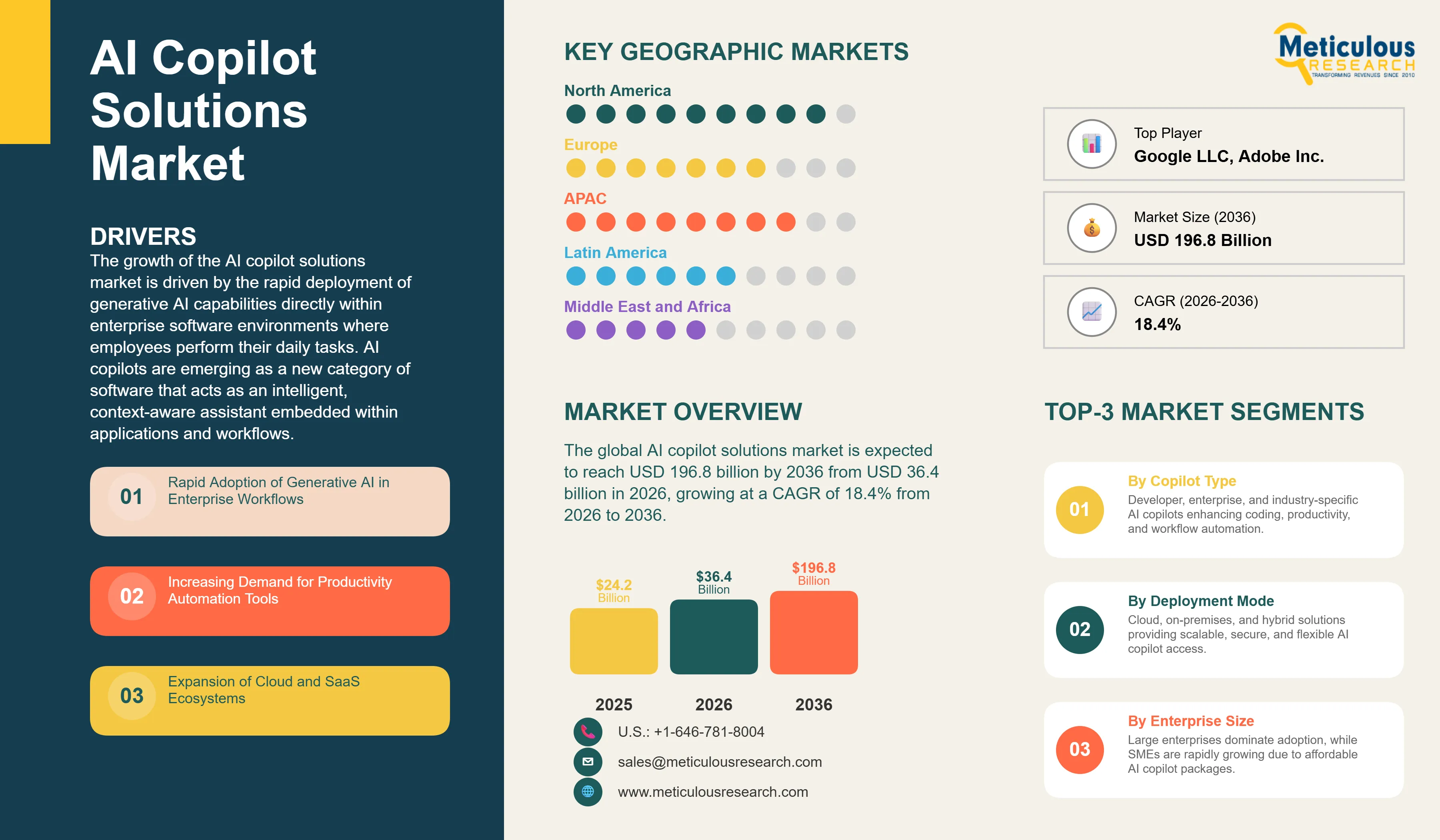

Report ID: MRICT - 1041876 Pages: 322 Apr-2026 Formats*: PDF Category: Information and Communications Technology Delivery: 24 to 72 Hours Download Free Sample ReportThe global AI copilot solutions market was valued at USD 24.2 billion in 2025. This market is expected to reach USD 196.8 billion by 2036 from USD 36.4 billion in 2026, growing at a CAGR of 18.4% from 2026 to 2036.

The growth of the AI copilot solutions market is driven by the rapid deployment of generative AI capabilities directly within enterprise software environments where employees perform their daily tasks. AI copilots are emerging as a new category of software that acts as an intelligent, context-aware assistant embedded within applications and workflows. These solutions provide real-time support for activities such as content creation, coding, data analysis, decision-making, and task automation, helping enhance productivity while still keeping human oversight in place. Unlike standalone AI tools or chatbots that require users to switch platforms, copilots work within the existing applications, making AI assistance seamless and part of the natural workflow.

The market gained strong momentum with the launch of Microsoft Copilot for Microsoft 365 in late 2023, which integrated advanced AI capabilities directly into widely used applications such as Word, Excel, PowerPoint, Outlook, and Teams. Its success demonstrated clear productivity benefits, with early enterprise studies showing significant improvements in both efficiency and work quality. This triggered a wave of similar product launches and investments across the industry. Solutions like GitHub Copilot have shown faster coding productivity, while platforms such as Salesforce Einstein Copilot and ServiceNow AI have improved efficiency in CRM and IT service management workflows. These proven use cases have strengthened the business case for AI copilot adoption across industries.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The AI copilot solutions market represents one of the fastest-growing segments of the generative AI space, where advanced AI technologies are being transformed into practical enterprise productivity tools. These solutions are embedded directly into the software environments used by organizations, helping employees perform tasks such as writing, coding, data analysis, customer communication, decision-making, and process automation. The strong growth of this market is driven by the clear productivity gains delivered by AI copilots, along with increasing pressure on enterprise software vendors to integrate AI capabilities into their platforms to remain competitive.

Modern AI copilot solutions go beyond basic chatbots by combining multiple AI capabilities into integrated platforms. A key feature is context awareness, which allows the system to understand what the user is working on—such as a document, code file, or dataset—and provide relevant assistance without requiring repeated inputs. These solutions also use retrieval-augmented generation, enabling them to access and utilize organizational data such as documents, databases, and internal knowledge systems, resulting in more accurate and context-specific outputs. In addition, advanced copilots are incorporating multi-step reasoning and automation capabilities, allowing them to handle complex tasks, execute actions across different systems, and deliver more complete outcomes rather than just suggestions.

The competitive landscape is shaped by a combination of large technology companies and specialized providers. Major players such as Microsoft, Google, Amazon, and Salesforce have strong advantages due to their control over AI models, cloud infrastructure, and large enterprise customer bases. Microsoft holds a particularly strong position by integrating advanced AI capabilities with its Microsoft 365 suite, Azure cloud platform, and GitHub ecosystem. At the same time, competitors such as Google (Gemini), Salesforce (Einstein Copilot), Amazon (Q), and IBM (watsonx Assistant) are actively expanding their presence by embedding AI copilots into their enterprise offerings. Alongside these large players, a growing number of startups and niche vendors are developing specialized copilots for specific industries and use cases, creating a competitive environment that is driving rapid innovation, improved product capabilities, and more competitive pricing for enterprise customers.

Rise of Embedded Copilots in Enterprise Applications

The most structurally significant trend in the AI copilot solutions market is the progressive embedding of AI copilot capabilities directly within the enterprise software applications ERP systems, CRM platforms, ITSM tools, HR management systems, and productivity suites that define organizational work processes, rather than requiring users to access AI assistance through separate tools or browser-based interfaces. This embedding trend is transforming AI copilot from an add-on productivity tool into a foundational feature expectation for enterprise software, analogous to how search functionality became a universal enterprise software feature expectation in the 2000s. Enterprise software vendors that have not yet incorporated AI copilot capabilities are facing accelerating competitive pressure from vendors that have, creating a race across the enterprise software industry to incorporate AI assistance into every product category.

The commercial consequences of AI copilot embedding within enterprise software are profound for both vendors and enterprise customers. For vendors, copilot capabilities represent a significant upsell and platform stickiness opportunity: Microsoft's Copilot for Microsoft 365 is priced at USD 30 per user per month as an add-on to existing Microsoft 365 subscriptions, representing a 50 to 100 percent increase in per-seat revenue for the world's largest enterprise productivity platform. Salesforce's Einstein Copilot capabilities are driving expansion revenue within existing Salesforce customer accounts as organizations add copilot-enabled features to their CRM deployments. ServiceNow's AI workflow capabilities are accelerating the platform's competitive differentiation in the ITSM market against legacy competitors that have been slower to incorporate AI. For enterprise customers, embedded copilots reduce the adoption friction that standalone AI tools face users encounter AI assistance within applications they already use daily rather than being required to develop new tool habits.

The second defining trend in the AI copilot market is the progressive shift from general-purpose language model-based copilots toward domain-specific AI assistants purpose-built for the specialized knowledge, regulatory compliance requirements, professional terminology, and workflow contexts of specific industries and professional functions. General-purpose copilots based on standard large language model capabilities deliver meaningful value for horizontal productivity tasks document drafting, meeting summarization, email composition but their performance on specialized professional tasks that require deep domain knowledge degrades significantly compared with purpose-built domain copilots trained or fine-tuned on industry-specific data and designed around the specific workflow requirements of specialized professional work.

The healthcare copilot category illustrates the domain specificity opportunity compellingly: clinical documentation copilots including Nuance DAX, which has been deployed at scale by Microsoft across U.S. hospital systems, use ambient listening technology to automatically generate clinical notes from physician-patient conversations in real time, dramatically reducing the documentation burden that contributes to physician burnout while generating structured clinical notes that meet EHR documentation standards. This capability requires not just general language understanding but deep understanding of medical terminology, ICD coding conventions, clinical documentation standards, HIPAA compliance requirements, and the specific documentation workflows of healthcare institutions domain-specific requirements that general-purpose copilots cannot satisfy. Similarly, legal copilots including Harvey AI, developed with OpenAI and deployed at major law firms, apply specialized legal reasoning capabilities trained on legal texts, case law, and regulatory materials to contract review, legal research, and due diligence tasks in ways that general-purpose AI assistants cannot replicate at professional-grade accuracy levels.

|

Parameter |

Details |

|

Market Size by 2036 |

USD 196.8 Billion |

|

Market Size in 2026 |

USD 36.4 Billion |

|

Market Size in 2025 |

USD 24.2 Billion |

|

Market Growth Rate (2026–2036) |

CAGR of 18.4% |

|

Dominating Region |

North America |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Copilot Type, Deployment Mode, Enterprise Size, End-Use Industry, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Rapid Adoption of Generative AI in Enterprise Workflows

The primary driver of the AI copilot solutions market is the extraordinary pace at which generative AI capabilities have been adopted within enterprise software environments following the demonstration of commercially viable large language model performance in real-world knowledge work tasks. The public release of ChatGPT in November 2022 and its achievement of 100 million users within two months represented an inflection point in enterprise AI adoption psychology, demonstrating to executives, IT decision-makers, and knowledge workers simultaneously that AI could produce genuinely useful assistance for complex professional tasks. This demonstration effect catalyzed a wave of enterprise AI investment that had been building since the transformer architecture's introduction but had not yet found the commercially compelling application form that copilot solutions provide.

Enterprise adoption of generative AI is proceeding simultaneously across multiple dimensions. Large language model APIs from OpenAI, Anthropic, Google DeepMind, Meta, and Mistral are being integrated by enterprise software developers into their product offerings at an unprecedented pace, with the number of commercial software products incorporating LLM capabilities growing from hundreds to thousands within two years of GPT-4's commercial availability. Microsoft's investment of USD 13 billion in OpenAI and the subsequent integration of OpenAI models throughout the Microsoft product portfolio represents the most commercially consequential deployment of generative AI in enterprise software history, instantly exposing hundreds of millions of Microsoft enterprise users to AI copilot capabilities. Google's deployment of Gemini models across Google Workspace, Amazon's introduction of AWS Q as an enterprise AI assistant, and Salesforce's Agentforce platform all represent hyperscale enterprise platform responses to the generative AI adoption wave that are collectively transforming the AI copilot landscape from a novelty category into a standard enterprise software capability expectation.

Increasing Demand for Productivity Automation Tools

The structural demand for enterprise productivity improvement tools has intensified significantly in the post-pandemic period as organizations face the dual challenge of sustaining revenue and service quality with workforce sizes constrained by economic pressures while simultaneously confronting the productivity expectations of employees who experienced the efficiency improvements of remote work technology adoption and are now demanding further technology-enabled productivity enhancements. AI copilot solutions address this demand by automating the high-volume, time-consuming, cognitively demanding but relatively structured components of knowledge worker tasks document drafting, data summarization, email drafting, meeting note generation, code completion, and report generation that collectively consume substantial proportions of knowledge workers' productive time without requiring the creative and judgment-intensive cognitive contributions that human expertise uniquely provides.

The economic case for AI copilot investment is increasingly supported by published productivity measurement studies from early enterprise deployments that provide the quantified ROI evidence that enterprise procurement processes require. Microsoft's large-scale productivity studies of Copilot for Microsoft 365 early access users, involving thousands of enterprise users across multiple industry verticals, reported that users saved an average of 1.2 hours per week through AI-assisted task completion a seemingly modest per-user figure that translates to substantial aggregate productivity value across organizations with thousands of licensed users. McKinsey Global Institute research published in 2023 estimated that generative AI automation potential across knowledge work categories could add the equivalent of USD 2.6 trillion to USD 4.4 trillion of value annually across the global economy, with significant concentrations in software engineering, customer operations, sales and marketing, and research and development the precise professional functions that commercial AI copilot products are targeting.

Industry-Specific Copilot Solutions (Healthcare, Legal, Finance)

The development of purpose-built AI copilot solutions for specialized professional domains healthcare, legal services, financial services, manufacturing, and government represents the highest-value commercial frontier of the AI copilot market, where domain-specific AI capabilities that understand specialized terminology, compliance requirements, and professional workflows command premium pricing, create strong customer switching costs, and deliver performance advantages over general-purpose copilots that justify the significant investment in domain-specific model development and deployment. The healthcare copilot opportunity is particularly large and commercially validated: the global healthcare AI market is among the most actively invested sectors of enterprise AI, with clinical documentation copilots, diagnostic decision support tools, and patient engagement AI assistants all demonstrating compelling clinical and operational value in deployed implementations. Nuance DAX, DeepScribe, Suki, and Microsoft's DAX Copilot are building commercial healthcare documentation copilot businesses that address the physician burnout crisis while demonstrating 7 to 10 minutes of clinical time saved per patient encounter a quantified clinical productivity benefit that supports strong ROI cases for health system procurement decisions.

The legal AI copilot market is developing rapidly with specialized AI legal research and contract review platforms including Harvey AI, CoCounsel by Thomson Reuters, Lexis+ AI, and Westlaw AI demonstrating performance on legal research, contract analysis, and due diligence tasks that law firms and corporate legal departments are incorporating into professional workflows. The financial services AI copilot market encompasses trading AI assistants, regulatory compliance documentation tools, credit analysis copilots, and customer advisory AI that financial institutions are deploying under rigorous internal validation and regulatory oversight frameworks. Each of these domain-specific markets represents a large commercial opportunity where specialized capability, deep domain knowledge integration, and compliance infrastructure create defensible competitive positions that pure technology capability alone cannot easily displace.

How Do Developer Copilots Lead the Market?

In 2026, the developer copilots segment is expected to hold the largest share of the AI copilot solutions market by copilot type. Developer copilots addressing code generation, code review, debugging, and DevOps automation represent the first AI copilot category to achieve at-scale commercial adoption, driven by the exceptional and readily quantifiable productivity impact of AI code completion on software engineering workflows, the high technical receptivity of software developer populations to AI tool adoption, and the early commercial success of GitHub Copilot in establishing the category's commercial viability and market expectations. GitHub Copilot's achievement of more than two million paid subscribers within two years of its commercial launch at USD 10 to 19 per developer per month for individual users and USD 19 per seat per month for enterprise demonstrated the commercial scalability of developer copilot subscription models and catalyzed the entry of competing developer AI tools including Amazon CodeWhisperer, Google Cloud Code Assist, Tabnine, Cursor, and Replit Ghostwriter. The global software development workforce of approximately 26 million developers represents the largest single professional population for AI copilot deployment, creating a structural demand base for developer copilot tools that sustains the segment's market size leadership.

However, the industry-specific copilots segment is expected to witness the fastest growth during the forecast period. Purpose-built copilots for healthcare, legal, financial services, and manufacturing are achieving commercial traction at the premium pricing that their domain-specific value propositions command healthcare clinical documentation copilots at USD 200 to 400 per physician per month, legal research and contract review copilots at USD 50 to 150 per attorney per month, and financial analysis copilots at USD 100 to 300 per analyst per month creating per-seat economics substantially higher than horizontal productivity copilots. The large addressable professional populations in each of these domain-specific markets, combined with the compelling productivity and quality improvement cases being established in early deployments, supports sustained high-growth trajectories for industry-specific copilot vendors through the forecast period.

How Does Cloud-Based Deployment Lead the Market?

In 2026, the cloud-based deployment segment is expected to hold the largest share of the AI copilot solutions market by deployment mode and is expected to maintain the fastest growth trajectory through the forecast period. Cloud delivery is not merely a preference but a structural necessity for the majority of commercial AI copilot services, as the foundation model inference infrastructure required for real-time AI response generation typically requiring access to hundreds of billions of parameter language models running on specialized GPU accelerator hardware cannot economically be replicated within enterprise on-premise data center environments for most organizations. The hyperscale cloud data centers of AWS, Azure, and Google Cloud provide the only commercially accessible infrastructure for foundation model-based AI copilot deployment at the scale, cost, and geographic distribution required to serve global enterprise customer bases.

However, on-premise and private AI deployment options are gaining commercial momentum for enterprise customer segments with stringent data sovereignty requirements, classified information handling obligations, or air-gapped infrastructure requirements that prohibit cloud-based AI data transmission. Vendors including IBM with its watsonx platform, Microsoft with its Azure Stack and local model deployment options, and a growing ecosystem of private AI deployment specialists are addressing this market with on-premise LLM deployment solutions that enable enterprises to run AI copilot capabilities on their own infrastructure using open-source models including Llama, Mistral, and Falcon or licensed enterprise model deployments. The hybrid deployment architecture combining on-premise deployment for sensitive data processing with cloud-based deployment for general knowledge tasks is emerging as a practical middle path for regulated enterprises seeking to balance AI capability access with data governance compliance requirements.

How Do Large Enterprises Lead the Market?

In 2026, the large enterprises segment is expected to hold the largest share of the AI copilot solutions market by enterprise size. Large enterprises organizations with more than 1,000 employees and typically more than USD 100 million in annual revenue represent the primary AI copilot procurement market in the current period, combining the large per-deployment revenue opportunity of thousands of licensed user seats with the organizational IT sophistication, procurement infrastructure, and budget authority required to evaluate, negotiate, and deploy enterprise AI software at scale. The large enterprise segment's AI copilot adoption is being driven by the same forces that historically drove large enterprise early adoption of enterprise software categories including ERP, CRM, and cloud computing: the competitive pressure to achieve productivity advantages over peers and competitors, the availability of dedicated IT budgets and implementation partner ecosystems, and the organizational complexity that creates the largest aggregate opportunity for AI automation.

However, the SME segment is expected to witness the fastest growth during the forecast period. The progressive reduction in AI copilot pricing through increased competition, the expanding availability of SME-targeted copilot packages from vendors including Zoho, Freshworks, and Microsoft, and the growing cloud and SaaS adoption among SMEs that provides the infrastructure foundation for AI copilot deployment are collectively enabling AI copilot adoption to expand into the vast SME market. The SME AI copilot opportunity is enormous in aggregate: the global SME sector encompasses approximately 330 million small and medium businesses employing over 4 billion people, representing a potential user base vastly larger than the large enterprise market. Even modest AI copilot penetration of this market at accessible price points generates revenue volumes comparable to deeper penetration of the large enterprise market.

How Does IT & Telecom Lead the End-Use Industry Segment?

In 2026, the IT & Telecom segment is expected to hold the largest share of the AI copilot solutions market by end-use industry. The technology industry's combination of AI-receptive workforce culture, developer-heavy employment composition, cloud-native infrastructure, and early access to AI copilot tools through industry relationships positions it as the highest AI copilot adoption and highest per-seat revenue industry vertical in the current market period. Technology companies across software development, cloud services, IT consulting, cybersecurity, and telecommunications are deploying AI copilots across developer workflows, IT service management, customer support, and internal knowledge management at scale, making the IT & Telecom sector both the largest current revenue contributor and the reference use case generator that validates AI copilot deployment models for other industries.

However, the BFSI segment is expected to witness the fastest growth during the forecast period. Financial institutions including commercial banks, investment banks, insurance companies, asset managers, and financial technology companies are deploying AI copilot capabilities across regulatory compliance documentation, customer advisory services, fraud detection assistance, credit underwriting analysis, trading support, and investment research workflows at an accelerating pace. The combination of large knowledge worker populations performing documentation and analysis-intensive tasks, significant regulatory compliance documentation burdens that AI assistance can reduce, and substantial competitive pressure to improve service quality and operational efficiency while managing headcount growth is creating strong institutional demand for AI copilot capabilities across all BFSI subsegments. JP Morgan's reported deployment of an AI co-pilot for equity research analysts, BlackRock's AI investment research assistant, and HSBC's AI compliance documentation tools represent early examples of the large-scale BFSI AI copilot deployments that are driving this segment's rapid growth trajectory.

How is North America Maintaining Market Leadership?

In 2026, North America is expected to hold the largest share of the global AI copilot solutions market. The United States' dominance within North America and globally reflects the country's unmatched concentration of AI research talent, foundation model technology leadership, enterprise software market scale, and venture capital investment in AI technology development. The leading AI copilot platform vendors Microsoft, Google, Amazon, Salesforce, Adobe, IBM, Oracle, ServiceNow, OpenAI, Anthropic, and GitHub are all headquartered in the United States, creating a technology supply chain concentration that translates into early product availability, deep ecosystem development, and market-shaping product decisions that favor the U.S. enterprise market. The U.S. enterprise software market's culture of early technology adoption and large IT budgets U.S. enterprises account for a disproportionate share of global enterprise software spending enables rapid commercial scaling of AI copilot products that find initial enterprise customers in the U.S. market.

However, Asia-Pacific is expected to witness the highest growth rate in the AI copilot solutions market during the forecast period. The region encompasses the world's largest and most rapidly growing enterprise digital transformation markets, the second-largest AI research and development ecosystem globally, and the most commercially significant domestic AI industry outside the United States in China's domestic AI technology sector. China's AI copilot market is developing rapidly with a distinct domestic ecosystem: Baidu's ERNIE Bot and Baidu AI Cloud copilot services, Alibaba's Tongyi Qianwen models embedded within Alibaba Cloud's DingTalk enterprise collaboration platform, Tencent's Hunyuan large model integrated across Tencent's WeChat Work and enterprise cloud services, and ByteDance's AI assistant capabilities embedded within Feishu's enterprise communication platform collectively address a Chinese enterprise market of hundreds of millions of knowledge workers and software developers. China's national AI development strategy, strong domestic AI research programs at institutions including Tsinghua University, Peking University, and dedicated AI research institutes, and the competitive intensity of the domestic technology sector are creating an AI copilot innovation environment that is generating distinctive product approaches adapted to Chinese enterprise workflows, language characteristics, and regulatory requirements.

Some of the key companies operating in the global AI copilot solutions market are Microsoft Corporation, Google LLC, Amazon Web Services Inc., Salesforce Inc., Adobe Inc., IBM Corporation, Oracle Corporation, ServiceNow Inc., SAP SE, OpenAI, Anthropic, GitHub (Microsoft), Zoho Corporation, Freshworks Inc., and Baidu Inc.

The global AI copilot solutions market is expected to grow from USD 36.4 billion in 2026 to USD 196.8 billion by 2036.

The global AI copilot solutions market is projected to grow at a CAGR of 18.4% from 2026 to 2036.

The developer copilots segment is expected to dominate the overall market in 2026, reflecting the early commercial maturity of code generation AI tools led by GitHub Copilot and the large global software developer workforce representing the category's primary user base. The industry-specific copilots segment is expected to witness the fastest CAGR, driven by the premium pricing achievable for domain-specialized copilots in healthcare, legal, financial services, and manufacturing, and the strong productivity and compliance improvement cases being established in early domain-specific deployments.

The cloud-based deployment segment is expected to dominate the overall market in 2026 and maintain the fastest growth rate through the forecast period, reflecting cloud delivery's structural necessity for foundation model-based AI copilot services and the strong alignment between cloud subscription pricing models and enterprise AI copilot commercial models. On-premise and hybrid deployment options are growing in regulated industries with data sovereignty requirements but represent a smaller overall market share.

The large enterprises segment is expected to dominate the overall market in 2026, reflecting large enterprises' early adoption pace and large per-deployment revenue. The SMEs segment is expected to witness the fastest CAGR, driven by the progressive reduction in AI copilot pricing, the expanding availability of SME-targeted copilot packages, and the enormous aggregate market size of the global SME sector that makes even modest AI copilot penetration highly commercially significant.

The IT & Telecom segment is expected to dominate the overall market in 2026, reflecting the technology industry's AI-receptive culture, developer-heavy workforce composition, and early access to AI copilot tools. The BFSI segment is expected to witness the fastest CAGR, driven by financial institutions' accelerating deployment of AI copilots for regulatory compliance documentation, customer advisory, fraud detection, and financial analysis workflows across large knowledge worker populations.

North America is expected to lead the global market in 2026, supported by the United States' unmatched concentration of leading AI copilot platform vendors, large enterprise early adoption culture, and substantial technology investment. Asia-Pacific is expected to witness the fastest CAGR, driven by China's domestic AI copilot ecosystem development, India's massive software developer population, and the accelerating enterprise digital transformation programs across Japan, South Korea, Singapore, and Australia.

The major players are Microsoft Corporation, Google LLC, Amazon Web Services Inc., Salesforce Inc., Adobe Inc., IBM Corporation, Oracle Corporation, ServiceNow Inc., SAP SE, OpenAI, Anthropic, GitHub (Microsoft), Zoho Corporation, Freshworks Inc., and Baidu Inc.

Published Date: Jan-2025

Published Date: Jul-2024

Published Date: Jan-2024

Published Date: Aug-2022

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates