Resources

About Us

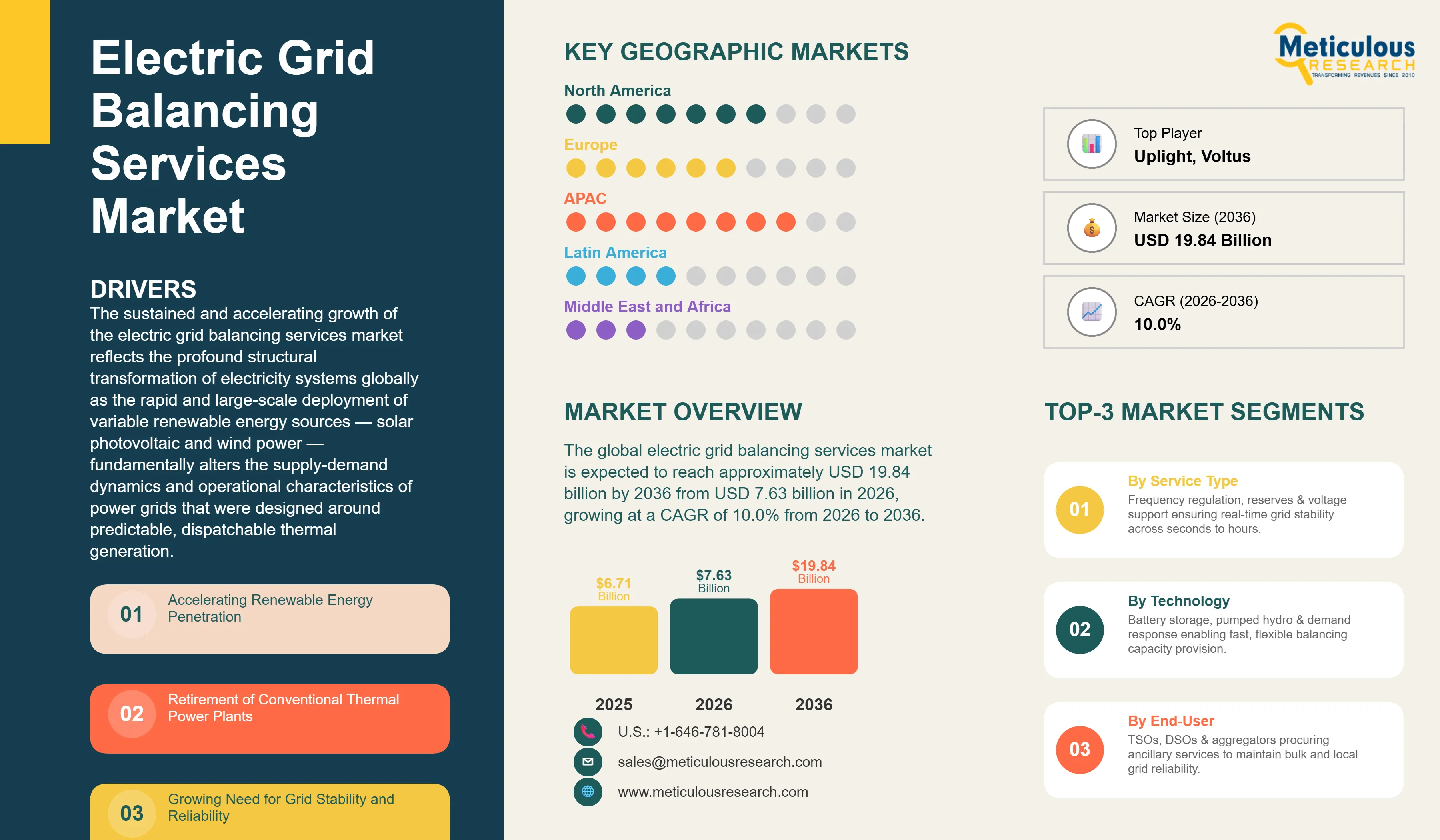

The global electric grid balancing services market was valued at USD 6.71 billion in 2025. The market is expected to reach approximately USD 19.84 billion by 2036 from USD 7.63 billion in 2026, growing at a CAGR of 10.0% from 2026 to 2036. The sustained and accelerating growth of the electric grid balancing services market reflects the profound structural transformation of electricity systems globally as the rapid and large-scale deployment of variable renewable energy sources — solar photovoltaic and wind power — fundamentally alters the supply-demand dynamics and operational characteristics of power grids that were designed around predictable, dispatchable thermal generation. Grid balancing services — encompassing the full spectrum of ancillary services that transmission and distribution system operators procure to maintain instantaneous supply-demand equilibrium, voltage stability, frequency within regulatory bounds, and system resilience following contingency events — are experiencing exponentially growing demand as the inertia-free, weather-dependent output profiles of renewable generation create balancing challenges of unprecedented scale and complexity. The simultaneous retirement of conventional thermal power plants that historically provided implicit balancing capability through their inherent rotating mass inertia and dispatchable output control is creating acute system needs for explicitly procured and remunerated balancing services from dedicated storage, demand response, and fast-response generation resources. Battery energy storage systems have emerged as the dominant new balancing technology, combining sub-second response capability far exceeding conventional generation resources with the flexibility to provide multiple balancing service types simultaneously from a single asset — creating compelling economics that are attracting billions in investment and displacing traditional gas peaker plant balancing strategies across high-renewable-penetration markets.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Electric grid balancing services constitute the essential operational services procured by system operators to maintain power system stability in real time, ensuring that electricity supply and demand remain continuously balanced across time scales ranging from sub-seconds to hours, that voltage levels are maintained within statutory limits at all points in the network, and that the system maintains adequate reserves to respond to unexpected generation losses or demand surges without service interruption. The fundamental physics of alternating current power systems — where all generators must operate in precise synchrony and any instantaneous imbalance between supply and demand manifests as frequency deviation from the 50 or 60 Hz system nominal — creates non-negotiable requirements for balancing services that system operators must procure through market mechanisms or regulatory mandates regardless of cost. The market for these services has existed in structured forms since electricity market liberalization in the 1990s and 2000s, but the renewable energy transition is dramatically reshaping both the quantity and characteristics of balancing services required, the technologies best positioned to provide them, and the market designs that efficiently procure them.

The grid balancing services market is structured around distinct service products operating across different timescales and providing different system functions. Frequency containment reserves — the fastest-acting balancing product responding automatically within seconds to frequency deviations — provide the primary defense against large generation losses, with battery storage systems increasingly dominating this segment given their sub-second response speed far exceeding the 5-30 second response requirements of conventional thermal plants. Frequency restoration reserves, operating over 30 seconds to 15 minutes, restore frequency to nominal following containment, with automatic and manual variants served by both battery storage and demand response. Replacement reserves, active over 15 minutes to hours, relieve faster-acting reserves and restore system margin, typically provided by slower-starting thermal plants, pumped hydro, and large demand response programs. Voltage support and reactive power services maintain voltage profiles across transmission and distribution networks, provided by synchronous condensers, static VAR compensators, and increasingly by grid-forming inverters attached to battery storage systems that can provide synthetic inertia alongside reactive power. The expanding scope of distributed energy resource aggregation — enabling collections of residential batteries, electric vehicles, smart appliances, and commercial building energy management systems to collectively provide balancing services through virtual power plant platforms — is democratizing balancing service provision beyond large utility-scale assets toward millions of small distributed resources.

The market design evolution enabling efficient grid balancing is as commercially significant as the technology advancement. European ancillary service markets — particularly the ENTSO-E harmonized products across Continental Europe and the highly developed UK Balancing Mechanism — have established sophisticated procurement frameworks that co-optimize across multiple balancing products, enable cross-border trading of balancing capacity, and provide multi-year capacity contracts giving storage developers revenue certainty for capital investment decisions. Australia's National Electricity Market has pioneered contingency Frequency Control Ancillary Services market designs enabling battery storage to competitively displace gas peakers in high-value regulation services, with Hornsdale Power Reserve and subsequent large-scale battery projects demonstrating transformational economics. US organized wholesale markets including PJM, MISO, CAISO, and ISO-NE have evolved performance-based frequency regulation market designs that explicitly value the fast response capability of battery storage at premium prices, creating investable revenue streams that have catalyzed gigawatt-scale BESS deployment for grid balancing purposes across North America.

Battery Energy Storage Displacing Gas Peakers as the Primary Balancing Technology

The most structurally transformative trend in the grid balancing services market is the rapid and accelerating displacement of gas peaker plants — historically the marginal balancing resource in most electricity markets — by grid-scale battery energy storage systems offering superior technical performance at increasingly competitive and declining total cost of ownership. Battery storage systems provide frequency regulation response in 100-200 milliseconds compared to 5-30 seconds for gas peakers, enabling BESS to capture the highest-priced fast frequency response products while simultaneously providing slower-acting reserves through degraded response mode — a revenue stacking capability unavailable to single-mode gas peaker assets. The Lazard Levelized Cost of Storage analysis documents BESS total costs declining from USD 400-600/MWh in 2016 to USD 100-200/MWh in 2025 for four-hour duration systems, with continued cost decline trajectories driven by lithium-ion battery manufacturing scale, cell chemistry improvements, and power electronics cost reduction making BESS competitive with or superior to gas peakers across virtually all balancing service applications. Pacific Gas & Electric's cancellation of multiple planned gas peaker projects in California in favor of battery storage contracts, CAISO's Emergency Load Reduction Program replacing emergency demand responses with contracted battery dispatch, and UK National Grid ESO's competitive tender results consistently showing battery storage winning frequency regulation contracts at prices undercutting gas peakers collectively document the commercial tipping point that has been reached across multiple major markets. The environmental regulatory dimension reinforces this technology transition: state and national air quality regulations imposing increasingly stringent emission limits on gas peaker operations — which historically operated at low capacity factors but generated disproportionate emissions per unit of energy when dispatched — create compliance costs and operating restrictions that further disadvantage gas peakers relative to zero-emission battery storage for balancing service provision.

Virtual Power Plants and Distributed Energy Resource Aggregation Transforming Market Access

The emergence of virtual power plant platforms aggregating millions of distributed energy resources — residential and commercial battery systems, electric vehicle chargers, smart water heaters, HVAC systems, and industrial flexible loads — into coherent balancing service portfolios that system operators can dispatch as single controllable entities represents a paradigm shift in how grid balancing services are sourced and delivered. VPP operators including AutoGrid, Enbala (now part of Uplight), CPower, Voltus, OhmConnect, and utility-operated platforms are aggregating portfolios exceeding 1 GW of controllable demand and distributed generation in leading markets, providing frequency regulation, demand response, and peak reduction services that compete directly with traditional utility-scale assets. The technology enabling VPP operations — cloud-based dispatch platforms communicating with millions of distributed endpoints through IoT protocols, real-time state-of-charge and demand prediction algorithms, and machine learning optimization systems maximizing revenue across multiple simultaneous balancing service products — has matured substantially, with dispatch latencies of 100-500 milliseconds enabling participation in fast frequency regulation markets previously accessible only to utility-scale assets. Regulatory evolution across US organized markets and European balancing market reforms is progressively lowering minimum participation thresholds and reducing technical qualification barriers that historically excluded distributed resources from balancing service markets, with FERC Order 2222 in the United States mandating organized market access for distributed energy resource aggregations representing a landmark regulatory milestone enabling nationwide VPP development. Electric vehicle integration with grid balancing represents the next frontier, with vehicle-to-grid capable bidirectional chargers enabling the combined battery capacity of millions of EVs — projected to reach terawatt-hour scale by 2030 in major markets — to contribute substantial balancing service capability while simultaneously meeting vehicle charging needs through intelligent charging management.

|

Parameter |

Details |

|

Market Size by 2036 |

USD 19.84 Billion |

|

Market Size in 2026 |

USD 7.63 Billion |

|

Market Size in 2025 |

USD 6.71 Billion |

|

Market Growth Rate (2026-2036) |

CAGR of 10.0% |

|

Dominating Region |

Europe |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Service Type, Technology, End-User, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Drivers: Accelerating Renewable Energy Penetration and Grid Stability Imperatives

The primary and most powerful driver of grid balancing services market growth is the unprecedented acceleration of renewable energy deployment globally that is transforming the operational characteristics of electricity systems in ways that dramatically increase the quantity and diversity of balancing services required. The International Energy Agency projects global solar and wind capacity additions exceeding 7,300 GW between 2024 and 2030 — representing more than a doubling of current renewable capacity in six years — with penetration reaching 40-60% of electricity generation in leading markets including Germany, Denmark, Spain, and California. This penetration level creates fundamental grid stability challenges that require systematic balancing service procurement at scales far exceeding historical requirements: solar generation creates steep morning ramp-up and evening ramp-down events — the California Independent System Operator's famous duck curve — requiring fast-ramping balancing resources capable of following multi-gigawatt generation swings within hours; wind variability creates minute-to-minute power fluctuations requiring continuous fast frequency regulation; and the displacement of synchronous thermal generators by inverter-based renewable generation reduces system inertia, making frequency excursions following generation loss events faster and deeper, requiring faster-responding frequency containment reserves. Grid operators including National Grid ESO (UK), REE (Spain), ELIA (Belgium), and Amprion (Germany) have published quantified balancing service procurement increases of 50-200% over 5-year planning horizons tied directly to renewable penetration growth targets, providing concrete market volume projections that enable storage developer and demand response aggregator investment planning.

Opportunity: Emerging Markets and Developing Electricity System Balancing Infrastructure

The global energy transition is creating substantial grid balancing market development opportunities in emerging economies that are simultaneously expanding electricity access, deploying large-scale renewable generation, and building the balancing market infrastructure necessary to operate high-renewable systems reliably. India's energy transition presents the most significant emerging market opportunity, with 500 GW renewable capacity targets requiring grid balancing services procurement frameworks that are being developed through India's Central Electricity Regulatory Commission's ancillary services market and the Flexible Innovative and New Electricity System Storage (FINESS) program supporting battery storage deployment for grid balancing. Brazil's highly renewable electricity system — already over 80% renewable from hydro, wind, and solar — is developing market mechanisms for battery storage and demand response to complement pumped hydro in providing balancing services as the system transitions from hydro-dominant to increasingly solar and wind dominated profiles. Southeast Asian electricity markets in Vietnam, Philippines, Indonesia, and Thailand are experiencing rapid renewable deployment that is outpacing balancing infrastructure development, creating urgent needs for ancillary service market design and balancing technology deployment that international storage developers, demand response aggregators, and grid management software providers are actively addressing through partnerships with local utilities and market regulators. The Middle East — transitioning from oil and gas-dominated generation toward renewable energy under Vision 2030 and national energy diversification programs — is developing grid balancing market frameworks from scratch, with Saudi Arabia, UAE, and Egypt designing ancillary service procurement systems informed by European and US market experiences but adapted for high solar penetration and regional interconnection development objectives.

Why Does Frequency Regulation Lead the Market?

Frequency regulation services command approximately 32-36% of total grid balancing services market revenue in 2026, reflecting their position as the most time-critical and highest-value ancillary service product — where instantaneous automated response capability in the sub-second to 30-second timeframe commands substantial price premiums over slower-acting reserves. Frequency regulation encompasses the automatic governor response and automated frequency restoration services that defend system frequency within statutory bands following any generation-load imbalance event, with market prices reflecting both the scarcity value of fast-response capability and the performance incentives that reward response accuracy and speed. Battery energy storage systems have become the dominant technology for frequency regulation in developed markets due to their exceptional performance characteristics — providing precisely calibrated power injection or absorption within 100-300 milliseconds, far exceeding the 5-30 second response times of gas turbines and steam generators — with PJM's performance-based frequency regulation market design explicitly pricing this speed advantage through performance scores that result in battery storage earning 2-4 times the revenue per MW of capacity compared to conventional generation. The spinning reserves service segment represents the second-largest revenue category, encompassing the synchronized generation capacity maintained at partial load ready to increase output within 10 minutes following a contingency event — traditionally provided by thermal generation running below full capacity but increasingly co-located with battery storage that provides the first 30-seconds of response while conventional reserves are ramping. Black start services — the capability to restart a power system following complete blackout without external power supply — represent a high-value niche balancing service where large-scale battery storage is emerging as a technically superior alternative to conventional diesel generators and gas turbines in isolated and renewable-heavy systems.

How Does Battery Energy Storage Dominate the Balancing Technology Market?

Battery energy storage systems represent approximately 40-45% of grid balancing services technology market revenue in 2026 and demonstrate the highest growth rate at approximately 13-15% CAGR — reflecting the combination of superior technical performance across multiple balancing service types, rapidly declining capital costs, and revenue stacking business models that aggregate multiple simultaneous balancing service revenue streams from single assets to deliver compelling investor returns. Lithium-ion chemistry — predominantly lithium iron phosphate (LFP) for stationary grid applications given its superior cycle life, thermal stability, and acceptable energy density — dominates BESS deployments for grid balancing, with utility-scale systems ranging from 10 MW/20 MWh to 1,000 MW/4,000 MWh operating at increasingly competitive levelized costs. The revenue stacking business model that defines BESS grid balancing economics combines frequency regulation revenue (typically the highest per-MW revenue stream), spinning reserve capacity payments, energy arbitrage revenue from wholesale price spread exploitation, and capacity market revenue where available — with sophisticated asset optimization software from companies including Fluence, Modo Energy, and REstore continuously optimizing dispatch across all revenue streams while managing battery state of charge and health constraints. Pumped hydro storage remains the largest installed capacity of grid balancing technology globally — representing approximately 90% of utility energy storage worldwide — but faces limited growth due to geographic constraints and multi-decade development timelines, maintaining its position as the dominant long-duration balancing technology while battery storage captures the growth in faster-responding short-duration services. Demand-side management platforms enabling industrial and commercial load flexibility represent a significant and growing technology segment, with software platforms aggregating controllable industrial processes, commercial building systems, and increasingly residential smart appliances into demand response portfolios providing balancing services at marginal cost for loads that would curtail or shift operations for grid payments.

Why Do Transmission System Operators Command Market Leadership?

Transmission system operators account for approximately 48-52% of grid balancing services market revenue in 2026, reflecting their role as the primary procurers of the highest-value system-critical balancing services — frequency regulation, spinning and non-spinning reserves, black start, and voltage support — that maintain bulk power system stability and security of supply across national and regional transmission grids. TSOs including National Grid ESO (UK), RTE (France), ELIA (Belgium), TenneT (Netherlands/Germany), REE (Spain), and CAISO (California) operate transparent competitive procurement processes for balancing services through tendering, capacity auctions, and real-time balancing markets that have become increasingly important revenue streams for battery storage and demand response asset owners. The distribution system operator end-user segment is growing rapidly at approximately 13-15% CAGR as increasing distributed energy resource penetration at distribution voltage levels creates local congestion, voltage violation, and power quality balancing challenges that distribution networks have not historically been designed to manage, requiring DSO-procured flexibility services from local distributed assets. Independent power producers utilizing battery storage assets for revenue stacking across multiple balancing service markets represent a growing commercial segment as specialized storage developers including Gresham House Energy Storage Fund, Harmony Energy, Zenobe Energy, and international players including Fluence's asset management division develop and operate merchant battery storage portfolios optimized for multi-service balancing revenue. Energy aggregators and VPP operators are the fastest-growing end-user category at approximately 16-18% CAGR, reflecting the platform business model advantages of aggregating diverse distributed resources into scalable balancing service portfolios with marginal cost advantages over utility-scale alternatives.

How is Europe Maintaining Market Leadership?

Europe holds approximately 38-42% of the global electric grid balancing services market in 2026, driven by the continent's leading renewable energy penetration creating the most acute grid balancing challenges globally combined with the most mature and commercially sophisticated ancillary service market structures that efficiently procure and remunerate balancing service provision. The UK's balancing mechanism represents one of the world's most developed balancing service markets, with National Grid ESO procuring multiple product types through competitive tenders that have catalyzed over 3 GW of battery storage deployment specifically for frequency regulation and fast reserve services. Germany's grid balancing market — managed by four transmission operators Amprion, TenneT, 50Hertz, and TransnetBW — has undergone substantial reform to accommodate growing renewable penetration, with the aFRR (automatic Frequency Restoration Reserve) and mFRR (manual FRR) products providing multi-hundred-million euro annual procurement volumes attracting significant battery storage and demand response investment. The ENTSO-E Framework Guidelines on Electricity Balancing and the subsequent Network Code on Electricity Balancing are driving harmonization of European balancing market designs — enabling cross-border balancing capacity trading through the PICASSO and MARI platforms — creating a progressively integrated European balancing market that improves procurement efficiency and provides larger revenue certainty for balancing service investors across member states. Nordic countries, led by Denmark and Sweden with wind penetration exceeding 50% of annual generation, demonstrate the most sophisticated balancing market operations globally, with Energinet and Svenska Kraftnat procuring diverse balancing products across timescales with advanced merit-order optimization that is increasingly serving as a global reference design for balancing market development.

Which Factors Drive Asia-Pacific's Rapid Growth?

Asia-Pacific demonstrates the highest regional growth rate at approximately 12-14% CAGR, propelled by China's extraordinary renewable energy deployment scale creating the world's most rapidly growing grid balancing requirement, Australia's pioneering battery storage balancing market demonstrating transformational economics that is inspiring regional replication, and India's emerging balancing market development responding to the renewable energy transition. China's State Grid Corporation and China Southern Grid are operating the world's largest grid balancing challenge — managing over 700 GW of installed renewable capacity across vast geographic transmission distances — with the National Development and Reform Commission developing comprehensive energy storage market frameworks that will create tens of gigawatts of grid balancing storage deployment through mandatory storage co-location requirements with renewable projects and explicit ancillary service market compensation mechanisms. Australia's National Electricity Market has become a global laboratory for battery storage grid balancing economics, with projects including the Hornsdale Power Reserve, Victoria Big Battery, and multiple subsequent large-scale BESS deployments demonstrating that battery storage can reduce frequency regulation costs, capture substantial ancillary service revenues, and improve system reliability outcomes simultaneously — attracting over AUD 10 billion in announced battery storage investment for grid balancing purposes. Japan's electricity system balancing market is evolving in response to the post-Fukushima energy policy transformation that has rapidly increased renewable penetration while retiring nuclear baseload, with the Japan Electric Power Exchange developing capacity market and balancing service procurement frameworks that are catalyzing battery storage deployment by independent power producers and vertically integrated utilities.

The global electric grid balancing services market encompasses diverse participant categories spanning technology providers, asset operators, and service platforms. On the technology supply side, Fluence Energy (Siemens and AES joint venture), Tesla Energy (Megapack), BYD Energy Storage, CATL (Electrochemical Energy Storage), and LG Energy Solution lead utility-scale battery storage system supply for grid balancing applications. Grid management software and optimization platform providers including AutoGrid Systems, Uplight (formerly Enbala), Voltus, CPower Energy Management, OhmConnect, and REstore (Honeywell) operate VPP and demand response aggregation platforms that provide balancing services from distributed resources. Independent power producers and storage asset developers including Gresham House Energy Storage Fund, Zenobe Energy, Harmony Energy Income Fund, and Gore Street Energy Storage Fund operate merchant battery storage portfolios specifically optimized for balancing service revenue in UK and European markets. Grid-scale energy storage developers and operators including AES Corporation (Fluence assets), NextEra Energy Resources, Pattern Energy, and Orsted are developing large battery storage portfolios for balancing service revenue across US and international markets. Traditional ancillary service providers including gas peaker operators Duke Energy, Calpine, NRG Energy, and Vistra Energy are transitioning portions of their peaker portfolios toward battery storage while maintaining conventional thermal balancing capacity during the transition period. Market design and advisory specialists including Wood Mackenzie, Aurora Energy Research, Modo Energy, and LCP Delta support balancing market development, asset optimization, and revenue forecasting for developers, investors, and system operators.

The global electric grid balancing services market is expected to grow from USD 7.63 billion in 2026 to USD 19.84 billion by 2036.

The global electric grid balancing services market is projected to grow at a CAGR of 10.0% from 2026 to 2036.

Frequency regulation dominates the market representing 32-36% of revenue through its position as the highest-value time-critical balancing product commanding premium pricing for sub-second automated response capability. Demand response services demonstrate the fastest growth at approximately 14-16% CAGR driven by virtual power plant platform aggregation of distributed energy resources and EV vehicle-to-grid capability providing scalable low-cost balancing services at unprecedented scale.

Battery energy storage systems provide frequency regulation response in 100-200 milliseconds compared to 5-30 seconds for gas peakers, capturing premium performance-based pricing while revenue stacking across multiple simultaneous balancing service products. BESS total costs have declined from USD 400-600/MWh in 2016 to USD 100-200/MWh in 2025, reaching competitive parity with gas peakers across most balancing applications while offering zero-emission operations increasingly favored by environmental regulation.

Europe leads with approximately 38-42% of global market driven by the highest renewable energy penetration creating acute balancing requirements, the most developed ancillary service market structures, and the ENTSO-E harmonized balancing market creating integrated cross-border procurement. Asia-Pacific demonstrates the fastest growth at 12-14% CAGR driven by China's massive renewable balancing challenge and Australia's pioneering battery storage balancing market economics.

The leading companies include Fluence Energy, Tesla Energy, BYD Energy Storage, AutoGrid Systems, Uplight, Voltus, CPower, Gresham House Energy Storage Fund, Zenobe Energy, AES Corporation, NextEra Energy Resources, and traditional balancing providers including Duke Energy, Calpine, and Vistra Energy transitioning toward battery storage balancing portfolios.

1.Introduction

1.1.Market Definition

1.2.Market Scope

1.3.Research Methodology

1.4.Assumptions & Limitations

2.Executive Summary

3.Market Overview

3.1.Introduction

3.2.Market Dynamics

3.2.1.Drivers

3.2.2.Restraints

3.2.3.Opportunities

3.2.4.Challenges

3.3.Ancillary Service Market Design Evolution & Regulatory Frameworks

3.4.Virtual Power Plants & Distributed Energy Resource Aggregation Landscape

3.5.Porter's Five Forces Analysis

4.Global Electric Grid Balancing Services Market, by Service Type

4.1.Introduction

4.2.Frequency Regulation

4.2.1.Frequency Containment Reserves (FCR / Primary Frequency Response)

4.2.2.Frequency Restoration Reserves - Automatic (aFRR)

4.2.3.Frequency Restoration Reserves - Manual (mFRR)

4.2.4.Replacement Reserves (RR)

4.3.Voltage Support & Reactive Power

4.3.1.Static VAR Compensation & STATCOM Services

4.3.2.Synchronous Condenser & Synthetic Inertia Services

4.4.Spinning & Non-Spinning Reserves

4.4.1.Operating Spinning Reserves (10-minute response)

4.4.2.Non-Spinning & Supplemental Reserves (30-minute)

4.5.Black Start Services

4.6.Demand Response

4.6.1.Emergency Demand Response

4.6.2.Economic & Price-Responsive Demand Response

4.6.3.Ancillary Service Demand Response (Fast DR)

4.7.Congestion Management & Redispatch

5.Global Electric Grid Balancing Services Market, by Technology

5.1.Introduction

5.2.Battery Energy Storage Systems (BESS)

5.2.1.Lithium Iron Phosphate (LFP) Battery Systems

5.2.2.NMC & Other Li-ion Chemistries

5.2.3.Long-Duration Battery Storage (Flow Batteries, Sodium-Ion)

5.3.Pumped Hydro Storage

5.3.1.Conventional Pumped Hydro Facilities

5.3.2.Advanced Variable-Speed Pumped Hydro

5.4.Gas Peaker Plants

5.4.1.Open Cycle Gas Turbines (OCGT)

5.4.2.Gas-Fired Fast-Start Reciprocating Engines

5.5.Demand-Side Management (DSM) Platforms

5.5.1.Industrial Load Control & Interruptible Supply

5.5.2.Commercial Building Energy Management Systems

5.5.3.Residential Smart Appliance & EV Charging Management

5.6.Virtual Power Plants (VPP)

5.6.1.Utility-Operated VPP Platforms

5.6.2.Independent VPP Aggregator Platforms

5.7.Flywheel Energy Storage

6.Global Electric Grid Balancing Services Market, by End-User

6.1.Introduction

6.2.Transmission System Operators (TSOs)

6.2.1.National TSOs in Liberalized Markets

6.2.2.Independent System Operators (ISOs/RTOs)

6.3.Distribution System Operators (DSOs)

6.3.1.DSO Local Flexibility Procurement

6.3.2.Active Distribution Network Management

6.4.Independent Power Producers & Storage Asset Owners

6.5.Large Industrial Consumers

6.5.1.Energy-Intensive Industries (Steel, Chemicals, Cement)

6.5.2.Data Centers & Hyperscale Operators

6.6.Aggregators & Virtual Power Plant Operators

7.Global Electric Grid Balancing Services Market, by Region

7.1.Introduction

7.2.North America

7.2.1.U.S. (PJM, CAISO, MISO, ISO-NE, NYISO, ERCOT)

7.2.2.Canada

7.3.Europe

7.3.1.United Kingdom (National Grid ESO)

7.3.2.Germany (Amprion, TenneT, 50Hertz, TransnetBW)

7.3.3.France (RTE)

7.3.4.Belgium (ELIA)

7.3.5.Netherlands (TenneT Netherlands)

7.3.6.Nordic Countries (Energinet, Svenska Kraftnat)

7.3.7.Rest of Europe

7.4.Asia-Pacific

7.4.1.China (State Grid, China Southern Grid)

7.4.2.Australia (NEM)

7.4.3.Japan (JEPX)

7.4.4.India (IEGC, CERC ancillary markets)

7.4.5.South Korea

7.4.6.Rest of Asia-Pacific

7.5.Latin America

7.5.1.Brazil

7.5.2.Chile & Colombia

7.5.3.Rest of Latin America

7.6.Middle East & Africa

7.6.1.Saudi Arabia & UAE

7.6.2.South Africa

7.6.3.Rest of Middle East & Africa

8.Competitive Landscape

8.1.Overview

8.2.Key Growth Strategies

8.3.Competitive Benchmarking

8.4.Competitive Dashboard

8.4.1.Industry Leaders

8.4.2.Market Differentiators

8.4.3.Vanguards

8.4.4.Emerging Companies

8.5.Market Ranking/Positioning Analysis of Key Players, 2025

9.Company Profiles

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

9.1.Fluence Energy, Inc. (Siemens & AES JV)

9.2.Tesla Energy (Tesla, Inc.) -- Megapack

9.3.BYD Company Limited -- Energy Storage Division

9.4.CATL (Contemporary Amperex Technology Co., Ltd.)

9.5.AutoGrid Systems, Inc.

9.6.Uplight, Inc. (formerly Enbala Power Networks)

9.7.Voltus, Inc.

9.8.CPower Energy Management

9.9.Zenobe Energy Ltd.

9.10.Gresham House Energy Storage Fund plc

9.11.AES Corporation (Fluence Assets & Clean Energy)

9.12.NextEra Energy Resources, LLC

9.13.Vistra Energy Corp.

9.14.REstore NV (Honeywell)

9.15.OhmConnect, Inc.

10.Appendix

10.1.Questionnaire

10.2.Related Reports

Published Date: Jun-2025

Published Date: Jul-2025

Subscribe to get the latest industry updates